CERTIFIED PRE OWNED

THE EVOLUTION AND FUTURE OF CPO IN CANADA

by

Strada IQMarch 2011

BACK IN THE DAY

We have heard all the urban

legends, and jokes from back in the

day about acquiring a used car.

Cars were not reliable when

new, with suspect durability.

You can just imagine when they

were used…it was a leap of faith to

buy a used car (vehicle) or was it?

IS THE CAR SICK?

Chances were good that the car

had at least a few ailments, some

obvious, some not so obvious,

some well camouflaged.

At a time when cars were relatively

simple, with common features, and

standardized components like

distributors, carburetors etc.

It was fraught with perils!

Also relatively easy to quickly

diagnose a car.

ACCIDENTS…

Most cars had frames, the common

knowledge was that if the frame

was not touched, it was only sheet

metal damage.

Some things never change.

Body panels were thick, repairable,

body filler was prevalent.

The various chrome moldings

camouflaged many surface

inaccuracies.

Was it much different than today?

With crush zones for safety frame

damage is prevalent.

BRING A MECHANIC

When cars had common

components, with a widespread

knowledge base.

The informed used car shopper

brought his mechanic with him, to

empower himself while inspecting

the car that was of interest.

The used car salesman as

expected had no clue of what was

wrong with the car.

The vehicle history was word of

mouth, and hear say.

PEACE OF MIND

The prospective used car buyer

was seeking peace of mind in his

purchase.

While the seller had the vehicle

which was already a huge

advantage.

The saying was: “ There is only one

like this one, and I have it”

For the buyer peace of mind was to

bring a knowledgeable mechanic to

empower himself to make a

purchase decision, and negotiate a

price.

HAPPY WITH THE PURCHASE

In most instances the buyer that did

some due diligence, empowered

himself.

Negotiated a price, had the car

reconditioned, by his mechanic.

This individual was satisfied with

his purchase.

Manufacturers literally staid away

from the used car department of

franchised dealers.

Used car dealers were usually

clustered on “used car row” to

facilitate locating used cars.

PROGRESSION

As cars progressed and improved

through the years. While acquiring

increased technology, and

complexity.

The purchase process evolved

supported by various forms of

technology which have become an

intrinsic part of the process.

The prospect/customer is

empowered by the information that

technology disseminates

While the technology content of

most vehicles continues to pose a

formidable challenge.

HOW DID CPO START?

Luxury cars were the first movers in

the voyage towards CPO. When a

used luxury car was the price of a

new “non luxury” car the customer

demanded assurances.

The recession of the early 1990’s

with the ensuing lease

repossessions. The introduction of

GST with the resulting residual

losses by the customers created

the initial steps of the remarketing

process.

Luxury manufacturers subjected to

lease repossessions, and

profoundly upset customers over

residuals losses.

Started connecting the dots.

PAIN

There was immense initial pain, with varying opinions from a myriad

of stakeholders.

Before the gains emerged from the dust and debris of the recession

and GST issues from 20 years ago.

Manufacturer supported used car warranties had been in place for a

short time, with a cursory knowledge base.

Closed end leases gave assurances to customers, and were

fraught with perils for manufacturers, and captive finance. Who had to put “skin in the game”.

The fellow that first offered “walkaway” leases on luxury cars in

Canada rocked the market.

CONNECTING THE DOTS

By connecting the dots the Certified

Pre Owned vehicle slowly emerged

with a distinct identity in the

Canadian used car market.

Initially the domain of luxury cars to

offer assurances to prospective

customers. The CPO pread at a

glacial pace.

“Luxury cars, complex, full of

electronics and black boxes,

expensive to repair”

Until leasing exploded to a high

penetration. The CDN dollar

increased in value.

Remarketing lease returns became

a priority and obligation.

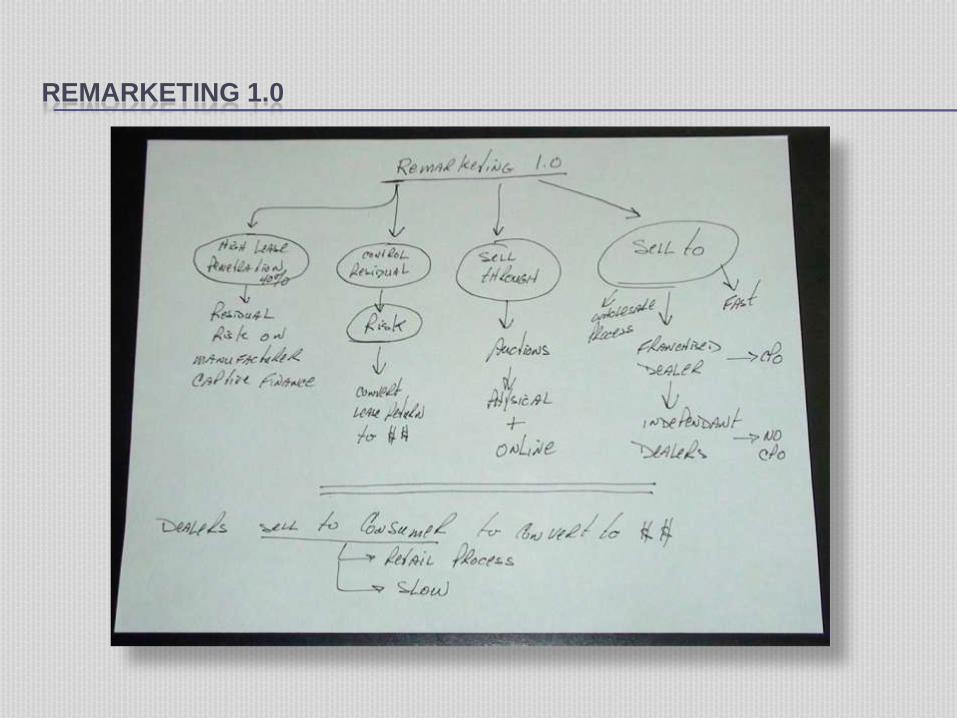

REMARKETING 1.0

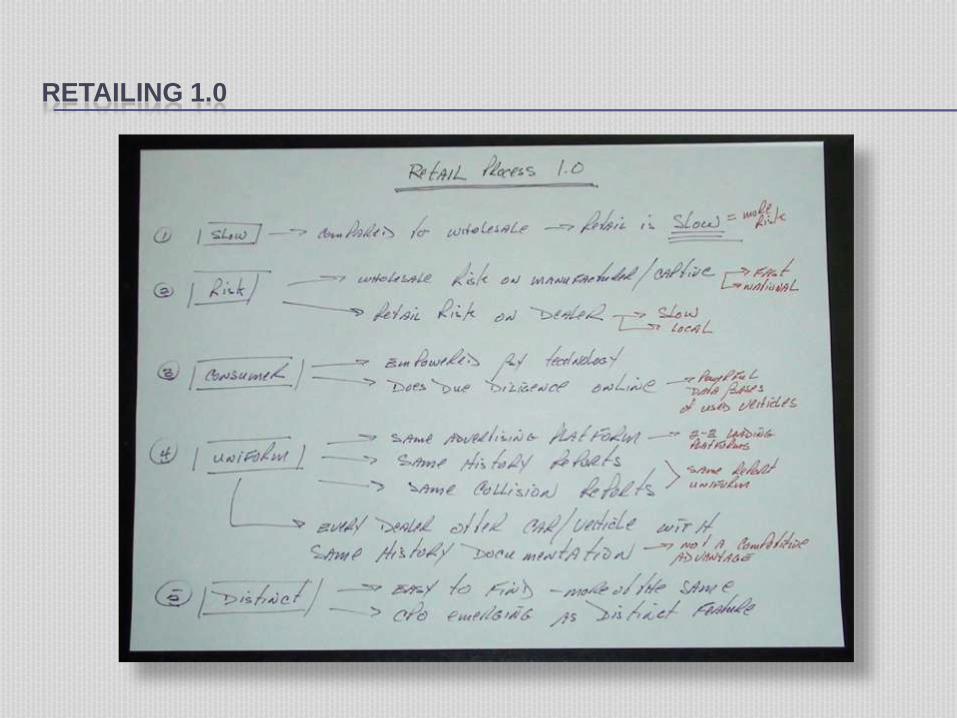

RETAILING 1.0

RELEVANT POINTS OF VERSION 1.0

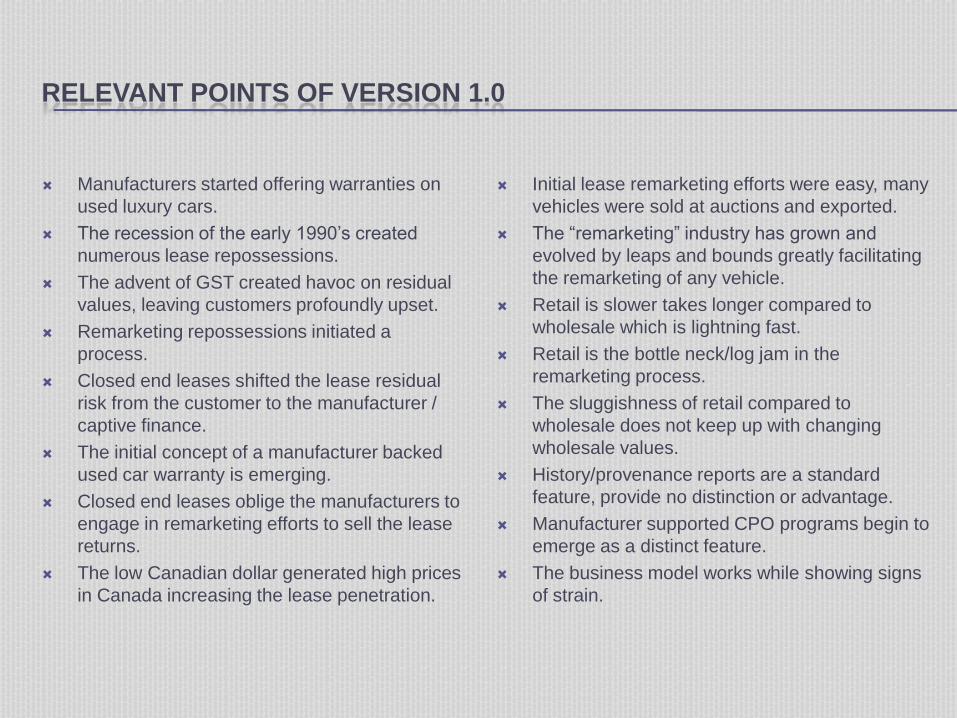

Manufacturers started offering warranties on

used luxury cars.

The recession of the early 1990’s created

numerous lease repossessions.

The advent of GST created havoc on residual

values, leaving customers profoundly upset.

Remarketing repossessions initiated a

process.

Closed end leases shifted the lease residual

risk from the customer to the manufacturer /

captive finance.

The initial concept of a manufacturer backed

used car warranty is emerging.

Closed end leases oblige the manufacturers to

engage in remarketing efforts to sell the lease

returns.

The low Canadian dollar generated high prices

in Canada increasing the lease penetration.

Initial lease remarketing efforts were easy, many

vehicles were sold at auctions and exported.

The “remarketing” industry has grown and

evolved by leaps and bounds greatly facilitating

the remarketing of any vehicle.

Retail is slower takes longer compared to

wholesale which is lightning fast.

Retail is the bottle neck/log jam in the

remarketing process.

The sluggishness of retail compared to

wholesale does not keep up with changing

wholesale values.

History/provenance reports are a standard

feature, provide no distinction or advantage.

Manufacturer supported CPO programs begin to

emerge as a distinct feature.

The business model works while showing signs

of strain.

ASYMMETRIC INFORMATION

The fear in the mind of the

consumer (buyer) was the fact that

the seller knew more about the

vehicle that the buyer.

For decades Asymmetric

Information posed a formidable

barrier to creating a level of trust in

a used vehicle transaction.

The current history reports for used

vehicles diminish the asymmetry of

information while creating a more

“level” playing field.

Increasing technological

complexity, creates an asymmetry

of technology challenging the

peace of mind that a consumer

demands.

ASYMMETRIC TECHNOLOGY

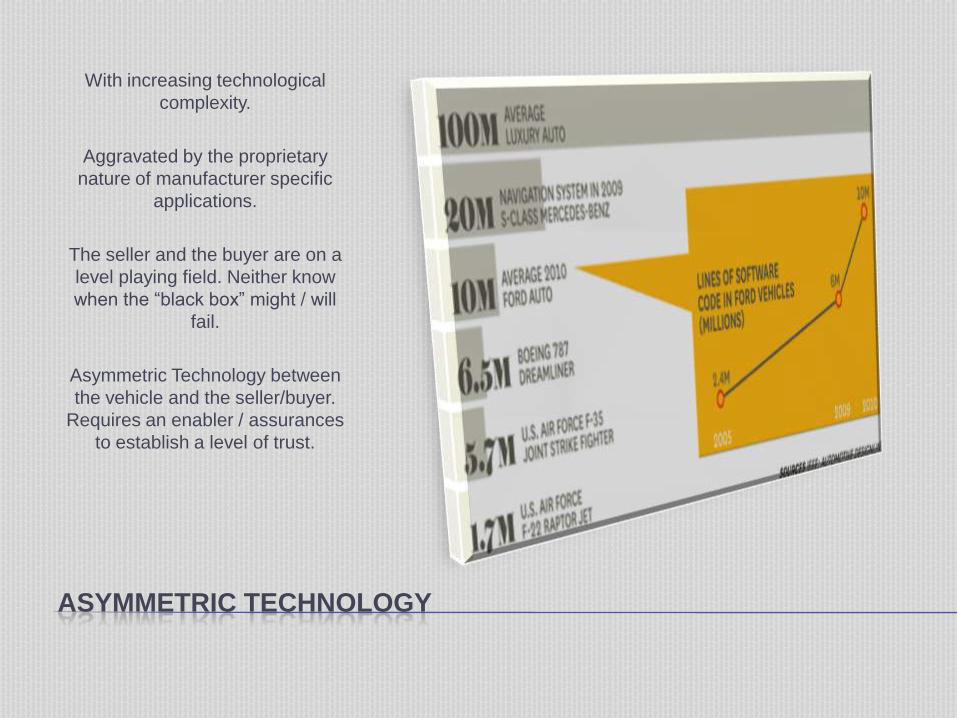

With increasing technological

complexity.

Aggravated by the proprietary

nature of manufacturer specific

applications.

The seller and the buyer are on a

level playing field. Neither know

when the “black box” might / will

fail.

Asymmetric Technology between

the vehicle and the seller/buyer.

Requires an enabler / assurances

to establish a level of trust.

EMERGING CPO

Manufacturer supported used

vehicle program with warranties,

alleviate the asymmetry of

technology.

A rigorous inspection process.

Various incentives applicable to a

CPO vehicle from lower rates, to

return policies.

Luxury dealers are active in CPO

programs more than non luxury

dealers.

The consumer can access a vehicle

that provides a higher level of

confidence and peace of mind.

DOWN THE ROAD IN CANADA

Retail must accelerate in speed of

creating customers and converting

vehicles to money.

The recent demise of leasing the

used vehicle value risk is

transferring from captive finance to

dealers.

The wholesale process is a finely

tuned operation and speed.

The retail process requires

recalibration to achieve a

competitive advantage.

The various technology platforms

are not a replacement for a

comprehensive pre owned

knowledge base.

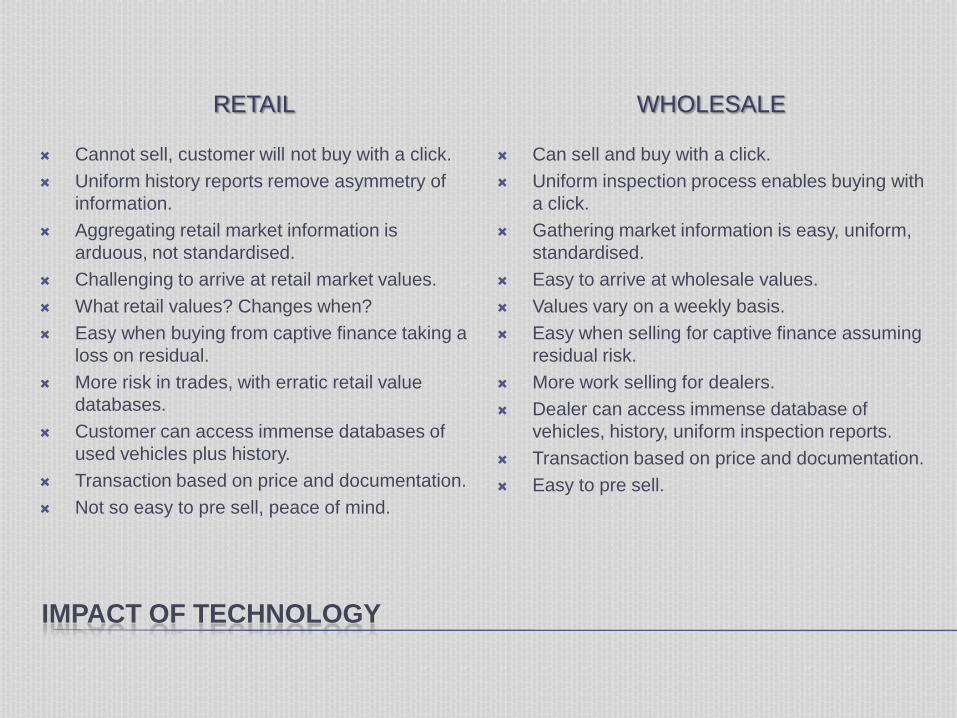

IMPACT OF TECHNOLOGY

RETAIL WHOLESALE

Cannot sell, customer will not buy with a click.

Uniform history reports remove asymmetry of

information.

Aggregating retail market information is

arduous, not standardised.

Challenging to arrive at retail market values.

What retail values? Changes when?

Easy when buying from captive finance taking a

loss on residual.

More risk in trades, with erratic retail value

databases.

Customer can access immense databases of

used vehicles plus history.

Transaction based on price and documentation.

Not so easy to pre sell, peace of mind.

Can sell and buy with a click.

Uniform inspection process enables buying with

a click.

Gathering market information is easy, uniform,

standardised.

Easy to arrive at wholesale values.

Values vary on a weekly basis.

Easy when selling for captive finance assuming

residual risk.

More work selling for dealers.

Dealer can access immense database of

vehicles, history, uniform inspection reports.

Transaction based on price and documentation.

Easy to pre sell.

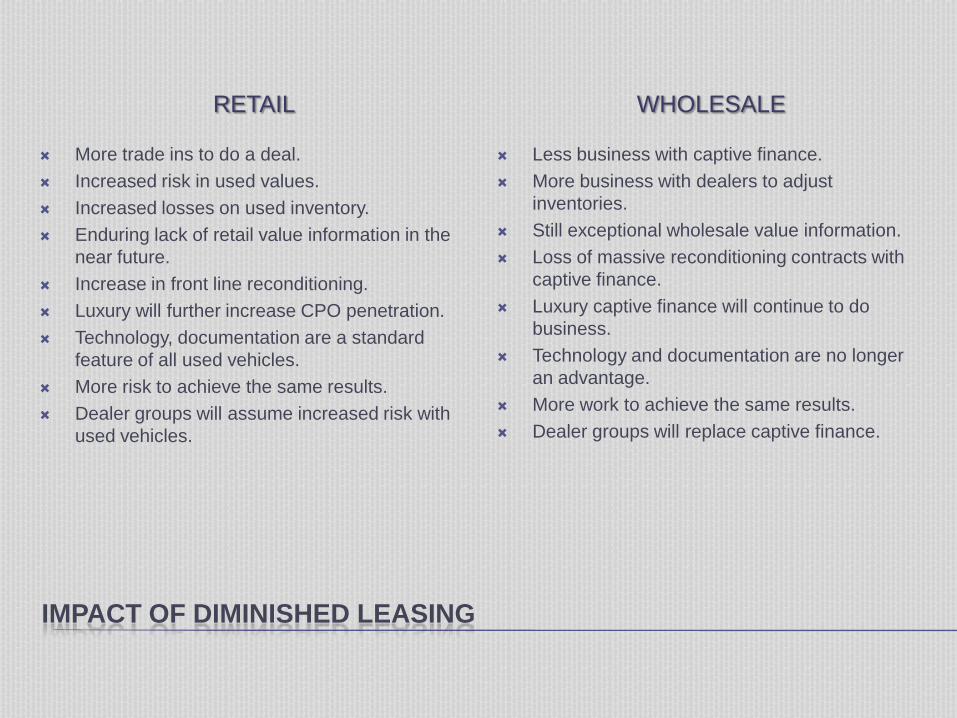

IMPACT OF DIMINISHED LEASING

RETAIL WHOLESALE

More trade ins to do a deal.

Increased risk in used values.

Increased losses on used inventory.

Enduring lack of retail value information in the

near future.

Increase in front line reconditioning.

Luxury will further increase CPO penetration.

Technology, documentation are a standard

feature of all used vehicles.

More risk to achieve the same results.

Dealer groups will assume increased risk with

used vehicles.

Less business with captive finance.

More business with dealers to adjust

inventories.

Still exceptional wholesale value information.

Loss of massive reconditioning contracts with

captive finance.

Luxury captive finance will continue to do

business.

Technology and documentation are no longer

an advantage.

More work to achieve the same results.

Dealer groups will replace captive finance.

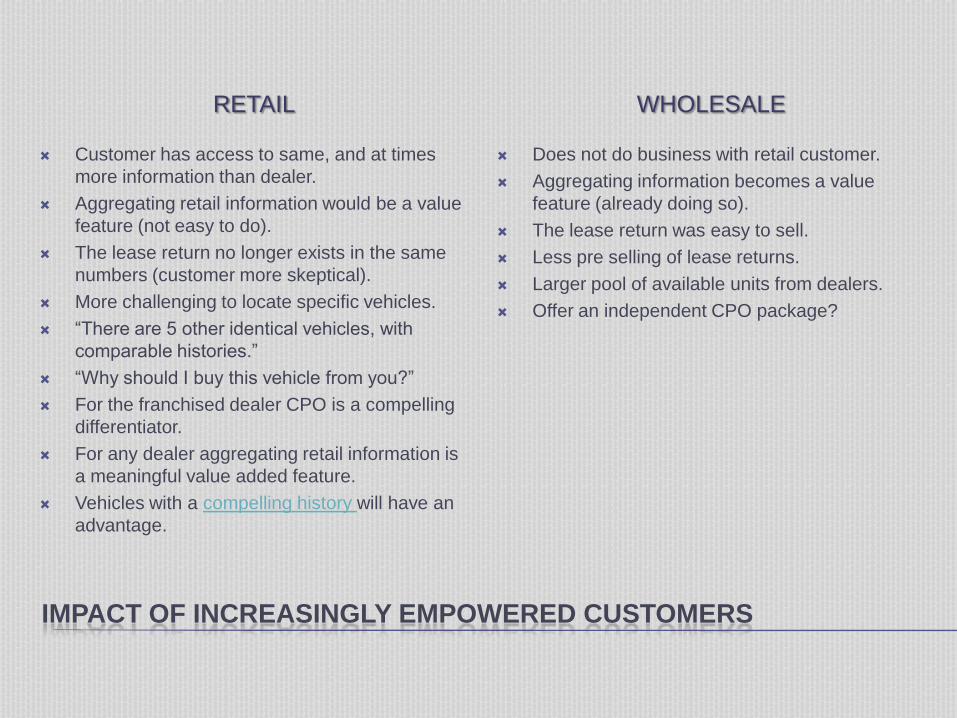

IMPACT OF INCREASINGLY EMPOWERED CUSTOMERS

RETAIL WHOLESALE

Customer has access to same, and at times

more information than dealer.

Aggregating retail information would be a value

feature (not easy to do).

The lease return no longer exists in the same

numbers (customer more skeptical).

More challenging to locate specific vehicles.

“There are 5 other identical vehicles, with

comparable histories.”

“Why should I buy this vehicle from you?”

For the franchised dealer CPO is a compelling

differentiator.

For any dealer aggregating retail information is

a meaningful value added feature.

Vehicles with a compelling history will have an

advantage.

Does not do business with retail customer.

Aggregating information becomes a value

feature (already doing so).

The lease return was easy to sell.

Less pre selling of lease returns.

Larger pool of available units from dealers.

Offer an independent CPO package?

IS VERSION 1.0 RESPONSIVE TO THE FUTURE?

Version 1.0 was effective during a

different Canadian used vehicle

reality, market, and demographics.

Will version 1.0 continue to function

…yes!

Will version 1.0 be responsive, and

pro active?

…NO

What do you think?

LETS TAKE A LOOK

LOOKING AT CANADA

For every new vehicle sold there are 1.5 used

vehicles sold…ratio is 1.0 new to 1.5 used.

Franchised dealers sell 39%, independent

dealers 24% and C2C (consumer to

consumer) 37% of sales.

How many are CPO…good question without a

good answer.

The following data for 2010 is from J.D.Power PIN

In 2010 the used vehicle buyer is younger

(1%). Yes Gen Y is emerging as good

prospect for used vehicles.

With a younger buyer cash sales are down,

while finance (financial services) is up (3.5%).

The female buyer is constant at 38.4% is there

an opportunity here?

Although the average vehicle is still 3.8 years

old, the price is up from 17.7K in 2009 to

18.4K in 2010. Is it the effect of CPO?

The distance is up by 1K kms not a huge

difference to 64.8K kms.

The F&I variables are constant, be it extended

warranty and insurances.

The retail turn rate is 57 days. A n eternity in the

used vehicle market powered by technology.

Points that grasped our attention

The used vehicle buyer will continue to be

younger…a Gen Y.

What is Gen Y seeking in a used vehicle?

Imagine consistent marketing to attract more

Gen Y and women.

When the bench mark is a 30 day turn, and at

45 days its get rid of the vehicle…57 days is an

eternity.

The retail process persists in being slow.

CURRENT POSITION OF CPO

Safe

To

Conclude

CPO

Is

Increasingly

Popular

In

Canada

WHAT WE KNOW…ABOUT CPO IN CANADA

Most manufacturers have a CPO program that

is deployed through their dealers.

CPO works well with luxury/hi line vehicles.

The manufactures that walk the talk are close

to 2 new for 1 CPO.

These same manufacturers gather data to

empower themselves, and their dealers with

timely retail information.

History, and provenance is no longer enough

to distinguish any vehicle. Like saying that a

car has ABS-Air Bags-Stability Control.

CPO sales have increased dramatically in

Canada during the past few years (data from

some manufacturers).

Conclude that the Canadian market is very

receptive to CPO vehicles.

CPO is a compelling trust inducing initiative

deployed by manufacturers, and executed by

franchised dealers.

Luxury manufacturers will continue to calibrate

their CPO offerings to be more responsive to the

market.

At a time when everyone disseminates the same

information from the same sources for vehicles

that are easy to locate by the consumer.

CPO is a powerful differentiator.

Dealers will assume a larger share of the used

value risk compared to market. CPO offers a

value added alternative to diminish risk.

The inspection/reconditioning procedure

provides service, and parts sales to the fixed

operation department.

RECONDITIONING & MAINTENANCE

Is it Detailing?

Is it Front Line

Ready?

Is it Cosmetics?

Is it Inspecting?

WHAT WE KNOW…ABOUT CPO RECONDITIONING

Implies a meticulous inspection and

reconditioning to factory standards, with

factory parts.

Sounds expensive…perhaps its is!

Is the market prepared to pay for such

reconditioning?

What is the expected CPO baseline for

reconditioning?

What are the average reconditioning costs on

a per unit per model basis?

More important what does the customer

expect from a CPO vehicle?

Will the customer understand and pay extra

for a higher level of reconditioning?

When its easy to locate vehicles online, with

the same history reports, is reconditioning a

factor for a consumer beyond the CPO

requirements?

Any CPO vehicle implies a specific level of

reconditioning to meet the CPO standards from

the manufacturer or the purveyor of the

independent program.

In most instances there are stipulations that

discourage reconditioning after the facts.

If Gen Y is emerging as the next wave of used

vehicle buyers.

Understanding Gen Y at large, and in a specific

market will provide insight to arrive at a

competitive advantage.

Gen Y’s are not inclined towards reconditioning

or maintenance, although they desire a good

vehicle.

Blending the required reconditioning with value

added maintenance, to arrive at a unique value

proposition.

WHOLESALE – AUCTION AND DEALER

RETAIL – DEALER

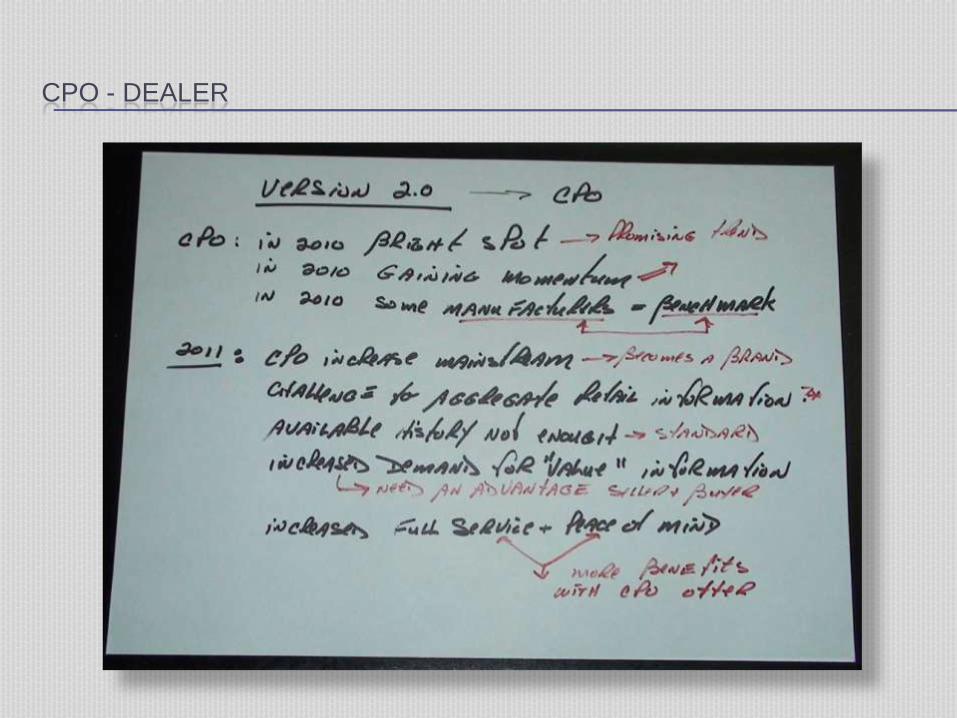

CPO - DEALER

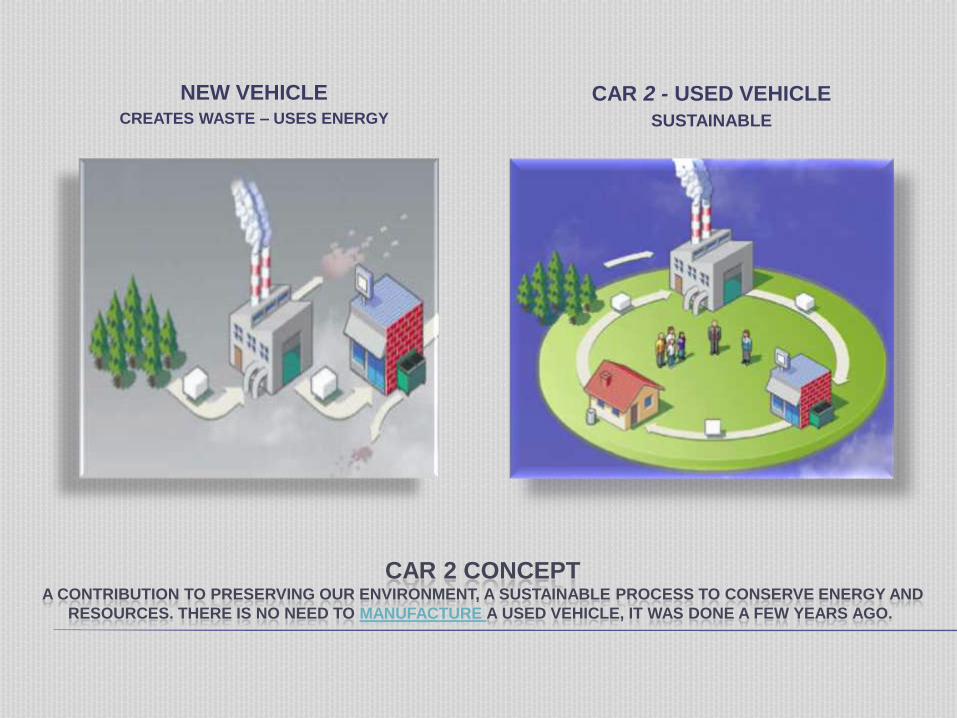

CAR 2 CONCEPTA CONTRIBUTION TO PRESERVING OUR ENVIRONMENT, A SUSTAINABLE PROCESS TO CONSERVE ENERGY AND

RESOURCES. THERE IS NO NEED TO MANUFACTURE A USED VEHICLE, IT WAS DONE A FEW YEARS AGO.

NEW VEHICLECREATES WASTE – USES ENERGY

CAR 2 - USED VEHICLE

SUSTAINABLE

RELEVANT POINTS OF VERSION 2.0

Retail turn rate must increase.

Focus on retail, creating customers,

converting assets to money.

Aggregating retail market information is

an urgent priority, ongoing challenge.

Alleviating the asymmetry between

wholesale (fast) and retail (slow).

Used vehicle valuation risk inexorably

shifting towards the dealer (in the short

term).

Trending towards a younger used

vehicle buyer, demanding more peace of

mind, services, value.

Increasingly empowered, informed,

mobile consumer.

Where is the advantage? The unique

value proposition?

Technology, software, apps, level the

playing field for the various stakeholders.

CPO becoming a mainstream pre owned

market segment.

Will CPO become a model similar to a

new vehicle?

Will reconditioning and maintenance be

packaged to increase value?

CPO vehicles should/will be reviewed

similar to new vehicles, an example..here.

Car 2 Concept = sustainability =

conservation of resources.

Car 2 Concept = Dark Side of Green Pre

Owned.

Recommended