Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus1

Chapter 1

Investments - Background and Issues

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus2

Investments & Financial Assets

• Essential nature of investment– Reduced current consumption– Planned later consumption

• Real Assets– Assets used to produce goods and

services

• Financial Assets– Claims on real assets

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus3

The Investment Process

• Asset allocation

• Security selection

• Risk-return trade-off

• Market efficiency

• Active vs. passive management

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus4

Active vs. Passive Management

Active Management

• Finding undervalued securities

• Timing the market

Passive Management

• No attempt to find undervalued securities

• No attempt to time

• Holding an efficient portfolio

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus5

Major Classes of Financial Assets or Securities

• Debt– Money market instruments– Bonds

• Common stock

• Preferred stock

• Derivative securities

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus6

Investments and Innovation

Technology and Delivery of Service• Computer advancements• More complete and timely informationGlobalization• Domestic firms compete in global

markets• Performance in regions depends on

other regions• Causes additional elements of risk

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus7

Key Trends - Globalization

International and Global Markets Continue Developing• Managing foreign exchange• Diversification to improve

performance• Instruments and vehicles continue

to develop• Information and analysis improves

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus8

Key Trends - Securitization

Securitization & Credit Enhancement• Offers opportunities for investors and

originators• Changes in financial institutions and

regulation• Improvement in information

capabilities• Credit enhancement and its role

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus9

Key Trends - Financial Engineering

Repackaging Services of Financial Intermediaries

• Bundling and unbundling of cash flows

• Slicing and dicing of cash flows

• Examples: strips, CMOs, dual purpose funds, principal/interest splits

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus10

The Future

• Globalization continues and offers more opportunities

• Securitization continues to develop

• Continued development of derivatives and exotics

• Strong fundamental foundation is critical• Integration of investments & corporate

finance

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus11

Chapter 2

Financial Markets and Instruments

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus12

Major Classes of Financial Assets or Securities

• Debt– Money market instruments– Bonds

• Common stock

• Preferred stock

• Derivative securities

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus13

Markets and Instruments

• Money Market– Debt Instruments– Derivatives

• Capital Market– Bonds– Equity– Derivatives

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus14

Money Market Instruments

• Treasury bills

• Certificates of deposit

• Commercial Paper

• Bankers Acceptances

• Eurodollars

• Repurchase Agreements (RPs) and Reverse RPs

• Federal Funds

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus15

Money Market Instrument Yields

• Yields on Money Market Instruments are not always directly comparable

Factors influencing yields

• Par value vs. investment value

• 360 vs. 365 days assumed in a year (366 leap year)

• Bond equivalent yield

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus16

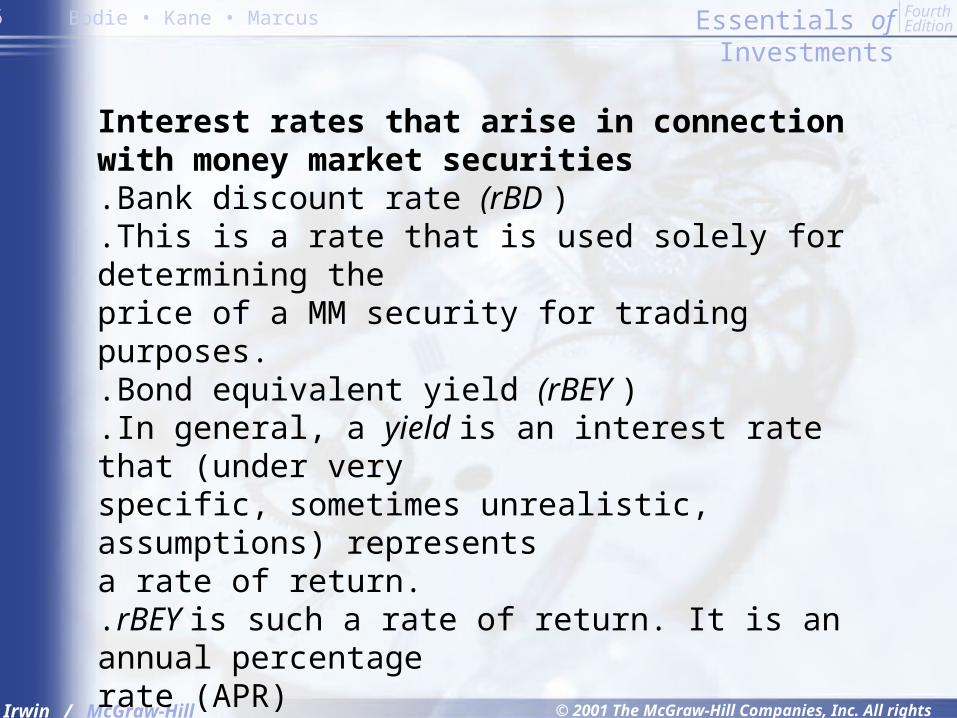

Interest rates that arise in connection with money market securities.Bank discount rate (rBD ).This is a rate that is used solely for determining theprice of a MM security for trading purposes..Bond equivalent yield (rBEY ).In general, a yield is an interest rate that (under veryspecific, sometimes unrealistic, assumptions) representsa rate of return..rBEY is such a rate of return. It is an annual percentagerate (APR).For comparing different MM instruments, we often use theeffective annual rate (EAR) of the rBEY .

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus17

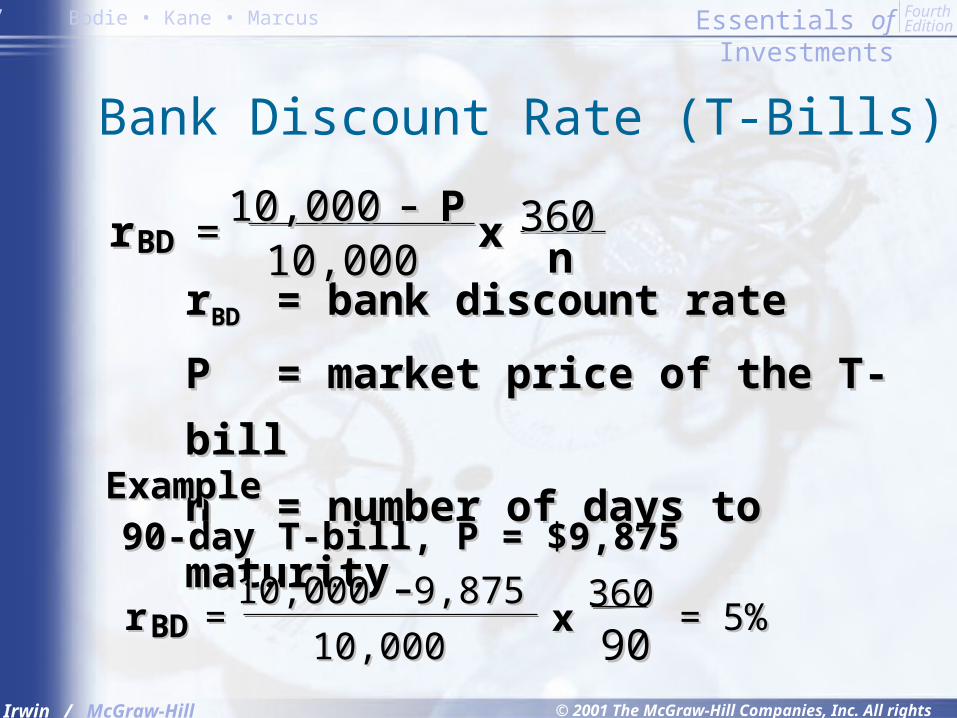

Bank Discount Rate (T-Bills)

rrBDBD = bank discount rate= bank discount rate

PP = market price of the T-bill= market price of the T-bill

nn = number of days to maturity= number of days to maturity

rrBDBD == 10,00010,000 -- PP10,00010,000

xx 360360nn

90-day T-bill, P = $9,87590-day T-bill, P = $9,875

rrBDBD == 10,00010,000 -- 9,8759,875

10,00010,000 x x

360360

9090== 5%5%

ExampleExample

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus18

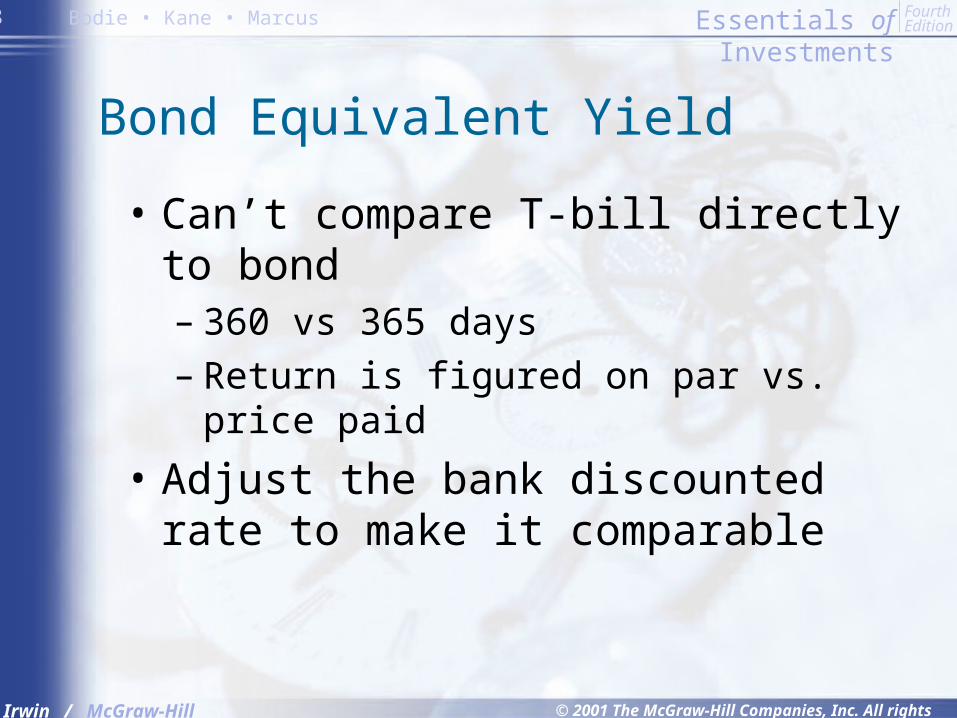

Bond Equivalent Yield

• Can’t compare T-bill directly to bond– 360 vs 365 days – Return is figured on par vs. price paid

• Adjust the bank discounted rate to make it comparable

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus19

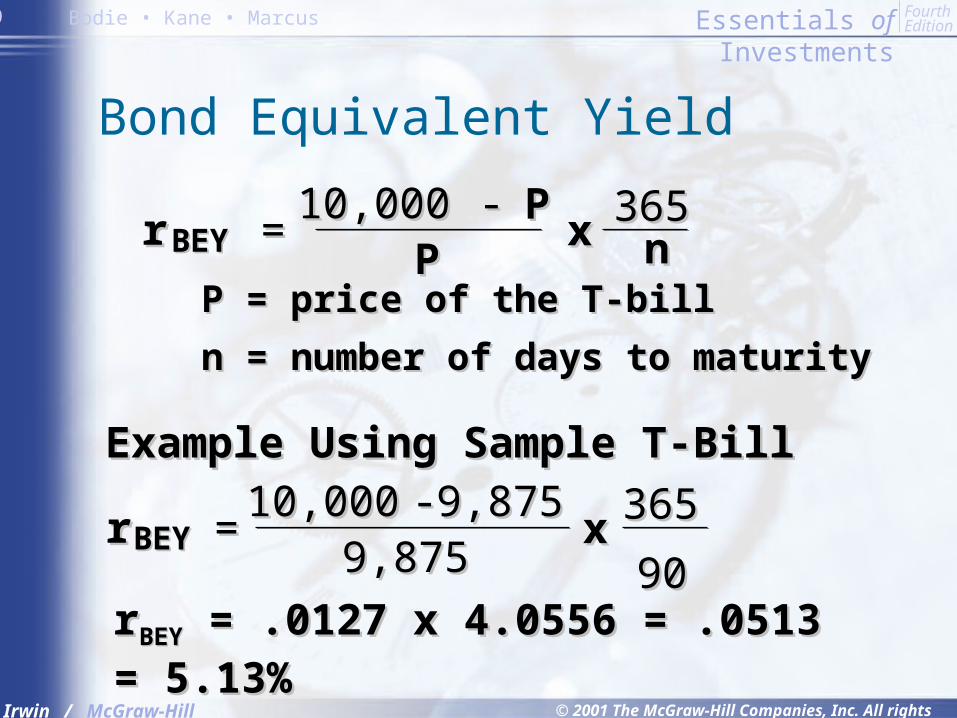

Bond Equivalent Yield

P = price of the T-billP = price of the T-bill

n = number of days to maturityn = number of days to maturity

rr BEYBEY == 10,00010,000 -- PP

PP xx 365365

nn

rrBEYBEY == 10,00010,000 -- 9,8759,875

9,8759,875 x x 365365

9090rrBEYBEY = .0127 x 4.0556 = .0513 = 5.13% = .0127 x 4.0556 = .0513 = 5.13%

Example Using Sample T-BillExample Using Sample T-Bill

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus20

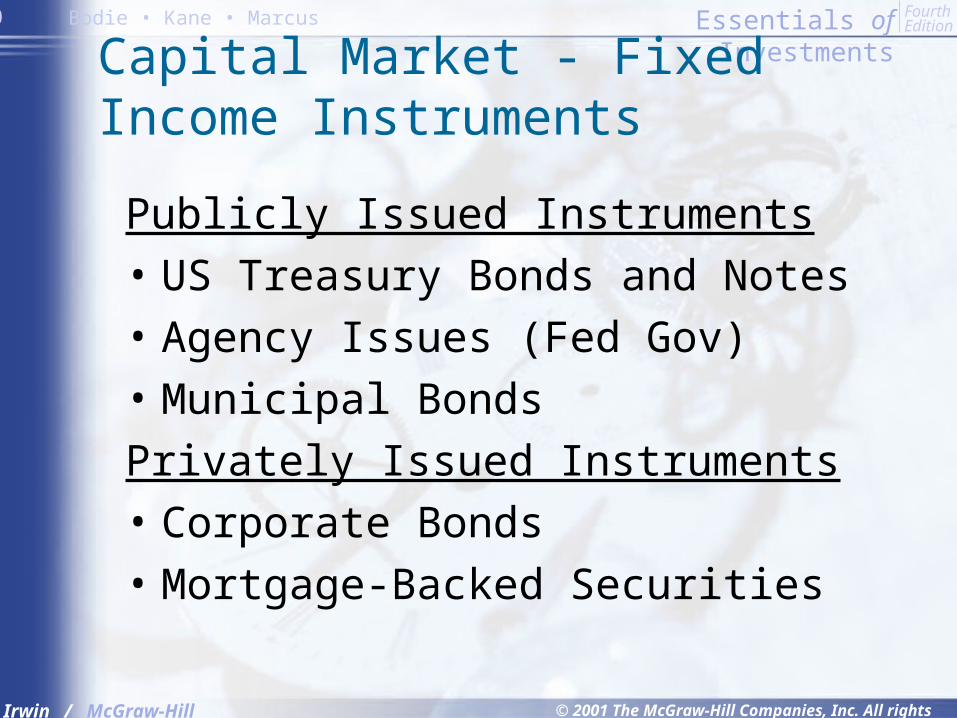

Capital Market - Fixed Income Instruments

Publicly Issued Instruments

• US Treasury Bonds and Notes

• Agency Issues (Fed Gov)

• Municipal Bonds

Privately Issued Instruments

• Corporate Bonds

• Mortgage-Backed Securities

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus21

Capital Market - Equity

• Common stock– Residual claim– Limited liability

• Preferred stock– Fixed dividends - limited– Priority over common– Tax treatment

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus22

Uses

• Track average returns

• Comparing performance of managers

• Base of derivatives

Factors in constructing or using an Index

• Representative?

• Broad or narrow?

• How is it constructed?

Stock Indexes

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus23

Examples of Indexes - Domestic

• Dow Jones Industrial Average (30 Stocks)

• Standard & Poor’s 500 Composite

• NASDAQ Composite

• NYSE Composite

• Wilshire 5000

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus24

Examples of Indexes - Int’l

• Nikkei 225 & Nikkei 300

• FTSE (Financial Times of London)

• Dax

• Region and Country Indexes– EAFE– Far East– United Kingdom

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus25

Construction of Indexes

• How are stocks weighted?– Price weighted (DJIA)– Market-value weighted (S&P500,

NASDAQ)– Equally weighted (Value Line Index)

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus26

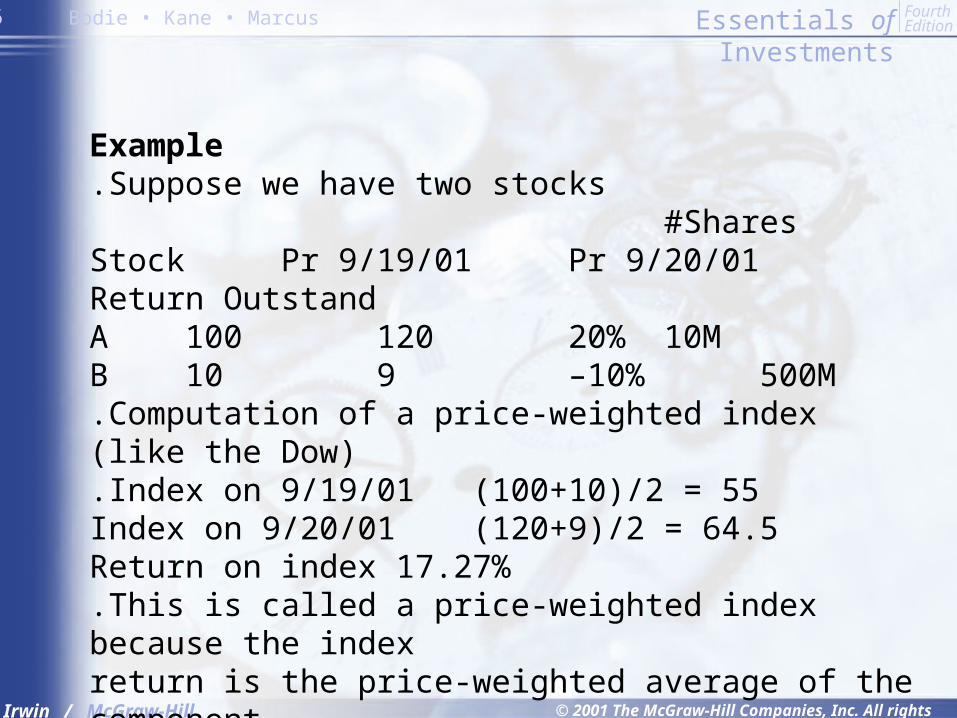

Example.Suppose we have two stocks

#SharesStock Pr 9/19/01 Pr 9/20/01 Return OutstandA 100 120 20% 10MB 10 9 –10% 500M.Computation of a price-weighted index (like the Dow).Index on 9/19/01 (100+10)/2 = 55Index on 9/20/01 (120+9)/2 = 64.5Return on index 17.27%.This is called a price-weighted index because the indexreturn is the price-weighted average of the component(100/110) x 20% + (10/110) x –10% = 17.27%.Portfolio: one share in each stock.

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus27

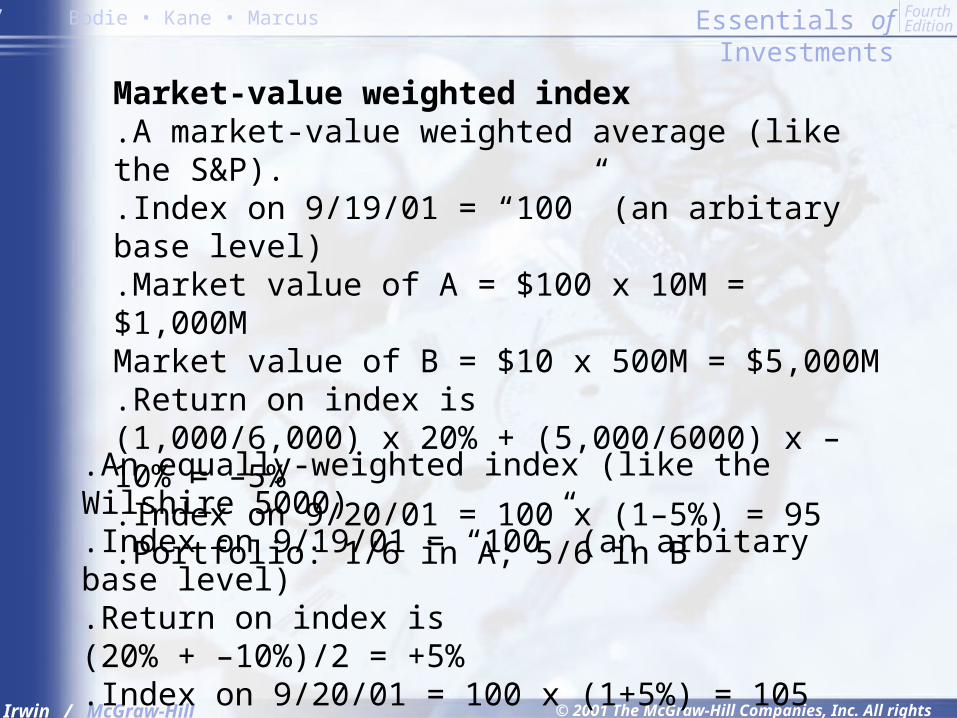

Market-value weighted index.A market-value weighted average (like the S&P)..Index on 9/19/01 = “100” (an arbitary base level).Market value of A = $100 x 10M = $1,000MMarket value of B = $10 x 500M = $5,000M.Return on index is(1,000/6,000) x 20% + (5,000/6000) x –10% = –5%.Index on 9/20/01 = 100 x (1–5%) = 95.Portfolio: 1/6 in A; 5/6 in B

.An equally-weighted index (like the Wilshire 5000)

.Index on 9/19/01 = “100” (an arbitary base level)

.Return on index is(20% + –10%)/2 = +5%.Index on 9/20/01 = 100 x (1+5%) = 105.Portfolio: equal amounts in A and B

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus28

Chapter 3

How Securities are Traded

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus29

Primary vs. Secondary Security Sales

• Primary– New issue– Key factor: issuer receives the proceeds

from the sale• Secondary

– Existing owner sells to another party– Issuing firm doesn’t receive proceeds

and is not directly involved

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus30

Investment Banking Arrangements

• Underwritten vs. “Best Efforts”– Underwritten: firm commitment on

proceeds to the issuing firm– Best Efforts: no firm commitment

• Negotiated vs. Competitive Bid– Negotiated: issuing firm negotiates terms

with investment banker– Competitive bid: issuer structures the

offering and secures bids

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus31

• Public offerings: registered with the SEC and sale is made to the investing public– Shelf registration (Rule 415, since 1982)

• Initial Public Offerings (IPOs)– Evidence of underpricing– Performance

Public Offerings

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus32

Private placement: sale to a limitednumber of sophisticated investors notrequiring the protection of registration• Dominated by institutions

• Very active market for debt securities

• Not active for stock offerings

Private Placements

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus33

Organization of Secondary Markets

• Organized exchanges

• OTC market

• Third market

• Fourth market

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus34

Organized Exchanges

• Auction markets with centralized order flow

• Dealership function: can be competitive or assigned by the exchange (Specialists)

• Securities: stock, futures contracts, options, and to a lesser extent, bonds

• Examples: NYSE, AMEX, Regionals, CBOE

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus35

Types of Orders

Instructions to the brokers on how tocomplete the order

• Market

• Limit

• Stop loss

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus36

Margin Trading

• Using only a portion of the proceeds for an investment

• Borrow remaining component

• Margin arrangements differ for stocks and futures

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus37

Stock Margin Trading

• Maximum margin is currently 50%; you can borrow up to 50% of the stock value

• Set by the Fed• Maintenance margin: minimum amount

equity in trading can be before additional funds must be put into the account

• Margin call: notification from broker you must put up additional funds

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus38

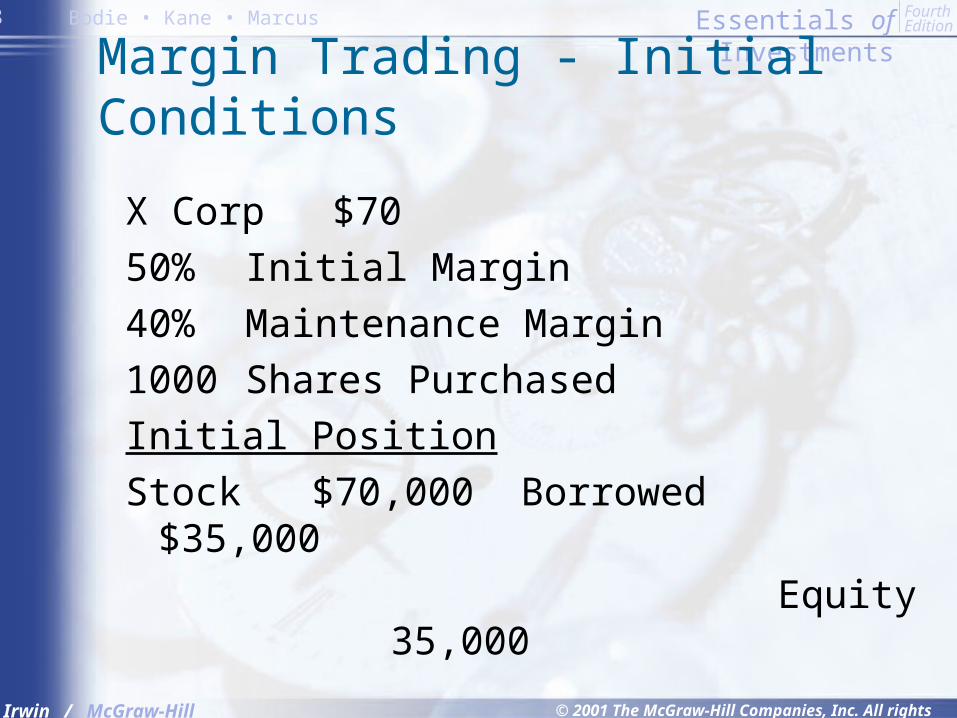

Margin Trading - Initial Conditions

X Corp $70

50% Initial Margin

40% Maintenance Margin

1000 Shares Purchased

Initial Position

Stock $70,000 Borrowed $35,000

Equity 35,000

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus39

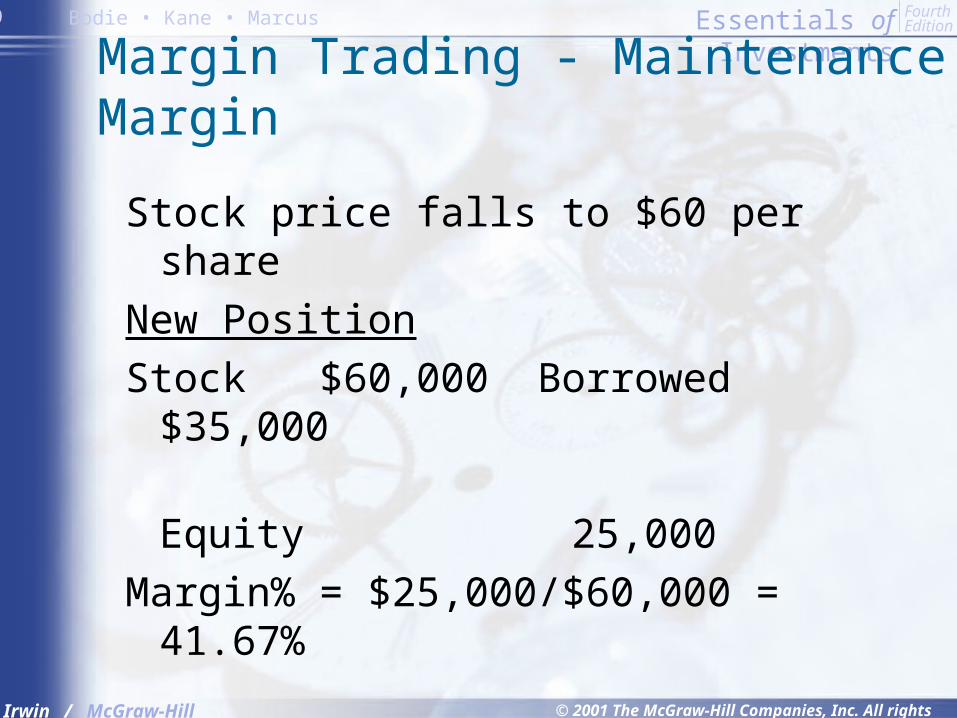

Margin Trading - Maintenance Margin

Stock price falls to $60 per share

New Position

Stock $60,000 Borrowed $35,000

Equity 25,000

Margin% = $25,000/$60,000 = 41.67%

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus40

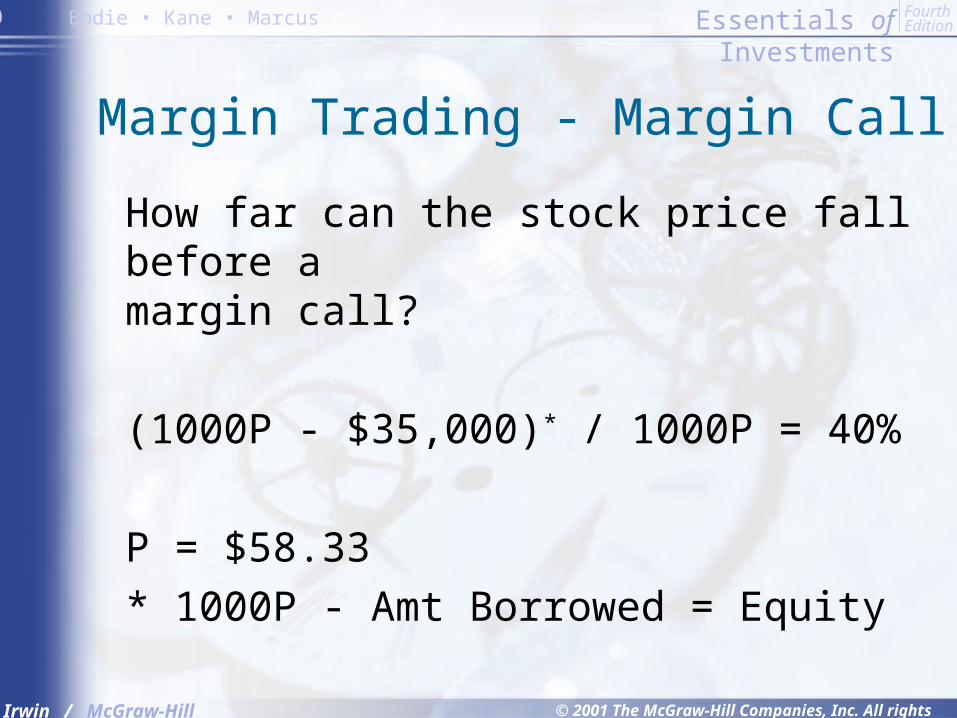

Margin Trading - Margin Call

How far can the stock price fall before amargin call?

(1000P - $35,000)* / 1000P = 40%

P = $58.33

* 1000P - Amt Borrowed = Equity

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus41

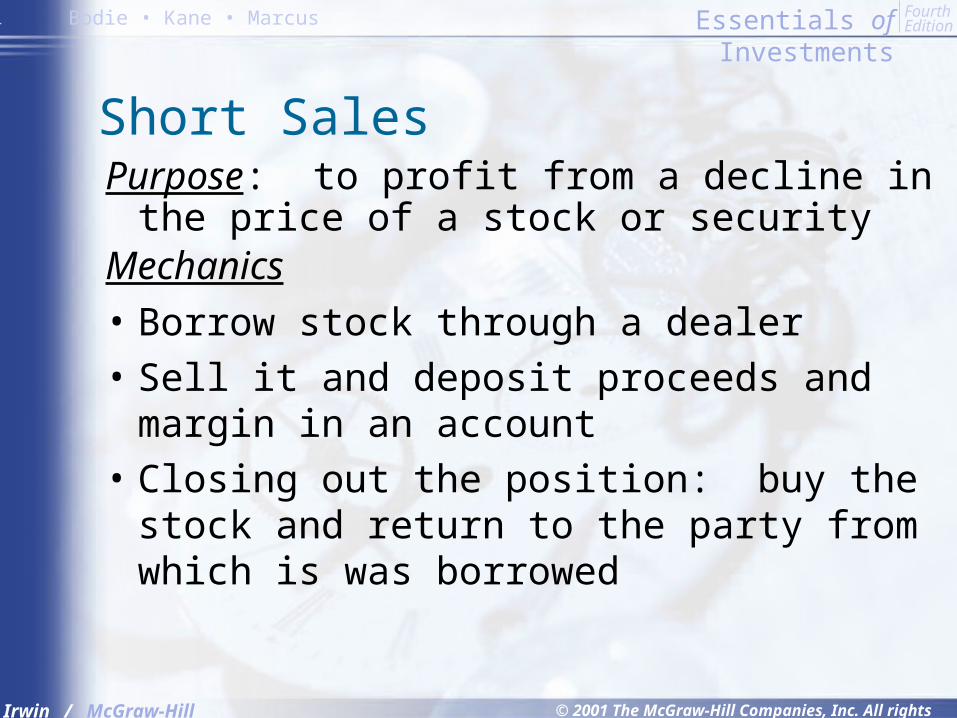

Short SalesPurpose: to profit from a decline in the

price of a stock or securityMechanics

• Borrow stock through a dealer

• Sell it and deposit proceeds and margin in an account

• Closing out the position: buy the stock and return to the party from which is was borrowed

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus42

Short Sale - Initial Conditions

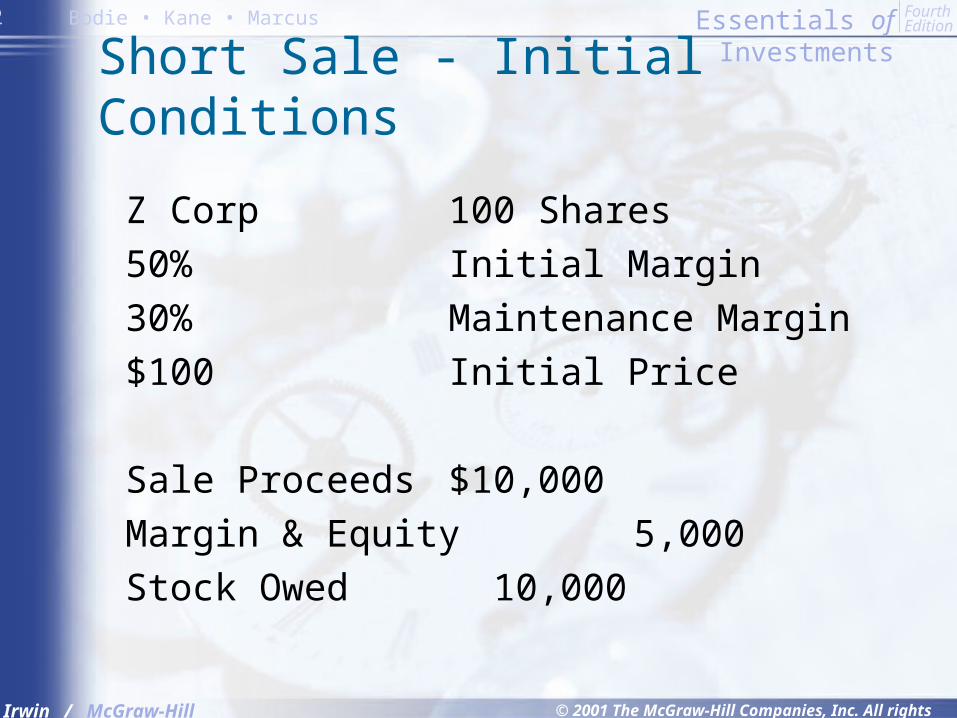

Z Corp 100 Shares

50% Initial Margin

30% Maintenance Margin

$100 Initial Price

Sale Proceeds $10,000

Margin & Equity 5,000

Stock Owed 10,000

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus43

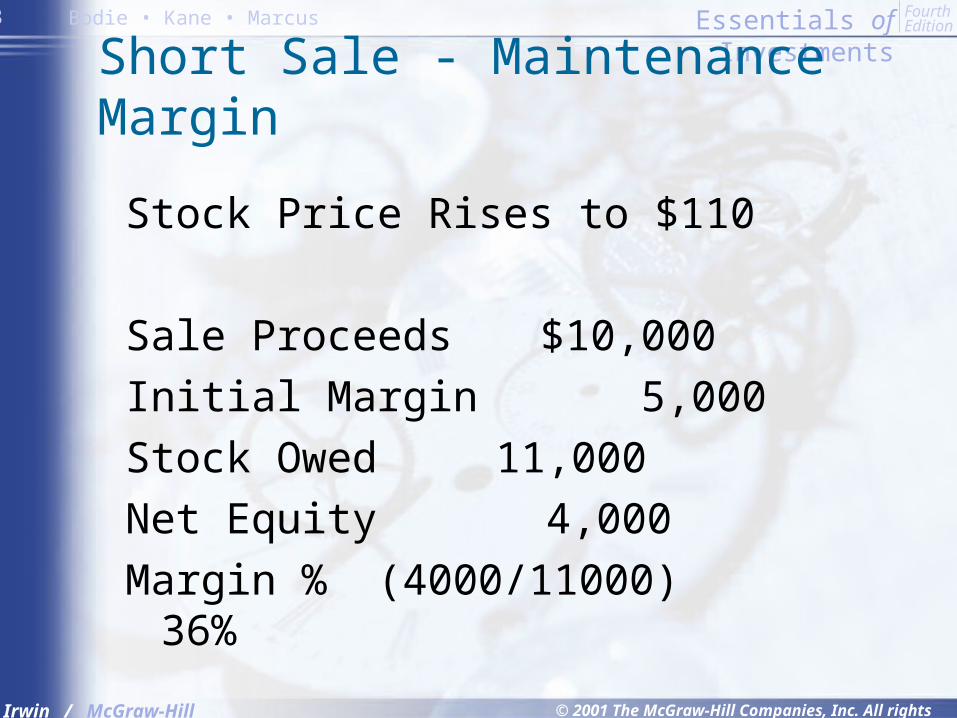

Short Sale - Maintenance Margin

Stock Price Rises to $110

Sale Proceeds $10,000

Initial Margin 5,000

Stock Owed 11,000

Net Equity 4,000

Margin % (4000/11000) 36%

Essentials of Investments

© 2001 The McGraw-Hill Companies, Inc. All rights reserved.

Fourth Edition

Irwin / McGraw-Hill

Bodie • Kane • Marcus44

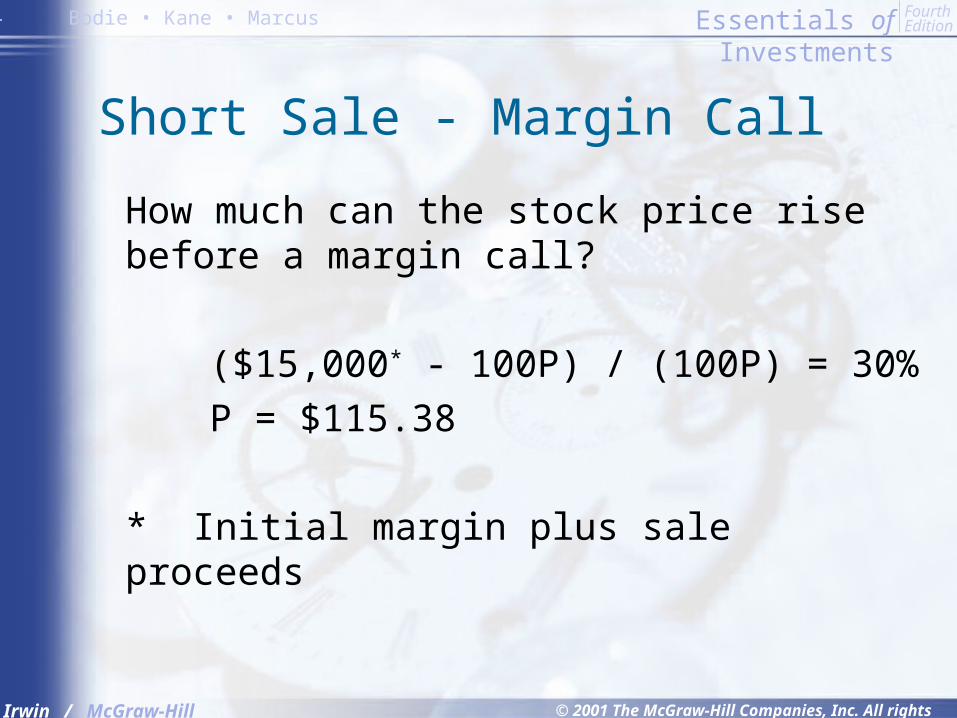

Short Sale - Margin Call

How much can the stock price rise before a margin call?

($15,000* - 100P) / (100P) = 30%

P = $115.38

* Initial margin plus sale proceeds

Recommended

![Chapter 1: Qlik Sense Self-Service Model€¦ · Qlik Sense. Graphics Chapter 1 [ 4 ] Graphics Chapter 1 [ 5 ] Graphics Chapter 1 [ 6 ] Graphics Chapter 1 [ 7 ] Chapter 3: Security](https://img.pdfslide.net/doc/110x75/603a754026637d7e176f5238/chapter-1-qlik-sense-self-service-model-qlik-sense-graphics-chapter-1-4-graphics.jpg)