AUTOMOTIVE BUYER INFLUENCE STUDY

FEBRUARY 26, 2015

2015

® 2015 Cox Automotive

Today’s Presenters

Vice President Research & Market Intelligence

Cox Automotive

Senior Analyst IHS Automotive

Isabelle Helms Stephanie Brinley

MARKET OVERVIEW

2015 AUTOMOTIVE BUYER

INFLUENCE STUDY

Q&A | RAFFLE

Overview | Agenda

MARKET OVERVIEW

® 2015 Cox Automotive

More and more difficult to increase market share

Nameplates growing again, after recession eliminated brands

Consumers have a lot to learn: New landscape, new technology

New technology and powertrains increase level of complexity in vehicle selection

Highly Competitive Market

® 2015 Cox Automotive

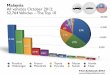

U.S. Light Vehicle Sales

Share

2000

Share

2010

Share

2014

Share

2020

Ford 20% 15% 14% 15%

Chevrolet 15% 13% 12% 12%

Toyota 8% 13% 12% 11%

Hyundai/Kia 2% 8% 8% 8%

Honda 6% 9% 8% 8%

17.8%

15.0%

14.4% 12.7%

10.9%

9.3%

8.4%

7.9% 3.6%

17.1%

15.4%

12.9%

12.1%

12.4%

9.1%

7.6%

8.3%

5.0%

GM

16.8%

Ford

15.6%

Toyota

13.0%

Fiat Chrysler

11.0%

Other

12.6%

Honda

9.4%

Renault/

Nissan

7.6%

Hyundai

8.8%

VW

5.1%

Market Share:

Harder to Gain

a Point

©2015 IHS

® 2015 Cox Automotive

Source: IHS ©2015 IHS

U.S. Light Vehicle Sales

US Sales versus Nameplates

0

50

100

150

200

250

300

350

400

10

11

12

13

14

15

16

17

18

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Mil

lio

ns

U

S S

ale

s

Nu

mb

er

of

Nam

ep

late

s

® 2015 Cox Automotive

Sales, Top 20 US Brands

U.S. Light Vehicle Sales

Source: IHS / ©2015 IHS

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2000 2005 2010 2015 2020

Chevrolet Ford Toyota Honda Nissan Hyundai Kia

Chrysler Jeep Volkswagen Subaru GMC Mercedes-Benz BMW

Mazda Ram Lexus Audi Buick Cadillac

® 2015 Cox Automotive

Brand 2010 2015 2020

Mercedes-Benz 16 21 24

Chevrolet 21 21 21

Nissan 18 20 19

BMW 11 19 23

Ford 21 18 20

Toyota 17 18 17

Honda 14 13 12

Hyundai 10 12 13

Audi 10 12 18

Lexus 10 11 11

Kia 12 10 12

Volkswagen 11 10 13

Cadillac 8 9 12

Infiniti 6 9 11

GMC 9 8 9

Mazda 11 8 8

Jeep 7 7 7

Dodge 11 7 3

Lincoln 7 7 8

Subaru 5 7 8

Sales Parent 2010 2015 2020

General Motors 58 44 49

Toyota 30 36 33

Volkswagen 35 36 48

Fiat 33 34 41

BMW 18 30 33

Renault/Nissan 24 29 30

Ford 33 25 28

Daimler 18 22 25

Hyundai 22 22 25

Honda 20 19 18

Tata (Jaguar Land Rover) 7 10 13

Mazda 11 8 8

Fuji Heavy (Subaru) 5 7 8

Geely (Volvo) 10 6 6

U.S. Nameplate Evolution

©2015 IHS

® 2015 Cox Automotive

U.S. Technology Evolution

First-Generation MyFord Touch Apple Car Play, Mercedes-Benz

SYNC III, Ford

Hyundai Genesis, Remote Start App

Cadillac CUE

Toyota Enform

BMW i3 Valet Park Audi Connect, On-Board 4G LTE

©2015 IHS

® 2015 Cox Automotive

U.S. Technology Evolution

Availability of Select Advanced Drive Assist Systems

Source: IHS / ©2015 IHS

0

50

100

150

200

250

2006

2012

® 2015 Cox Automotive

U.S. Powertrain Evolution

BMW i8

Acura NSX

General Motors 8AT

Ram 1500 EcoDiesel

Mercedes-Benz F-Cell

2015 Ford 2.7-liter EcoBoost

2012 Mustang

©2015 IHS

® 2015 Cox Automotive

A total of 2,297 buyers participated

2015 Automotive Buyer Influence Study

• 1,313 new buyers

• 984 used buyers

Representative of online and offline car buyers

Fourth year conducting this study

SHOPPER FRAME OF MIND

® 2015 Cox Automotive

New buyers more likely to purchase out of “want”

Purchased due to a need

Purchased due to a want

39%

61%

® 2015 Cox Automotive

New buyers “research” vehicles first

Set budget first

64% Research first

36%

® 2015 Cox Automotive

2 out of 3 not sure what they want

Knew Exact

Knew Make

Knew Something

Knew Nothing

Knew the exact vehicle 38%

Knew the body style but not the make or model 26%

Didn't know specific vehicle but knew vehicle class 14%

Didn't know specific vehicle but knew features 8%

Knew the vehicle make 12%

Didn't know anything when research began 3%

RESEARCHING & SHOPPING RESOURCES

® 2015 Cox Automotive

Time spent researching online has increased from 59% to 70%

2015

2011

11hrs 12min

online

7hrs 54min

offline

11hrs 38min

online

5hrs 16min

offline

16hrs 54min

Total Shopping Time

19hrs 6min

Total Shopping Time

® 2015 Cox Automotive

Internet continues to be the top source used for shopping

Internet

Referral

Television

Magazine

Newspaper

Direct Mail

Outdoor Ads

Radio

75%

23%

20%

14%

9%

9%

5%

5%

® 2015 Cox Automotive

Internet is the most effective source leading to dealer

Internet

Prior experience

with dealership

Drove by /

Walked in

Referral from

friend / family

Direct Mail

Newspaper

Outdoor Ads

Radio

Television

Magazine

37%

19%

14%

11%

2%

2%

1%

<1%

1%

1%

® 2015 Cox Automotive

Internet is the most effective source leading to dealer

Internet

Prior experience

with dealership

Drove by /

Walked in

Referral from

friend / family

Direct Mail

Newspaper

Outdoor Ads

Radio

Television

Magazine

37%

19%

14%

11%

2%

2%

1%

<1%

1%

1%

® 2015 Cox Automotive *Source: NADA 2014 Report, does not add exactly to 100% due to rounding

Dealer advertising expenditures*

5%

16%

11%

33%

21%

15%

Other

Newspaper

Radio

Television

Direct Mail

Internet

® 2015 Cox Automotive

Reasons for using Internet

Compare different

models using reviews,

options, or pictures

Research car

pricing

Find info on

special offers

Find out what

current car

is worth

62%

61%

43%

37%

Find actual vehicles

listed for sale 42%

ROLE OF WEBSITES

® 2015 Cox Automotive

Online sources used to shop

Third

Party

Sites

OEM

Sites

Dealer

Sites

Search

Sites

66%

64%

61%

46%

Usage

® 2015 Cox Automotive

66% | 30%

64% | 28%

61% | 23%

46% | 13%

Online sources used to shop

Third

Party

Sites

OEM

Sites

Dealer

Sites

Search

Sites

Usage Time Spent

® 2015 Cox Automotive

Top 3 shopping activities on third-party sites

Third-Party

Sites

Dealer

Sites

OEM

Sites

1 2 3

Research car pricing

Compare models using reviews,

options or pictures

56%

49%

Find out what your current car

is worth

48%

® 2015 Cox Automotive

Top activities on AutoTrader

1

2 3

Find actual vehicles listed for sale

Research vehicle pricing

Compare models using reviews, options or pictures

® 2015 Cox Automotive

Top 3 shopping activities on dealer sites

Third-Party

Sites

Dealer

Sites

OEM

Sites

1 2 3

Find actual vehicles for sale

Research car pricing

52%

48%

Find special offers

40%

Research car pricing

Compare different models using reviews,

options or pictures

56%

49%

Find out what your current car is worth

48%

® 2015 Cox Automotive

Top 3 shopping activities on manufacturer sites

Research car pricing

57%

42%

Find special offers

35%

Third-Party

Sites

Dealer

Sites

OEM

Sites

1 2 3

Find actual vehicles listed for sale

Research car pricing

52%

48%

Find special offers

40%

Research car pricing

Compare different models using reviews,

options or pictures

56%

49%

Find out what your current car is worth

48%

Compare models using reviews,

options or pictures

® 2015 Cox Automotive

Top 3 shopping activities across all sites

Compare models using reviews,

options or pictures

Research car pricing

57%

42%

Find special offers

35%

Third-Party

Sites

Dealer

Sites

OEM

Sites

1 2 3

Find actual vehicles listed for sale

Research car pricing

52%

48%

Find special offers

40%

Research car pricing

Compare models using reviews,

options or pictures

56%

49%

Find out what your current car

is worth

48%

® 2015 Cox Automotive

Most useful online source

37%

34%

19%

Third

Party

Sites

OEM

Sites

Dealer

Sites

33

AN OMNI-CHANNEL APPROACH

® 2015 Cox Automotive

Multi-device usage is on the rise

33% 2014

27%

2013

38%

2015

2013

2014

2015

® 2015 Cox Automotive

Tablet & smartphone use is also on the rise

93%

85%

Laptops & Desktops Tablets Phones

2014

2015

2013

19%

33%

2014

2013

2015

22%

32%

2014

2013

2015

® 2015 Cox Automotive

Mobile research is becoming more prevalent

61% Proportion of research & shopping time on mobile

(among mobile users)

® 2015 Cox Automotive

A poor mobile experience has a negative impact

47% Said it would have a

negative impact on their brand impression

® 2015 Cox Automotive

Top 3 shopping activities on all devices (per device)

Locate a Dealer

Compare Models

59%

45%

Research Pricing

41%

71%

61%

51%

Compare Models

Research Pricing

82%

70%

Find Special Offers

63%

Compare Models

Research Pricing

Find Special Offers

1 2 3

CLOSING THE DEAL

® 2015 Cox Automotive

purchased model they had in mind

prior to dealership visit

Opportunity to influence is online

77%

® 2015 Cox Automotive

Closing thoughts

Auto market is increasingly competitive, market share more difficult to increase

Consumers have much broader level of choice than ever before, and receiving information from a greater variety of sources

Understanding how, when and where to reach the customer is increasingly critical

Provide meaningful content that’s always available to shoppers whenever, wherever and however they want it

You can’t close the deal if you can’t get the customer in the door

Q&A RAFFLE

® 2015 Cox Automotive

Raffle Sonos PLAY:5

® 2015 Cox Automotive

Q&A

Recommended