The workings under the heading of “Additional Working” are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.weebly.com

2014

Compiled and Solved by:

Sameer Hussain

B.COM – II – COST ACCOUNTING

REGULAR

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 2

COST ACCOUNTING – 2014

REGULAR Instructions: (1) Attempt any FIVE questions in all. (2) All questions carry equal marks.

(3) Answers without necessary computations will not be accepted.

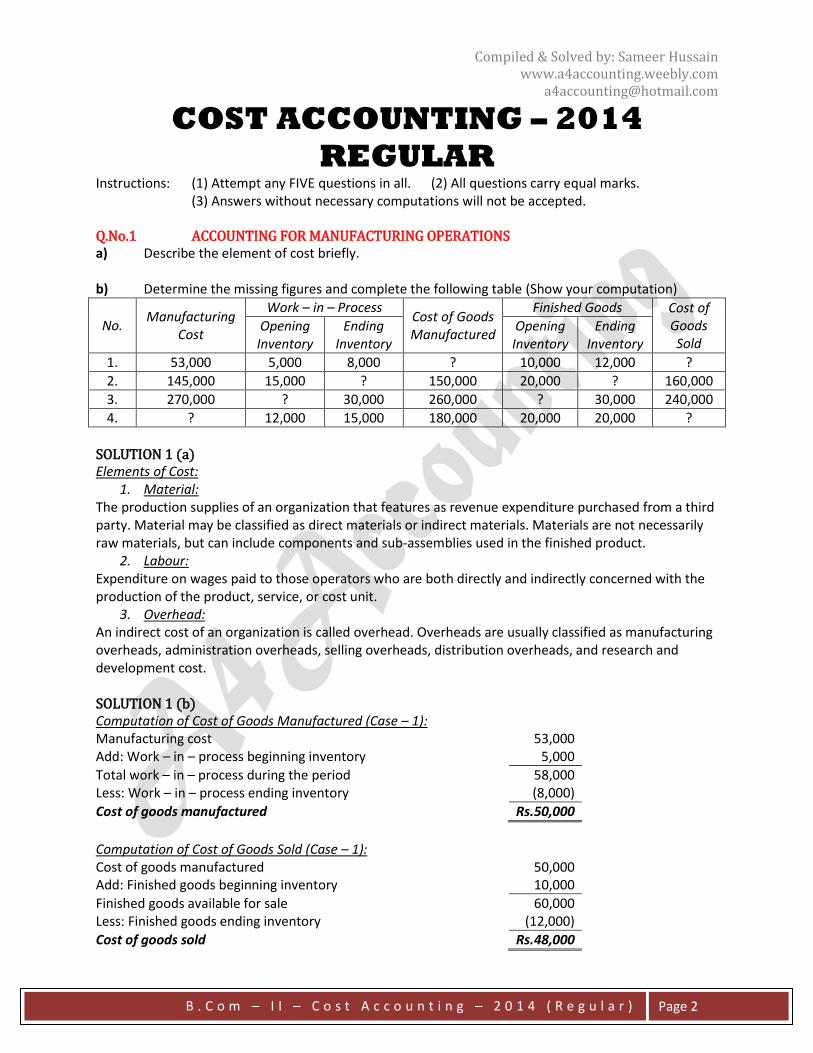

Q.No.1 ACCOUNTING FOR MANUFACTURING OPERATIONS a) Describe the element of cost briefly. b) Determine the missing figures and complete the following table (Show your computation)

No. Manufacturing

Cost

Work – in – Process Cost of Goods Manufactured

Finished Goods Cost of Goods Sold

Opening Inventory

Ending Inventory

Opening Inventory

Ending Inventory

1. 53,000 5,000 8,000 ? 10,000 12,000 ?

2. 145,000 15,000 ? 150,000 20,000 ? 160,000

3. 270,000 ? 30,000 260,000 ? 30,000 240,000

4. ? 12,000 15,000 180,000 20,000 20,000 ?

SOLUTION 1 (a) Elements of Cost:

1. Material: The production supplies of an organization that features as revenue expenditure purchased from a third party. Material may be classified as direct materials or indirect materials. Materials are not necessarily raw materials, but can include components and sub-assemblies used in the finished product.

2. Labour: Expenditure on wages paid to those operators who are both directly and indirectly concerned with the production of the product, service, or cost unit.

3. Overhead: An indirect cost of an organization is called overhead. Overheads are usually classified as manufacturing overheads, administration overheads, selling overheads, distribution overheads, and research and development cost. SOLUTION 1 (b) Computation of Cost of Goods Manufactured (Case – 1): Manufacturing cost 53,000 Add: Work – in – process beginning inventory 5,000

Total work – in – process during the period 58,000 Less: Work – in – process ending inventory (8,000)

Cost of goods manufactured Rs.50,000

Computation of Cost of Goods Sold (Case – 1): Cost of goods manufactured 50,000 Add: Finished goods beginning inventory 10,000

Finished goods available for sale 60,000 Less: Finished goods ending inventory (12,000)

Cost of goods sold Rs.48,000

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 3

Computation of Work – in – Process Ending Inventory (Case – 2): Manufacturing cost 145,000 Add: Work – in – process beginning inventory 15,000

Total work – in – process during the period 160,000 Less: Cost of goods manufactured (150,000)

Work – in – process ending inventory Rs.10,000

Computation of Finished Goods Ending Inventory (Case – 2): Cost of goods manufactured 150,000 Add: Finished goods beginning inventory 20,000

Finished goods available for sale 170,000 Less: Cost of goods sold (160,000)

Finished goods ending inventory Rs.10,000

Computation of Work – in – Process Opening Inventory (Case – 3): Cost of goods manufactured 260,000 Add: Work – in – process ending inventory 30,000

Total work – in – process during the period 290,000 Less: Manufacturing cost (270,000)

Work – in – process opening inventory Rs.20,000

Computation of Finished Goods Opening Inventory (Case – 3): Cost of goods sold 240,000 Add: Finished goods ending inventory 30,000

Finished goods available for sale 270,000 Less: Cost of goods manufactured (260,000)

Finished goods opening inventory Rs.10,000

Computation of Manufacturing Cost (Case – 4): Cost of goods manufactured 180,000 Add: Work – in – process ending inventory 15,000

Total work – in – process during the period 195,000 Less: Work – in – process opening inventory (12,000)

Manufacturing cost Rs.183,000

Computation of Cost of Goods Sold (Case – 4): Cost of goods manufactured 180,000 Add: Finished goods beginning inventory 20,000

Finished goods available for sale 200,000 Less: Finished goods ending inventory (20,000)

Cost of goods sold Rs.180,000

No. Manufacturing

Cost

Work – in – Process Cost of Goods Manufactured

Finished Goods Cost of Goods Sold

Opening Inventory

Ending Inventory

Opening Inventory

Ending Inventory

1. 53,000 5,000 8,000 50,000 10,000 12,000 48,000

2. 145,000 15,000 10,000 150,000 20,000 10,000 160,000

3. 270,000 20,000 30,000 260,000 10,000 30,000 240,000

4. 183,000 12,000 15,000 180,000 20,000 20,000 180,000

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 4

Q.No.2 STANDARD COSTING Amjad Company presents the following information about standard cost and actual cost for the month of November 2014:

Standard Actual

Material 5,000 units at a cost of Rs.75,000 Costing Rs.79,200 at a unit price of Rs.16.00

Labour 5,500 hours at an hourly rate of Rs.9.00 5,600 hours at an hourly rate of Rs.9.50

Factory overhead

Fixed cost Rs.8,000 and variable cost Rs.5,000 for a normal volume of 10,000 units

Fixed cost Rs.8,000 and variable cost Rs.4,800 for production of 9,000 units

REQUIRED (a) Calculate:

(i) Material price and quantity variance. (ii) Labour wage and efficiency variance. (iii) Factory overhead controllable and volume variance.

(b) Give entries in General Journal to record and to close the variance accounts. SOLUTION 2 (a) Computation of Material Price Variance: Material price variance = (Standard price – Actual price) x Actual quantity Material price variance = (75,000/5,000 – 16.00) x (79,200/16.00) Material price variance = (15.00 – 16.00) x 4,950 Material price variance = (4,950) (Unfavourable) Computation of Material Quantity Variance: Material quantity variance = (Standard quantity – Actual quantity) x Standard price Material quantity variance = {5,000 – (79,200/16.00)} x (75,000/5,000) Material quantity variance = (5,000 – 4,950) x 15.00 Material quantity variance = 750 (Favourable) Computation of Labour Wage Variance: Labour wage variance = (Standard price – Actual price) x Actual hours Labour wage variance = (9.00 – 9.50) x 5,600 Labour wage variance = (2,800) (Unfavourable) Computation of Labour Efficiency Variance: Labour efficiency variance = (Standard hours – Actual hours) x Standard price Labour efficiency variance = (5,500 – 5,600) x 9.00 Labour efficiency variance = (900) (Unfavourable) Computation of Factory Overhead Rate: Fixed factory overhead rate (8,000/10,000) Rs.0.80 Variable factory overhead rate (5,000/10,000) Rs.0.50

Factory overhead rate Rs.1.30

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 5

Computation of Factory Overhead Controllable Variance: Actual factory overhead (8,000 + 4,800) 12,800 Less: Budgeted allowance based on standard output: Fixed factory overhead budgeted 8,000 Variable factory overhead (10,000 x 0.50) 5,000

Budgeted allowance based on standard output (13,000)

Factory overhead controllable variance (Favourable) Rs.200

Computation of Volume Variance: Budgeted allowance based on standard output 13,000 Less: Applied factory overhead for actual output (9,000 x 1.30) (11,700)

Factory overhead volume variance (Unfavourable) Rs.1,300

SOLUTION 2 (b)

AMJAD COMPANY GENERAL JOURNAL

Date Particulars P/R Debit Credit

1 Work in process 75,000 Material price variance 4,950 Material quantity variance 750 Raw material 79,200 (To record the material price and quantity variance)

2 Work in process (5,500 x 9.00) 49,500 Labour wage variance 2,800 Labour efficiency variance 900 Accrued payroll (5,600 x 9.50) 53,200 (To record the labour rate and efficiency variance)

3 Work in process (9,000 x 1.30) 11,700 Factory overhead volume variance 1,300 Factory overhead controllable variance 200 Factory overhead (8,000 + 4,800) 12,800 (To record the factory overhead variance)

AMJAD COMPANY CLOSING ENTRIES

Date Particulars P/R Debit Credit

1 Material quantity variance 750 Factory overhead controllable variance 200 Cost of goods sold 9,000 Material price variance 4,950 Labour wage variance 2,800 Labour efficiency variance 900 Factory overhead volume variance 1,300 (To close the all variances)

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 6

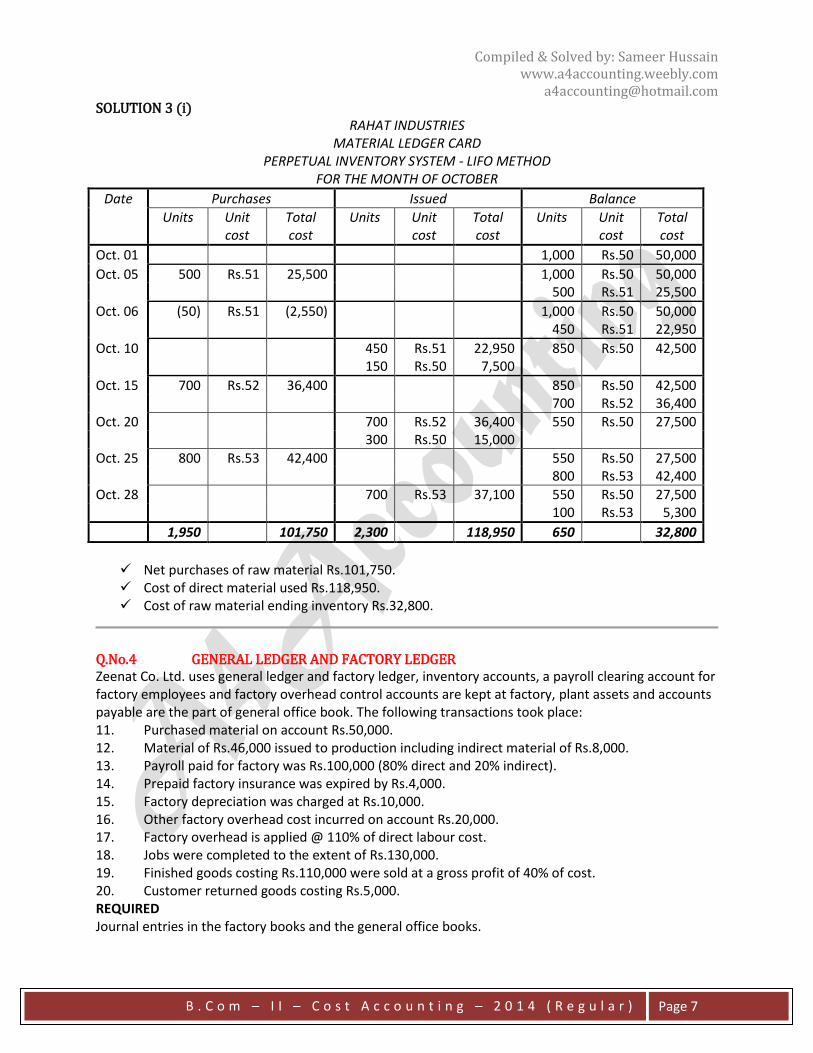

Q.No.3 MATERIAL COSTING – INVENTORY SYSTEM Rahat Industries uses a single type of material. The following data relate to purchases and issue of the material: October 01: Balance 1,000 units @ Rs.50 October 05: Purchased 500 units @ Rs.51 October 06: Returned to supplier 50 units October 10: Issued to job 600 units October 15: Purchased 700 units @ Rs.52 October 20: Issued to job 1,000 units October 25: Purchased 800 units @ Rs.53 October 28: Issued to job 700 units REQUIRED Prepare inventory card under perpetual system using:

(i) First in First out. (ii) Last in First out. SOLUTION 3 (i)

RAHAT INDUSTRIES MATERIAL LEDGER CARD

PERPETUAL INVENTORY SYSTEM - FIFO METHOD FOR THE MONTH OF OCTOBER

Date Purchases Issued Balance

Units Unit cost

Total cost

Units Unit cost

Total cost

Units Unit cost

Total cost

Oct. 01 1,000 Rs.50 50,000

Oct. 05 500 Rs.51 25,500 1,000 Rs.50 50,000 500 Rs.51 25,500

Oct. 06 (50) Rs.51 (2,550) 1,000 Rs.50 50,000 450 Rs.51 22,950

Oct. 10 600 Rs.50 30,000 400 Rs.50 20,000 450 Rs.51 22,950

Oct. 15 700 Rs.52 36,400 400 Rs.50 20,000 450 Rs.51 22,950 700 Rs.52 36,400

Oct. 20 400 Rs.50 20,000 550 Rs.52 28,600 450 Rs.51 22,950 150 Rs.52 7,800

Oct. 25 800 Rs.53 42,400 550 Rs.52 28,600 800 Rs.53 42,400

Oct. 28 550 Rs.52 28,600 650 Rs.53 34,450 150 Rs.53 7,950

1,950 101,750 2,300 117,300 650 34,450

Net purchases of raw material Rs.101,750. Cost of direct material used Rs.117,300. Cost of raw material ending inventory Rs.34,450.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 7

SOLUTION 3 (i) RAHAT INDUSTRIES

MATERIAL LEDGER CARD PERPETUAL INVENTORY SYSTEM - LIFO METHOD

FOR THE MONTH OF OCTOBER

Date Purchases Issued Balance

Units Unit cost

Total cost

Units Unit cost

Total cost

Units Unit cost

Total cost

Oct. 01 1,000 Rs.50 50,000

Oct. 05 500 Rs.51 25,500 1,000 Rs.50 50,000 500 Rs.51 25,500

Oct. 06 (50) Rs.51 (2,550) 1,000 Rs.50 50,000 450 Rs.51 22,950

Oct. 10 450 Rs.51 22,950 850 Rs.50 42,500 150 Rs.50 7,500

Oct. 15 700 Rs.52 36,400 850 Rs.50 42,500 700 Rs.52 36,400

Oct. 20 700 Rs.52 36,400 550 Rs.50 27,500 300 Rs.50 15,000

Oct. 25 800 Rs.53 42,400 550 Rs.50 27,500 800 Rs.53 42,400

Oct. 28 700 Rs.53 37,100 550 Rs.50 27,500 100 Rs.53 5,300

1,950 101,750 2,300 118,950 650 32,800

Net purchases of raw material Rs.101,750. Cost of direct material used Rs.118,950. Cost of raw material ending inventory Rs.32,800.

Q.No.4 GENERAL LEDGER AND FACTORY LEDGER Zeenat Co. Ltd. uses general ledger and factory ledger, inventory accounts, a payroll clearing account for factory employees and factory overhead control accounts are kept at factory, plant assets and accounts payable are the part of general office book. The following transactions took place: 11. Purchased material on account Rs.50,000. 12. Material of Rs.46,000 issued to production including indirect material of Rs.8,000. 13. Payroll paid for factory was Rs.100,000 (80% direct and 20% indirect). 14. Prepaid factory insurance was expired by Rs.4,000. 15. Factory depreciation was charged at Rs.10,000. 16. Other factory overhead cost incurred on account Rs.20,000. 17. Factory overhead is applied @ 110% of direct labour cost. 18. Jobs were completed to the extent of Rs.130,000. 19. Finished goods costing Rs.110,000 were sold at a gross profit of 40% of cost. 20. Customer returned goods costing Rs.5,000. REQUIRED Journal entries in the factory books and the general office books.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 8

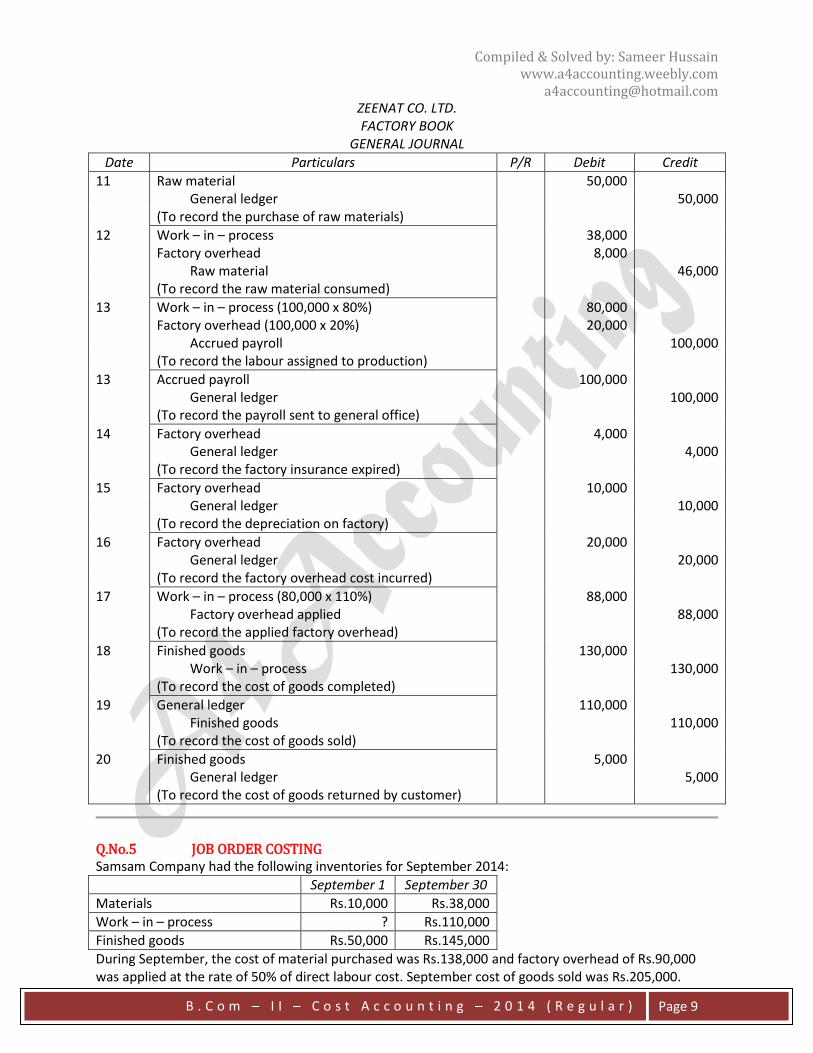

SOLUTION 4 ZEENAT CO. LTD.

GENERAL OFFICE BOOK GENERAL JOURNAL

Date Particulars P/R Debit Credit

11 Factory ledger 50,000 Voucher payable 50,000 (To record the purchase of raw materials)

12 No entry

13 Payroll 100,000 Accrued payroll 100,000 (To record the factory payroll)

13 Accrued payroll 100,000 Voucher payable 100,000 (To record the voucher prepared for payroll)

13 Voucher payable 100,000 Bank 100,000 (To record the payment of payroll)

13 Factory ledger 100,000 Payroll 100,000 (To close the payroll account)

14 Factory ledger 4,000 Prepaid insurance 4,000 (To record the factory insurance expired)

15 Factory ledger 10,000 Allowance for depreciation 10,000 (To record the depreciation charged on factory)

16 Factory ledger 20,000 Voucher payable 20,000 (To record the factory overhead incurred on account)

17 No entry

18 No entry

19 Cost of goods sold 110,000 Factory ledger 110,000 (To record the cost of goods sold)

19 Accounts receivable (110,000 x 140%) 154,000 Sales 154,000 (To record the goods sold on account)

20 Sales return and allowance 7,000 Accounts receivable (5,000 x 140%) 7,000 (To record the goods returned by customer)

20 Factory ledger 5,000 Cost of goods sold 5,000 (To record the cost of goods returned by customer)

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 9

ZEENAT CO. LTD. FACTORY BOOK

GENERAL JOURNAL

Date Particulars P/R Debit Credit

11 Raw material 50,000 General ledger 50,000 (To record the purchase of raw materials)

12 Work – in – process 38,000 Factory overhead 8,000 Raw material 46,000 (To record the raw material consumed)

13 Work – in – process (100,000 x 80%) 80,000 Factory overhead (100,000 x 20%) 20,000 Accrued payroll 100,000 (To record the labour assigned to production)

13 Accrued payroll 100,000 General ledger 100,000 (To record the payroll sent to general office)

14 Factory overhead 4,000 General ledger 4,000 (To record the factory insurance expired)

15 Factory overhead 10,000 General ledger 10,000 (To record the depreciation on factory)

16 Factory overhead 20,000 General ledger 20,000 (To record the factory overhead cost incurred)

17 Work – in – process (80,000 x 110%) 88,000 Factory overhead applied 88,000 (To record the applied factory overhead)

18 Finished goods 130,000 Work – in – process 130,000 (To record the cost of goods completed)

19 General ledger 110,000 Finished goods 110,000 (To record the cost of goods sold)

20 Finished goods 5,000 General ledger 5,000 (To record the cost of goods returned by customer)

Q.No.5 JOB ORDER COSTING Samsam Company had the following inventories for September 2014:

September 1 September 30

Materials Rs.10,000 Rs.38,000

Work – in – process ? Rs.110,000

Finished goods Rs.50,000 Rs.145,000

During September, the cost of material purchased was Rs.138,000 and factory overhead of Rs.90,000 was applied at the rate of 50% of direct labour cost. September cost of goods sold was Rs.205,000.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 10

REQUIRED (a) Prepare T – accounts for inventories showing the flow of the cost of goods manufactured and

sold. (b) Assuming that the inventory of work – in – process at September 30 was consisted of Rs.32,000

of materials, determine the cost of direct labour and factory overhead. SOLUTION 5 (a) Computation of Work – in – Process Beginning Inventory: Cost of goods sold 205,000 Add: Finished goods ending inventory 145,000

Finished goods available for sale 350,000 Less: Finished goods beginning inventory (50,000)

Cost of goods manufactured 300,000 Add: Work – in – process ending inventory 110,000

Total work – in – process during the period 410,000 Less: Manufacturing Cost: Raw material beginning inventory 10,000 Add: Purchases of raw material 138,000

Raw material available for use 148,000 Less: Raw material ending inventory (38,000)

Direct material used 110,000 Add: Direct labour (90,000 x 100/50) 180,000

Prime cost 290,000 Add: Factory overhead 90,000

Total manufacturing cost (380,000)

Work – in – process beginning inventory Rs.30,000

Raw Material

Sep. 1 Balance 10,000 Work – in – process 110,000 Purchases 138,000 Sep. 30 Balance c/d 38,000

148,000 148,000

Oct. 1 Balance b/d 38,000

Work – in – Process

Sep. 1 Balance 30,000 Finished goods 300,000 Raw material 110,000 Sep. 30 Balance c/d 110,000 Accrued payroll 180,000 Factory overhead 90,000

410,000 410,000

Oct. 1 Balance b/d 110,000

Finished Goods

Sep. 1 Balance 50,000 Cost of goods sold 205,000 Work – in – process 300,000 Sep. 30 Balance c/d 145,000

350,000 350,000

Oct. 1 Balance b/d 145,000

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 11

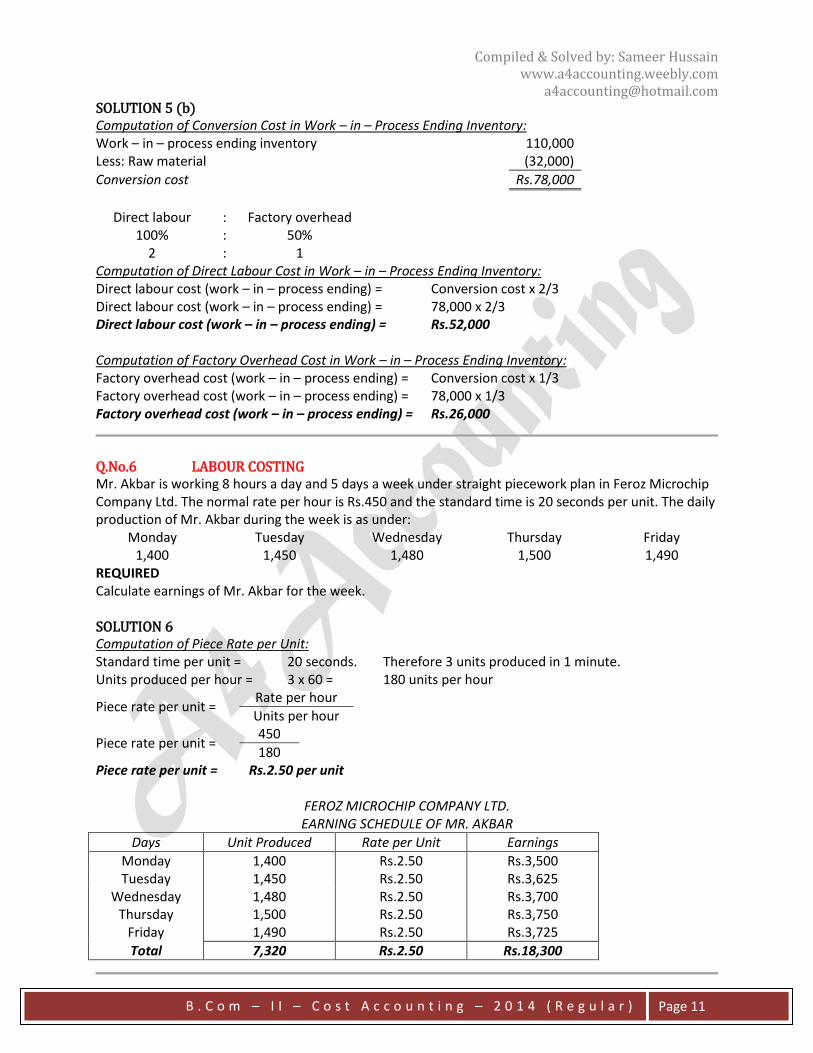

SOLUTION 5 (b) Computation of Conversion Cost in Work – in – Process Ending Inventory: Work – in – process ending inventory 110,000 Less: Raw material (32,000)

Conversion cost Rs.78,000

Direct labour : Factory overhead

100% : 50% 2 : 1

Computation of Direct Labour Cost in Work – in – Process Ending Inventory: Direct labour cost (work – in – process ending) = Conversion cost x 2/3 Direct labour cost (work – in – process ending) = 78,000 x 2/3 Direct labour cost (work – in – process ending) = Rs.52,000 Computation of Factory Overhead Cost in Work – in – Process Ending Inventory: Factory overhead cost (work – in – process ending) = Conversion cost x 1/3 Factory overhead cost (work – in – process ending) = 78,000 x 1/3 Factory overhead cost (work – in – process ending) = Rs.26,000

Q.No.6 LABOUR COSTING Mr. Akbar is working 8 hours a day and 5 days a week under straight piecework plan in Feroz Microchip Company Ltd. The normal rate per hour is Rs.450 and the standard time is 20 seconds per unit. The daily production of Mr. Akbar during the week is as under:

Monday Tuesday Wednesday Thursday Friday 1,400 1,450 1,480 1,500 1,490

REQUIRED Calculate earnings of Mr. Akbar for the week. SOLUTION 6 Computation of Piece Rate per Unit: Standard time per unit = 20 seconds. Therefore 3 units produced in 1 minute. Units produced per hour = 3 x 60 = 180 units per hour

Piece rate per unit = Rate per hour

Units per hour

Piece rate per unit = 450

180 Piece rate per unit = Rs.2.50 per unit

FEROZ MICROCHIP COMPANY LTD. EARNING SCHEDULE OF MR. AKBAR

Days Unit Produced Rate per Unit Earnings

Monday 1,400 Rs.2.50 Rs.3,500 Tuesday 1,450 Rs.2.50 Rs.3,625

Wednesday 1,480 Rs.2.50 Rs.3,700 Thursday 1,500 Rs.2.50 Rs.3,750

Friday 1,490 Rs.2.50 Rs.3,725

Total 7,320 Rs.2.50 Rs.18,300

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 12

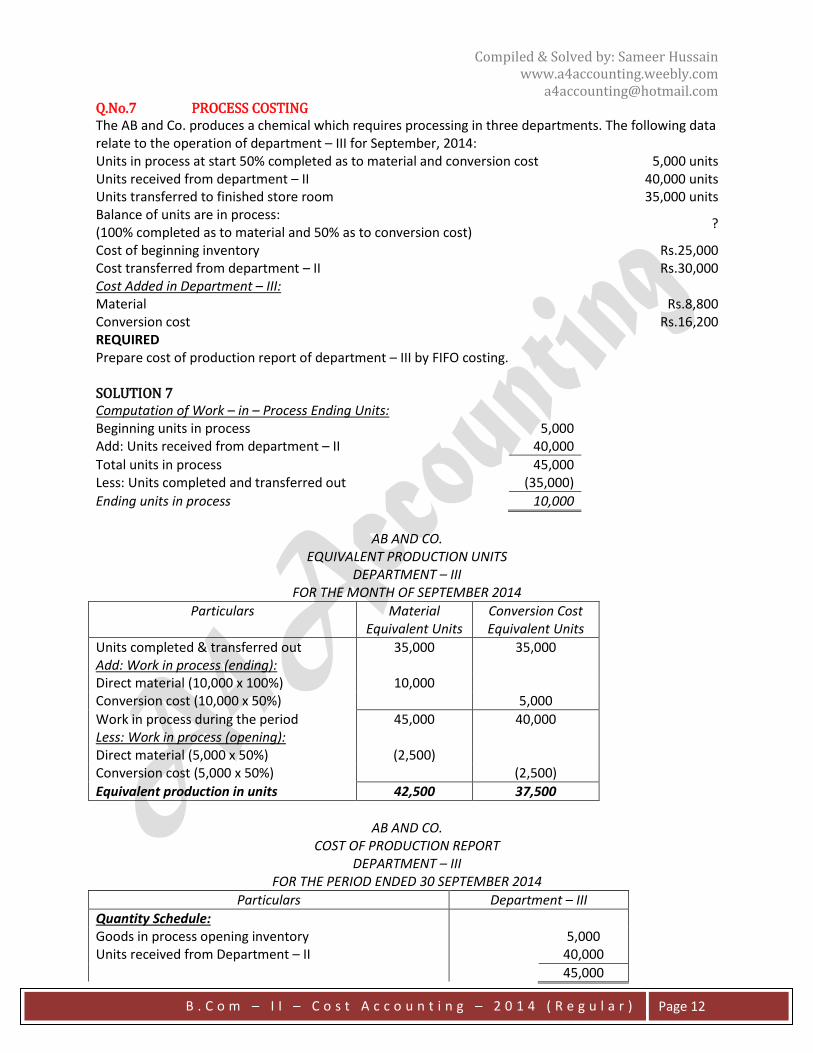

Q.No.7 PROCESS COSTING The AB and Co. produces a chemical which requires processing in three departments. The following data relate to the operation of department – III for September, 2014: Units in process at start 50% completed as to material and conversion cost 5,000 units Units received from department – II 40,000 units Units transferred to finished store room 35,000 units Balance of units are in process: (100% completed as to material and 50% as to conversion cost)

?

Cost of beginning inventory Rs.25,000 Cost transferred from department – II Rs.30,000 Cost Added in Department – III: Material Rs.8,800 Conversion cost Rs.16,200 REQUIRED Prepare cost of production report of department – III by FIFO costing. SOLUTION 7 Computation of Work – in – Process Ending Units: Beginning units in process 5,000 Add: Units received from department – II 40,000

Total units in process 45,000 Less: Units completed and transferred out (35,000)

Ending units in process 10,000

AB AND CO.

EQUIVALENT PRODUCTION UNITS DEPARTMENT – III

FOR THE MONTH OF SEPTEMBER 2014

Particulars Material Equivalent Units

Conversion Cost Equivalent Units

Units completed & transferred out 35,000 35,000 Add: Work in process (ending): Direct material (10,000 x 100%) 10,000 Conversion cost (10,000 x 50%) 5,000

Work in process during the period 45,000 40,000 Less: Work in process (opening): Direct material (5,000 x 50%) (2,500) Conversion cost (5,000 x 50%) (2,500)

Equivalent production in units 42,500 37,500

AB AND CO.

COST OF PRODUCTION REPORT DEPARTMENT – III

FOR THE PERIOD ENDED 30 SEPTEMBER 2014

Particulars Department – III

Quantity Schedule: Goods in process opening inventory 5,000 Units received from Department – II 40,000

45,000

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 13

Units completed and transferred out 35,000 Units still in process 10,000

45,000

Cost Charged to the Department - III: Total Cost Unit Cost

Goods in process opening inventory 25,000 Cost received from department – II (30,000/40,000) 30,000 Rs.0.750 Cost Added by Department – III: Material (8,800/42,500) 8,800 Rs.0.207 Conversion cost (16,200/37,500) 16,200 Rs.0.432

Total cost added 25,000 Rs.0.639

Total cost to be accounted for 80,000 Rs.1.389

Cost Accounted for as Follows: Goods in process opening inventory 25,000 Add: Cost Added in September: Material (5,000 x 50% x 0.207) 518 Conversion cost (5,000 x 50% x 0.432) 1,080

Total cost of 5,000 units 26,598 Add: Cost of remaining units (30,000 x 1.389) 41,672

Total cost of units completed and transferred out 68,270 Cost of Work in Process Ending Inventory: Cost from Department – II (10,000 x 0.750) 7,500 Material (10,000 x 100% x 0.207) 2,070 Conversion cost (10,000 x 50% x 0.432) 2,160

Total cost of work in process ending inventory 11,730

Total cost accounted for Rs.80,000

Q.No.8 DEPARTMENTALIZATION OF FACTORY OVERHEAD Ahsan Mining Corporation has producing department A and B, and service department C, D and E. it is company’s policy that once a service department costs have been distributed, no cost from other service department are to be distributed to it. The information given below pertains to the month just ended. Cost of service departments are distributed as follows: Department C on the basis of number of employees. Department D on the basis of investment in equipment. Department E on the basis of floor space.

Department Cost Square Feet Employees Investment in Equipment

A Rs.15,000 2,000 40 Rs.170,000

B Rs.12,000 3,000 30 Rs.80,000

C Rs.14,000 4,000 20 Rs.130,000

D Rs.8,000 2,000 30 Rs.70,000

E Rs.2,000 1,500 20 Rs.50,000

Total Rs.51,000 12,500 140 Rs.500,000

REQUIRED Distribute the overhead of service department.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

B . C o m – I I – C o s t A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 14

SOLUTION 8 AHSAN MINING COMPANY

FACTORY OVERHEAD DISTRIBUTION SHEET

Particulars Total Producing Department Service Department

A B C D E

Overhead before allocation 51,000 15,000 12,000 14,000 8,000 2,000 Allocation of Service Departments Cost:

Department – C 4,667 3,500 (14,000) 3,500 2,333 Department – B 6,517 3,066 --- (11,500) 1,917 Department – D 2,500 3,750 --- --- (6,250)

Overhead after allocation 51,000 28,684 22,316 --- --- ---

Distribution of Cost of Department – C: Department A = 14,000 x 40/120 = 4,667 Department B = 14,000 x 30/120 = 3,500 Department D = 14,000 x 30/120 = 3,500 Department E = 14,000 x 20/120 = 2,333 Distribution of Cost of Department – D: Department D cost = 8,000 + 3,500 = 11,500 Department A = 11,500 x 170,000/300,000 = 6,517 Department B = 11,500 x 80,000/300,000 = 3,066 Department E = 11,500 x 50,000/300,000 = 1,917 Distribution of Cost of Department – E: Department E cost = 2,000 + 2,333 + 1,917 = 6,250 Department A = 6,250 x 2,000/5,000 = 2,500 Department B = 6,250 x 3,000/5000 = 3,750

Recommended

![B.COM (F & CA) BACHELOR OF COMMERCE - Indira ...FCA) MCom [MAFS].pdfPROSPECTUS AND PROGRAMME GUIDE B.COM (F & CA) BACHELOR OF COMMERCE with Major in Financial and Cost Accounting M.COM](https://img.pdfslide.net/doc/110x75/5ab885d67f8b9ac60e8cedff/bcom-f-ca-bachelor-of-commerce-indira-fca-mcom-mafspdfprospectus-and.jpg)