eR seR s

Bank CorporateGovernancein Azerbaijan

Bank CorporateGovernancein Azerbaijan

Survey ultsSurvey ultsy eSurve R sultsy eSurve R sults

2005

2005

00

25

00

25

40838

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Bank CorporateGovernance in Azerbaijan

Survey Results

Baku, Azerbaijan 2005

This report is available free of charge, in print or electronic form, at the following address:

International Finance CorporationAzerbaijan Corporate Governance Project21 Istiglaliyyat StreetThe Venetian Palace, Second Floor Baku AZ1001AzerbaijanTel: +994 12 497 7698Fax: +994 12 497 0891http://www.ifc.org/acgp

© 2006 International Finance CorporationAny or all portions of this report may be reproduced, without prior permission, provided the source is cited as follows: Azerbaijan Corporate Governance Project, International Finance Corporation, World Bank Group, 2121 Pennsylvania Ave., N.W., Washington, D.C. 20433, United States of America.

Table of ContentsTable of Contents

INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5INTERNATIONAL FINANCE CORPORATION AND CORPORATE GOVERNANCE . . . . . . . . . . . . . . . . . . . . . . 5

ABOUT THE INTERNATIONAL FINANCE CORPORATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5IFC'S FOCUS ON CORPORATE GOVERNANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5IFC AND AZERBAIJAN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

THE SURVEY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6OBJECTIVES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6METHODOLOGY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Questionnaire Design . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Selection of Survey Participants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

IMPLEMENTATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6EXECUTIVE SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

ORGANIZATIONAND OWNERSHIP OF BANKS IN AZERBAIAN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7AWARENESS OF AND COMMITMENT TO GOOD CORPORATE GOVERNANCE PRACTICES . . . . . . . . . . . . 8SUPERVISORY AND MANAGEMENT BOARD PRACTICES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8SHAREHOLDERS' RIGHTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9DISCLOSURE AND TRANSPARENCY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

ORGANIZATION AND OWNERSHIP OF BANKS IN AZERBAIJAN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11BANKS AND THEIR MAJOR OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

YEARS IN OPERATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

B a n k C o r p o r a t e G o v e r n a n c e i n

N D BRANCHES

N EMPLOYEES

N CUSTOMERS

MAIN OPERATIONS

LEGAL FORM

M RAISING CAPITAL

RECENT I CAPITAL REQUIREMENTS

S REGISTRATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15 SHAREHOLDERS

NUMBER

DESCRIPTION

STATE PARTICIPATION

A MAJOR SHAREHOLDERS

CORPORATE CHARTERS

B POLICIES

O IMPROVING CORPORATE GOVERNANCE

M IMPROVE CORPORATE GOVERNANCE

DIVISION OF RESPONSIBILITIES

N MEMBERS

F MEETINGS

P MEETINGS

PERFORMANCE EVALUATION

REMUNERATION

BOARD COMMITTEES

F DESCRIPTION

F MEETINGS

C SUPERVISORY BOARD

CONFLICTS OF INTEREST

SHAREHOLDERS' RIGHTS

NOTICE TIMELINESS, M INFORMATION PROVIDED

SHAREHOLDER ATTENDANCE

EXTRAORDINARY SHAREHOLDERS' MEETINGS

VOTING PROCEDURES

D RESULTS

DIVIDENDS

D SIGNIFICANT T RELATED PARTY TRANSACTIONS

S I POTENTIAL INVESTORS

FINANCIAL CONTROLS

AUDIT COMMITTEE

INTERNAL AUDIT

I INTERNAL AUDIT FUNCTION

EXTERNAL AUDIT

APPENDIX

A z e r b a i j a n

UMBER AND ISTRIBUTION OF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 UMBER OF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 UMBER OF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

ETHODS OF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 NCREASES IN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

HARES AND

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

FFILIATIONS OF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18 SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

AWARENESS OF AND COMMITMENT TO GOOD CORPORATE GOVERNANCE PRACTICES. . . . . . . . . . . . . . . . . . 19 COMPLIANCE WITH CORPORATE GOVERNANCE PRINCIPLES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19 CORPORATE DOCUMENTATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 YLAWS AND . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

IMPROVING CORPORATE GOVERNANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 BSTACLES TO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 EASURES TO . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

COMPLIANCE WITH THE NATIONAL BANK CORPORATE GOVERNANCE REGULATION . . . . . . . . . . . . . . 23 SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

SUPERVISORY AND MANAGEMENT BOARD PRACTICES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

SUPERVISORY BOARD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 UMBER OF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 REQUENCY OF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 REPARATION FOR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

MANAGEMENT BOARD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29 UNCTION AND . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29 REQUENCY OF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29 OMMUNICATION WITH THE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30 RELATED PARTY TRANSACTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30 SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31 AUTHORITY AND FUNCTIONS OF THE ANNUAL GENERAL MEETING . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31 PROCEDURES FOR SHAREHOLDERS' MEETINGS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

ETHOD AND . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

ISCLOSURE OF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 DISCLOSURE AND TRANSPARENCY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

COMPLIANCE WITH IFRS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37 MANDATORY DISCLOSURE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38 ANNUAL REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

ISCLOSURE OF RANSACTIONS AND . . . . . . . . . . . . . . . . . 39 OURCES OF NFORMATION FOR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

FINANCIAL CONTROL AND AUDIT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

NDEPENDENCE OF THE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

IntroductionIntroduction

INTERNATIONAL FINANCE CORPORATION AND CORPORATE GOVERNANCE

ABOUT THE INTERNATIONAL FINANCE CORPORATION

The International Finance Corporation (IFC) is the private sector arm of the World Bank Group. IFC's mission is to promote sustainable private sector investment in developing countries, thereby contributing to reducing poverty and improving the quality of life in these countries. IFC finances investments with its own resources and by mobilizing capital in the international financial markets. IFC also provides technical assistance and advice to governments and businesses. Since its foundation in 1956, IFC has invested nearly $40 billion of its own capital and has syndicated more than $20 billion in investment in some 2,800 companies in 140 countries.

IFC'S FOCUS ON CORPORATE GOVERNANCE

IFC is a leader among multilateral financial institutions in integrating corporate governance considerations into all phases of the investment process. IFC's long history of direct involvement in structuring investments, appraising investment opportunities and nominating board members has allowed it to put corporate governance principles into action. By focusing on good corporate governance practices in client companies, IFC can manage risk and add value to its clients. In addition to the benefits to individual client companies from IFC's work in improving corporate governance, these efforts contribute to IFC's broader mission to promote sustainable private sector investment and strengthen capital markets in developing countries.

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

IFC AND AZERBAIJAN

IFC approved its first loan in Azerbaijan in 1995. Since then, it has committed $465 million in financing to projects in Azerbaijan.

IFC's strategy in Azerbaijan is to help diversify the country's economic base and support growth and the creation of employment in nonoil sectors. IFC's areas of strategic focus inAzerbaijan include:

strengthening the financial sector by promoting domestic and foreign competition in the banking sector and by providing technical assistance to local private bankspromoting the development of micro, small and medium enterprises through lines of credit to local private banks and by providing technical assistancesupporting investment in the agricultural sector by targeting competitive agroprocessing ventures and identifying areas for potential IFC supportacting as a catalyst for foreign direct investment in competitive nonoil sectors, particularly those focusing on exports or on generating foreign income and those involving privatization of critical manufacturing activities or infrastructuresupporting increased private provision of public services such as health care and educationsupporting investment in the oil and gas sectors, including oil export pipelinespromoting a level playing field for domestic and foreign investorsbroadening opportunities to obtain financing for private enterprises outside the oil sector

IFC launched the Azerbaijan Corporate Governance Project (ACGP) on January 26, 2005 with funding from Switzerland's State Secretariat for Economic Affairs (SECO). The project staff works with companies and banks to improve their corporate governance practices, with the government ofAzerbaijan to improve the regulatory framework for corporate governance in the country and with educational institutions to ensure that future business leaders are introduced to corporate governance principles over the course of their education.

THE SURVEY

OBJECTIVES

The survey set out to analyze the current state of corporate governance practices in Azerbaijani banks and to determine the extent to which they implemented internationally recognized corporate governance best practices. The survey was also intended to provide baseline data against which the impact of ACGP's corporate training events, consultations and pilot programs on corporate governance practices can be measured, thus furnishing a basis for possible future technical assistance programs.

METHODOLOGY

Questionnaire Design

ACGP staff developed the questionnaire for the survey based on IFC's experience with corporate governance projects in Russia, Ukraine and Georgia.

The draft questionnaire was tested in five commercial banks in order to identify and correct deficiencies in the questions and the interview instructions. The questionnaire and survey methods were reviewed and revised based on these test results and on consultations with the interviewers.

Selection of Survey Participants

Except for one bank with headquarters in Ganja (the country's secondlargest city), all banks in Azerbaijan were headquartered in Baku (the capital) at the time of the survey. The banks surveyed were all located in Baku. Thirtyfour of the fortythree commercial banks operating in the country at the time of sampling (79.1%) were included in the survey.

IMPLEMENTATION

The questionnaire was administered in the course of an interview with each participant. The results herein are based on their responses, recorded as given and not verified using other sources of information. Consequently, this selfreported data may include inflated, adjusted, or otherwise biased information, given in order to avoid admitting to violations of the law or simply to portray the company and its practices in a favorable light.

The survey team began work in August 2005. A local research company, Sigma, conducted the interviews. The ACGPstaff trained the interviewers in corporate governance practices and principles. Interviews with company representatives began inAugust 2005 and theACGP team received the compiled data in November 2005.

66

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

INTRODUCTION

Executive SummaryExecutive Summary

This report is an analysis of the results of a survey of thirtyfourAzerbaijani commercial banks with respect to their corporate governance practices. The survey was based on a questionnaire and interview. The participating banks were all located in Baku, Azerbaijan. In a majority of cases, the survey respondents were either management board members or its chairperson 1

The key findings from the survey data are herein considered in the following broad categories:

organization and ownership

awareness of and commitment to corporate governance practices

supervisory and management board practices

shareholders' rights

disclosure and transparency practices

ORGANIZATIONAND OWNERSHIP OF BANKS IN AZERBAIJAN

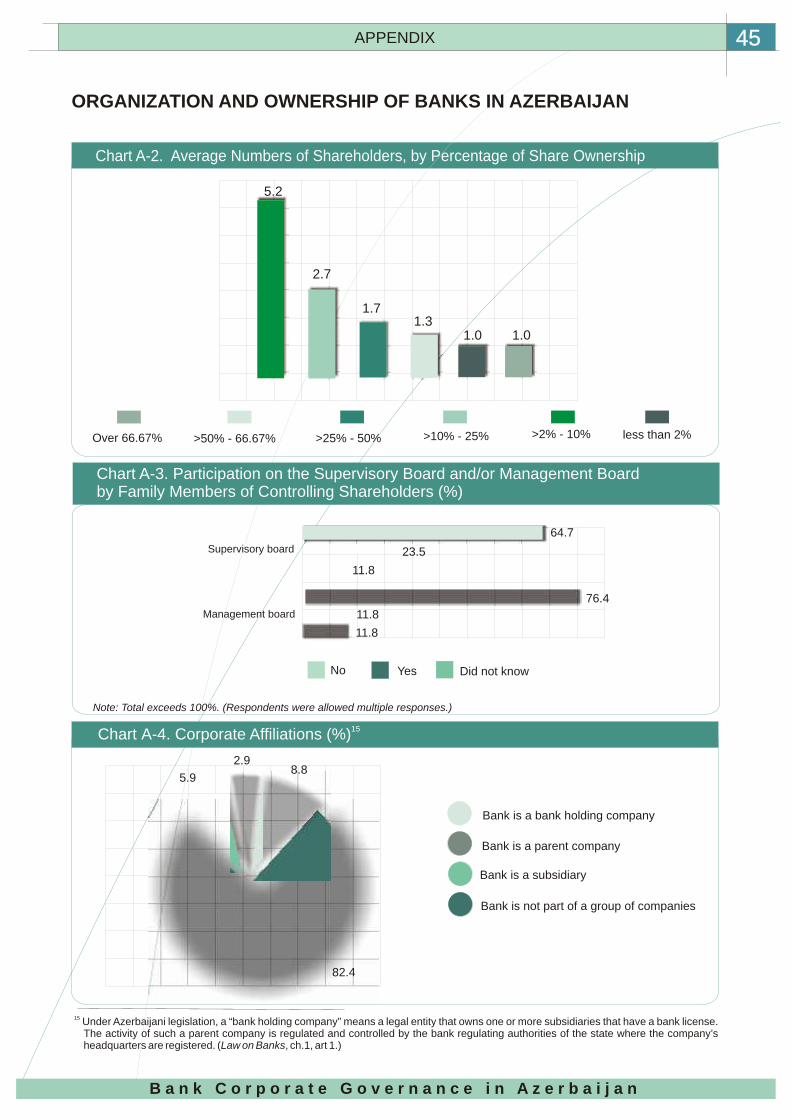

By law, all banks must be registered as open joint stock companies; however, four respondents (11.8%) reported that their banks were in violation of this fundamental requirement.

Only three of the banks surveyed (8.8%) were owned by a holding company or a group of companies.

See Chart A1 “Respondent's Position” in the Appendix.

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

1

88 EXECUTIVE SUMMARY

Only six of the thirty respondents who answered the question (20.0%) reported that their banks issued preferred shares.

Only one of the banks surveyed was state-owned, with the government owning 50.2% of the shares.

Ownership in most banks in Azerbaijan was concentrated and most had only a small number of shareholders. In over onethird of the banks surveyed, an individual shareholder had a controlling interest. In addition, quite often (in 40.6% of the banks surveyed) relatives of major shareholders were likewise major shareholders.

Major shareholders were often involved in the management of banks as members of either the supervisory board or the management board. In 41.2% of the banks surveyed, the largest shareholder was a member (quite often, the chairperson) of the supervisory board. The management board included one of the three largest shareholders in 17.6% of the banks surveyed. That figure would have been even higher but for the law prohibiting a shareholder who owns 20% or more from being a member of the management board.

The banking sector was experiencing general growth and development and the National Bank of Azerbaijan had recently increased the capital requirements for banks. As a result, Azerbaijani banks were seeking, and planned to continue to seek, infusions of capital. Of the banks surveyed, 91.2% had attracted investment over the previous five years and 97.1% planned to seek more capital in the next three years.

Of the banks surveyed, 73.5% were listed on the Baku Stock Exchange. However, public offerings were not the banks' preferred method of raising capital. Rather, 60.6% of respondents said that they preferred to seek capital from international financial institutions.

AWARENESS OF AND COMMITMENT TO GOOD CORPORATE GOVERNANCE PRACTICES

Of the thirtyfour respondents, thirty (88.0%) stated that they understood corporate governance principles. However, in the course of conducting seminars and other training events, the ACGP observed that few bank managers were actually knowledgeable in corporate governance best practices. It seems likely, therefore, that some respondents did not wish to admit their lack of knowledge in this area.

Most respondents rated the level of compliance with corporate governance best practices in their own banks as better than that of the banking sector generally and better than that of corporate governance legislation. In the course of the survey, 38.3% of respondents rated their own corporate governance at the maximum level, while only 11.8% assessed corporate governance in the banking sector at that level and only 14.7% rated corporate governance legislation at the maximum best practices level.

Respondents seemed to perceive the benefits of corporate governance in terms of operational efficiencies rather than as protections for shareholders and other stakeholders. For example, only one (2.9%) said that disclosure was an important benefit of good corporate governance.

Respondents placed little value on integrating corporate governance principles beyond the legally required minimum. Most banks had adopted new charter provisions to comply with recent legislative changes, but only a handful of respondents stated that their banks had gone beyond the legislative requirements to include further provisions dealing with fundamental corporate governance issues. For example, only 14.7% indicated that provisions regarding independent directors were included in the bank's charter.

According to respondents, the three major obstacles to improving corporate governance practices were ineffective legislation (cited by 61.8%), the scarcity of specialists competent in the field (41.2%) and the general lack of awareness of the subject (26.5%).

Encouragingly, fifteen of the respondents (44.1%) reported that they were seeking to improve corporate governance in their banks and had documented improvement plans. In order of the frequency of responses, their corporate governance improvement priorities were to establish supervisory board committees, train board members and implement the International Financial Reporting Standards (IFRS).

Another indication that banks were seeking to improve their corporate governance was that fourteen (41.2%) of the banks surveyed had hired consultants specializing in corporate governance training. (Local firms provided this service in all but one instance.) Nearly all respondents (94.1%) indicated that they were interested in receiving training in corporate governance.

SUPERVISORYAND MANAGEMENT BOARD PRACTICES

The responses to questions regarding the duties of the supervisory board indicated that, instead of

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

99EXECUTIVE SUMMARY

exercising oversight, the supervisory board (not the management board) was managing the daytoday operations of the bank.

In 67.6% of the banks surveyed, the supervisory board consisted of the legally mandated minimum of three members. The rest had fivemember boards.

Most of the banks surveyed held the legally required minimum of four supervisory board meetings per year. Only two banks (5.9%) held these meetings two or three times a year. However, the survey indicated that banks should improve their pre and postmeeting practices. Although all but 8.8% of respondents indicated that they had established procedures for providing materials to members prior to the meetings, only half reported that they included minutes of the last meeting.

Effectively, there was no evaluation of supervisory board performance. Only eight banks (23.5%) had carried out a board assessment within the last two years.

Development of remuneration systems for supervisory boards is needed. Of the banks surveyed, 52.9% did not remunerate supervisory board members at all and 41.1% based remuneration solely on net profit without regard to other factors such as responsibilities, meeting attendance, or the bank's growth.

The management board consisted of five members in 44.1% of the banks surveyed, three members in 35.4%, seven in 14.7%, four in one of the banks (2.9%) and nine in one other (2.9%).

Potential conflicts of interest are a serious concern given that 44.1% of the banks surveyed had no bylaws requiring conflict disclosure or approval of related party transactions.

SHAREHOLDERS' RIGHTS

All of the respondents said that they complied with the legal requirement to hold an annual general meeting of shareholders (AGM) in 2004. However, less than half (44.1%) said that they had complied with the requirement to notify shareholders of the meeting at least fortyfive days in advance.

Among those who gave notice of the AGM and provided premeeting materials, 94.1% included an agenda, 41.1% included a description of each agenda item, 44.1% enclosed the annual report and financial statements and 32.4% provided supporting documents related to the agenda. Notably, only 17.6% included proxy voting instructions.

Significantly, 55.9% of respondents indicated that changes to the agenda were permitted during the AGM, even though this practice contravenes both good corporate governance practice and related legislation.

Although not prohibited by law and arguably permissible, cumulative voting is not common in Azerbaijan. Only 20.6% of the banks surveyed elected the supervisory board through cumulative voting.

In general, AGMs were well attended. In roughly threequarters of the banks surveyed, at least 85.0% of the shareholders attended the most recent AGM. Also, a little over half of the banks surveyed indicated that at least 66.7% of the minority shareholders attended. Although attendance was high, shareholders did not necessarily have adequate opportunity to exercise their rights: 91.2% of the banks surveyed indicated that voting took place by a show of hands and only 35.3% accepted votes by proxy.

The results of AGMs were most commonly communicated verbally; for 64.7% of the respondents it was the main method of disclosure, followed by regular mail (14.7%) and registered mail (5.9%). A further 14.7% reported that they either communicated this information in another manner or did not know how the results were communicated. Roughly a quarter of the banks surveyed (26.5%) did not make AGM results available to the public.

A significant number of respondents (32.4%) refused to answer questions on the payment of dividends. Sixteen of the twentythree (69.6%) who did answer said that they had not paid dividends for the years 2002 to 2004. Only seven said that they had declared dividends in any of those years and only four had declared dividends in all three years.

Twenty of the banks surveyed (58.8%) had held extraordinary shareholders' meetings in the last two years. Most often, the purpose was to seek approval to amend the charter.

DISCLOSUREAND TRANSPARENCY

2 3The Law of the Republic of Azerbaijan on Accounting and the Law of the Republic of Azerbaijan on Banksrequire banks to prepare financial reports in accordance with IFRS. The passage of these laws signified a

2 June 2004. Hereinafter, the “Accounting Law”. Note that the effective date of this legislation was November 2004.

3 January 2004. Hereinafter, the “Law on Banks”. Note that the effective date of this legislation was March 2004.

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

4 November 2004. Hereinafter, the “National Bank Corporate Governance Regulation”.

1010 EXECUTIVE SUMMARY

step toward improving disclosure and transparency in the banking sector. However, even though all banks surveyed were said to comply with IFRS, the survey revealed that improvement is needed in this area.

In addition to financial disclosure, stricter legislative provisions regarding nonfinancial disclosure now apply to banks, and practice is improving in this regard. For example, 88.2% of respondents said that their annual reports were made public. This is a promising trend, but the content needs improvement. Only 5.9% disclosed the names of beneficial shareholders and provided profiles of the members of the governing bodies of the bank, and only 2.9% disclosed the shareholdings of those individuals.

Most respondents (91.2%) claimed that they disclosed financial information upon request and 82.4% said that most information was disclosed in the annual report. In practice, however, a significant number regularly failed to meet even the minimum disclosure standards set by law.

Disclosure of significant transactions was not common practice. Only 35.3% of the banks surveyed disclosed both related party transactions and transactions in excess of 10% of the book value of the bank's assets. A further 8.8% disclosed related party transactions only and 5.9% disclosed significant transactions only, but 47.1% did not disclose any of this information.

Supervisory board committees play an important role in corporate governance best practices. In particular, a supervisory board audit committee is critical to an effective internal control system. In general, most of the banks surveyed met the minimum legal requirements and complied with best practices regarding the formation of their audit committees. Most banks (91.2%) had an audit committee and the same percentage had an internal audit function. Staffing a competent audit committee is a challenge in Azerbaijan, but 67.6% complied with the minimum legal requirement that the audit committee consist of at least three members.

In most of the banks surveyed (76.5%), the audit committee met at least quarterly. Roughly a quarter (23.5%) indicated that the committee met less frequently, which not only fails to meet best practices standards, but is

4also in violation of the Regulation on Implementing Corporate Governance Standards in Banks.

Banking legislation requires independence in the audit function. The survey responses suggest that audit committees were not truly independent and that internal audit departments were not operating independently of management. For example, in eight of the banks surveyed (23.5%), most members of the audit committee were bank employees. The majority of the audit committee members were independent in only nineteen of the banks (55.9%).

Seventeen respondents (50.0%) reported that most members of the audit committee were knowledgeable in finance, as in international best practices, and fourteen (41.2%) reported that at least one member of the audit committee was a finance and/or accounting specialist.

Over half of respondents (58.8%) said that their internal audit functions had established an effective audit program. However, only 38.2% indicated that the internal audit function included periodic assessment of the bank's internal control systems and only 26.5% said that regular and extraordinary internal audits of the bank were carried out.

Only 29.0% of the banks surveyed reported that the internal audit function appropriately reported to the audit committee as required by legislation and in accordance with best practices. Annual external audits were performed in all of the banks surveyed. In 79.4%, these services were performed by an international firm rather than a local audit company. Changing auditors was common, and 47.1% of the banks surveyed (sixteen banks) had changed their external auditor during the last three years.

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

O gan onr izatian O s ip ofd wner h

Ba s A er jank in z bai n

O gan onr izatian O s ip ofd wner h

Ba s A er jank in z bai n

To understand the status of corporate governance in the Azerbaijani banking sector, some general information about the sector is necessary.Azerbaijan had only fortyfour licensed banks as of January 1, 2006. Of these, fortyone were privately owned and two were owned by the state.

According to the National Bank of Azerbaijan, as of January 1, 2006 the total assets of Azerbaijani banks were approximately USD $2,451.5 million. Loans, not including loss provisions, totalled approximately USD $1,566.3 million. Total deposits were approximately USD $1,400.0 million. Total capital was approximately USD $401.74 million.5

The banking sector is in development and there has been rapid growth. For example, from December 31, 2004 to December 31, 2005, total assets increased by 35.1%. Corporate governance practices are likewise in a state of development. Since appropriate good governance measures are dependent on operating circumstances, the following overview of the banks surveyed will provide context for the information gathered about their corporate governance practices.

National Bank of Azerbaijan, Bulletin of Banking Statistics (Dec. 2005), available at www.nba.az.

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

5

1989-1994

1995-2000

2001-2004

76.5

17.6

5.9

Chart 1. Formation of Banks Surveyed (%)

BANKSAND THEIR MAJOR OPERATIONS

YEARS IN OPERATION

In the first six years following independence (1989 to 1994), as Azerbaijan made the initial transition to a market economy, more than 200 banks were established. Twentysix (76.5%) of the banks surveyed were created during this period. Six (17.6%) were established between 1995 and 2000 and two (5.9%) were created between 2001 and 2004.

NUMBER AND DISTRIBUTION OF BRANCHES

At the time of the survey, there were 360 bank branches in the country (an average of 8.3 branches per bank), of which 280 (78.0%) were branches of the banks surveyed. The International Bank of Azerbaijan (IBA) and Tekhnikabank had thirtyfive and twentyfive branches respectively. Three of the banks surveyed had no branches at all. The rest had an average of 7.6 branches. Branches were not spread geographically; 60.0% of them were located in Baku and 11.8% of the banks surveyed did not have branches outside Baku at all. Excluding IBA, the banks surveyed each had an average of 4.6 branches in Baku and 2.8 branches in other areas.

NUMBER OF EMPLOYEES

The banks surveyed varied considerably in size of staff. About a quarter of them (eight banks) had fewer than fifty employees. The largest portion (35.3%) was in the medium range, with 51 to 150 employees. Ten banks (29.4%) were quite large financial institutions, with staff of 151 to 250. Only three banks (8.8%) had more than 250 employees.

1212 ORGANIZATION AND OWNERSHIP OF BANKS IN AZERBAIJAN

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

1313ORGANIZATION AND OWNERSHIP OF BANKS IN AZERBAIJAN

NUMBER OF CUSTOMERS

Of the banks surveyed, 17.7% had fewer than 1,000 customers, 35.3% had between 1,001 and 10,000, and 14.7% had between 10,001 and 50,000. IBAhad more than 250,000 customers.

Up to 1,000

50,001-250,000

Over 250,000

1,001-10,000

10,001-50,000

Did not know

Chart 2. Number of Customers (%)

17.7

35.314.7

2.9

2.9

26.5

MAIN OPERATIONS

Chart 3 shows the current distribution of banking services, based on profit from the given activity as a portion of the total income of the bank, assessed by respondents on a scale of one to ten with ten being the most important. The chart also shows the distribution of those services based on the banks' strategic plans and national economic development priorities.

Servicing corporate accounts

Corporate lending

Deposits

Retail banking

Retail/consumer lending

Cash services including credit cards

Trade finance

Housing (mortgage loans)

Investment

75.0

72.0

73.0

56.0

49.0

33.0

41.0

46.0

55.0

46.0

41.0

41.0

29.0

39.0

58.0

64.0

64.0

68.0

Chart 3. Current Main Operations and Strategic Growth Priorities (%)

Current operations Strategic growth priorities

Note: Total exceeds 100%. (Respondents were allowed multiple responses.)

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

LEGAL FORM

Under the Law on Banks, banks can be registered only as open joint stock companies. Though this legislation had been in force for over a year at the time of the survey, four of the banks surveyed (11.8%) were still operating as closed joint stock companies. Thirty respondents (88.2%), including the representatives of two banks currently operating as closed joint stock companies, believed that the open joint stock company form was best for banks in terms of legal status, regardless of the legal requirement or the number of shareholders and other ownership factors. It is likely, therefore, that banks not already so registered will soon reregister as open joint stock companies.

Most of the banks surveyed (82.4%) were not owned by other companies, three (8.8%) were owned by holding companies, one (2.9%) was a subsidiary and two (5.9%) had subsidiaries of their own.

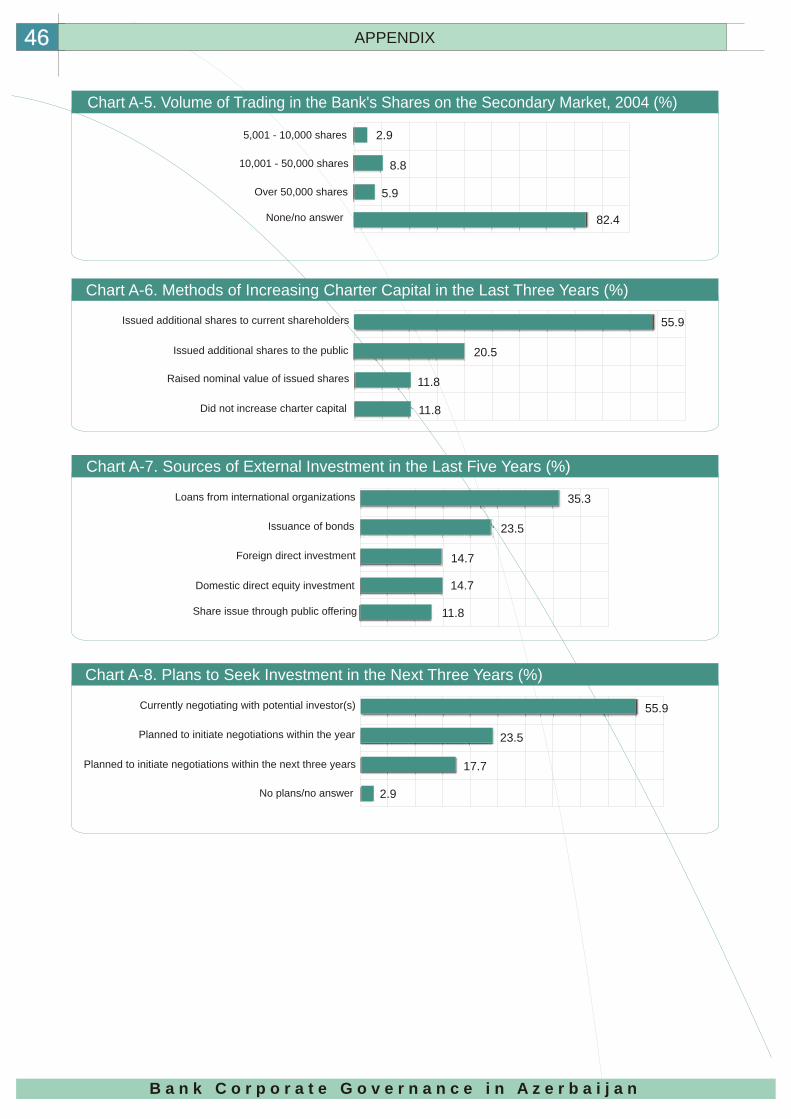

METHODS OF RAISING CAPITAL

Thirtythree respondents (97.1%) indicated that they planned to raise new capital in the next three years. Of those, most (70.6%) stated a preference for equity investment, with 42.4% seeking foreign direct investment and 39.4% looking for local direct investment. With the nascent bond market inAzerbaijan gaining ground, onethird of the banks surveyed reported that they envisaged a bond issue within the next three years. Of the banks surveyed, 60.6% had plans to seek funds from international organizations. The least popular method of raising capital was through a public offering on the Baku Stock Exchange (24.2%).

Ten respondents were unwilling to issue shares of any kind to raise funds. Six of them said they were reluctant to change the bank's ownership structure, three cited the high cost of issuing shares versus borrowing from IFIs and one believed that shares would not be attractive to investors.

Nineteen respondents (55.9%) were negotiating with potential investors. A further eight (23.5%) planned to identify investors later in the year and six (17.6%) planned to find investors within three years. Only one bank had not made plans to seek investors.

Most of the banks surveyed (73.5%) were listed on the Baku Stock Exchange. Of the rest, one had plans to become listed within three years. The rest were either not going to be listed or had no decision in place yet. None of the banks was listed on any other stock exchange, but two had plans to undertake a listing on a foreign stock exchange.

Although most banks' shares were traded on the Baku Stock Exchange, trading was rather thin. In 2004, total bank shares issued and placed was $21.0 million. In fact, 47.1% of respondents noted that their shares did not circulate on the secondary market in 2004 and 35.3% did not know one way or the other. In 2005, new bank shares on the market increased, with $65.0 million in shares issued and $54.0 million in shares placed, but trading

6volume on the secondary market was only $4.0 million. This activity involved only a few banks and represented7just 1.4% of the total nominal value of all bank shares as of January 1, 2006.

During the last three years, 17.6% of the banks surveyed repurchased shares from shareholders. Notably, most (66.7%) repurchased the shares at a nominal price rather than at fair market value. The remainder did not give the repurchase price.

6 Note that this number reflects the volume of trading on the secondary market of the Exchange and does not represent the actual volume of trading on the overall secondary market. Correspondence from the Baku Stock Exchange, Sept. 4, 2006 (on file with author).

7 According to the National Bank of Azerbaijan, the total paidin capital of all banks in Azerbaijan was $233.3 million as of January 1, 2005 and $288.0 million as of January 1, 2006. National Bank ofAzerbaijan, Bulletin of Banking Statistics (Jan. 2006), available at www.nba.az.

1414 ORGANIZATION AND OWNERSHIP OF BANKS IN AZERBAIJAN

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

1515

RECENT INCREASES IN CAPITAL REQUIREMENTS

8Owing to the increased minimum capital requirements set by the National Bank of Azerbaijan, and general development and growth in the banking industry, all but two of the banks surveyed increased their charter capital during the last three years. Their means of doing so included issuing additional shares to existing shareholders (55.8%), raising the nominal price of shares in circulation (11.8%) and new public offerings (20.6%).

Shares issued to existing shareholders

New public offering

Increased nominal value of issued shares

Did not increase capital

20.6

55.8

11.8

11.8

Chart 4. Means of Meeting Increased Minimum Capital Requirements (%)

Within the last five years, thirtytwo of the banks surveyed (94.1%) attracted external investment. Of these, five banks (15.6%) sold shares to local investors, five (15.6%) sold shares to foreign investors, two (6.3%) offered shares on the stock market, eight (25.0%) issued bonds and eleven (34.4%) obtained a line of credit from an international financial institution.

Chart 5. Sources of Financing (%)

Foreign direct equity investments

Bond issue

Loan from an international organization

Domestic direct equity investments

Public offering

Other

15.6

15.6

6.3

25.0

34.4

3.1

SHARES AND REGISTRATION

The banks surveyed mainly issued common shares. Thirty banks provided complete information on this matter and among those, common shares constituted 96.5% of the nominal value of all shares issued. Only six of those banks (20.0%) issued preferred shares, at an average of 14.0% of total shares. The highest portion reported was 27.0%. The ceiling prescribed by law is 25%.

Most of the banks surveyed (76.5%) registered their securities with an independent registration bureau, in most cases the National Depositary Center of the Republic of Azerbaijan. Only one used another external registry. One bank did not provide any information and 20.6% said that the security register was maintained by the bank itself.

As of January 1, 2004, the minimum capital requirement set by the National Bank was USD $2.5 million. As of January 1, 2005, it was $3.5 million and as of January 1, 2006, it was $5 million. Effective January 1, 2006, the minimum capital requirement for new banks becameAZN 10 million (approximately USD $11 million) and existing banks must meet this capital requirement on or before July 1, 2007. National Bank of Azerbaijan Board Decree No. 18 (Jun. 30, 2005) and National Bank ofAzerbaijan Board Decree No. 38 (Dec. 29, 2005).

ORGANIZATION AND OWNERSHIP OF BANKS IN AZERBAIJAN

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

8

SHAREHOLDERS

NUMBER

The average number of shareholders in the banks surveyed was small. Most commonly, shares were concentrated in a few individual shareholders, and 55.9% had between four and ten shareholders. Five banks (14.7%) had only three shareholders, and three (8.8%) had over fifty shareholders, including one with 832 and another with 1,425.

3

4 to 10

11 to 50

Over 50

20.6

8.8 14.7

55.9

Chart 6. Number of Shareholders (%)

DESCRIPTION

Foreign investors held 15.0% of the common shares of the banks surveyed. Azerbaijani legal entities and individuals owned 85.0%. Of the Azerbaijani portion, the government accounted for 1.5%. This mainly consisted of the government's share in the charter capital of the IBA. The IBA's charter capital was several times greater than the average charter capital of the other banks surveyed and the government owned 50.2% of its shares. The IBA was the only bank with direct government investment (via the Ministry of Finance) in its charter capital. Stateowned entities had some minimal investment (an average of 1.6%) in the charter capital of five of the banks surveyed (14.7%). The highest level of investment by a stateowned nonbanking institution in one private bank was 46.0%.

Supervisory board members

Azerbaijani individuals except supervisory and management board members

Foreign entities/individuals except supervisory and management board members

Azerbaijani private entities

Management board members

State-owned entities

Government (direct)

Other

32.0

30.0

15.0

15.0

4.0

1.5

1.5

1.0

Chart 7. Description of Shareholders (%)

1616 ORGANIZATION AND OWNERSHIP OF BANKS IN AZERBAIJAN

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

1717

The survey showed that ownership of banks was highly concentrated. Often, one or two shareholders had a controlling interest. In 20.6% of the banks surveyed, one shareholder held over twothirds of the shares. In 14.7%, one shareholder held between onehalf and twothirds of the bank's shares. Thus, in more than onethird of the banks surveyed, one individual had a controlling interest. Although 41.2% of the banks surveyed had shareholders who individually owned less than 2% of the shares, their collective participation in the paidin capital was very small. Excluding two banks with a large number of minority shareholders, banks that had shareholders holding less than 2% had an average of 11.9 of them. The average number of shareholders was 4.4 for all banks surveyed (again excluding the two banks with a large number of minority shareholders).

Ownership was further narrowed through family relationships: 38.3% of the banks surveyed had major shareholders who were related to other shareholders in the same bank. On the other hand, only 2.9% had shareholders whose business associates in other activities also owned shares in the same bank. More than half (52.9%) reported that their shareholders did not have family or business relationships with other shareholders in the same bank.

As shown in Chart 9, in 41.2% of cases the bank's largest shareholder was a supervisory board member (usually the chairperson). In 14.7% and 20.6% of cases respectively, a supervisory board member was the second or thirdlargest shareholder. It should be noted that there was overlap in these figures: in some banks, all three of the largest shareholders were supervisory board members. In four of the banks, the two largest shareholders were on the supervisory board. Over all, about 33.0% of shareholders (holders of common shares) were members of the supervisory board and 4.0% were members of the management board, indicating that shareholders were deeply involved in the daytoday management of banks.

STATE PARTICIPATION

The government or a stateowned enterprise was the largest shareholder in only two of the banks surveyed. As mentioned, the government owned 50.2% of IBA.Astateowned credit institution owned 46.0% of another private bank. Notably, more of the local large shareholders were individuals (61.7%) rather than legal entities (26.5%).

ORGANIZATION AND OWNERSHIP OF BANKS IN AZERBAIJAN

Business associates were also shareholders

Relatives were also shareholders

No answer/did not know

No family/business relationship with other shareholders52.9

2.9

38.3

5.9

Chart 8. Affiliations of Shareholders (%)

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

Supervisory board members

Management board members

State-owned entities

Foreign entities/individuals except supervisory and management board members

Azerbaijani private entities

Azerbaijani individuals except supervisory and management boards members

Other/N/A

41.2

14.7

2.9

2.9

2.9

2.9

0.0

20.6

23.5

35.4

11.8

11.8

14.7

14.7

14.7

17.7

20.6

23.5

8.8

8.8

5.9

First major shareholder Second major shareholder Third major shareholder

9Chart 9. Major Shareholders (%)

In 17.6% of the banks surveyed (27.0% of those that provided complete information on this matter), a management board member was one of the three largest shareholders. This figure would likely have been higher if not for the legal provision that an owner of over 20% of the shares of a bank may not be a member of the bank's management board.

AFFILIATIONS OF MAJOR SHAREHOLDERS

The survey found that, frequently, members of a bank's supervisory board were relatives of the bank's controlling shareholder. Taking into account that, as mentioned, the largest shareholder was often also on the board, many supervisory boards can be considered controlled by one major shareholder.

SUMMARY

In recent years, there has been dramatic expansion and development in Azerbaijan's banking sector. In the year 2005 alone, total bank assets increased by 35.1%, loans increased by 48.9% and deposits increased by 34.1%.

Corporate governance practices in banks were likewise in a state of development. With very few exceptions, the ownership of most banks was highly concentrated. Often, the major shareholders were involved in the management of the bank as members of the supervisory board or in management. As a result, existing corporate governance practices resembled the practices of closely held corporations.Any impetus to modify those practices came mostly from recent legislative change initiated by the National Bank ofAzerbaijan.

Many banks were seeking investment from international financial institutions as the preferred source of capital. The need for increased capital arose from regulatory requirements and from growth. In order to attract external investment, however, banks will have to improve their corporate governance practices.

1818 ORGANIZATION AND OWNERSHIP OF BANKS IN AZERBAIJAN

9 “Major shareholders” means the shareholders who individually hold the three largest percentages of the bank's shares.

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

Note: Total exceeds 100%. (Respondents were allowed multiple responses.)

IFC focuses on good corporate governance practices in order to add value to client companies and manage risk. Investors look to good corporate governance practices as a key indicator of shareholder value and effective stewardship. As mentioned, most of the banks surveyed (97.1%) were planning to raise capital from external

Awareness of and Commitment to

Good Corporate Governance Practices

Awareness ofand Commitment to

Good CorporateGovernance Practices

sources. Adherence to corporate governance principles will be a key factor in their ability to attract investors. Of the banks surveyed, 85.3% indicated that they were knowledgeable in corporate governance principles, specifically the Organisation for Economic Cooperation and Development Principles of Corporate Governance (2004) (hereinafter, the “OECD Principles of Corporate Governance”).

COMPLIANCE WITH CORPORATE GOVERNANCE PRINCIPLES

In addition to gauging awareness of good corporate governance practices in the banking sector, the survey sought respondents' views on the level of compliance with corporate governance best practices in their own banks, in the country's banking industry and in corporate governance legislation. Their responses varied depending on the body assessed: 38.2% of respondents (thirteen banks) scored corporate governance practices in their own banks at the maximum level (four or five points on a fivepoint scale), while only 11.8% (four banks) rated the banking sector in general at the maximum level and only 14.7% (five banks) assessed corporate governance legislation at the maximum level of compliance with best practices.

Only 20.6% of respondents scored compliance with corporate governance practices in their banks at a minimal level (one or two points), but 47.1% assessed compliance in the banking sector in general as minimal and 47.1% assessed compliance with best practices inAzerbaijan's corporate governance legislation as minimal.

The survey responses notwithstanding, based on observations in the course of providing technical assistance, the ACGP believes that the number of respondents who actually understood corporate governance was much lower than their selfassessment indicated.

The survey also asked respondents to indicate the most important benefits of good corporate governance. The top

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

Improved decision-making process

Increased operational efficiency

Improved reputation

Increased transparency of supervisory board and/or management board

Mitigation of risk (takeover, blackmail by shareholders, unfair use of information by competitors)

Better access to capital markets in Azerbaijan and abroad

Protection of shareholders’ rights

Prevention/resolution of internal conflict

Protection of stakeholders’ rights

Enhanced ability to attract investment

Improved efficiency of coordination between shareholders and management board

Improved disclosure

55.9

41.2

35.3

32.4

23.5

20.6

17.6

17.6

17.6

17.6

11.8

2.9

Chart 10. Perceived Benefits of Good Corporate Governance (%)

Note: Total exceeds 100%. (Respondents were allowed multiple responses.)

CORPORATE DOCUMENTATION

CORPORATE CHARTERS

In general, the survey indicated that the governing documents of banks needed improvement. For example, only 14.7% of banks included in their charters a provision regarding the appointment of independent directors. The charters of only 23.5% had provisions on the treatment of minority shareholders in the event of a takeover or merger. Even though both the law and good corporate governance practice preclude any restriction on the transfer of shares, almost a quarter of the banks surveyed (23.5%) included such restrictions in their charters.

Defining authority/responsibilityof management board and its head

Procedures for annual general meetings

General principles of shareholders rights

Procedure for establishing supervisory board committees

Qualifications required for supervisory board members

Treatment of minority shareholders in the event of a takeover

Prohibition/restrictions on sale of shares

Requirements/criteria for independent directors

Requirements for rotation of external auditor

82.4

79.4

73.5

50.0

44.1

23.5

23.5

14.7

8.8

Chart 11. Charter Provisions in Place (%)

Note: Total exceeds 100%. (Respondents were allowed multiple responses.)

2020

three responses were improving the bank's decisionmaking process, increasing the bank's operational efficiency and improving the bank's reputation. Chart 10 shows all responses.

Fundamental governance principles such as shareholders' or stakeholders' rights and disclosure were seen as benefits much less frequently than factors such as increased operational efficiency and an improved decisionmaking process. Only one respondent indicated that improved disclosure was an important benefit of improving corporate governance.

AWARENESS OF AND COMMITMENT TO GOOD CORPORATE GOVERNANCE PRACTICES

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

2121

Some notable provisions were commonly included in the banks' charters. For example, 82.4% of respondents indicated that their charters included such fundamental provisions as defining responsibility and authority as between the management board and its chairperson. General principles of shareholders rights were included in 73.5% of charters and 79.4% included procedures for theAGM.

BYLAWS AND POLICIES

Most banks had adopted basic bylaws with respect to the activities of the bank's governing bodies. For example, most banks had bylaws regarding the AGM (64.7%), the supervisory board (67.6%), the management board (73.5%), the audit committee (70.6%) and the internal audit function (73.5%). Most of those without such provisions indicated that they planned to introduce them in the near future.

Fundamental documentation was in place at most banks, but the survey showed that fewer banks had adequately documented policies concerning compliance with corporate governance best practices. Only 23.5% of respondents had a written policy with respect to a corporate secretary and 55.9% had no plans to implement one. Twothirds of the banks surveyed had no written policies concerning supervisory board committees or the payment of dividends. At the time of the survey, recent legislation had required all banks to report financial information in accordance with IFRS, yet only 32.3% of the banks surveyed had any bylaw with respect to disclosure. Chart 12 shows the bylaws and policies in place, along with respondents' plans to implement those not currently in force.

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

Annual general meeting

Supervisory board

Management board

Audit committee

Corporate secretary

Supervisory board committees

Corporate governance for a company group

Disclosure

Dividends

In place Planned Not planned/did not know

Internal audit function

Code of corporate governance

Code of ethics

64.7 23.5

11.8

23.5 67.7

8.8

73.5 17.7

8.8

70.6 20.6

23.5

8.8

8.8

5.9

20.6

32.3 41.2

26.5

14.7 20.6

64.7

32.3 38.2

26.5

32.3 50.0

17.7

73.5

32.3

32.3

14.7

17.7

53.0

61.8

55.9

Chart 12. Existing and Planned Bylaws and Policies (%)

Note: Total exceeds 100%. (Respondents were allowed multiple responses.)

AWARENESS OF AND COMMITMENT TO GOOD CORPORATE GOVERNANCE PRACTICES

IMPROVING CORPORATE GOVERNANCE

OBSTACLES TO IMPROVING CORPORATE GOVERNANCE

A key objective of this survey was to determine the extent to which the banks applied key corporate governance principles and to identify obstacles to improving corporate governance. The most frequently mentioned obstacle (61.8%) was ineffective corporate governance legislation. Next was the scarcity of specialists qualified in the field (41.2%), followed by the general lack of awareness of the subject (26.5%).

Respondents rated ineffective legislation as the most serious obstacle to improved corporate governance, yet they also rated this legislation as “much better than average.” On a scale of one to five (with one meaning “bad” and five meaning “good”), respondents gave an average rating of four to the legislation covering areas such as registration/startup, AGMs, composition of the supervisory board and management board and shareholders' rights. It is doubtful, therefore, that legislation is indeed the main obstacle.

MEASURES TO IMPROVE CORPORATE GOVERNANCE

Almost half of the banks surveyed (fifteen, or 44.1%) had a written corporate governance improvement plan, approved by the supervisory board or the AGM. When asked to identify the measures they believed would improve corporate governance, 52.9% indicated the establishment of supervisory board committees; however, establishing such committees became mandatory with the passage of the Law on Banks and the National Bank Corporate Governance Regulation. Other frequently mentioned priorities included training of supervisory board members and implementation of IFRS.

Implement IFRS

Appoint independent members to the supervisory board

Establish an audit committee

Establish the corporate secretary position

Implement a remuneration system for supervisory board members

Establish supervisory board committees

Disclosure information quarterly

Adopt a corporate governance code

Train supervisory board members in corporate governance

Hire corporate governance consultant

Introduce an internal control system

Introduce an internal audit function

23.5

11.8

17.6

5.9

17.6

52.9

11.8

14.7

38.2

20.6

8.8

2.9

Chart 13. Priorities for Improving Corporate Governance (%)

Note: Total exceeds 100%. (Respondents were allowed multiple responses.)

In most of the banks surveyed (82.4%), the management board was responsible for developing policies and bylaws. In almost half, the supervisory board or the chief legal counsel also participated in developing these documents.

2222

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

AWARENESS OF AND COMMITMENT TO GOOD CORPORATE GOVERNANCE PRACTICES

2323

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

AWARENESS OF AND COMMITMENT TO GOOD CORPORATE GOVERNANCE PRACTICES

Supervisory and Management

Board Practices

Supervisory and Management

Board Practices

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

2525SUPERVISORY AND MANAGEMENT BOARD PRACTICES

Chart 14. Responsibilities of the Supervisory Board, Management Board and AGM (%)

Representing the bank

Electing chair of supervisory board

Electing supervisory board members

Approving remuneration of supervisory board

Appointing head of management board

Appointing management board members

Approving remuneration of management board

Approving governing bodies bylaws

Approving other bylaws

Setting strategy

Developing operating plan

Approving budget

11.8 88.2

0.0

5.9 0.0

94.1

2.9 0.0

0.0 8.8

91.2

0.0 35.3

64.7

44.1 0.0

55.9

8.8 79.4

11.8

11.8 20.6

67.6

55.9

2.9 41.2

11.8 70.6

17.6

8.8 88.2

2.9

76.5 5.9

17.6

Supervisory board Management board Annual general meeting

Note: Total exceeds 100%. (Respondents were allowed multiple responses.)

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

97.1

SUPERVISORY BOARD

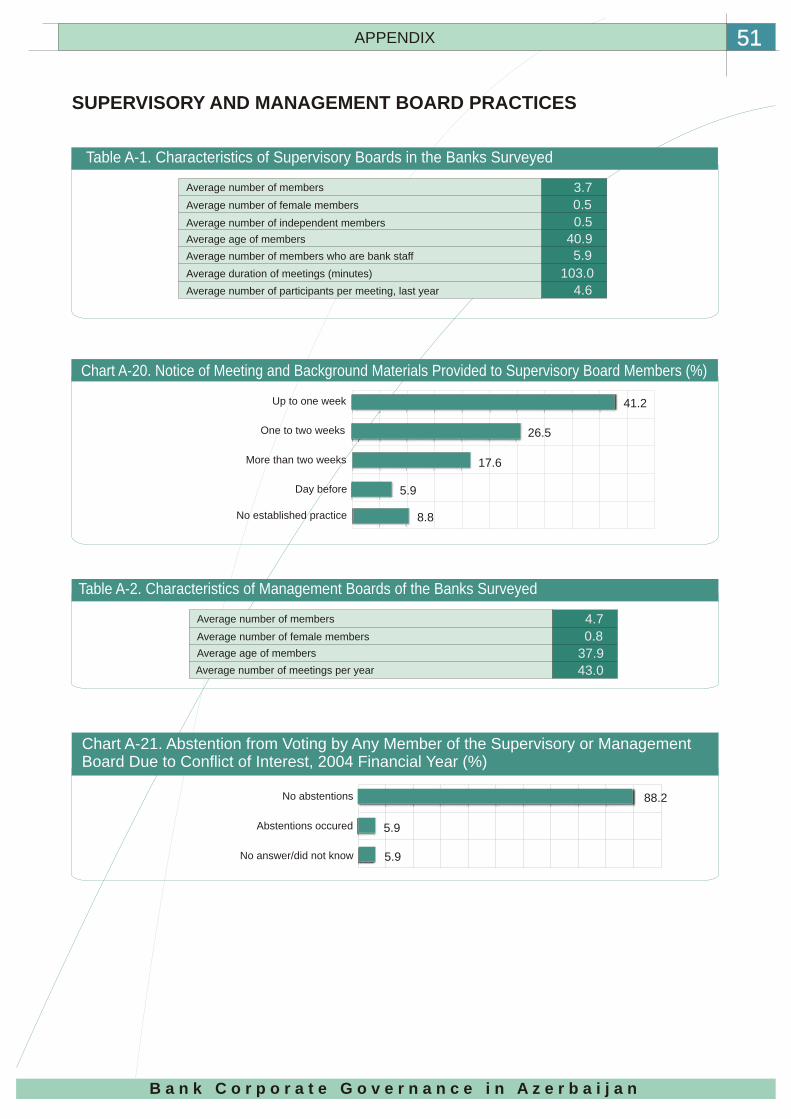

NUMBER OF MEMBERS

Good corporate governance practice requires that boards be large enough to encompass individuals with a range of specific finance, legal and commercial skills. On the other hand, a board exceeding a dozen members can be unwieldy. The law in most Eurasian countries prescribes a minimum number of board members, ranging

10from three to five. InAzerbaijan, the minimum for banks is three.

Threemember boards were most common (67.6%) in the banks surveyed, followed by fivemember boards (29.4%). One bank had a sevenmember board. The average was 3.7.

FREQUENCY OF MEETINGS

The Law on Banks requires that the supervisory boards of banks hold meetings at least quarterly. Most of the banks surveyed complied, convening meetings monthly (44.1%) or quarterly (38.2%). Meetings were held less frequently than quarterly in only two banks.

Monthly

2-3 times a year

Quarterly

Other11.8

44.1

5.9

38.2

Chart 16. Frequency of Supervisory Board Meetings (%)

Major shareholders and persons affiliated with major shareholders

Independent

Other67.6

10.2

22.2

Chart 15. Description of Supervisory Board Members (%)

2626

10 Corporate Governance in Eurasia: A Comparative Overview, OECD Roundtable, Kyiv, Ukraine (May 2004).

SUPERVISORY AND MANAGEMENT BOARD PRACTICES

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

2727

PREPARATION FOR MEETINGS

Most banks held the requisite number of meetings, but the survey showed that preparation for meetings needed improvement. Although all but 8.8% of the banks surveyed had established procedures for distributing materials to members prior to the meetings, some important documents were frequently lacking. For example, only half of the respondents reported that minutes of the last meeting were included. Chart 17 shows the documents provided.

PERFORMANCE EVALUATION

The survey results showed that in Azerbaijan, as in most developing economies, selfassessment of supervisory board performance is not a wellestablished practice. Within the last two years, the supervisory board carried out selfassessment in only eight of the banks surveyed (23.5%). The concept is quite new in Azerbaijan and the 23.5% figure is probably inflated.

REMUNERATION

Appropriate remuneration of the supervisory board is a principle of good corporate governance. Notably, Azerbaijani legislation allows for remuneration of supervisory board members to be computed as a percentage of the company’s net income. Roughly half of the banks surveyed (47.1%) paid the supervisory board members for their services. Of those, 41.2% based the remuneration on the net income of the bank. In determining remuneration, none of the banks took into account factors such as the market value of shares, meeting attendance or additional responsibilities.

Interestingly, more than half of the banks surveyed (55.9%) did not have contracts with the members of the supervisory board. Fourteen banks had contracts resembling employee contracts with the board members, governed by the strict provisions of the Labor Code of Azerbaijan. Only one bank had civil contracts in place, governed by the more flexible terms of the Civil Code of Azerbaijan.

Tied to bank net income

Tied to bank gross income

Fixed monthly amount

Based on evaluation of board activity

Not tied to any indicators

41.2

Chart 18. Remuneration Criteria for Supervisory Board Members (%)

SUPERVISORY AND MANAGEMENT BOARD PRACTICES

Agenda

Explanation of each agenda item

Most recent financial statements

Draft resolutions

Minutes of last meeting

Other

88.2

70.6

61.8

58.8

50.0

2.9

Chart 17. Materials Provided in Advance of Supervisory Board Meetings (%)

Note: Total exceeds 100%. (Respondents were allowed multiple responses.)

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

The reported periods for providing notice of the meeting and supporting materials were more than two weeks (17.6%), one to two weeks (26.5%) and one week (41.2%). In two banks, board members received the materials the day before the meeting.

23.5

23.5

5.9

5.9

28 28 SUPERVISORY AND MANAGEMENT BOARD PRACTICES

BOARD COMMITTEES

Board committees play an important role in corporate governance best practices. These committees became mandatory with the advent of the National Bank Corporate Governance Regulation. As a result, most banks had formally established the requisite committees, at least on paper. As mentioned, all of the banks surveyed had established a credit committee, most had an audit committee and many had an assetliability management committee. Chart 19 shows the existing and planned board committees.

Chart 19. Existing and Planned Committees (%)

Audit committee

Strategic planning committee

Nomination and remuneration committee

Corporate governance committee

Conflict resolution committee

Ethics committee

Credit committee

Assets-liability management committee

Information technology committee

Risk management committee

8.8 0.0

32.3

32.3

35.4

5.9

11.8

82.3

8.8

38.2

53.0

11.8

14.7

73.5

11.8

14.7

73.5

0.0 0.0

79.4

14.7

5.9

38.2

32.3

29.5

53.0 23.5

23.5

91.2

In place Planned Not planned/no answer

Note: Total exceeds 100%. (Respondents were allowed multiple responses.)

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

100.0

2929

MANAGEMENT BOARD

FUNCTION AND DESCRIPTION

By law, all banks must have a management board as well as a supervisory board. The management board is intended to be responsible for the daytoday operations of the bank. There is no upper limit on the size of the management board, but it must be an odd number and a minimum of three. The banks surveyed had five (44.1%), three (38.2%), or seven (14.7%) individuals on the management board. One bank had nine members. Women participated on the management boards of fourteen banks (41.2%). The average age of the management board members in the banks surveyed was thirtyeight.

The Law on Banks has some minimal requirements regarding the competency of board members, but some of the banks elaborated upon those requirements in their charters. For example, twentysix of the banks surveyed (76.5%) had competency requirements such as education and experience for management board members. For comparison, twentythree (67.6%) had competency requirements for supervisory board members. The key functions of the management board are shown in Chart 14 above.

FREQUENCY OF MEETINGS

The number of management board meetings per year ranged from four to 219 among the respondents. In part, the discrepancy can be attributed to each respondent's definition of a formal meeting. Most respondents said that their management board met daily to discuss minor issues, but these meetings were considered informal and not recorded in minutes. Others did consider these daily meetings formal and reported them as such.

COMMUNICATION WITH THE SUPERVISORY BOARD

Corporate governance best practices include having in place a system for the management board to report to and regularly communicate with the supervisory board, designed to enhance the operating efficiency of the bank. The management board reported to the supervisory board in writing in all of the banks surveyed. These reports were made quarterly (44.1%), monthly (38.2%), at every meeting of the supervisory board (11.8%), or annually (2.9%). In only eighteen of the banks surveyed (52.9%) did the management board report to the supervisory board verbally as well. Chart 20 shows the reporting intervals and means.

Monthly

Quarterly

Annually

At every meeting

Chart 20. Management Board Reports (%)

Written Verbal

SUPERVISORY AND MANAGEMENT BOARD PRACTICES

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

Note: Total exceeds 100%. (Respondents were allowed multiple responses.)

38.2

23.5

5.9

44.1

2.9 0.0

11.8

23.5

CONFLICTS OF INTEREST

Good corporate governance practice requires that supervisory board and management board members disclose conflicts of interest and abstain from voting on resolutions when a conflict exists. Ten respondents (29.4%) reported that their banks had regulations requiring conflict disclosure and seven (20.6%) had regulations requiring abstention from voting where a conflict exists. Notably, only two respondents (5.9%) indicated that members of the supervisory or management boards ever abstained from voting owing to conflicts of interest.

RELATED PARTY TRANSACTIONS11As discussed at a recent OECD Corporate Governance Roundtable, supervisory boards must take a much more

active role in managing and disclosing conflicts of interest and related party transactions. The Law on Banksrequires that the supervisory board approve related party transactions. In the majority of the banks surveyed (64.7%), this responsibility did indeed rest with the supervisory board. In the rest, related party transactions were approved by the management board (23.5%), or occasionally at theAGM (5.9%). Two respondents (5.9%) did not answer the question or did not know the answer.

SUMMARY

The survey revealed an unsatisfactory degree of compliance with good corporate governance practices at both the supervisory board and management board levels. Both bodies often performed functions beyond the scope of their responsibility, to the point of violating the law.

Most supervisory boards were composed of major shareholders or their affiliates.Asmall percentage of the banks surveyed had independent members on their supervisory boards, but even that modest number is suspect.

As to form, most banks complied with the requirements set out in law, such as the minimum number of supervisory board members, the minimum number of supervisory board meetings per year and the requisite committees. However, improvement is needed in practice and function.

In addition, potential conflicts of interest are a serious concern. A sizeable number of banks (43.6%) had no bylaws requiring either conflict disclosure or approval of related party transactions.

3030 SUPERVISORY AND MANAGEMENT BOARD PRACTICES

11 Corporate Governance in Eurasia: A Comparative Overview, OECD Roundtable, Kyiv, Ukraine (May 2004).

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

Shareholders’ RightsShareholders’ Rights

By law, the shareholders are the ultimate governing body of a bank. The AGM is their opportunity to participate in managing their investment and to ensure that their interests and rights are protected. What follows is a discussion of the practices related to protection of shareholders' rights among the banks surveyed, including their compliance with corporate governance best practices andAzerbaijani law.

AUTHORITYAND FUNCTIONS OF THEANNUAL GENERAL MEETING

Azerbaijani banking legislation confers more authority and functions on bank AGMs than nonbank corporate legislation assigns to other companies. As mentioned, some bank AGM prerogatives are exclusive and may not be delegated; others are nonexclusive and may be delegated to the supervisory board. The banks surveyed largely, but not fully, complied with allowing the AGM to execute its exclusive rights. For example, while the AGM usually elected the supervisory board members (97.1%) and the chair (94.1%), only 58.9% of respondents reported that the AGM approved the issuance of securities such as bonds. More remarkably, less than half of the banks surveyed indicated that the AGM approved the annual report or significant transactions (more than 25% of the net book value of assets). Chart 21 shows the exclusive rights of the AGM and the degree to which respondents complied in each case.

B a n k C o r p o r a t e G o v e r n a n c e i n A z e r b a i j a n

Elect supervisory board members

Elect supervisory board chair

Approve share issues

Approve declaration and distribution of dividends

Appoint head of management board

Approve significant transactions

Approve annual report

Approve bylaws of governing bodies*

Approve remuneration of management board members

97.1

94.1

79.6

67.6

64.7

47.1

44.1

20.6

11.8

Chart 21. Exclusive Functions Performed by the AGM (%)