A.T. Kearney 82/7478 1

Supply Chain Financing

Dr. Dale S. RogersNevada Logistics Institute

Reno, NV

13 August 2015

2

2

Overview Strategic Supply Chain Financing

• Supply chain financing defined• Fund the Growth• Working capital

Tactics• Supply chain finance – reverse factoring• E-Payables• Cash Conversion Cycle• Options

3

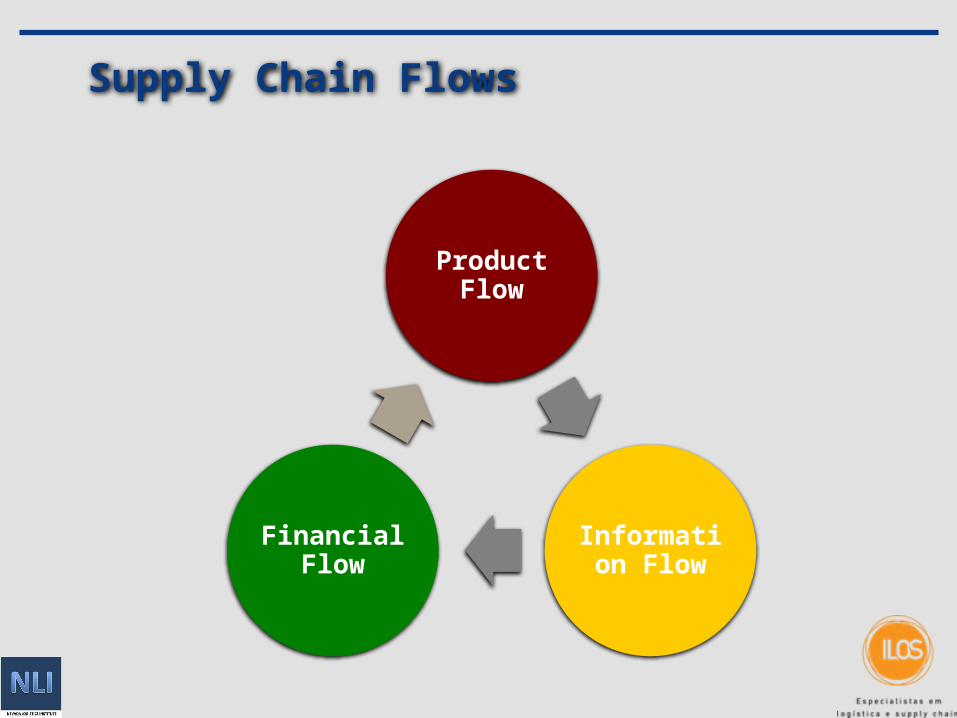

Supply Chain Flows

Product Flow

Information Flow

Financial Flow

4

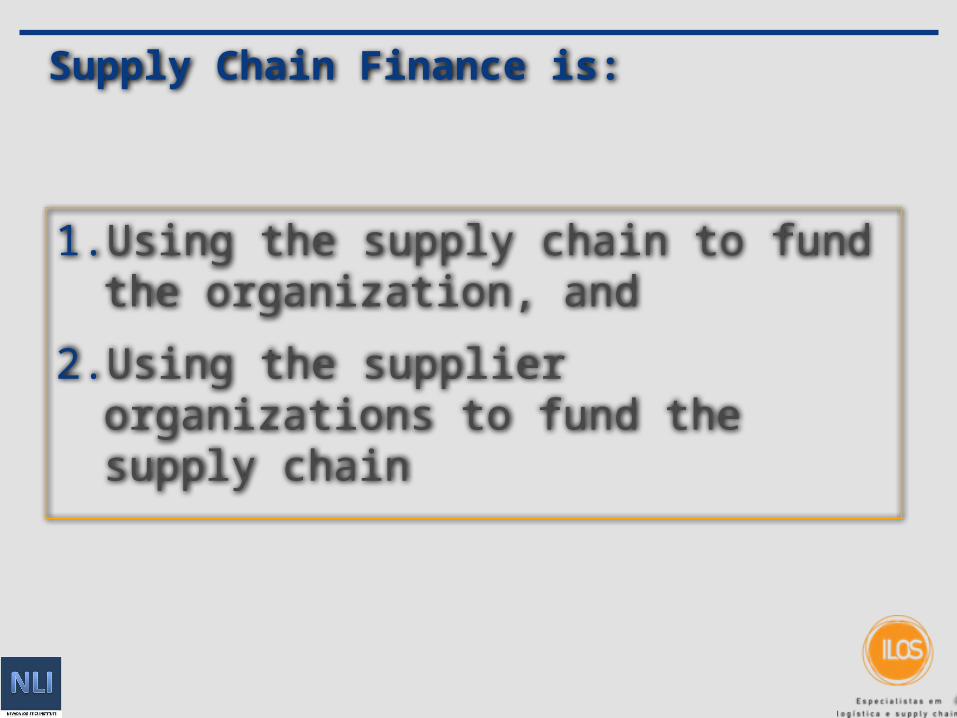

Supply Chain Finance is:

1. Using the supply chain to fund the organization, and

2. Using the supplier organizations to fund the supply chain

5

5

Supply Chain Financing

Fund the Growth!

6

6

Fund the Growth

Firms are looking to an efficient and effective supply chain to fund the growth of the company.

Companies cannot only be dependent on revenues and financial management to grow profit.

7

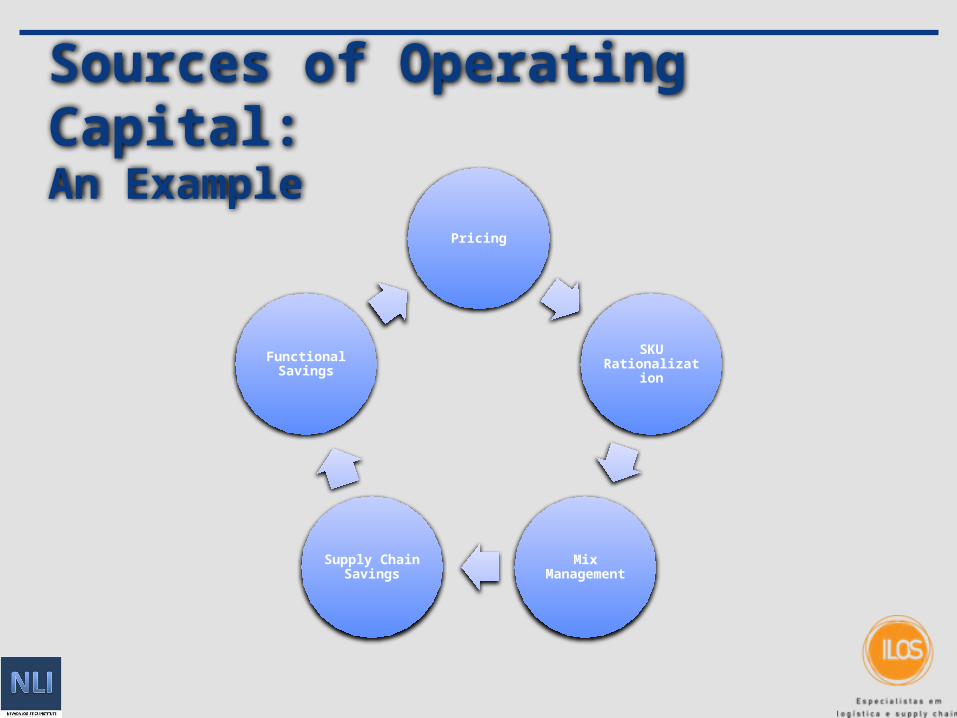

Sources of Operating Capital: An Example

Pricing

SKU Rationalizati

on

Mix Management

Supply Chain Savings

Functional Savings

8

Reasons for Increases In Cash Holdings

Inventories have fallen

Cash flow risk for

firms has increased

Capital expenditures have

fallen

R&D expenditures have

increased.

Source: THOMAS W. BATES, KATHLEEN M. KAHLE, and REN´E M. STULZ (2009). Why Do U.S. Firms Hold So Much More Cashthan They Used To? Journal of Finance

9

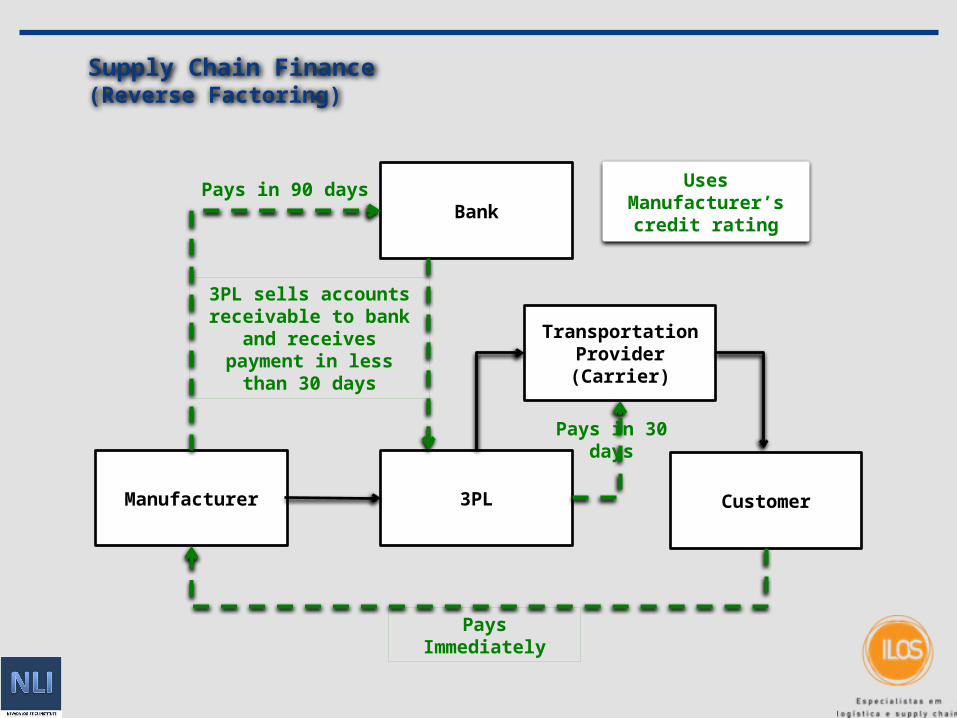

Manufacturer 3PL Customer

Transportation Provider (Carrier)

Bank

Supply Chain Finance(Reverse Factoring)

Pays Immediately

3PL sells accounts receivable to bank and

receives payment in less than 30 days

Pays in 30 days

Uses Manufacturer’s

credit rating

Pays in 90 days

10

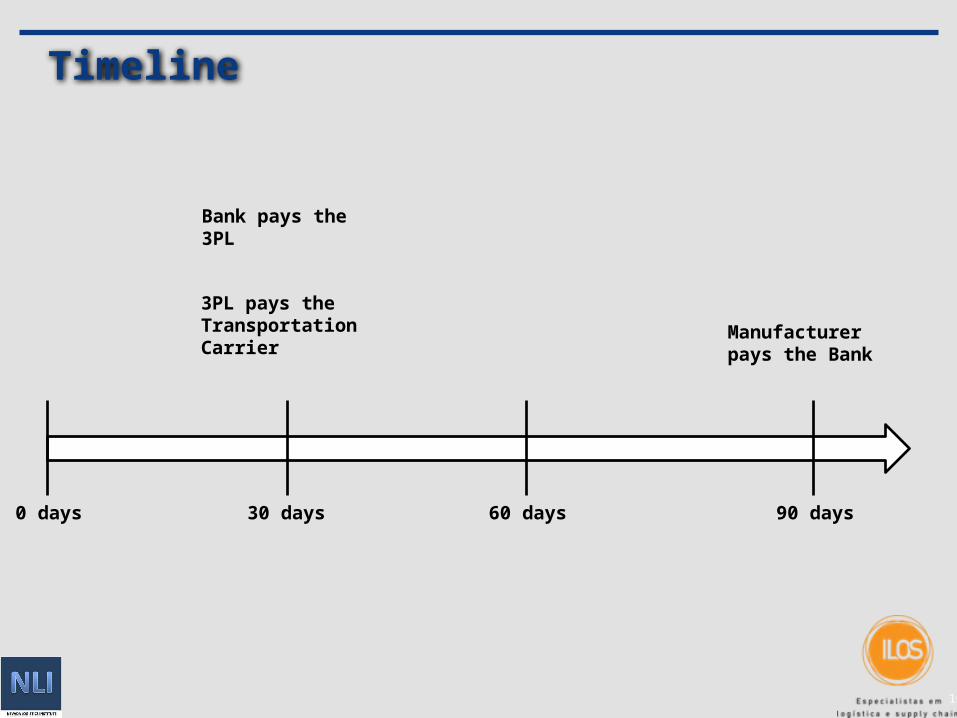

Timeline

0 days 30 days 60 days 90 days

3PL pays the Transportation Carrier

Manufacturer pays the Bank

Bank pays the 3PL

11

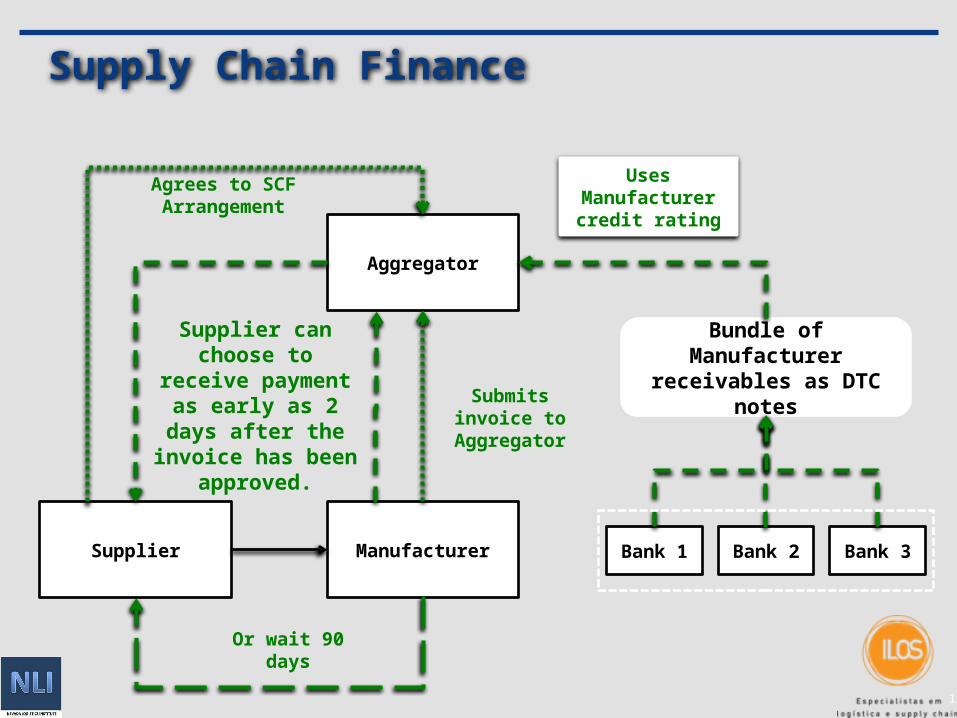

Supplier Manufacturer

Aggregator

Supply Chain Finance

Or wait 90 days

Supplier can choose to receive

payment as early as 2 days after the

invoice has been approved.

Uses Manufacturer credit rating

Bundle of Manufacturer

receivables as DTC notes

Bank 1 Bank 2 Bank 3

Submits invoice to Aggregator

Agrees to SCF Arrangement

12

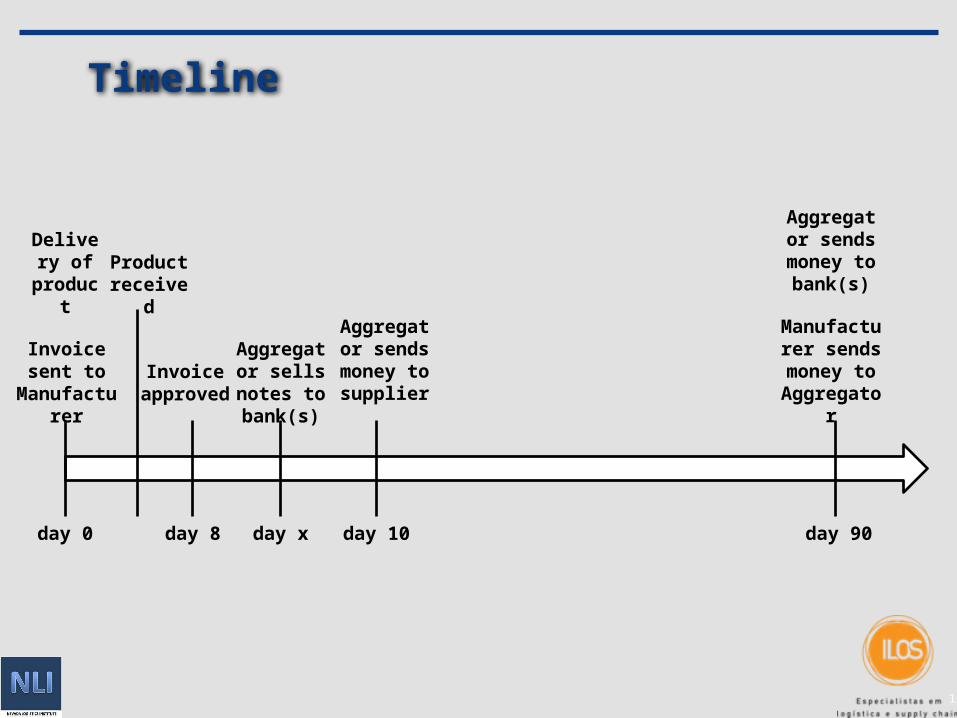

Timeline

day 0 day 10day x day 90

Invoice sent to

Manufacturer

Invoice approved

Aggregator sends

money to supplier

day 8

Manufacturer sends money to

Aggregator

Aggregator sells

notes to bank(s)

Aggregator sends

money to bank(s)

Delivery of

productProduct received

13

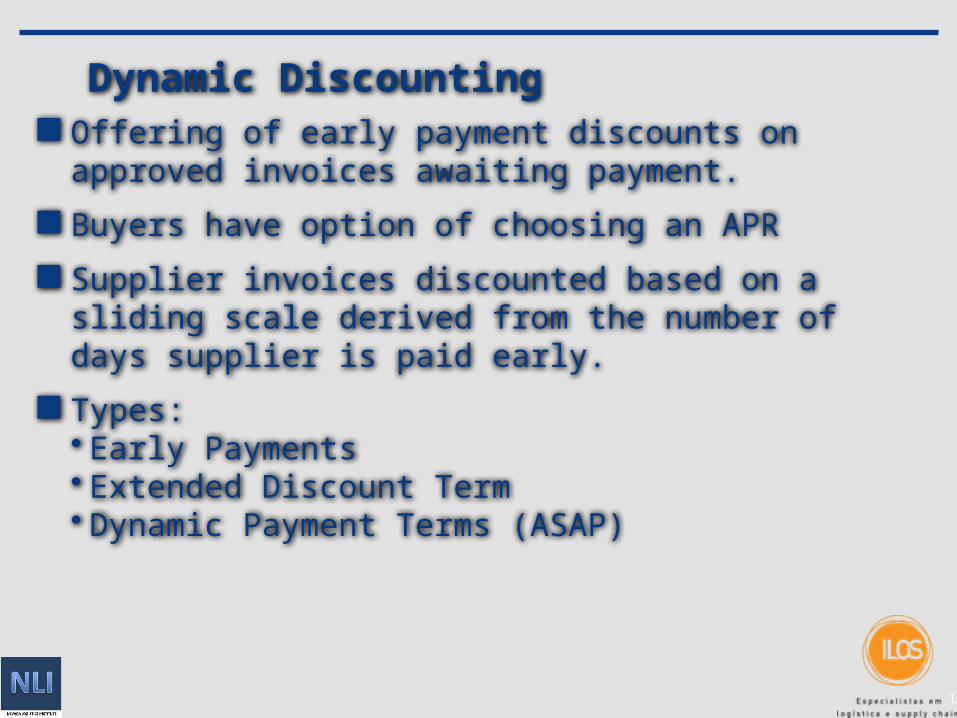

Dynamic Discounting Offering of early payment discounts on approved

invoices awaiting payment.

Buyers have option of choosing an APR

Supplier invoices discounted based on a sliding scale derived from the number of days supplier is paid early.

Types:• Early Payments• Extended Discount Term• Dynamic Payment Terms (ASAP)

14

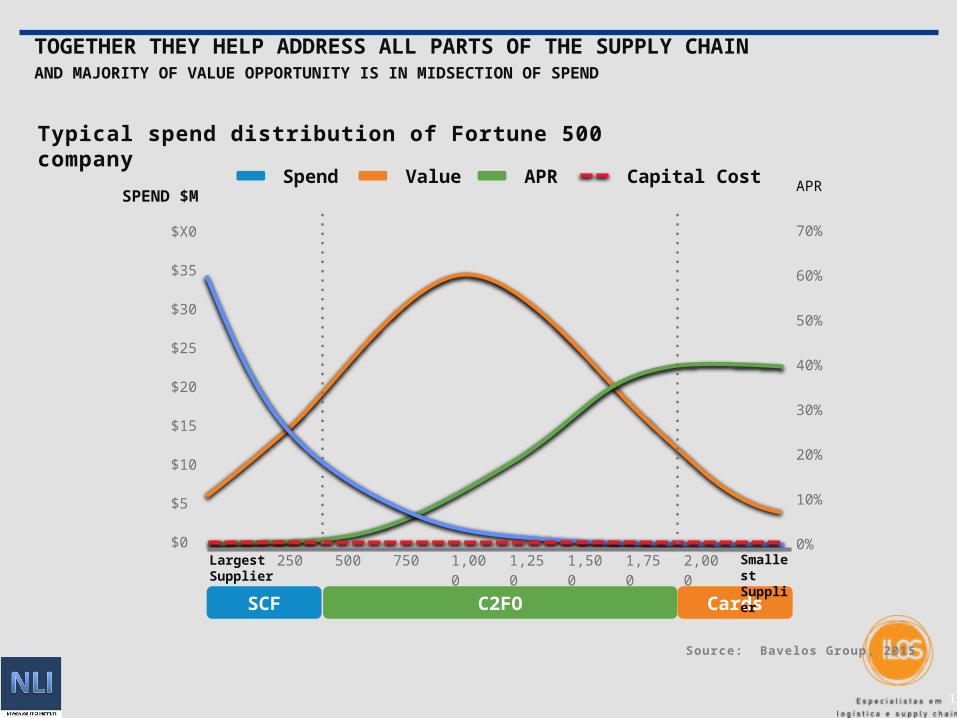

HOW DOES IT FIT WITH OTHER EARLY PAY PROGRAMS?THEY COMPLEMENT EACH OTHER PERFECTLY

Acco

un

ts P

ay

ab

le V

alu

e

Larger

Supplier Size

Smaller

C2FOSCF

Buyer push

Buyer extends DPO

Supplier pull

Buyer generates

profit

Cards

SPEND LEVELS

= SCF $50M+

= C2FO everything in between= P-Cards less than $1M

15

Source: Bavelos Group, 2015

SCF C2FO Cards

250 500 750 1,000

1,250

1,500

1,750

2,000

$X0

$35

$30

$25

$20

$15

$10

$5

$0

APR

70%

60%

50%

40%

30%

20%

10%

0%

SPEND $M

APRSpend Value Capital Cost

Typical spend distribution of Fortune 500 company

TOGETHER THEY HELP ADDRESS ALL PARTS OF THE SUPPLY CHAINAND MAJORITY OF VALUE OPPORTUNITY IS IN MIDSECTION OF SPEND

LargestSupplier

SmallestSupplier

16

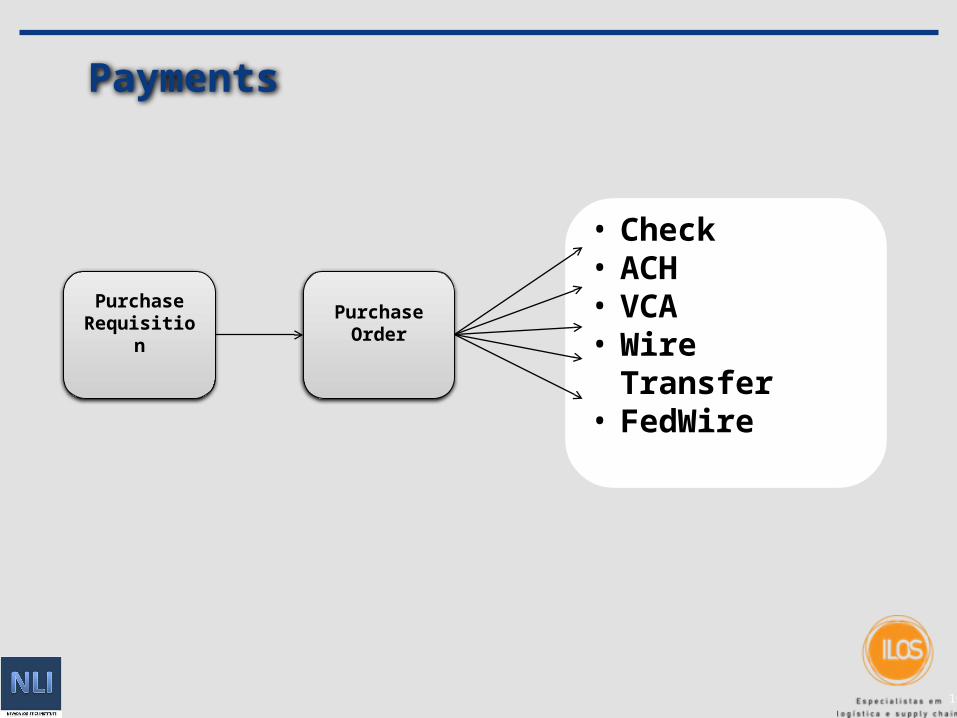

Payments

PurchaseRequisition

PurchaseOrder

• Check• ACH• VCA• Wire Transfer• FedWire

17

E-Payables

E-Payabl

es

P-Card

Ghost

Card

Virtual

Card

18

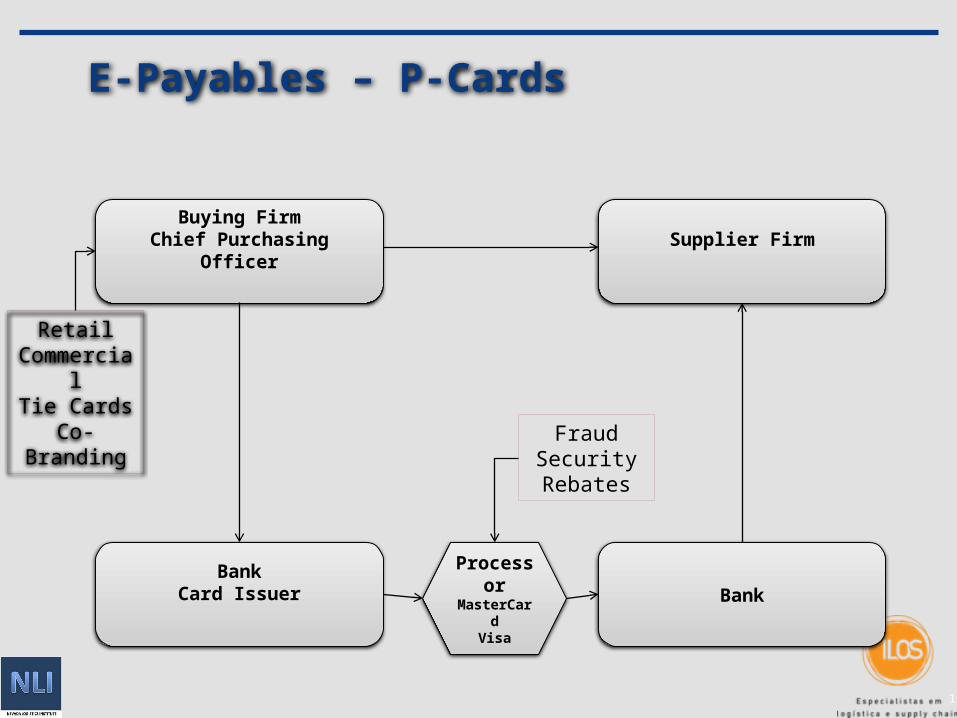

E-Payables – P-Cards

RetailCommercial

Tie CardsCo-Branding

Buying FirmChief Purchasing Officer Supplier Firm

BankCard Issuer Bank

ProcessorMasterCard

Visa

FraudSecurityRebates

19

SCF vs. E-Payables

SCF brings CPO and CFO together. The tension used to be on CPO focusing on price and CFO on working cap.

SCF for core suppliers, large volume of money, frequent transactions.

P-card (or virtual card) more for lots of SME suppliers.

20

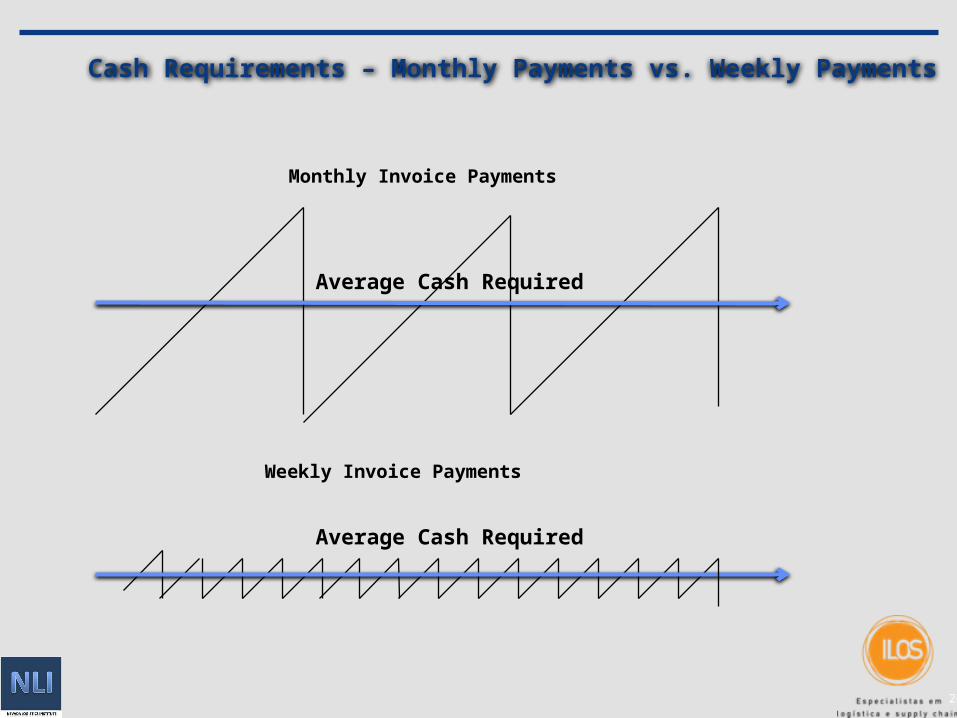

Cash Requirements – Monthly Payments vs. Weekly Payments

Monthly Invoice Payments

Weekly Invoice Payments

Average Cash Required

Average Cash Required

21

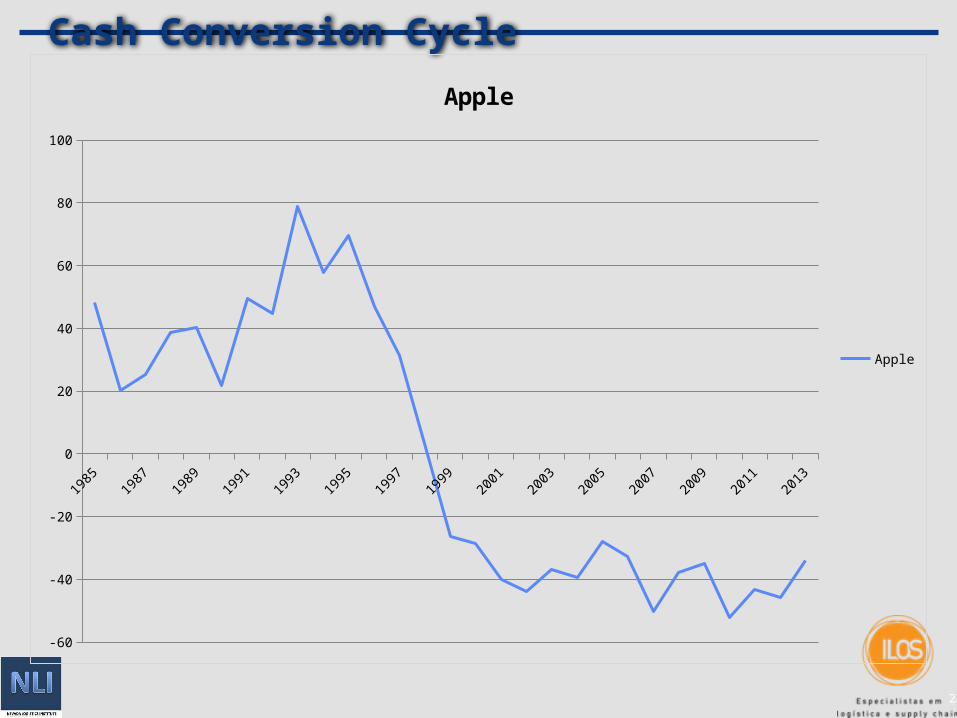

Cash Conversion Cycle

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

-60

-40

-20

0

20

40

60

80

100

Apple

Apple

22

Cash Conversion Cycle

CCC = DSO + DIO – DPO

Days Sales Outstanding (DSO): the number of days needed to collect on sales.

Days Inventory Outstanding (DIO): how many days it takes to sell the inventory.

Days Payable Outstanding (DPO): the company's payment of its own bills.

23

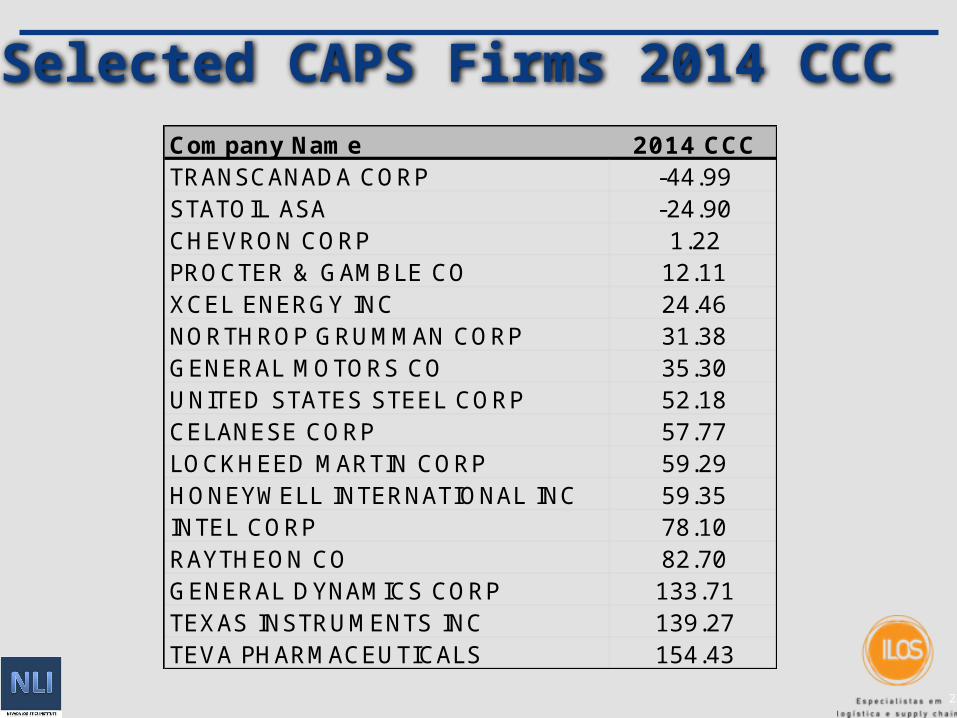

Selected CAPS Firms 2014 CCCCompany Name 2014 CCCTRANSCANADA CORP -44.99STATOIL ASA -24.90CHEVRON CORP 1.22PROCTER & GAMBLE CO 12.11XCEL ENERGY INC 24.46NORTHROP GRUMMAN CORP 31.38GENERAL MOTORS CO 35.30UNITED STATES STEEL CORP 52.18CELANESE CORP 57.77LOCKHEED MARTIN CORP 59.29HONEYWELL INTERNATIONAL INC 59.35INTEL CORP 78.10RAYTHEON CO 82.70GENERAL DYNAMICS CORP 133.71TEXAS INSTRUMENTS INC 139.27TEVA PHARMACEUTICALS 154.43

24

Further Explanation

http://financing.supply

25

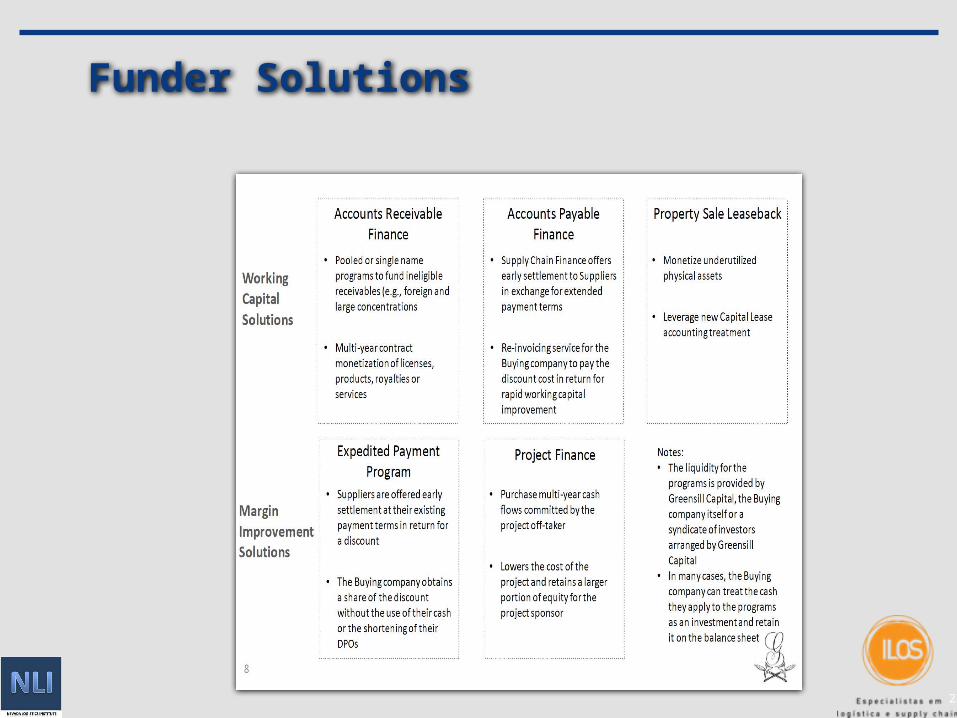

Funder Solutions

26

End Of Presentation

Extra slides follow

27

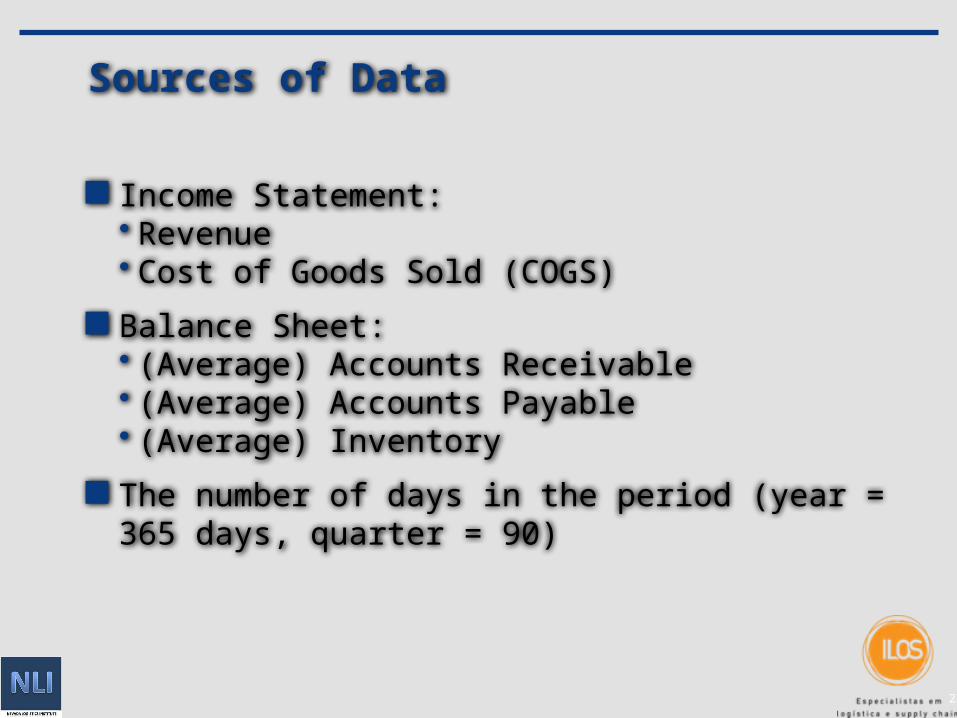

Sources of Data

Income Statement:• Revenue• Cost of Goods Sold (COGS)

Balance Sheet:• (Average) Accounts Receivable• (Average) Accounts Payable• (Average) Inventory

The number of days in the period (year = 365 days, quarter = 90)

28

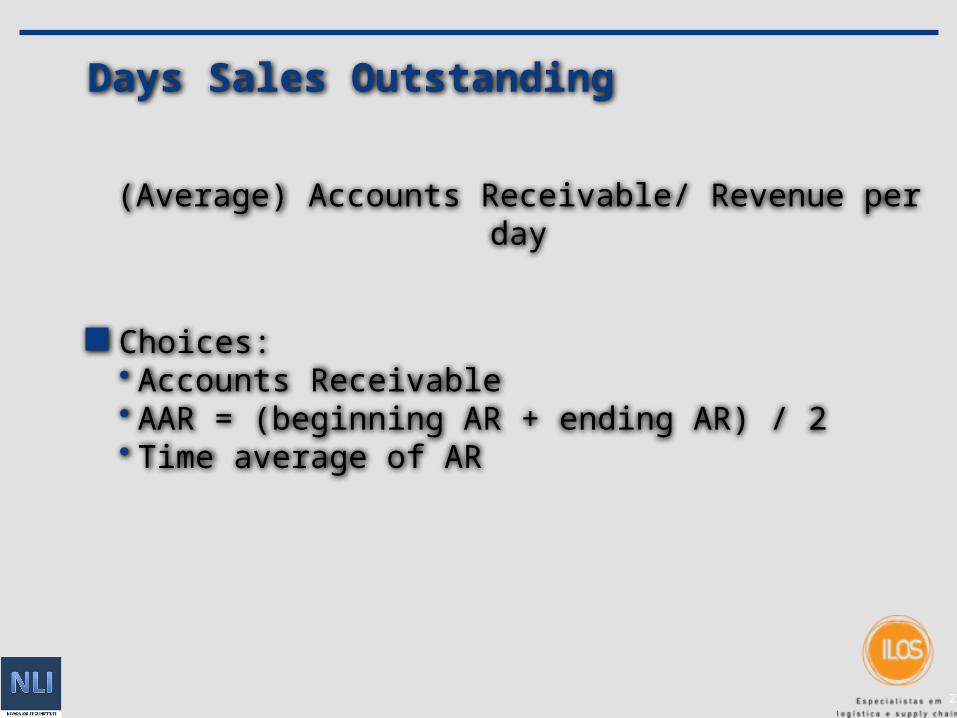

Days Sales Outstanding

(Average) Accounts Receivable/ Revenue per day

Choices:• Accounts Receivable• AAR = (beginning AR + ending AR) / 2• Time average of AR

29

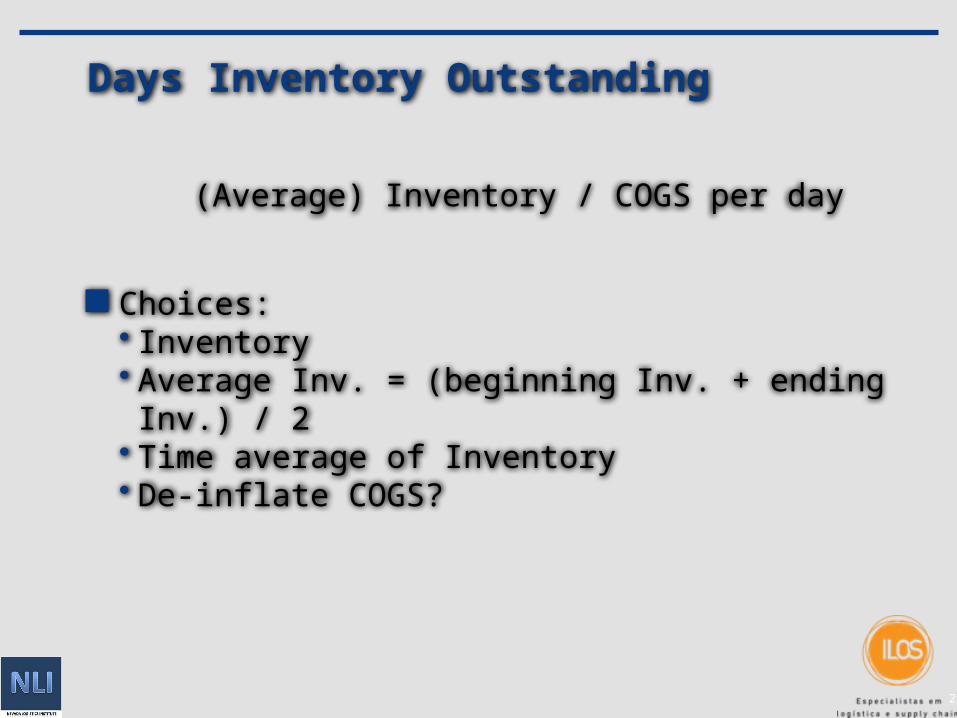

Days Inventory Outstanding

(Average) Inventory / COGS per day

Choices:• Inventory• Average Inv. = (beginning Inv. + ending Inv.) / 2• Time average of Inventory• De-inflate COGS?

30

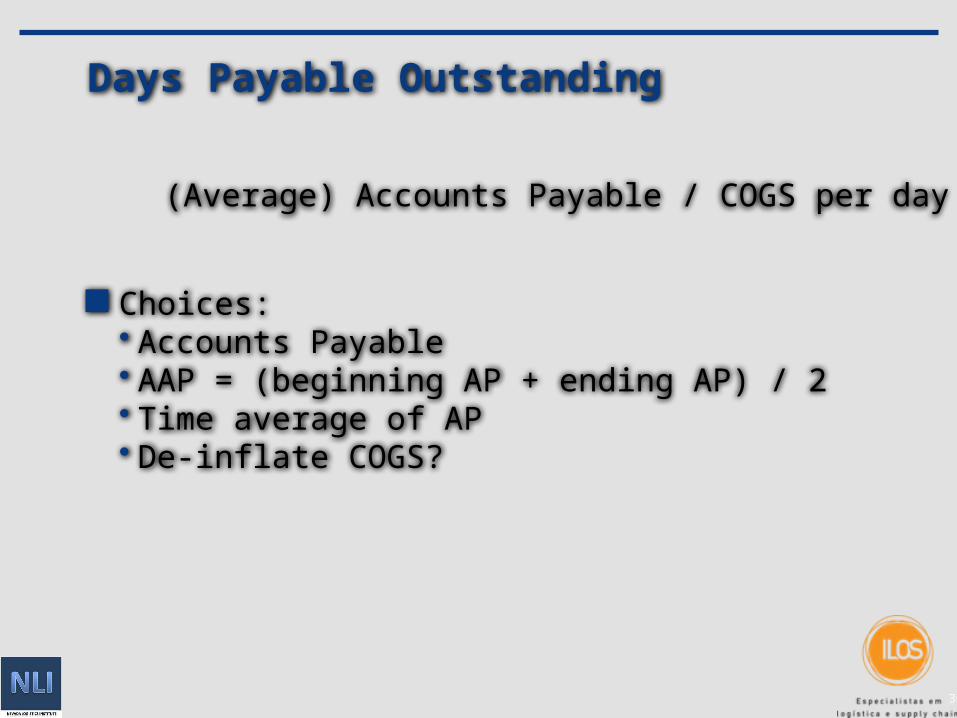

Days Payable Outstanding

(Average) Accounts Payable / COGS per day

Choices:• Accounts Payable• AAP = (beginning AP + ending AP) / 2• Time average of AP• De-inflate COGS?

Recommended

![[XLS]KDCB Music Library - Home | SESD Music Department · Web viewZoot Suit Riot Perry, Steve Kennard-Dale Kennard-Dale Kennard-Dale Kennard-Dale Kennard-Dale Kennard-Dale Kennard-Dale](https://img.pdfslide.net/doc/110x75/5b1a7c437f8b9a28258d8e9a/xlskdcb-music-library-home-sesd-music-web-viewzoot-suit-riot-perry-steve.jpg)