Bakken and Permian: Deal Metrics in the Two Hottest Plays

Ward PolzinJuly 11, 2012

Industry Leading Investment Banking Practice

2010 - 2012 YTD

Firm Value ($MM)

Barclays $143,412

2010 - 2012 YTD

Firm # Deals

Tudor Pickering Holt & Co 63

Advisory

Sell-side & Buy-side

Joint Ventures

Opinions

S i l C itt

Capital Markets

Public Equity

Hybrids

Fixed income

P i t l t

Top Energy Advisor(1)

($ in millions)

Goldman Sachs 121,989

Tudor Pickering Holt & Co 76,902

Credit Suisse 71,046

Evercore Partners Inc 65,828

Citi 64,354

Morgan Stanley 60,881

J ff i & C 57 868

RBC Capital Markets 45

Barclays 44

Jefferies & Company 37

Bank of America Merrill Lynch 34

Goldman Sachs 30

JPMorgan 30

C dit S i 28

Special Committee

Strategic advisory

Restructuring

Private placements

QIU

Jefferies & Company 57,868

JPMorgan 50,179

Deutsche Bank 40,258

Credit Suisse 28

Citi 28

Deutsche Bank 20UpstreamMidstream/MLP OFS Power

Overview TPH combines banking expertise with engineering talent to deliver

Coverage of Midstream/MLP, OFS, Power and Upstream sectors

Senior execution expertise in M&A, Corporate Finance, A&D and Capital Markets

Banking Expertise Engineering Talent

high quality advice to energy clients

Managing Director

11Analyst

12

Capital Markets

Industry/engineering expertise integrated into IB effort across all sectors

Three-year old team achieved 25% market share(1) in 2010T t l T 40

Senior Advisor1

Director3

Vice President4

Associate9

2___________________________________(1) Source: Dealogic: United States Oil & Gas – Exploration & Development/Field Equipment & Services/Diversified/Pipeline and

Utility & Energy – Gas, pending and completed M&A transactions announced 1/1/2010 to 6/22/2012.

>25% market share(1) in 2010Total Team: 40

TPH Investment Banking TPH Research

TPH Resource Experience

Bakken

Current Sell-side: Helis Oil & GasCurrent Sell-side: Cornerstone Natural ResourceBuy-side: Crestview Partners acquisition of Samson Investment CompanyBuy-side: Statoil ASA acquisition of Brigham ExplorationSell-side: Citation Oil & Gas Corp. sale to multiple buyersSell-side: Kaiser Francis Oil CompanySell-side: TRZ Energy (Tracker) sale to HessS ll id A i Oil & G l t H

Upstream companies covered with Bakken exposure: 12□ Selected Bakken operator coverage: CLR, EOG, HES,

NFX, OAS, OXY, STO, WLL, XOMPublished detailed Williston Basin primer

Sell-side: American Oil & Gas sale to HessAtinum investment in Triangle PetroleumCapital markets: Oasis IPO/high yield & multiple BEXP follow-on offerings

Permian

Buy-side: Apollo & Riverstone acquisition of El Paso’s upstream businessBuy-side: Laredo Petroleum acquisition of Broad Oak EnergySell-side: OGX Resources sale to undisclosed buyerSell-side: Eagle Oil and Gas to Comstock ResourcesS ll id RKI E l ti & P d ti it i t t

Upstream companies covered with Permian exposure: 24□ Selected Permian operator coverage: APA, APC, BRY,

CXO, DVN, EOG, OXY, PXD, SD, WLL, XECPublished detailed Permian Basin primer focused on the S b T d i M h 2009e a Sell-side: RKI Exploration & Production equity investment

Sell-side: Yates Drilling Company to undisclosed buyerBuy-side: Crestview acquisition of equity in Select Energy ServicesSell-side: Arena Resources merger with SandRidge Energy

Spraberry Trend in March 2009

Eagle Ford

Sell-side: Antares Energy sale to ChesapeakeBuy-side: CNOOC/Chesapeake Joint VentureSell-side: Pioneer Joint Venture with RelianceB id L i t t d

Upstream companies covered with Eagle Ford exposure: 15□ Selected Eagle Ford operator coverage: APC, EOG,

GDP, HK, NFX, PXD, ROSE, SM R tl l d “Sh ll Di ” i t E l F d i 2010Buy-side: Large integrated

Buy-side: Potential $400MM private equity investmentRecently released “Shallow Dive” into Eagle Ford in 2010Continuing close coverage of well results in play

Haynesville

Sell-side: Ellora Energy sale to ExxonMobilSell-side: Undisclosed Private Company to undisclosed buyerBuy-side: Large public company seeking to establish E Tx positionRegency/GE/Alinda Haynesville Expansion Project (midstream)

Upstream companies covered with Hayesville exposure: 13□ Selected Haynesville operator coverage: APC, BG, CHK,

GDP, RRC, XCO, XOM Significant recent focus on midstream issues in basin

Marcellus

Buy-side: $400MM Private Equity Joint VentureBuy-side: Enerplus Joint Venture with Chief for $406MMBuy-side: Potential $500MM Private Equity investmentSell-side: Quest Resources Corp to Multi

Upstream companies covered with Marcellus exposure: 16□ Selected Marcellus operator coverage: CHK, COG, CRZ,

RRC, SWN, UPL, XCO Released in-depth report on the play simultaneously with initiation of Cabot in June

Ni b

Sell-side: DIA mineral lease saleSell-side: Undisclosed private company

Upstream companies covered with Niobrara exposure: 14□ Selected Niobrara operator coverage: APC, CHK, CLR, Niobrara p p y

Sell-side: Joint ResourcesBuy-side: CNOOC/Chesapeake Joint Venture

p g , , ,EOG, NBL, SM

UticaSell-side: Marquette sale to HessSell-side: PDC Energy Joint Venture

Upstream companies covered with Utica exposure: 8□ Selected Utica operator coverage: APC, CHK, HES

3

Commodity Prices Set the Stage

Long Term Oil Price is KeyToday’s Question: At what oil price do we drop rigs?Today s Question: At what oil price do we drop rigs?

$150

Historical WTI Spot

$150

Historical WTI Spot 1/1/2009 Strip

$150

Historical WTI Spot 1/1/2009 Strip 1/1/2010 Strip

$150

Historical WTI Spot 1/1/2009 Strip 1/1/2010 Strip 1/1/2011 Strip

$150

Historical WTI Spot 1/1/2009 Strip 1/1/2010 Strip 1/1/2011 Strip 1/1/2012 Strip

$150

Historical WTI Spot 1/1/2009 Strip 1/1/2010 Strip 1/1/2011 Strip 1/1/2012 Strip 7/2/2012 Strip

$110

$130

) $110

$130

) $110

$130

) $110

$130

) $110

$130

) $110

$130

)

$70

$90

WTI Pric

e ($/Bbl)

$70

$90

WTI Pric

e ($/Bbl)

$70

$90

WTI Pric

e ($/Bbl)

$70

$90

WTI Pric

e ($/Bbl)

$70

$90

WTI Pric

e ($/Bbl)

$70

$90

WTI Pric

e ($/Bbl)

$50

$70

$50

$70

$50

$70

$50

$70

$50

$70

$50

$70

$30$30$30$30$30$30

5___________________________________Source: Bloomberg as of 7/2/2012.

Negative Gas Outlook Impacting Deal Metrics

$15

Historic Henry Hub Spot

$15

Historic Henry Hub Spot 1/1/2009 Strip

$15

Historic Henry Hub Spot 1/1/2009 Strip 1/1/2010 Strip

$15

Historic Henry Hub Spot 1/1/2009 Strip 1/1/2010 Strip 1/1/2011 Strip

$15

Historic Henry Hub Spot 1/1/2009 Strip 1/1/2010 Strip 1/1/2011 Strip 1/1/2012 Strip 7/2/2012 Strip

$9

$12

ce ($/M

Mbtu)

$9

$12

ce ($/M

Mbtu)

$9

$12

ce ($/M

Mbtu)

$9

$12

ce ($/M

Mbtu)

$9

$12

ce ($/M

Mbtu)

$6

Natural G

as Pric

$6

Natural G

as Pric

$6

Natural G

as Pric

$6

Natural G

as Pric

$6

Natural G

as Pric

$0

$3

$0

$3

$0

$3

$0

$3

$0

$3

6___________________________________Source: Bloomberg as of 7/2/2012.

Recent Decline in NGL Prices

$160100%Representative NGL Barrel % of WTI WTI Spot Price ($/Bbl)

Ethane prices

~74%

$12075%

~74%

$8050%

WT

I Spot ($/Bbl)N

GL

% o

f W

TI

$4025%

NGL prices

~44%

$00%Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12

___________________________________Source: Bloomberg as of 7/2/2012.Note: Representative consists of barrel 40% ethane, 10% normal butane, 25% propane, 15% natural gasoline and 10% iso butane.

7

Liquids Rig Count Shift Has Been Dramatic

2,500

U.S. Onshore Rig Count

534

2,030 2,005 1,955 2,000

1,606

935

879 1,000

1,500 27%

1,070

1,421

700

879

500 73%

424 179

0

Peak3Q09

Trough2Q09

Near-Term Peak 3Q11 Current6/29/12

___________________________________Source: Baker Hughes as of 6/29/2012.Note: “Peak 3Q09” defined as 9/12/2008, “Trough 2Q09” defined as 6/5/2009, and “Near-Term Peak” as 10/7/2011.

GasLiquids

8

Permian and Bakken Driving Oily Rig Shift

Selected Gas Shales Permian Eagle Ford Bakken Granite Wash Niobrara Hz. Ms Lime

1,200

1,500

t

Selected Oily Rig Count: ~940

Bakken: ~215

900

cted

Rig

Cou

nt

300

600

Sele

c

0Q1'07 Q3'07 Q1'08 Q3'08 Q1'09 Q3'09 Q1'10 Q3'10 Q1'11 Q3'11 Q1'12

9___________________________________Source: TPH Research as of 7/2/2012.

Bakken Vaults North Dakota to #2 US Producer

March 2012 Production by State (Mbbl/d)

TX 1,790 240650

Monthly Avg. Rig Count

Bakken Production (Mboe/d)

Montana Bakken Production North Dakota Bakken Production Bakken Rig Count

AK

ND

,

587

579 180

200

220

450

500

550

600

CA

OK

548

226

100

120

140

160

300

350

400

450

40

60

80

100

100

150

200

250

0

20

0

50

100

Mar-01 Mar-02 Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12

10___________________________________Source: Baker Hughes Montana and North Dakota rig count, HPDI and EIA.Note: HPDI production data reported with a 3 month lag.Note: Texas, North Dakota and Alaska production per state industrial commissions.

Bakken Rig Count Close to a Peak?Has Bakken rig count peaked in the 200 – 225 rig range in light of the current commodity backdrop? Has Bakken rig count peaked in the 200 – 225 rig range in light of the current commodity backdrop?

$125250 Williston Basin Rig Count WTI Spot Price

$100

$125

200

250

$75150

WTI Spot Price ($/n

Basi

n Ri

g Co

unt

$25

$50

50

100

/bbl)W

ilist

on

$00 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12

11__________________________________Source: HPDI and RigData as of 7/2/2012.

Deal Flow Follows Commodities

Gas Down, Oil Up: Shocking!

$60 40 $60

Resource Deal Volume Gas Deals

40 $60

Resource Deal Volume Gas Deals Oil Deals

$35 1

$40.6

$51.4

$45

me

($Bn

)

$35 1

$40.6

$51.4

30 $45

Resme

($Bn

)

$35 1

$40.6

$51.4

30 $45

Resme

($Bn

)

$22.7

$35.1

$18.4

$30

sour

ce D

eal V

olu

$22.7

$35.1

$18.4

20 $30

ource Deal Coun

sour

ce D

eal V

olu

$22.7

$35.1

$18.4

20 $30

ource Deal Coun

sour

ce D

eal V

olu

$6.9

$15

Res

$6.9

$

10 $15

ntRe

s

$6.9

$

10 $15

ntRe

s

$02007 2008 2009 2010 2011 2012

0 $02007 2008 2009 2010 2011 2012

0 $02007 2008 2009 2010 2011 2012

13_______________________________Source: IHS Herold as of 7/2/2012.

Deals Shifting to Oil/Liquids-Rich

2010 Deal Count 2011 - 2012 YTD Deal Count

Oil Deals47%

Gas Deals53% Oil Deals

68%

Gas Deals32%

14_______________________________Source: IHS Herold as of 7/2/2012. Includes transactions greater than $50 million in which United States is the primary country. Note: Oil and gas transactions are separated on the basis of reserve composition.

Gas Transactions Oil/Liquids-Rich Transactions

Diversity Among Oil/Liquids-Rich Deal Flow2011 Present Deal Count2011 – Present Deal Count

Permian Shale15%

Bakken29%

Niobrara8%

MS Lime6%

Uti

Granite Wash2%

Eagle Ford27%

Utica13%

____________________________________Source: IHS Herold as of 7/2/2012.Note: Deal value >$50 million. Reflects transactions where United States listed as primary country. Excludes JVs.

15

Conventional Oil Metrics Stable

$32

$/BoeReserves ($/Boe)

$160,000 $32

$/Boe/d$/BoeReserves ($/Boe) Production ($/Boe/d)

$23.58 $24

$32

$23.58 $120,000

$160,000

$24

$32

$20.10

$16.07

$20.06

$16.38

$19.16 $17.79 $17.63 $17.49

$16

$20.10

$16.07

$20.06

$16.38

$19.16 $17.79 $17.63 $17.49

$80,000

,

$16

$8 $40,000 $8

$0Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12

$0 $0Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12

16____________________________________Source: IHS Herold as of 7/2/2012.Note: Deal value >$50 million. Reflects transactions where United States listed as primary country. Excludes JVs.

Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12

Bakken Deal Specifics

Strong Deal Market Throughout the BasinKodiak – Peak Magnum Hunter - Baytex Hess - American

Oxy - Cirque30K acres, 3Q 2010

Ursa

15K acres, $7,600/acre, 500 boe/d, 4Q 2010

g y50K acres, $5,200/acre, 1,300

boe/d, 2Q 2012

85K acres, $5,400/acre, 167 boe/d, 3Q 2010

Statoil - Brigham375K acres,

$12,500/acre, 16,800 boe/d, 3Q 2011

Crescent Point -

Linn - Cade & Holt4.6K acres, 800 boe/d

Petro-Hunt51K acres

Anschutz25k acres

HK – GEOI55k acres, Q2 2012

Nesson Anticline

Li l K if

Linn – Concho11K acres, $17,500/acre,

1,350 boe/d, 1Q 2010

Kodiak – North Plains50K acres, $11,800/acre,

3,500 boe/d, 4Q 2011

Oasis2 undisclosed transactions,

16.7K + 10K acres, $3,000/acre, 300 boe/d,

4Q 2010

Enerplus – Peak

Little KnifeAnticline

Williams – Dakota 385K acres, $10,800/acre, 3,300

boe/d, 4Q 2010

3,500 boe/d, 4Q 2011

Ursa100K acres

Petro-Hunt5K acres

Occidental – Anschutz180K acres, $7,800/acre, 5,500

boe/d, 4Q 2010

47K acres, $9,800/acre, 800 boe/d, 3Q 2010

GMXR-Undisclosed26K acres, $2,165, 1Q 2011

Petro-Hunt22K acres

18

Lower Bakken LimitHess - Tracker

167K acres, $8,000/acre, 4,400

boe/d, 4Q 2010

___________________________________Note: TPH estimates of current market conditions.

Petro-Hunt12K acres /

5K acres

Kodiak - BTA13.5K acres, $17,400/acre,

3,000 boe/d, 3Q 2011

Citation30K acres

Bakken Transactions Through Time

$10,068 $9 303$10 000

$12,000

$14,000 Average $/Acre

Deal Metrics Remain Stable(1)

$10,068 $9 303$10 000

$12,000

$14,000 Median $/Acre Median $/Acre

Constant ~$90/bbl price deck = Constant valuation

$7,118 $6,057

$3,047

$4,415

$9,303

$7,946

$5,233

$4,000

$6,000

$8,000

$10,000

Ad

just

ed $

/Acr

e

$7,118 $6,057

$3,047

$4,415

$9,303

$7,946

$5,579

$4,000

$6,000

$8,000

$10,000

Ad

just

ed $

/Acr

e

Median $/Acre = ~$6,600

$0

$2,000

Q3'10 Q4'10 Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12

Bakken Deal Flow Shaped by Large Transactions

$0

$2,000

Q3'10 Q4'10 Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12

$5,295

5

6

7

$5,000

$6,000

$7,000

Numbe

MM

)

Other Transaction Volume ($MM) Single Transaction Volume ($MM) Deal Count

Bakken Deal Flow Shaped by Large Transactions

Statoil / BEXP: $4.7 Bn OXY / Anschutz: $1.4 Bn

$914

$3,565

$638 $399$1,055

$1,326

1

2

3

4

$1 000

$2,000

$3,000

$4,000

er of TransactionsDe

al V

olu

me

($M

HES / Tracker: $1.0 BnHK/GEOI: $945 MM

$$251 $399

0

1

$0

$1,000

Q3'10 Q4'10 Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12

19___________________________________Source: Company Investor Presentations and press releases.(1) Adjusted $/acre estimate excludes PDP and does not correct for developed acres. PDP valued at $50,000 boe/d.

Strong Deal Metrics Throughout the BasinFactors Impacting Value:

$3,000 - $5,500/acre

Factors Impacting Value:Bakken and Three Forks present?Offset well performanceIs the area “de-risked”?# of wells/DSU?

$4,000 - $8,000/acre

>$10,000/acre

Deeper Three Forks?

$6,000 - $12,000/acre

$6,000 - $12,000/acre

$8,000 - $10,000/acre

20___________________________________Note: TPH estimates of current market conditions.

Acreage values are after subtracting current production at $50,000 boe/d

Bakken Pure Play Public Companies…A Tale of the Tape

2011 Performance 2012 YTD Performance

232% Bakken 1% Marcellus

74%

92%

166%

High G th Oil

Transition

Permian

(4%)

(3%)

Focused Gas Growth

Oily

43%

58%

74%

Marcellus

GoM / Gulf Coast

High Growth Oil

(10%)

(8%)

(6%)

Small Cap Gas

GoM / Gulf Coast

High Growth Oil

(18%)

(13%)

36%

F d G G th

Diversified Gas Growth

Oily

(14%)

(13%)

Diversified Gas Growth

Permian

___________________________________Source: FactSet as of 7/2/2012.Bakken: OAS, KOG, NOG, TPLM and BEXP (until acquired by STO).

(49%)

(18%)

Small Cap Gas

Focused Gas Growth

(18%)

(16%)

Transition

Bakken

21

Transition: AREX, EOG, ROSE, SD and SM.High Growth Oil: CLR, CXO, DNR and OAS.Oily: BRY, CWEI, PXD, PXP, REN, VQ and WLL.GOM / Gulf Coast: ATPG, CPE, CXPO, EPL, EXXI, MCF, PQ, SFY, SGY and WTI.Focused Gas Growth: COG, GDP, KWK, RRC, SWN and UPL.Diversified Gas Growth: CHK, DVN, ECA, EOG, FST, NFX, QEP, XCO, and XEC. Small Cap Gas: BBG, CRK, GMXR, PETD and PVA. Permian: AREX, CWEI, CXO, LPI and PXD.Marcellus: GOG, RRC and EQT.

Permian Deal Metrics

22

Stacked Oil Plays Drive the PermianCurrent Permian Drilling ActivityCurrent Permian Drilling Activity

Horizontal RigVertical Rig

Midland B i

Bone Spring Delaware

Basin

Central Platform

Basin

Wolfberry

Delaware Sands

Wolfberry

Cline

Avalon Shale

Spraberry

Wolfcamp / Wolfbone

Wolfcamp (University)(University)

__________________________________Source: HPDI and RigData.

23

Permian M&A Deal Flow

2009 - 2012 YTD Deal Flow

DelawareConventional22%

Conventional25%

75% of deals in“resource” playsresource plays

Wolfberry53%

24_______________________________Source: IHS.

Industry Weighted Towards Oily Production

Gas (Boe/d)Oil (Boe/d) Gas (Boe/d) Well Count

Wolfcamp and Bone Spring Production

100,000

120,000

oe/d

)

10-Yr gas production up ~20%

3,500

4,200

100,000

120,000

oe/d

)

10-Yr oil production up ~153%

60,000

80,000

Dai

ly P

rodu

ctio

n (B

o

2,100

2,800

60,000

80,000

Well Count

Dai

ly P

rodu

ctio

n (B

o

20,000

40,000

D

700

1,400

20,000

40,000

D

0Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11

00Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11

25___________________________________Source: HPDI.Note: Includes all Texas producing wells with Wolfcamp, Bone Spring or Trend Area as a target reservoir; Excludes wells with field reported as Spraberry.

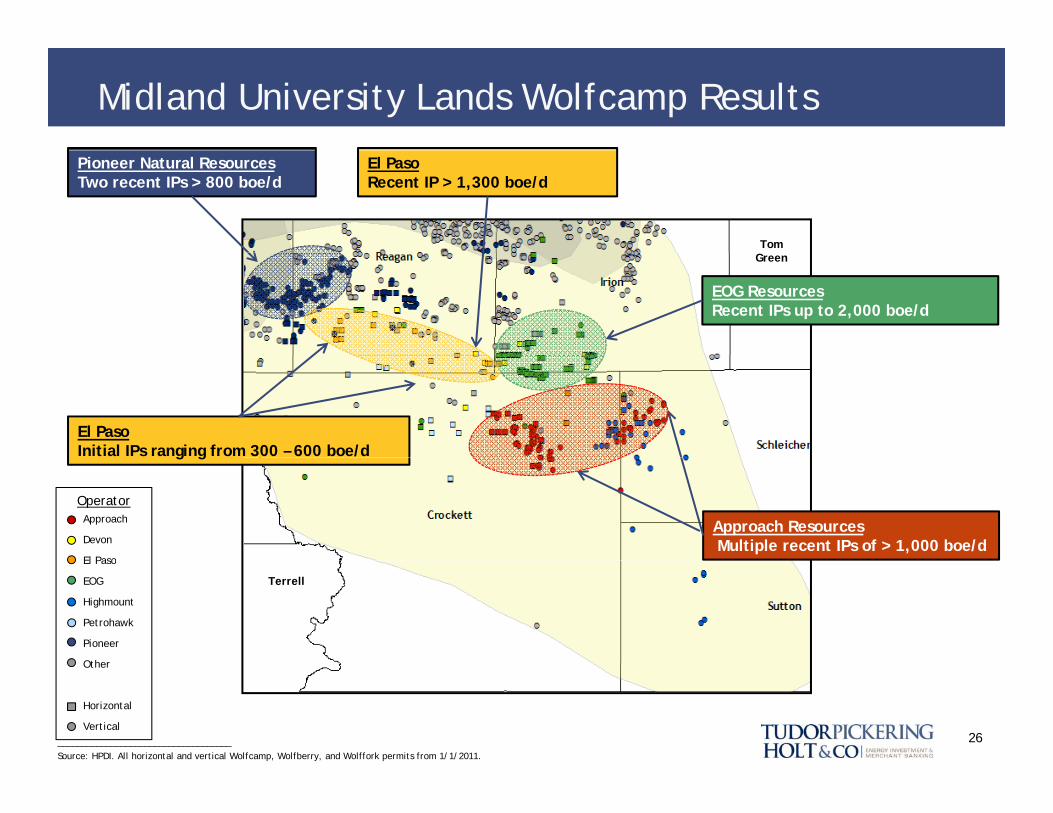

Midland University Lands Wolfcamp Results

Pioneer Natural ResourcesTwo recent IPs > 800 boe/d

El PasoRecent IP > 1,300 boe/d

Tom

EOG ResourcesRecent IPs up to 2,000 boe/d

Green

El PasoInitial IPs ranging from 300 – 600 boe/d

OperatorApproach

Devon

El Paso

Approach ResourcesMultiple recent IPs of > 1,000 boe/d

g g

El Paso

EOG

Highmount

Petrohawk

Pioneer

Other

Terrell

26____________________________________Source: HPDI. All horizontal and vertical Wolfcamp, Wolfberry, and Wolffork permits from 1/1/2011.

Other

Horizontal

Vertical

The Evolution of a Permian Play…Wolfberry 2009

Andrews CountryMax: $1,554/acreShaw Interest Inc

Concho / Terrace Petroleum11/23/2009$260 million

Shaw Interest, Inc.October 2009

Reagan CountyMax: $566/acreWindsor Permian, LLCApril 2009

Crane CountyMax: $207/acre April 2009

Upton CountyCrockett CountyMax: $301/acreWTG E l i

Max: $207/acreSan Luis EnergyOctober 2009

p yMax: $289/acrePioneer Nat. ResourcesOctober 2009

WTG ExplorationOctober 2009

Pioneer Southwest / PXD

M&A DealsLease Sales

d l

Pioneer Southwest / PXD8/31/2009$171 million

27

UT Lands 2009 Lease Sale157 Tracts Sold for average $287/acre

Highest bid $1,555/acre___________________________________Source: UT Lands, Company Investor Presentations and press releases.(1) $/acre estimate excludes PDP and does not correct for developed acres. PDP valued at $50,000/Boe/d.

The Evolution of a Permian Play…Wolfberry 2010

Andrews CountryMax: $3,587/acrePrivate Broker

Energen / Undisclosed8/23/2010$185 million; $18,678/acre(1)

Private BrokerSeptember 2010

Reagan CountyMax: $1,626/acreEl Paso E&PSeptember 2010

Crane CountyMax: $455/acre September 2010

Upton CountyCrockett CountyMax: $1,797/acreEl P E&P

Max: $455/acreSan Luis EnergySeptember 2010

p yMax: $1,610/acePrivate BrokerSeptember 2010

El Paso E&PSeptember 2010

Berry Petroleum / Undisclosed10/25/2012

Energen / Undisclosed8/23/2010

M&A DealsLease Sales

d l

10/25/2012$180 million; $12,903/acre(1) $75 million; $7,239/acre(1)

28

UT Lands 2010 Lease Sale510 Tracts Sold for average $985/acre

Highest bid $3,587/acre___________________________________Source: UT Lands, Company Investor Presentations and press releases.(1) $/acre estimate excludes PDP and does not correct for developed acres. PDP valued at $50,000/Boe/d.

The Evolution of a Permian Play…Wolfberry 2011Andrews CountryMax: $10,000/acrePDC EnergySeptember 2011

Berry Petroleum / Undisclosed4/28/2011$123 million; $16,333/acre(1)

Concho / PDC Energy12/23/2011$175 million; $11,765/acre(1) Laredo Petroleum / Broad Oak

6/16/2011$1.0 billion; $9,273/acre(1)

Reagan CountyMax: $5,580/aceConocoPhillipsSeptember 2011

Crane CountyMax: $511/acreSandRidge EnergySeptember 2011

p

Upton CountyMax: $5,580/aceConocoPhillipsSeptember 2011 Crockett County

Max: $5,580/aceC Philli

M&A DealsLease Sales

d l

ConocoPhillipsSeptember 2011

29___________________________________Source: UT Lands, Company Investor Presentations and press releases.(1) $/acre estimate excludes PDP and does not correct for developed acres. PDP valued at $50,000/Boe/d.

UT Lands 2011 Lease Sale496 Tracts Sold for average $2,245/acre

Highest bid $10,000/acre

The Evolution of a Permian Play…Wolfberry 2012

Andrews CountryMax: $3,000/acreWindsor PetroleumMarch 2012

Reagan CountyMax: $5,814/acePioneer Nat. ResourcesMarch 2012Crane County

Energen / Undisclosed2/10/2012$66 million; $20,563/acre(1)

March 2012

Crockett CountyMax: $2,507/aceP h k P i

Crane CountyMax: $525/acreHenry Energy LPMarch 2012

Upton CountyMax: $7,058/aceVeritas Energy PartnersMarch 2012

Petrohawk PropertiesMarch 2012

M&A DealsLease Sales

d h l

30

UT Lands March 2012 Lease Sale86 Tracts Sold for average $645/acre

Highest bid $7,123/acre___________________________________Source: UT Lands, Company Investor Presentations and press releases.(1) $/acre estimate excludes PDP and does not correct for developed acres. PDP valued at $50,000/Boe/d.

Wolfberry / Wolfcamp Acreage Now First In Class

$25,000

Lease Sales

$25,000

Lease Sales Highest Lease Sale Bid

$25,000

Lease Sales Highest Lease Sale Bid M&A Deals

$20,000$20,000

$20,563

$20,000

$15,000

erag

e $/

Acre

$10 000

$15,000

rage

$/A

cre

$10 000

$12,940$11,971

$15,000

erag

e $/

Acre

$5,000

$10,000Ave Average $/acre up ~10x since 2009

$3 587

$10,000

$7,123

$5,000

$10,000Ave

$3 587

$10,000

$7,123

$5,000

$10,000Ave

$287$985

$2,245

$645

$02009 2010 2011 2012

$287$985

$2,245

$645$1,555

$3,587

$02009 2010 2011 2012

$287$985

$2,245

$645$1,555

$3,587

$02009 2010 2011 2012

31___________________________________Source: Company Investor Presentations and press releases.Note: $/acre estimate excludes PDP and does not correct for developed acres. PDP valued at $50,000/Boe/d.

Avalon / Bone Spring Production Rapidly Increasing

1,50075,000

Oil (Boe/d) Gas (Boe/d) Well Count

1,20060,000

W (Boe

/d) First Avalon Shale Horizontal Producer

600

900

30,000

45,000

Well CountD

aily

Pro

duct

ion

30015,000

00Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11

32___________________________________Source: HPDI.

Recent Industry Results in the Delaware

Avalon ShaleDevon IP of 950 boe/d1st, 2nd, 3rd Bone Spring

Bone Spring (2nd/3rd)XEC: 7 recent wells IPs 560-1,100 boe/d

Hz Brushy/Cherry

Avalon ShaleCHK IP of 1,160 boe/d

Delaware SandsYates IPs of 794 - 1,067 boe/d

Avalon Shale (Loving)

Avalon Shale

Avalon ShaleCXO IP of 1,368 boe/d

3rd B S i (W d)

Avalon Shale (Loving)APC TC IP ~800 boe/d (60% liquids)

Wolfcamp

Avalon ShaleEOG IP of 1,474 boe/d

3rd Bone Spring (Ward)APC TC IP ~700 boe/d (85% liquids)

WolfboneCXO IPs of 200-450 boe/dCRK IPs of 150-300 boe/d

A d k C h EOG O

3rd Bone SpringCHK IP of 2,200 boe/d

33___________________________________Source: Company Investor Presentations, HPDI: Vertical Wolfbone and all horizontal permits since 7/1/2011.

Anadarko Concho EOG OxyChesapeake Devon Mewbourne WhitingCimarex Energen Clayton OtherComstock

Recent Notable Delaware Basin Transactions

June 2011 Land Auction$5,076 - $5,630/acreSeptember 2011 Land Auction$6,150/acre

August 2010 Land Auction$5,313/acre

August 2010 Land Auction$7,250/acre

$ ,

May 2010 Land Auction$3,957/acre July 2011 Land Auction

$6 000/acre$6,000/acre

April 2011 Land Auction$4,200/acre

Concho / Undisclosed: 11/2/2011$330 million; $2,237/acre(1)Comstock Resources / Eagle Oil & Gas:

12/5/2011$333 million: $5,970/acre(1)

Forest Oil Corp. / Undisclosed: 2/16/2012$103 million; $1 635/acre(1)

Clayton Williams$3,333/acreMarch 2012

M&A DealsLease Sales___________________________________Source: Company Investor Presentations and press releases.(1) $/acre estimate excludes PDP and does not correct for developed acres. PDP valued at $50,000/Boe/d.

34

$103 million; $1,635/acre( )

Conclusions

Metrics Should Increase With DrillingLittle to No Type Curve Being EstablishedType Curve Established

$18,000

$20,000

Little to No Horizontal Results

$18,000

$20,000

Type Curve Being EstablishedFocused Horizontal Results

$18,000

$20,000

Type Curve EstablishedWidespread Horizontal Results

$12 000

$14,000

$16,000

re)

$12 000

$14,000

$16,000

e) $12 000

$14,000

$16,000

e)

$8,000

$10,000

$12,000

Pric

e ($

/acr

$8,000

$10,000

$12,000

Pric

e ($

/acr

e

$8,000

$10,000

$12,000

Pric

e ($

/acr

e

$2 000

$4,000

$6,000

$2 000

$4,000

$6,000

$2 000

$4,000

$6,000

$0

$2,000

0.5 1.5 2.5 3.5 4.5 5.5 6.5$0

$2,000

0.5 1.5 2.5 3.5 4.5 5.5 6.5$0

$2,000

0.5 1.5 2.5 3.5 4.5 5.5 6.5

For

d ns

ate

kken

Uti

ca

ellu

s

mia

n ou

rce

brar

a

Lim

e

36_______________________________Source: IHS Herold and TPH research.

Eagl

e Co

nden Ba

U

Mar

c

Perm

Reso

Nio

b

Mis

s. L

Permian – Right Place at Right Time

Oil prices to remain strong

Liquids pricing strong enoughLiquids pricing strong enough

Oil deals increasing

Horizontal applicationsHorizontal applications

Vertical – accessing new pay

Scale running roomScale – running room

Multiple targets

O f b iOpen for business

37

Bakken Themes – Now and In The Future

Major Themes and Catalysts as the Bakken Continues to Evolve

1) Completion Technology 1) Continues to Advance1) Completion Technology

2) Well Performance

3) Infill Drilling/Spacing

1) Continues to Advance

2) IPs Define Sweet Spots

3) Denser Over Time with Pad Drilling

B kk V l ill 4) Three Forks

5) Deep Three Forks

4) Similar to Bakken and Contiguous

5) Emerging Value

Bakken Values will Rise

6) Drilling Costs

7) Western Rough Rider

6) Improve With Time

7) Core Extends West of the Nesson

38

Tudor, Pickering, Holt & Co. does not provide accounting, tax or legaladvice. In addition, we mutually agree that, subject to applicable law, you(and your employees, representatives and other agents) may disclose anyaspects of any potential transaction or structure described herein that are

Disclosure Statement

Tudor Pickering Holt & Co LLC is an integrated energy investment

p y pnecessary to support any U.S. federal income tax benefits, and all materialsof any kind (including tax opinions and other tax analyses) related to thosebenefits, with no limitations imposed by Tudor, Pickering, Holt & Co.

The information contained herein is confidential (except for informationrelating to United States tax issues) and may not be reproduced in whole orin part.

About The Firm

Tudor, Pickering, Holt & Co., LLC is an integrated energy investmentand merchant bank, providing high quality advice and services toinstitutional and corporate clients. Through the company’s two broker-dealer units, Tudor, Pickering, Holt & Co. Securities, Inc. (TPHCSI) andTudor, Pickering, Holt & Co. Advisors, LLC (TPHCA), the company offerssecurities and investment banking services to the energy community.TPH Asset Management, LLC (TPHAM) is an SEC registered investmentadviser that delivers a suite of energy investment strategies TPH

Tudor, Pickering, Holt & Co. assumes no responsibility for independentverification of third-party information and has relied on such informationbeing complete and accurate in all material respects. To the extent suchinformation includes estimates and forecasts of future financial performance(including estimates of potential cost savings and synergies) prepared by,reviewed or discussed with the managements of your company and/ or other

i l i i i b i d f bli hadviser that delivers a suite of energy investment strategies. TPHPartners Management, LLC is an SEC exempt reporting advisor. Certainemployees of TPHAM are also employees of TPHCSI.

The firm, headquartered in Houston, Texas, has approximately130 employees and offices in Denver, Colorado; and in New York, NewYork. Its affiliate, Tudor, Pickering Holt & Co. International, LLP, islocated in London, England.

potential transaction participants or obtained from public sources, we haveassumed that such estimates and forecasts have been reasonably preparedon bases reflecting the best currently available estimates and judgments ofsuch managements (or, with respect to estimates and forecasts obtainedfrom public sources, represent reasonable estimates). These materials weredesigned for use by specific persons familiar with the business and theaffairs of your company and Tudor, Pickering, Holt & Co. materials.

located in London, England.

Contact UsHouston (Research, Sales and Trading): 713-333-2960Houston (Investment Banking): 713-333-7100Denver (Sales): 303-300-1900Denver (Investment Banking): 303-300-1900New York (Research, Sales): 212-220-9254

Under no circumstances is this presentation to be used or considered as anoffer to sell or a solicitation of any offer to buy, any security. Prior tomaking any trade, you should discuss with your professional tax, accounting,or regulatory advisers how such particular trade(s) affect you. This briefstatement does not disclose all of the risks and other significant aspects ofentering into any particular transaction.

( , )London: +011 44(0) 20 3008 6428

www.TudorPickeringHolt.com

Tudor, Pickering, Holt & Co. International, LLP is authorized and regulatedby the Financial Services Authority and is the United Kingdom affiliate ofTudor, Pickering, Holt & Co., LLC.

39

Recommended