Chapter 17: Vertical and Conglomerate Mergers

1

Vertical and Conglomerate Mergers

Chapter 17: Vertical and Conglomerate Mergers

2

Introduction

• General Electric and Honeywell proposed to merge in 2000– GE supplies jet engines for commercial aircraft

– Honeywell produced various electrical and other control systems for jet aircraft

• Deal was approved in the US

• But was blocked by the EU Competition Directorate– this was a merger of complementary firms

– it is “like” a vertical merger

– so can potentially remove inefficiencies in pricing• benefiting the merged firms and consumers

– so why block the merger?

Chapter 17: Vertical and Conglomerate Mergers

3

Introduction 2

• Vertical mergers can be detrimental– if they facilitate market foreclosure by the merged firms

• refuse to supply non-merged rivals

• But they can also be beneficial– if they remove market inefficiencies

• Regulators need to look for the balance these two forces in considering any proposed merger

Chapter 17: Vertical and Conglomerate Mergers

4

Complementary Mergers

• Consider first a merger between firms that supply complementary products

• A simple example:– final production requires two inputs in fixed proportions

– one unit of each input is needed to make one unit of output

– input producers are monopolists

– final product producer is a monopolist

– demand for the final product is P = 140 - Q

– marginal costs of upstream producers and final producer (other than for the two inputs) normalized to zero.

• What is the effect of merger between the two upstream producers?

Chapter 17: Vertical and Conglomerate Mergers

5

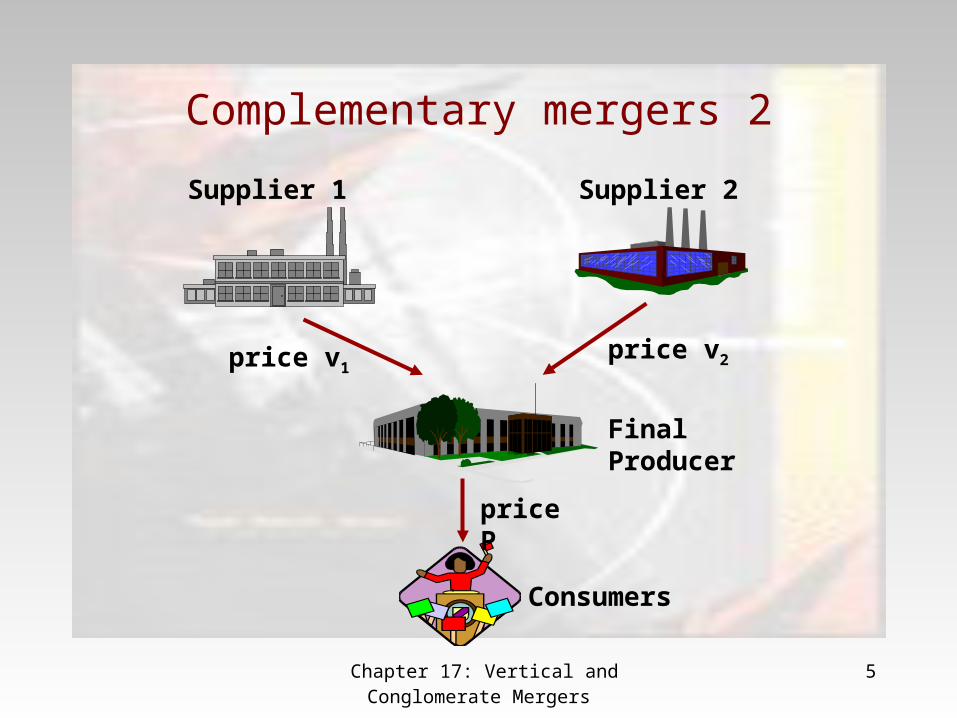

Complementary mergers 2

Supplier 1 Supplier 2

price v1price v2

price P

Final Producer

Consumers

Chapter 17: Vertical and Conglomerate Mergers

6

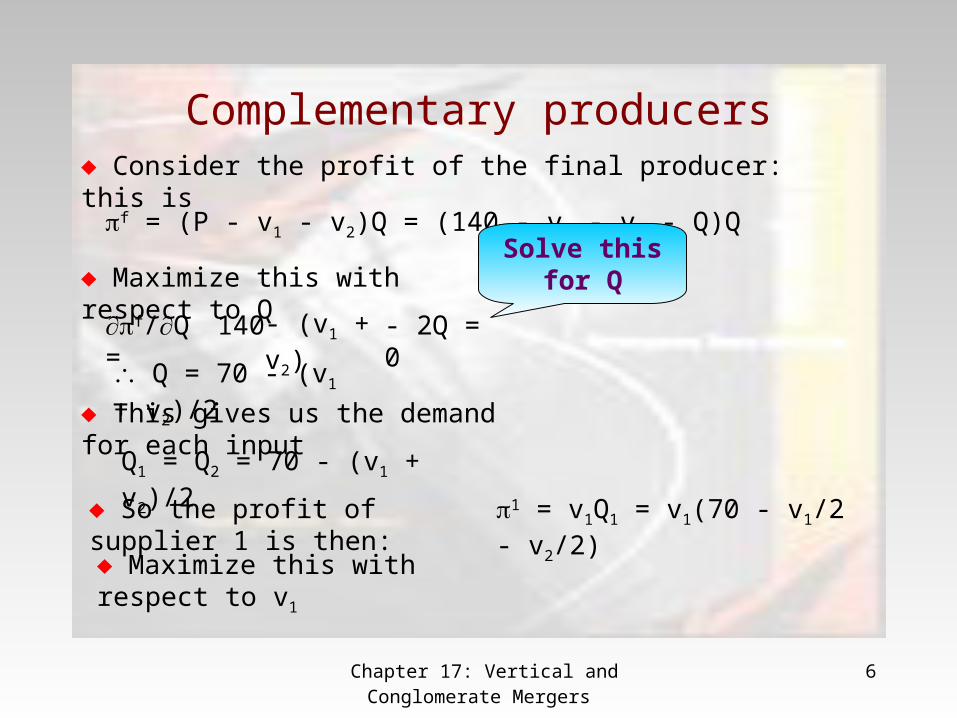

Complementary producers Consider the profit of the final producer: this is

f = (P - v1 - v2)Q = (140 - v1 - v2 - Q)Q

Maximize this with respect to Q

f/Q = 140 - (v1 + v2) - 2Q = 0

Solve this for Q

Q = 70 - (v1 + v2)/2

This gives us the demand for each input

Q1 = Q2 = 70 - (v1 + v2)/2

So the profit of supplier 1 is then: 1 = v1Q1 = v1(70 - v1/2 - v2/2)

Maximize this with respect to v1

Chapter 17: Vertical and Conglomerate Mergers

7

Complementary producers 2

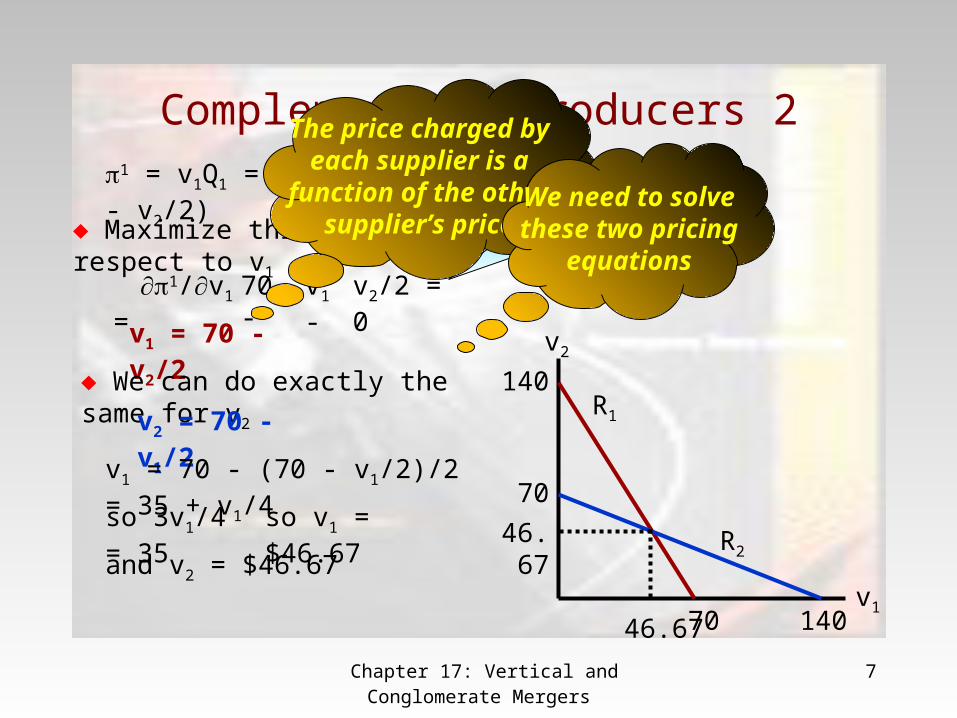

Maximize this with respect to v1

1 = v1Q1 = v1(70 - v1/2 - v2/2)

1/v1 =

70 - v1 - v2/2 = 0

Solve this for v1

v1 = 70 - v2/2

We can do exactly the same for v2

v2 = 70 - v1/2

The price charged byeach supplier is a

function of the othersupplier’s price

We need to solvethese two pricing

equations

v2

v1

140

70

R1

70

140

R2

v1 = 70 - (70 - v1/2)/2 = 35 + v1/4

so 3v1/4 = 35 so v1 = $46.67

46.67

and v2 = $46.6746.67

Chapter 17: Vertical and Conglomerate Mergers

8

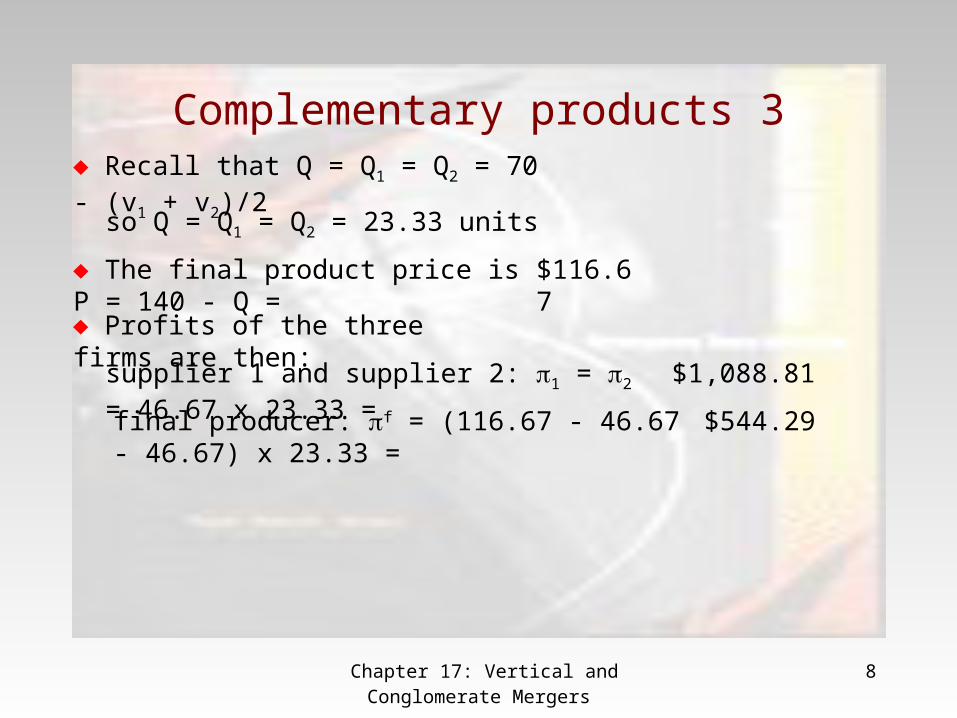

Complementary products 3 Recall that Q = Q1 = Q2 = 70 - (v1 + v2)/2

so Q = Q1 = Q2 = 23.33 units

The final product price is P = 140 - Q = $116.67

Profits of the three firms are then:

supplier 1 and supplier 2: 1 = 2 = 46.67 x 23.33 = $1,088.81

final producer: f = (116.67 - 46.67 - 46.67) x 23.33 = $544.29

Chapter 17: Vertical and Conglomerate Mergers

9

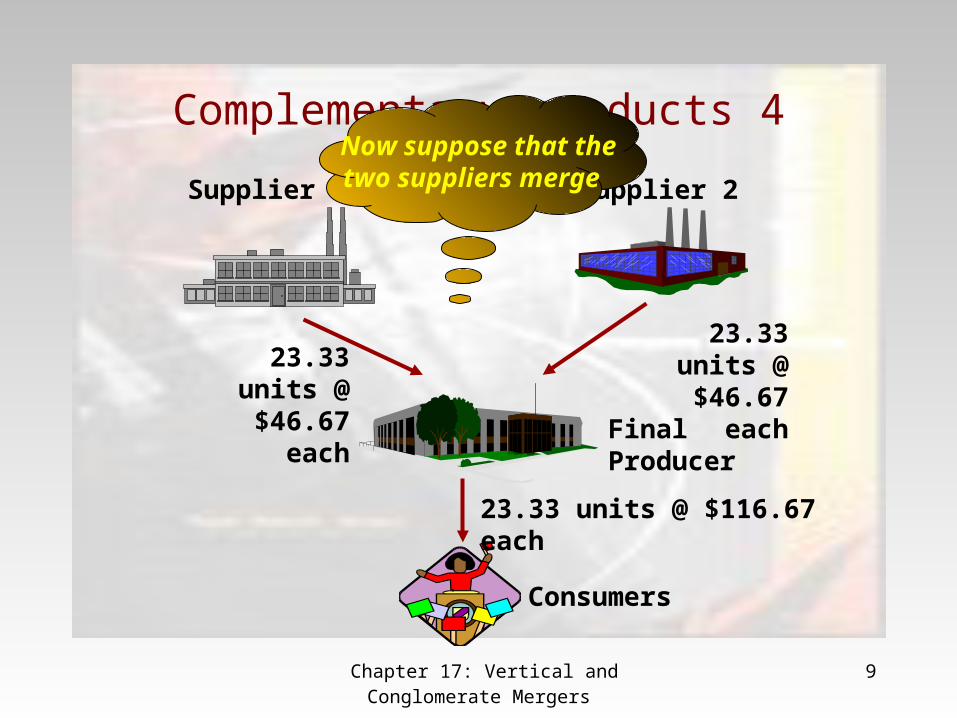

Complementary products 4

Supplier 1 Supplier 2

23.33 units @ $46.67 each

23.33 units @ $116.67 each

Final Producer

Consumers

23.33 units @ $46.67 each

Now suppose that thetwo suppliers merge

Chapter 17: Vertical and Conglomerate Mergers

10

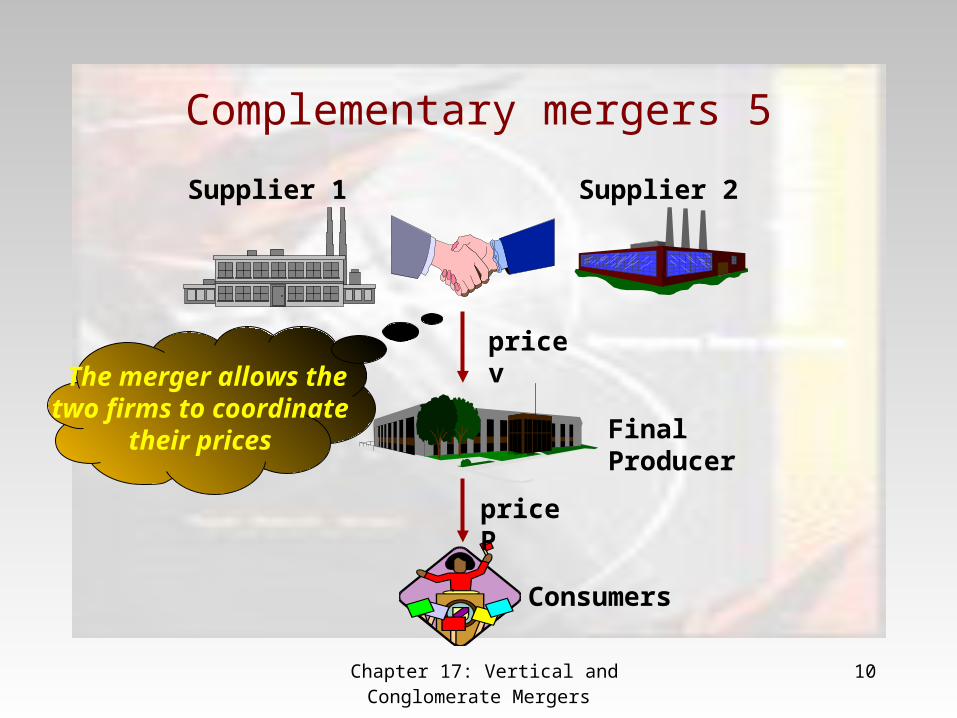

Complementary mergers 5

Supplier 1 Supplier 2

price v

price P

Final Producer

Consumers

The merger allows thetwo firms to coordinate

their prices

Chapter 17: Vertical and Conglomerate Mergers

11

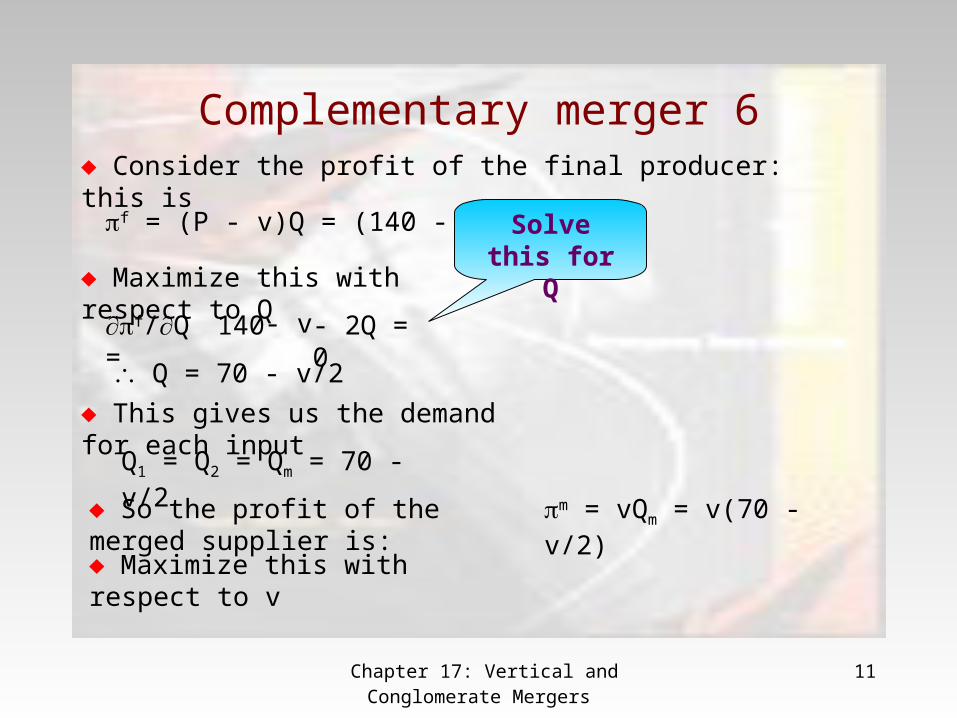

Complementary merger 6 Consider the profit of the final producer: this is

f = (P - v)Q = (140 - v - Q)Q

Maximize this with respect to Q

f/Q = 140 - v - 2Q = 0

Solve this for Q

Q = 70 - v/2

This gives us the demand for each input

Q1 = Q2 = Qm = 70 - v/2

So the profit of the merged supplier is: m = vQm = v(70 - v/2)

Maximize this with respect to v

Chapter 17: Vertical and Conglomerate Mergers

12

Complementary merger 7

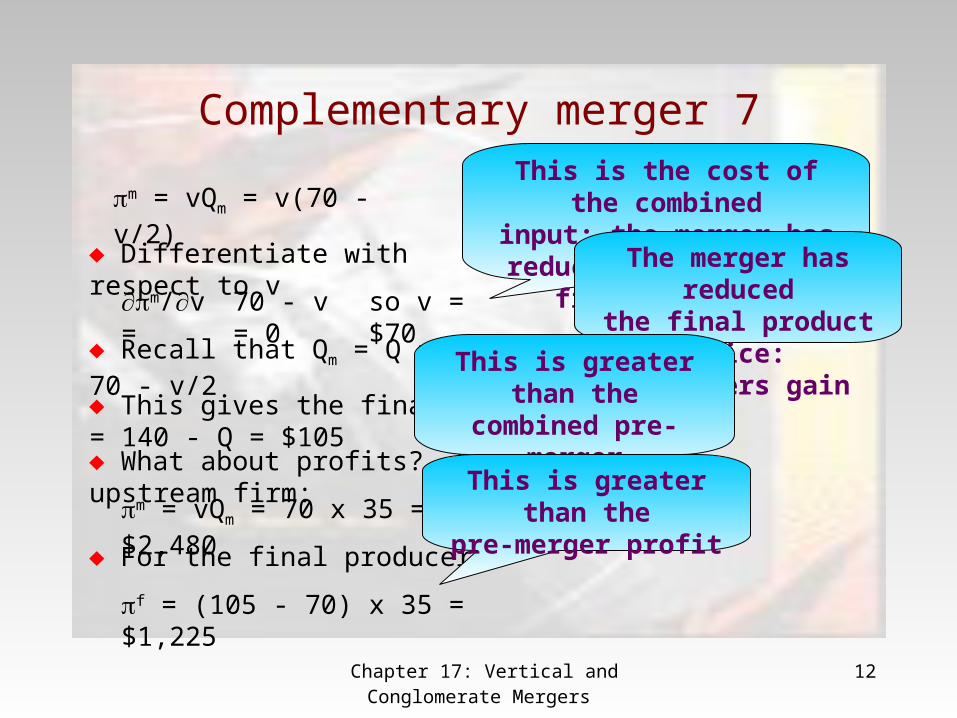

m = vQm = v(70 - v/2)

Differentiate with respect to v

m/v = 70 - v = 0 so v = $70

This is the cost of the combinedinput: the merger has reduced

costs to the final producer

Recall that Qm = Q = 70 - v/2 so Qm = Q = 35 units

This gives the final product price P = 140 - Q = $105

The merger has reducedthe final product price:

consumers gain

What about profits? For the merged upstream firm:

m = vQm = 70 x 35 = $2,480

This is greater than thecombined pre-merger

profit

For the final producer:

f = (105 - 70) x 35 = $1,225

This is greater than thepre-merger profit

Chapter 17: Vertical and Conglomerate Mergers

13

Complementary mergers 8• A merger of complementary producers has

– increased profits of the merged firms

– increased profit of the final producer

– reduced the price charged to consumers

Everybody gains from this merger: a Pareto improvement! Why?

• This merger corrects a market failure– prior to the merger the upstream suppliers do not take full account of

their interdependence– reduction in price by one of them reduces downstream costs,

increases downstream output and benefits the other upstream firm– but this is an externality and so is ignored

• Merger internalizes the externality

Chapter 17: Vertical and Conglomerate Mergers

14

Vertical Mergers• The same result arises when we consider vertical mergers:

mergers of upstream and downstream firms• If the merging firms have market power

– lack of co-ordination in their independent decisions– double marginalization– merger can lead to a general improvement

• Illustrate with a simple model– one upstream and one downstream monopolist

• manufacturer and retailer

– upstream firm has marginal costs c– sells product to the retailer at price r per unit– retailer has no other costs: one unit of input gives one unit of output– retail demand is P = A – BQ

Chapter 17: Vertical and Conglomerate Mergers

15

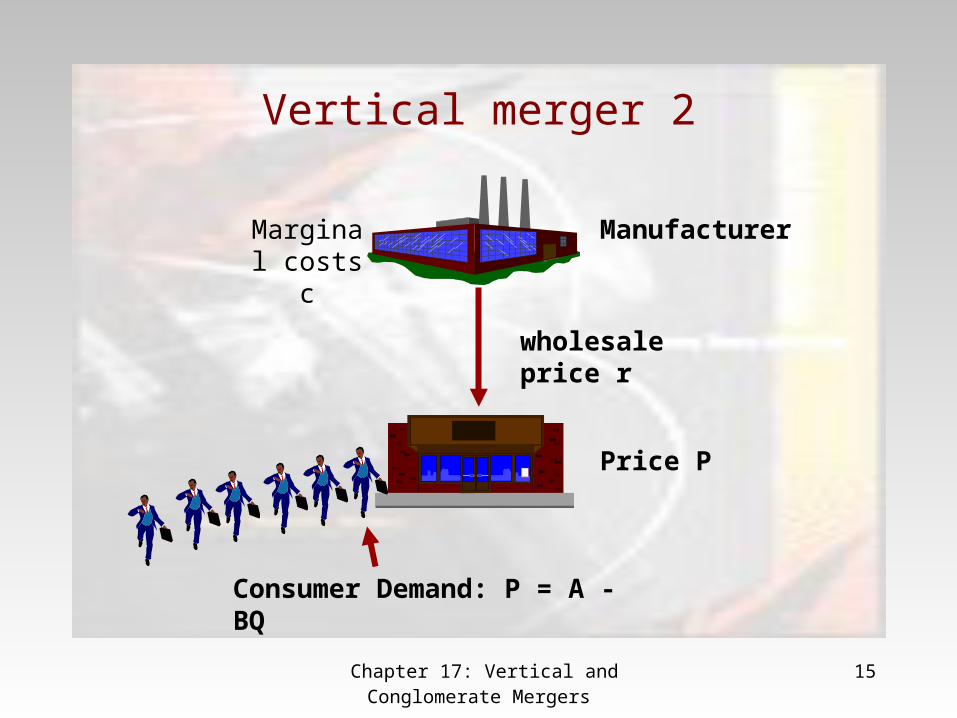

Vertical merger 2

ManufacturerMarginal costs c

wholesale price r

Price P

Consumer Demand: P = A - BQ

Chapter 17: Vertical and Conglomerate Mergers

16

Vertical merger 3

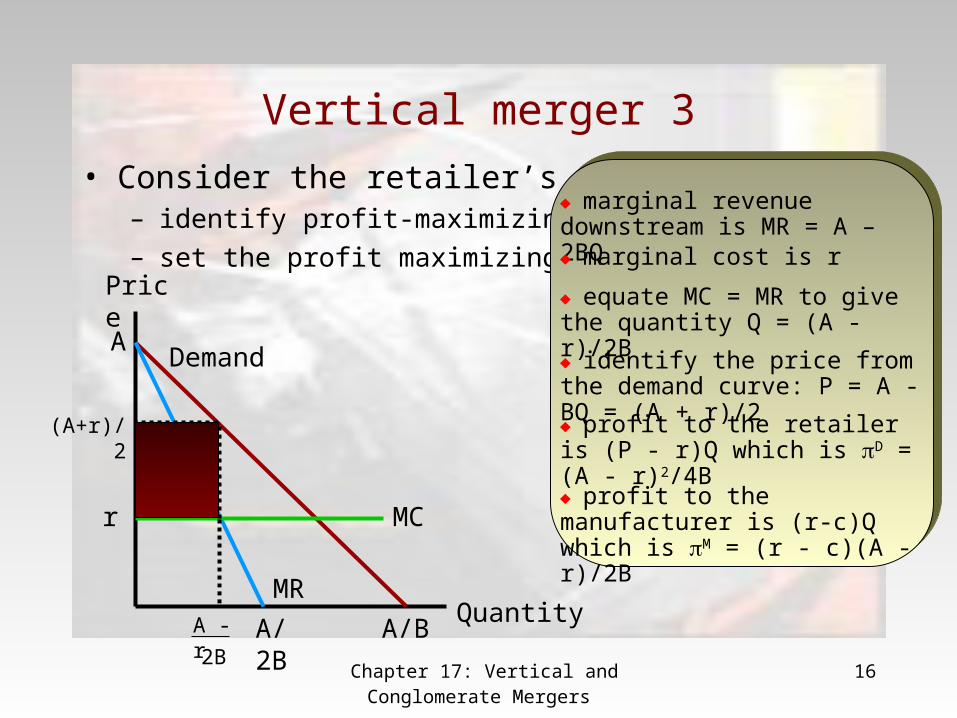

• Consider the retailer’s decision– identify profit-maximizing output

– set the profit maximizing pricePrice

Quantity

DemandA

A/B

marginal revenue downstream is MR = A – 2BQ

MR

A/2B

marginal cost is r

MCr

equate MC = MR to give the quantity Q = (A - r)/2B

A - r

2B

identify the price from the demand curve: P = A - BQ = (A + r)/2

(A+r)/2 profit to the retailer is (P - r)Q which is D = (A - r)2/4B

profit to the manufacturer is (r-c)Q which is M = (r - c)(A - r)/2B

Chapter 17: Vertical and Conglomerate Mergers

17

Vertical merger 4

Price

Quantity

DemandA

A/B

MR

A/2B

MCr

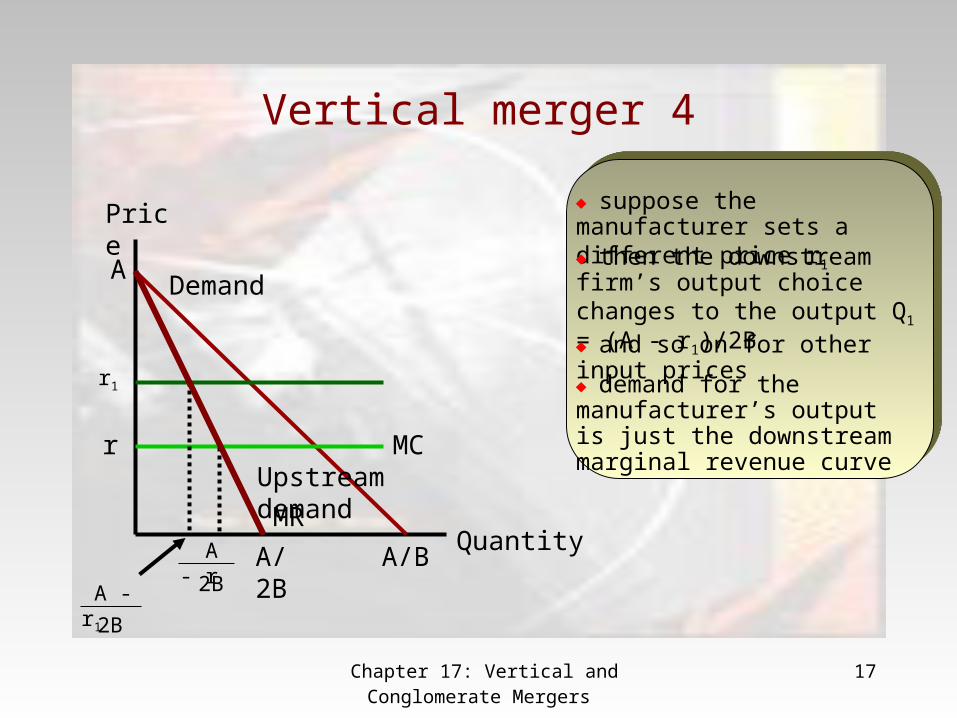

suppose the manufacturer sets a different price r1

r1

A - r

2B

then the downstream firm’s output choice changes to the output Q1 = (A - r1)/2B

A - r1

2B

and so on for other input prices

demand for the manufacturer’s output is just the downstream marginal revenue curve

Upstream demand

Chapter 17: Vertical and Conglomerate Mergers

18

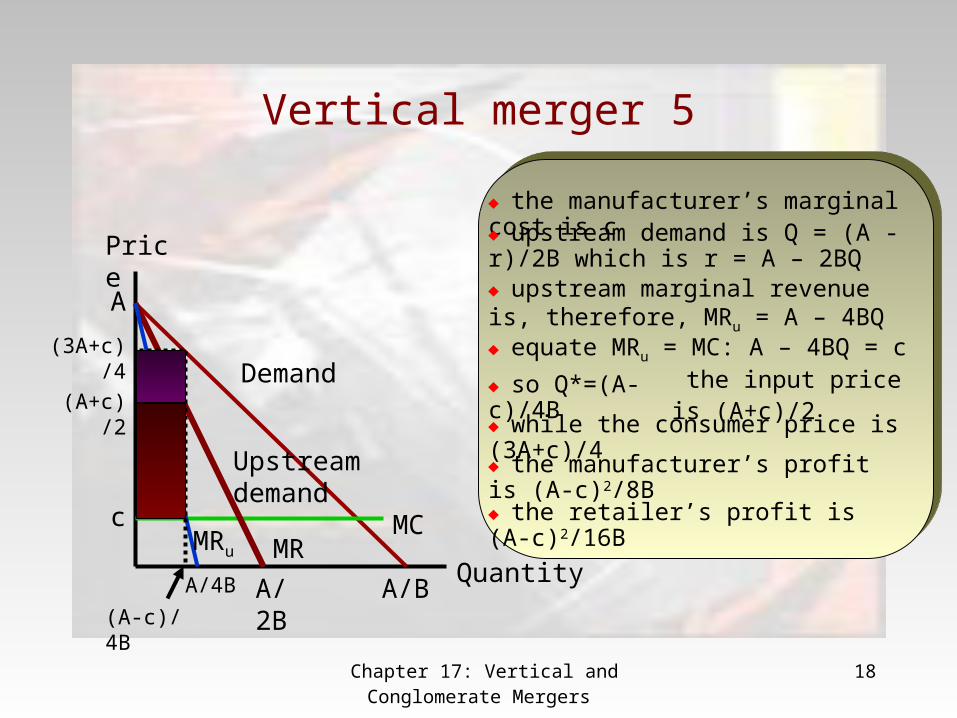

Vertical merger 5

Price

Quantity

Demand

A

A/B

MR

A/2B

the manufacturer’s marginal cost is c

Upstream demand

c MC

upstream demand is Q = (A - r)/2B which is r = A – 2BQupstream marginal revenue is, therefore, MRu = A – 4BQ

A/4B

equate MRu = MC: A – 4BQ = c

so Q*=(A-c)/4B

(A-c)/4B

the input price is (A+c)/2 (A+c)/2

while the consumer price is (3A+c)/4

(3A+c)/4

the manufacturer’s profit is (A-c)2/8B

the retailer’s profit is (A-c)2/16BMRu

Chapter 17: Vertical and Conglomerate Mergers

19

Vertical merger 6• Now suppose that the retailer and manufacturer merge

– manufacturer takes over the retail outlet– retailer is now a downstream division of an integrated firm– the integrated firm aims to maximize total profit– Suppose the upstream division sets an internal (transfer) price of r

for its product– Suppose that consumer demand is P = P(Q)– Total profit is:

• upstream division: (r - c)Q• downstream division: (P(Q) - r)Q• aggregate profit: (P(Q) - c)Q

The internal transferprice nets out of theprofit calculations

• Back to the example

Chapter 17: Vertical and Conglomerate Mergers

20

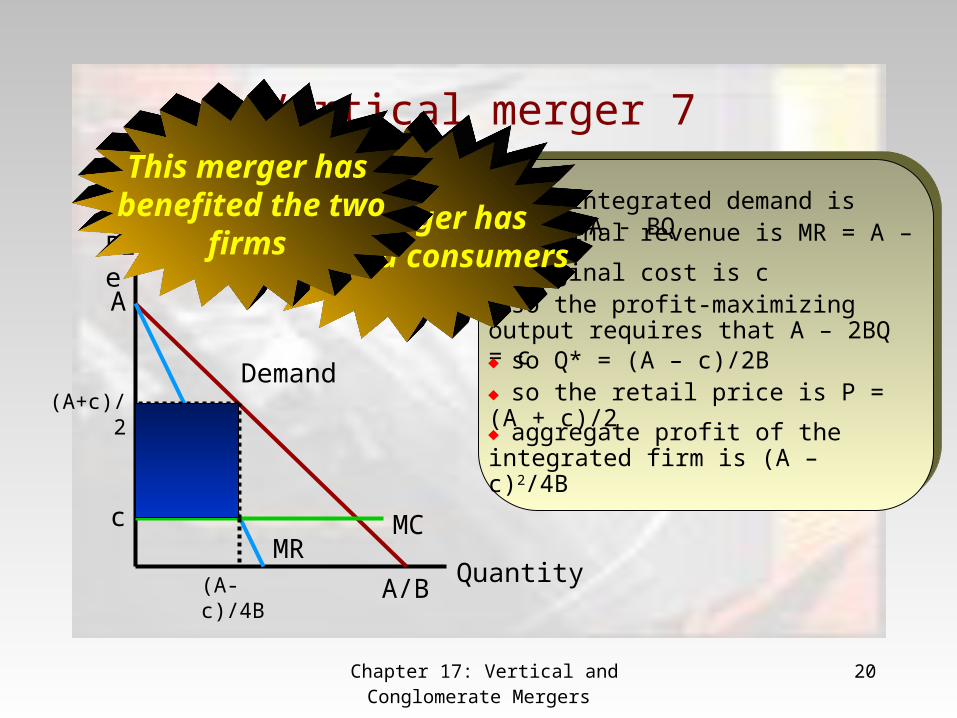

Vertical merger 7

Price

Quantity

Demand

A

A/B

MR

the integrated demand is P(Q) = A - BQ

c MC

marginal revenue is MR = A – 2BQ

marginal cost is cso the profit-maximizing output requires that A – 2BQ = cso Q* = (A – c)/2B

(A-c)/4B

so the retail price is P = (A + c)/2(A+c)/2

This merger has benefited consumers

aggregate profit of the integrated firm is (A – c)2/4B

This merger has benefited the two

firms

Chapter 17: Vertical and Conglomerate Mergers

21

Vertical merger 8• Integration increases profits and consumer surplus• Why?

– the firms have some degree of market power– so they price above marginal cost– so integration corrects a market failure: double marginalization

• What if manufacture were competitive?– retailer plays off manufacturers against each other– so obtains input at marginal cost– gets the integrated profit without integration

• Why worry about vertical integration?– two possible reasons

• price discrimination• vertical foreclosure

Chapter 17: Vertical and Conglomerate Mergers

22

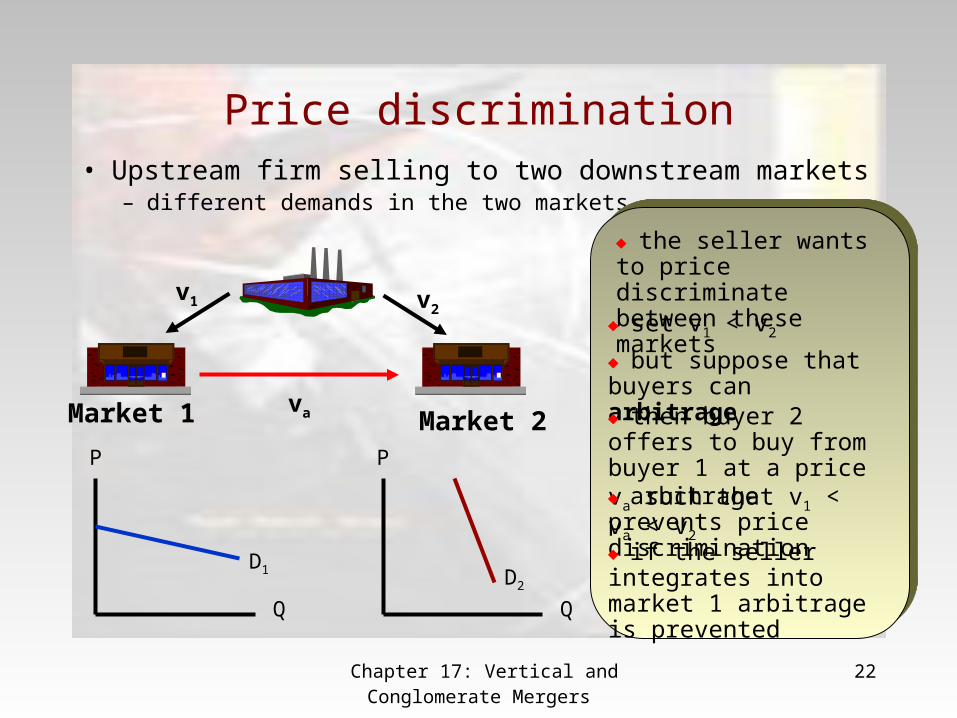

Price discrimination• Upstream firm selling to two downstream markets

– different demands in the two markets

Market 1 Market 2P

Q

P

Q

D1 D2

the seller wants to price discriminate between these marketsv1 v2

set v1 < v2

but suppose that buyers can arbitragethen buyer 2 offers to buy from buyer 1 at a price va such that v1 < va < v2

va

arbitrage prevents price discrimination if the seller integrates into market 1 arbitrage is prevented

Chapter 17: Vertical and Conglomerate Mergers

23

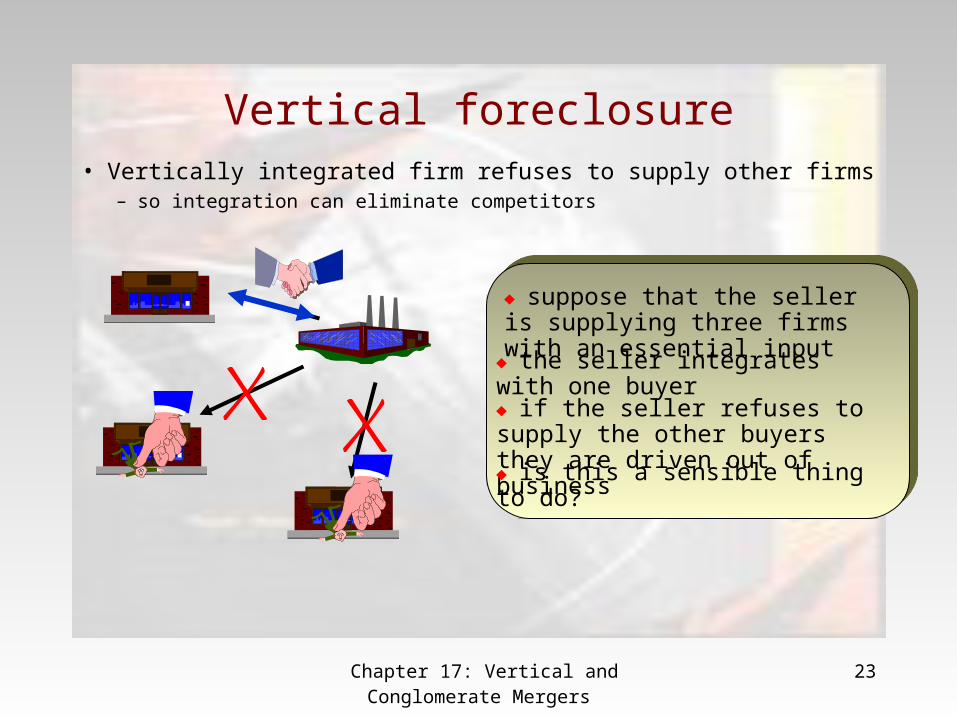

Vertical foreclosure

• Vertically integrated firm refuses to supply other firms– so integration can eliminate competitors

suppose that the seller is supplying three firms with an essential input

the seller integrates with one buyer

if the seller refuses to supply the other buyers they are driven out of business

is this a sensible thing to do?

Chapter 17: Vertical and Conglomerate Mergers

24

Vertical foreclosure 2

• Vertical foreclosure may reduce competition– offsets benefits of removing double marginalization

• But for this to work– foreclosure has to be a credible strategy for the merged firms

– foreclosure must be subgame perfect

• Consider two models of foreclosure– Salinger (1988) with Cournot competition

– Ordover, Saloner and Salop (1990) with price competition

Chapter 17: Vertical and Conglomerate Mergers

25

Vertical foreclosure 3 Suppose that there are some integrated firms and some independent upstream and downstream producers

Profit of an integrated firm is:

I = (PD - cU - cD)qDi

Profit of an independent upstream firm is:

U = (PU - cU)qUn

Profit of an independent downstream firm is:

D = (PD - PU - cD)qDn

The integrated firm willnot source on the independent

market

The integrated firm willnot sell on the independent

market

Chapter 17: Vertical and Conglomerate Mergers

26

Vertical foreclosure 4 For the independent upstream firms to survive requires PU - cU > 0

The downstream unit of an integrated firm obtains input at cost cU

Buying from an independent firm costs PU > cU

so the downstream divisions will not source externally

Now suppose that an upstream division of an integrated firm is selling to independent downstream firms it earns PU - cU on each unit sold

Divert one unit to its downstream division: this leaves the downstream price unchanged: it earns PD - cU - cD on this unit diverted

PD - PU - cD > 0 for independent downstream firms to survive

PD - cU - cD PD - PU - cD > 0

But this is true: sodiverting output fromthe external market

increases profits

so the upstream divisions will not sell externally

> PU - cU requires:

Profit from selling

internally

Profit from selling

externally

Chapter 17: Vertical and Conglomerate Mergers

27

Vertical foreclosure 5

• Foreclosure happens– but is not necessarily harmful to consumers

• reduces number of buyers in the upstream market

• increases prices charged by independent sellers to non-integrated downstream firms

• but integrated downstream divisions obtain inputs at cost

• puts pressure on non-integrated downstream firms

– provided there are “enough” independent upstream firms the anti-competitive effects of foreclosure will be offset by the cost advantages of vertical integration

• There are also strategic effects that might prevent foreclosure– to avoid non-integrated firms from integrating

Chapter 17: Vertical and Conglomerate Mergers

28

Vertical foreclosure 6

• The strategic aspects are considered in Ordover, Saloner and Salop (OSS)– suppose that there are two downstream and two upstream firms

• downstream firms make differentiated products

• upstream firms make homogeneous products

– both sets of firms compete in prices

– suppose that U1 merges with D1

• suppose also that they credibly refuse to supply D2

• then U2 is a monopoly supplier to D2

• U2 and D2 set prices reflecting double marginalization

• so they may well choose to merge also

– but U1 and D1 can foresee this and so may choose not to merge

Chapter 17: Vertical and Conglomerate Mergers

29

Vertical foreclosure 7• The OSS analysis thus far requires that there is no other source of the

input supply– if there is such a source this will constrain U2’s price

• may make merger of U2 and D2 less likely

• Also, U1D1 may try to undermine the merger another way

– offer to supply D2 undercutting U2

– find a price such that U2 and D2 have no incentive to merge

– so complete foreclosure is avoided

• Note that there is a timing problem with this analysis– U1 and D1 decide whether or not to merge

• if they do not the market continues as is

• if they do they seek to undermine a merger of U2 and D2

– but if U1 and D1 don’t merge U2 and D2 have a strong incentive to merge

Chapter 17: Vertical and Conglomerate Mergers

30

Vertical Merger and Oligopoly• The implication is that we should consider a simultaneous

model– fear of vertical merger by one pair of firms might induce vertical

merger by other firms– this might lead to a prisoners’ dilemma game

• vertical merger harms firms• benefits consumers• and is a Nash equilibrium for the merging firms

• Consider a (reasonably) simple model– two upstream and two downstream Cournot firms– downstream demand is P = A – BQ– upstream firms’ marginal costs are cU and downstream firms’

marginal costs (excluding the upstream input) are cD

Chapter 17: Vertical and Conglomerate Mergers

31

Vertical merger and oligopoly 2

• Competition in three stages– stage 1:

• upstream and downstream firms choose simultaneously whether or not to merge

– U1 merges with D1 and/or U2 with D2

– stage 2:• non-merged upstream firms compete in quantities

• merged upstream firms supply their downstream divisions at marginal cost cU

– stage 3:• downstream firms compete in quantities

• Three cases:– no vertical merger; one vertical merger; two vertical mergers

Chapter 17: Vertical and Conglomerate Mergers

32

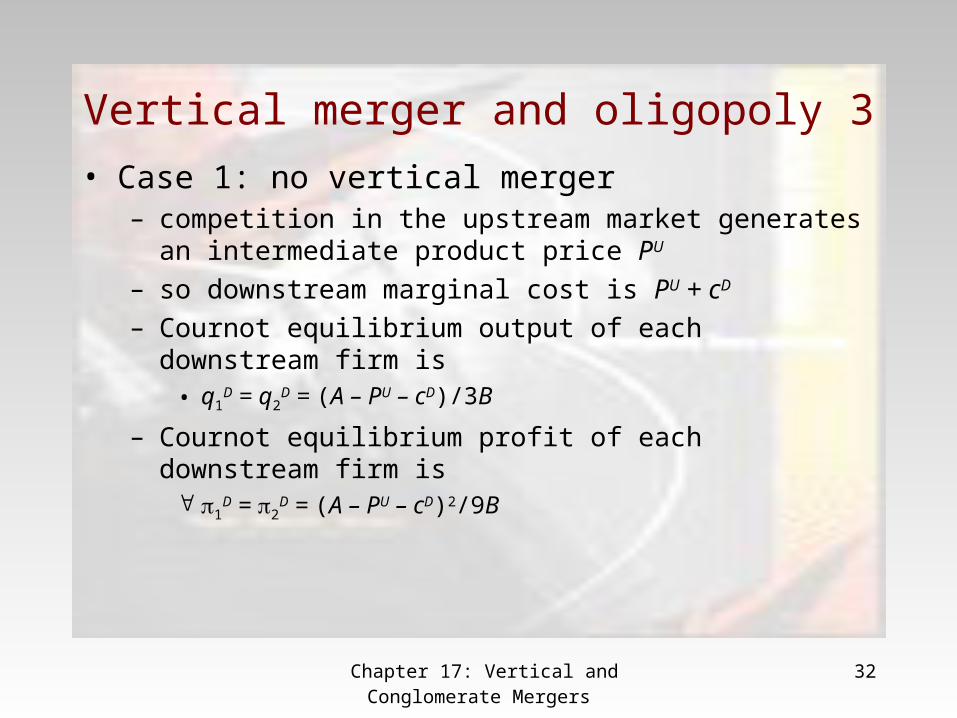

Vertical merger and oligopoly 3

• Case 1: no vertical merger– competition in the upstream market generates an intermediate

product price PU

– so downstream marginal cost is PU + cD

– Cournot equilibrium output of each downstream firm is• q1

D = q2D = (A – PU – cD)/3B

– Cournot equilibrium profit of each downstream firm is 1

D = 2D = (A – PU – cD)2/9B

Chapter 17: Vertical and Conglomerate Mergers

33

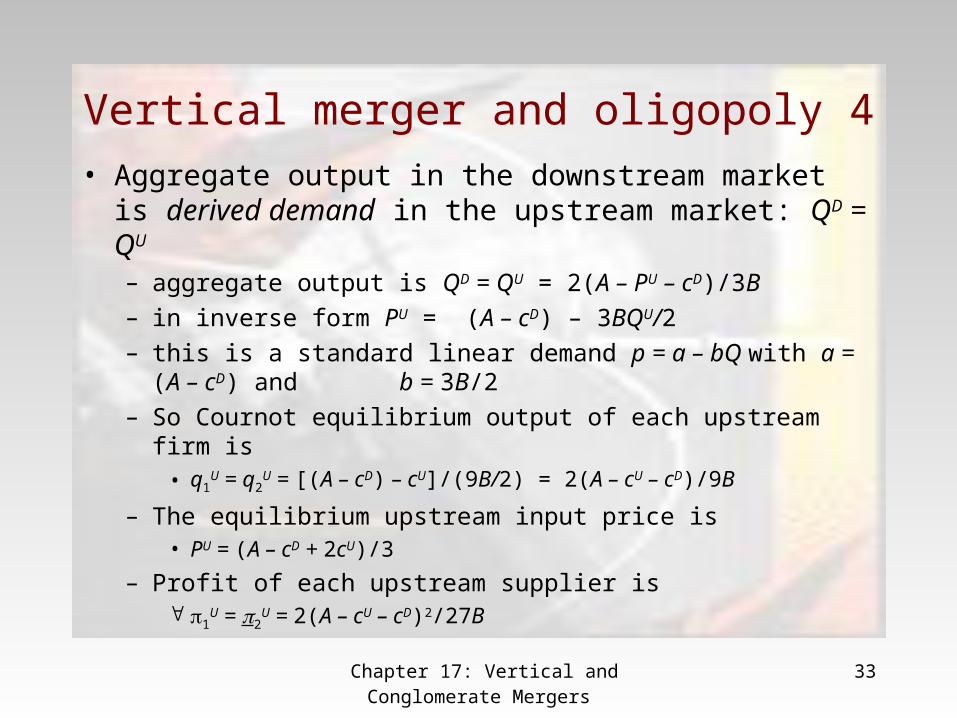

Vertical merger and oligopoly 4

• Aggregate output in the downstream market is derived demand in the upstream market: QD = QU

– aggregate output is QD = QU = 2(A – PU – cD)/3B

– in inverse form PU = (A – cD) – 3BQU/2

– this is a standard linear demand p = a – bQ with a = (A – cD) and b = 3B/2

– So Cournot equilibrium output of each upstream firm is• q1

U = q2U = [(A – cD) – cU]/(9B/2) = 2(A – cU – cD)/9B

– The equilibrium upstream input price is• PU = (A – cD + 2cU)/3

– Profit of each upstream supplier is 1

U = 2U = 2(A – cU – cD)2/27B

Chapter 17: Vertical and Conglomerate Mergers

34

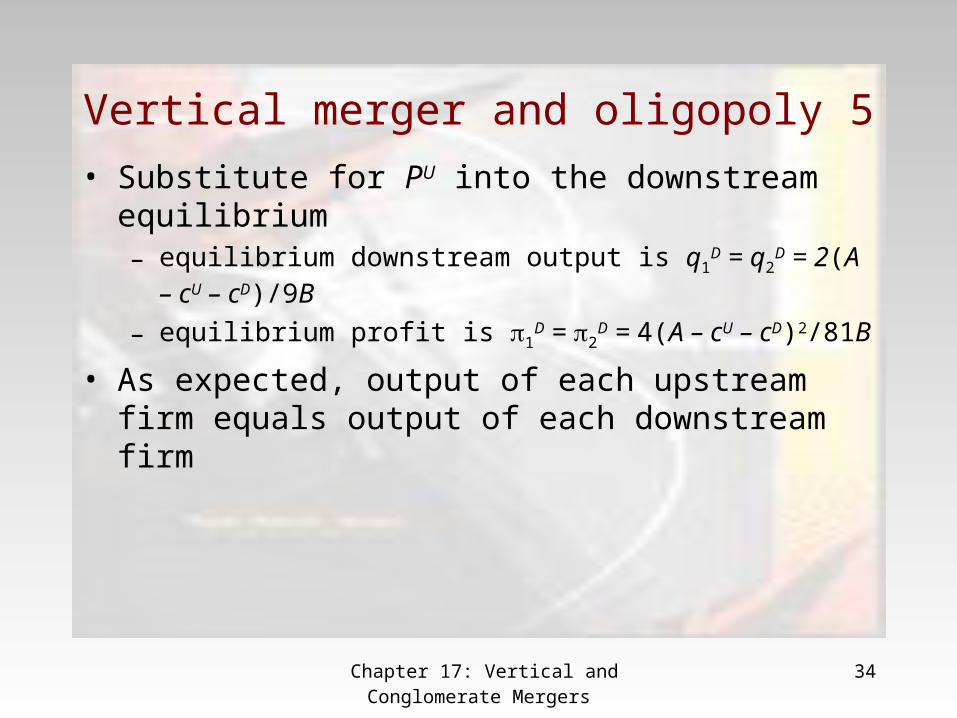

Vertical merger and oligopoly 5

• Substitute for PU into the downstream equilibrium– equilibrium downstream output is q1

D = q2D = 2(A – cU – cD)/9B

– equilibrium profit is 1D = 2

D = 4(A – cU – cD)2/81B

• As expected, output of each upstream firm equals output of each downstream firm

Chapter 17: Vertical and Conglomerate Mergers

35

Vertical merger and oligopoly 6

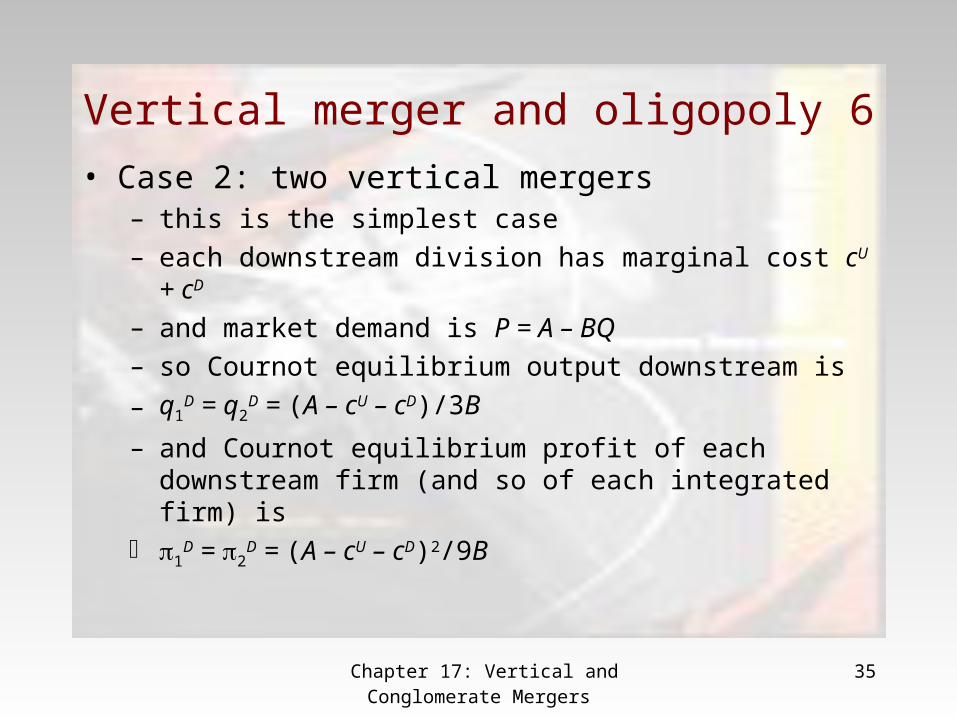

• Case 2: two vertical mergers– this is the simplest case

– each downstream division has marginal cost cU + cD

– and market demand is P = A – BQ

– so Cournot equilibrium output downstream is

– q1D = q2

D = (A – cU – cD)/3B

– and Cournot equilibrium profit of each downstream firm (and so of each integrated firm) is

1D = 2

D = (A – cU – cD)2/9B

Chapter 17: Vertical and Conglomerate Mergers

36

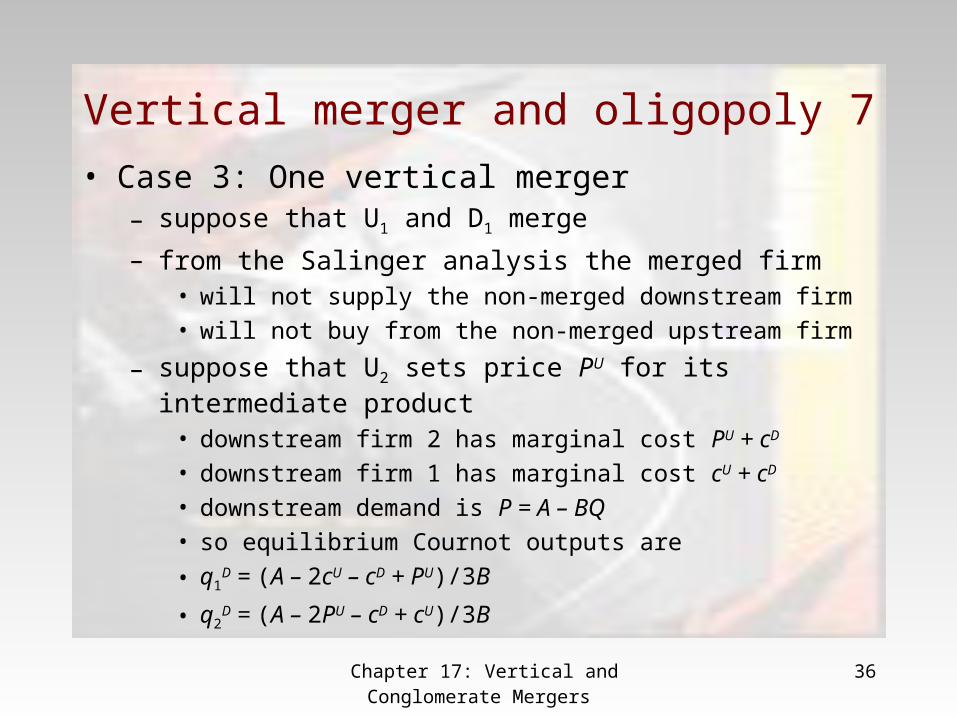

Vertical merger and oligopoly 7

• Case 3: One vertical merger– suppose that U1 and D1 merge

– from the Salinger analysis the merged firm• will not supply the non-merged downstream firm

• will not buy from the non-merged upstream firm

– suppose that U2 sets price PU for its intermediate product

• downstream firm 2 has marginal cost PU + cD

• downstream firm 1 has marginal cost cU + cD

• downstream demand is P = A – BQ

• so equilibrium Cournot outputs are

• q1D = (A – 2cU – cD + PU)/3B

• q2D = (A – 2PU – cD + cU)/3B

Chapter 17: Vertical and Conglomerate Mergers

37

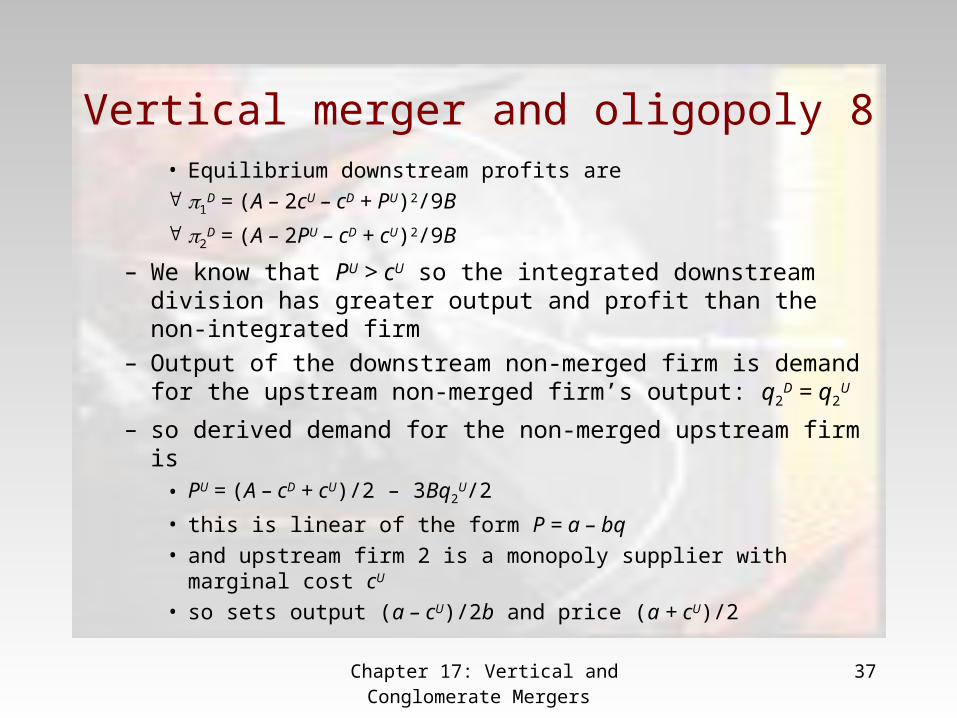

Vertical merger and oligopoly 8• Equilibrium downstream profits are 1

D = (A – 2cU – cD + PU)2/9B

2D = (A – 2PU – cD + cU)2/9B

– We know that PU > cU so the integrated downstream division has greater output and profit than the non-integrated firm

– Output of the downstream non-merged firm is demand for the upstream non-merged firm’s output: q2

D = q2U

– so derived demand for the non-merged upstream firm is• PU = (A – cD + cU)/2 – 3Bq2

U/2

• this is linear of the form P = a – bq

• and upstream firm 2 is a monopoly supplier with marginal cost cU

• so sets output (a – cU)/2b and price (a + cU)/2

Chapter 17: Vertical and Conglomerate Mergers

38

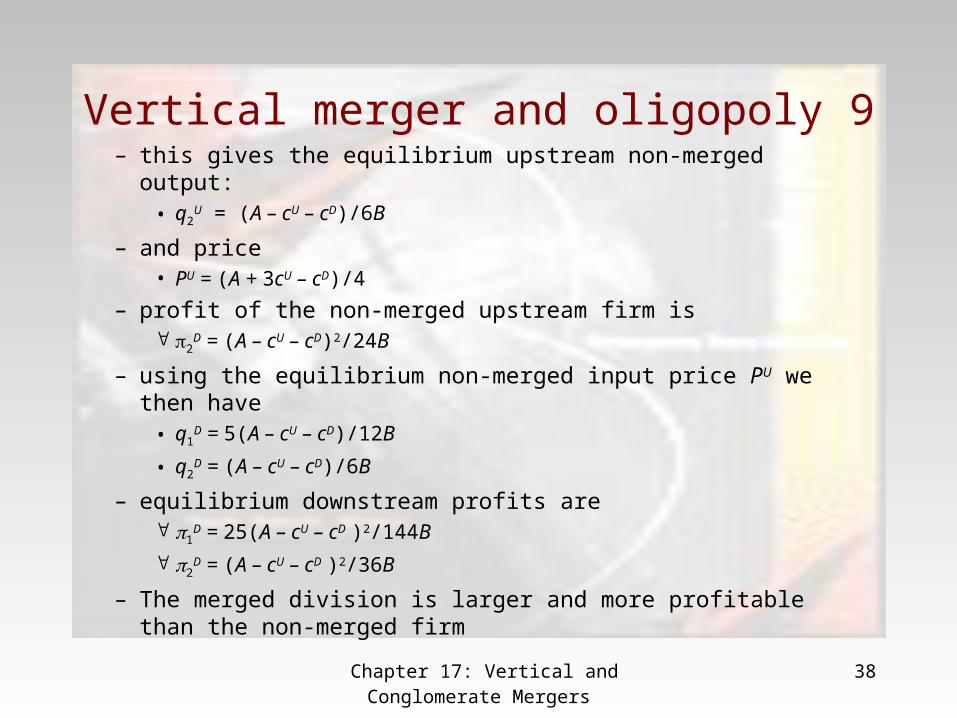

Vertical merger and oligopoly 9– this gives the equilibrium upstream non-merged output:

• q2U = (A – cU – cD)/6B

– and price• PU = (A + 3cU – cD)/4

– profit of the non-merged upstream firm is 2

D = (A – cU – cD)2/24B

– using the equilibrium non-merged input price PU we then have• q1

D = 5(A – cU – cD)/12B

• q2D = (A – cU – cD)/6B

– equilibrium downstream profits are 1

D = 25(A – cU – cD )2/144B

2D = (A – cU – cD )2/36B

– The merged division is larger and more profitable than the non-merged firm

Chapter 17: Vertical and Conglomerate Mergers

39

Vertical merger and oligopoly 10

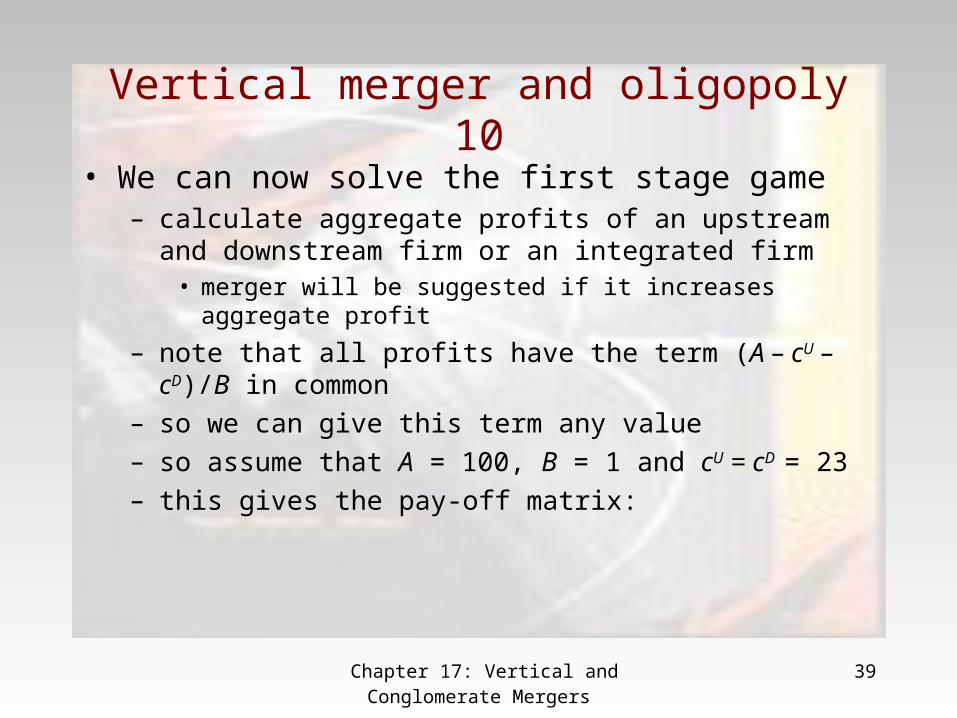

• We can now solve the first stage game– calculate aggregate profits of an upstream and downstream firm or

an integrated firm• merger will be suggested if it increases aggregate profit

– note that all profits have the term (A – cU – cD)/B in common

– so we can give this term any value

– so assume that A = 100, B = 1 and cU = cD = 23

– this gives the pay-off matrix:

Chapter 17: Vertical and Conglomerate Mergers

40

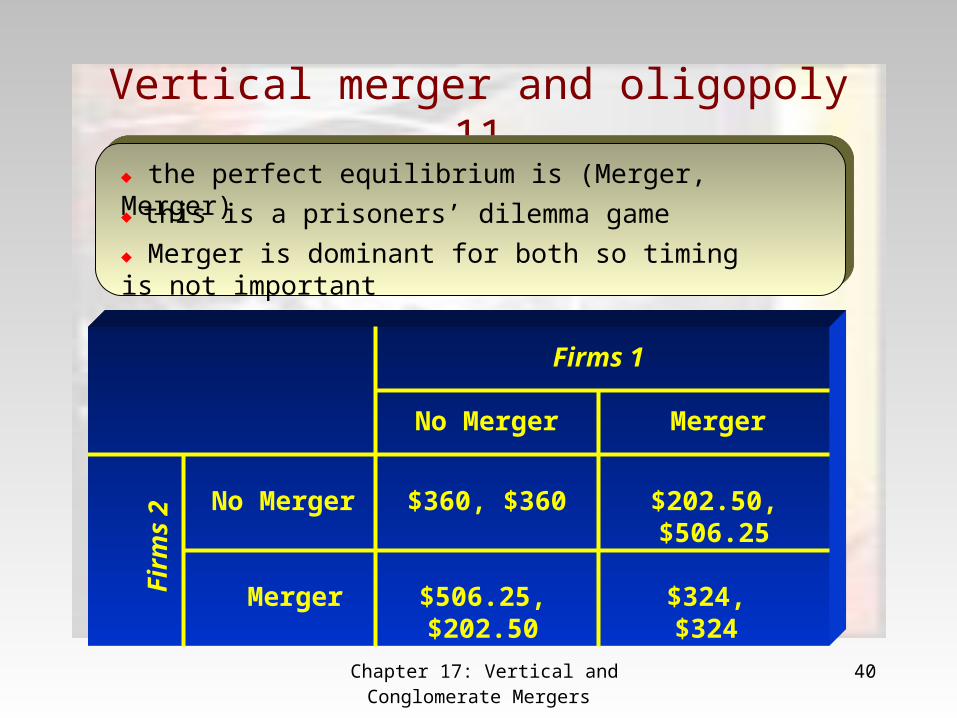

Vertical merger and oligopoly 11

Firms 1

Fir

ms

2

No Merger Merger

No Merger

Merger

$360, $360 $202.50, $506.25

$506.25, $202.50 $324, $324

the perfect equilibrium is (Merger, Merger)

this is a prisoners’ dilemma game

Merger is dominant for both so timing is not important

Chapter 17: Vertical and Conglomerate Mergers

41

Vertical merger - reappraisal

• Vertical merger has three effects in this model– removes double marginalization

– reduces cost for a downstream integrated firm and makes downstream market more competitive

– reduces competitive pressures in the upstream market

• In the model the first two effects dominate– so consumers benefit from lower prices even with only one

vertical merger

– but in equilibrium the firms lose from vertical merger

Chapter 17: Vertical and Conglomerate Mergers

42

Vertical merger – reappraisal 2

• Recall the proposed GE-Honeywell merger– if this is the only merger then the merged firm gains and the non-

merged firms lose• appears to be this that guided the EU Competition Directorate

• but consumers benefit even in this scenario

• and rivals have a clear strategic response: merge

– so the EU must have believed that merger by rivals was not possible

• ever!

– and that if the integrated GE-Honeywell gains a monopoly position price will rise

• but it is easy to check in the example that price would not rise

• So the decision remains questionable

Chapter 17: Vertical and Conglomerate Mergers

43

Conglomerate Mergers

• Bring under common control firms whose products are neither substitutes nor complements– results in a diversified firm

– period from 1960s to early 1980s is when many were forms

• Is there a convincing rationale for this type of merger?– if not then probably an accident of history

– gradually corrected by downsizing and focus on “core competence”

• Possible rationales:

Chapter 17: Vertical and Conglomerate Mergers

44

Conglomerate mergers 2

• Economies of scope– but these generally derive from use of common inputs

– so merged firms should be related in some respect• similar markets

• similar technologies

– data do not support this hypothesis

Chapter 17: Vertical and Conglomerate Mergers

45

Conglomerate mergers 3• Economize on transactions costs

– take a specialized machine can produce two goods A and B• markets for A and B are concentrated• if machine is used to produce only A there is spare capacity

– then owner may wish also to produce B – conglomeration– the owner could also lease use of the machine to a specialized B

producer to avoid conglomeration• but this has problems

– negotiating and bargaining over the lease

• conglomeration avoids these problems

– particularly important when the asset is knowledge intensive– so this motive is reasonable

• but the assets are common to all the conglomerates products• not supported by the data

Chapter 17: Vertical and Conglomerate Mergers

46

Conglomerate mergers 4

• Managerial motives– conglomeration suits interests of management but not shareholder

• division of ownership and control of large public corporations

• monitoring of management is far from perfect

• so management can pursue its own agenda to some extent

– suppose management compensation based on company growth• easier to grow by acquisition than internally

• horizontal merger may be blocked by regulators

• so grow by conglomeration

– conglomeration to reduce management risk• diversified firm has diversified risk

• this diversifies the risk that management faces

• Seems to be supported by the evidence

Chapter 17: Vertical and Conglomerate Mergers

47

Recommended