January 2017

Asian fixed income guide

For professional clients only

2

Contents

Introduction 3

Developments in Asian fixed income 4

Asian fixed income at a glance 5

Asian USD credit 6

Asian local currency 7

Markets in focus 8

HSBC Global Asset Management in Asian fixed income 12

Important information 13

HSBC Global Asset Management’s Asian Fixed Income Capability

– USD72 billion in Asian fixed income assets, managed by award-winning investment teams based in Asia

– Awarded Best of the Best Award by Asia Asset Management in 2008-2010, 2012, 2013 and 2015

– Long track record in Asian fixed income dating back to 1996

– Embedded into the strong compliance and governance framework of HSBC Group

3

Introduction

Asia continues to be the world’s fastest growing region despite signs of moderation. It is forecast to

grow at around 6% in 2016, while growth in the rest of the world will barely touch 2%

The sovereign ratings of Asian countries have been stable and in some cases upgraded on the back of

improving economic fundamentals

Any adverse impact from slowing growth is likely to be alleviated by more accommodative monetary

policies in the region

While accounting for over half of the world’s population, Asia is considerably underrepresented in both

developed and emerging bond indices, and accounts for less than 4% and 21% of Barclays Global

Aggregate Index and JP Morgan Emerging Market Bond Index respectively

Investor interest for Asian bonds has increased significantly, given their diversification benefits and

relatively low correlation with other asset classes. While new issuance in Asia is expected to increase

slightly, the demand continues to grow strong due to uncertainties surrounding the outlook of different

markets. This should continue to provide support to the performance of Asian bonds

-3

-2

-1

0

1

2

3

4

5

6

7

Asia ex-Japan North America Latin America EuropeanUnion

2014 2015e 2016e 2017e

Notes:

1. Source: IMF, Bloomberg, as of October 2016

2. Source: Bloomberg, as of November 2016

Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC accepts no liability

for failure to meet such forecasts, projections or targets. For illustrative purposes only

Asia is underrepresented in Global Bond Indices1

Asian economic growth higher than other

major regions1

Higher yield in Asia compared to US and

Europe2

Rest of the World Asia

Asia accounts for

about 60% of the

world’s population

Asia accounts for

about 36% of the

world’s GDP

Asia accounts for less

than 4% of Barclays

Global Aggregate1

0

1

2

3

4

5

6

Nov-12 Nov-13 Nov-14 Nov-15 Nov-16

Euro IG Corp US IG Corp Asian IG Corp

(%)(%)

4

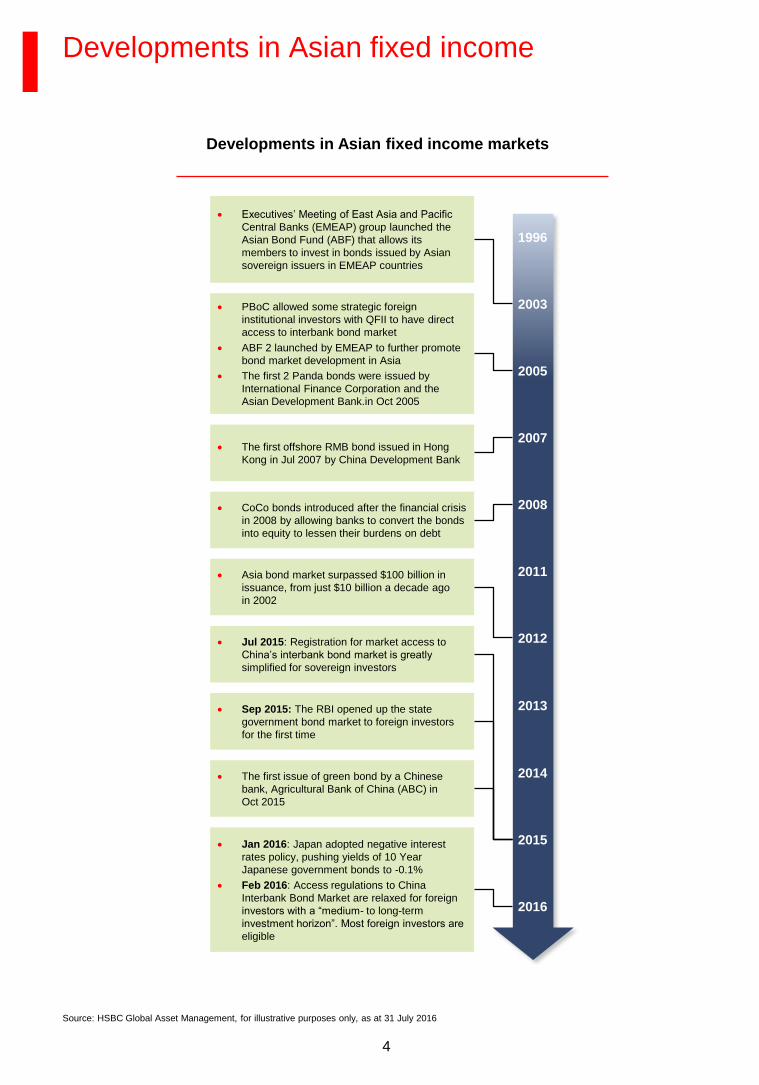

Developments in Asian fixed income

Source: HSBC Global Asset Management, for illustrative purposes only, as at 31 July 2016

Developments in Asian fixed income markets

Executives’ Meeting of East Asia and Pacific

Central Banks (EMEAP) group launched the

Asian Bond Fund (ABF) that allows its

members to invest in bonds issued by Asian

sovereign issuers in EMEAP countries

PBoC allowed some strategic foreign

institutional investors with QFII to have direct

access to interbank bond market

ABF 2 launched by EMEAP to further promote

bond market development in Asia

The first 2 Panda bonds were issued by

International Finance Corporation and the

Asian Development Bank.in Oct 2005

CoCo bonds introduced after the financial crisis

in 2008 by allowing banks to convert the bonds

into equity to lessen their burdens on debt

The first offshore RMB bond issued in Hong

Kong in Jul 2007 by China Development Bank

Asia bond market surpassed $100 billion in

issuance, from just $10 billion a decade ago

in 2002

Jul 2015: Registration for market access to

China’s interbank bond market is greatly

simplified for sovereign investors

Sep 2015: The RBI opened up the state

government bond market to foreign investors

for the first time

Jan 2016: Japan adopted negative interest

rates policy, pushing yields of 10 Year

Japanese government bonds to -0.1%

Feb 2016: Access regulations to China

Interbank Bond Market are relaxed for foreign

investors with a “medium- to long-term

investment horizon”. Most foreign investors are

eligible

The first issue of green bond by a Chinese

bank, Agricultural Bank of China (ABC) in

Oct 2015

2003

2005

2007

2015

2008

2011

2012

2016

2014

1996

2013

5

Asian fixed income at a glance

Asian Fixed Income market can be split broadly into two categories:

– 1) Asian USD credit market

– 2) Local currency bond market

Asian USD credit market is approximately USD680 billion in market size and is made up of a diverse

geography of countries, and categorized by investment grade and high yield bonds. It is freely

available to global investors, with no tax implications other than those normally incurred in the

investments. The following chart shows the breakdown of the JPMorgan Asia Credit Index (JACI),

which is one of the most comprehensive and inclusive indices available

The Asian Local currency bond market is approximately USD10 trillion in market size and

approximately half of this is made up of China alone, a market which has been difficult for foreigners

to access

(USDbn) (%)

Asian local currency bond markets2

Asian USD credit markets1

(USDbn) (%)

Notes:

1. Source: JPMorgan Asia Credit Index, as of 31 October 2016

2. Source: AsiaBondsOnline; market sizes as of 30 September 2016 (India market size as of June 2016, taken from CCIL, RBI, SEBI); Yield numbers as of

10 November 2016

Data shown is for illustrative purposes only and does not constitute any investment recommendation to buy or sell in the above-mentioned countries and

asset classes

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

0

50

100

150

200

250

300

350

China Korea Indonesia Hong Kong India Philippines Singapore Malaysia Thailand

Size of Asian USD credit market (LHS) Yield (RHS)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

China Korea India Thailand Malaysia Singapore Indonesia Hong Kong Philippines

Size of Asian local currency bond market (LHS) 10-year Government Yields (RHS)

6

Asian USD credit

Reasons for considering Asian credit

Healthy macro conditions. Solid external balances should help keep Asian currencies more stable and

improve Asian institutions’ ability to pay debts denominated in foreign currencies

Solid credit profile on the corporate level. Default rate for Asian hard currency bonds is expected to

moderate to 1.8% in 2016, and Asia is the only region that received a cut in the latest default forecast

Good diversification for global credit portfolios. Asian fixed income has registered low volatility, and

low correlation with other asset classes, including US Treasuries

Competitive yields relative to developed markets. Despite stronger credit fundamentals in the region,

Asian credits are still trading at a yield premium over comparable US and Euro credits. This should

offer better value for Asian bond investors

Strong market demand with limited increase in supply. Estimated net financing to remain relatively low

with gross supply expected to pick up slightly in 2016, however, the strong demand for Asian bonds

should outweigh the increase in supply

Notes:

1. Source: JP Morgan as of 31 August 2016

2. Source: JP Morgan as of 23 November 2016

Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC accepts no liability

for any failure to meet such forecasts, projections or targets. For illustrative purpose only

Asian default rate expected to stay below most other regions in 20172

2012 2013 2014 2015 2016 YTD 2017f

Asia 2.7% 1.2% 1.5% 3.1% 1.0% 2.0%

EM Europe 5.2% 2.3% 4.0% 2.5% 3.0% 1.1%

Latin America 3.6% 10.6% 6.5% 5.7% 9.2% 2.6%

MENA 0.2% 0.0% 4.6% 4.0% 4.6% 3.4%

EM (total) 3.5% 4.3% 3.8% 3.8% 4.9% 2.1%

US 1.2% 0.7% 3.0% 2.6% 3.6% 2.5%

(USDbn)

13

5268

57

116 119

180

148163

-6 -9 -12 -16 -19 -24 -31 -34 -37-13 -20 -17 -26 -24 -16-39 -44 -54

-6

2439

16

74 79

110

71 73

-80

-30

20

70

120

170

220

2008 2009 2010 2011 2012 2013 2014 2015 2016e

Gross supply Coupon Maturity Net financing

Estimated net financing remains low1

7

Asian local currency

Reasons for considering Asian currency bonds

Strong Current account positions. Current account positions are strong for most Asian countries as

backed up by healthy FX reserves, which suggest potential for appreciation

Debt ratios are much lower. Government gross debt as a percentage of GDP for G7 countries are

expected to stay at above 100%, versus the 50% for the emerging market and developing economies

Underrepresentation in Emerging market indices. Despite accounting for 65% of EM’s GDP, Asia’s

weight in emerging markets indices is substantially below that figure

Increased likelihood of further rating upgrades. Some parts of the region are widely regarded as

“developed” with investment grade rating. As macro economic fundamentals improve in the region,

further rating upgrades are likely

Source: 1. Bloomberg, 30 September 2016

Countries S&P’s credit rating

Singapore AAA

Hong Kong SAR AAA

China AA-

Korea AA-

Malaysia A-

Thailand BBB+

Philippines BBB

India BBB-

International reserve assets1

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Chin

a

Jap

an

Sw

itzerlan

d

Sa

udi A

rabia

Ta

iwan

Hong K

on

g

So

uth

Kore

a

Bra

zil

India

Russia

Eu

rozone

Sin

ga

pore

Me

xic

o

Th

aila

nd

Alg

eria

United K

ingdom

Indonesia

Tu

rkey

Mala

ysia

Isra

el

Po

lan

d

U.A

.E.

Cze

ch R

epublic

Ph

ilippin

es

Lib

ya

Canada

Norw

ay

Pe

ru

Denm

ark

Sw

eden

US

So

uth

Afr

ica

Germ

any

Asia ex Japan Others

(USDbn)

Key Asian markets with investment grade sovereign rating1

8

Local rating

International rating

(S&P)

AAA

AA+

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

BB

BB-

B+

B

B-

CCC

Markets in focus – China

Onshore Offshore

Where are the bonds traded? Mainland China Outside mainland China

Market size USD6,150 billion USD107 billion

Accessibility

Accessible on a restricted basis to certain

investor types– Onshore institutional investors

– Offshore institutions with QFII/RQFII licenses

– Foreign investors with a medium- to long-term

investment horizon, eligible for access to CIBM1

Can be accessed by all

offshore investors– Retail and institutional

investors

– No quota restriction

Rating agencies

Local rating agencies, eg Chengxin,

Dagong,

Pengyuan, etc

International rating

agencies, eg Moody’s,

Fitch, S&P

Market Composition

Sovereigns: 21%

Policy banks: 29%

Others2: 50%

Sovereigns: 26%

Non-Sovereigns: 74%

AAA

AA+

AA

AA-

A+ and

below

Sovereign rating

Notes:

1. CIBM refers to China’s Interbank Bond Market. Most real money

investors are eligible, including commercial banks, insurance companies,

securities houses, fund/asset management companies, as well as

pension funds, charity funds and endowment funds, so long as they

have a medium- or long-term investment horizon

2. Others include local government bonds, corporates, enterprise bonds etc

3. Source: ChinaBond, as of 31 August 2016

4. Source: HSBC Global Asset Management, September 2016. The table

is provided for discussion purposes only. There is no official mapping to

convert local rating into international rating

5. The rating criteria and methodology used by Chinese local rating

agencies may differ from those adopted by established international

credit rating agencies. Therefore, the Chinese local credit rating system

may not provide an equivalent standard for comparison with securities

rated by international credit rating agencies

Any forecast, projection or target contained in this presentation is for

information purposes only and is not guaranteed in any way. HSBC Global

Asset Management accepts no liability for any failure to meet such

forecasts, projections or targets

For illustrative purposes only

Mapping local credit ratings to

international equivalents4,5

Onshore and offshore RMB bonds

RMB bonds can be differentiated by onshore and offshore. The two markets currently have materially

different accessibility requirements and characteristics

Onshore RMB bond market used to be largely closed to foreign investors, except those with certain licenses

and quotas. With new regulations announced in February 2016, most foreign investors with a medium or

long-term investment horizon can invest in the market, with a relatively simple application process

With the continued opening up of the onshore bond market, we expect the onshore and offshore bond

markets to eventually evolve into one

Local credit ratings vs international credit ratings5

China’s offshore RMB bonds are rated by international agencies. China onshore bonds are rated by local rating

agencies, which have difference methodologies, scales and standards

Over 98% of the onshore market is rated AA or above by local credit agencies, less than 2% is rated AA- or

below. As a result, there is currently limited ratings and pricing differentiation in the onshore RMB credit market.

The emergence of credit events (from zero defaults historically) will likely drive improved pricing differentiation

going forward. Credit selection and research capabilities is key to investing in this market

AAA (63.0%)

AA+ (18.9%)

AA (17.1%)

AA- (0.7%)

A+ (0.1%)

A & Below (0.1%)

Credit quality breakdown (onshore)3

9

Markets in focus – China (cont’d)

Source: JP Morgan, Barclays, Citi; June 2015

Any forecast, projection or target contained in this document is for illustrative purpose only and is not guaranteed in any way. HSBC accepts no liability for

any failure to meet such forecasts, projections or targets

Reasons for considering RMB bonds

Higher yields compared with international markets of similar size or the same credit rating (AA- or Aa3)

Low historical volatility and correlation compared with other asset classes

Potential inclusion in global bond indices could lead to increased future investor demand

Potential inclusion in global bond indices

There is substantial speculation as to if and when China may be included in global bond indices. The Chinese

bond market is already tracked by the key index providers. JP Morgan, Citigroup and Barclays have been

maintaining their own Chinese bond indices for some years

We had an attempt in forecasting China’s weight in global/emerging market bond indices should full inclusion take

place. We have used a ‘base case’ assumption of China’s full inclusion within 5 years’ time. Our forecast was

based on the current market value of the Chinese bond index and the market value of the indices maintained by

the same index provider. We then worked out China’s current weight in the indices should China be included. We

assumed the allocation to the Chinese bond market and other markets would grow in line with their GDP over the

next 5 years. In this scenario, China could make up a significant part of the emerging market bond indices after 5

years. (52% of Citigroup Emerging Market Government Bond Index, 38% of Barclays Emerging Market Local

Currency Government Index and 33% of JP Morgan GBI-EM Global Index). The impact from China’s inclusion in

the global bond indices would be less significant but the market would still be a meaningful addition to the global

indices. The initial weights of China in emerging market indices are unlikely to be the levels outlined above. Some

indices will limit the weight of China to 10% under their index diversification rules. We expect China’s inclusion to

be gradual, starting from a low level and grow in line with the gradual path of market opening, reflecting the actual

investability over time

Following the recent announcement on enhanced market access, JPMorgan has placed China under review for

potential GBI-EM Global Diversified inclusion (15 March 2016). It is believed that USD180bn AUM is tracking this

index, and so as China’s weight grows to its maximum 10% (maximum incremental increase 1% per month), this

would imply extra demand of USD18bn for onshore RMB bonds (about 0.35% of overall market size)

China’s weight in global indices if

included in global indices

China’s weight in global indices if

included in GEM indices

0.0%

29.3%

32.6%

35.3%38.0%

49.3%52.2%

0%

10%

20%

30%

40%

50%

60%

Current Current if China isincluded

(hypothetical)

Year 2020 if Chinais included(forecast)

JPM GBI-EM Global

Barclays EM Local Ccy Govt

Citi EMGBI

0.0%

1.8%

2.3%

2.2%

2.8%

4.5%

5.7%

0%

1%

2%

3%

4%

5%

6%

Current Current if China isincluded

(hypothetical)

Year 2020 if Chinais included(forecast)

JPM GBI Global

BGA

Citi WGBI

China’s weight in index China’s weight in index

10

Markets in focus – India

Indian bond market

The Indian bond market has grown rapidly in the past few years. It is a large, well diversified and liquid

market that is dominated by government issuance.

The market can be broadly classified in three segments:

– Government Securities comprising the Central and State Government securities and treasury bills

– Public Sector Undertaking (PSU) bonds, generally treated as surrogates of sovereign paper, often due to the comfort of

Government ownership of the PSUs

– Corporate securities comprising debentures/corporate bonds and commercial papers

Reasons for considering India bonds

Attractive yields - Indian government bond yields are attractive relative to emerging market peers, but

especially so against developed markets

Supportive macro environment – A number of effective measures have been put in place by RBI and

the government to help control inflation, and keep liquidity at neutral level. Current account deficit has

narrowed significantly thanks to the increased foreign direct investments

Greater accessibility – Recent reforms on the development of the onshore fixed income and currency

markets have facilitated market access to foreign investors. The reduction on withholding tax on

interest income of the Masala bonds also boosted investor demand. All of these measures have

helped widen the investor base and increase inflows from foreign investments

Onshore Offshore

Where are the bonds traded? India Outside India

Currency INR USD/INR

Market size USD1307 billion1 USD53 billion2

Accessibility

Not freely accessible to foreign

investors, but can be accessed

through FPI (Foreign Portfolio

Investor) license

– There are limitations to active

management once the license is

obtained

– There is tax to pay on coupons and

capital gains

Can be accessed by all offshore

investors

– A number of USD bonds linked to

Indian companies or institutions

– There can be hedged into Rupee

with non-deliverable forwards (NDF)

– Limited supply of offshore INR bonds

/ Masala bonds

Notes:

1. HSBC Global Asset Management, as of June 2016

2. JPMorgan Asia Credit Index, as of 30 September 2016

3. Selected 10 year bond yields. Bloomberg, data as of 3 November 2016

Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC Global Asset

Management accepts no liability for any failure to meet such forecasts, projections or targets. For illustrative purposes only

Relative Attractive Yields3

6.82

0

2

4

6

8

10

So

uth

Afr

ica

Indonesia

India

Me

xic

o

Ph

ilippin

es

Mala

ysia

Hungary

Chin

a

Th

aila

nd

US

Sp

ain UK

Germ

any

Yield (%)

11

Markets in focus – Indonesia

Onshore Offshore

Where are the bonds traded? Indonesia Outside Indonesia

Currency IDR USD/IDR

Market Size USD 165 billion1 USD 65 billion2

Average govt duration 6.343 8.022

Notes:

1. ABD, as of 30 September 2016

2. JP Morgan Asia credit index as of 31 October 2016

3. Markit iBoxx ALBI Indonesia, as of 31 October 2016

4. Bank of Indonesia, as of August 2016.

Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC Global Asset

Management accepts no liability for any failure to meet such forecasts, projections or targets. For illustrative purposes only

Indonesian bond market

The Indonesian bond market has steadily expanded with improving liquidity in the past few years and is

dominated by government issues

There are no restrictions on foreign investments in this market

Even though Indonesia is the region’s fifth largest economy, the size of its government bond market

ranks tenth in the region. There is significant room for more state project financing to take place via the

government bond market

Reasons for considering Indonesian bonds

Positive market technicals – The market offers competitive yields, which attract steady capital inflows

from foreign investors in the long term. Moreover, recent domestic regulatory changes have led to

increasing demand from local pension funds and insurance companies

Attractive yields - Indonesian bond yields are attractive relative to emerging market peers as well as

developed markets. At the time of writing, the yield of the 10 year government bonds is over 7.5%

Constructive macro environment – Indonesia sovereign rating is steadily improving on the back of

relatively low leverage, current account improvement, and benign inflation. Meanwhile, the

improvement in macro fundamental provides better stability for the currency

Improving policy environment – Recent reform progress should benefit Indonesian economy and bond

market in the medium to long term. The government has unveiled numerous ‘stimulus’ packages since

September 2015 aiming to reinvigorate growth dynamics. Current account deficit has narrowed

significantly in recent years due to a large fall in imports than exports

(USDbn)

3.7

1.2

(4.7)

(7.6)

(1.9)

-15

-10

-5

0

5

10

15

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2011 2012 2013 2014 2015 2016

Goods Services Income Secondary Inc. Current Acc.

2011:

CA surplus

USD1.7bn

2012:

CA deficit

USD24.4bn

2013:

CA deficit

USD29.1bn

2014:

CA deficit

USD27.5bn

2015:

CA deficit

USD17.8bn

2016:

CA deficit

USD4.7bn

Import compression narrows CAD4

12

AMG’s Asian fixed income capabilityLong track record in Asian fixed income

Recognised leadership in Asian fixed income

USD72 billion in Asian fixed income assets under

management

Award winning investment team in Asia

Well resourced, experienced and integrated investment team

Long track record in Asian fixed income dating back to 1996

22 managers, 11 analysts

Investment process built on solid proprietary research

Best use of global resources with local insight

Collective thinking on global investment risks and themes

Local decision-making to ensure empowerment and flexibility

~40 credit analysts

~10 macro-economists

USD189.7bn fixed income

asset under management*

~170 investment

professionals

Source: HSBC Global Asset Management, as of 30 September 2016

Firm-wide Statistics

(Fixed Income)

13

Important information

For Professional Clients only and should not be distributed to or relied upon by Retail Clients.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in

whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the

responsibility of the user and may lead to legal proceedings. The material contained in this document is for

general information purposes only and does not constitute advice or a recommendation to buy or sell

investments. Some of the statements contained in this document may be considered forward looking

statements which provide current expectations or forecasts of future events. Such forward looking statements

are not guarantees of future performance or events and involve risks and uncertainties. Actual results may

differ materially from those described in such forward-looking statements as a result of various factors. We do

not undertake any obligation to update the forward-looking statements contained herein, or to update the

reasons why actual results could differ from those projected in the forward-looking statements. This document

has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the

purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views

and opinions expressed herein are subject to change at any time. These views may not necessarily indicate

current portfolios' composition. Individual portfolios managed by HSBC Global Asset Management primarily

reflect individual clients' objectives, risk preferences, time horizon, and market liquidity.

The value of investments and the income from them can go down as well as up and investors may not get

back the amount originally invested. Past performance contained in this document is not a reliable indicator of

future performance whilst any forecasts, projections and simulations contained herein should not be relied

upon as an indication of future results. Where overseas investments are held the rate of currency exchange

may cause the value of such investments to go down as well as up.

We accept no responsibility for the accuracy and/or completeness of any third party information obtained from

sources we believe to be reliable but which have not been independently verified.

HSBC Global Asset Management (UK) Limited provides information to Institutions, Professional Advisers and

their clients on the investment products and services of the HSBC Group.

This presentation has been produced by HSBC Global Asset Management (Hong Kong) Limited and has been

approved for issue in the United Kingdom by HSBC Global Asset Management (UK) Limited. Authorised and

regulated by the Financial Conduct Authority. www.assetmanagement.hsbc.com/uk

Copyright © HSBC Global Asset Management (UK) Limited 2017. All rights reserved.

17-I-00242/0117ex160717/FP17-0035

Recommended

![Fixed Income Index Guide - BlackRock · [10] FIXED INCOME INDEX GUIDE Bloomberg Barclays index family ... Broad family of fixed income indices, including: aggregate, government, corporate,](https://img.pdfslide.net/doc/110x75/5b0274907f8b9af1148fb575/fixed-income-index-guide-blackrock-10-fixed-income-index-guide-bloomberg-barclays.jpg)