CHAPTER-1 INTRODUCTION

1.1 BACKGROUND TO THE STUDY

Marketers use promotional activities as a major tool in communicating their intentions. In

order for a particular promotional program to be effective it should lead to an increase in

sales, survival of the business and change in the consumer or visitor's attitude towards the

products or services. Promotion is one way in which marketers communicate with the public

and particularly the set target market. "Marketing theorists have accepted the terms

'Promotional Mix' or 'Promotional Blend' to classify the tools available to communicate with

and persuade current and potential customers".

1.2 STATEMENT OF THE PROBLEM

Big Bazaar a leading hypermarket chain with presence across the country & category

leader.

Big Bazaar in Hyderabad opened their 7th store at Kukatpally in the month of January,

2014 as FBB (Fashion at Big Bazaar), later in the month of March they introduced

Hypermarket.

Post the launch of Kukatpally branch we conducted a research to understand the

Customer awareness and level of satisfaction in terms of offers / Merchandise at

Kukatpally

1.3 THE PURPOSE OF THE STUDY

The purpose of the study is to determine the Effectiveness of Promotional Activities and

Perception about the Store either FBB or Hypermarket

1.4 OBJECTIVES OF THE STUDY

To know the Effectiveness of Promotional Activities at Kukatpally Big Bazaar To know whether the customer are aware about the change from FBB to Hypermarket

1

1.5 SCOPE OF THE STUDY Geographical Area:

The research basically covered inside Big Bazaar outlet and area in and around Kukatpally

(Hyderabad)

Subject Matter:

This was a study of marketing a product with special reference to promotion of a product.

Usually promotion causes a change in sales volume. However, a change in sales does not

necessarily imply the role of promotion. The change could have resulted from other factors.

Hence the study seeks to establish the position of promotion in causing a change in sales volume.

1.6 CONCEPTUAL FRAMEWORK

Promotion has been identified as one of the elements of an organization's marketing mix that

influence its customers. This makes it stand out in the famous traditional 4Ps amongst others that

include Product, Price and Place. The model to be adopted will emphasize Promotion to include

Advertising, Sales Promotion, Personal Selling, Publicity and Public Relations. These, combined

have an effect in terms of making customers to buy the products.

1.7 JUSTIFICATION AND SIGNIFICANCE OF THE STUDY

The study is likely to benefit several parties including scholars, marketing, and Operation

division to reach and serve as many customers as possible. The findings from the study may be a

base for promotional decisions. The findings of the study should act as a guideline in the making

effective management decision.

2

CHAPTER-2

2.0 INDUSTRY PROFILE

Retail consists of the sale of goods or merchandise from a fixed location, such as a

department store, boutique or mall, in small or individual lots for direct consumption by the

purchaser. Retailing may include subordinated services, such as delivery. Purchasers may be

individuals or businesses. In commerce, a ‘retailer’ buys goods or products in large quantities to

the end-user. Retail establishments are often called shops or stores. Retailers are at the end of the

supply chain. Manufacturing marketers see the process of retailing as a necessary part of their

overall distribution strategy.

2.1 Retail Sector

The retail sector in India is witnessing a huge revamping exercise as traditional markets

make way for new formats such as departmental stores, hypermarkets, supermarkets and

specialty stores. Western-style malls have begun appearing in metros and Tier-2 cities alike

introducing the Indian consumer to a shopping experience like never before. The sector is at an

inflexion point where the growth of organised retailing and growth in the consumption by the

Indian population is going to take a higher growth trajectory. The Indian population is witnessing

a significant change in its demographics. Organised retail is on all-time high in India.

Retailing consists of the location sale of goods or merchandise from a very fixed location,

such as a department store, by mall, in small or individual lots direct consumption by the

purchaser. Retailing may include subordinated services, such as delivery. Retail is usually

classified by type of products as follows:

Food products

Hard Goods – Appliances, Electronics, Furniture, etc

Soft Goods- clothing, apparel, and other fabrics.

There are the following retailers by marketing strategy:

Departmental stores - very large stores offering a huge assortment of soft and hard goods

Supermarkets - Is a self-service store consisting mainly of grocery and limited products

on non-food items. Sells mostly food products

3

Warehouse stores - warehouses that offer low-cost, often high quantity goods piled on

pallets or steel shelves, warehouse clubs charge a membership fee.

General stores - A rural store that supplies the main needs for the local community.

Convenience stores - Is essentially found in residential areas. They provide limited

amount of merchandise at more than average prices with a speedy checkout. This store is

ideal for the emergency and immediate purchases.

Hypermarkets - provides variety and huge volumes of exclusive merchandise at low

margins. The operating cost is comparatively less than other retail formats.

Malls - range of retail shops at a single outlet.

Indian retail market is expected to grow at a CAGR of 13% till 2018

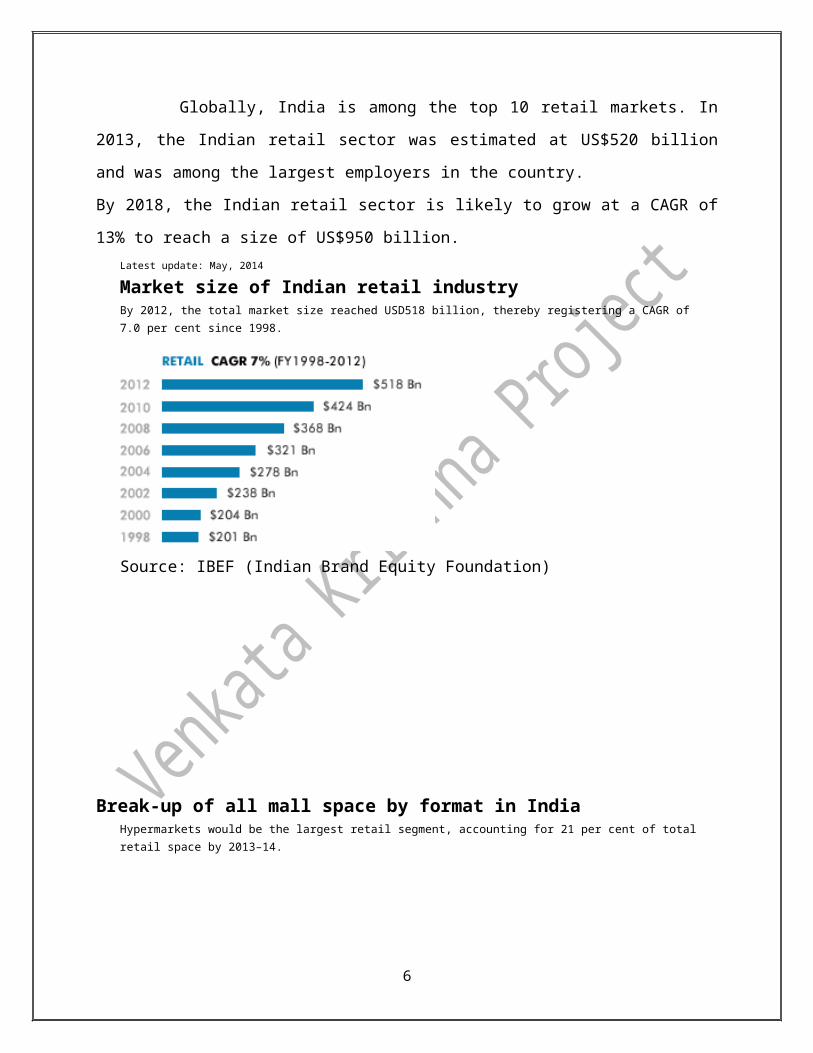

Globally, India is among the top 10 retail markets. In 2013, the Indian retail sector was

estimated at US$520 billion and was among the largest employers in the country.

By 2018, the Indian retail sector is likely to grow at a CAGR of 13% to reach a size of US$950

billion.Latest update: May, 2014

Market size of Indian retail industryBy 2012, the total market size reached USD518 billion, thereby registering a CAGR of 7.0 per cent since 1998.

Source: IBEF (Indian Brand Equity Foundation)

4

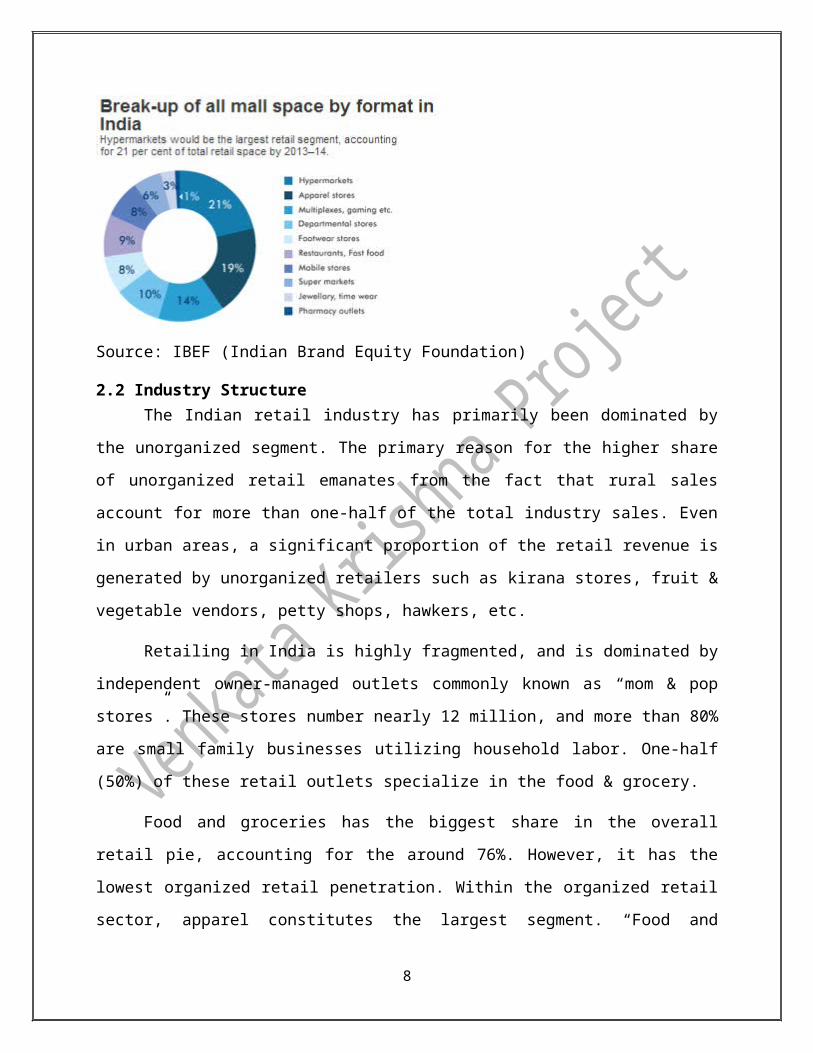

Break-up of all mall space by format in IndiaHypermarkets would be the largest retail segment, accounting for 21 per cent of total retail space by 2013–14.

Source: IBEF (Indian Brand Equity Foundation)

Organized retail market in India is burgeoning and is expected to grow at CAGR of 19-20% over the next 5 years

The Indian retail sector is set to grow rapidly with a gradual shift toward organized Retailing

formats. Organized retail penetration is expected to increase from 7.5% in 2013 to 10% in 2018

at a robust CAGR of 19-20% during the same period.

This will be driven by a combination of demand, supply and regulatory factors, which are

expected to be the growth engines of the Indian consumer and retail market.

Source: IBEF (Indian Brand Equity Foundation)

5

Source: IBEF (Indian Brand Equity Foundation)

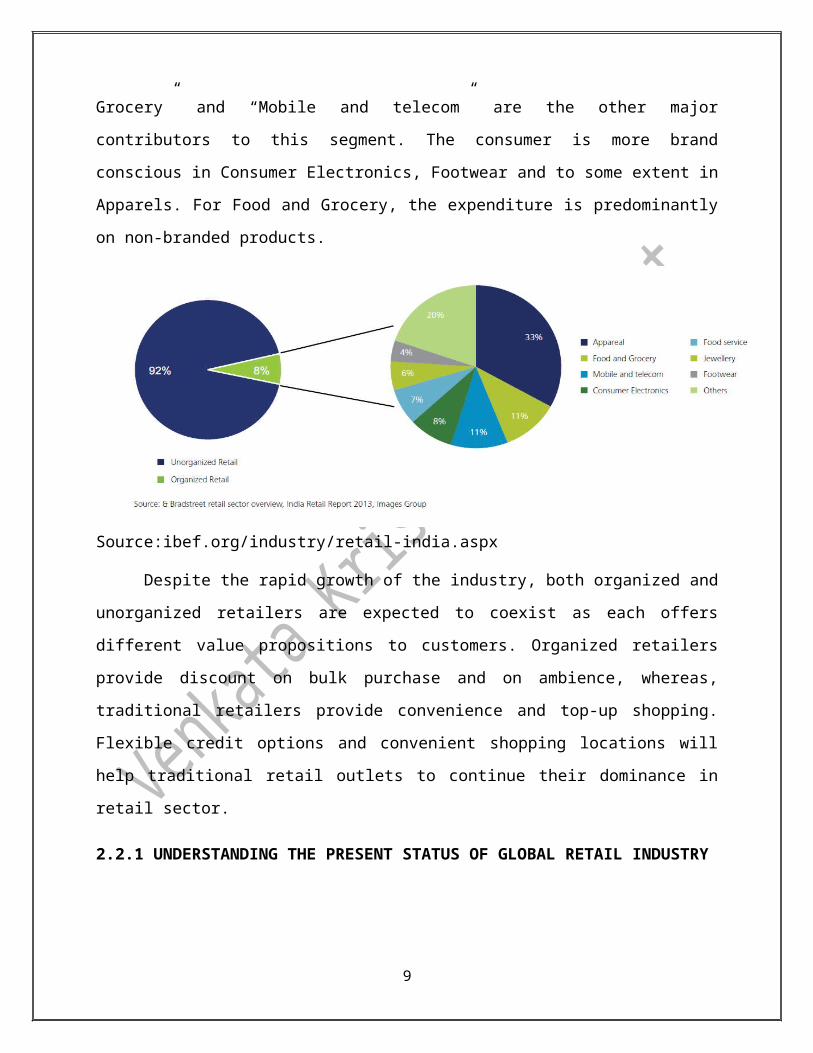

2.2 Industry StructureThe Indian retail industry has primarily been dominated by the unorganized segment. The

primary reason for the higher share of unorganized retail emanates from the fact that rural sales

account for more than one-half of the total industry sales. Even in urban areas, a significant

proportion of the retail revenue is generated by unorganized retailers such as kirana stores, fruit

& vegetable vendors, petty shops, hawkers, etc.

Retailing in India is highly fragmented, and is dominated by independent owner-managed

outlets commonly known as “mom & pop stores”. These stores number nearly 12 million, and

more than 80% are small family businesses utilizing household labor. One-half (50%) of these

retail outlets specialize in the food & grocery.

Food and groceries has the biggest share in the overall retail pie, accounting for the

around 76%. However, it has the lowest organized retail penetration. Within the organized retail

sector, apparel constitutes the largest segment. “Food and Grocery” and “Mobile and telecom”

are the other major contributors to this segment. The consumer is more brand conscious in

Consumer Electronics, Footwear and to some extent in Apparels. For Food and Grocery, the

expenditure is predominantly on non-branded products.

6

Source:ibef.org/industry/retail-india.aspx

Despite the rapid growth of the industry, both organized and unorganized retailers are

expected to coexist as each offers different value propositions to customers. Organized retailers

provide discount on bulk purchase and on ambience, whereas, traditional retailers provide

convenience and top-up shopping. Flexible credit options and convenient shopping locations will

help traditional retail outlets to continue their dominance in retail sector.

2.2.1 UNDERSTANDING THE PRESENT STATUS OF GLOBAL RETAIL INDUSTRY

It’s not all good news, however. Respondents in India most often cite inflation as a threat

to domestic growth, with commodity and energy prices identified as the primary factors that

make it a risk. Inflation is also top of mind in Latin America, where 53 percent of respondents

say it’s a risk, compared with the global average of 21 percent. And while most executives in

India expect their inflation rate will stay the same or decrease over the next six months, those in

Latin America and developed Asia

Australia, Hong Kong, Japan, New Zealand, the Philippines, Singapore, South Korea, and

Taiwan are the most likely to expect inflation rates in their countries will increase. Across

regions, many executives agree that economic conditions are improving and will continue to do

so in the coming months. At the country level, they are twice more likely to say current

conditions at home have improved than to say conditions have worsened. Looking ahead, 53

percent expect conditions will improve in the next six months. While geopolitical instability still

poses the biggest threat to global growth.

7

Sixty percent of all respondents cite geopolitical instability as a top risk to global

economic growth in the next 12 months. During the week the survey was in the field, a group of

militants defeated Iraqi military forces and took control of Mosul, the country’s second-largest

city—one week after militants invaded Samarra, another city in Iraq as it did in March,

executives maintain a positive view of conditions—both current and future—in the world

economy. In most geography, respondent’s views on current global conditions have either met or

surpassed their expectations from six months ago.

In most regions, assessments of the global economy either meet or exceed earlier expectations.

Source: McKinsey & Company Global Survey

8

CHAPTER-3

COMPANY PROFILE

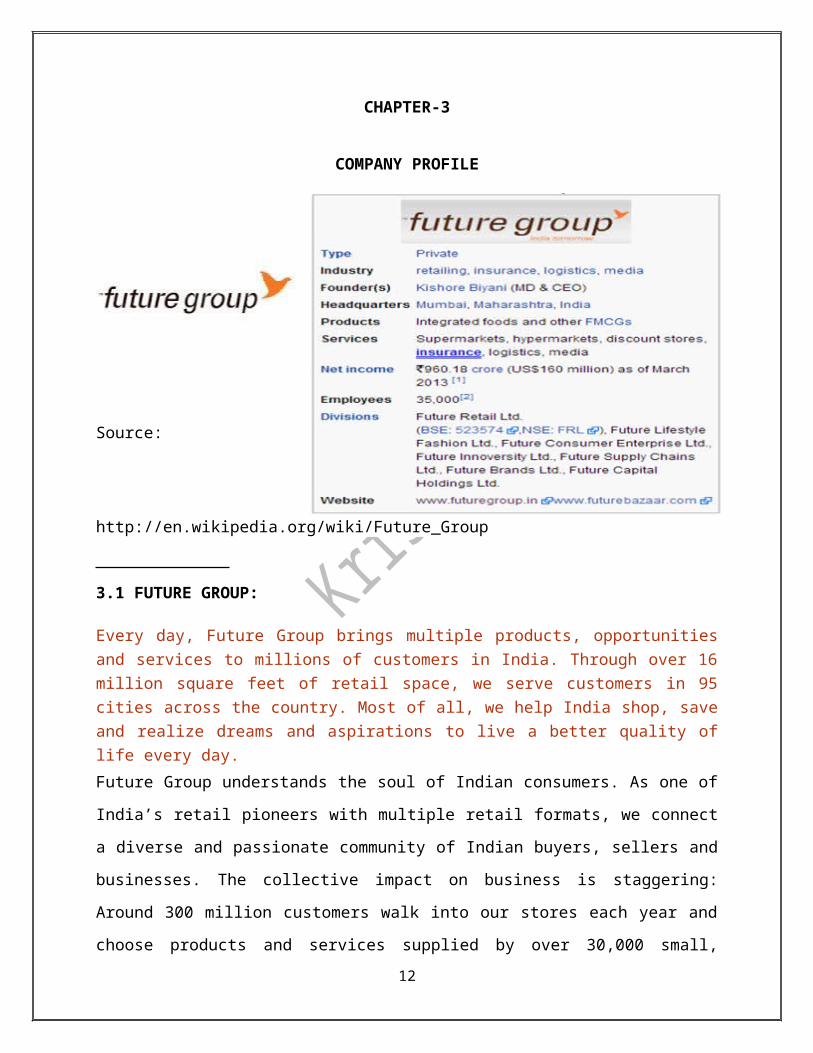

Source: http://en.wikipedia.org/wiki/Future_Group

3.1 FUTURE GROUP:

Every day, Future Group brings multiple products, opportunities and services to millions of

customers in India. Through over 16 million square feet of retail space, we serve customers in 95

cities across the country. Most of all, we help India shop, save and realize dreams and aspirations

to live a better quality of life every day.

Future Group understands the soul of Indian consumers. As one of India’s retail pioneers with

multiple retail formats, we connect a diverse and passionate community of Indian buyers, sellers

and businesses. The collective impact on business is staggering: Around 300 million customers

walk into our stores each year and choose products and services supplied by over 30,000 small,

medium and large entrepreneurs and manufacturers from across India. And this number is set to

grow.

Future Group employs 30,000 people directly from every section of our society. We source our

supplies from enterprises across the country, creating fresh employment, impacting livelihoods,

empowering local communities and fostering mutual growth.

9

We believe in the ‘Indian dream’ and have aligned our business practices to our larger objective

of being a premier catalyst in India’s consumption-led growth story. Working towards this end,

we are ushering positive socio-economic changes in communities to help the Indian dream fly

high and the ‘Sone Ki Chidiya’ soar once again. This approach remains embedded in our ethos

even as we rapidly expand our footprints deeper into India.

About Future Group

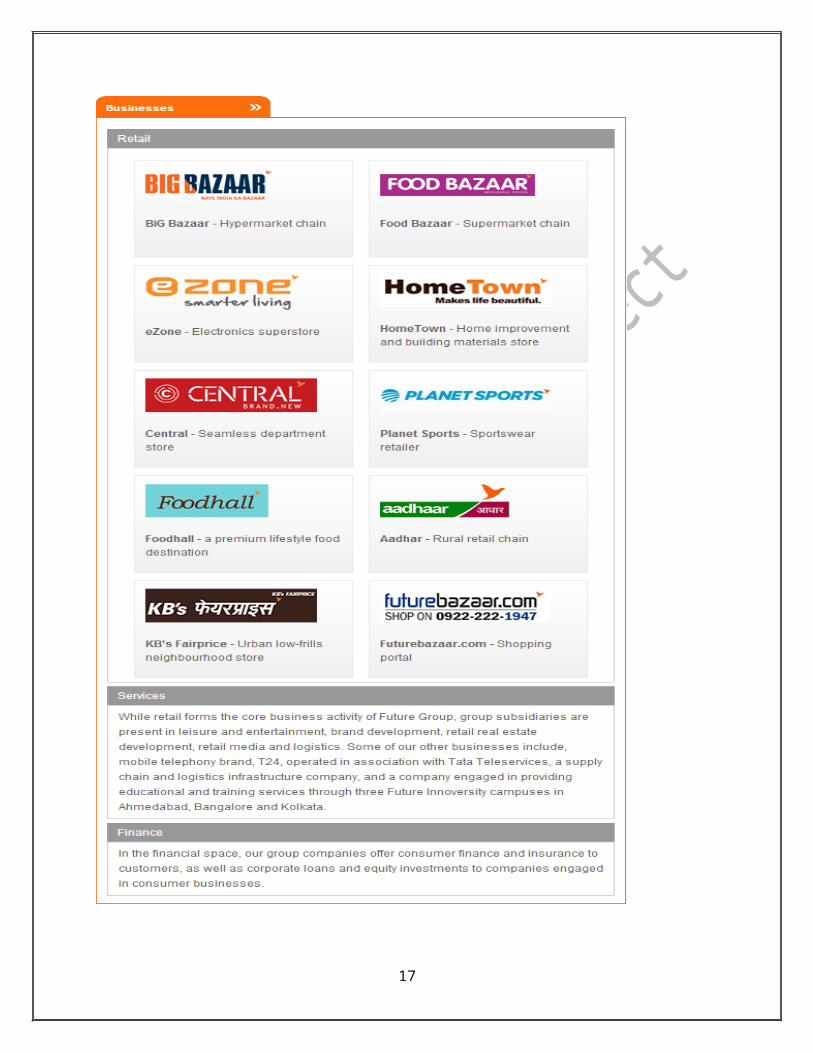

Big Bazaar is part of the retail network of Future Group. Future Group operates some of India’s

most popular retail chains including Pantaloons, Central, Big Bazaar, Food Bazaar, Home Town

and eZone and also has allied businesses in consumer finance, life and non-life insurance,

logistics infrastructure and supply chain and brand development. The group operates over 17

million square feet of retail space in over 90 cities and towns and 60 rural locations across India.

The group’s retail formats connect over 300 million customers to over 30,000 small, medium and

large enterprises that supply products and services to its retail chains. Future Group believes in

developing strong insights on Indian consume

Retail

Winning the Hearts of Indian Consumers

Future Group was conceived as a force to drive domestic consumption and capture every

addressable need of Indian consumers.

Future Group makes every effort to delight its customers, tailoring store formats to changing

Indian lifestyles and adapting products and services to their desires.

The group is credited with creating some of India’s most popular retail chains. The 162-store

hypermarket chain, Big Bazaar is ranked amongst the top 3 service brands in the country by The

Nielsen Company. Other retail chains include, department store chain, Central, outlet stores

chain, Brand Factory, sportswear chain, Planet Sports, home improvement and consumer

durables chain, Home Town and Ezone, supermarket chain, Food Bazaar, convenience stores

chain, KB’s Fairprice and a growing rural distribution network through Aadhaar.

As modern retail drives fresh demand and consumption in new categories, our strategy is based

on a deep understanding of Indian consumers, the products they want, and making these products

10

available in every city, in every store format. Future Group offers innovative offerings at

affordable prices tailored to the needs of every Indian household.

Pioneers in the India’s retail space, our formats are household names in more than 95 cities

across the country

Our stores cover around 16 million square feet of retail space and attract around 300 million

customers each year

Future Retail Limited focuses on the hypermarket & supermarket business led by formats like

BB, FB, FBB, Food hall, Home town & eZone

Future Lifestyle fashion focuses on the fashion businesses with over 24 popular fashion brands

& retail formats like Central, Brand Factory, Planet Sports, I m in and all

Future Consumer Enterprise Ltd is group's integrated food company with Food & FMCG

brands & retail formats like KB’s fair price & Aadhar. It also has interest in Food Pa

3.1.1 The Future of Future Group

Organized retail is a new phenomenon in India and despite the downturns, the market is

growing exponentially, as economic growth brings more of India’s people into the consuming

classes and organized retail lures more and more existing shoppers into its open doors. By 2015,

more than 300 million shoppers are likely to patronize organized retail chains.

The growing middle class is an important factor contributing to the growth of retail in

India. By 2030, it is estimated that 91 million households will be ‘middle class’, up from 21

million today. Also by 2030, 570 million people are expected to live in cities, nearly twice the

population of the United States today.

Consumer markets in emerging market economies like India are growing rapidly owing to

robust economic growth. India's modern consumption level is set to double within five years to

US$ 1.5 trillion from the present level of US$ 750 billion. With India's large ‘young’ population

and high domestic consumption, the macro trends for the sector look favorable.

Online retail business is another format which has high potential for growth in the near

future. The online retail segment in India is growing at an annual rate of 35 per cent, which

would take its value from Rs 2,000 cr. (US$ 429.5 million) in 2011 to Rs 7,000 cr. (US$ 1.5

billion) by 2015.

11

12

3.1.2 Group VisionFuture Group shall deliver Everything, Everywhere, Every time for Every Indian Consumer in

the most profitable manner.

3.1.3 Group Mission

3.1.4 Core Values

13

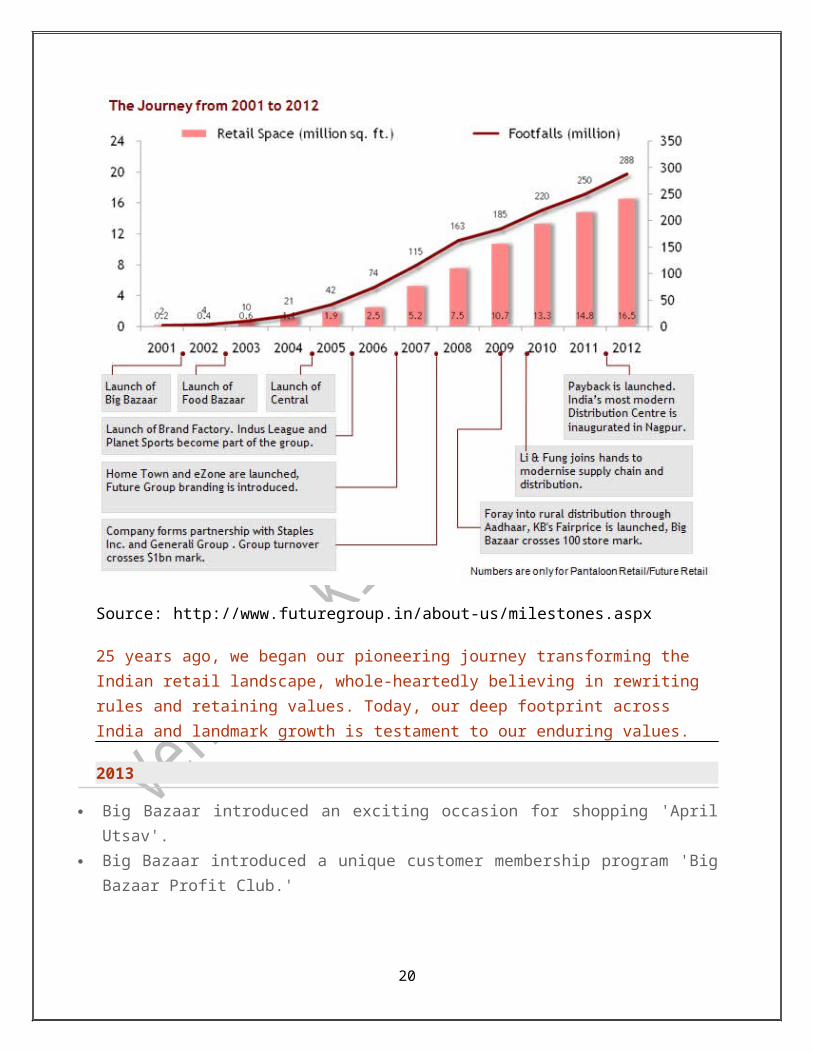

Source: http://www.futuregroup.in/about-us/milestones.aspx

25 years ago, we began our pioneering journey transforming the Indian retail landscape, whole-heartedly believing in rewriting rules and retaining values. Today, our deep footprint across India and landmark growth is testament to our enduring values.

2013

Big Bazaar introduced an exciting occasion for shopping 'April Utsav'.

Big Bazaar introduced a unique customer membership program 'Big Bazaar Profit Club.'

2011

April 2011 – KB's Fairprice celebrates opening its 200 stores in India

May 2011 – Future Supply Chains becomes ISO certified

14

2010

Future Group launches its telecom brand T24 in partnership with Tata Teleservices to provide

additional loyalty benefits to its customers.

Future Group connects over 4000 small and medium Indian manufacturers and entrepreneurs

with consumers.

2009

Future Group celebrates its first Shopping Festival across all retail formats in key Indian cities.

2008

Total operational retail space crosses the 10 million square feet mark.

Future Group acquires rural retail chain Aadhar from the Godrej Group, which has a presence in

65 rural locations.

Big Bazaar crosses the 100-store mark, marking one of the fastest expansions of the

hypermarket format anywhere in the world.

2007

Pantaloon Retail wins the International Retailer of the Year award at US-based National Retail

Federation convention in New York, and Emerging Retailer of the Year award at the World

Retail Congress held in Barcelona.

Future Group crosses the $1 billion turnover mark.

Specialized companies in retail media, logistics, IPR and brand development and retail-led

technology services become operational.

Online portal Futurebazaar.com becomes India's most popular shopping portal.

2006

Future Capital Holdings, the group's financial arm, is formed to manage over $1.5 billion in real

estate, private equity and retail infrastructure funds.

Future Group forms joint ventures with US office stationery retailer Staples.

Home Town, the home building and improvement products retail chain, is launched along with

consumer durables format eZone and furniture chain Furniture Bazaar.

2005

Future Group moves beyond retail and acquires a stake in Galaxy Entertainment, Indus League

Clothing and Planet Retail.

15

Future Group sets up Kshitij, India's first real estate investment fund, to build a chain of

shopping malls.

2004

Future Group launches India's first seamless mall, Central, in Bangalore.

2002

Food Bazaar, the supermarket chain is launched.

2001

Future Group launches three Big Bazaar stores within a span of 22 days in Kolkata, Bangalore

and Hyderabad.

1997

Future Group enters modern retail with the launch of the first 8000-sq. ft. store Pantaloons in

Kolkata.

1995

Future Group launches John Miller, a brand for Formal shirts.

1994

The Pantaloon Shoppe, Future Group's exclusive menswear store in a franchisee format is

launched across the nation. The company starts distribution of branded garments through multi-

brand retail outlets across the nation.

1992

Initial Public Offer (IPO) of shares by the Company

1991

BARE, an Indian denim brand is launched.

1987

The company is incorporated under the name of Manz Wear Private Ltd.

Pantaloons, one of India’s first formal trouser brands, are launched.

16

3.2 BIG BAZAAR

Big Bazaar is not just another

hypermarket. It caters to every need of your

family. Where Big Bazaar scores over other

stores is its value for money proposition for the

Indian customers.

Kishore Biyani led the company’s foray

into organized retail with the opening up of the

Big Bazaar in the year 2001.

It is a unit of Pantaloon Retail (India)

Ltd was started as a hypermarket format head

quartered in Jogeshwari, Mumbai with approx.

50,000 sqft of space. Its values and missions are to be the best in Value Retailing by providing

the cheapest prices.

It sells variety of merchandise at affordable rates, the prices of which it claims are lowest

in the city. Usually the items are clubbed together for offers as on the lines of Wal-Mart and

Carrefour, offer weekend discounts and works on the same economy model as Wal-Mart and has

considerable success in many Indian cities and small towns.

At Big Bazaar, you will definitely get the best products at the best prices - that’s what

they guarantee. It has also opened the doors into the world of fashion and general merchandise

including Home furnishings, utensils, crockery, cutlery, sports goods.

Wednesday Bazaar

The concept of Wednesday Bazaar was promoted as 'Hafte Ka Sabse Sasta Din' (Cheapest Day

of the Week). Initiated in January 2007, the idea behind this scheme was to draw customers to

stores on Wednesdays, the day when consumer presence is usually less. According to the chain,

the aim of the concept was 'to give Home Makers the power to save the most

Advertising campaigns and marketing initiatives

New logo

On the occasion of completion of ten (10) years in the Indian retail industry (in 2011) Big Bazaar

came up with a new logo for the company with a tag line that says: 'Naye India Ka Bazaar'

17

(Market for New India). This replaces the earlier tag line: 'Isse Sasta Aur accha Kahin Nahin'

(Nothing is Cheaper and good than Here).

Advertising initiatives

Big Bazaar has launched a promotion drive covering the three prime media, television, print and

social media, to mark the launch of the new logo. The media campaign was developed by Mudra

Communications.

3.2.1 Big Bazaar timeline

2001

Three stores launched within a span of 22 days in Kolkata, Bangalore and Hyderabad

2002

ICICI Bank Card is launched.

Food Bazaar becomes part of Big Bazaar with the launch of the first store in Mumbai at High

Street Phoenix

2003

Enters Tier II cities with the launch of the store in Nagpur

Welcomes its 10 millionth customer at its new store in Gurgaon

2004

Wins its first award and national recognition. Big Bazaar and Food Bazaar awarded the

country’s most admired retailer award in value retailing and food retailing segment at the

India Retail Forum

A day before Diwali, the store at Lower Parel becomes the first to touch Rs 10 million

turnover on a single day

2005

Implementation of SAP and pilots a RFID project at its central warehouse in Tarapur

Launch of a shopping program: the Big Bazaar Exchange Offer, inviting customers to

exchange household junk at Big Bazaar

Electronic Bazaar and Furniture Bazaar are launched

18

Big Bazaar and ICICI Bank launched ICICI Bank-Big Bazaar Gold credit card program to

reward its loyal customers

2006

Mohan Jadhav set a national record at Big Bazaar Sangli with a Rs 137,367 shopping bill

The Sangli farmer becomes Big Bazaar’s largest ever customer

Launches Shakti, India’s first credit card program tailored for housewives

Navaras – the jewellery store launched within Big Bazaar stores

2007

The 50th Big Bazaar store is launched in Kanpur

Partners with Futurebazaar.com to launch India's most popular shopping portal

Initiates the "Power of One" campaign to help raise funds for the Save The Children India

Fund

Pantaloon Retail wins the International Retailer of the Year at US-based National Retail

Federation convention in New York and Emerging Retailer of the Year award at the World

Retail Congress held in Barcelona

2008

New section, Fashion@BigBazaar, starts

Voted among the top ten service brands in the country in the latest Pitch-IMRB international

survey

Initiates the Mega Saving "Monthly Bachat Bazaar" campaign, to provide deals on groceries

and food items during the first week of every month

2009

Opens its second store in Assam at Tinsukia

Initiates Maha Annasantarpane program at its stores in South India – an initiative to offer

meals to visitors and support local social organizations

Mahendra Singh Dhoni and Asin, youth icons of India, were chosen as the brand

ambassadors of Big Bazaar

Announced the launch of 'The Great Exchange Offer'

Formed a joint venture with Hidesign to launch Holii, a new brand of handbags, laptop bags

and other accessories

19

2010

Future Value Retail Limited is formed as a subsidiary to spearhead the group’s value

retail business through Big Bazaar, Food Bazaar and other formats

Wins CNBC Awaaz Consumer Awards for the third consecutive year. Adjudged the Most

Preferred Multi Brand Food & Beverage Chain, Most Preferred Multi Brand Retail Outlet

and Most Preferred Multi Brand One Stop Shop

Opens its third store in Kanpur at Z Square Mall

Vidya Balan was chosen as the brand ambassador of Big Bazaar's Price Challenge exercise

Ranked six among the Top 50 Service Brands in India

2011

Enters the rural wholesale and distribution business through 'Aadhaar Wholesale' store at

Kalol, Gujarat

Big Bazaar has come up a new logo with a new tag line: 'Naye India Ka Bazaar'

200th store opened in India

Future Group launched Food hall – a premium food destination across 10 metros in India

Entered into an agreement with Hindustan Unilever to co-develop and co-brand bakery

products, which would be sold exclusively at Big Bazaar stores

2012

Entered into a five-year multi-million dollar deal with Cognizant Technology Solutions for

IT infrastructure services that support Future Group's network of stores, warehouses, offices,

and data centers

Sakshi Tanwar & Ram Kapoor chosen brand ambassadors to promote more turnover

Partnered with Disney to launch "Kidz Cookies" for kids across India

20

CHAPTER-4

LITERATURE REVIEW

Awareness Building and Lead Generation, Marketing's Dynamic Duo

A well rounded marketing communications plan contains programs for awareness building and

sales lead generation. To maximize the effectiveness of your programs, they should be

coordinated, and based on a strategic plan that comprehends your business goals.

An awareness building program can:

Shorten your sales cycle by letting audiences know you exist and offer something they want.

Educate prospective customers that your products or services meet their needs.

Decrease your prospects’ perception of risk in selecting you as a vendor.

Awareness Building:

In this first article in a series of two, we concentrate specifically on awareness building. For this,

we discuss using coordinated advertising and PR tactics.

Profile your target audiences:

When setting out to profile your prospective customers, make sure you recognize that there’s a

difference between a customer and a market. A market is an aggregate of customers that has

needs in common, but it’s a customer that actually pays you for your product or service. At the

end of the day, individual customers are whom you must influence.

Questions that you should be able to answer about your prospective customers include:

How many of them are there?

How easy is it to identify them (company type and point of entry)? Do you have their

contact information?

What are their hot buttons or pain points and how does your product or service relate to

them?

How do they make decisions?

Where do they get their information?

Can you address them as a group?

Do they know you?

Are competitive solutions entrenched?

21

Where are they currently in their purchasing process and relationship with you?

Select your communications media

Sales and marketing can be described as the process of bringing prospects and then customers

closer to you. The vehicles you choose to communicate can make a big difference in whether

your message gets through. Time spent understanding how customers get their information and

the role that information sources play in purchase decision making can have a critical effect on

the success of marketing programs.

4.1 Marketing - Promotion StrategyPromotion is the method you use to spread the word about your product or service to customers,

stakeholders and the broader public.

1. Advertising

What is Advertising?

Advertising is a form of communication designed to persuade potential customers to choose your

product or service over that of a competitor.

It should be a planned, consistent activity that keeps the name of your business and the benefits

of your products or services uppermost in the mind of the consumer.

Why Advertise?

Advertising aims to:

Make your business and product name familiar to the public Create goodwill and build a favorable image Educate and inform the public Offer specific products or services Attract customers to find out more about your product or service

Aim - What is the primary purpose of the advertisement? Is it to inform, sell, produce listings or

improve the image of your business?

Target - Who is the target? From which sector of the public are you trying to achieve a

response? For example is it male, female, adult, teenager, child, mother, father etc.

22

Media – Bearing the aim and target in mind, which of the media available to you is the most

suitable – i.e. TV, radio, press or Internet?

Competitors – What are your competitors doing? Which media channel do they use? Are they

successful? Can you improve on their approach and beat them in competition?

Commonly used media

There are many media options open to advertisers. Which media you use will depend on who

you are trying to reach, what you want to say and your budget.

Stationery which includes letterheads, envelopes and business cards

Window display or office front The external presentation of your business office or shop is

one of the principal ways of establishing your business image

Press advertising This is a commonly used form of general advertising and includes

advertising in all press such as newspapers, magazines and journals

Radio is considered by many advertisers as an ideal medium due to its ability to reach

specific target groups.

Television is a powerful advertising medium because it creates impact through sight, sound

and movement.

Direct mail this is a broad category covering direct communication with the consumer

through email, post or fax

Outdoor this is any type of advertising which is done outdoors, including static advertising

such as billboards, backs of street benches and bus shelters or mobile advertising displayed

on buses, trains, taxis or towed signage

Point of Sale advertising at the point where the consumer makes a purchase decision eg:

floor stickers, in-store digital advertising

Online The options for online advertising continue to grow rapidly. They include advertising

on your website, advertising on other websites, creating links to your website from other

websites, publishing blogs, offering online product games, social networks and forums.

Directory listings Many consumers use business directories to find a supplier. Directories

include the yellow or white pages, union directories, trade directories or local business

directories.

23

Evaluating the effectiveness of your advertising

Famous American department store merchant John Wanamaker (1838-1922) was attributed as

saying “Half the money I spend on advertising is wasted – the trouble is I don’t know which

half.” This quote is often still true today as many businesses do not evaluate the effectiveness of

their advertising.

Evaluating effectiveness can be as simple as staff asking every new customer “How did you hear

about us?” or asking every customer that responds to an advertised special “where did you see or

hear our advertisement?”

Whatever method you use, it is absolutely critical in getting top value for your advertising dollar

by finding out which media works and which doesn't.

2. Selling

What is selling?

Put simply, selling is the exchange of goods or services for an agreed sum of money.

Prospecting and qualifying – identifying qualified prospects ie: those that are likely to want or

need your product or service and can afford to pay for it.

Pre-approach – undertaking research about prospects to assist in the actual selling process.

Approach – making actual contact with the prospect in person, by phone or in writing.

Presentation and demonstration – presenting and demonstrating the features and benefits of

your product or service in order to convince the prospect that their want or need can be satisfied.

Handling objections – demonstrating the product or service value to overcome real or perceived

objections or misunderstandings that are impeding the purchase decision.

Closing – bringing the selling process to a successful conclusion by either asking for the order or

responding to a positive decision from the prospect.

Follow-up – proactive or reactive contact with the purchaser to establish their satisfaction level

and to address any problems that may exist.

24

In planning the selling element of your marketing strategy you will need to consider the

following:

The size and structure of your sales team

Recruiting, training, motivating and evaluating individuals and the team as a whole

The remuneration structure

The location/territory to be serviced

Management and communication systems

Selling is a particularly important element if you are marketing services because the purchaser

of a professional service is in fact buying the capabilities of the seller.

What is sales promotion?

Sales promotion relates to short term incentives or activities that encourage the purchase or sale

of a product or service. Sales promotions initiatives are often referred to as “below the line”

activities.

What are the major sales promotion activities?

Sales promotion activities can be targeted toward final buyers (consumer promotions), business

customers (business promotions), retailers and wholesalers (trade promotions) and members of

the sales force (sales force promotions). Here are some typical sales promotion activities:

3. Public Relations

What are public relations?

The Public Relations Institute of Australia (PRIA) defines Public Relations (PR) as: “The

deliberate, planned and sustained effort to establish and maintain mutual understanding between

an organization (or individual) and its (or their) publics”.

Put more simply, public relations is about building good relations with the stakeholders (public)

of your business by obtaining favorable publicity, building a good corporate image and handling

or heading off unfavorable rumors’, stories and events.

25

By building good relationships with your stakeholders, particularly customers, you can generate

positive word of mouth and referrals from satisfied customers.

What are the main public relations tools?

Typical PR tools include:

News creation and distribution (media releases)

Special events such as news conferences, grand openings and product launches

Speeches and presentations

Educational programs

Annual reports, brochures, newsletters, magazines and AV presentations

Community activities and sponsorships

What are the key steps in implementing public relations?

Implementing effective public relations activities requires careful planning. The three major

steps are outlined below

Setting the objectives

Deciding on the message and the vehicle

Evaluating the results

The Stages of Perception in Marketing

by Vanessa Cross, Demand Media

Perception establishes the meaning about a product or brand when a consumer makes initial

contact. In marketing, this is described as consumer information processing. At this stage all of

the senses are engaged in receiving brand marketing communicate messages. In marketing

literature, four distinct stages of perception occur during consumer information processing:

sensation, attention, interpretation and retention.

Sensation:

Sensation describes what occurs when a person's senses are initially exposed to the external

stimulus of a product or brand marketing. Background music and a unique store design round out

26

the experience of the taste of hot or cold coffee and food products that can be enjoyed in-store at

quaint cafe tables.

Attention:

Attention occurs when a person lingers and gives mental processing capacity to the external

stimulus from a product or brand. Selective perception is when a consumer pays attention to

messages that are consistent with her attitudes, beliefs and needs.

Interpretation:

Interpretation occurs when a person assigns a meaning to the sensory stimulus from a product or

brand marketing. Comprehension is aided by expectations and familiarity.

Retention:

The conclusion of the consumer perception process is the retention stage. This is marked by the

storage of product or brand information in short-term and long-term memory.

4.2 Consumer Perception Theory:

by Chris Blank, Demand Media

Merchants aim to increase their sales by determining what drives their customers' purchase

decisions. Consumer perception theory attempts to explain consumer behavior by analyzing

motivations for buying -- or not buying -- particular items. Three areas of consumer perception

theory relate to consumer perception theory: self perception, price perception and perception of a

benefit to quality of life.

Definition:

Consumer perception applies the concept of sensory perception to marketing and advertising.

Just as sensory perception relates to how humans perceive and process sensory stimuli through

their five senses, consumer perception pertains to how individuals form opinions about

companies and the merchandise they offer through the purchases they make. Merchants apply

consumer perception theory to determine how their customers perceive them. They also use

27

consumer perception theory to develop marketing and advertising strategies intended to retain

current customers -- and attract new ones.

Self Perception:

Self perception theory attempts to explain how individuals develop an understanding of the

motivations behind their own behavior. Self perception by customers relates to values and

motivations that drive buying behavior -- which is also an important aspect of consumer

perception theory.

Price Perception:

While mass merchandisers such as Wal-Mart emphasize low prices as an inherent virtue, upscale

merchants attempt to emphasize quality and value for money to appeal to potential customers.

Researchers at the School of Business Administration at LaSalle University and LeBow College

of Business at Drexel University considered several factors, including price perception --

whether consumers believed they were being charged fair prices -- in determining whether online

shoppers would make repeat purchases through the same website.

Benefit Perception:

"It's good, and it's good for you." Many consumers are familiar with this phrase frequently

associated with food advertising. Researchers from Marquette University, Louisiana State

University and the University of Arkansas surveyed customers to determine how nutrition claims

associated with food affected their perception of that food's nutritional value.

4.3 Customer Satisfaction

Customer satisfaction can help your business to achieve a sustainable competitive advantage. It

is about understanding the way a customer feels after purchasing a product or service and, in

particular, whether or not that product or service met the customer’s expectations.

Customers primarily from their expectations through past purchasing experiences, word-of-

mouth from family, friends and colleagues and information delivered through marketing

28

activities, such as advertising or public relations. If the customer’s expectation isn’t met, they

will be dissatisfied and it’s very likely they will tell others about their experience.

Why customer satisfaction is important

Don’t underestimate the value of customer satisfaction. It’s becoming an important area of

competition.

A high level of satisfaction can deliver many benefits, including:

Loyalty: a highly satisfied customer is a loyal customer

Repeat purchase: a highly satisfied customer buys more products

Referrals: a highly satisfied customer tells their family and friends about the product or

service

Retention: a highly satisfied customer is less likely to switch brands

Reduced costs: a highly satisfied customer costs less to serve than a new customer

Premium prices: a highly satisfied customer is willing to pay more for the product or

service

Customer satisfaction research

Satisfaction surveys are an important method for collecting information about how your

customers think and feel about your brand, product or service.

A satisfaction survey can help you to understand the expectations of your customers, determine

whether your customers believe you are meeting those expectations, identify new customer

requirements or trends in the market and determine what areas of your business need investment.

4.4 Competitive EdgeBy differentiating your product, service, personnel or brand, you can establish a unique position

in your market.

The following strategies can help to distinguish your offering in the market and create a

competitive edge.

Be first in the market

Leverage your expertise: Establish leadership

Focus your market expertise

Make your products stand out as new and improved

29

How to maintain your competitive edge

Once you have defined your competitive edge, you must work to maintain that upper hand. Your

competitors will constantly work to improve their products and build their expertise, and so

should you.

What is not a competitive edge?

Avoid focusing on the following areas or characteristics, as they will not set you apart from your

competition.

Quality and Customer Orientation

Although it is important to manufacture good quality products and be customer-oriented, these

factors will not set you apart from the competition.

Customer Service

It is assumed that you will work diligently to ensure customer satisfaction. This alone will not

keep those customers coming back to you.

Price

Although pricing your products below market price might attract some buyers, it will not

differentiate your product for long. Being cheaper than an alternative will not position you as

unique. It will place you in a weak position because your competition could change their price to

match yours at any time.

Breadth of Line

Based on the success of “superstores,” you might be tempted to become “everything to

everyone.” However, this is not differentiation. You might solve some problems for some

customers, but it is more likely that you will not fully solve any customers’ problems.

Provide a specific solution to ensure that you solve real problems for a specific target market.

30

CHAPTER -5

RESEARCH METHODOLOG

Data Source : Primary Data - from questionnaire and personal interaction

Secondary Data – old records, Internet

Research approach : Survey method

Research Instrument : Questionnaire

Sample plan : Personal Interview

Sample unit : Customers of Big Bazaar and Nearby Areas

Sampling method : Convenience sampling

Sample Size : 336 Respondents

Data Interpretation : Percentage method

DURATION OF PROJECT

Duration of the Project 20th May 2014 to 5th July 2014.

5.1 DATA COLLECTIONThis section was basically divided to address 3 areas: Sources of data, data collection methods

and data collection instruments.

5.1.1 Data Collection Sources

Data was collected from the following two main sources.

1) Primary Data and 2) Secondary Data.

Primary data was sourced directly from the respondents i.e. Customers

Secondary data was obtained from Journals such as those of Marketing and Consumer Research;

5.2 DATA PROCESSING AND ANALYSISThe data collected was processed and analyzed using the Statistical Package for Social Sciences

(SPSS) Software.

31

5.2.1 Data Processing

Processing involved classifying, coding, entering, editing and tabulating the data.

5.2.2 Data Analysis

Statistical analysis of historical data was used to assess promotional effectiveness. Primary data

analysis involved calculation of frequencies and percentages. This was followed by cross

tabulations and correlation studied through Pearson's Coefficient of partial correlation. The

findings were cross tabulated at a 0.05 level of significance with a view to establish relationships

between the variables under study. Multiple regression analysis was carried out to test the

strength of relationships since the study involved one dependent variable i.e. the decision to visit

(also the purchase decision) which is presumed to be a function of independent variables like

promotional activities, service quality.

32

DATA ANALYSIS

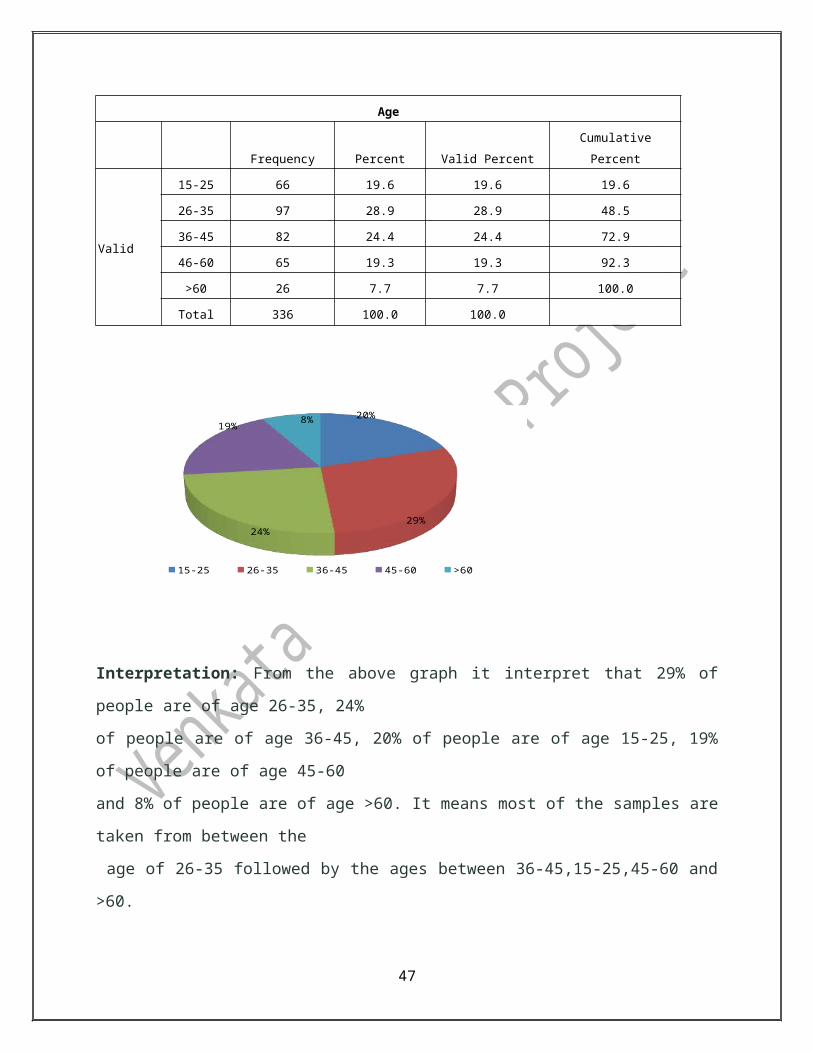

1) Frequency table for AGE:

Age

Frequency Percent Valid Percent Cumulative Percent

Valid

15-25 66 19.6 19.6 19.6

26-35 97 28.9 28.9 48.5

36-45 82 24.4 24.4 72.9

46-60 65 19.3 19.3 92.3

>60 26 7.7 7.7 100.0

Total 336 100.0 100.0

20%

29%24%

19%8%

15-25 26-35 36-45 45-60 >60

Interpretation: From the above graph it interpret that 29% of people are of age 26-35, 24%

of people are of age 36-45, 20% of people are of age 15-25, 19% of people are of age 45-60

and 8% of people are of age >60. It means most of the samples are taken from between the

age of 26-35 followed by the ages between 36-45,15-25,45-60 and >60.

33

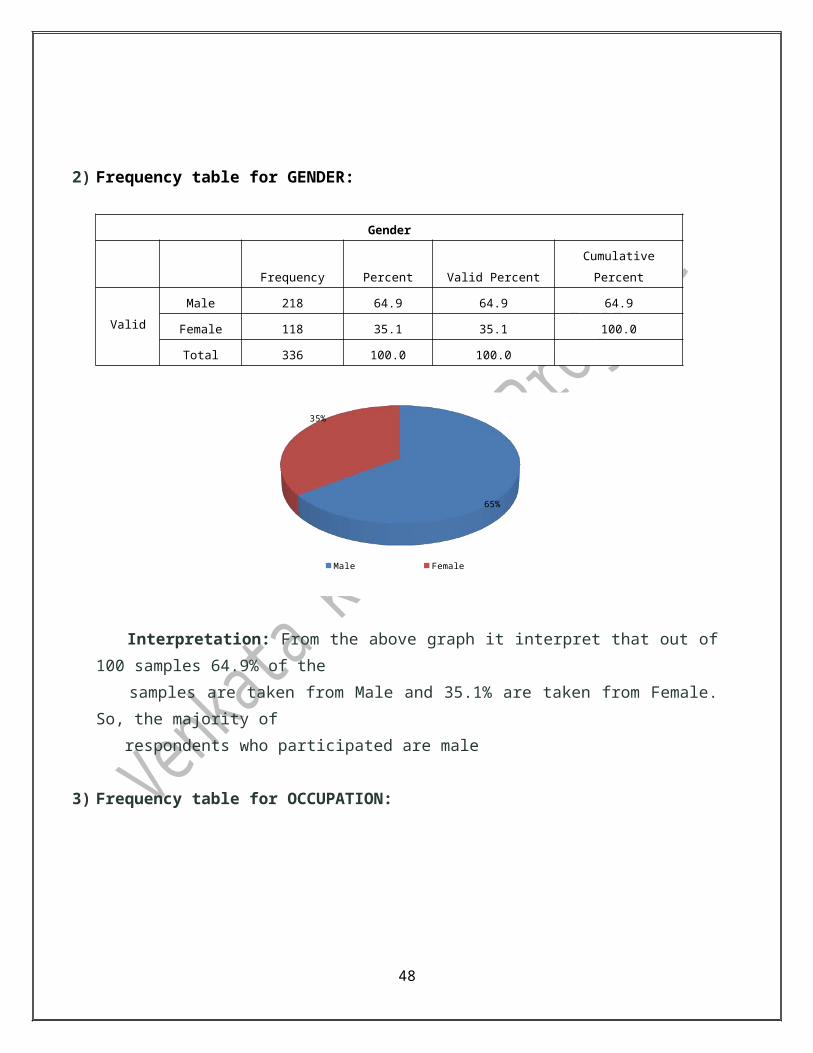

2) Frequency table for GENDER:

Gender

Frequency Percent Valid Percent Cumulative Percent

Valid

Male 218 64.9 64.9 64.9

Female 118 35.1 35.1 100.0

Total 336 100.0 100.0

65%

35%

Male Female

Interpretation: From the above graph it interpret that out of 100 samples 64.9% of the

samples are taken from Male and 35.1% are taken from Female. So, the majority of

respondents who participated are male

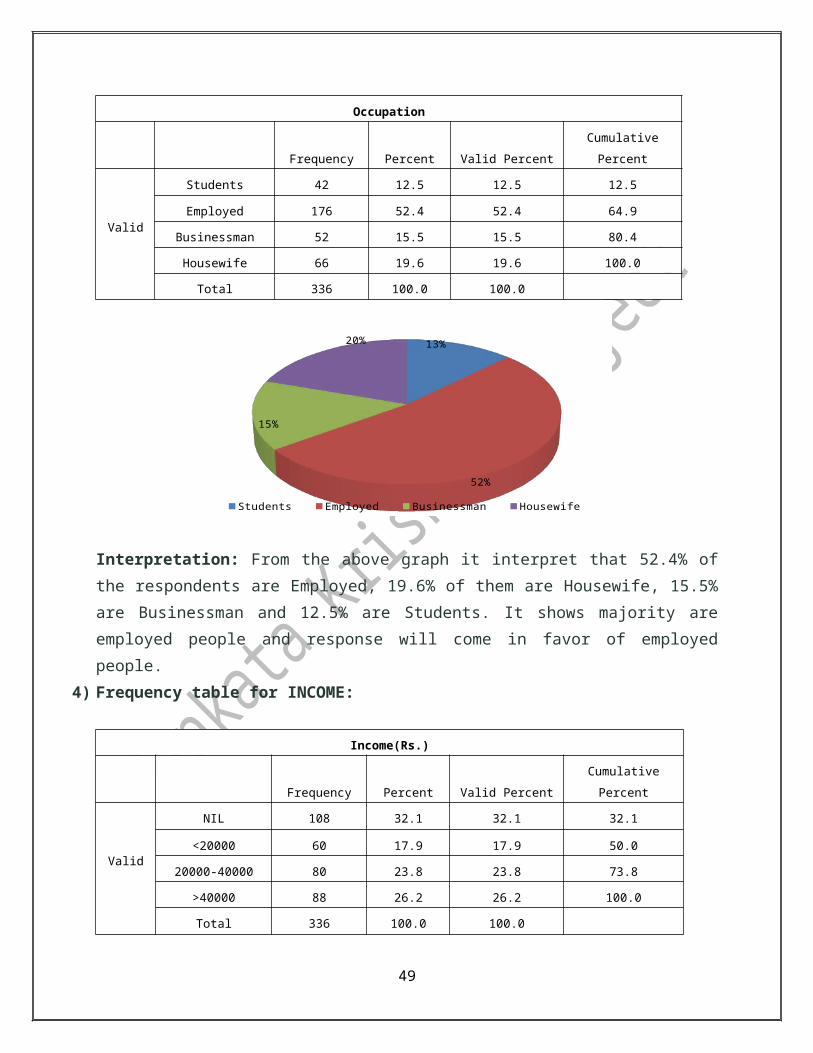

3) Frequency table for OCCUPATION:

Occupation

Frequency Percent Valid Percent Cumulative Percent

Valid

Students 42 12.5 12.5 12.5

Employed 176 52.4 52.4 64.9

Businessman 52 15.5 15.5 80.4

Housewife 66 19.6 19.6 100.0

Total 336 100.0 100.0

34

13%

52%

15%

20%

Students Employed Businessman Housewife

Interpretation: From the above graph it interpret that 52.4% of the respondents are Employed,

19.6% of them are Housewife, 15.5% are Businessman and 12.5% are Students. It shows

majority are employed people and response will come in favor of employed people.

4) Frequency table for INCOME:

Income(Rs.)

Frequency Percent Valid Percent Cumulative Percent

Valid

NIL 108 32.1 32.1 32.1

<20000 60 17.9 17.9 50.0

20000-40000 80 23.8 23.8 73.8

>40000 88 26.2 26.2 100.0

Total 336 100.0 100.0

32%

18%24%

26%

NIL Less than 20,000 20,000-40,000 More than 40,000

35

Interpretation: From the above graph it interpret that, majority of sample is taken from the

students with NIL income and followed by Middle income people and the income levels are

between <20,000 and 20,000 to 40,000.

5) Do you know about Kukatpally Big Bazaar?

(Yes / No)

Kukatpally BB?

Frequency Percent Valid Percent

Cumulative

Percent

Valid Yes 236 70.2 70.2 70.2

No 100 29.8 29.8 100.0

Total 336 100.0 100.0

70%

30%

Yes No

Interpretation: From the above graph it interpret that, 70.2% of the respondents are aware of

Kukatpally Big Bazaar and 29.8% of respondents are not aware of Kukatpally Big Bazaar

36

6) What is your perception about the Kukatpally Store?

FBB (Fashion at Big Bazaar) / Hypermarket (Variety of products under one roof)

Perception?

Frequency Percent Valid Percent

Cumulative

Percent

Valid FBB 5 1.5 2.1 2.1

Hypermarket 231 68.8 97.9 100.0

Total 236 70.2 100.0

Missing System 100 29.8

Total 336 100.0

1%

69%

30%

FBB Hypermarket Missing

Interpretation: From the above graph it interpret that, majority of respondents are aware about

the change from FBB to Hypermarket

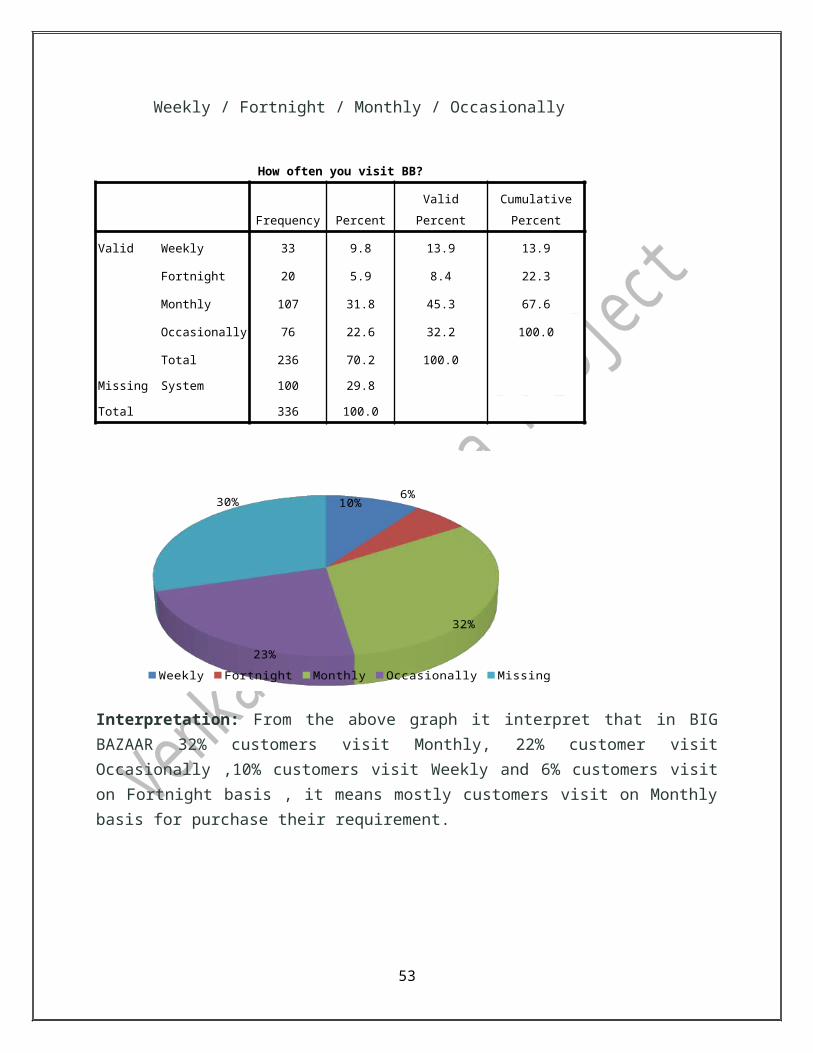

7) How often you visit Big Bazaar?

37

Weekly / Fortnight / Monthly / Occasionally

How often you visit BB?

Frequency Percent Valid Percent

Cumulative

Percent

Valid Weekly 33 9.8 13.9 13.9

Fortnight 20 5.9 8.4 22.3

Monthly 107 31.8 45.3 67.6

Occasionally 76 22.6 32.2 100.0

Total 236 70.2 100.0

Missing System 100 29.8

Total 336 100.0

10%6%

32%

23%

30%

Weekly Fortnight Monthly Occasionally Missing

Interpretation: From the above graph it interpret that in BIG BAZAAR 32% customers visit Monthly, 22% customer visit Occasionally ,10% customers visit Weekly and 6% customers visit on Fortnight basis , it means mostly customers visit on Monthly basis for purchase their requirement.

38

5.3.1 DATA ANALYSIS OF INSIDE

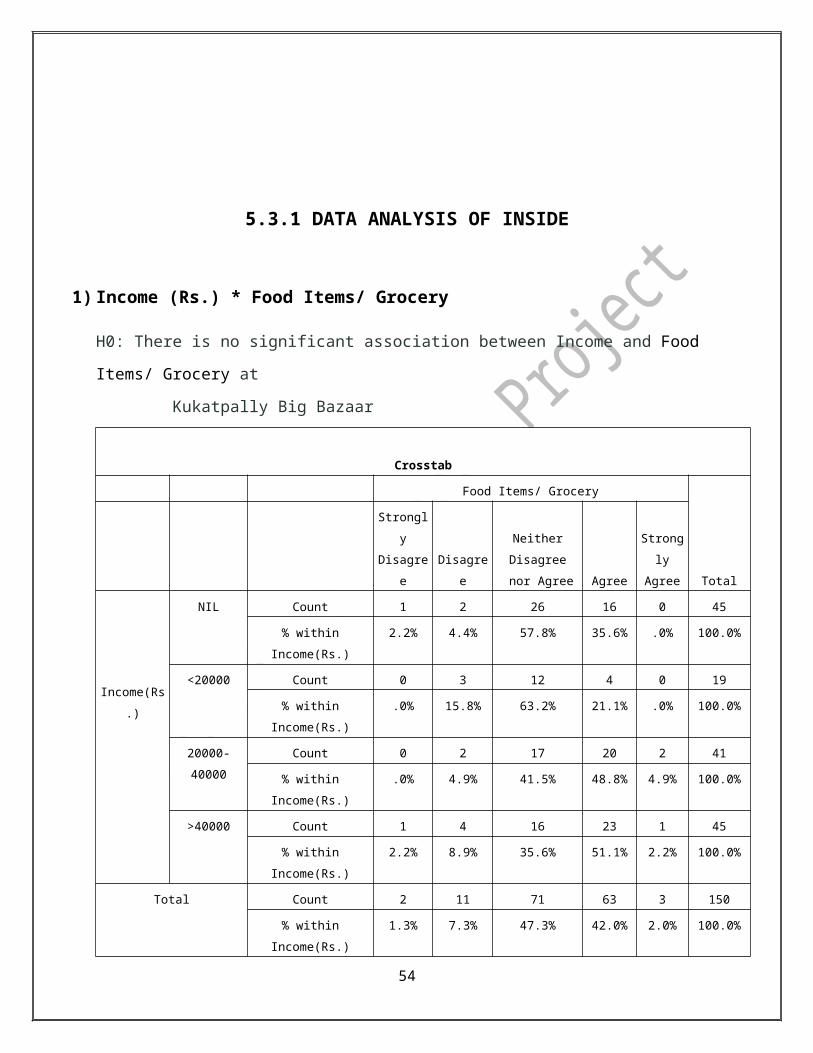

1) Income (Rs.) * Food Items/ Grocery

H0: There is no significant association between Income and Food Items/ Grocery at

Kukatpally Big Bazaar

Crosstab

Food Items/ Grocery

Total

Strongly

Disagree Disagree

Neither

Disagree

nor Agree Agree

Strongly

Agree

Income(Rs.)

NIL Count 1 2 26 16 0 45

% within Income(Rs.) 2.2% 4.4% 57.8% 35.6% .0% 100.0%

<20000 Count 0 3 12 4 0 19

% within Income(Rs.) .0% 15.8% 63.2% 21.1% .0% 100.0%

20000-40000 Count 0 2 17 20 2 41

% within Income(Rs.) .0% 4.9% 41.5% 48.8% 4.9% 100.0%

>40000 Count 1 4 16 23 1 45

% within Income(Rs.) 2.2% 8.9% 35.6% 51.1% 2.2% 100.0%

Total Count 2 11 71 63 3 150

% within Income(Rs.) 1.3% 7.3% 47.3% 42.0% 2.0% 100.0%

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 14.601a 12 .264

Likelihood Ratio 16.122 12 .186

Linear-by-Linear Association 2.678 1 .102

N of Valid Cases 150

12 cells (60.0%) have expected count less than 5. The minimum expected count is .25

39

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null

Hypothesis. There is no significant association between Income and Food Items/ Grocery at

Kukatpally Big Bazaar.

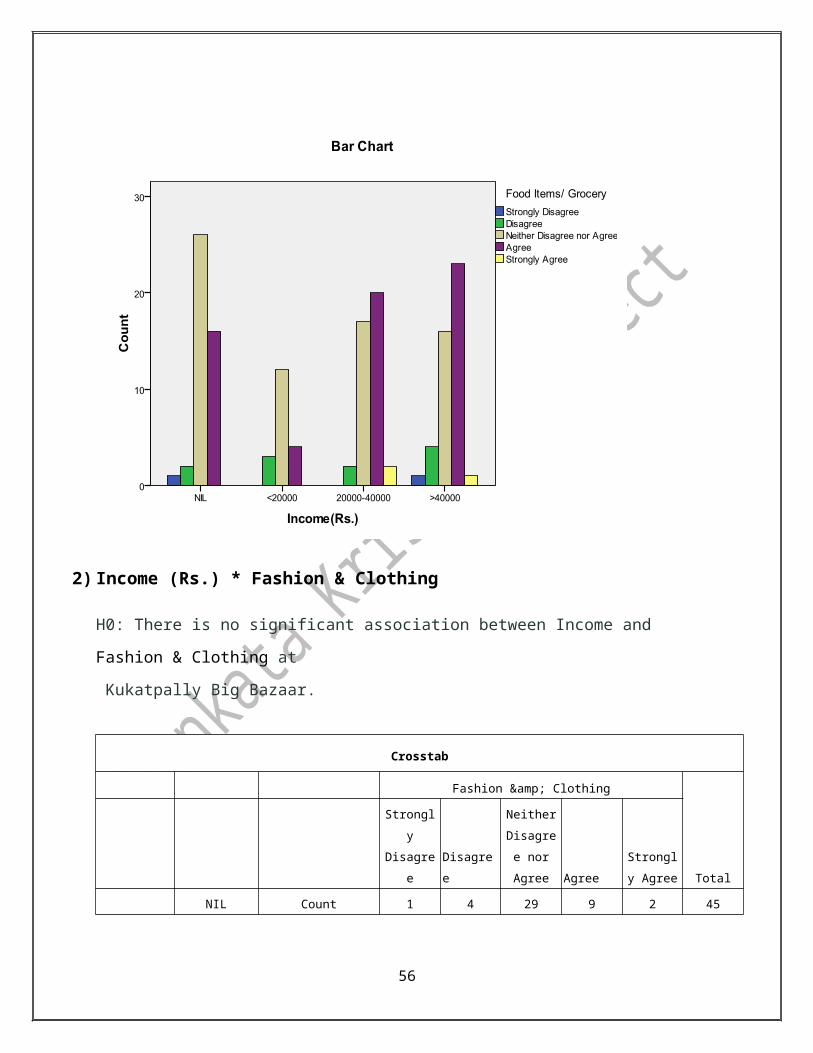

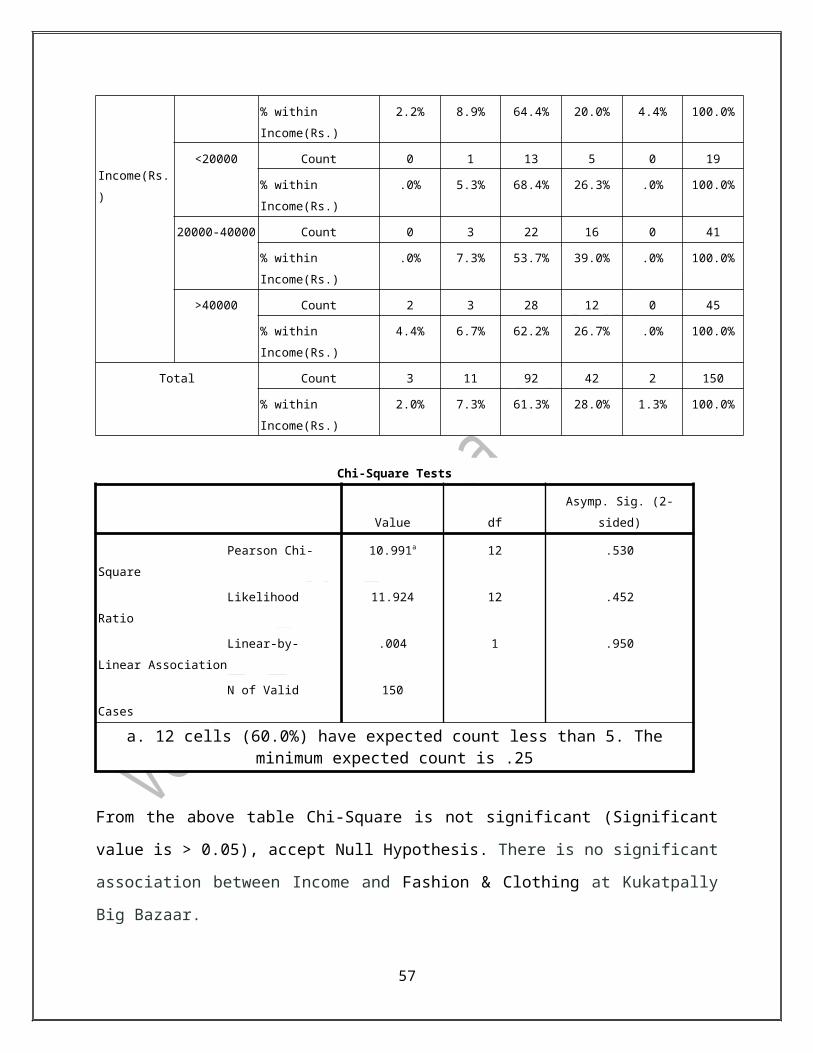

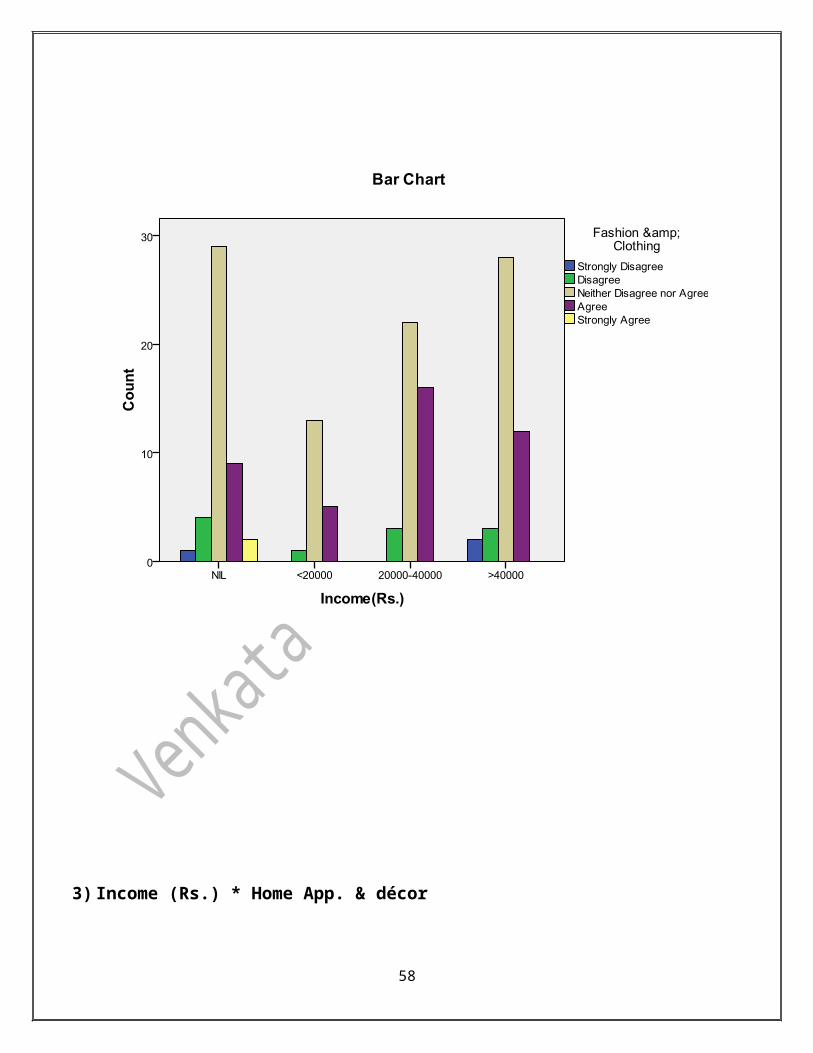

2) Income (Rs.) * Fashion & Clothing

H0: There is no significant association between Income and Fashion & Clothing at

Kukatpally Big Bazaar.

Crosstab

Fashion & Clothing

Total

Strongly

Disagree Disagree

Neither

Disagree

nor Agree Agree

Strongly

Agree

NIL Count 1 4 29 9 2 45

40

Income(Rs.)

% within Income(Rs.) 2.2% 8.9% 64.4% 20.0% 4.4% 100.0%

<20000 Count 0 1 13 5 0 19

% within Income(Rs.) .0% 5.3% 68.4% 26.3% .0% 100.0%

20000-40000 Count 0 3 22 16 0 41

% within Income(Rs.) .0% 7.3% 53.7% 39.0% .0% 100.0%

>40000 Count 2 3 28 12 0 45

% within Income(Rs.) 4.4% 6.7% 62.2% 26.7% .0% 100.0%

Total Count 3 11 92 42 2 150

% within Income(Rs.) 2.0% 7.3% 61.3% 28.0% 1.3% 100.0%

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 10.991a 12 .530

Likelihood Ratio 11.924 12 .452

Linear-by-Linear Association .004 1 .950

N of Valid Cases 150

a. 12 cells (60.0%) have expected count less than 5. The minimum expected count is .25

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null

Hypothesis. There is no significant association between Income and Fashion & Clothing at

Kukatpally Big Bazaar.

41

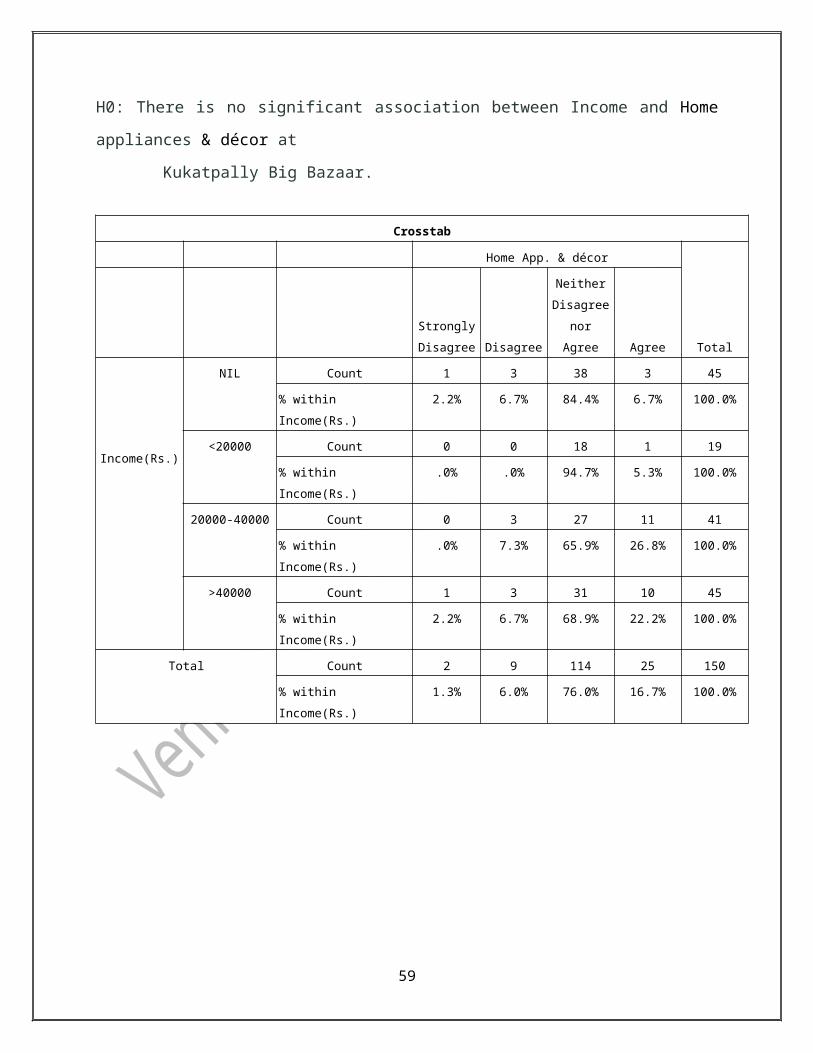

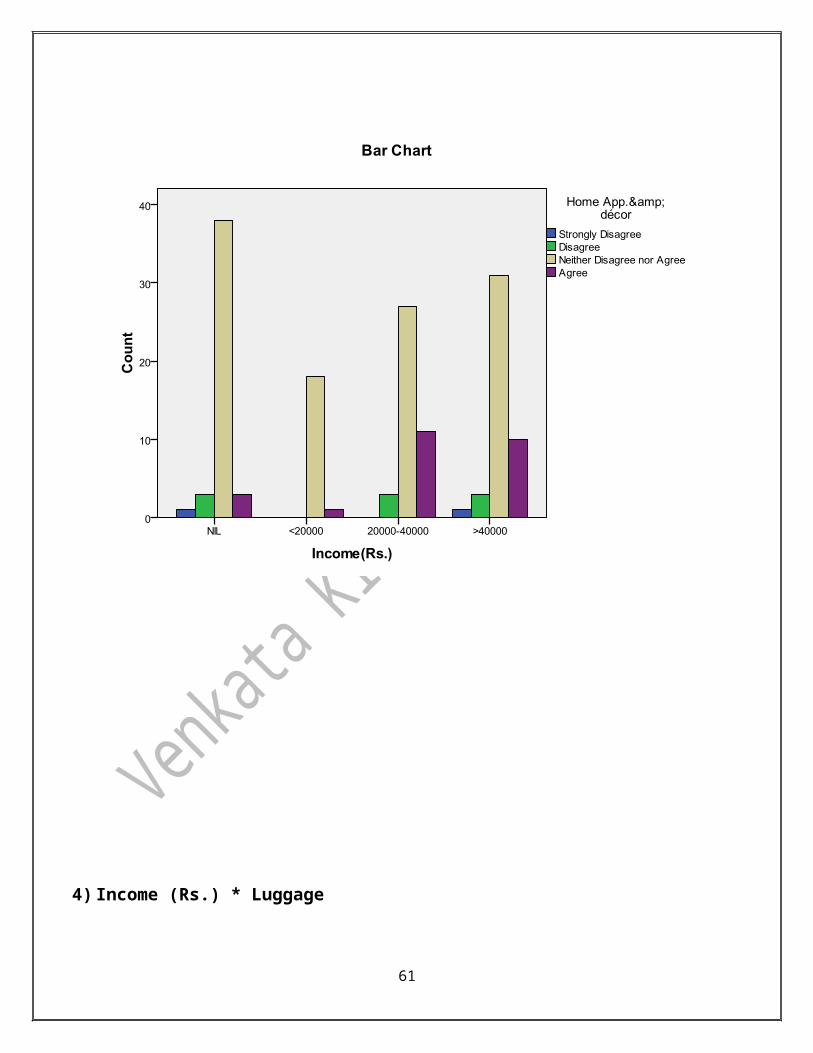

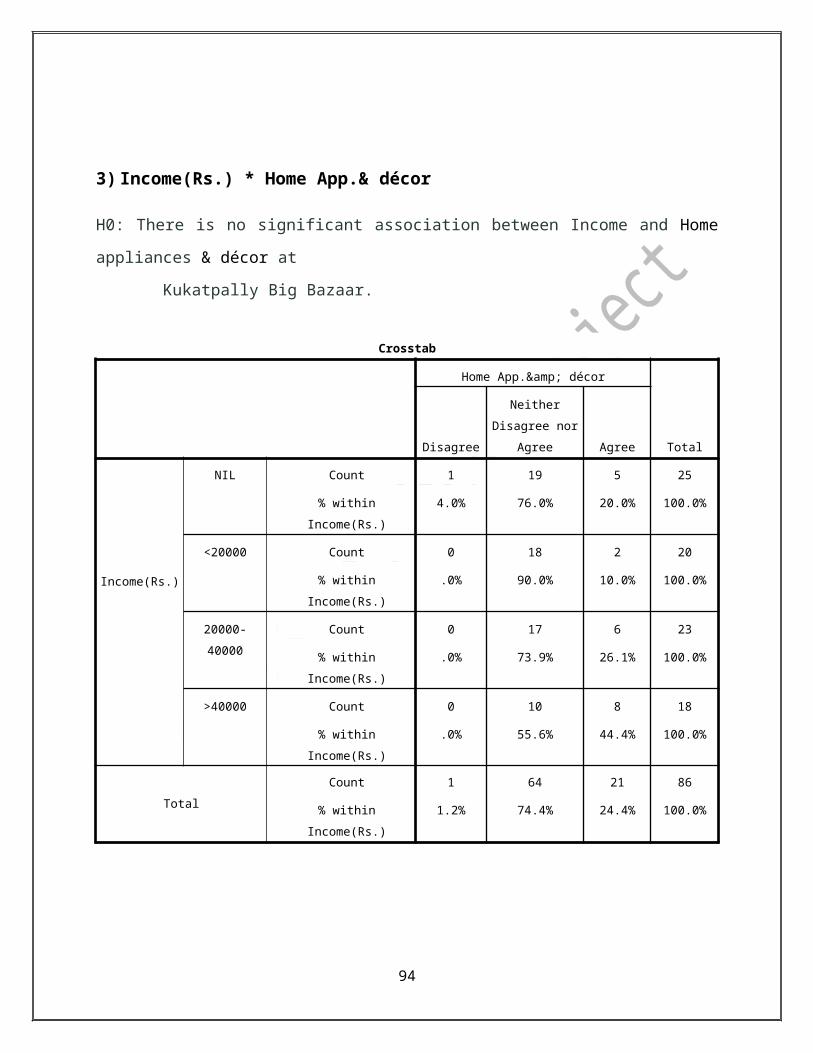

3) Income (Rs.) * Home App. & décor

H0: There is no significant association between Income and Home appliances & décor at

Kukatpally Big Bazaar.

42

Crosstab

Home App. & décor

Total

Strongly

Disagree Disagree

Neither

Disagree

nor Agree Agree

Income(Rs.)

NIL Count 1 3 38 3 45

% within Income(Rs.) 2.2% 6.7% 84.4% 6.7% 100.0%

<20000 Count 0 0 18 1 19

% within Income(Rs.) .0% .0% 94.7% 5.3% 100.0%

20000-40000 Count 0 3 27 11 41

% within Income(Rs.) .0% 7.3% 65.9% 26.8% 100.0%

>40000 Count 1 3 31 10 45

% within Income(Rs.) 2.2% 6.7% 68.9% 22.2% 100.0%

Total Count 2 9 114 25 150

% within Income(Rs.) 1.3% 6.0% 76.0% 16.7% 100.0%

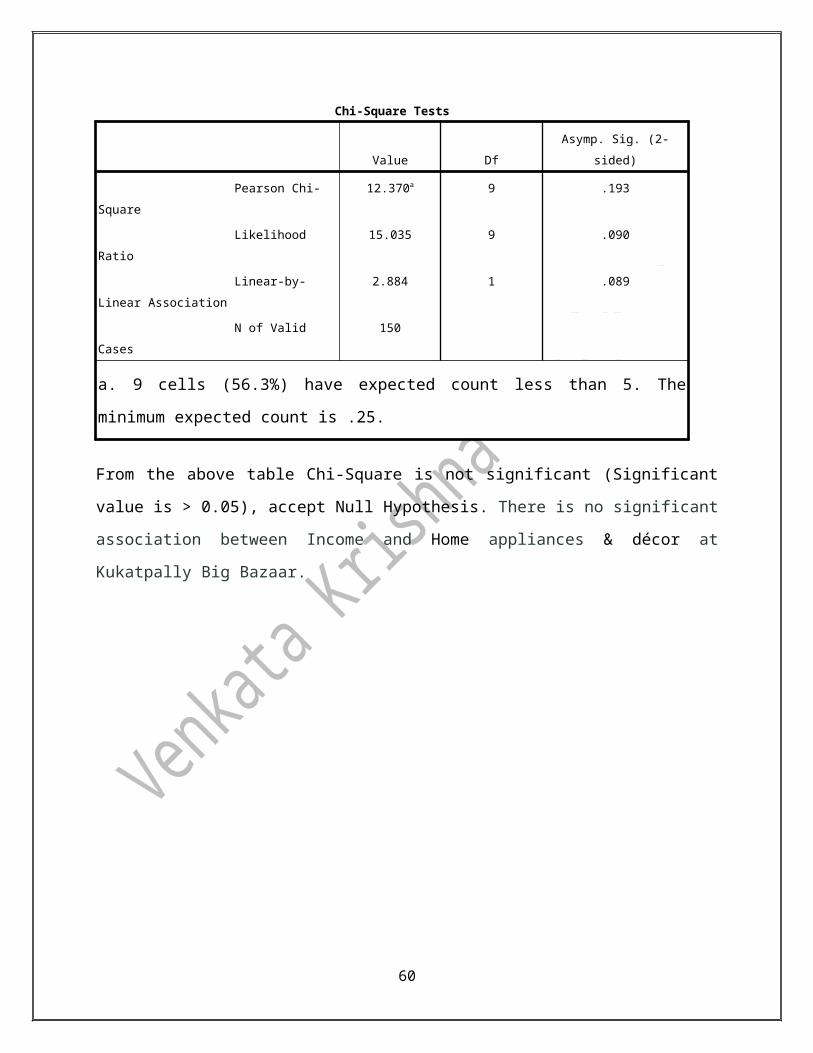

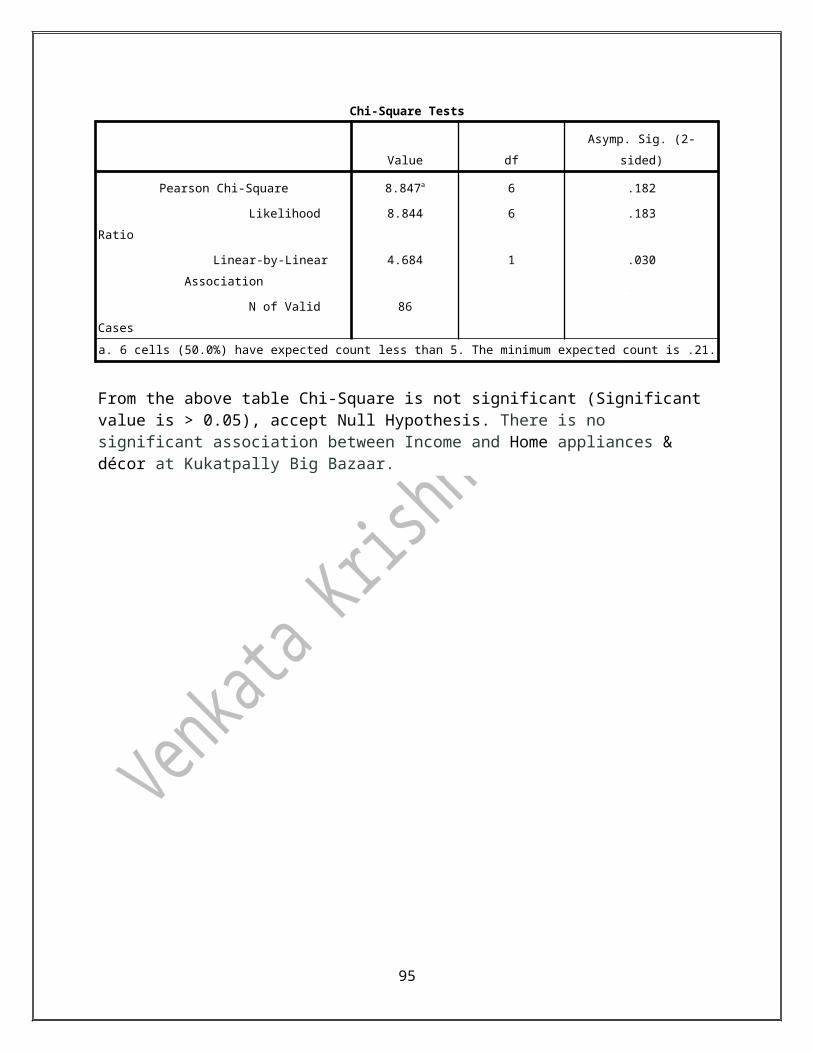

Chi-Square Tests

Value Df Asymp. Sig. (2-sided)

Pearson Chi-Square 12.370a 9 .193

Likelihood Ratio 15.035 9 .090

Linear-by-Linear Association 2.884 1 .089

N of Valid Cases 150

a. 9 cells (56.3%) have expected count less than 5. The minimum expected count is .25.

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null

Hypothesis. There is no significant association between Income and Home appliances & décor at

Kukatpally Big Bazaar.

43

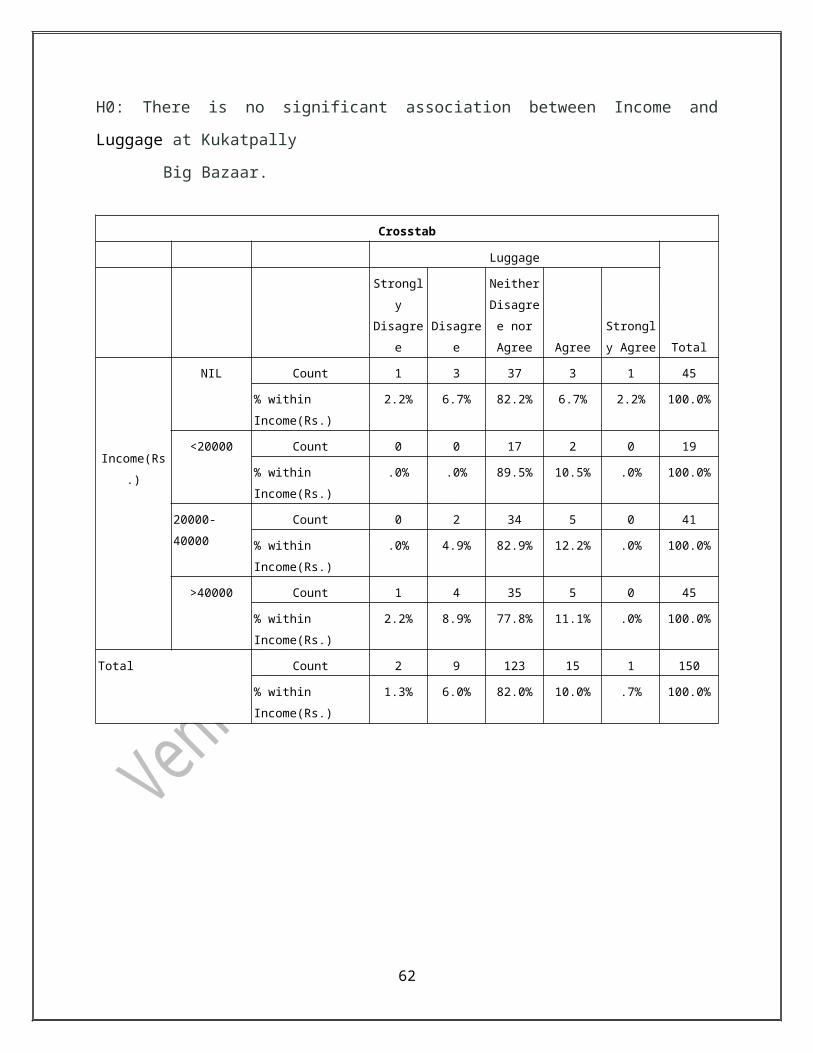

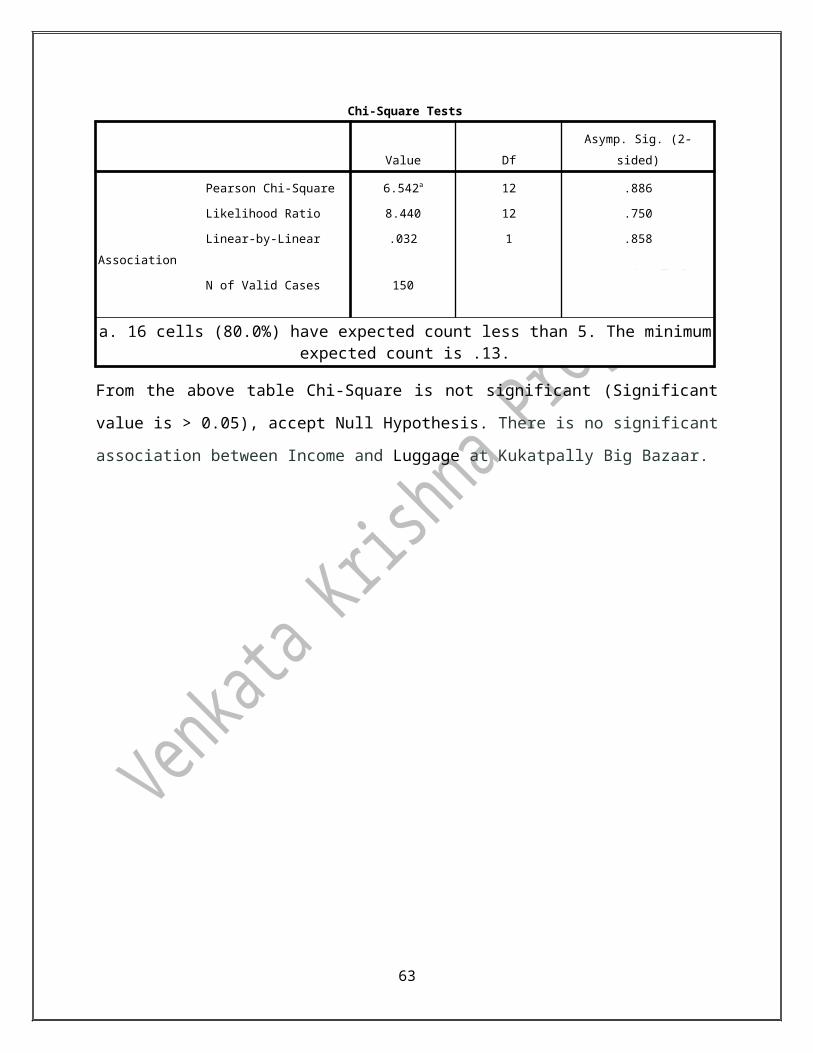

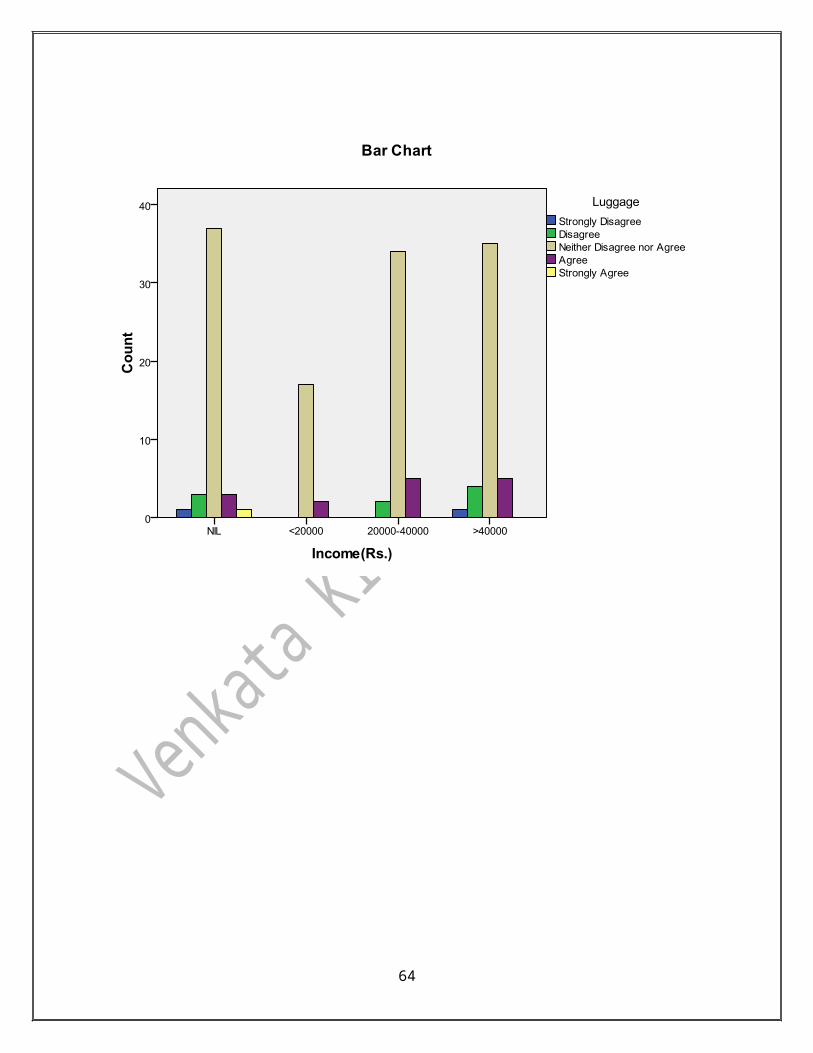

4) Income (Rs.) * Luggage

H0: There is no significant association between Income and Luggage at Kukatpally

Big Bazaar.

44

Crosstab

Luggage

Total

Strongly

Disagree Disagree

Neither

Disagree

nor Agree Agree

Strongly

Agree

Income(Rs.)

NIL Count 1 3 37 3 1 45

% within Income(Rs.) 2.2% 6.7% 82.2% 6.7% 2.2% 100.0%

<20000 Count 0 0 17 2 0 19

% within Income(Rs.) .0% .0% 89.5% 10.5% .0% 100.0%

20000-40000 Count 0 2 34 5 0 41

% within Income(Rs.) .0% 4.9% 82.9% 12.2% .0% 100.0%

>40000 Count 1 4 35 5 0 45

% within Income(Rs.) 2.2% 8.9% 77.8% 11.1% .0% 100.0%

Total Count 2 9 123 15 1 150

% within Income(Rs.) 1.3% 6.0% 82.0% 10.0% .7% 100.0%

Chi-Square Tests

Value Df Asymp. Sig. (2-sided)

Pearson Chi-Square 6.542a 12 .886

Likelihood Ratio 8.440 12 .750

Linear-by-Linear Association .032 1 .858

N of Valid Cases 150

a. 16 cells (80.0%) have expected count less than 5. The minimum expected count is .13.

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null

Hypothesis. There is no significant association between Income and Luggage at Kukatpally Big

Bazaar.

45

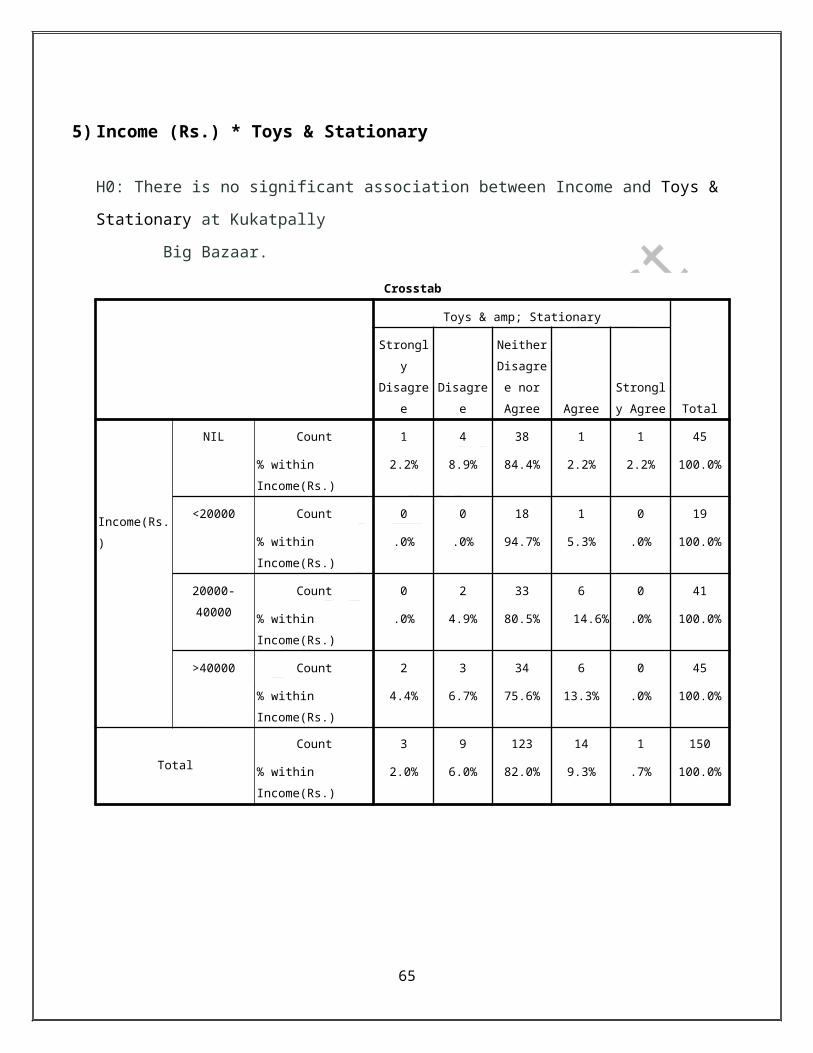

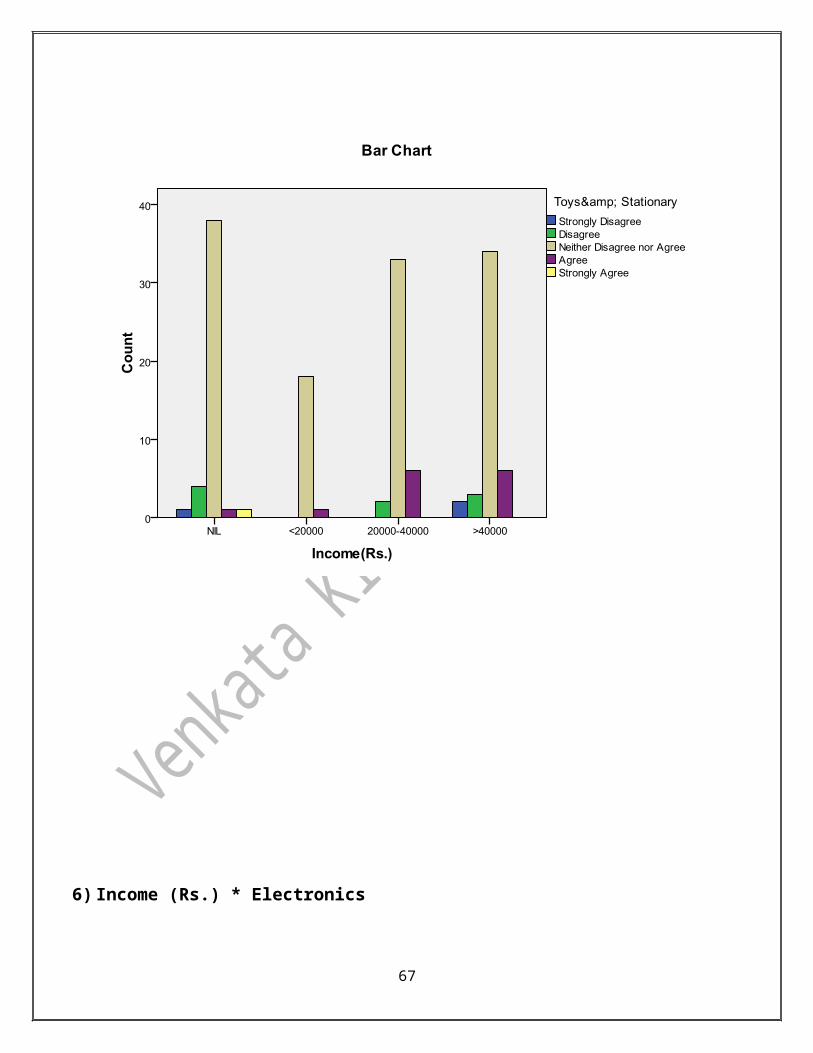

5) Income (Rs.) * Toys & Stationary

46

H0: There is no significant association between Income and Toys & Stationary at Kukatpally

Big Bazaar.

Crosstab

Toys & amp; Stationary

Total

Strongly

Disagree Disagree

Neither

Disagree

nor Agree Agree

Strongly

Agree

Income(Rs.)

NIL Count 1 4 38 1 1 45

% within Income(Rs.) 2.2% 8.9% 84.4% 2.2% 2.2% 100.0%

<20000 Count 0 0 18 1 0 19

% within Income(Rs.) .0% .0% 94.7% 5.3% .0% 100.0%

20000-40000 Count 0 2 33 6 0 41

% within Income(Rs.) .0% 4.9% 80.5% 14.6% .0% 100.0%

>40000 Count 2 3 34 6 0 45

% within Income(Rs.) 4.4% 6.7% 75.6% 13.3% .0% 100.0%

Total

Count 3 9 123 14 1 150

% within Income(Rs.) 2.0% 6.0% 82.0% 9.3% .7% 100.0%

Chi-Square Tests

Value Df Asymp. Sig. (2-sided)

Pearson Chi-Square 12.203a 12 .429

Likelihood Ratio 15.058 12 .238

Linear-by-Linear Association .346 1 .557

N of Valid Cases 150

a. 16 cells (80.0%) have expected count less than 5. The minimum expected count is .13.

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null

Hypothesis. There is no significant association between Income and Toys & Stationary at

Kukatpally Big Bazaar.

47

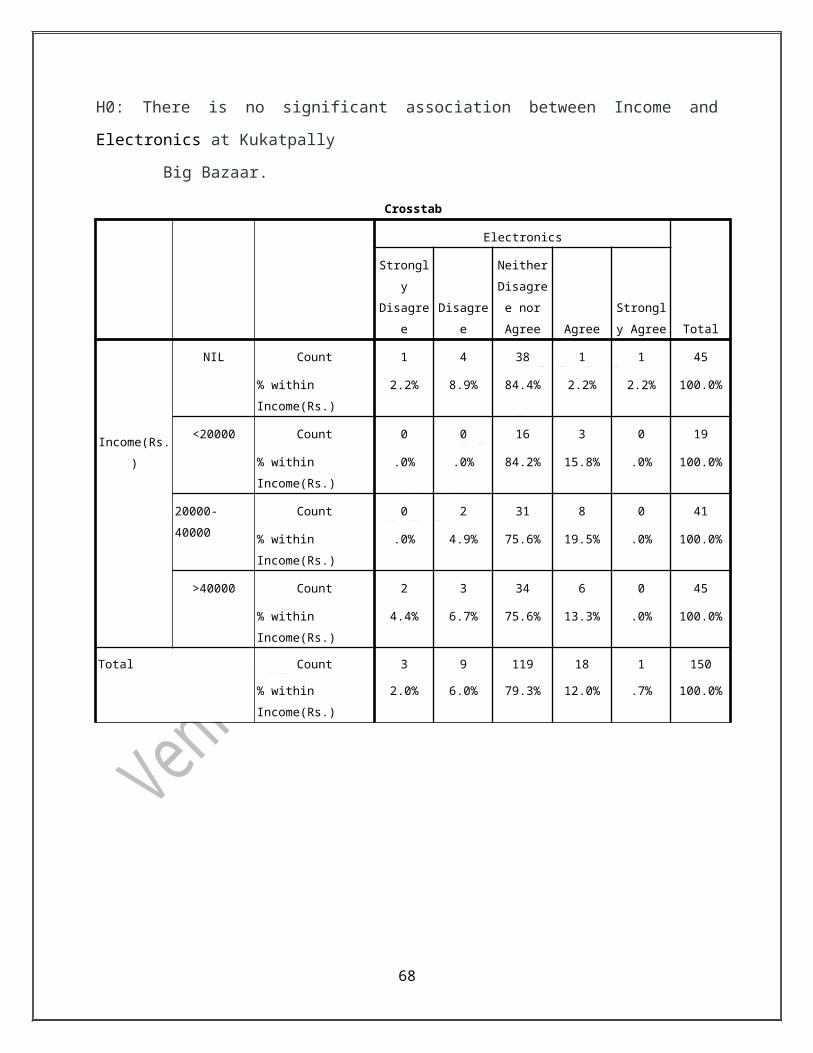

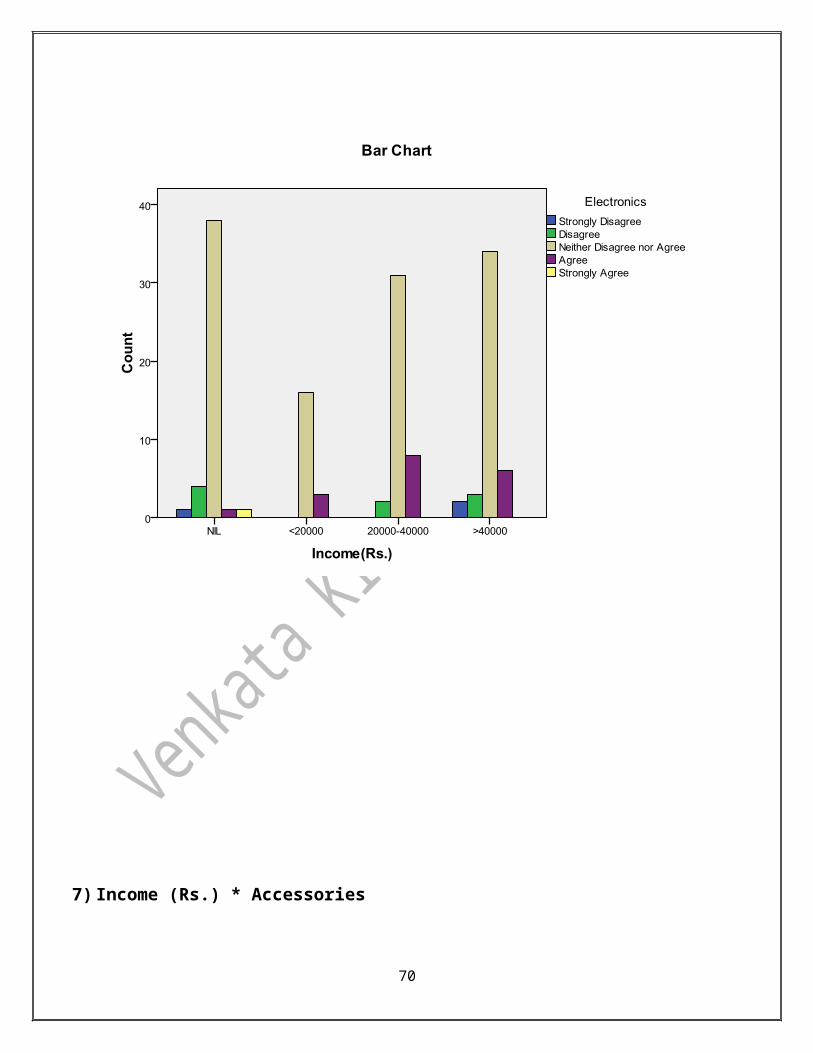

6) Income (Rs.) * Electronics

H0: There is no significant association between Income and Electronics at Kukatpally

Big Bazaar.

48

Crosstab

Electronics

Total

Strongly

Disagree Disagree

Neither

Disagree

nor Agree Agree

Strongly

Agree

Income(Rs.)

NIL Count 1 4 38 1 1 45

% within Income(Rs.) 2.2% 8.9% 84.4% 2.2% 2.2% 100.0%

<20000 Count 0 0 16 3 0 19

% within Income(Rs.) .0% .0% 84.2% 15.8% .0% 100.0%

20000-40000 Count 0 2 31 8 0 41

% within Income(Rs.) .0% 4.9% 75.6% 19.5% .0% 100.0%

>40000 Count 2 3 34 6 0 45

% within Income(Rs.) 4.4% 6.7% 75.6% 13.3% .0% 100.0%

Total Count 3 9 119 18 1 150

% within Income(Rs.) 2.0% 6.0% 79.3% 12.0% .7% 100.0%

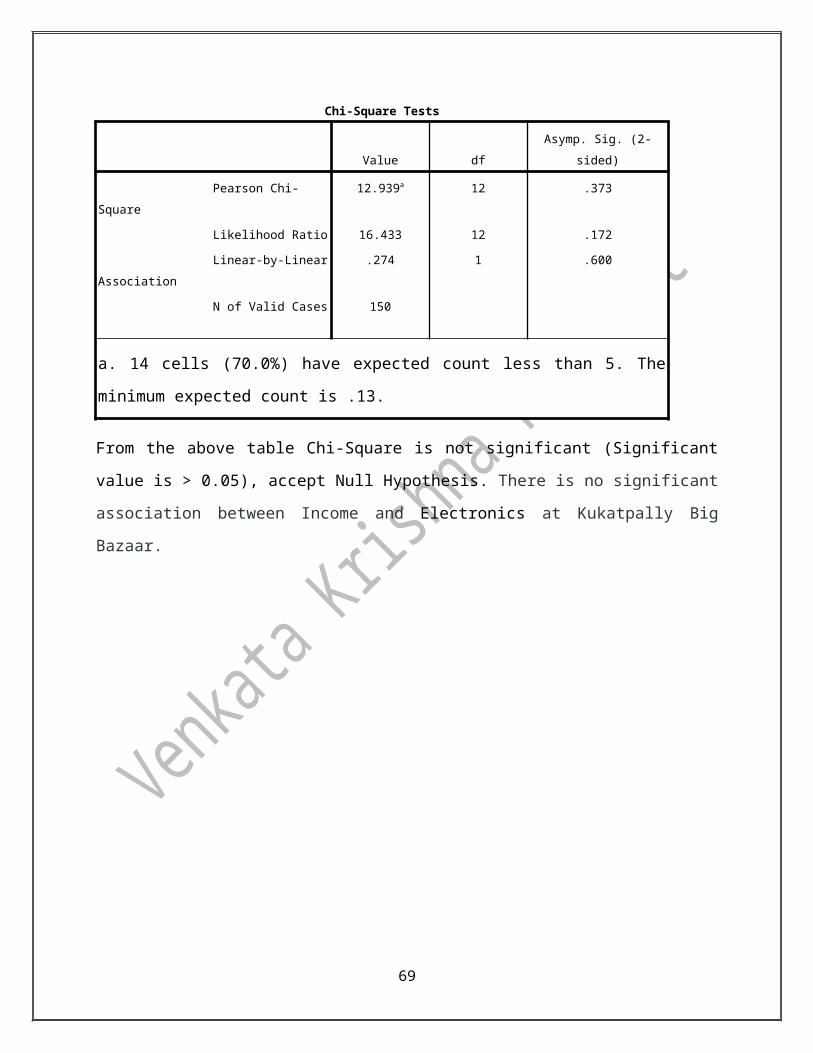

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 12.939a 12 .373

Likelihood Ratio 16.433 12 .172

Linear-by-Linear Association .274 1 .600

N of Valid Cases 150

a. 14 cells (70.0%) have expected count less than 5. The minimum expected count is .13.

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null

Hypothesis. There is no significant association between Income and Electronics at Kukatpally

Big Bazaar.

49

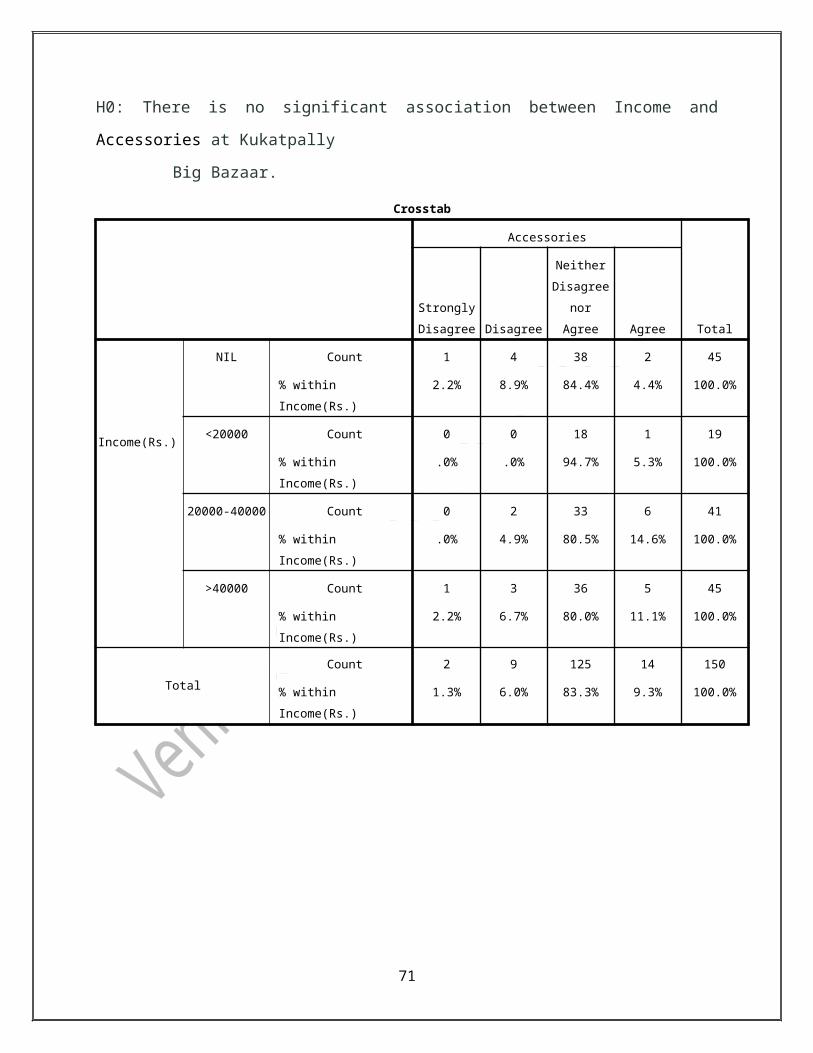

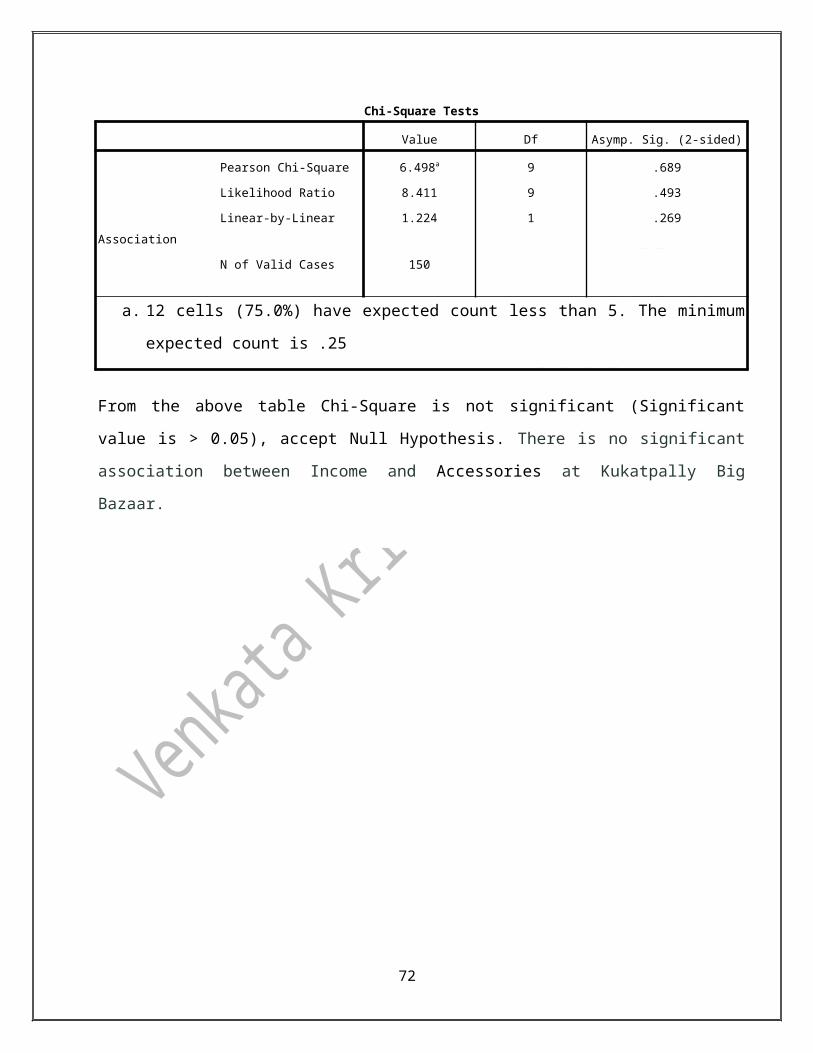

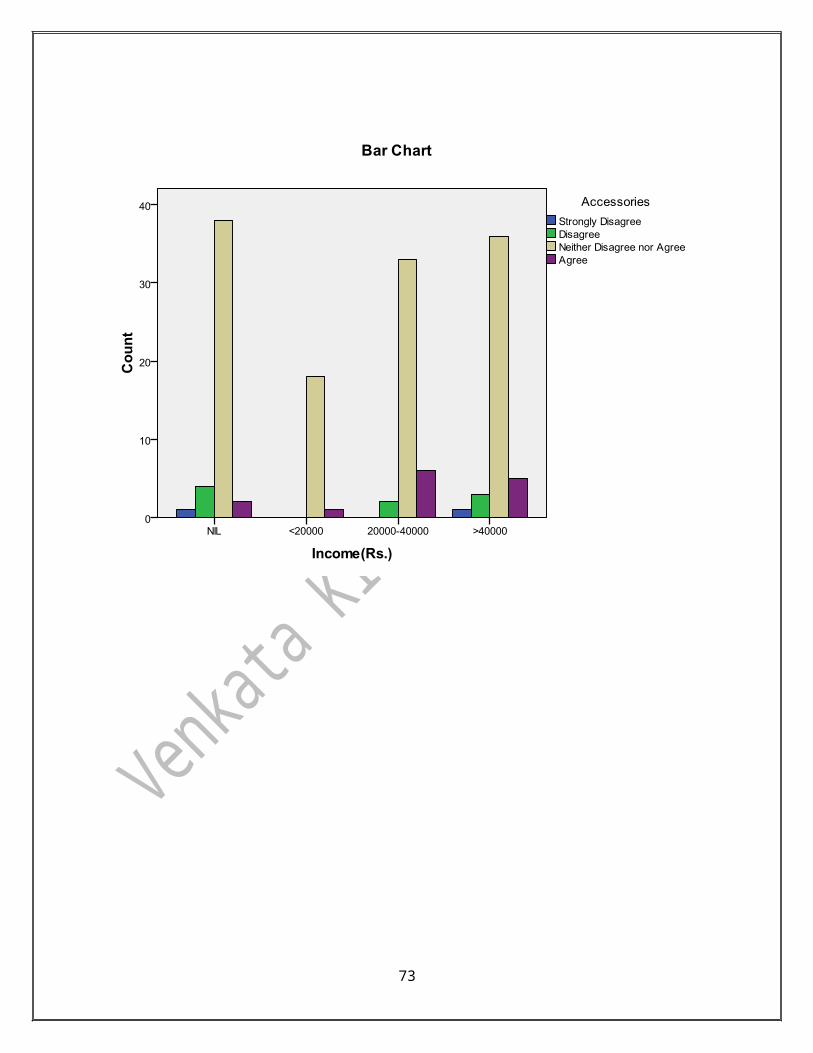

7) Income (Rs.) * Accessories

H0: There is no significant association between Income and Accessories at Kukatpally

Big Bazaar.

50

Crosstab

Accessories

Total

Strongly

Disagree Disagree

Neither

Disagree

nor Agree Agree

Income(Rs.)

NIL Count 1 4 38 2 45

% within Income(Rs.) 2.2% 8.9% 84.4% 4.4% 100.0%

<20000 Count 0 0 18 1 19

% within Income(Rs.) .0% .0% 94.7% 5.3% 100.0%

20000-40000 Count 0 2 33 6 41

% within Income(Rs.) .0% 4.9% 80.5% 14.6% 100.0%

>40000 Count 1 3 36 5 45

% within Income(Rs.) 2.2% 6.7% 80.0% 11.1% 100.0%

Total

Count 2 9 125 14 150

% within Income(Rs.) 1.3% 6.0% 83.3% 9.3% 100.0%

Chi-Square Tests

Value Df Asymp. Sig. (2-sided)

Pearson Chi-Square 6.498a 9 .689

Likelihood Ratio 8.411 9 .493

Linear-by-Linear Association 1.224 1 .269

N of Valid Cases 150

a. 12 cells (75.0%) have expected count less than 5. The minimum expected count is .25

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null

Hypothesis. There is no significant association between Income and Accessories at Kukatpally Big

Bazaar.

51

52

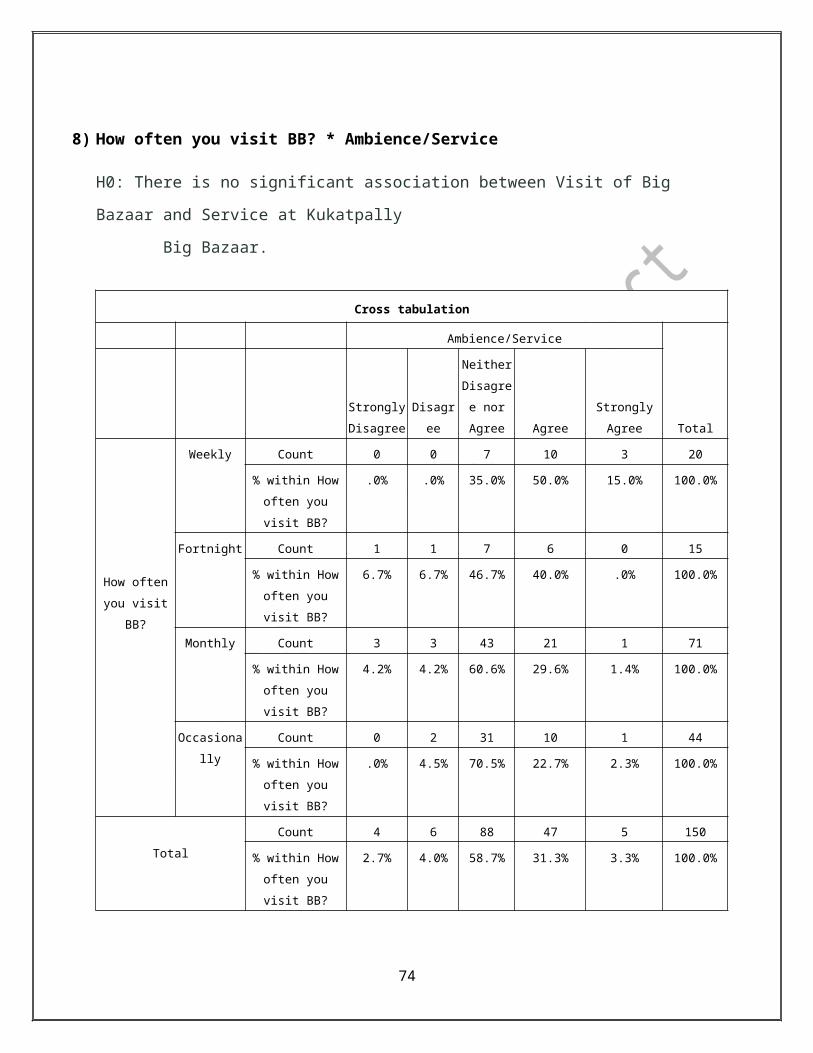

8) How often you visit BB? * Ambience/Service

H0: There is no significant association between Visit of Big Bazaar and Service at Kukatpally

Big Bazaar.

Cross tabulation

Ambience/Service

Total

Strongly

Disagree

Disagre

e

Neither

Disagree

nor

Agree Agree

Strongly

Agree

How often

you visit BB?

Weekly Count 0 0 7 10 3 20

% within How

often you visit

BB?

.0% .0% 35.0% 50.0% 15.0% 100.0%

Fortnight Count 1 1 7 6 0 15

% within How

often you visit

BB?

6.7% 6.7% 46.7% 40.0% .0% 100.0%

Monthly Count 3 3 43 21 1 71

% within How

often you visit

BB?

4.2% 4.2% 60.6% 29.6% 1.4% 100.0%

Occasionall

y

Count 0 2 31 10 1 44

% within How

often you visit

BB?

.0% 4.5% 70.5% 22.7% 2.3% 100.0%

Total

Count 4 6 88 47 5 150

% within How

often you visit

BB?

2.7% 4.0% 58.7% 31.3% 3.3% 100.0%

53

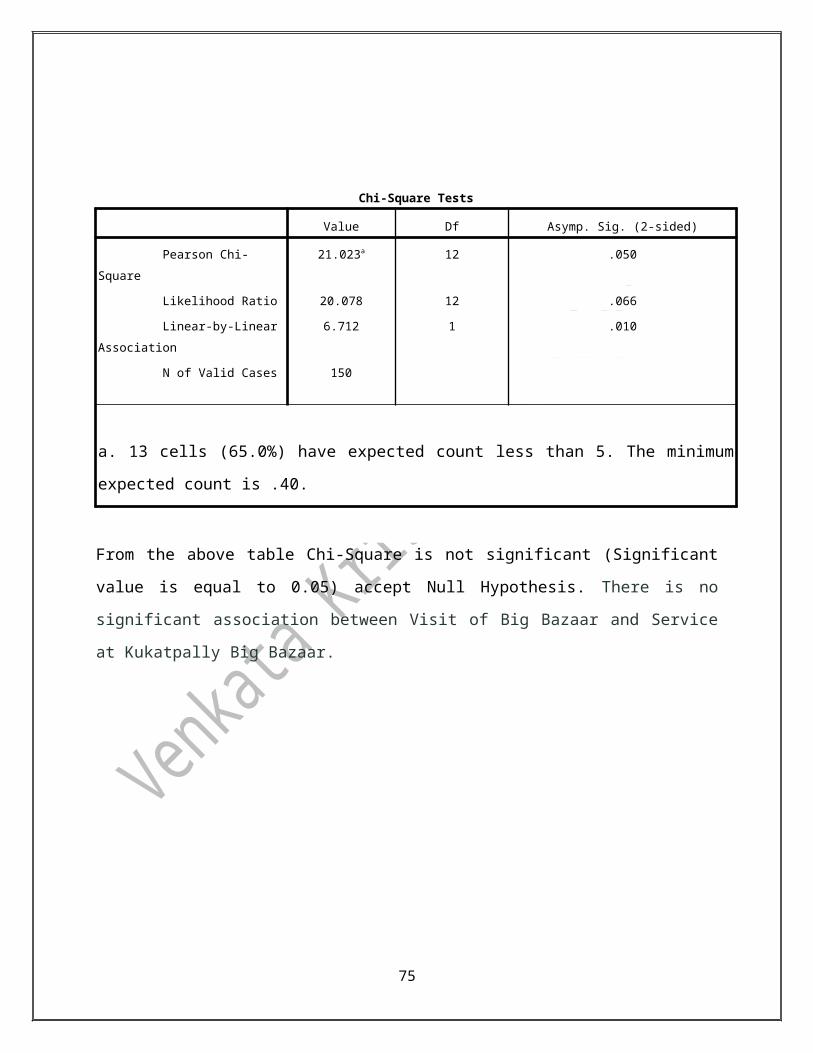

Chi-Square Tests

Value Df Asymp. Sig. (2-sided)

Pearson Chi-Square 21.023a 12 .050

Likelihood Ratio 20.078 12 .066

Linear-by-Linear Association 6.712 1 .010

N of Valid Cases 150

a. 13 cells (65.0%) have expected count less than 5. The minimum expected count is .40.

From the above table Chi-Square is not significant (Significant value is equal to 0.05) accept

Null Hypothesis. There is no significant association between Visit of Big Bazaar and Service at

Kukatpally Big Bazaar.

54

55

Null Hypothesis Sig. value Result

H0: There is no significant association between Income and Food

Items/ Grocery at Kukatpally Big Bazaar..264 Accepted

H0:There is no Significant association between Income and

Fashion & Clothing at Kukatpally Big Bazaar..530 Accepted

H0:There is no significant association between Income and Home

Appliances & décor at Kukatpally Big Bazaar..193 Accepted

H0: There is no significant association between Income and

Luggage at Kukatpally Big Bazaar..886 Accepted

H0:There is no significant association between Income and Toys

& Stationary at Kukatpally Big Bazaar..429 Accepted

H0:There is no significant association between Income and

Electronics at Kukatpally Big Bazaar..373 Accepted

H0:There is no significant association between Income and

Accessories at Kukatpally Big Bazaar..689 Accepted

H0:There is no significant association between Visit of Big

Bazaar and Service at Kukatpally Big Bazaar..050 Accepted

56

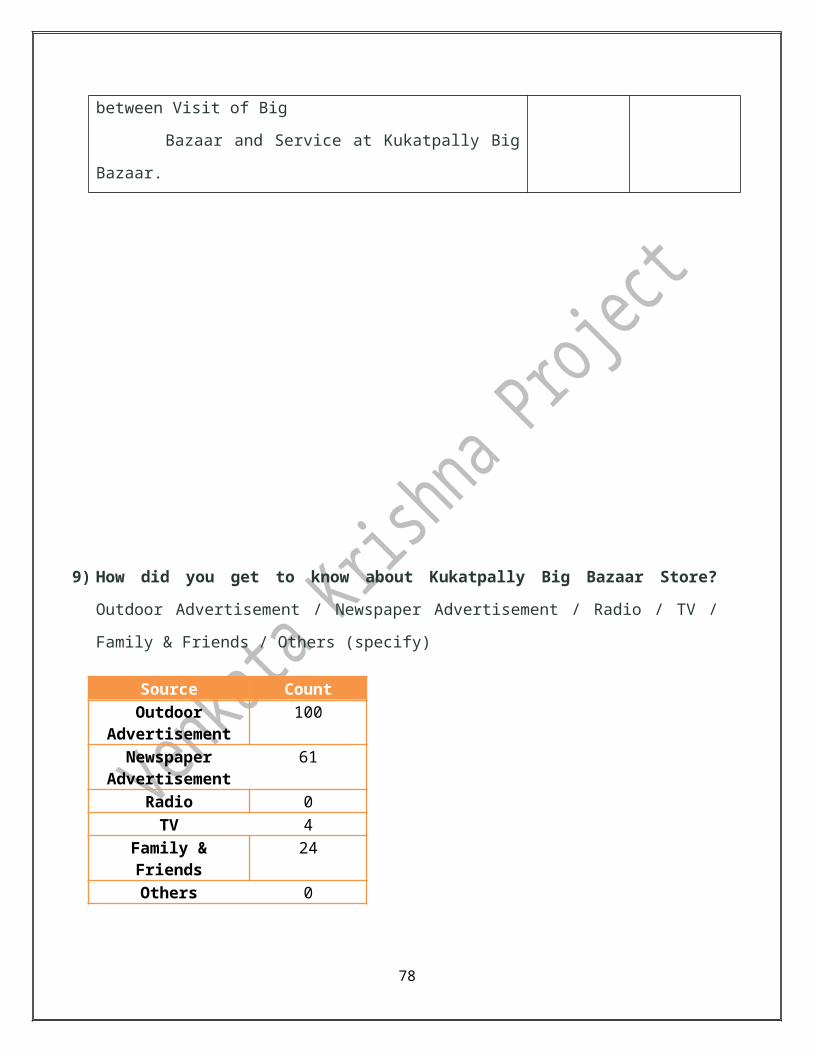

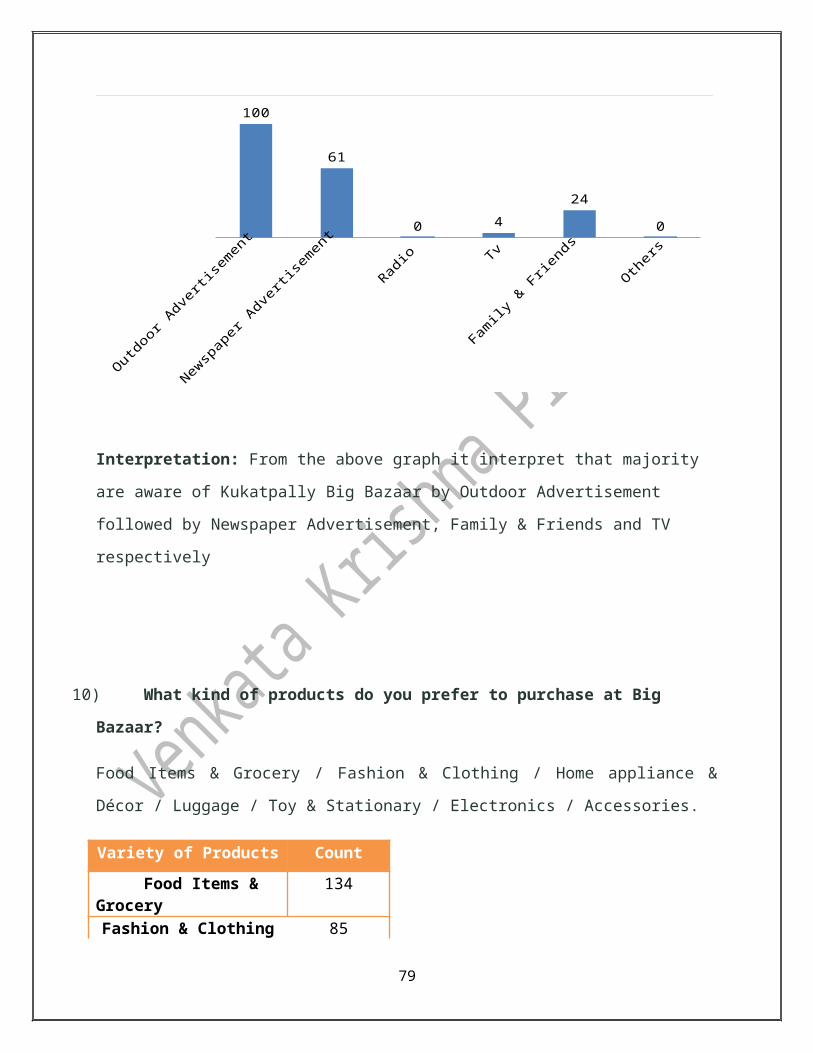

9) How did you get to know about Kukatpally Big Bazaar Store?

Outdoor Advertisement / Newspaper Advertisement / Radio / TV / Family & Friends / Others

(specify)

Source Count

Outdoor Advertisement

100

Newspaper Advertisement

61

Radio 0

TV 4

Family & Friends 24

Others 0

Outd

oor Adver

tisem

ent

New

spap

er A

dvertis

emen

t

Rad

io

Tv

Family

& F

riends

Oth

ers

100

61

0 4

24

0

Interpretation: From the above graph it interpret that majority are aware of Kukatpally Big

Bazaar by Outdoor Advertisement followed by Newspaper Advertisement, Family & Friends and

TV respectively

57

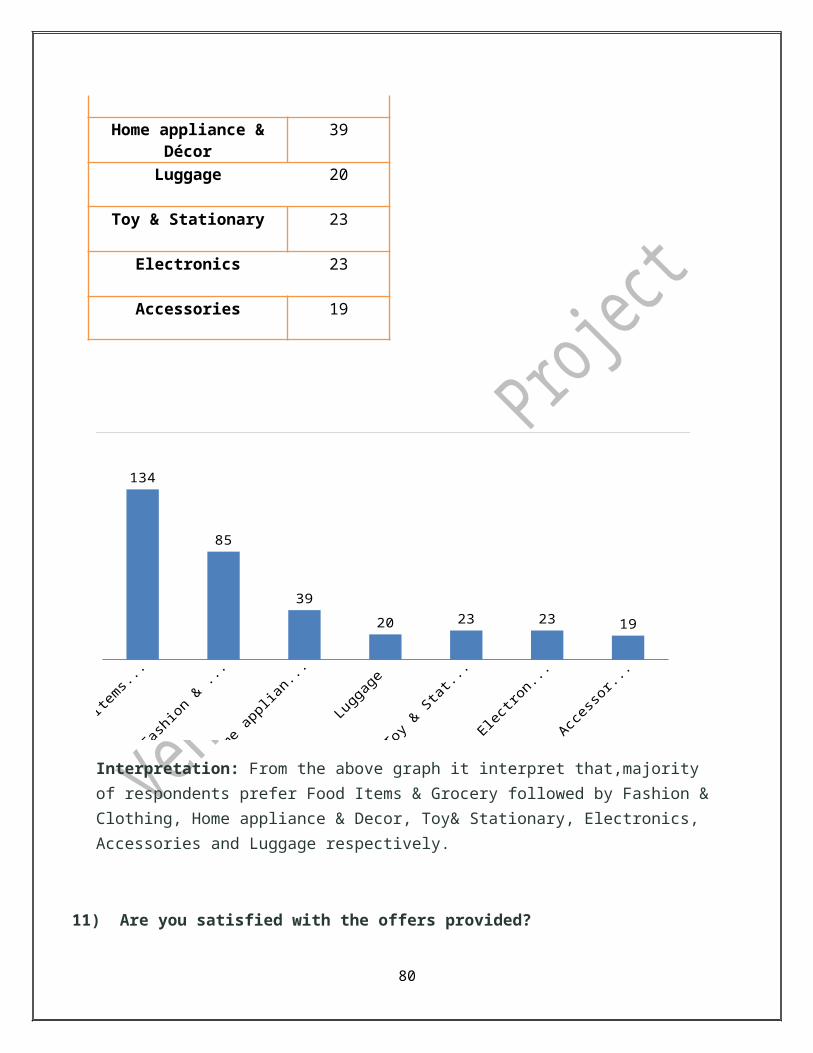

10) What kind of products do you prefer to purchase at Big Bazaar?

Food Items & Grocery / Fashion & Clothing / Home appliance & Décor / Luggage / Toy &

Stationary / Electronics / Accessories.

Variety of Products Count

Food Items & Grocery 134

Fashion & Clothing 85

Home appliance & Décor 39

Luggage 20

Toy & Stationary 23

Electronics 23

Accessories 19

Food Item

s &...

Fashio

n & C

lo...

Hom

e ap

pliance

...

Luggage

Toy & S

tatio

n...

Elect

ronic

s

Acc

esso

ries

134

85

39

20 23 23 19

Interpretation: From the above graph it interpret that,majority of respondents prefer Food Items & Grocery followed by Fashion & Clothing, Home appliance & Decor, Toy& Stationary, Electronics, Accessories and Luggage respectively.

58

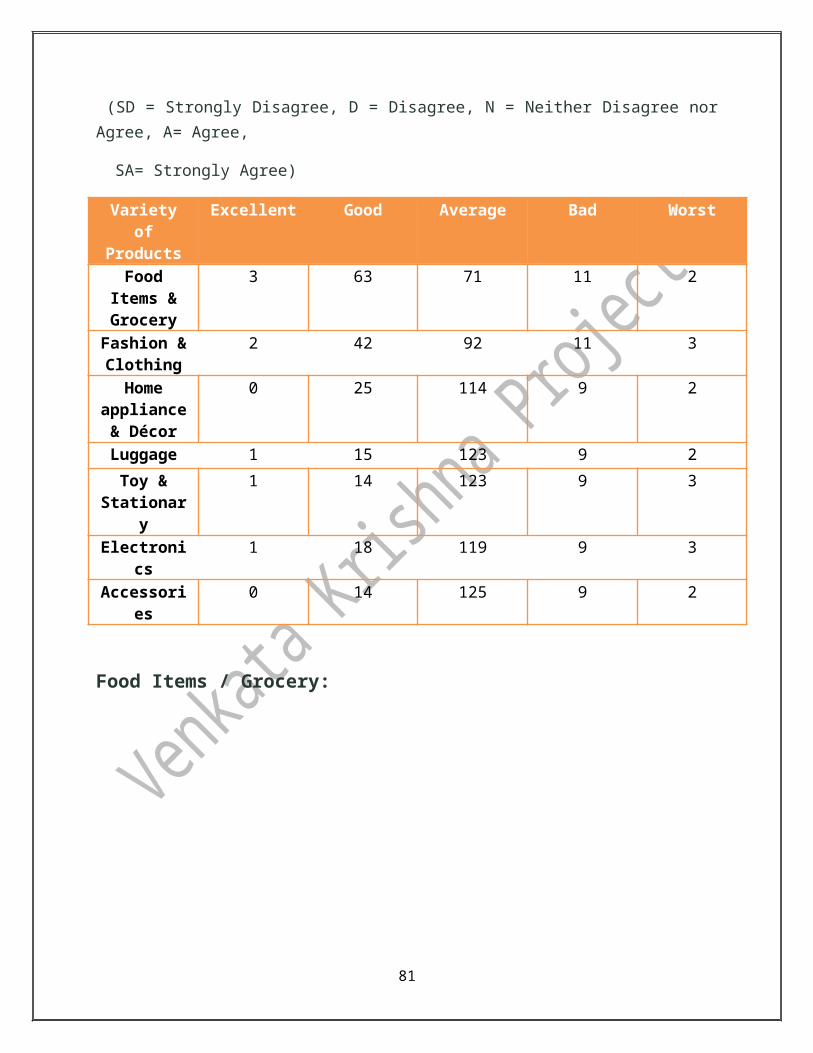

11) Are you satisfied with the offers provided?

(SD = Strongly Disagree, D = Disagree, N = Neither Disagree nor Agree, A= Agree,

SA= Strongly Agree)

Variety of Products

Excellent Good Average Bad Worst

Food Items & Grocery

3 63 71 11 2

Fashion & Clothing

2 42 92 11 3

Home appliance &

Décor

0 25 114 9 2

Luggage 1 15 123 9 2

Toy & Stationary

1 14 123 9 3

Electronics 1 18 119 9 3

Accessories 0 14 125 9 2

Food Items / Grocery:

2%

42%

47%

7%1%

Excellent Good Average Bad Worst

59

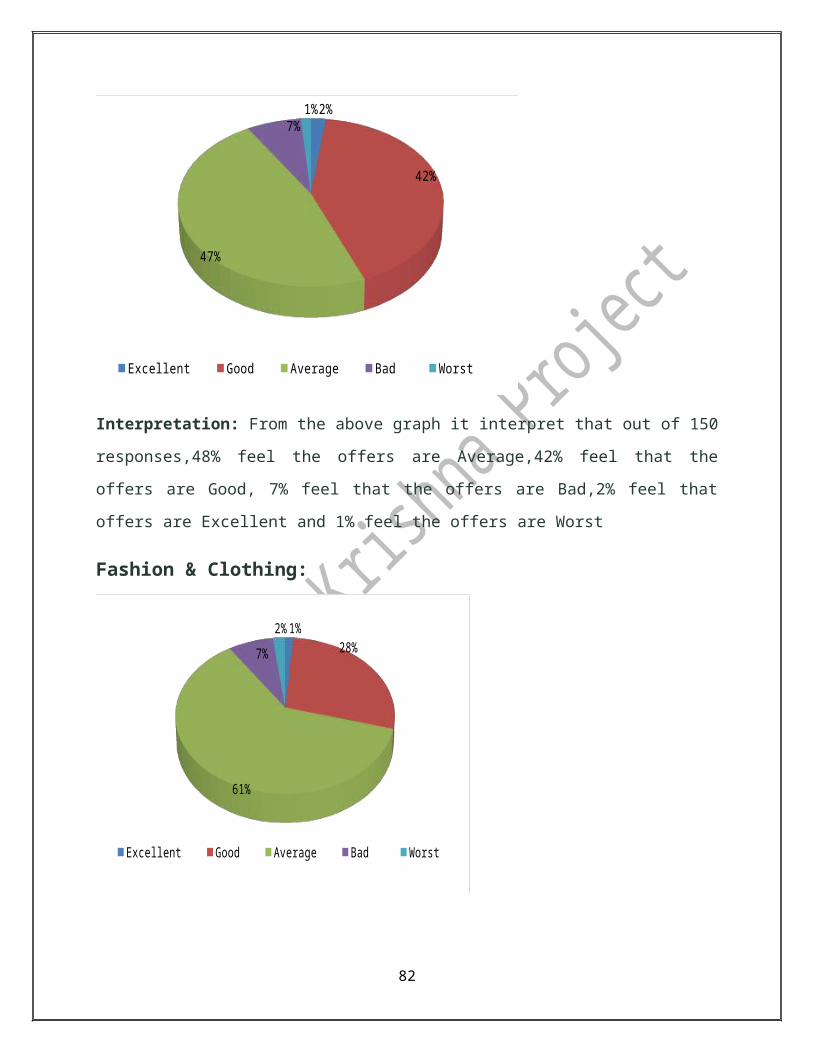

Interpretation: From the above graph it interpret that out of 150 responses,48% feel the offers

are Average,42% feel that the offers are Good, 7% feel that the offers are Bad,2% feel that offers

are Excellent and 1% feel the offers are Worst

Fashion & Clothing:

1%28%

61%

7%

2%

Excellent Good Average Bad Worst

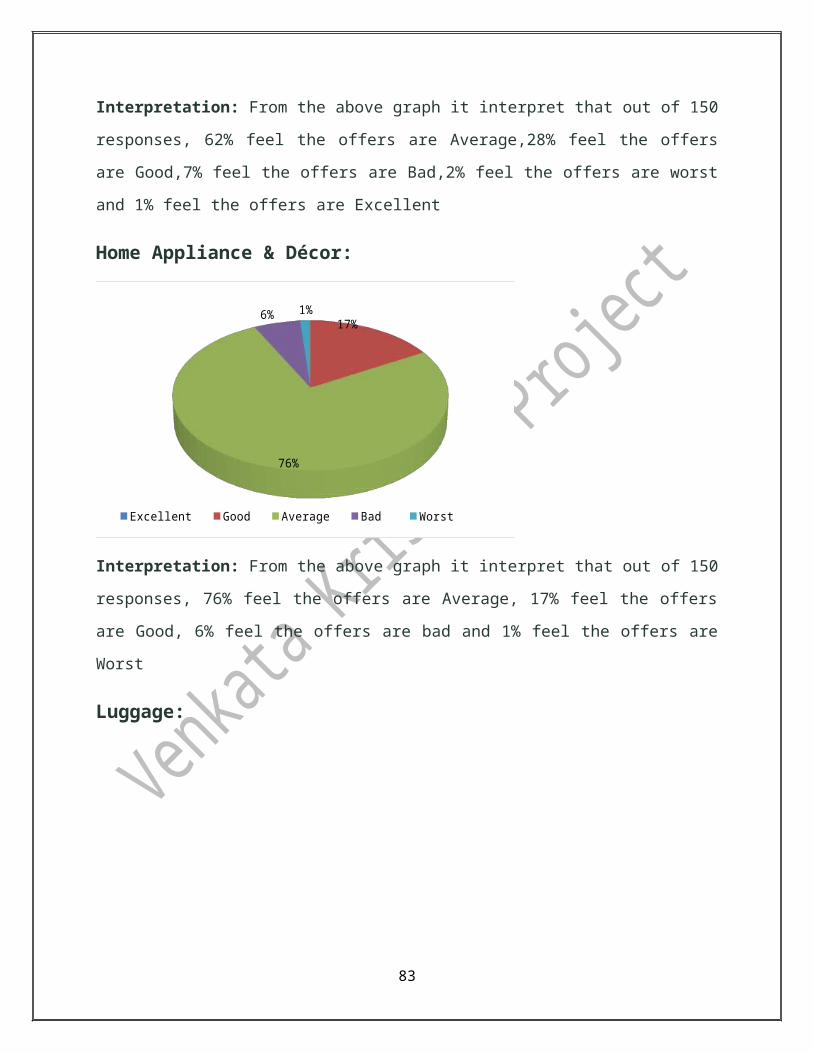

Interpretation: From the above graph it interpret that out of 150 responses, 62% feel the offers

are Average,28% feel the offers are Good,7% feel the offers are Bad,2% feel the offers are worst

and 1% feel the offers are Excellent

Home Appliance & Décor:

17%

76%

6% 1%

Excellent Good Average Bad Worst

60

Interpretation: From the above graph it interpret that out of 150 responses, 76% feel the offers

are Average, 17% feel the offers are Good, 6% feel the offers are bad and 1% feel the offers are

Worst

Luggage:

1%10%

82%

6%1%

Excellent Good Average Bad Worst

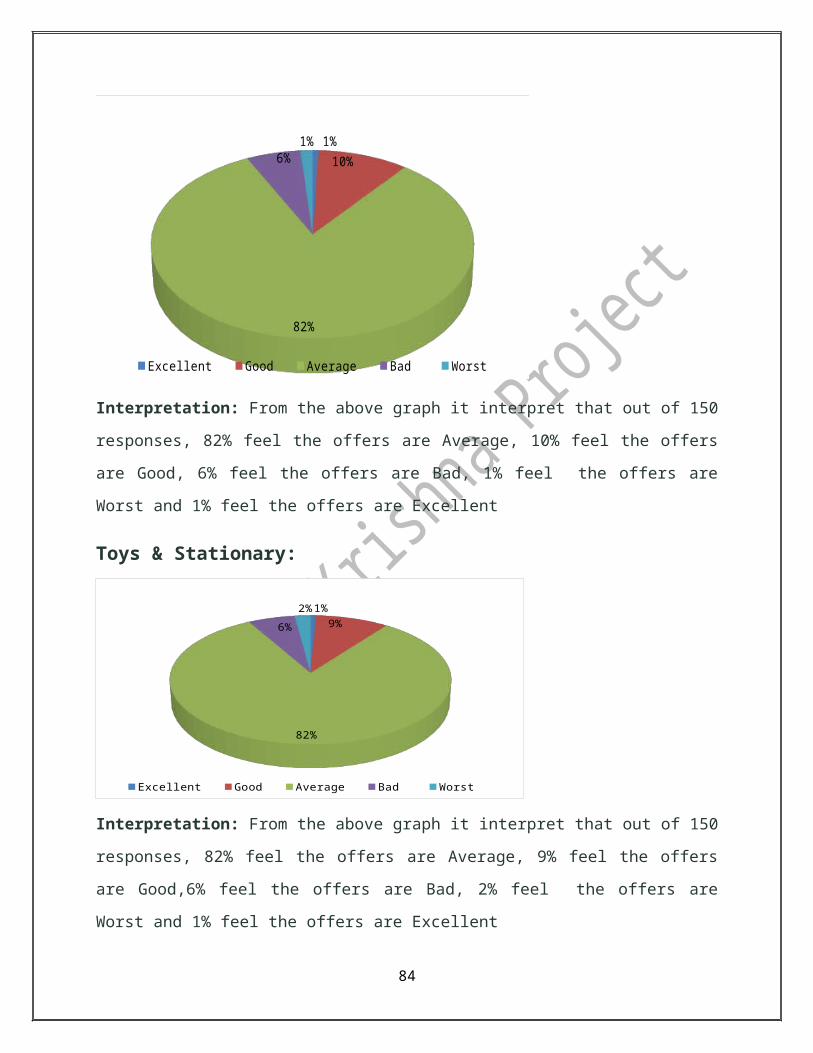

Interpretation: From the above graph it interpret that out of 150 responses, 82% feel the offers

are Average, 10% feel the offers are Good, 6% feel the offers are Bad, 1% feel the offers are

Worst and 1% feel the offers are Excellent

Toys & Stationary:

1%9%

82%

6%

2%

Excellent Good Average Bad Worst

61

Interpretation: From the above graph it interpret that out of 150 responses, 82% feel the offers

are Average, 9% feel the offers are Good,6% feel the offers are Bad, 2% feel the offers are

Worst and 1% feel the offers are Excellent

Electronics:

1%12%

79%

6%

2%

Excellent Good Average Bad Worst

Interpretation: From the above graph it interpret that out of 150 responses, 79% feel the offers

are Average, 12% feel the offers are Good, 6% feel the offers are Bad, 2% feel the offers are

Worst and 1% feel the offers are Excellent

Accessories:

9%

83%

6%1%

Excellent Good Average Bad Worst

62

Interpretation: From the above graph it interpret that out of 150 responses, 83% feel the offers

are Average, 10% feel the offers are Good, 6% feel the offers are Bad and 1% feel the offers are

Worst

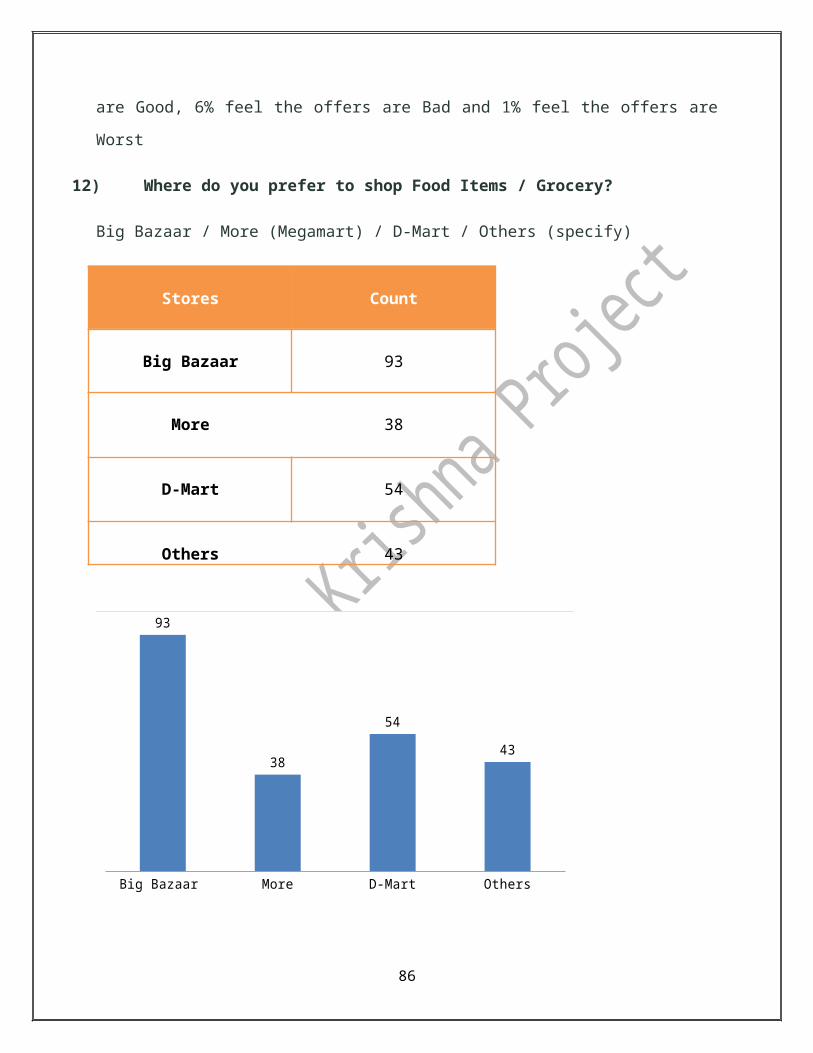

12) Where do you prefer to shop Food Items / Grocery?

Big Bazaar / More (Megamart) / D-Mart / Others (specify)

Stores Count

Big Bazaar 93

More

38

D-Mart

54

Others 43

Big Bazaar More D-Mart Others

93

38

54

43

Interpretation: From the above graph it interpret that most of the respondents prefered to

purchase Food Items & Grocery is Big Bazaar followed with D-Mart, Others and More

respectively.

63

13) Do you like our Ambience and Services?

(SD = Strongly Disagree, D = Disagree, N = Neither Disagree nor Agree, A= Agree,

SA= Strongly Agree)

SD D N A SA

3%

31%

59%

4% 3%

Excellent Good Average Bad Worst

Interpretation: From the above graph it interpret that out of 150 responses, 59% is Average,

31% is Good, 4% is Bad, 3% is Excellent and 3% is Worst

64

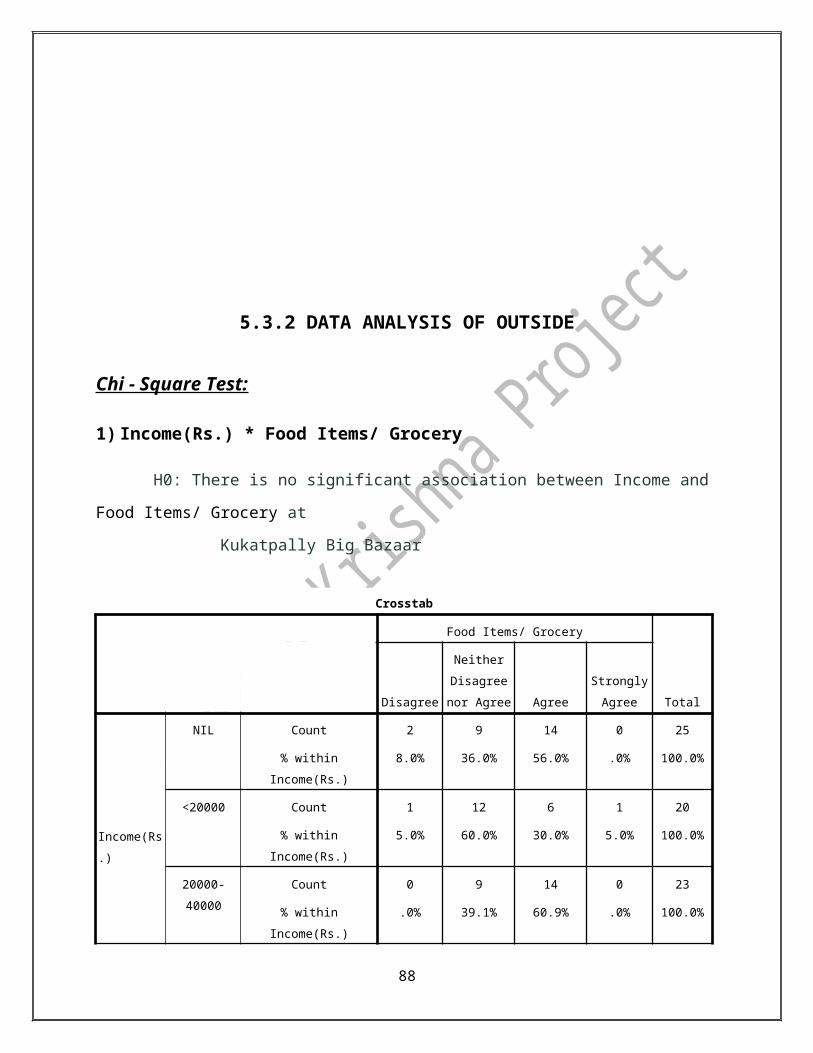

5.3.2 DATA ANALYSIS OF OUTSIDE

Chi - Square Test:

1) Income(Rs.) * Food Items/ Grocery

H0: There is no significant association between Income and Food Items/ Grocery at

Kukatpally Big Bazaar

Crosstab

Food Items/ Grocery

TotalDisagree

Neither

Disagree

nor Agree Agree

Strongly

Agree

Income(Rs.)

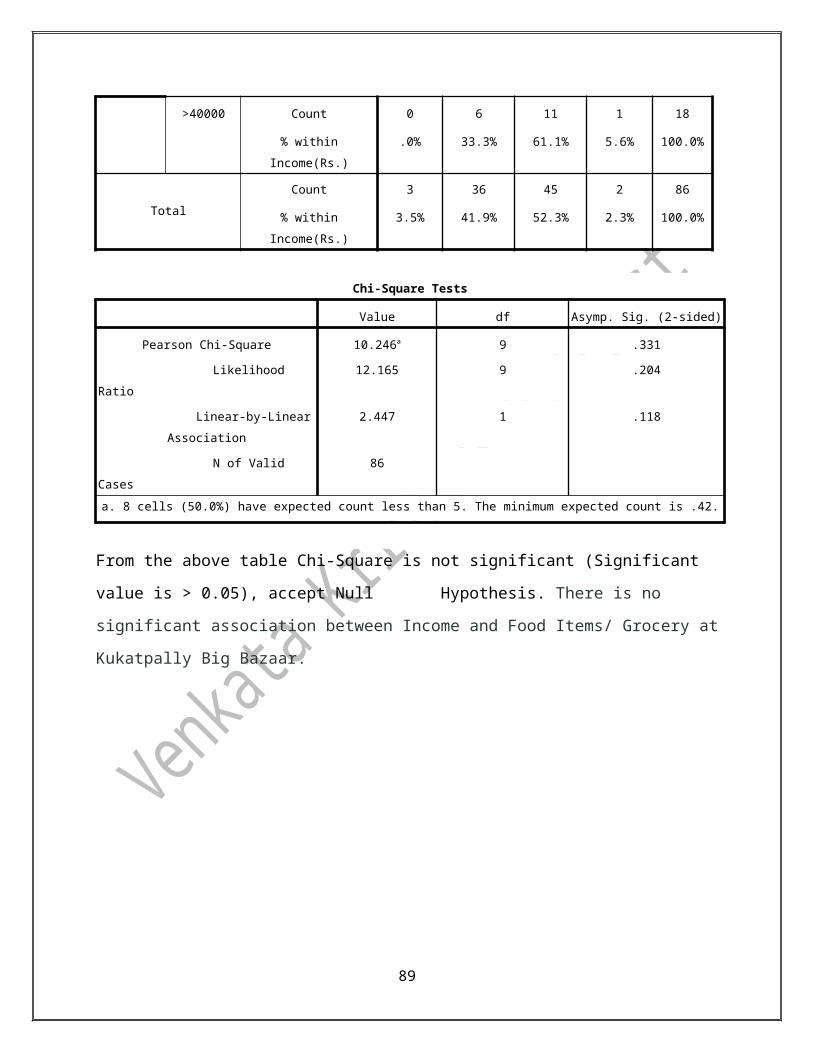

NIL Count 2 9 14 0 25

% within Income(Rs.) 8.0% 36.0% 56.0% .0% 100.0%

<20000 Count 1 12 6 1 20

% within Income(Rs.) 5.0% 60.0% 30.0% 5.0% 100.0%

20000-40000 Count 0 9 14 0 23

% within Income(Rs.) .0% 39.1% 60.9% .0% 100.0%

>40000 Count 0 6 11 1 18

% within Income(Rs.) .0% 33.3% 61.1% 5.6% 100.0%

Total

Count 3 36 45 2 86

% within Income(Rs.) 3.5% 41.9% 52.3% 2.3% 100.0%

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 10.246a 9 .331

Likelihood Ratio 12.165 9 .204

Linear-by-Linear Association 2.447 1 .118

N of Valid Cases 86

a. 8 cells (50.0%) have expected count less than 5. The minimum expected count is .42.

65

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null

Hypothesis. There is no significant association between Income and Food Items/ Grocery at

Kukatpally Big Bazaar.

66

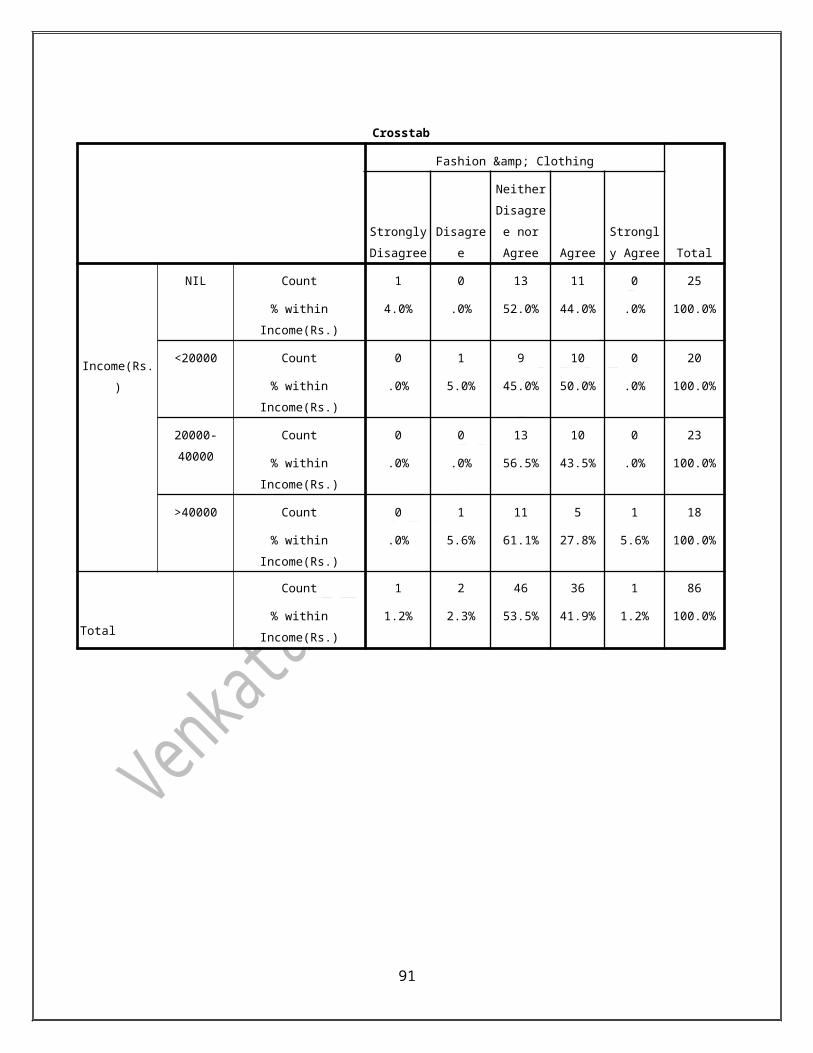

2) Income(Rs.) * Fashion & Clothing

H0: There is no significant association between Income and Fashion & Clothing at

Kukatpally Big Bazaar

Crosstab

Fashion & Clothing

Total

Strongly

Disagree Disagree

Neither

Disagree

nor Agree Agree

Strongly

Agree

Income(Rs.)

NIL Count 1 0 13 11 0 25

% within Income(Rs.) 4.0% .0% 52.0% 44.0% .0% 100.0%

<20000 Count 0 1 9 10 0 20

% within Income(Rs.) .0% 5.0% 45.0% 50.0% .0% 100.0%

20000-40000 Count 0 0 13 10 0 23

% within Income(Rs.) .0% .0% 56.5% 43.5% .0% 100.0%

>40000 Count 0 1 11 5 1 18

% within Income(Rs.) .0% 5.6% 61.1% 27.8% 5.6% 100.0%

Total

Count 1 2 46 36 1 86

% within Income(Rs.) 1.2% 2.3% 53.5% 41.9% 1.2% 100.0%

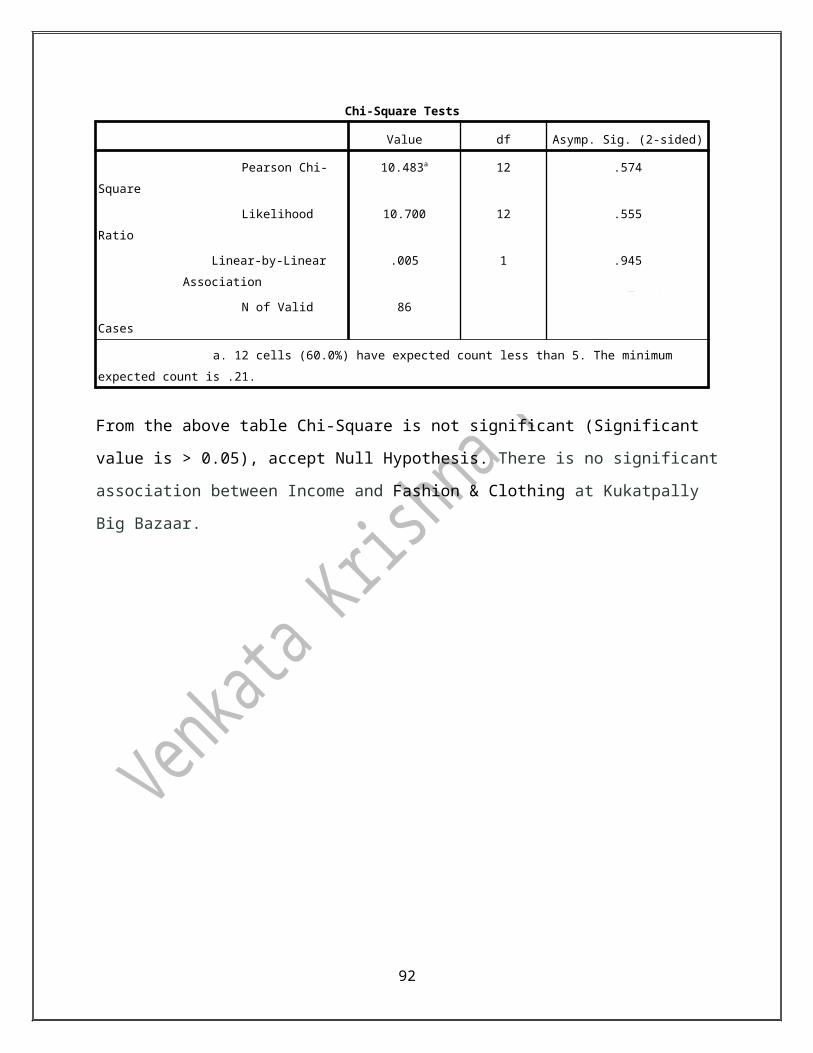

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 10.483a 12 .574

Likelihood Ratio 10.700 12 .555

Linear-by-Linear Association .005 1 .945

N of Valid Cases 86

a. 12 cells (60.0%) have expected count less than 5. The minimum expected count is .21.

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null

Hypothesis. There is no significant association between Income and Fashion & Clothing at

Kukatpally Big Bazaar.

67

68

3) Income(Rs.) * Home App.& décor

H0: There is no significant association between Income and Home appliances & décor at

Kukatpally Big Bazaar.

Crosstab

Home App.& décor

TotalDisagree

Neither Disagree

nor Agree Agree

Income(Rs.)

NIL Count 1 19 5 25

% within Income(Rs.) 4.0% 76.0% 20.0% 100.0%

<20000 Count 0 18 2 20

% within Income(Rs.) .0% 90.0% 10.0% 100.0%

20000-40000 Count 0 17 6 23

% within Income(Rs.) .0% 73.9% 26.1% 100.0%

>40000 Count 0 10 8 18

% within Income(Rs.) .0% 55.6% 44.4% 100.0%

Total

Count 1 64 21 86

% within Income(Rs.) 1.2% 74.4% 24.4% 100.0%

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 8.847a 6 .182

Likelihood Ratio 8.844 6 .183

Linear-by-Linear Association 4.684 1 .030

N of Valid Cases 86

a. 6 cells (50.0%) have expected count less than 5. The minimum expected count is .21.

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null Hypothesis. There is no significant association between Income and Home appliances & décor at Kukatpally Big Bazaar.

69

70

4) Income (Rs.) * Luggage

H0: There is no significant association between Income and Luggage at Kukatpally

Big Bazaar.

Crosstab

Luggage

TotalDisagree

Neither Disagree

nor Agree Agree

Income(Rs.)

NIL Count 0 21 4 25

% within Income(Rs.) .0% 84.0% 16.0% 100.0%

<20000 Count 0 18 2 20

% within Income(Rs.) .0% 90.0% 10.0% 100.0%

20000-40000 Count 0 17 6 23

% within Income(Rs.) .0% 73.9% 26.1% 100.0%

>40000 Count 1 13 4 18

% within Income(Rs.) 5.6% 72.2% 22.2% 100.0%

Total Count 1 69 16 86

% within Income(Rs.) 1.2% 80.2% 18.6% 100.0%

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 6.024a 6 .420

Likelihood Ratio 5.455 6 .487

Linear-by-Linear Association .238 1 .626

N of Valid Cases 86

a. 8 cells (66.7%) have expected count less than 5. The minimum expected count is .21.

From the above table Chi-Square is not significant (Significant value is > 0.05), accept

Null Hypothesis. There is no significant association between Income and Luggage at

Kukatpally Big Bazaar.

71

72

5) Income (Rs.) * Toys & Stationary

H0: There is no significant association between Income and Toys & Stationary at Kukatpally

Big Bazaar.

Crosstab

Toys & Stationary

Total

Neither Disagree

nor Agree Agree

Income(Rs.)

NIL Count 18 7 25

% within Income(Rs.) 72.0% 28.0% 100.0%

<20000 Count 18 2 20

% within Income(Rs.) 90.0% 10.0% 100.0%

20000-40000 Count 17 6 23

% within Income(Rs.) 73.9% 26.1% 100.0%

>40000 Count 13 5 18

% within Income(Rs.) 72.2% 27.8% 100.0%

Total Count 66 20 86

% within Income(Rs.) 76.7% 23.3% 100.0%

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 2.594a 3 .459

Likelihood Ratio 2.960 3 .398

Linear-by-Linear Association .062 1 .803

N of Valid Cases 86

a. 2 cells (25.0%) have expected count less than 5. The minimum expected count is 4.19.

From the above table Chi-Square is not significant (Significant value is > 0.05), accept Null

Hypothesis. There is no significant association between Income and Toys & Stationary at

Kukatpally Big Bazaar.

73

74

6) Income(Rs.) * Electronics

H0: There is no significant association between Income and Electronics at Kukatpally

Big Bazaar.

Crosstab

Electronics

Total

Neither Disagree

nor Agree Agree

Income(Rs.)

NIL Count 19 6 25

% within Income(Rs.) 76.0% 24.0% 100.0%

<20000 Count 18 2 20

% within Income(Rs.) 90.0% 10.0% 100.0%

20000-40000 Count 17 6 23

% within Income(Rs.) 73.9% 26.1% 100.0%

>40000 Count 12 6 18

% within Income(Rs.) 66.7% 33.3% 100.0%

Total Count 66 20 86

% within Income(Rs.) 76.7% 23.3% 100.0%

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 3.104a 3 .376

Likelihood Ratio 3.410 3 .333

Linear-by-Linear Association .871 1 .351

N of Valid Cases 86

a. 2 cells (25.0%) have expected count less than 5. The minimum expected count is 4.19.

From the above table Chi-Square is not significant (Significant value is > 0.05),

accept Null Hypothesis. There is no significant association between Income and

Electronics at Kukatpally Big Bazaar.

75

76

7) Income(Rs.) * Accessories

H0: There is no significant association between Income and Accessories at Kukatpally Big

Bazaar.

Crosstab

Accessories

Total

Neither Disagree

nor Agree Agree

Income(Rs.)

NIL Count 20 5 25

% within Income(Rs.) 80.0% 20.0% 100.0%

<20000 Count 18 2 20

% within Income(Rs.) 90.0% 10.0% 100.0%

20000-40000 Count 18 5 23

% within Income(Rs.) 78.3% 21.7% 100.0%

>40000 Count 15 3 18

% within Income(Rs.) 83.3% 16.7% 100.0%

Total Count 71 15 86

% within Income(Rs.) 82.6% 17.4% 100.0%

Chi-Square Tests

Value df Asymp. Sig. (2-sided)

Pearson Chi-Square 1.185a 3 .757

Likelihood Ratio 1.277 3 .735

Linear-by-Linear Association .000 1 .986

N of Valid Cases 86

a. 4 cells (50.0%) have expected count less than 5. The minimum expected count is 3.14.

From the above table Chi-Square is not significant (Significant value is > 0.05), accept

Null Hypothesis. There is no significant association between Income and Accessories at

Kukatpally Big Bazaar.

77

78

8) How often you visit BB? * Ambience/Service Cross tabulation