Beyond Procurement Options for procurement to drive company-wide productivity Survey rePOrt

Matthias Kaesser

Sammy Rashed

With contribution of:

Giles Breault

Michael Henke

Daniel Hollos

Beyond ProcurementOptions for procurement to drive company-wide productivitySurvey report

Giles BreaultMichael HenkeDaniel HollosMatthias KaesserSammy Rashed

Imprint

Prof. Dr. Michael Henke Head of Institute Phone +49 611 7102 2100 [email protected] www.ebs.edu/iscm

Dr. Daniel Hollos Project Manager for Industrial Research Projects Phone +49 611 7102 2138 [email protected] www.ebs.edu/iscm

Dipl.-Ing. Matthias Kaesser External Doctoral Candidate (on educational leave at McKinsey & Company) Phone +49 89 5594 8586 [email protected] www.ebs.edu/iscm

Sammy Rashed, MBA Novartis Pharma AG Executive Partner for Corporate Research, Institute for Supply Chain Management Phone +41 79 593 9121 [email protected]

Giles Breault, MBA, C.P.M., MCIPS Former CPO, Roche & Aventis, Head of Global Productivity and Business Services, Novartis Pharma AG Chairman of Advisory Board – Procurement Leader Network Phone +41 79 820 3706 [email protected]

Aut

hors

C

ontr

ibut

ors

Practitioners Academia EBS Business School, Institute for Supply Chain

Management – Procurement and Logistics

0

© Supply Chain Management Institute (SMI), Wiesbaden, 2012

Breault, Giles; Henke, Michael; Hollos, Daniel; Kaesser, Matthias; Rashed, Sammy

Beyond Procurement, Options for procurement to drive company-wide productivity, Survey report

Publisher: EBS Universität für Wirtschaft und Recht

EBS Business School

Institute for Supply Chain Management - Procurement and Logistics (ISCM)

Composition and layout: plaindesigns gmbh, Haifastrasse 73, 28279 Bremen, www.plaindesigns.com

All rights reserved, also for translations into other languages. No part of this publication may be reproduced or processed, duplicated or

distributed by electronic means in any way, even for use in teaching curricula, without the written consent of the publisher.

Bibliographic information from Deutsche Bibliothek (Central Archival Library and National Bibliographic Centre for the Federal Republic of

Germany): Deutsche Bibliothek has registered this publication in the German National Bibliography; detailed bibliographic data can be found

on the Internet at http://dnb.ddb.de.

4 Beyond Procurement

Over the last three decades the procurement function has been

one of the most progressive organizations within large companies,

moving from a transactional “back office” activity to a vital element

for ensuring smooth supply, risk reduction and profitability growth.

Gains in these areas however eventually reach a point of dimin-

ishing return, which contrasts with the ever-growing pressure on

the function to contribute more and play a greater role in driving

productivity. Likewise, progressive practitioners in the Supply Chain

and Procurement arena have become increasingly frustrated by the

inability to “move the needle” with respect to their own contribu-

tion; while believing that they can deliver much more, they often

feel “boxed in” by restrictive internal mandates and organizational

barriers.

Industry practitioners reached out to the academic community to

assess the importance of this trend, and to evaluate which direc-

tions were considered by different companies as the best way to

Preface

steer their procurement resources to drive a new value proposi-

tion. In the course of this investigation seeking to establish a clear

future direction, it was found that very little could be gained from

the literature and that while certain trends could be gleaned from

anecdotal interviews, no real body of thought had emerged as to

how and where should a modern, globally distributed procurement

function be directing its future efforts, and to what degree those

efforts would be seen by their employers as providing a boost in

real value.

This survey and related research projects intend to bridge that gap

in the literature, and most importantly to provide practitioners with

a menu of possibilities on where to apply resources and further

guide them towards what is seen by companies as most impor-

tant – an endeavor likely to redefine the nature of the function, its

direction and overall contribution.

Contents

1 Management Summary .............................................................................................................................................................6

2 evolution of procurement .........................................................................................................................................................7

3 Survey method and sample ......................................................................................................................................................7

4 Future options to drive company-wide productivity ..................................................................................................................9

4.1 the “top ten options” .....................................................................................................................................................9

4.2 Survey results ................................................................................................................................................................10

4.2.1 Overall results...................................................................................................................................................10

4.2.2 Performance measures .....................................................................................................................................10

4.2.3 Feasibility measures .........................................................................................................................................12

4.3 Deep dive on the “Innovation Sourcing” option ............................................................................................................13

4.4 Deep dive on the “total Cost-Base Management” option...............................................................................................14

5 Outlook ...................................................................................................................................................................................15

6 Literature ................................................................................................................................................................................15

5Beyond Procurement

1 Management Summary

Where is procurement heading? Which con-

tribution could the function make beyond its

traditional territory? Which roles and respon-

sibilities could it pursue in the future?

In the course of the Beyond Procurement

survey introduced here we asked CXOs

and managers from procurement, finance

and other business functions to share their

opinion about ten short-listed options for

procurement to drive firm-wide productiv-

ity. Furthermore we were interested in the

professionals’ opinions about where the func-

tion should evolve to in the near future and

which major obstacles it would face along the

way. Overall we based our findings on 119

respondents working for companies of vari-

ous industries selected mainly across Europe,

North America and Asia. Our findings can be

summarized as follows:

Procurement is under constant and increas-

ing pressure to deliver more, however the

development of new solutions has evolved at

a slower pace than the growing expectations.

≈ The contribution of the function could be

significant to yield higher levels of firm-

wide productivity, yet is often confined

within current mandate to drive compli-

ance and cost savings.

≈ The survey aimed to identify “what‘s

next” for the function, moving from secur-

ing supply to globally and holistically man-

aging company spend, and specifically to

validate the hypothesis that the biggest

impact would come from the following

options:

a) Better leverage the supply base to

spark greater innovation

b) Apply and combine proven productivity

approaches across the entire cost base

≈ In workshops, focus groups and discus-

sions with professionals on CPO confer-

ences throughout 2011 and 2012, the

following 10 options were identified as the

most promising for procurement to drive

company-wide productivity:

≈ “Top-line Contributor”

≈ “Innovation Sourcing”

≈ “Total Cost-Base Management”

≈ “Global Business Services”

≈ “Comprehensive Risk Management”

≈ “Take Over Operational Activities”

≈ “Next Level Collaborative Buying”

≈ “Internal Consulting / Project Manage-

ment”

≈ “Extended SRM”

≈ “Embed Function Into The Business”

From the received responses, four options for

growth stood-out:

≈ “Innovation Sourcing” and “Total Cost-

Base Management” come out as the two

most promising options in terms of perfor-

mance and feasibility, which validates the

survey hypothesis.

≈ “Global Business Services” is expected to

continue delivering high returns, although

the approach appears to be already imple-

mented in many organizations.

≈ Looking forward, participants plan greater

external involvement via “Extended SRM”

(e.g. helping build lean management / six-

sigma capabilities at suppliers) to deliver

additional value. However the function

may lack the required capabilities to drive

such developments further at the mo-

ment.

6 Beyond Procurement

2 evolution of procurement

Professionals from the supply chain and

procurement area repeatedly point out the

paradigm shift that purchasing has gone

through in recent decades: The function

evolved from a rather administrative and

operational “order-executor” to an or-

ganization with more strategic importance

for their companies1. Many procurement

organizations turned around completely

when going through this progression by

installing cross-functional or cross-business

coordination, or even building up separate

and centralized procurement organiza-

tions. These changes were mainly driven by

increasing globalization that lead to a more

fierce competition and a focus on produc-

tivity and costs, as well as higher levels of

outsourcing – adding more weight to the

function as the share of purchasing volume

on the total cost base increased – and the

rise of E-Commerce2. As a consequence

of this increased focus on the function,

procurement organizations became more

professional and managed to achieve

higher returns then before, allowing Pro-

curement to receive significant attention

from top management; especially in these

times of financial crises and high economic

volatility.

As much as this development is a reason

for procurement professionals to celebrate,

it cannot be seen as a guarantee for endur-

ing prosperity of the function. For example,

purchasing departments are not immune

to the increasing levels of outsourcing

themselves. The most operational activities

are especially bound to be outsourced to a

shared services center or even externally,

and the current trend to spin out separate

procurement companies could just as well

be an interim step in that direction. As a

consequence there is an ongoing lively

debate on the future of Procurement3. This

leaves us with the question on where the

function is heading and whether there

are realistic options for procurement to

enhance the overall performance of their

companies – beyond driving savings from

third party spend.

3 Survey method and sample

The structure of the Beyond Procurement

survey is illustrated in figure 1. The survey

contains two main sections: The first focus-

ing on “Performance” of the respondents’

procurement organizations in regard to the

ten pre-defined options, the second one

focusing on the “Feasibility” of a respective

implementation. The first part – “Perfor-

mance” – is furthermore divided into two

different time-wise perspectives – past

performance and future expectations – each

time asking for the actual or planned im-

plementation priority as well as the actual

or expected return by option. The second

part focuses on two separate dimensions of

implementation feasibility: i) the readiness

of the whole organization in regards to the

implementation of each option, and ii) the

Future expectations – “looking ahead”

In the next two years: • Please indicate which of top ten options are planned to be rolled-out? • What return is expected for each option that will be implemented? • What function will be responsible for driving the implementation / taking the option over?

Organizational readiness

Please answer for each of the top ten options: • What is today the level of organizational readiness (i.e. the willingness of your company to

implement it)?

Capability proficiency

Please answer for each of the top ten options: • What is today the capability proficiency (i.e. skill / ability of the procurement function to

successfully drive)?

Status quo – “looking back”

In the past two years: • Please indicate which of top ten options have been implemented? • What return was achieved for each option implemented? • What function was responsible for driving the implementation / taking the option over?

PER

FOR

MAN

CE

FEAS

IBIL

ITY

Survey Questions Section

Survey structure and questions

Fig. 1 Survey structure and questions

1 Cf. Carr & Smeltzer (1997); Lamming et al. (2000); Handfield & Nichols (2002); Knudsen (2003); Paulraj, Chen & Flynn (2006); Zheng et al. (2007)2 Cf. Gadde & Hakansson (1994); Carter et al. (2000), 3 Cf. van Weele & Rozemeijer (1996); Harland, Lamming & Cousins (1999); Zheng et al. (2007)

7Beyond Procurement

capability of the procurement function itself

to successfully deliver on this offering.

Participants responded by selecting their

level of agreement regarding the imple-

mentation priority as well as the feasibility

dimensions by option on a scale from “1”

(very low) to “5” (very high) and selected

the return figure in percent on a scale from

“0%” to “9%+”. The survey was conducted

online to provide quick access and maxi-

mum convenience for participants.

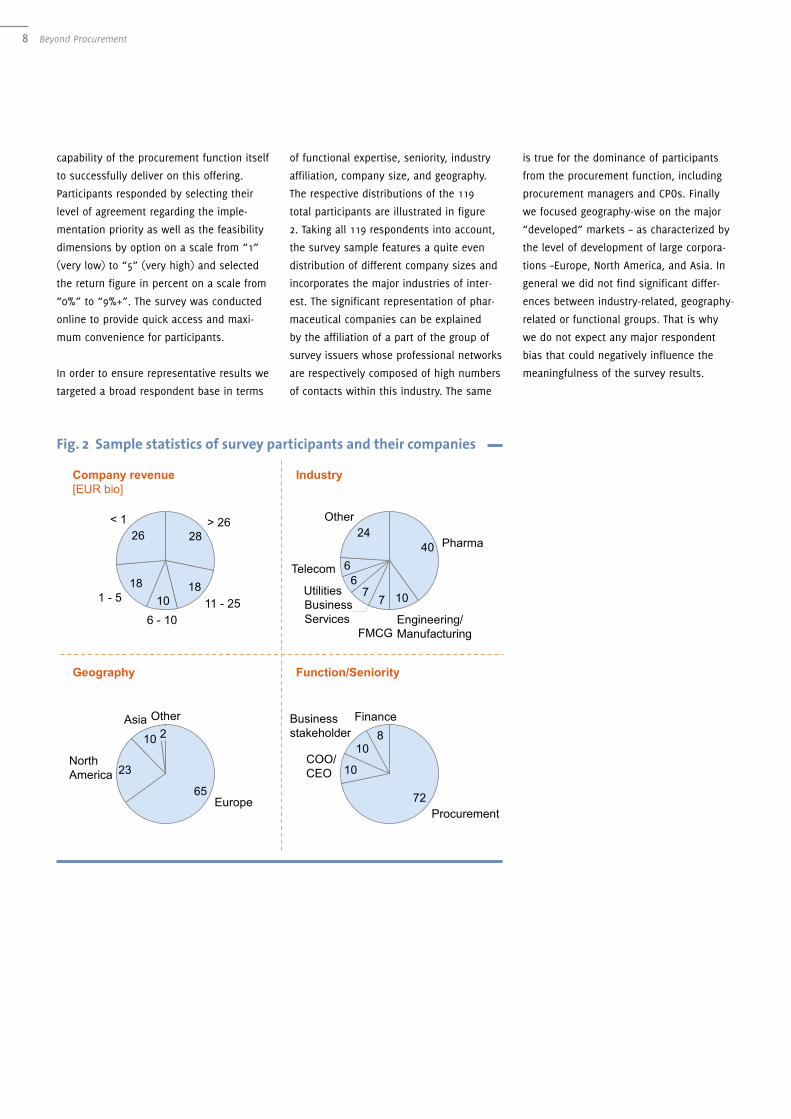

In order to ensure representative results we

targeted a broad respondent base in terms

of functional expertise, seniority, industry

affiliation, company size, and geography.

The respective distributions of the 119

total participants are illustrated in figure

2. Taking all 119 respondents into account,

the survey sample features a quite even

distribution of different company sizes and

incorporates the major industries of inter-

est. The significant representation of phar-

maceutical companies can be explained

by the affiliation of a part of the group of

survey issuers whose professional networks

are respectively composed of high numbers

of contacts within this industry. The same

is true for the dominance of participants

from the procurement function, including

procurement managers and CPOs. Finally

we focused geography-wise on the major

“developed” markets – as characterized by

the level of development of large corpora-

tions –Europe, North America, and Asia. In

general we did not find significant differ-

ences between industry-related, geography-

related or functional groups. That is why

we do not expect any major respondent

bias that could negatively influence the

meaningfulness of the survey results.

Sample statistics of survey participants and their companies

26

1810

18

28< 1

1 - 5

6 - 10 11 - 25

> 26 24

66

77 10

40

Engineering/ Manufacturing

Pharma

Other

Telecom

Utilities Business Services

FMCG

10

23

65

Other 2

Asia

North America

Europe

810

10

72Procurement

Finance Business stakeholder

COO/ CEO

Company revenue [EUR bio]

Function/Seniority Geography

Industry

Fig. 2 Sample statistics of survey participants and their companies

8 Beyond Procurement

4 Future options to drive company-wide productivity

1. top-Line Contributor: Companies

could leverage Procurement’s transferable

skills, capabilities, and process expertise

to impact sales growth. Examples of this

include training the sales team on negotia-

tions, applying procurement’s mastery of

contract management in the areas of busi-

ness development or licensing, using SRM

best practices to better manager relations

with key customers, or creating a new

offering all together which can then be

offered to external parties.

2. Innovation Sourcing:

The supply base’s potential to drive

product and process innovations seems

to be under-leveraged in many firms. By

recognizing and even creating “innova-

tion sparks” as well as developing those

through a well-managed and replicable

process companies could improve overall

innovativeness. Since innovation is best

triggered not only by adding money but

also when facing financial constraints, the

pressure to realize savings can represent a

useful burning platform.

3. total Cost-Base Management:

By combining proven approaches and

processes such as demand management,

lean management / six-sigma, and offshor-

ing & outsourcing, procurement could offer

a broader range of solutions to internal

stakeholders. This also allows to expand

procurement’s scope beyond 3rd party

spend.

4. Global Business Services:

An approach adopted by many lead-

ing global organizations, to reduce costs

and free-up time and resources, allow-

ing management to focus on customers

and growing the business. It streamlines

non-customer facing activities (such as HR,

finance, IT, facilities, legal services, etc.)

and aggregates them into an internal unit

that services the rest of the business.

4.1 the “top ten options”

5. risk Protection & Management:

Beyond the specific role of ensuring compli-

ance when committing funds to 3rd parties,

this option targets a more comprehensive

and proactive approach to mitigating risks

for the company. For example, moving from

traditionally having key categories sup-

ported by back-up suppliers to a full supply

risk management and business continuity

plan – that may also involve sharing risks

from the customer side with the supply

base.

6. take Over Operational Activities:

Often as a result of category projects,

procurement can be left holding the opera-

tional responsibilities when the function

– which previously owned it – is reduced

or in some cases outsourced (e.g., travel,

fleet, facility management). This option

extends the Procurement function agent

role beyond leading the acquisition process

and adds a service-delivery responsibility

for supporting the internal users with their

operational needs.

7. “Next Level” Collaborative Buying:

In contrast to the various current forms of

consortium buying, this approach recog-

nizes the risks of collaborative sourcing

and capitalizes on procurement’s ability to

scan joint-buying opportunities but de-risk

the benefit stream through the creation of

individual joint ventures focused at narrow

categories of spend.

8. Internal Consultant/Project Managers:

Since most category initiatives are usually

complex initiatives that require cross-

functional leadership skills and strong

stakeholder engagement, procurement

could take these skills to the next level and

turn them into an internal capability, which

offers an alternative to external consult-

ants.

9. extended SrM (building lean manage-

ment / six-sigma capabilities at suppliers):

Variation of some other options above, this

applies the lean / six-sigma process early

in the production cycle by ensuring a clear

and relentless focus on the ’voice of cus-

tomer’, removing all activities considered

non-value-add and which bring unneces-

sary costs. There have been many good

examples of this in the direct areas, but

not as many in the indirect categories so

far.

10. embed Function into Business:

Take a critical look at procurement’s scope

and identify which categories of spend

are better managed centrally (typically

general and corporate spend), as well as

infrastructure-related activities (guidelines,

training, talent development), and consider

embedding the procurement resources for

more customer –focused categories directly

in the line-functions.

9Beyond Procurement

4.2 Survey results

4.2.1 Overall results

Overall the survey results suggest focusing

on four options for procurement to develop

further: “Innovation Sourcing”, “Total

Cost-Base Management”, “Global Business

Services”, and “Extended SRM”. Whereas

TCBM2

Extended SRM3

Sourcing Innovation

6

1 Based on implementation priority and return performance 2 Total Cost Base Management 3 Extend SRM building up lean management / six-sigma capabilities at suppliers

TCBM2

Global Business Services

Sourcing Innovation

Importance1 today

Importance1 in the future

“Top 3” options voted1 Four main productivity options to pursue

THE CHAMPIONS Both options Sourcing Innovation and

TCBM2 rank amongst the highest in terms of implementation priority as well as actual / expected return (ranging from 4 – 5 %); today as well as in the future

THE NEWCOMER Extended SRM3 shows the highest

increase in importance. An average return of ~5% ist expected from this option

THE VETERAN Continuing to deliver high returns of ~5%,

participants still highly value GBS, but do not expect further implementation efforts

Overall findings based on survey results

the first two come through as the preferred

options today as well as the foreseeable

future, the appeal of “Global Business

Services” diminishes somewhat (perhaps

because it has already been implemented

to a large extent) while “Extended SRM”

is expected to become a more compel-

ling approach in the future (cf. figure 3).

In the next two sections we will discuss

the results by option in more depth.

Fig. 3 Overall findings based on survey results

4.2.2 Performance measures

The survey results suggest to clearly

distinguish between two major groups

regarding the performance of the options.

Figure 4 provides an overview of the

respondents’ voting regarding today’s

as well as expected future implementa-

tion priorities and return by option.

Looking at the status quo, the group of

options that currently delivers high returns

of around 4 to 5 percent – “Innovation

Sourcing”, “Global Business Services”,

“Top Line Contributor”, “Total Cost-Base

Management”, and partly also “Internal

Consultant” – also expel the highest imple-

mentation scores. In that regard companies

have apparently prioritized the implemen-

tation of options that help to deliver the

highest returns or they are executing the

implemented ones very well and do not

spend too much focus on others. The only

exception from this observed pattern is the

option of “Risk Protection & Management”

which is very well implemented in the

majority of companies that participated,

however does not seem to yield particularly

high returns. This might be the case due to

the original nature of risk mitigation where

an immediate positive return is more diffi-

cult to measure because it helps to protect

from exceptional negative effects. In our

context, however, we also see risk manage-

ment as a way to increase productivity

by sharing risks not only from the supply,

but also from the customer side with all

parties involved in the supply chain. In that

10 Beyond Procurement

regard we assume that most organizations

still approach risk management in terms of

mitigating exceptional events. In summary,

it seems that there are three top perform-

ing options already present in procurement

today – based on a combination of imple-

mentation status and returns (cf. “total

performance score” in figure 4): “Innova-

tion Sourcing”, “Total Cost-Base Manage-

ment”, and “Global Business Services”.

Regarding the participants’ future expec-

tations this “top 3” list does not change

too much interestingly: Looking forward

there is no clear picture regarding the

implementation priorities in comparison

to the status quo; the spread between the

different options is quite low compared to

the “status quo situation” (51 percentage

points spread in “status quo” situation vs.

30 percentage points spread in the “future

outlook”). However, the overall expected

In summary these results suggest that

professionals are open and may welcome

Procurement’s contribution beyond its tradi-

tional remit - the management of the entire

cost base, as well as the stark involvement

in increasing the company’s innovative-

ness being the two most popular over time

(cf. figure 4). Secondly the results also

suggest that risk management – despite its

obvious “shortfall” of not being applicable

to the measurement in percentages of

return – is and remains a core responsibil-

ity of the procurement function. On the

other side of the scale, the two options

of “Taking Over Operational Activities” as

well as “Next Level Collaborative Buying”

appear to be – in terms of implementation

as well as return – relatively less attrac-

tive options from responding companies.

8

Top-Line Contributor

Sourcing Innovation

TCBM1

GBS2

Risk Protect. /Mmgmt.

Take Over Op. Activ.

Next Level Collb. Buying

Int. Consultant

Extended SRM

Embed func. into bus

Option

Implementation priority3 Positive answers in percent

Today / status quo

Estimated return4 In percent

Total performance score5 Illustrative

Future outlook

52

43

67

26

56

77

62

68

70

60

3,2

3,3

3,7

2,3

2,9

2,5

4,4

4,0

4,8

4,2

55

65

70

59

44

74

55

62

74

56

4,5

4,8

3,7

3,6

2,9

2,6

5,3

4,8

5,0

5,2

Implementation priority3 Positive answers in percent

Estimated return4 In percent

Total performance score5 Illustrative

1 Total cost base management 2 Global business services 3 Number of “yes” answers compared to total answers of whether option is (currently being) implemented or will be implemented in the future 4 Actual or expected/estimated return per option as implemented or planned 5 Importance score (index) combining indices of the prior two questions – implementation priority and return

Detailed performance measures by option

return increases (from 3.5% to 4.3%

average return across all options) most

probably factoring in increasing levels of

expectation. Applying the same reasoning

described above, that implementation pri-

oritization should follow high-level returns,

a group of 6 options with an expected

return of 4.5% and higher emerges from the

picture of results. Amongst these, the “top

3” options of the “status quo” situation

are also expected to deliver the high-

est returns in the future; all at or above

5%. Conversely, it appears that “Global

Business Services” has been implemented

already to a large extent as its imple-

mentation priority number decreases.

This makes the option “Extended SRM” a

newcomer in the “future top 3” options

to consider – alongside with “Innovation

Sourcing” and “Total Cost-Base Manage-

ment” as in the “status quo” situation.

Fig. 4 Detailed performance measures by option

11Beyond Procurement

4.2.3 Feasibility measures

Focusing first on the “top 3” options identi-

fied above, procurement needs to continue

working on the required skills internally.

“Total Cost-Base Management” and “Inno-

vation Sourcing” seem to entail some addi-

tional capabilities that are currently not yet

present; both ranking between around the

“medium” position (voted around “3”; right

in the middle between “1” – “low capabil-

ity proficiency” and “5” – “high capabil-

ity proficiency”). The skills to perform a

global business service center, the third

top option, seem to be even less devel-

oped in procurement organizations at the

moment. Still, compared to the rest of the

options, the “top 3” performing options are

amongst those where procurement can pro-

vide a rather developed capability profile.

As important as the development of skills

and capabilities is the results also suggest

the need to continuously engage internal

stakeholders and raise their awareness &

acceptance of procurement’s contribution

clearly stood out, as most of the options

presented rank below average in regards

to the respective organizational readiness.

Taking a closer look, it becomes apparent

that the options of “Innovation Sourcing”

as well as “Risk Protection” are by the far

the most “desired” ones from the busi-

ness side. A clear coincidence with the very

high implementation importance scorings

of these two options discussed above. As

for the capability dimension, procurement

seems to have already started to either

respond to the request from the business

or promoting its future areas of responsi-

bility already; nonetheless further work is

needed to get full account and trust from

the organization as a whole (cf. figure 5).

10

2

3

4

2 3 4

GBS

Organizational readiness Grades: 1 (low) to 5 (high)

Capability proficiency Grades: 1 (low) to 5 (high)

NLCB

TCBM

IS TLC

ESRM EFIB

IC

RPM

TOA

Detailed feasibility measures by option

1 Willingness of the respondents’ company to implement 2 Skills / ability of the procurement function to successfully drive the respective option forward

TLC – Top-Line Contributor IS – Innovation Sourcing TCBM – Total Cost Base Management GBS – Global Business Services RPM – Risk Protection & Management TOA – Take Over Operational Activities NLCB – Next Level Collaborative Buying IC – Internal Consultant ESRM – Extended SRM EFIB – Embed Function into Business

Fig. 5 Detailed feasibility measures by option

12 Beyond Procurement

4.3 Deep dive on the “Innovation Sourcing” option

Innovation has always been and remains

a key area of interest for businesses as it

has been identified as a key resource for

competitive advantage. And as suppliers

now take over more responsibilities for

product as well as process innovations

– given the higher levels of outsourcing –

and do engage in closer collaboration with

their customers, this leads to innovation

alliances and “open innovation” networks,

which can nicely leverage the procurement

function’s natural interface to the sup-

ply base. However innovations come at a

price; or more precisely, implies a series

of challenges that are difficult to address:

How to trigger, how to replicate, how to

sustain and how to measure innovations?

The results of the survey clearly show

that procurement nowadays and in the

future already focuses on the sourcing of

innovations. Still not all of the required

capabilities seem to be present and devel-

oped already (cf. figure 6). Following the

conversations we had around this topic in

our focus groups and with survey partici-

pants, the identification and promotion of

innovations to bring them to success is the

achievement of tenacious individuals within

procurement, sometimes supported by a

loose structure of incentives for innovative

suppliers (e.g., yearly supplier innovation

awards) and the incorporation of an inno-

vations dimension in supplier assessments.

So far we have not yet encountered a pro-

curement organization that has rigorously

defined processes and systems that allow

for a broader screening of the supply base

for innovations and that provide a basis for

innovations to be driven through their vari-

ous stages of development against internal

resistance. This makes innovativeness

based on the suppliers great knowledge

base rather accidental than intentional.

In order to give the function enough space

to better identify where sparks happen

and ensure we are the first customer with

whom suppliers share their innovation,

it might be fruitful to allow the function

to focus on areas other than for example

process compliance and/or cost savings.

Furthermore it is essential and a prereq-

uisite to expand the procurement team’s

mindset beyond the pure cost manage-

ment focus. For example, there will be

only little motivation to buyers for bringing

innovation that drives top-line growth if

they are only measured on bottom-line

impact. Here, procurement can create a

huge opportunity and leverage its supplier

management to help grow its contribu-

tion beyond cost performance resulting

in a competitive edge for the company. In

that sense, as, procurement could be just

as important a source for innovation as

R&D - and may even get results faster.

•Better leverage the supply base’s potential to drive product and process innovations by defining a well-managed and replicable process

•Recognize and incentivize for “innovation sparks” at suppliers through a burning platform that considers elements of close relationship as well as extraordinary pressure

•Preserve disruptive innovations from getting rejected in their early development phase through internal skepticism and biased review process

Description of productivity option

Survey results – high level overview

Implementation priority

today future Comment

Actual / expected return

Organizational readiness

Capability proficiency

Very high

Very high

Respectively ranking #2 (today) and #1 (future) – out of 10

About 5% annual productivity increase expected

Average to high

One of 3 top options that are supported / required by the org.

n/a Currently only some professionals show the required capabilities

Very high

Very high

Average

n/a

Survey item

Average level,

Upcoming research on…

12

…how to leverage potential:

How can procurement ensure to “trigger and spot innovation sparks”?

What is the right supplier management / relationship / governance to improve suppliers‘ innovativeness?

How can the function overcome allergies to disruptive change internally?

…how to increase procurement‘s capabilities:

Which profile of a procurement professional required for innovation sourcing?

What are appropriate performance measures for sourced innovations?

Deep dive information on “Innovation Sourcing”

Fig. 6 Deep dive information on “Innovation Sourcing”

13Beyond Procurement

4.4 Deep dive on the “total Cost-Base Management” option

“Total Cost-Base Management” (TCBM) is a

comprehensive end-to-end way of looking

at the spend base. Its basic tenet sug-

gests that integrating all of the functions

normally associated with creating value

and driving productivity will generate

higher and compounded levels of benefits

if properly tasked, targeted and rewarded

for that effort. This approach views costs

across organisation boundaries and not just

as discrete components but also as sys-

tems that drive demand and expenditure.

By combining functions and processes such

as Procurement, Offshoring & Outsourc-

ing (O&O), and Lean / Six Sigma (LSS),

with a robust global project management

approach, an end-to-end cost management

team is created. This helps organiza-

tions diagnose, evaluate and implement

measures that focus on the sources of

costs to create more durable solutions

and deliver savings above average levels.

The basic principle on which it builds

is that any activity that leads to a cost

whether internal or external is a product

of a system of business needs. When

those needs are evaluated by traditional

structures these costs are treated sub-

optimally because they are considered

independently. By recognizing this segrega-

tion, creating a powerful systemic costs

analysis, and applying related comprehen-

sive solutions, cost management moves

out from independently managed budget

cuts to root-cause based solutions that

are consistent with business objectives.

Results from the survey indicate a sus-

tained interest in the TCBM approach,

based on past performance and future

expectations which reflect a 20% increase

in targeted savings (cf. figure 4). From

the feasibility perspective, this option is

positioned amongst the top ones in terms

of the organization appetite to receive it,

and the procurement department’s abil-

ity to deploy it (cf. figure 7). The above

average performance return expected,

combined with the limited risk to roll-

ing it out (as it is comprised of existing

functions being pulled together) explain

why TCBM is one of the top contemplated

options for driving additional value.

Interviews and outcomes of the focus

groups also indicate that Procurement

practitioners had a strong feeling that

this collaborative approach would drive

new value. Experience with LEAN / Six

Sigma and similar problem evaluation

models had given participants a strong

belief that when a more comprehensive

approach would be applied across larger

organisations, the opportunity to get at the

root cause of costs would provide much

greater insights and visibility that could

be successfully mined for new value.

Description of productivity option

today future Comment

Organizational readiness

Capability proficiency

Very high High Respectively ranking #3 (today)

and #5 (future) – out of 10

Expected return increases from ~4% to ~5%

Average Amongst top 60% of options that are supp. / required by the org.

n/a Average proficiency level of procurement professionals

High Very high

Average

n/a

Survey item

Average level,

Upcoming research to…

… better understand:

•What industries and areas (F&A, Commercial, Production,…) are best suited for TCBM?

•Key drivers and initiators behind adopting approach?

•Which processes / functions other than Procurement, LSS, and O&O are typically included in TCBM?

•Major organizational barriers and how they were overcome?

… validate:

•Actual % savings returns generated by TCBM

•What other KPIs/metrics are used to demonstrate versatility of new combined organization

• Increase in Sr. Execs in organizations who’s career included TCBM

Implementation priority

Actual / expected return

•Comprehensive method of managing all costs, both internal and external.

•Combines existing functions like Procurement, Offshoring & Outsourcing (O&O), and Lean / Six Sigma (LSS) into a single organization, with robust project management approach

•Offers end-to-end cost management team which help organizations diagnose, drive, and deliver optimization projects

Survey results – high level overview

Deep dive information on “Total Cost Base Management”

Fig. 7 Deep dive information on “Total Cost Base Management”

14 Beyond Procurement

5 Outlook

The procurement function has come a long

way since its humble beginnings. Where it

was once a necessary enabler, it has moved

beyond the transactional world to become

a function that has broad impact on busi-

ness continuity, risk, and profitability. Yet

even this broader mandate has its limits

and it is reasonable to infer that without

seeking mandate beyond its historical

boundaries and use of traditional tools,

the function has done as much as it can.

Today, procurement groups are seeking

ways to further impact the organizations

they serve, and this will require new capa-

bilities and enlightened organizations that

will allow procurement to further integrate

it more intensely into the business at large.

While that direction will need to be aligned

with the actual business needs and strat-

egy for each company and industry, the

choices that are more meaningful involve

Procurement collaborating and integrating

with organizations beyond it own doors.

The research team comprised of Academia

and industry practitioners, through this

survey gained a unique insight into the

aspirations of contemporary procure-

ment functions across a broad spectrum

of industry. Additional research will build

on the foundation created here, focusing

more narrowly on the choices that seem

to be preferred throughout industry. This

later research will evaluate and quantify

the benefits that organizations accrue when

they develop the internal capability offering

and grow the organizational readiness to

break from old mandates and expectations.

On a final note, many participants in this

survey as well as others who have become

acquainted with these results expressed

their desire to stay in contact with the

authors and participating contributors as

a way of evaluating their own company

direction and benefit. In all of the focus

groups that were conducted as a part of

the research, participants looked eagerly to

the results and many have subsequently

sought guidance in furthering their own

efforts. We recognize this need and have

established a communication & exchange

platform allowing the researcher and

respondent community to participate in

an even broader discussion on this topic.

6 LiteratureCarr, A.S., Smeltzer, L.R. (1997). An

empirically based operational definition of

strategic purchasing. European Journal of

Purchasing and Supply Management, 3 (4),

199-207.

Carter, P., Carter, R., Monczka, R., Slaight, T.,

Swan, A. (2000). The future of purchasing

and supply: A ten-year forecast. Journal of

Supply Chain Management, 36 (1), 14-26.

Handfield, R.B., Nichols, E.L. (2002). Supply

Chain Redesign: Converting Your Supply

Chain into an Integrated Value System.

Financial Times Prentice-Hall, NJ.

Harland, C., Lamming, R., Cousins, P. (1999).

Developing the concept of supply strategy.

International Journal of Operations & Pro-

duction Management, 19 (7), 650-673.

Knudsen, D. (2003). Aligning corporate

strategy, procurement strategy and procure-

ment tools. International Journal of Physical

Distribution and Logistics Management, 33

(8), 720-734.

Lamming, R., Johnsen, T., Zheng, J., Harland,

C. (2000). An initial classification of supply

networks. International Journal of Opera-

tions and Production Management, 20 (6),

675-691.

Paulraj, A., Chen, I.J., Flynn, J. (2006). Levels

of strategic purchasing: impact on supply

integration and performance. Journal of

Purchasing and Supply Management, 12 (3),

107-122.

van Weele, A., Rozemeijer, F. (1996).

Revolution in purchasing: building competi-

tive power through proactive purchasing.

European Journal of Purchasing & Supply

Management 2 (4), 153-160.

Zheng, J., Knight, L., Harland, C., Humby, S.,

James, K., (2007). An analysis of research

into the future of purchasing and supply

management. Journal of Purchasing and

Supply Management, 13 (1), 69-83.

Gadde, L.-E., Hakansson, H. (1994). The

changing role of purchasing: reconsidering

three strategic issues. European Journal of

Purchasing & Supply Management, 1 (1),

27-35.

15Beyond Procurement

Institute for Supply Chain Management - Procurement and Logistics (ISCM)eBS university for economics and Law

Konrad-Adenauer-Ring 15 65187 WiesbadenGERMANY

Tel.: +49 (0) 611 - 7102-2100Fax: +49 (0) 611 - 7102-1990

www.ebs.edu/iscm

Recommended