Blackmore

BUY-SIDE PRIVATE EQUITY ADVISORY

• A Introduction to Private Equity and How to Succeed

partners

Agenda

Why Now?

How Private Equity Creates Value

Blackmore Programs

What are the Options

Deal Shopping Process

What is an Actionable Deal

What Blackmore Provides Determinants of Growth in 2012

What is Private Equity?

Sample Project Time-Line

Debt Market Summary

Who are the Investors?

Next Steps

Private Equity Acquisition Process

Private Equity Fund Structure

What is a P/E Intermediary?

Current Trend in Private Equity

Types of Transaction by P/E

Types of Deals Blackmore Looks for

Your Role

19 3

4

5

8

9

12

15

17

18

50

40

36

35

30

22

52

53

54

14

Blackmore Provides

• are considered a respected intermedary by the industry • are paid by PE to help, place you in a company or share closing fees with you Maintain relationships with… • 1,500 PE firms in U.S. • 8,000 PE firms globally • We narrow focus to 50 – 200 specific PE groups.

• Provide “back-ups” in case deal falls through.

• Option to Co-invest in company

• Significantly lower sale price than investment banking sale = More initial wealth creation for you •Receive Finders/Consulting fee for “lining up” deals.

•Experienced guidance through acquisition Process.

• Payment from Private equity firm.

You Gain We…

Compensation Fee Seller - 98% Executuve Fee- .08%

Blackmore Fee- 1.2% Compensation

• Placed executives receive a minimum of 5% equity in new company, without capital investment. • Generally increased salaries and bonus packages.

If you do not meet the buyers requirements to run a company then you can benefit from our Finder Program •Line up deals and get paid out of our Fee •From 5% -40%

Blackmore Programs

Connectors Backed

Executives Requirements

• +10 years of industry experience • Direct operational P/L responsibilities of +$100 M (or, approximately double size of acquired company) • References that support you as CEO •Previous role as CEO, COO, GM, President, VP operations

And/Or

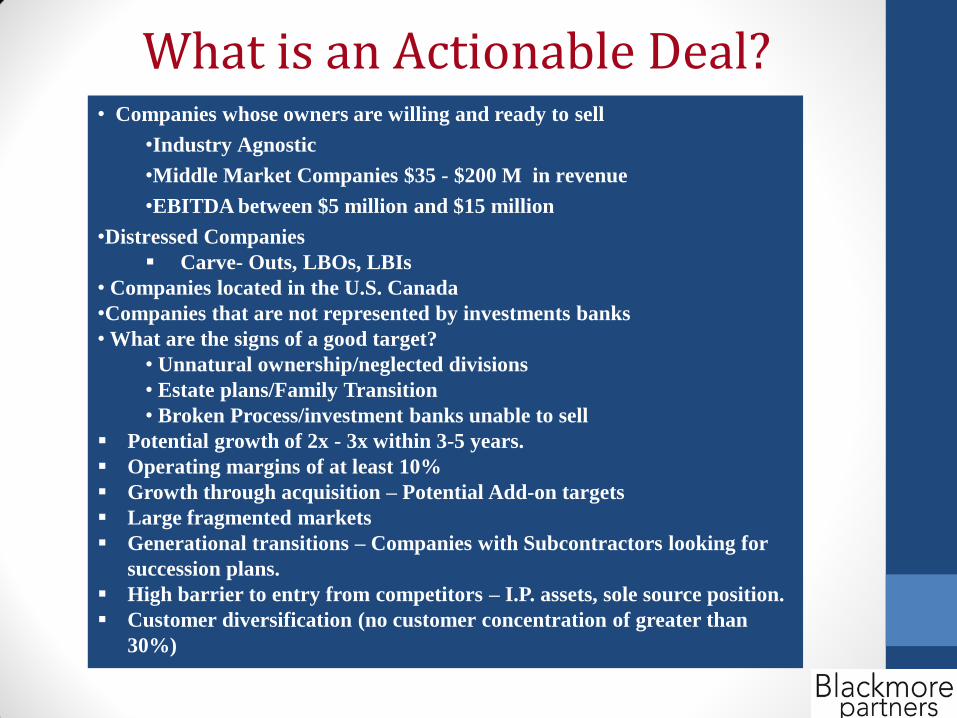

What is an Actionable Deal? • Companies whose owners are willing and ready to sell

•Industry Agnostic

•Middle Market Companies $35 - $200 M in revenue

•EBITDA between $5 million and $15 million

•Distressed Companies

Carve- Outs, LBOs, LBIs

• Companies located in the U.S. Canada

•Companies that are not represented by investments banks

• What are the signs of a good target?

• Unnatural ownership/neglected divisions

• Estate plans/Family Transition

• Broken Process/investment banks unable to sell

Potential growth of 2x - 3x within 3-5 years.

Operating margins of at least 10%

Growth through acquisition – Potential Add-on targets

Large fragmented markets

Generational transitions – Companies with Subcontractors looking for

succession plans.

High barrier to entry from competitors – I.P. assets, sole source position.

Customer diversification (no customer concentration of greater than

30%)

WHY IS NOW A GREAT TIME TO BUY A BUSINESS?

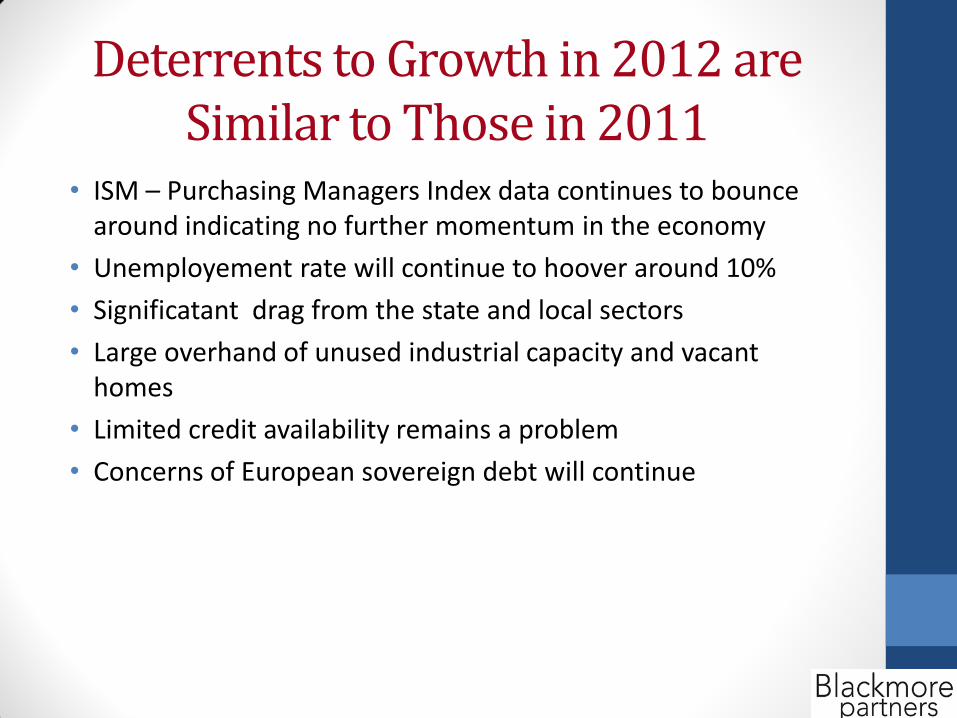

Deterrents to Growth in 2012 are Similar to Those in 2011

• ISM – Purchasing Managers Index data continues to bounce around indicating no further momentum in the economy

• Unemployement rate will continue to hoover around 10%

• Significatant drag from the state and local sectors

• Large overhand of unused industrial capacity and vacant homes

• Limited credit availability remains a problem

• Concerns of European sovereign debt will continue

Ten-year transfer cycle

Current seller’s market Taxes are going up in 2013

In the next 15 years, eight million business owners will exit

The number of buyers will remain stable

More supply and limited demand means a lower multiple paid for businesses

Post recession means many markets are

at bottom of cycle and will reverse course

Deal timeline

We can get deals funded in as little as 90 days from now if there is a ready, willing and able seller.

A sale will take from 12 to 24 months to complete in our normal process.

An owner considering retirement in the near future is advised to begin the selling process as early as possible

Why now?

Source: Rob Slee – Midas Nation

Create true wealth by gaining equity in your company

WHAT ARE THE OPTIONS?

What are the options?

Start your own business

Less capital needed for investment

Pride of building own company

Time consuming to establish

Initial cash flow issues

Buy a company without partners

Structure and organization in place

100% of equity and ability to control

Potentially smaller business

Limited resources and capabilities

Employ CEO for succession plan

opportunity

Less capital needed

Reasonable transition time

Ego of owner

Inability to control timing, direction

Buy a company with PE partner

Able to buy bigger company

Capital and expertise provided

Private equity could be ruthless

Short time frame for value creation

Pros & Cons Options Goals

Ownership of a

business

Buying With Private Equity Partner

ON ACQUISITION ON EXIT

Revenue $ 25,000,000 $ 32,000,000

Revenue Growth 28%

EBITDA

5,000,000 20.0%

8,000,000 25.0%

EBITDA Growth 60%

EBITDA Multiple 4.0X 5.0X

Enterprise Value 20,000,000 40,000,000

Typical Structure

Debt 12,000,000 60.0% 12,000,000 30.0%

Equity 8,000,000 40.0% 28,000,000 70.0%

20,000,000 100.0% 40,000,000 100.0%

Injected Equity

Management Team 500,000 6.3% 3,990,000 14.3%

PEG 7,500,000 93.8% 24,010,000 85.8%

$ 8,000,000 100.0% $ 28,000,000 100.0%

Increase in management ownership with stock options 8%

Buying with no Partner

ON ACQUISITION ON EXIT

Revenue $ 2,083,333 $ 6,514,286

Revenue Growth 213%

EBITDA 416,667 20.0%

1,628,571 25.0%

EBITDA Growth 291%

EBITDA Multiple 3.0X 3.5X

Enterprise Value 1,250,000 5,700,000

Typical Structure

Debt 750,000 60.0% 1,710,000 30.0%

Equity 500,000 40.0% 3,990,000 70.0%

1,250,000 100.0% 5,700,000 100.0%

Injected Equity

Management Team 500,000 100.0% 3,990,000 100.0%

PEG - 0.0% - 0.0%

$ 500,000 100.0% $ 3,990,000 100.0%

What are the options?

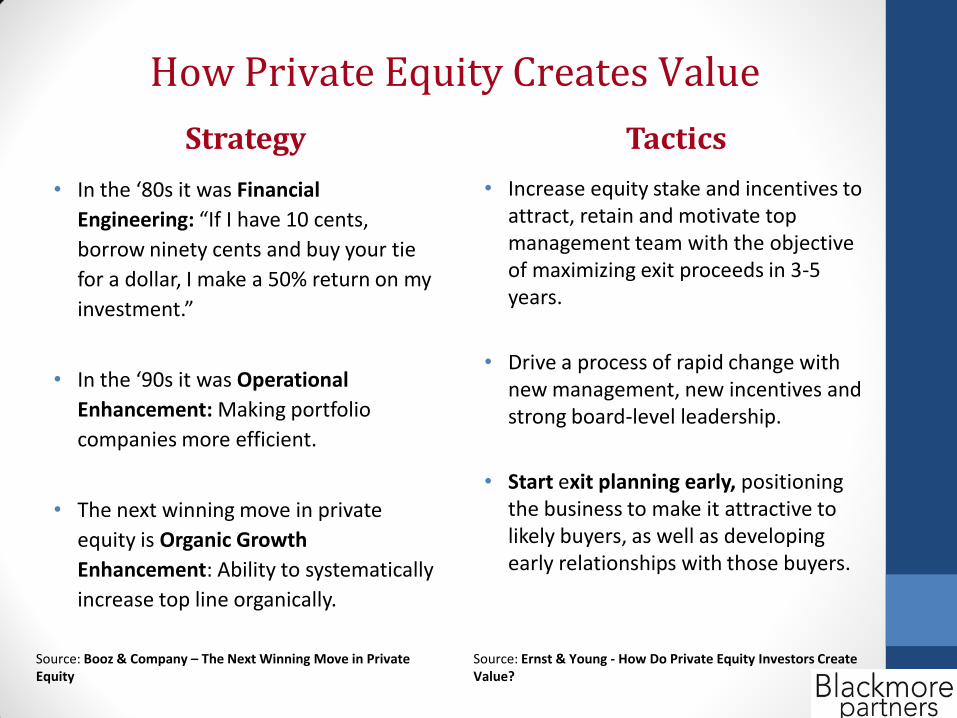

Strategy

• In the ‘80s it was Financial

Engineering: “If I have 10 cents,

borrow ninety cents and buy your tie

for a dollar, I make a 50% return on my

investment.”

• In the ‘90s it was Operational

Enhancement: Making portfolio

companies more efficient.

• The next winning move in private

equity is Organic Growth

Enhancement: Ability to systematically

increase top line organically.

Tactics

• Increase equity stake and incentives to attract, retain and motivate top management team with the objective of maximizing exit proceeds in 3-5 years.

• Drive a process of rapid change with new management, new incentives and strong board-level leadership.

• Start exit planning early, positioning the business to make it attractive to likely buyers, as well as developing early relationships with those buyers.

How Private Equity Creates Value

Source: Ernst & Young - How Do Private Equity Investors Create Value?

Source: Booz & Company – The Next Winning Move in Private Equity

THE PRIVATE EQUITY PROCESS

Deal Shopping Process

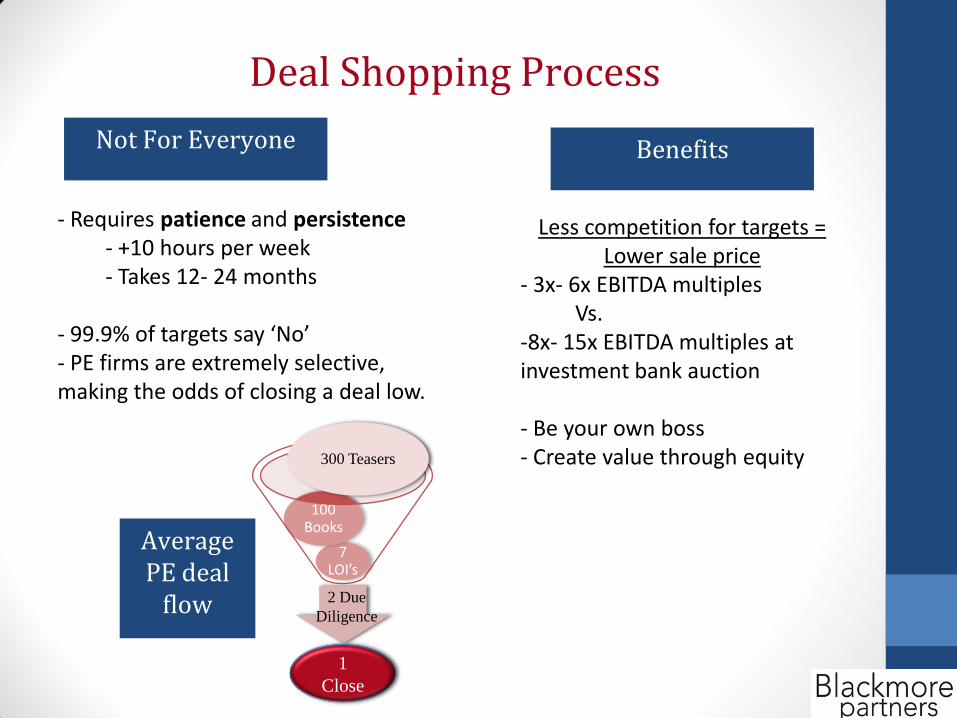

Not For Everyone

- Requires patience and persistence - +10 hours per week - Takes 12- 24 months

- 99.9% of targets say ‘No’ - PE firms are extremely selective, making the odds of closing a deal low.

7 LOI’s

100 Books

300 Teasers

2 Due

Diligence

1

Close

Average PE deal

flow

Benefits

Less competition for targets = Lower sale price

- 3x- 6x EBITDA multiples Vs. -8x- 15x EBITDA multiples at investment bank auction - Be your own boss - Create value through equity

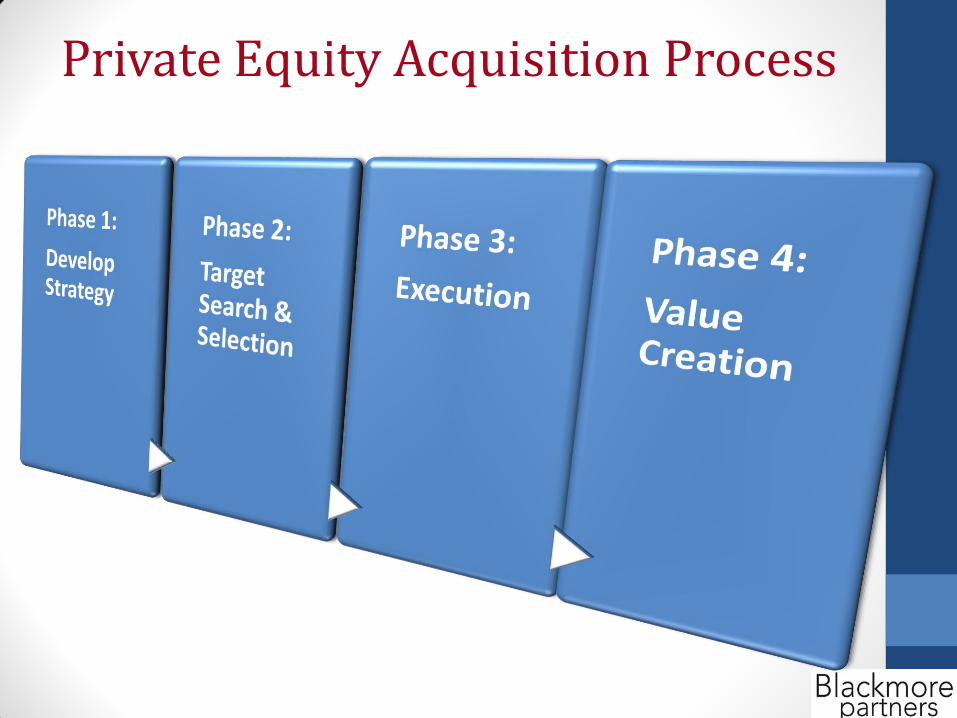

Private Equity Acquisition Process

Key activities and deliverables

Develop Strategy

Target Search & Selection

Execution Value

Creation

Establish relationship with qualified target businesses and PE partner

Executive acquisition process

Goals and outcomes

Create a vision and focus to establish the acquisition framework

Work toward closing a transaction with a PE partner

Drive innovation to achieve competitive advantage and a streamlined organization

Industry niche selection and research

Acquisition criteria summary

Buy-side teaser Executive’s

resume

Initial identification and screening

Target and PE profiling and contacting

Target and PE selection

Letter of intent Due diligence Investment

information memo and financial model

Finalize the deal

Align management and incentives

Establish and execute business plan

Operational improvements

Phase 1 Phase 2 Phase 3 Phase 4

Private Equity Acquisition Process

Backed Executives

Connectors

Next Steps

1. This is a formal process in which we meet every two weeks by phone. All meetings are 15-30 minutes. • Schedule a 1 to 1phone meeting by emailing • [email protected]

2. The process will take 10 hrs a week. I will email you the next steps, involving approximately of 2hrs due diligence on your part. 3. We will identify 100’s target by searching our database (NAICS) and by

Blackmore paying brokers who will search for targets on your behalf. In addition, we will reach out to our 8000 execs on linkedin to help you.

1. We can make this a formal process or ad-hoc 2. Send me a note at [email protected] to set up 1- to - 1 phone meeting to discuss opportunities.

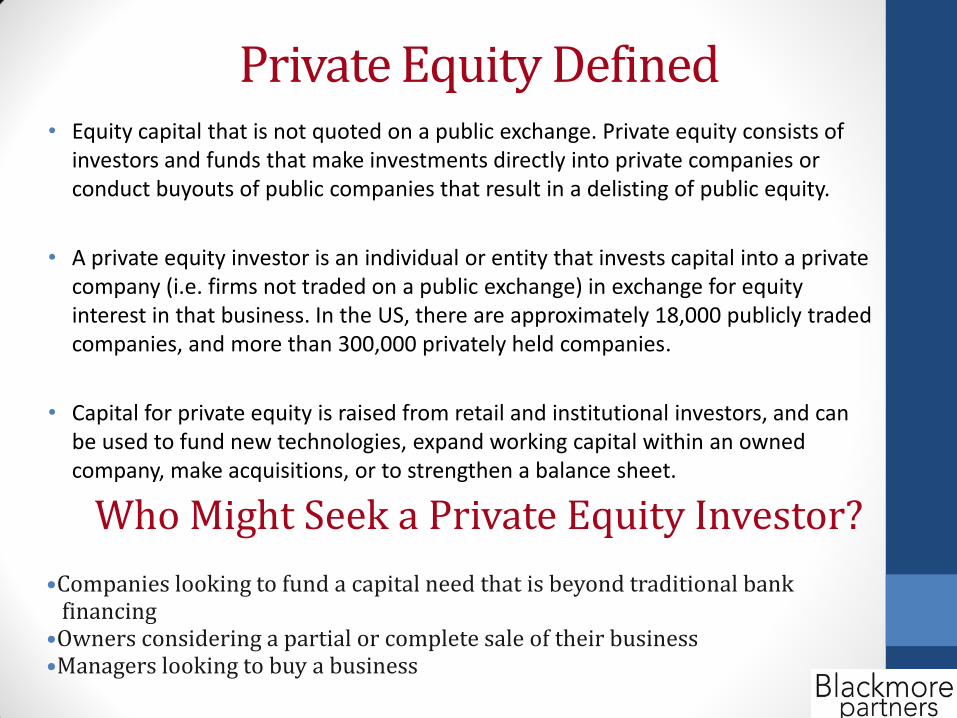

What is Private Equity?

Private Equity Defined • Equity capital that is not quoted on a public exchange. Private equity consists of

investors and funds that make investments directly into private companies or conduct buyouts of public companies that result in a delisting of public equity.

• A private equity investor is an individual or entity that invests capital into a private company (i.e. firms not traded on a public exchange) in exchange for equity interest in that business. In the US, there are approximately 18,000 publicly traded companies, and more than 300,000 privately held companies.

• Capital for private equity is raised from retail and institutional investors, and can be used to fund new technologies, expand working capital within an owned company, make acquisitions, or to strengthen a balance sheet.

Who Might Seek a Private Equity Investor?

•Companies looking to fund a capital need that is beyond traditional bank financing •Owners considering a partial or complete sale of their business •Managers looking to buy a business

A Brief History of Private Equity

• During the 25 years from 1980 to 2005, the top-quartile private equity firms generated annualized returns to investors of 39.1percent (net of all fees and expenses). By contrast, the S&P 500 returned 12.3 percent a year during the same period.

• Since 2006 the returns have declined and even become negative during the recession

Companies Owned by Private Equity

• J.D. Byrider

• AMC Theaters

• Linens ‘N Things

• Hertz

• Michael’s

• J. Crew

• Petco

• Travelocity

• Toys ‘R Us

• LL Bean

• Levi’s

• Bausch & Lomb

• Polaroid

Who are the investors?

• Public pension funds, university endowments, and leading foundations; these funds represent the single largest group of investors in PE and collectively accounted for one-third of all capital allocated to private equity in 2006

• Individual Investors, Other institutional investors (insurance)

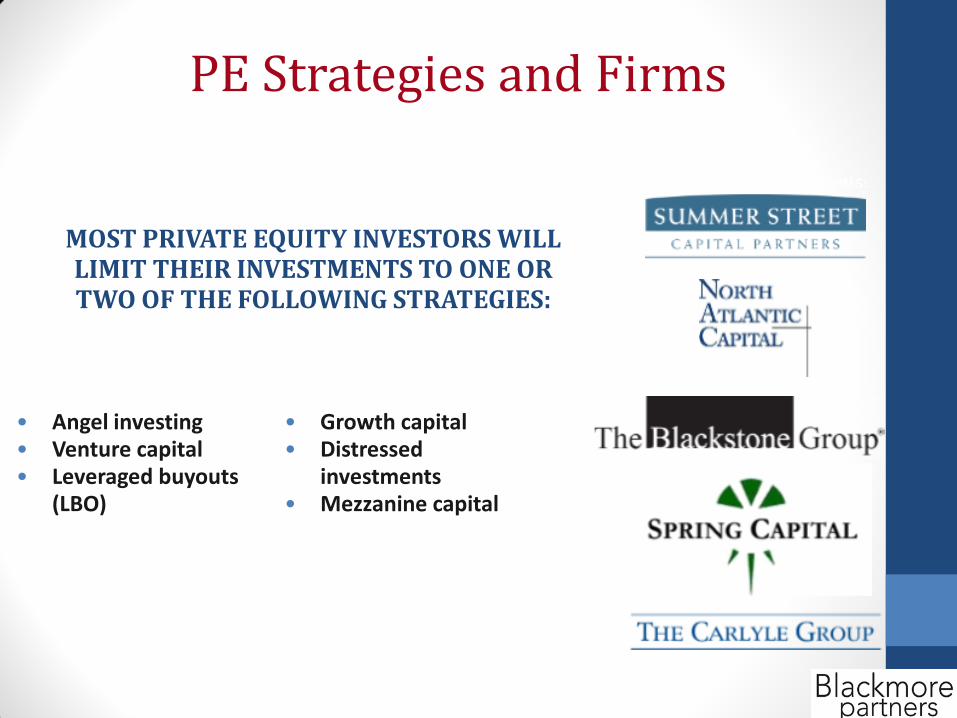

Private equity strategies. EXAMPLES OF PRIVATE EQUITY FIRMS:

MOST PRIVATE EQUITY INVESTORS WILL LIMIT THEIR INVESTMENTS TO ONE OR TWO OF THE FOLLOWING STRATEGIES:

• Angel investing • Venture capital • Leveraged buyouts

(LBO)

• Growth capital • Distressed

investments • Mezzanine capital

PE Strategies and Firms

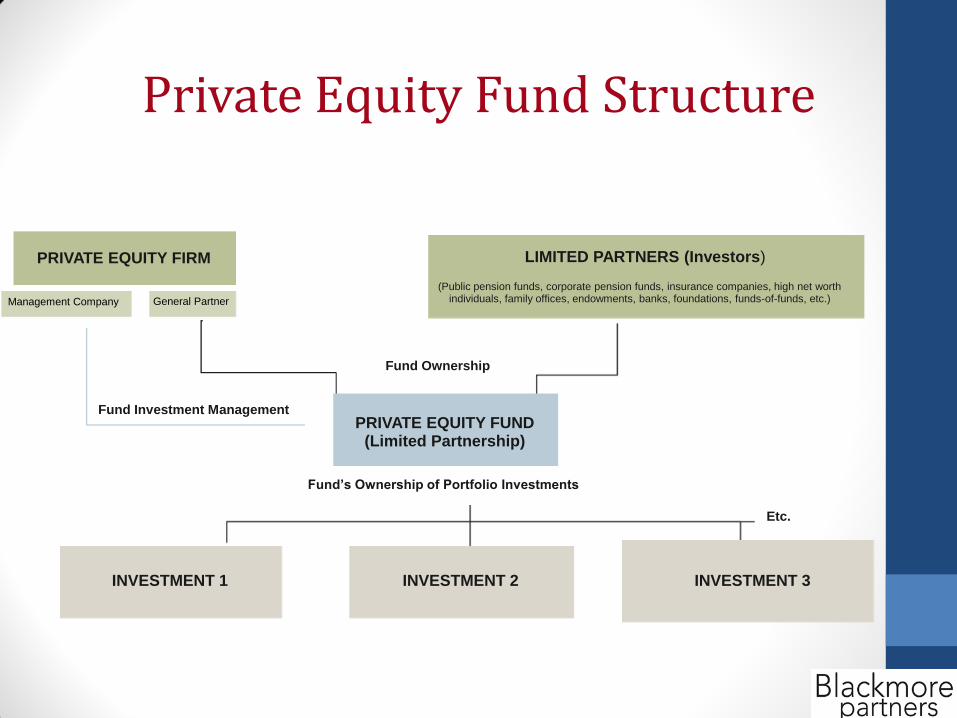

Private Equity Fund Structure

Etc.

Fund Ownership

PRIVATE EQUITY FIRM

Management Company

INVESTMENT 1 INVESTMENT 3 INVESTMENT 2

Fund Investment Management

Fund’s Ownership of Portfolio Investments

General Partner

PRIVATE EQUITY FUND

(Limited Partnership)

LIMITED PARTNERS (Investors)

(Public pension funds, corporate pension funds, insurance companies, high net worth individuals, family offices, endowments, banks, foundations, funds-of-funds, etc.)

Sources of capital for PE funds

• Firms with a dedicated fund, with the majority of the capital sourced from institutional investors (i.e. pension funds, banks, endowments, etc.) and accredited investors (i.e. high net worth individual investors)

• Firms that raise capital from investors on a per-deal basis (pledge funds)

THERE ARE TWO TYPES OF PRIVATE EQUITY FIRMS:

• Typical investment period is 3−10 years, after which capital is distributed to investors

• Rates of return are higher than public market returns, typically 15−30%, depending on the strategy

INVESTMENT DURATION AND RETURNS.

What is a Private Equity Intermediary?

• A PE intermediary sources (informs) deals to private equity firms for a fee.

• Blackmore gets “target” companies from its network of CEOs, which is termed a “deal”

• These deals are pitched to Private Equity firms as an investment package with 2 parts:

1. A CEO and management team

2. A specific company or companies

Types of Transactions by PE

• LBO (Leveraged Buy-out): The acquisition of another company using a significant amount of borrowed money (bonds or loans) to meet the cost of acquisition. Often, the assets of the company being acquired are used as collateral for the loans in addition to the assets of the acquiring company. The purpose of leveraged buyouts is to allow companies to make large acquisitions without having to commit a lot of capital.

• MBO (Management Buy-out): When the managers and/or executives of a company purchase controlling interest in a company from existing shareholders.

More Types of Transactions by PE

• Management Buy-In (MBI): Outside executive team is buying out the current management/owners

• Corporate Carve-out/Spinoff: Corporation is selling off/divesting a division of its company-can be an MBO or MBI

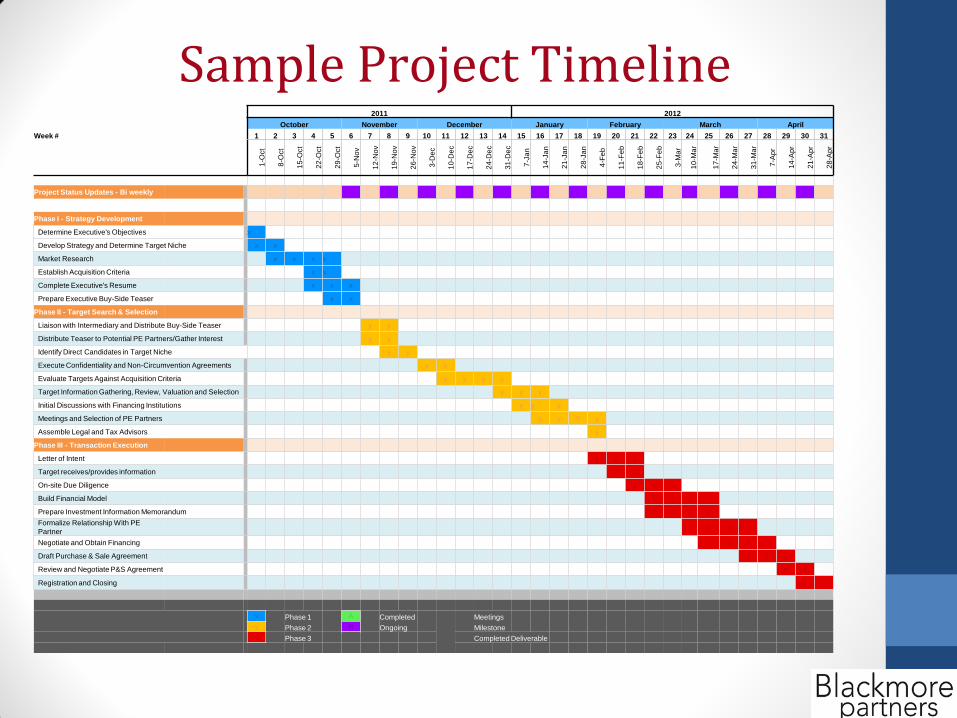

Sample Project Timeline 2011 2012

October November December January February March April

Week # 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31

1-O

ct

8-O

ct

15

-Oct

22

-Oct

29

-Oct

5-N

ov

12

-No

v

19

-No

v

26

-No

v

3-D

ec

10

-De

c

17

-De

c

24

-De

c

31

-De

c

7-J

an

14

-Ja

n

21

-Ja

n

28

-Ja

n

4-F

eb

11

-Fe

b

18

-Fe

b

25

-Fe

b

3-M

ar

10

-Ma

r

17

-Ma

r

24

-Ma

r

31

-Ma

r

7-A

pr

14

-Ap

r

21

-Ap

r

28

-Ap

r

Project Status Updates - Bi weekly

Phase I - Strategy Development

Determine Executive's Objectives x

Develop Strategy and Determine Target Niche x x

Market Research x x x x

Establish Acquisition Criteria x x

Complete Executive's Resume x x x

Prepare Executive Buy-Side Teaser x x

Phase II - Target Search & Selection

Liaison with Intermediary and Distribute Buy-Side Teaser y y

Distribute Teaser to Potential PE Partners/Gather Interest y y

Identify Direct Candidates in Target Niche y y

Execute Confidentiality and Non-Circumvention Agreements y y

Evaluate Targets Against Acquisition Criteria y y y y

Target Information Gathering, Review, Valuation and Selection y y y

Initial Discussions with Financing Institutions y y y

Meetings and Selection of PE Partners y y Y y

Assemble Legal and Tax Advisors y

Phase III - Transaction Execution

Letter of Intent z z z

Target receives/provides information z z

On-site Due Diligence z z z

Build Financial Model z z z z

Prepare Investment Information Memorandum z z z z

Formalize Relationship With PE

Partner z z z z

Negotiate and Obtain Financing z z z z

Draft Purchase & Sale Agreement z z z

Review and Negotiate P&S Agreement z z

Registration and Closing z z

x Phase 1 A Completed Meetings

y Phase 2 B Ongoing Milestone

z Phase 3 Completed Deliverable

Backed Executives

Acquisition Advisors

Next Steps

1. This is a formal process in which we meet every two weeks by phone. All meetings are 15-30 minutes.

Schedule a 1 on 1 phone meeting by emailing [email protected]

2. The process will take 10 hrs a week. I will email you the next steps, involving approximately of 2 hours of due diligence on your part. 3. We will identify 100’s target by searching our database (NAICS) and by

Blackmore paying brokers who will search for targets on your behalf. In addition, we will reach out to our 8000 execs on linkedin to help you.

1. We can make this a formal process or ad-hoc 2. Send me a note at [email protected] to set up 1 on 1 phone meeting to discuss opportunities.

Pre-Seed Seed Venture and

Early Stage Growth and Expansion

Buyout and Recapitalization

• Pre-revenue/start-up

• Building management team

• Early stage product

development

• Significant market opportunity

• $500K-5MM in revenue

• Management team near

complete

• Commercial acceptance

• Significant market

opportunity

• Profitable, with TTM revenue of $3MM+

• Mature management team

• Year-over-year revenue

growth

• Defensible market position

• Revenue greater than $10MM

• Mature management team

• Growth strategy − organic or

acquisition

• Defensible market position

Seed and Angel Venture Capital

Private Equity

Mezzanine Funding

Distressed Investments

Private Equity Investment Strategies

Mission of Private Equity Funds

• Ultimately, the mangers of private equity firms understand that they must improve the underlying value of the companies they own over time to generate the returns their investors demand and to attract the capital they will want to raise for future funds.

Current Trends in PE

• Multiples are creeping up again, were down in last 2 years, now at 4-6x

• 2011: Owners have been hanging on to their firms through the crisis, need to sell

• Overleveraging in 2006-07 is resulting in distressed debt, IRR’s negative in 2008-9

• Funds-Use it or lose it

• Fund timeline: typically 10 years. First 5 years is to invest, last 5 years is to exit

$40 $83

$126

$174

$305

$570

$195

$62

$158

$100

840

1,221

1,679

2,029

2,519

3,025

2,216

1,363

1,778

1,244

0

500

1,000

1,500

2,000

2,500

3,000

3,500

$0

$100

$200

$300

$400

$500

$600

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Capital Invested ($B) # of Deals Closed *Through 3Q 2011 Source: PitchBook

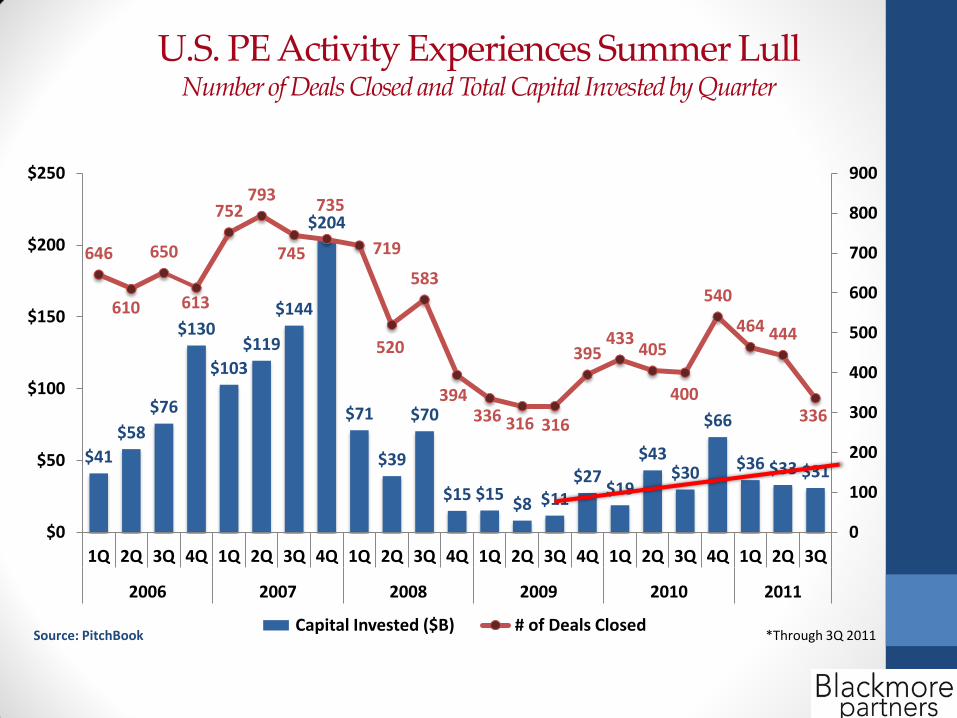

U.S. PE on Pace for Similar Year to 2010 Number of Deals Closed (red line) and Total Capital Invested by Year (blue bars)

$41

$58

$76

$130

$103

$119

$144

$204

$71

$39

$70

$15 $15 $8 $11

$27 $19

$43 $30

$66

$36 $33 $31

646

610

650

613

752 793

745

735

719

520

583

394 336 316 316

395 433

405

400

540

464 444

336

0

100

200

300

400

500

600

700

800

900

$0

$50

$100

$150

$200

$250

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2006 2007 2008 2009 2010 2011

Capital Invested ($B) # of Deals Closed *Through 3Q 2011 Source: PitchBook

U.S. PE Activity Experiences Summer Lull Number of Deals Closed and Total Capital Invested by Quarter

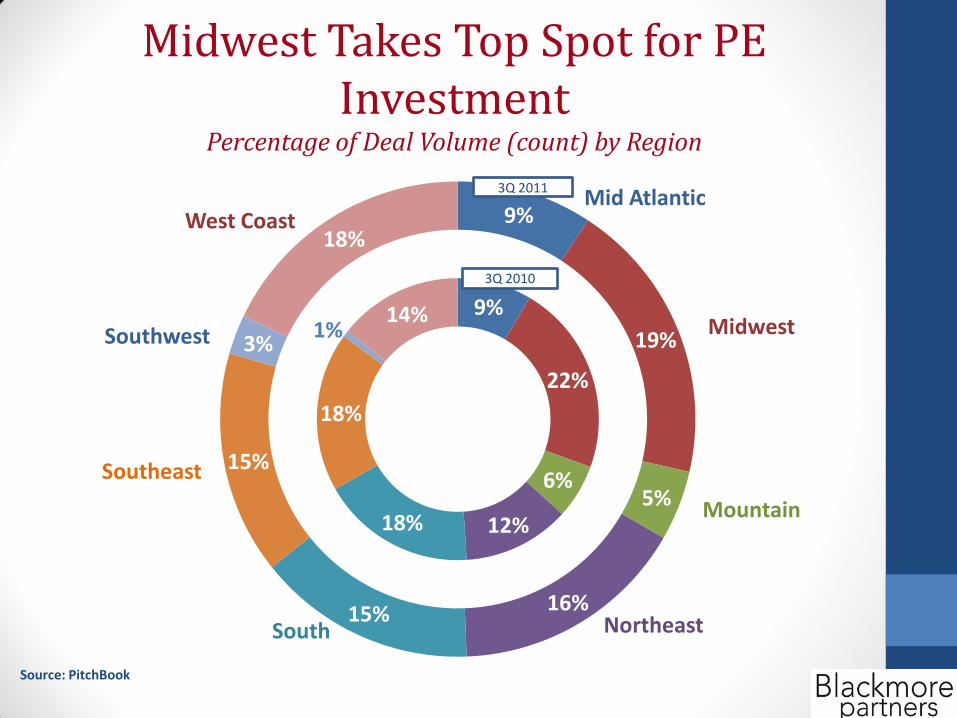

9%

22%

6%

12% 18%

18%

1% 14%

Mid Atlantic

Midwest

Mountain

Northeast South

Southeast

Southwest

West Coast 9%

19%

5%

16% 15%

15%

3%

18%

3Q 2011

3Q 2010

Source: PitchBook

Midwest Takes Top Spot for PE Investment

Percentage of Deal Volume (count) by Region

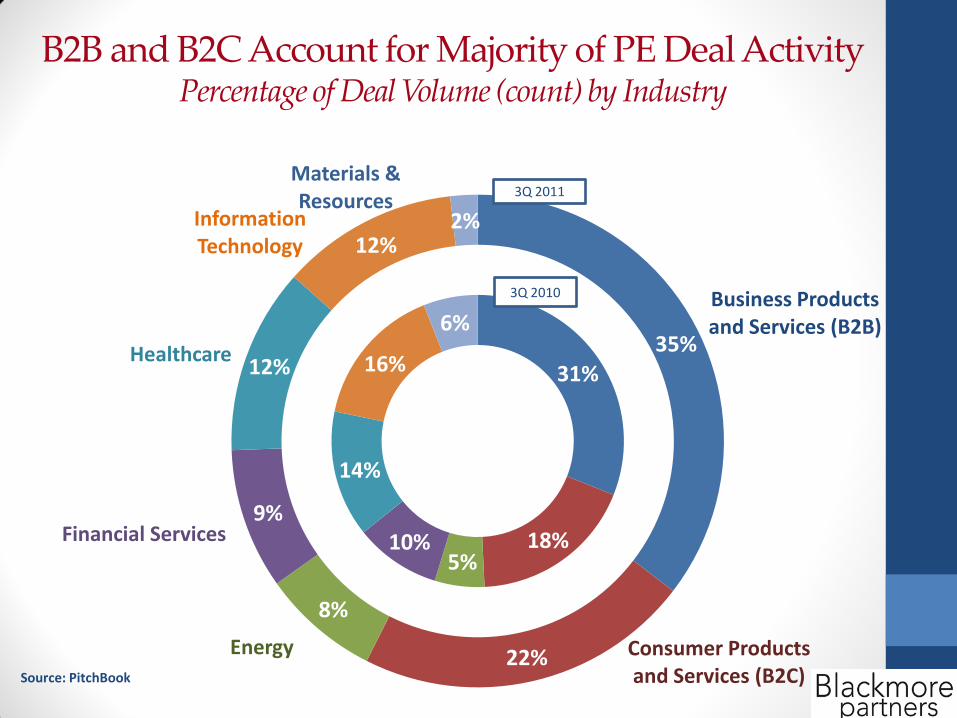

31%

18% 5%

10%

14%

16%

6% Business Products and Services (B2B)

Consumer Products and Services (B2C)

Energy

Financial Services

Healthcare

Information Technology

Materials & Resources

35%

22%

8%

9%

12%

12% 2%

3Q 2011

3Q 2010

Source: PitchBook

B2B and B2C Account for Majority of PE Deal Activity Percentage of Deal Volume (count) by Industry

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

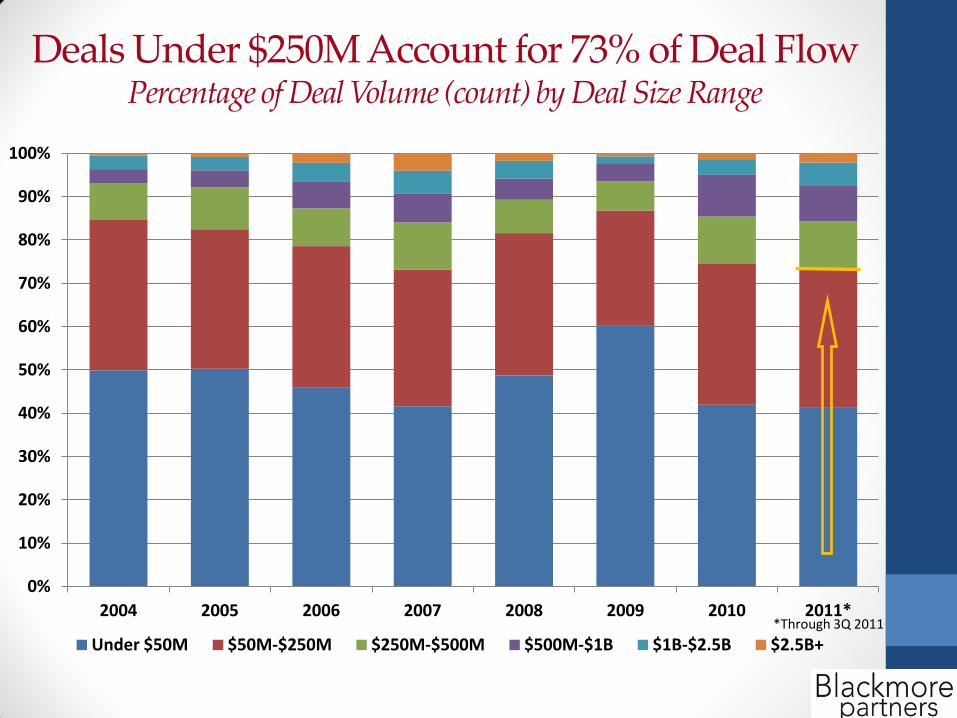

2004 2005 2006 2007 2008 2009 2010 2011*

Under $50M $50M-$250M $250M-$500M $500M-$1B $1B-$2.5B $2.5B+ *Through 3Q 2011

Deals Under $250M Account for 73% of Deal Flow Percentage of Deal Volume (count) by Deal Size Range

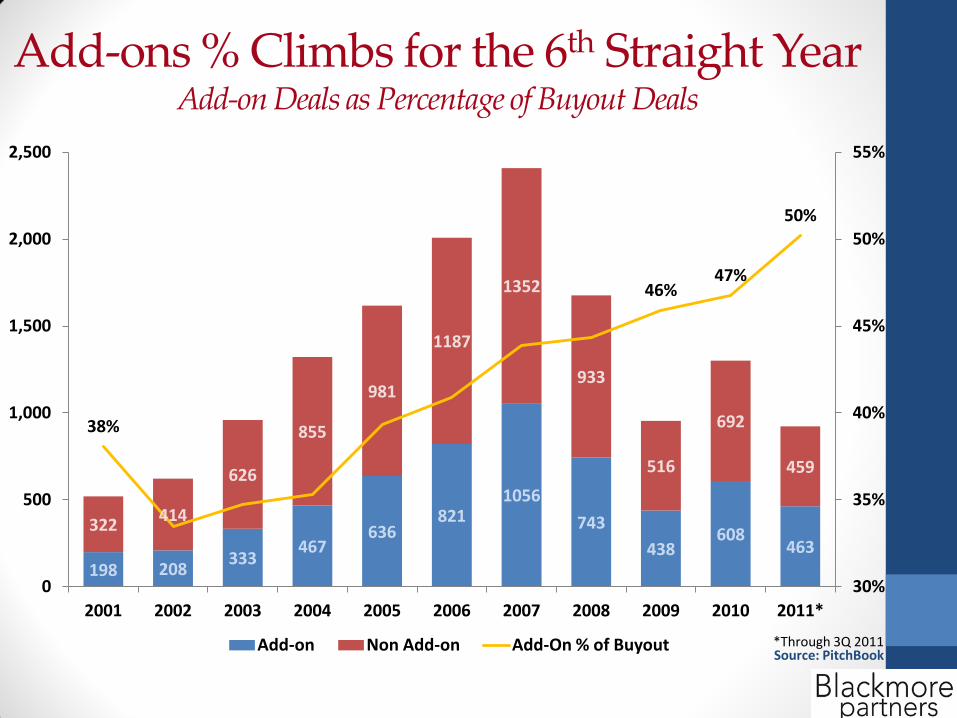

Add-ons % Climbs for the 6th Straight Year Add-on Deals as Percentage of Buyout Deals

198 208 333

467 636

821 1056

743

438 608

463 322

414

626

855

981

1187

1352

933

516

692

459

38%

46% 47%

50%

30%

35%

40%

45%

50%

55%

0

500

1,000

1,500

2,000

2,500

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Add-on Non Add-on Add-On % of Buyout Source: PitchBook *Through 3Q 2011

48% 48%

51%

45%

40%

58% 56%

63%

71%

67%

62%

59%

35%

40%

45%

50%

55%

60%

65%

70%

75%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Under $250M $250M - $1B Over $1B Source: PitchBook *Through 3Q 2011

LBOs Over $1B Using the Most Debt Percentage of Debt Used in Buyouts

4.27

3.85

4.23 3.97

3.68 3.60 3.85 3.92

4.71 4.83

0

1

2

3

4

5

6

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Year

s H

eld

Median Time to Exit - Yr Source: PitchBook

*Through 3Q 2011

PE Firms Holding onto Companies Longer Median Time from Buyout to Exit

U.S. PE Fundraising Experiences Summer Lull Number of Funds Closed and Total Capital Raised by Quarter

$99 $94 $73 $41 $62 $35 $12 $30 $28 $22 $26 $10 $37 $25 $17

121

58

46 43

58

31

12

31

49

31 26 27

41 34

27

0

20

40

60

80

100

120

140

$0

$20

$40

$60

$80

$100

$120

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q

2008 2009 2010 2011

Capital Raised ($B) # of Funds Closed *Through 3Q 2011 Source: PitchBook

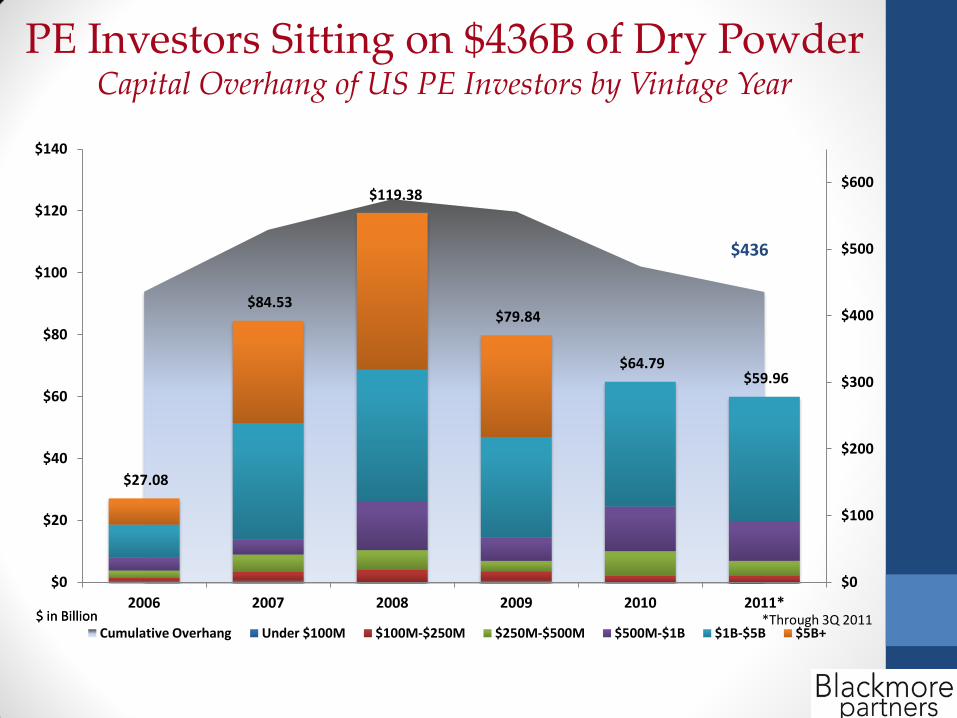

“Over the last few years, there has been a spectacular accumulation of PE dry powder. The U.S. PE capital overhang steadily increased each year from $197 billion in 2004 to $521 billion in 2009. However, it crested in 2009 before dropping to $477 billion as of September 30, 2010. About three-fourths of that dry powder is sitting in funds with vintage years from 2007 to 2009. While the large amount of dry powder is allowing PE firms to pursue bigger, more expensive companies, it has also contributed to a tough fundraising environment, as limited partners wait on distributions before committing capital to new funds.” PITCHBOOK DATA

Recent PE Trend: Dry Powder

PE Investors Sitting on $436B of Dry Powder Capital Overhang of US PE Investors by Vintage Year

$27.08

$84.53

$119.38

$79.84

$64.79 $59.96

$0

$100

$200

$300

$400

$500

$600

$0

$20

$40

$60

$80

$100

$120

$140

2006 2007 2008 2009 2010 2011*

Cumulative Overhang Under $100M $100M-$250M $250M-$500M $500M-$1B $1B-$5B $5B+ $ in Billion $ in Billion

$436

*Through 3Q 2011

Types of Deals Blackmore Looks for

• Headquarters & Majority of Operations in the United States

• Revenues of $30 million+

• EBITDA of $3 million+

• Distressed Opportunities

• CEOs with Operating Experience and $100 million+ Profit/Loss

Your Role

• Understanding a business plan including operations and financials

• Writing a teaser for that plan

• Pitching the deal to different private equity firms based on geographic location, industry, size($)

• Talking to PE firms with the executive of the deal to close the PE buyout

Recommended