Asian Polyester Markets and the

Impact of Feedstocks

Jeffrey Ong & Samuel Wong

ICIS Markets Editors

5 August 2014, Mumbai

www.icis.com

0

500

1000

1500

2000

2500

3000

3500

4000

2009 2010 2011 2012 2013

tho

usa

nd

to

nn

es

China's Polyester Export Volumes

Polyester filament yarn Polyester short staple PET bottle chips

1455

1846

2411

2696

3474

China’s polyester export volumes

continue rising Year on Year

In 2013, China’s polyester export volumes grew by about

30% compared with 2012.

Source: Industry

www.icis.com

Slowdown in China’s export volumes

in Mar-May 2014

Dip in export volumes in February 2014; very little growth in

export volumes from Mar-May 2014.

0

50

100

150

200

250

300

350

400

450

Jan Feb Mar Apr May

tho

usa

nd

to

nn

es

China's Polyester Export Volumes (Jan-May 2013 vs 2014)

2013 2014

Source: Industry

www.icis.com

Exports of China’s POY 150 Denier

mainly headed for Egypt and Turkey

From Jan 2013 to May 2014, Egypt and Turkey imported

186,000 tonnes of POY; over 80% of total exports from China.

Source: ICIS China

www.icis.com

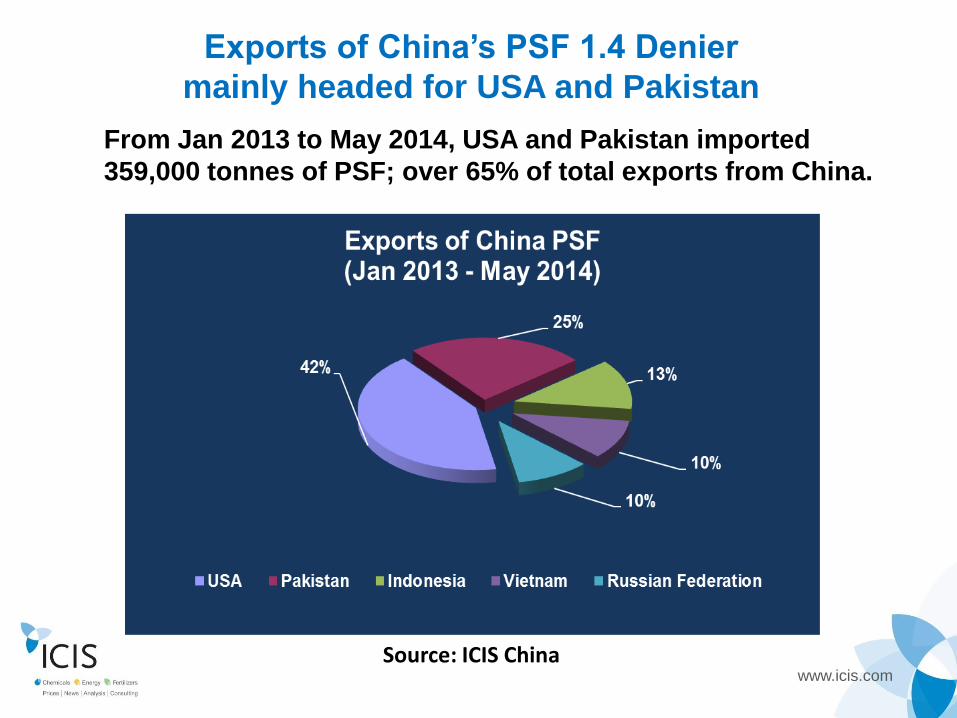

Exports of China’s PSF 1.4 Denier

mainly headed for USA and Pakistan

From Jan 2013 to May 2014, USA and Pakistan imported

359,000 tonnes of PSF; over 65% of total exports from China.

Source: ICIS China

www.icis.com

China Polyester Production in 2011-Apr 2014

2011 2012 2013 Jan-Apr

2014

Output (m tonnes)

26.6 30.2 32.5 11

Change (yoy)

(+13.6%) (+13.5%) (+7.62%) (+9%)

Av. Op Rate 87% 87% 81% 76%

Source: Industry

www.icis.com

Prices of MEG/PTA and polyester demand drive

China’s polyester export prices

Recovery of polyester demand slower than expected; more

restocking in late March/early April; higher offers from June

on feedstock price rise; dip in early July

Source: ICIS

www.icis.com

Feedstock: Monoethylene Glycol

Asia Monoethylene Glycol (MEG)

Market Brief / Key Price Drivers

www.icis.com

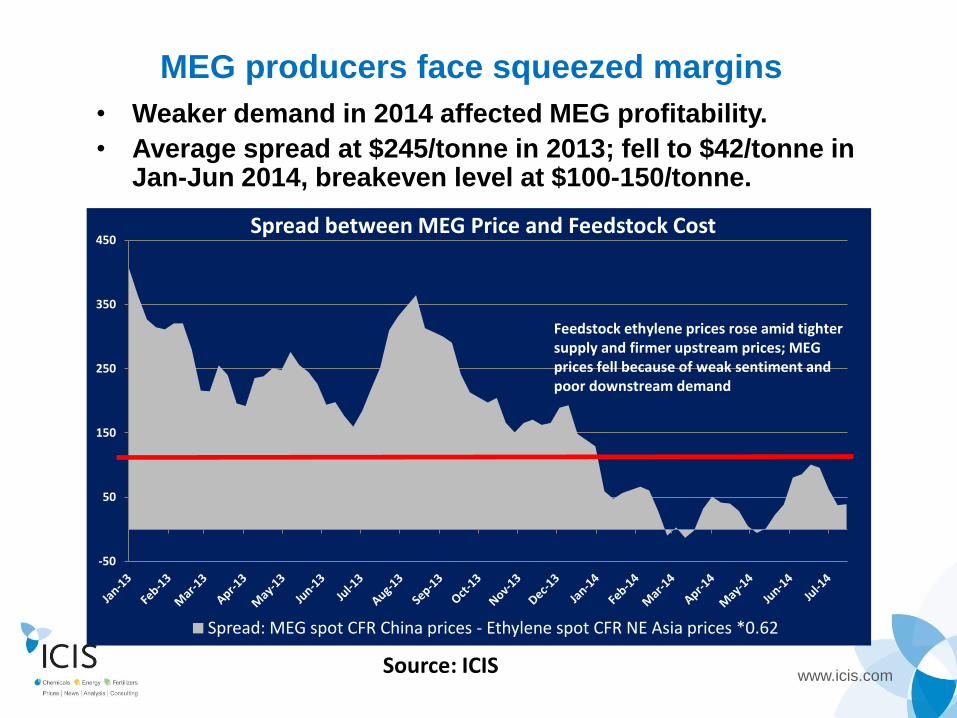

MEG producers face squeezed margins

• Weaker demand in 2014 affected MEG profitability.

• Average spread at $245/tonne in 2013; fell to $42/tonne in Jan-Jun 2014, breakeven level at $100-150/tonne.

-50

50

150

250

350

450 Spread between MEG Price and Feedstock Cost

Spread: MEG spot CFR China prices - Ethylene spot CFR NE Asia prices *0.62

Feedstock ethylene prices rose amid tighter supply and firmer upstream prices; MEG prices fell because of weak sentiment and poor downstream demand

Source: ICIS

www.icis.com

Several production routes for MEG projects

Naphtha, Coal and gas-based MEG projects dominate the

market

Source: Industry

www.icis.com

MEG supply growth higher than demand growth

• Demand growth expected at 6-7% in the coming years

• Capacity growth to reach 8% per year on average in 2013-

2017

-5%

0%

5%

10%

15%

20%

2011 2012 2013 2014E 2015E 2016E 2017E

Gro

wth

rat

e, %

Asia & Middle East MEG Supply vs Demand Growth

Supply Growth Demand growth

Source: Industry

www.icis.com

China’s MEG port inventories stay high, indicating

ample supply in short term

• China’s MEG port inventories hit record high of 1.14m tonnes in

end-Feb 2014 because of import influx and weak domestic

consumption

• Inventories have declined since May, driven by improved demand

Source: ICIS

www.icis.com

Traders dominate Asia spot MEG trade; highly

speculative market

• MEG was viewed by traders as a financial product in 2012-2013 • Tighter credit supply and stringent checks in 2014 curbed

speculation • Entrance of traders not in polyester-related business in 2014

Source: ICIS

www.icis.com

How ethylene prices affect MEG prices

0

500

1000

1500

2000

Jul-03 Jul-04 Jul-05 Jul-06 Jul-07 Jul-08 Jul-09 Jul-10 Jul-11 Jul-12 Jul-13

Asia Ethylene Spot Price vs Asia MEG Spot Price in a 10-year Span

Ethylene spot prices, CFR NE Asia MEG spot prices, CFR China Main Port

In a 10-year time span, the correlation coefficient

between ethylene and MEG spot prices is 0.67

Source: ICIS

www.icis.com

How PTA futures affect MEG spot prices

The correlation coefficient between PTA futures and

spot prices rose to 0.82 in Jun 2013-Jun 2014 from 0.72

in 2011-2012

6000

6500

7000

7500

8000

8500

9000

Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14

Pri

ces,

yu

an (

CN

Y)/

ton

ne

PTA Futures vs MEG Domestic Spot Prices

PTA Futures - the most actively traded contract month MEG spot prices in east China, ex-warehouse

Source: ICIS / Zhengzhou Commodity Exchange

www.icis.com

How downstream demand affects MEG prices

Strong polyester sales drive up prices; weak polyester

demand dampens prices; the correlation coefficient is 0.56

0%

100%

200%

300%

500

750

1000

1250

$/tonne Polyester Sales-to-output Ratios vs MEG Spot Prices

MEG Spot Prices, CFR China Main Port Sales-to-output ratios of yarn producers

Trendline of sales-to-output ratio

Source: ICIS

www.icis.com

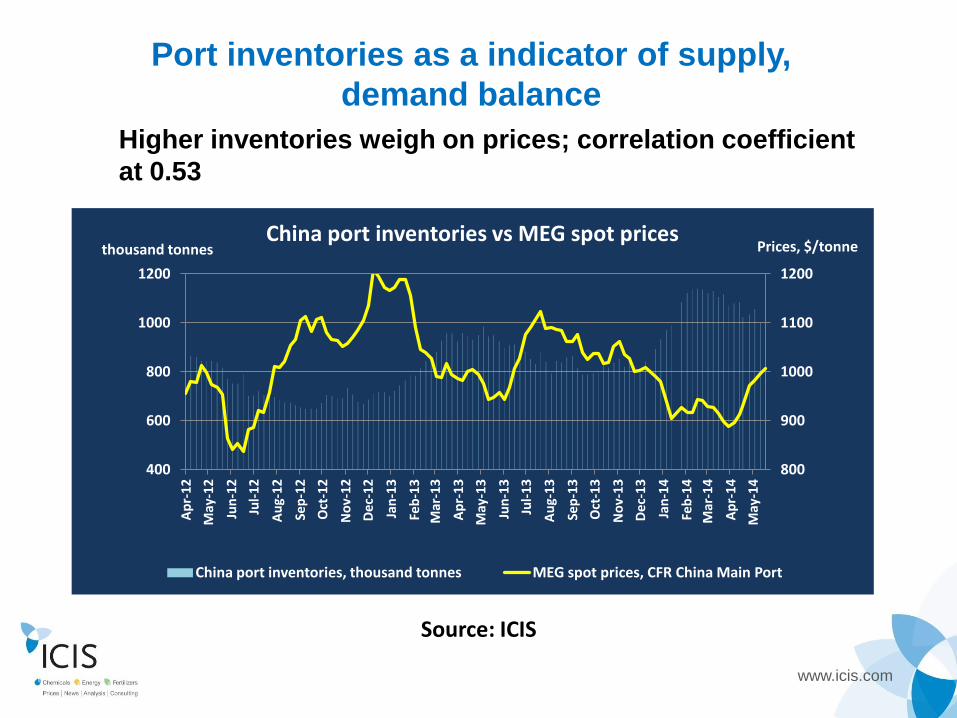

Port inventories as a indicator of supply,

demand balance

Higher inventories weigh on prices; correlation coefficient

at 0.53

800

900

1000

1100

1200

400

600

800

1000

1200

Ap

r-1

2

May

-12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-1

2

De

c-1

2

Jan

-13

Feb

-13

Mar

-13

Ap

r-1

3

May

-13

Jun

-13

Jul-

13

Au

g-1

3

Sep

-13

Oct

-13

No

v-1

3

De

c-1

3

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Prices, $/tonne thousand tonnes China port inventories vs MEG spot prices

China port inventories, thousand tonnes MEG spot prices, CFR China Main Port

Source: ICIS

www.icis.com

Asia Monoethylene Glycol (MEG)

Market Outlook

www.icis.com

Speculation adds uncertainty to MEG spot market

• MEG seen as financial commodity by traders, because of its

balanced-to-tight market fundamentals and price volatility

• As a financial commodity, MEG’s price trend is affected by

• Macroeconomic factors; perfect for speculation

• Crude futures

• China’s monetary policy; credit renewals

• MEG forward-trading prices, PTA futures’ prices

• MEG supply issues, plant outages

• Polyester demand

Traders dominate Asia’s spot MEG market

www.icis.com

China’s port inventories – seen as a good indicator of

supply-and-demand balance

• Supply likely to decrease in H2 2014, because:

• More plant shutdown plans in H2 2014

• One new MEG plant start-up in Korea

• Demand likely to increase in H2 2014, because:

• Peak textile manufacturing season in China in Sep-Oct

• PET capacity expansion in India, PET peak season in US

Asia to see balanced-to-tight supply-demand

balance in near future

www.icis.com

Asia MEG capacity expansion to accelerate

• More coal-based MEG production but quality of MEG from the

process still not satisfactory for polyester production

• MEG capacity expansion to speed up in 2016-2017

• Asian markets might be outlets for shale-gas MEG

Asian MEG supply/demand balance expected to turn balanced-to-long

www.icis.com

Polyester capacity in 2014

Plant name Cap ’13

(kt) New cap ’14

(kt) Start date

for new cap Type

Hainan Yi Sheng Petrochemicals

500 500 Feb Bottle chip

Zhejiang Guxiandao Industrial Fiber Co.

500 500 Mid Mar Industrial

filament yarn

Xin Feng Ming Group Co.

1350 250 Apr (est) Filament yarn

Tong Kun Group Co. 2200 400 Mid Apr Filament yarn

Jiangsu Sanfangxiang 2800 200 Mid May Filament yarn

Shangli Chemical Fiber Co.

0 200 Q4 2014 Short staple

Zhejiang Hua Xin Chemical Fiber Co

25 40 Aug Filament yarn

New capacity will reach 5.57m tonnes

Source: ICIS China

www.icis.com

Feedstock: Purified Terephthalic Acid

Asia Purified Terephthalic Acid (PTA)

Market Brief / Key Price Drivers

www.icis.com

When One Suffers, a Chain Effect Begins

Crude oil Heavy naphtha Crude gasoline Mixed xylenes Para-xylene

Long-chained producers Medium-chained producers

Short-chained producers

Para-xylene *.665 PTA *.86 Polyester *.34 MEG

Key End Use Markets – Consumer Goods

Food & Beverage Personal Care & Home Care

Apparel, Home Textile Apparel, Home Textile Electronics

www.icis.com

PX capacity expansion to accelerate in Asia

Source: Industry

www.icis.com

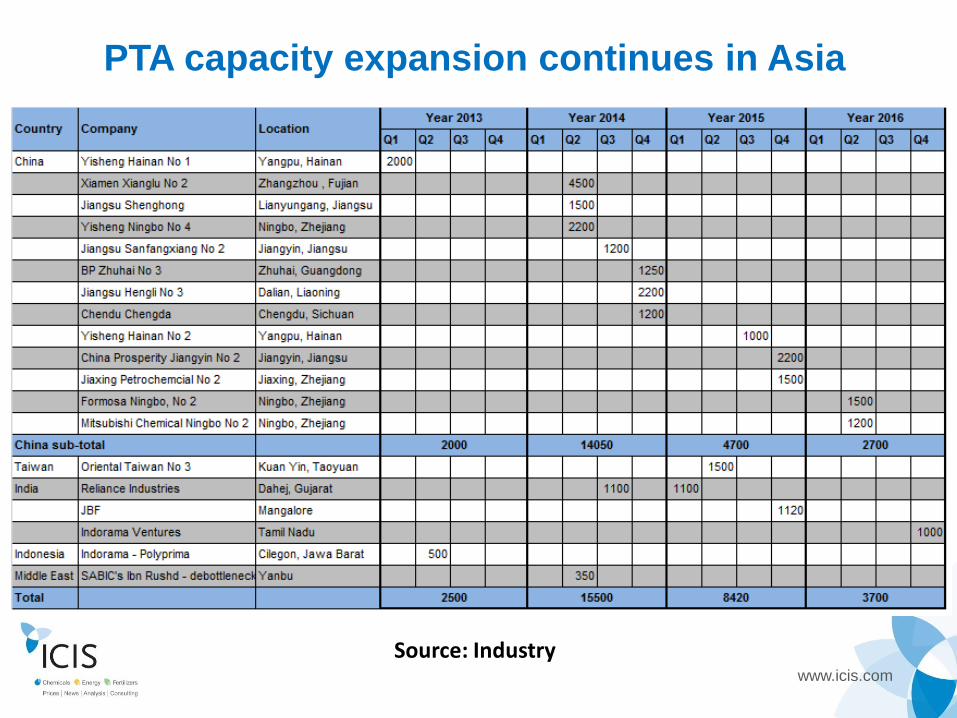

PTA capacity expansion continues in Asia

Source: Industry

www.icis.com

Asia PX capacity growth peaks in 2013-2015

Data source: Industry sources

• Asia’s PX demand growth expected to remain at 5-6% annually.

• Capacity growth forecast at 14-17% annually in 2013-2015, to decline to

5% in 2016. Supply growth acceleration to keep up with downstream

capacities.

9%

2%

17% 15%

14%

5%

8% 5%

6% 5% 5% 6%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2011 2012 2013E 2014E 2015E 2016E

Gro

wth

rate

, %

Asia PX Supply vs Demand Growth

Supply growth rate Demand growth rate

www.icis.com

Asia PTA market to remain oversupplied

Demand expected to grow 6-7%/year; capacity

growth to accelerate again in 2014

Source: Industry

3%

12%

25%

12%

20%

12%

5%

14.5%

7.3% 6.2% 6.5% 7.1% 6.7% 6.8%

0%

5%

10%

15%

20%

25%

30%

2010 2011 2012 2013 2014E 2015E 2016E

Gro

wth

rate

, %

Asia PTA Supply vs Demand Growth

Supply growth rate Demand growth rate

www.icis.com

Asian PTA Producers Under Constant Pressure

-100

-50

0

50

100

150

200

250

300

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Jan

-07

Ap

r-0

7

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Mar

gin

s ($

/to

nn

e)

PX

*0.6

6+$

12

0/t

on

ne

Pri

ces

($/t

on

ne

CFR

CM

P b

asis

)

Time Period

PTA-PX Margins

Margins PTA PX

www.icis.com

PX

Marg

ins

0

200

400

600

800

Jul'13 Aug'13 Sep'13 Oct'13 Nov'13 Dec'13 Jan'14 Feb'14 Mar'14 Apr'14

$/t

on

ne

Naphtha-PX Spread

MARGINS Break Even

0

50

100

150

200

250

Jul'13 Aug'13 Sep'13 Oct'13 Nov'13 Dec'13 Jan'14 Feb'14 Mar'14 Apr'14

$/t

on

ne

MX-PX Spread

MARGINS BREAKEVEN

BREAKEVEN

BREAKEVEN

0

50

100

150

200

250

300

Jul'13 Aug'13 Sep'13 Oct'13 Nov'13 Dec'13 Jan'14 Feb'14 Mar'14 Apr'14

$/t

on

ne

TDP Margins Based on Tol/BZ/PX

TDP Margins BREAKEVEN

BREAKEVEN

www.icis.com

Weak Polyester Demand, PTA Cutbacks

CA

PAC

ITY

80%

72% 68%

55%

68% 63%

69%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Jan'14 Feb'14 Mar'14 Apr'14 May'14 Jun'14 Jul'14

Tho

usa

nd

to

nn

es/m

on

th

China's PTA Operating Rates 2014

TOTAL CAP EFFECTIVE CAP O/R

UTI

LIZA

TIO

N

UTI

LIZA

TIO

N

UTI

LIZA

TIO

N

UTI

LIZA

TIO

N

UTI

LIZA

TIO

N

UTI

LIZA

TIO

N

UTI

LIZA

TIO

N

CA

PAC

ITY

CA

PAC

ITY

CA

PAC

ITY

CA

PAC

ITY

CA

PAC

ITY

CA

PAC

ITY

CA

PAC

ITY

www.icis.com

PX Makers Attempt To Balance Market

South Korea’s makers have largely maintained high operating rates as downstream PTA makers were running their plants at around 95%. Several makers continue to operate TDP at full, while cutting operating rates at PX site, selling feedstock MX, or pushing it for blending.

0

200

400

600

800

1000

1200

1400

1600

1800

2000

60%

65%

70%

75%

80%

85%

90%

95%

100%

105%

Jan Feb Mar Apr

PX Operating Rates

China South Korea Japan China South Korea Japan

www.icis.com

Why The Squeezed Margins In Q1 2014?

76%

82%

74%

80%

72% 68%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

January February March

Import PX Requirement Local Build Up PX O/R PTA O/R

• Build up in stocks in China

• Weak downstream performance

www.icis.com

96% 95% 98%

89%

82%

76% 76%

0%

20%

40%

60%

80%

100%

120%

0

5

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013 2014E 2015E 2016E

Op

erati

ng

rate

s

Un

it:

millio

n t

on

nes/

year

Asia PX Plants Operating Rate

Asia PX capacity Asia PX O/R

To balance supply/demand conditions

www.icis.com

Asia PTA plants to run at lower operating rates

Source: Industry

• PTA capacity reached 60.5m tonnes/year in 2013, up by 12%

from 2012, after a 25% growth in 2012

• Continued expansions will lower operating rates further

91%

77% 73%

66%

63% 64%

55%

70%

85%

100%

0

20

40

60

80

100

2010 2011 2012 2013 2014E 2015E

Op

erati

ng

rate

s

Un

it:

millio

n t

on

nes/

year

Asia and Middle East PTA Capacity Expansion

PTA capacity PTA operating rates

www.icis.com

Thank you!

For enquiries, please contact:

Samuel Wong

Tel: +65 6780 4348

Email: [email protected]

Jeffrey Ong

Tel: +65 6780 4346

Email: [email protected]

Acknowledgments:

ICIS China

Sandra Shen & Luo Xiao Li

Tel: +8621 5155 0208, +86 535-3606408

Email: [email protected],

Recommended