COMMERCIAL AUDIT MANUAL

OFFICE OF THE ACCOUNTANT GENERAL (C& RA)

ANDHRA PRADESH, HYDERABAD

(For Official use only)

i

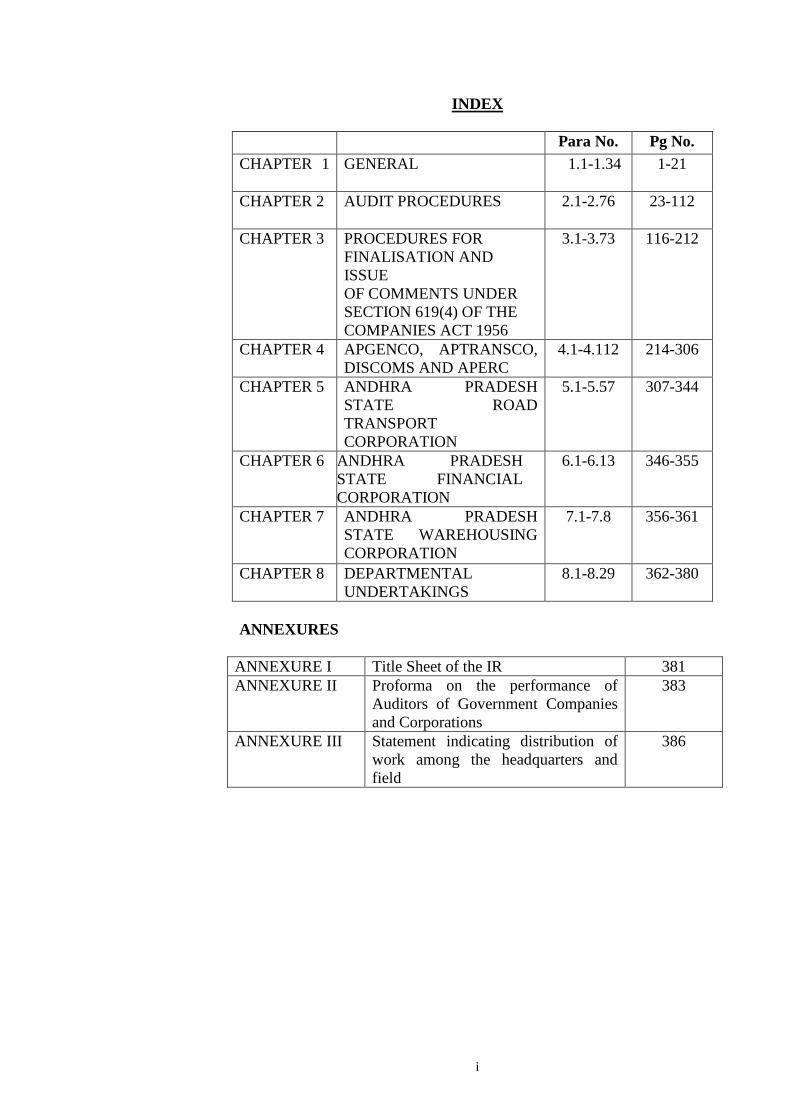

INDEX

Para No. Pg No.

CHAPTER 1

GENERAL

1.1-1.34 1-21

CHAPTER 2 AUDIT PROCEDURES

2.1-2.76 23-112

CHAPTER 3 PROCEDURES FOR

FINALISATION AND

ISSUE

OF COMMENTS UNDER

SECTION 619(4) OF THE

COMPANIES ACT 1956

3.1-3.73 116-212

CHAPTER 4 APGENCO, APTRANSCO,

DISCOMS AND APERC

4.1-4.112 214-306

CHAPTER 5 ANDHRA PRADESH

STATE ROAD

TRANSPORT

CORPORATION

5.1-5.57 307-344

CHAPTER 6 ANDHRA PRADESH

STATE FINANCIAL

CORPORATION

6.1-6.13 346-355

CHAPTER 7 ANDHRA PRADESH

STATE WAREHOUSING

CORPORATION

7.1-7.8 356-361

CHAPTER 8 DEPARTMENTAL

UNDERTAKINGS

8.1-8.29 362-380

ANNEXURES

ANNEXURE I Title Sheet of the IR 381

ANNEXURE II Proforma on the performance of

Auditors of Government Companies

and Corporations

383

ANNEXURE III Statement indicating distribution of

work among the headquarters and

field

386

ii

Reference to

CHAPTER 1 Paragraph Page(s)

Organisation and functions 1.1 1

Organisation 1.2 1

Audit of Annual Accounts 1.3 2

Introduction CAW (H) Sections 1.4 3

Organisational Chart of CAW 1.5 4

Sanctioned strength of Commercial Audit Wing 1.6 5

Procedure for Forecast and Staff proposals 1.7 5

Distribution of work in Headquarters Section 1.8 6

Functions of Commercial Audit Headquarters Section 1.9 6

Dissemination of Information 1.10 8

Responsibility for keeping the Commercial Audit Manual

up to date

1.11 8

Undertaking of new audits 1.12 9

Coordination with other Wings of the Office 1.13 9

Tour programmes 1.14 9

Traveling Allowance 1.15 9

Report work 1.16 10

Committee on Public Undertakings work 1.17 10

Resident Audit Organisation of AP Electricity Companies &

AP ERC

1.18 10

Resident Audit Organisation of A.P.S.R.T.C 1.19 12

Selection-of documents for audit 1.20 13

Review of Audit 1.21 14

Local Audit 1.22 14

Composition of the field parties 1.23 14

Selection of staff to be deputed for inspection work 1.24 15

Quantum of Audit 1.25 15

Percentage of supervision 1.26 15

Movement of the field parties 1.27 16

Deviation from tour programmes and extension of time for

local audit

1.28 16

Audit of accounts of offices of the State Government

situated outside the State

1.29 17

General 1.30 17

Time schedule for work in Commercial Audit Headquarters

Section

1.31 18

Pursuance and settlement of outstanding audit Objections 1.32 18

Maintenance of objection books in respect of Autonomous

bodies set up under specific Acts of Parliament/State

Legislature

1.33

20

Calculation of Audit Fees 1.34 21

CHAPTER-2

AUDIT PROCEDURE - GENERAL

Types of Audit

2.1 23

Audit of Accounts 2.2 23

iii

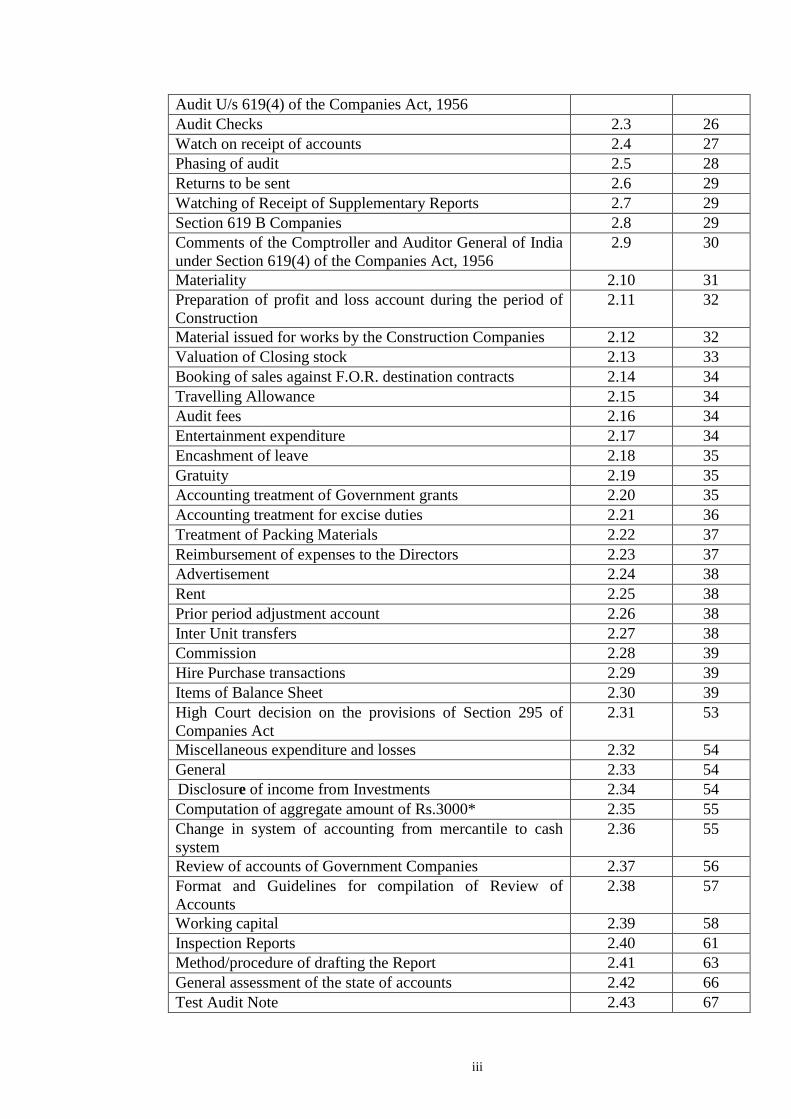

Audit U/s 619(4) of the Companies Act, 1956

Audit Checks 2.3 26

Watch on receipt of accounts 2.4 27

Phasing of audit 2.5 28

Returns to be sent 2.6 29

Watching of Receipt of Supplementary Reports 2.7 29

Section 619 B Companies 2.8 29

Comments of the Comptroller and Auditor General of India

under Section 619(4) of the Companies Act, 1956

2.9 30

Materiality 2.10 31

Preparation of profit and loss account during the period of

Construction

2.11 32

Material issued for works by the Construction Companies 2.12 32

Valuation of Closing stock 2.13 33

Booking of sales against F.O.R. destination contracts 2.14 34

Travelling Allowance 2.15 34

Audit fees 2.16 34

Entertainment expenditure 2.17 34

Encashment of leave 2.18 35

Gratuity 2.19 35

Accounting treatment of Government grants 2.20 35

Accounting treatment for excise duties 2.21 36

Treatment of Packing Materials 2.22 37

Reimbursement of expenses to the Directors 2.23 37

Advertisement 2.24 38

Rent 2.25 38

Prior period adjustment account 2.26 38

Inter Unit transfers 2.27 38

Commission 2.28 39

Hire Purchase transactions 2.29 39

Items of Balance Sheet 2.30 39

High Court decision on the provisions of Section 295 of

Companies Act

2.31 53

Miscellaneous expenditure and losses 2.32 54

General 2.33 54

Disclosure of income from Investments 2.34 54

Computation of aggregate amount of Rs.3000* 2.35 55

Change in system of accounting from mercantile to cash

system

2.36 55

Review of accounts of Government Companies 2.37 56

Format and Guidelines for compilation of Review of

Accounts

2.38 57

Working capital 2.39 58

Inspection Reports 2.40 61

Method/procedure of drafting the Report 2.41 63

General assessment of the state of accounts 2.42 66

Test Audit Note 2.43 67

iv

General 2.44 68

Revision of Title Sheet of Inspection Report 2.45 68

Certificate to be recorded on the report 2.46 69

Discussion of the Report 2.47 70

Documents to accompany the report 2.48 70

Functions of Inspecting Audit Officers/Senior Audit

Officers/Senior Audit Officer

2.49 72

Review of the system of Audit Committees 2.50 76

Procedure for preparation of Draft Paras 2.51 77

Procedure for pursuance of Draft Paragraphs in respect of

Companies under Section 619-B of the Companies Act

1956

2.52

78

Compilation of Reviews/Comprehensive Appraisals 2.53 79

Principles for selection 2.54 79

Preliminary Scrutiny 2.55 80

Performance Audit 2.56 80

Characteristics of good report 2.57 82

Adherence to style guide 2.58 82

Forwarding of the draft report 2.59 83

Response of the entity 2.60 84

Second journey of the report to SAI headquarters 2.61 84

Final report 2.62 84

Information Sources 2.63 85

Audit Findings 2.64 86

Presentation of results 2.65 91

Procedure for obtaining the approval of Headquarters Office 2.66 93

Size of the Audit Report to be printed 2.67 94

Committee On Public Undertakings 2.68 96

Accountant General to assist the Committee 2.69 97

Reports Section (Commercial Audit Wing) 2.70 97

Time Schedule for finalisation of material for Reports 2.71 99

Due dates for submission of material to Headquarters Office 2.72 99

Selection of topics/reviews for inclusion in the Audit Report

(Commercial) and finalisation of report

2.73 100

Criteria for selection of reviews 2.74 103

Separate audit reports on the accounts of statutory

corporations for which the C&AG of India is the sole

auditor

2.75 110

Uniformity in use of capital and small letters in the official

publications

2.76 112

CHAPTER-3

Procedure for finalisation and issue of comments under

Section 619(4) of the Companies Act, 1956

3.1 116

General 3.2 120

Procedure to be adopted where the annual accounts of a

Company were adopted in the Annual General Meeting

without the comments of the C&AG of India under Section

3.3 121

v

619(4) of the Companies Act, 1956.

Where the report of the Statutory Auditors is in negative 3.4 121

Appointment of Auditors 3.5 121

Printing of Management's replies in the Annual Report

against C.A.G's comments under Section 619(4) of the

Companies Act 1956

3.6 124

Study of accounting policies, etc. 3.7 124

Qualifications of Statutory Auditors 3.8 125

A gist of opinions (as expressed by the Expert Advisory

Committee of the Institute of Chartered Accountants of

India) on some accounting aspects are given

3.9 125

General principles of Audit of Transactions 3.10 130

Scrutiny of Memorandum and Articles of Association of

Government Companies

3.11 131

Internal control system in auditee organizations 3.12 131

Capital restructuring in public enterprises - guidelines 3.13 134

Distribution of work in inspection 3.14 134

First Audit of an Institution 3.15 135

Intelligent exercise of checks 3.16 135

Calling of files and records for checking 3.17 136

Certificate of cash balance 3.18 136

Procedure for simplification of initial accounts etc. 3.19 137

Special investigation and independent enquiry by Audit 3.20 137

Report of defalcations, frauds etc. 3.21 138

Raising and pursuance of observations 3.22 139

Prompt settlement of Audit observations 3.23 139

Procedure for auditing cash transactions 3.24 140

Works expenditure 3.25 147

Log books 3.26 150

Capital structure - Equity and Loans, total investments. 3.27 152

Remuneration for consultancy services 3.28 154

Stores 3.29 154

Disposal of unserviceable, obsolete and surplus stores, spare

parts, vehicles, tools, empties, scrap, by-products, etc.

3.30 156

Investments made by the Government Statutory

Corporations, Government Companies, Autonomous bodies

3.31 158

General 3.32 160

Interview with the Head of the Office inspected

Periodicity of audit: Under Section 619(3)(b) of the

Companies Act, 1956: Government Companies

3.33 162

Section 619 B Companies 3.34 162

Phasing of audits 3.35 162

List of government companies 3.36 162

Government Companies 3.37 180

Annual General Meeting and Accounts 3.38 182

Applicability of Section 619 of the Companies Act in

respect of the accounts for the period up to the final

3.39 182

vi

dissolution of a Company

Internal audit 3.40 183

Statutory audit 3.41 183

Organisational set-up 3.42 186

Review of Budgets 3.43 187

Borrowings 3.44 187

Debt-equity ratio 3.45 187

Cash Management 3.46 188

General 3.47 189

Computerised accounts 3.48 189

Supplementary report of the Statutory Auditors under

Section 619 (3) (a) of the Companies Act, 1956.

3.49

190

Audit of Cost accounts/records 3.50 191

Pricing 3.51 193

Recovery or Absorption of Overheads 3.52 194

Financial and service organisations 3.53 195

Service 3.54 198

Hire Purchase Scheme 3.55 198

Marketing Assistance Scheme 3.56 198

Raw Material Servicing Centre 3.57 199

Infrastructure Facilities 3.58 199

Coal Mines 3.59 201

Production Performance 3.60 201

Major equipment and plant and machinery 3.61 206

Manpower analysis 3.62 206

Sales performance and marketing 3.63 206

Price Fixation 3.64 207

Accounting Systems 3.65 207

Management Information System 3.66 208

Accidents 3.67 208

Hospitals 3.68 208

Sand stowing operations 3.69 209

Protective works 3.70 209

Sugar Industry 3.71 209

Irrigation 3.72 211

Trading 3.73 212

CHAPTER-4

Introductory 4.0 214

Constitutional provisions pertaining to Electricity 4.1 214

Central Legislation dealing with Electricity 4.2 214

Restructuring of APSEB 4.3 - 4.7 214-219

Constitution of Resident Audit office 4.8 219

Scope of extent of Audit 4.9 - 4.11 220-224

Delegation of Financial Powers 4.12 224

Results of Inspection and Local Audit 4.13 224

Compilation of Inspection Report 4.14 224

Instructions regarding writing and compiling the Inspection 4.15 - 4.16 225-226

vii

reports

Audit Of Receipts 4.17 - 4.68 226-250

Audit of Expenditure 4.69 - 4.90 251-281

Audit of Power Generating Stations 4.91 - 4.101 281-290

Annual Accounts 4.102 - 4.103 290-293

Miscellaneous 4.104 - 4.112 294-306

CHAPTER-5

Introduction 5.1 307

Scope of Audit 5.2 308

Resident Audit Section 5.3 308

Local Audit 5.4 309

Inspection Reports 5.5 309

Some Important Instructions/Guidelines for Audit 5.6 309

Head office wings/units 5.7 310

Budget, Budgetary Control and Financial Planning Fund of

the Corporation

5.8

311

Budget Estimates 5.9 311

Form of Budget (Rule 12 of the APSRTC Rules, 1958) 5.10 311

Financial Planning 5.11 313

Capital Contributions 5.12 313

investment of Surplus Funds 5.13 313

Borrowings 5.14 313

General Review in Audit 5.15 313

Remittances of Daily Earnings and Transfer of Surplus

Funds

5.16 315

Opening of Current Account of a New Depot 5.17 315

Internal Audit Wing 5.18 316

General Guidelines for Audit 5.19 316

Chief Traffic Manager (Commercial) 5.20 316

Chief traffic manager (operations) 5.21 317

Chief Traffic Manager (marketing) 5.22 318

Rotation of Vehicles 5.23 319

Vehicles Plying On Inter-State Route Permits 5.24 319

Guidelines For Audit 5.25 320

Payment through D.D. 5.26 320

Mechanical Engineering Department 5.27 320

Works Manager (Body Building Unit) 5.28 321

Works Manager (Printing And Stationery) 5.29 322

Controller of Stores - (BBU) 5.30 322

Chief Mechanical Engineer (Operation) 5.31 322

Personnel Department 5.32 323

Chief Controller of Stores 5.33 324

Chief Engineer(It & Ms) 5.34 325

Civil Engineering Department 5.35 326

Board Secretariat 5.36 327

Director-Vigilance and Security (V & S) 5.37 328

Land Acquisition Officer 5.38 328

viii

Chief Law Officer 5.39 329

Provident Fund Trust 5.40 329

APSRTC EDLIF Scheme 5.41 330

Zonal Office 5.42 331

Regional Office 5.43 331

Zonal/Regional Stores 5.44 332

Zonal/Regional Workshops 5.45 333

Tyre Retreading Shop 5.46 333

Regional/Zonal Staff Training College 5.47 334

Hospitals/Dispensaries 5.48 334

Civil Engineering Division (at each Zonal Level) 5.49 334

Depot 5.50 335

Way bills (MTD-5) 5.51 336

Maintenance and Stores Wing 5.52 338

Accounts and Personnel Wing 5.53 339

Payment of compounding fees/M.V. fines 5.54 340

Operation of Services on Special Hire 5.55 340

Cash books 5.56 340

Annual Accounts 5.57 344

CHAPTER-6

Andhra Pradesh State Financial Corporation 6.1 346

Objectives of the Corporation 6.2 346

Share Capital 6.3 346

Power to give instructions to the Corporation 6.4 347

Furnishing of returns 6.5 347

Appointment of Auditor 6.6 347

Issue of directions to the auditors 6.7 347

Audit by the Comptroller and Auditor General of India 6.8 347

Form of communication of Audit Report 6.9 348

Internal Audit 6.10 348

Provision for Wealth Tax 6.11 350

General 6.12 351

Revision of Accounts 6.13 355

CHAPTER-7

Andhra Pradesh State Warehousing corporation 7.1 356

Share capital 7.2 356

Borrowing powers 7.3 357

Accounts and audit 7.4 357

Form of communication of audit report 7.5 358

Audit of accounts of state warehousing corporation 7.6 359

General 7.7 359

Head office 7.8 361

CHAPTER-8

Nature and importance 8.1 362

Procedure for receipts and payments 8.2 363

Accounts 8.3 363

ix

Audit Arrangement 8.4 364

General Audit Principles 8.5 364

Establishment Bills 8.6 366

Travelling Allowance bills 8.7 367

Contingencies 8.8 367

General Cash Book 8.9 367

Cheques 8.10 368

Imprest or Permanent Advance Accounts 8.11 369

Stock and Store Books 8.12 369

Advance Ledger 8.13 369

Register of Movable and Immovable Properties 8.14 370

Register of Loans 8.15 370

Security Register 8.16 370

Service Books and Leave Accounts 8.17 370

Government Press 8.18 370

Scope of Audit 8.19 370

Process of Audit 8.20 371

Forms control and Despatch Section 8.21 374

Printing at Private Presses 8.22 374

Andhra Pradesh Government Text Book Press 8.23 374

Translations and Printing Department 8.24 375

Process of Audit 8.25 376

Proforma Accounts 8.26 377

Special points to be Seen 8.27 378

Comments on Proforma Accounts 8.28 378

Revision of accounts by the Organisation in the light of

Audit Comments

8.29

380

1

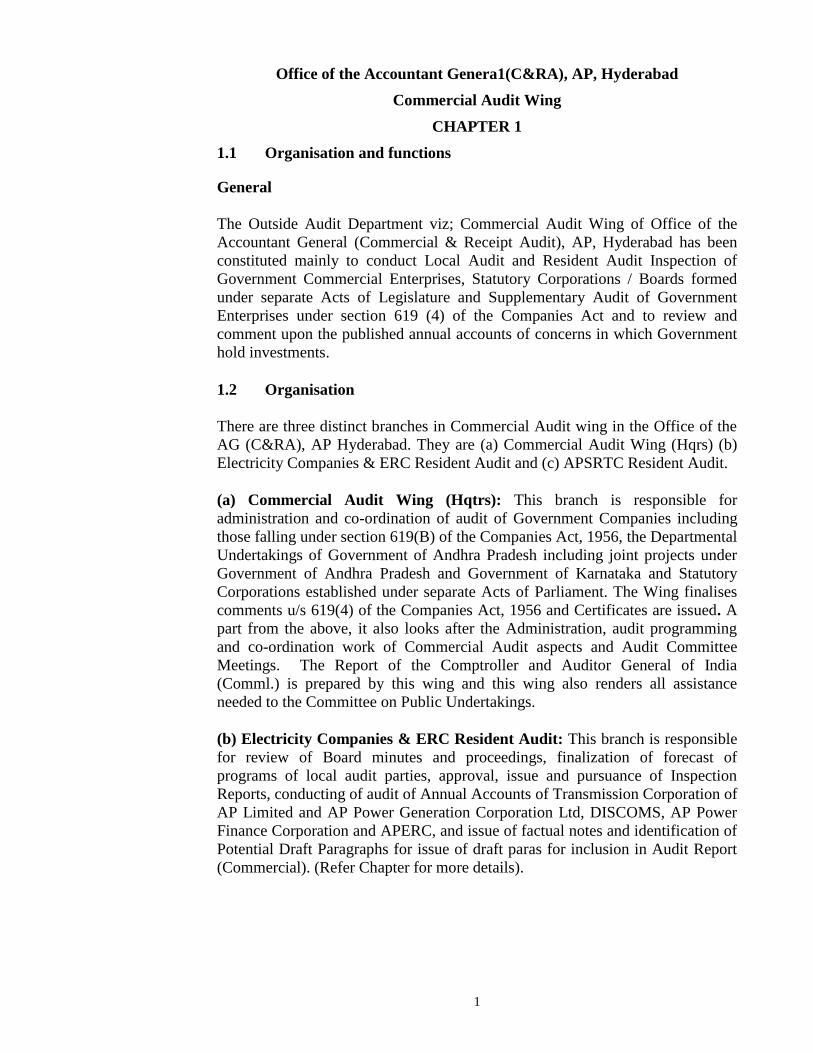

Office of the Accountant Genera1(C&RA), AP, Hyderabad

Commercial Audit Wing

CHAPTER 1

1.1 Organisation and functions

General

The Outside Audit Department viz; Commercial Audit Wing of Office of the

Accountant General (Commercial & Receipt Audit), AP, Hyderabad has been

constituted mainly to conduct Local Audit and Resident Audit Inspection of

Government Commercial Enterprises, Statutory Corporations / Boards formed

under separate Acts of Legislature and Supplementary Audit of Government

Enterprises under section 619 (4) of the Companies Act and to review and

comment upon the published annual accounts of concerns in which Government

hold investments.

1.2 Organisation

There are three distinct branches in Commercial Audit wing in the Office of the

AG (C&RA), AP Hyderabad. They are (a) Commercial Audit Wing (Hqrs) (b)

Electricity Companies & ERC Resident Audit and (c) APSRTC Resident Audit.

(a) Commercial Audit Wing (Hqtrs): This branch is responsible for

administration and co-ordination of audit of Government Companies including

those falling under section 619(B) of the Companies Act, 1956, the Departmental

Undertakings of Government of Andhra Pradesh including joint projects under

Government of Andhra Pradesh and Government of Karnataka and Statutory

Corporations established under separate Acts of Parliament. The Wing finalises

comments u/s 619(4) of the Companies Act, 1956 and Certificates are issued. A

part from the above, it also looks after the Administration, audit programming

and co-ordination work of Commercial Audit aspects and Audit Committee

Meetings. The Report of the Comptroller and Auditor General of India

(Comml.) is prepared by this wing and this wing also renders all assistance

needed to the Committee on Public Undertakings.

(b) Electricity Companies & ERC Resident Audit: This branch is responsible

for review of Board minutes and proceedings, finalization of forecast of

programs of local audit parties, approval, issue and pursuance of Inspection

Reports, conducting of audit of Annual Accounts of Transmission Corporation of

AP Limited and AP Power Generation Corporation Ltd, DISCOMS, AP Power

Finance Corporation and APERC, and issue of factual notes and identification of

Potential Draft Paragraphs for issue of draft paras for inclusion in Audit Report

(Commercial). (Refer Chapter for more details).

2

(c) APSRTC Resident Audit: This branch is responsible for review of Board

Minutes and proceedings, finalisation of forecast of programs of local audit

parties, approval, issue and pursuance of Inspection Reports and conducting, of

audit of Annual Accounts of the units of Andhra Pradesh State Road Transport

Corporation, which is a Statutory Corporation. (Refer Chapter for more details).

1.3 Audit of Annual Accounts

a) Corporations

(i) APSRTC

On receipt of intimation from the Management that the accounts i,e., trial

balance/ Account current at unit level are kept ready, the same shall be audited

annually at respective units and draft comments are communicated along with

audited trial balance/account current to the respective units and Head Office. The

audit of consolidated accounts (unadopted) shall be taken up after the audit of

accounts of unit offices are over and the approved report shall be issued

Corporation/State Government.

(ii) APSFC & APSWHC

On receipt of annual accounts duly approved by the Board and audited by the

statutory auditors appointed by the State Government, audit shall be conducted

every year and comments thereof issued to the Corporation.

b) Government Companies

Two sets of Statutory Auditors' report and adopted accounts of each Government

Company for each year are received from the statutory auditors in the

Commercial Audit Hqrs. Section. Immediately on receipt, audit of the annual

accounts shall be arranged, Processing of draft provisional comments/review of

accounts received from the field party, replies to the Statutory Auditors and

Management on provisional comments shall be done on priority, obtain the

approval of comments from the Headquarters office and communicate the same

to the Management before the date of Annual General Meeting/ adjourned

Annual General Meeting.

c) Departmental undertakings

Proforma Accounts received from the respective Departmental Undertakings,

shall be audited and the final comments thereof shall be communicated to the

Head of the Department.

3

1.4 Introduction CAW (H) Sections

Commercial Audit Wing of the AG(C&RA) AP is under the charge of a Senior

Deputy Accountant General/Deputy Accountant General. The functions of

various sections in Headquarters of the wing are as follows.

(a) Headquarters

There are four sections in Main office viz (1) Headquarters Sections (ii)

Companies–I section (iii) Companies–II section and (iv) Departmental

Undertakings under the charge of Sr. Audit Officers (Hqrs). The Headquarters

section deals with drawal of audit programmes of all the fieds parties, transfer

and posting of staff, proforma accounts of Departmental Undertaking, vetting of

draft inspection reports, pursuance of draft comments, all administrative matters

etc. It coordinates the affairs of the Commercial Wing as a whole.

(b) Reports

There are three sections in Main office viz., (i) Reports (ii) Draft Paras cell and

(iii) COPU section under the charge of Sr. Audit Officers (Reports).

The Reports Sections deals with the Reports of the CAG of India containing the

audit observations relating to Government Companies/Corporations. This

activity of the section includes selection of Companies/topics for detailed

Review for the Audit Report, vetting the draft Inspection Report/draft

reviews/draft reviews/draft paras received from the field parties, sending draft

reviews /drafts paras to Hqrs, attending to their marginal remarks, obtaining the

final approval of Hqrs for the Reports, getting the Report printed, obtaining

counter signature of CAG and issue to the Government.

The Sections also deals with the work relating to the meetings of Committeee on

Public Undertakings (COPU) and Audit Committees, and portion of Civil Audit

Report work dealing with the departmental undertakings.

(c) Resident Audit Sections

In addition to the above two sections located in Main Office, one resident audit

wing each for Electricity Companies and another for APSRTC were created to be

under the direct charge of Sr.DAG/DAG for coordinating the audit of the

respective organizations.

(d) Field Parties

Apart from the above, there are 20 field parties each headed by an

Assistant Audit Officers/Section Officers, conducting the audit of various

4

organizations and supervised by Inspecting Audit Officers/Sr. Audit

Officers.

1.5 Organisational Chart of CAW

COMMERCIAL AUDIT WING

Sr.AO (HQrs) 4 Sections

Sr.AO(Reports, Copu & DPs)

Field Supervising Officer Field

parties 20

R.A.O., I & II ECs & ERC RA

(Reports & DP Cell)

R.A.O APSRTC RA (Reports & DP Cell)

5

1.6 Sanctioned strength of Commercial Audit Wing

The sanctioned strength of the Wing as on 1st July 1991 consisted of the

following staff:

Office SrAO

/AOS

AAOs

/SOs

Sr.Ars/A

rs

Steno/Typ

ist

Clerk

s

Gr.’D

’

CAW Hqrs 2 6 14 2 2 2

Elec.Co RA 1 4 22 4 2

APSRTC, RA 1 3 12 1 2

Field-Com and

Corporations

31 36 23

Electricity

Companies

25 26

APSRTC 13 20

TOTAL 35 87 117 2 7 6

1.7 Procedure for forecast and Staff proposals

Every year during December the Commercial Audit Headquarters section and the

two Resident Audit Sections shall address all the existing Government

Companies, Statutory Corporations (APSRTC, APSFC, APSWHC)

Departmental undertakings APERC, Director of Industries and all TAD Sections

to furnish the list of units in existence as on that date, in order to ascertain

whether any new units have come into existence and/or any existing units were

closed along with the dates of formation/closure. This shall form the basis for

preparation of forecast for the next year. The party days required for each new

unit shall be assessed on the basis of detailed data collected. In regard to existing

units, the party days shall be calculated keeping in view the experience gained,

diversification of activities and increase in the existing workload. The forecast

shall also include the probable internal and external arrears. The forecast shall be

submitted to the Accountant General, through the Sr. Deputy Accountant

General (CAW) for approval by the respective Sections on or before 2nd

February.

The approved forecast forms the basis for staff proposals which are to be

forwarded by the respective Resident Audit Sections to the Commercial Audit

Headquarters section. The staff proposals shall contain the detailed supporting

data in justification for seeking additional posts of each category. The

circumstances, leading to accumulation of internal/external arrears and reasons

for unutilised man days, if any, shall also be dealt with in detail. The proposals

are to be made keeping in view the instructions issued by the Headquarters

Office from time to time. The Commercial Audit Headquarters Section shall

send the consolidated staff proposals of the wing to CASS-Co-ordination Section

for their scrutiny by July, after obtaining the approval of the Senior Deputy

6

Accountant General (CAW). After it is cleared by the CASS-Coordination

Section, the same shall be forwarded to the Administration Section duly

obtaining the approval of the Accountant General.

1.8 Distribution of work in Headquarters Section

Full particulars regarding duties allotted to each individual Auditor in

Headquarters Section shall remain on record in the Duty Register, which shall be

kept in the custody of the Asst. Audit Officer/Section Officer (Headquarters).

Whenever there is a change in the incumbency of a post, the detailed duties shall

be communicated to the incoming incumbent and his initials obtained in the Duty

Register, in token thereof.

Besides the Duty Register, a separate staff position register shall be maintained

in Headquarters Section, which serves as a continuous record of the duration of

services of the Gazetted Officers as well as other staff posted to Commercial

Audit Wing . Particulars regarding date of proceeding on leave, return from the

leave (other than casual leave), reversion from field inspection duty to

Headquarters, date of relief in previous section, date of reporting to Headquarters

Section, transit days etc., shall also be noted in the remarks column of this

Register. Whenever there is a change in the incumbency, the date of relief of the

outgoing incumbent and the date of joining of the incoming incumbent shall

invariably be noted in the " remarks" column.

1.9 Functions of Commercial Audit Headquarters Section

Commercial Audit Headquarters (CAW) Section is responsible for the following

items of work:

Supplying of records relating to local audit as well as previous years Inspection

Reports to the field parties. Besides sending the old inspection reports of the

offices under the current local audit in a station, the Headquarters’ section should

send reports of other offices in that station, though not covered by audit

programme, to the Inspecting Audit Officer for an on the spot settlement.

Editing the draft Inspection Reports received from the Inspecting Audit

Officers/Senior Audit Officers including the general verification of the facts and

figures given in the draft Inspection Report with reference to the A.Es and replies

thereof for submission to the Sr. Audit Officer (Headquarters, CAW)/Deputy

Accountant General. (CAW)/ Sr. Deputy Accountant General (CAW) for

necessary vetting and onward issue to the respective Managements.

Important Financial irregularities, losses, the value of which is more than

10,00.000/- shall be processed- as Draft Paragraphs. A separate register of such

Potential Draft Paragraphs shall be maintained.

7

maintenance of Register of Audit

scrutiny of replies to outstanding Inspection Reports and their settlement

maintenance of Register of serious financial irregularities

scrutiny of sanctions accorded by the Government for guarantees given by them

with reference to para 479 of the MSO(Tech)

issue of Sectional Office orders wherever necessary and supply of copies of

Codes and Manuals and all important office orders and circulars to the field audit

parties.

preparation of Monthly Reports of Arrears relating to Commercial Audit Wing

Preparation of:

(a) Staff position statement to be sent to Administration Section on the first of every

month,

(b) Acquittance Roll (separately for Headquarters and field parties) due to Bills

Section on the 20th of every month,

(c) Events statements (consolidated statement of Headquarters and field parties) due

to Bills Section on the 17th of every month

(d) Submission of all other returns and statements required by Administration

Section

Transmission of old records not required for- current work, to old records

section.

Issue of internal posting orders in respect of staff attached to Commercial Audit

Wing.

Processing and forwarding of applications connected with the Administration

Section, like applications for reversion from field inspection, applications for

appointments outside, etc., in respect of both gazetted and non-gazetted officers.

The following items are also attended by the RAP-APSRTS

Scrutiny of Corporation resolutions, Minutes of the meetings of the various

committees of the Corporations and Agenda papers, circulars, provisions of the

Act and rules made there under.

Finalisation of Separate Audit Report on the annual accounts of the Corporation.

8

Review of operational statistics

Scrutiny of establishment matters

Check of incorporation of units accounts by Main Accounts Section

Check of Journal entries passed by Main –Accounts Section and Budget and

Finance Sections of CAO's Office

Tracing of cash journal vouchers pertaining to Pay Master's Office

Check of allocation of vouchers (allocation of expenditure between capital and

revenue)

Audit of establishment, T.A. and contingent bills of C.A.O’s establishment,

Members and Officers of the Corporation at Headquarters.

Important financial irregularities, losses the value of which is more than

Rs.10,00,000/- shall be processed as draft paras. A separate register of all such

potential draft paras should be maintained.

1.10 Dissemination of Information

All the circular instructions received from various authorities from time to time

shall be compiled by Headquarters Section and circulated to all field parties for

their guidance in discharging their duties while conducting audit. Compendium

of comments on various Corporations/Government Companies/Departmental

undertakings, important and peculiar objections noticed in audit and study notes

of professional institutions on various subject matters and articles on topics of

interest and relevant to audit aspects shall also be got compiled and circulated

amongst field staff.

1.11 Responsibility for keeping the Commercial Audit Manual up to date

The Officer, in charge of Commercial Audit Headquarters Section, shall be

responsible for keeping this Manual up to date. He shall put up draft corrections

as soon as any Rules, orders or other communications affecting the contents in

this Manual come to notice, and supply correction slips thereto to the field staff

and Supervising Officers. The general unit is responsible for proper maintenance

of stock (guard) file of office orders/circulars issued from time to time which

shall be serially numbered. The Section Officers/Assistant Audit Officers of

field parties whenever they touch Headquarters shall, after the scrutiny of the

stock file of the Headquarters Section, record their dated signature in a register

maintained for the purpose in token of the scrutiny of the file. The register shall

be submitted to the Branch Officer once a month along with the stock file of

9

office orders/circulars (00 No.OAD.I/XII/38-Misc./70-71/22 Dt.23.11.1970 File

38-Misc./70-72 OAD Civil Headquarters).

The field, Inspection parties shall also scrutinise at each inspection, the relevant

portion of the Manual with a view to examine whether any amendment is

required in any respect and make suggestions accordingly.

1.12 Undertaking of new Audits

Every new audit undertaken under para 13(2) of the Indian Audit and Accounts

Order (now under Section 16 and 17 of C&AG's: (DPC) Act, 1971 or the

discontinuance of such an audit shall be reported to CAG for his information. In

making such a report, the effect of the addition or discontinuance on the strength

of the establishment of the audit office shall also be mentioned (Lr. No. 156-

Admn.I/30. 38 dt,4, 3.1938).

1.13 Coordination with other Wings of the Office

The Commercial Audit Headquarters Section shall have close and cordial

coordination with Administration Section/Bills Section/CTM Section etc., in

regard to staff Matters, scrutiny of T.A.Bills, forwarding tour advance

applications, salaries of field staff, periodical returns and instructions received

from the Headquarters Office, etc.

1.14 Tour programmes

Quarterly tour programmes of all field inspection parties and Inspecting Audit

Officers/Senior Audit Officers of the entire wing shall be drawn by Commercial

Audit Headquarters Section based on the approved forecasts and keeping in view

the timely receipt of annual accounts. Further the tour programmes should reflect

the effective deployment of available manpower to achieve objectives of

certification of annual accounts and propriety audit of various organisations. The

tour programmes so drawn shall be approved by the Sr. Dy.Accountant General

(CAW) and communicated to the concerned in time. Notice of information to

the offices to be visited shall also be sent well in advance.

1.15 Traveling Allowances

The Commercial Audit Headquarters Section shall receive the tour- advance

applications from the fie1d staff and officers every month. After scrutiny with

reference to the approved tour programmes and pendency in submission of

detailed T.A. bills, etc., the same shall be forwarded to Bills Section for

necessary action at their end. The field staff and officers shall submit their

detailed T.A. bills to Commercial Audit Headquarters Section before 5th of the

succeeding month positively.

10

The following procedure shall be adopted before forwarding the same to Bills

Section:

i) Diarise the detailed T.A bills received from the field parties and officers

indicating the name of the official, month and amount of the bill, etc.,

ii) Intimate the Bills Section the fact of receipt of detailed T.A. bills indicating

the name of the official, month and amount of the bills soon after their receipt

in Headquarters Section.

iii) Verify the correctness of the detailed T.A. bills with reference to approved tour

programme and deviations, if-any.

iv) Verify the leave spells.

v) Local journey by scooter, stay in lodges at places other than the place of duty for

want of accommodation facilities, etc., and record the endorsement and

certificates suitably and forward the bills to bills section for necessary action.

1.16 Report Work

The Report Section of the Commercial Wing is entrusted with the work of

preparation of material for the Report of the C&AG of India (Comml.). It shall

initiate steps for sending the proposals for selection of topics by the Headquarters

Office every year. The material for Reviews and Draft Paragraphs received from

Resident Audit Sections and Commercial Audit Headquarters section shall be

processed till the same are approved by the Headquarters office.

The responsibility for getting the report printed and presented to the both Houses

of State Legislature devolves on this Section.

1.17 Committee on Public Undertaking work

On receipt of intimation of sittings of the Committee on Public Undertakings and

the subjects to be taken up for discussion from the State Legislature Secretariat,

the Sr.DAG/DAG(CAW), the AG and the Headquarters Office shall be informed

of the same. On the dates of sitting of the Committee on Public Undertakings,

the SO/AAO, AO(COPU), the Sr.DAG/DAG(CAW) and/or AG shall be present

at the Meeting with all the relevant files and assist the Committee in their

deliberations.

1.18 Resident Audit Organisation of AP Electricity Companies & AP

ERC

The main duties of the resident audit branch are:

11

To despatch the previous outstanding Inspection Reports to the field parties, edit

the Draft Inspection Reports received from the Inspection parties including the

general verification of the facts and figures given in the Inspection Reports, with

reference to audit enquiries and the replies thereof.

To issue the Inspection Reports after the approval of Sr. DAG/DAG (CAW)

where the Inspections are supervised by the IAOs, and after the approval of the

RAO where the audits were not supervised by the lAOs. The IRs are to be

pursued until they are finally settled.

Important financial irregularities, losses, the value of which is more than

Rs.10,00,000 should be processed as draft paras.

A separate register of such potential draft paras shall be maintained.

To maintain a register showing the commencement and completion of audit, the

date of receipt of the IR in the Resident Audit Branch, Date of approval of the

appropriate authority and date of issue of the IR.

To supply to the Inspection parties copies of all important orders and

classifications received, if any, which are useful for inspection purposes.

To scrutinise the various proceedings, Board minutes, agenda notes and

resolutions passed at the periodical meetings of the AP Electricity Companies &

APERC and calling for the relevant files, etc., where ever considered necessary.

To calculate the audit fees recoverable from Andhra Pradesh Electricity

Regulatory Commission (APERC) based on the instructions issued by the Office

of the Comptroller and Auditor General of India regarding the formula for

calculation as well as charges, if any, in the average cost of a particular category

of post. The average cost of each post and the miscellaneous charges to be taken

into account are communicated by the Administration every year. The amount so

calculated is checked by I.T.A Section after which the approval of Sr.DAG/DAG

(CAW) and the Accountant General shall be obtained and recovered from

APERC.

To maintain 'Register of Points’ specifically noticed and requiring verification

during local audits and send the same for verification to local audit parties.

To scrutinize the high value purchase orders approved by the Board of Directors

(or by the subcommittee of the Board constituted for the purpose) of

APTRANSCO/APGENCO.

To finalise the comments of the Comptroller and Auditor General of India under

section 619(4) of the Companies Act 1956 on the Annual accounts of

APTRANSCO, APGENCO, APEPDCL, APSPDCL, APNPDCL, APCPDCL

12

and AP Power Finance Corporation Limited and to issue the same to the

management of the respective Companies with the approval of the competent

authority.

To finalise the Separate Audit Report on the Annual accounts of APERC and

forward the same along with the Audit Certificate to the Company and the State

Government and APERC after obtaining the approval of the Comptroller and

Auditor General of India in respect of APERC.

1.19 Resident Audit Organisation of A.P.S.R.T.C

The audit of the accounts of the following units situated at GM.'s office of

A.P.S.R.T.C. is being conducted by Resident Audit Party consisting of two

Section Officers/Assistant Audit Officers under the supervision of Resident

Audit Officer and the report is being issued every half year.

a) G. M.’s Office

b) Chief Industrial Engineer

c) Chief Accounts Officer

d) Chief Civil Engineer (East and West)

e) Land Acquisition Officer

f) Printing Press

g) Headquarters Depot

h) G.P.F. Trust

i) Chief Mechanical Engineer

j) Chief Controller of Stores

k) Controller of Stores - Including purchases, receipts

l) Controller of Stores - issues and disposal of stores and their accounts

m) Central Workshops

n) Tyre/Retreading Shop

o) Body Building Unit

p) Labour Welfare Officer

q) Internal Audit Wing

r) Deputy Chief Accounts Officer, P.F.Trust.

s) Deputy Chief Accounts Officer, Inspection

13

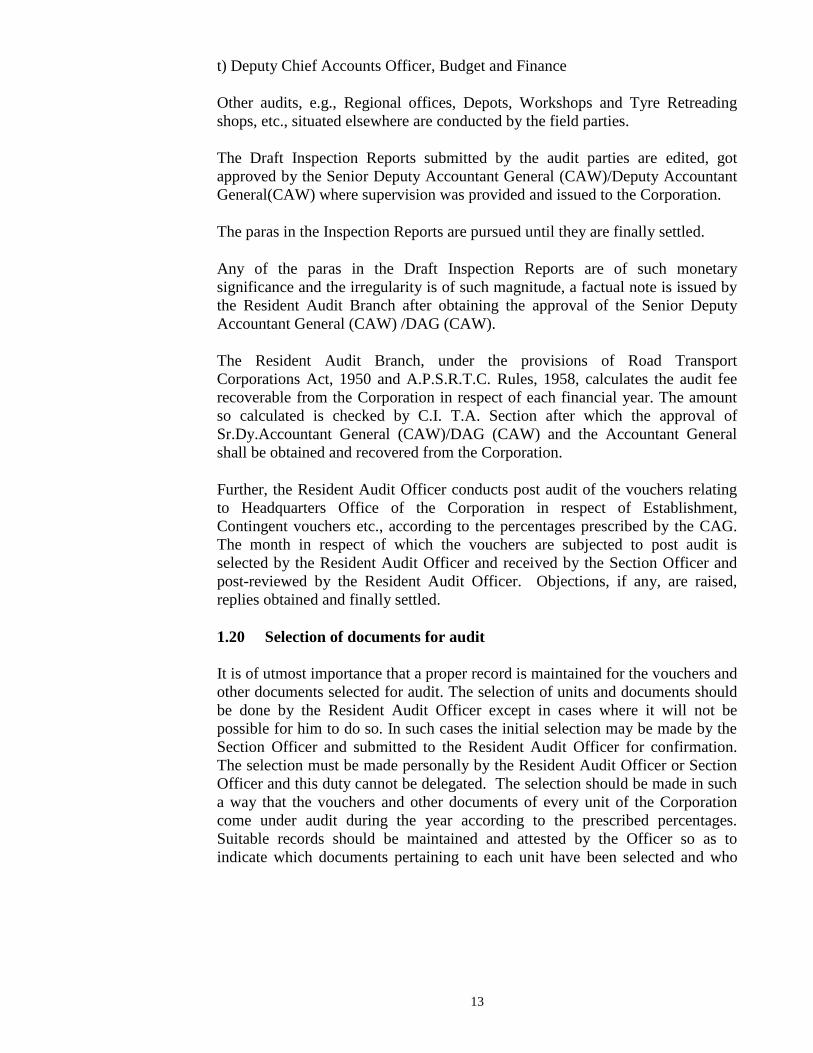

t) Deputy Chief Accounts Officer, Budget and Finance

Other audits, e.g., Regional offices, Depots, Workshops and Tyre Retreading

shops, etc., situated elsewhere are conducted by the field parties.

The Draft Inspection Reports submitted by the audit parties are edited, got

approved by the Senior Deputy Accountant General (CAW)/Deputy Accountant

General(CAW) where supervision was provided and issued to the Corporation.

The paras in the Inspection Reports are pursued until they are finally settled.

Any of the paras in the Draft Inspection Reports are of such monetary

significance and the irregularity is of such magnitude, a factual note is issued by

the Resident Audit Branch after obtaining the approval of the Senior Deputy

Accountant General (CAW) /DAG (CAW).

The Resident Audit Branch, under the provisions of Road Transport

Corporations Act, 1950 and A.P.S.R.T.C. Rules, 1958, calculates the audit fee

recoverable from the Corporation in respect of each financial year. The amount

so calculated is checked by C.I. T.A. Section after which the approval of

Sr.Dy.Accountant General (CAW)/DAG (CAW) and the Accountant General

shall be obtained and recovered from the Corporation.

Further, the Resident Audit Officer conducts post audit of the vouchers relating

to Headquarters Office of the Corporation in respect of Establishment,

Contingent vouchers etc., according to the percentages prescribed by the CAG.

The month in respect of which the vouchers are subjected to post audit is

selected by the Resident Audit Officer and received by the Section Officer and

post-reviewed by the Resident Audit Officer. Objections, if any, are raised,

replies obtained and finally settled.

1.20 Selection of documents for audit

It is of utmost importance that a proper record is maintained for the vouchers and

other documents selected for audit. The selection of units and documents should

be done by the Resident Audit Officer except in cases where it will not be

possible for him to do so. In such cases the initial selection may be made by the

Section Officer and submitted to the Resident Audit Officer for confirmation.

The selection must be made personally by the Resident Audit Officer or Section

Officer and this duty cannot be delegated. The selection should be made in such

a way that the vouchers and other documents of every unit of the Corporation

come under audit during the year according to the prescribed percentages.

Suitable records should be maintained and attested by the Officer so as to

indicate which documents pertaining to each unit have been selected and who

14

has been made responsible for the various processes of scrutiny connected with

the audit of these documents.

The Officer-in-charge should take a personal part in original audit work in

addition to his supervision, direction and review of the audit work done by the

Auditors and conducted by the Section Officers/Assistant Audit Officers.

1.21 Review of Audit

After the accounts and vouchers have been audited they should be subjected to

review according to the prescribed procedure. The Officer-in-charge and the

Section Officer, when reviewing the accounts, should bear in mind the

requirements of audit against propriety (vide para 54 of M.S.O. (Tech)

Volume.I).

After the Auditors have completed the audit of documents and of accounting, the

Section Officer should review them generally to see that no important points

have escaped the Auditor's scrutiny. Particular attention should be given to the

adjustment vouchers to see the necessity and regularity of the adjustment. It

should be further ensured that the review conducted is in accordance with the

prescribed percentages.

Review and communication of audit remarks should normally be completed

within the period prescribed for the audit of the various accounts and documents.

Any such review not completed before the date fixed for the completion of audit

should be deemed to be in arrears and exhibited as such in the Green Book.

1.22 Local Audit

Audit of accounts of Corporations, Government Companies and Departmental

undertakings etc., is conducted at respective units by deploying local Audit

Parties. The provisions of paras 767 to 795 of the Manual of Standing Orders

(Tech) Vol-I form the basis for the detailed procedure of conducting local audit.

The principles of efficiency audit, overall performance audit and audit against

propriety laid down in the said Manual shall also be kept in view as guidelines

for local audit.

1.23 Composition of the field parties

Each field party attached to the Commercial Audit Wing shall comprise of atleast

one Section Officer/Assistant Audit Officer and one auditor depending upon the

availability of auditors.

15

1.24 Selection of staff to the deputed for inspection work

a) If inspections are to serve their purpose and if the maximum value is to be

obtained for the expenditure incurred on inspections, the inspection work shall be

entrusted to specially trained, competent and intelligent staff who would, in

addition to exercising the routine prescribed checks, also examine the accounts

intelligently and pay due regard to the principles of efficiency audit. Special

attention shall, therefore, be paid to the selection of staff deputed for inspection

work, so that it may be ensured that inspections are conducted in a really

effective manner. (CAG's Lr.No.539/Admn/5Rep/49 dt.23.3.1950).

b) As far as possible preference shall be given to Auditors who have about three

years experience of inspection work (CAG's Lr.No.5117-El/53-58

dt.31.10.1958).

c) It shall be ensured that the personnel of the local audit party particularly

Section Officers/Assistant Audit Officers and Audit Officers/Senior Audit

Officers are not changed in the midst of an inspection, as such changes seriously

affect the efficiency of local audit.

(D.O. Lr.No.673/TA.I/JO(TA)75 dt.5.8.1976 of Addl.Dy.CAG).

1.25 Quantum of Audit

While detailed quantum of checks to be exercised were prescribed for

conducting the audit of accounts of Electricity Companies, A.P. State Road

Transport Corporation and Departmental undertakings, no such checks were

prescribed in respect of audit of Government Companies/AP State Financial

Corporation and AP State Warehousing Corporation. Audit of Government

Companies/Corporations shall be conducted keeping in view the various

provisions of the respective Acts and Instructions issued from time to time by

Headquarters Office. The checks to be exercised are detailed in respective parts.

1.26. Percentage of supervision

The following percentages have been prescribed by CAG for supervision.

1. Government Companies/Corporations with paid-up capital of above Rs.2

crores. 100%

2. (a) Government Companies/Corporations with paid-up capital of above Rs.25

lakhs and up to Rs.2 crores - 50%

(b) Statutory/Autonomous bodies other than Government Companies and

Statutory Corporations 50%

16

3. With a paid-up capital of less than Rs.25 lakhs - 33 1/3%

4. Government departmental commercial undertakings 33% to 50% depending

upon the size/importance

5. Various units of APSRTC 50%

The above mentioned supervision shall be provided after excluding transit days

and holidays (CAG's Lr.No.1055CA/23/GE~II dt. 28. 3.1967 IV-22/58-59Nol.P.

189).

1.27 Movement of the field parties

The movement of the field parties shall be strictly regulated according to the

approved programmes, Any deviation in adherence to the approved programmes

of supervising officers and parties shall receive the prior approval of the Sr.

DAG (CAW).

1.28 Deviation from tour programmes and extension of time for local

audit

The time allowed for local audit should not be exceed without prior approval of

the Sr.DAG (CAW)/DAG (CAW) and the time schedule should be adhered to

scrupulously by making extra efforts, if necessary.

The AAOs/SOs incharge of the field parties should be in a position to gauge the

quantum of work in a day or two after the commencement of local audit and any

extension of time, found necessary, should be applied for immediately. In

applying for extension of time in any particular case, the circumstances which

render the extension necessary should be fully narrated for consideration and

orders. It should be especially noted by the field staff that extension of time will

not be granted as a matter of course in all cases. When extension of time is

absolutely necessary, it would be applied for sufficiently in advance, with the

definite recommendations of Inspecting Audit. Officer (in the case of supervised

inspection) so that orders of Sr.DAG(CAW)/ DAG(CAW) on the application for

extension of time may be communicated in time before the extension is availed

of.. Unauthorised extension of time will entail forfeiture of daily allowance

unless the case of extension is sanctioned by the Sr.DAG (CAW)/ DAG(CAW).

Note: The local audit of an office undertaken should not be left unfinished on the

plea that time allocated is insufficient. The field party should promptly initiate

action as above and obtain the required extension, lest it should lead to deputing

another party to complete the unattended items of work.

17

1.29 Audit of accounts of offices of the State Government situated outside

the State

Where Civil Departments of the State Government and Units of the Companies

have their activities in other States, the audit of the accounts of such offices may,

with the prior approval of CAG be entrusted to the AG in whose jurisdiction the

offices exist.

Receipt of Board Minutes and agenda of various Government Companies/

Corporations shall be watched and the same shall be reviewed and submitted to

the DAG(CAW)/ Sr.DAG(CAW). Areas of interest. shall be intimated to the

parties for indepth study.

1.30 General

1.30.1 Reportss, returns and Registers

A calendar of returns is to be maintained in accordance with the instructions

contained in para 6.01 of the Manual of General Procedure in the form

prescribed, in order to observe the due dates prescribed for the various items of

work and returns to be submitted to various outside authorities, officers in the

office and other sections. The actual date on which the work is completed shall

be filled in, in each case and the calendar duly completed shall be submitted to

the officer on due dates as prescribed from time to time.

1.30.3 Quaterly Review Meetings

Generally conference of Section Officers/Assistant Audit Officers and Audit

Officers/Senior Audit Officers of the Wing is held quarterly to review the

following:

(i) audits/reviews conducted during the last quarter and important points raised

and salient features to ascertain whether all aspects and areas were covered in -

audit with the desired efficiency, if not to tone up the system of approach to

audit.

(ii) identification of areas of interest having potential material for conducting

indepth study/review.

(iii) points of interest raised by the participants.

(iv) important studies made by various professional institutions. .

(v) difficulties encountered by the field staff for taking remedial action.

18

1.31 Time schedule for work in Commercial Audit Headquarters Section

The following is the time schedule for issue of various Reports.

a)Inspection Reports and comments on

proforma accounts of Departmental

undertakings

One month from the date of audit

b)Comments on accounts of

Government Companies

Two months from the date of

receipt of adopted accounts

c)Separate Audit Reports As early as possible

i)AP State Financial Corporation 31st October

ii)AP State Road Transport Corporation As early as possible

iii)AP State Warehousing Corporation As early as possible after receipt

of the certified accounts

d)Report of the C&AG of India For obtaining the signature of the

CAG of India on the printed

Audit Reports. For presentation

to both the Houses of State

Legislature

Time Schedule right from the date of receipt of annual accounts till the despatch

of approved Audit Reports in respect of item (C) supra is detailed in respective

paras.

1.32 Pursuance and settlement of outstanding audit Objection

Objections from previous Reports shall be incorporated in the current Inspection

Reports to bring this to the notice of the authorities concerned to enable to have

outstanding items in one place for facilitating their effective pursuit by Audit.

However, pursuance of these objections has to be done on the basis of the

original Inspection Reports and their progress watched through the prescribed

register. Outstanding objections shall not be pursued merely on the basis of

extracts appearing in part 1B of subsequent reports. Occasions may arise when

an outstanding objection in a previous report is examined at the time of current

inspection and the original incorporated as a separate item in part-II of the

current report, as a result of the current inspection and discussions. In such cases

pointed attention of the departmental authorities shall be drawn to focus the

inadequacy of action taken in the past. In such cases, outstanding objection

appearing in the original Report may be treated as settled. Such a procedure

should arise only in exceptional cases.

The objections for more than a certain period of years may be dropped, after (i)

furnishing the departments concerned as well as the Finance

Ministry/Department with a list of such objections and obtaining certificate from

the department concerned to the effect that the amounts held under objections

19

constitute bonafide public expenditure and (ii) making a report of the fact to

Parliament/Legislature through the Audit Report.

In cases where the objections involve money value (as for example, recovery of

overpayments, want of financial sanction etc.) the objections have to be pursued

to a finality and shall not be dropped from Reports. Where, however, objections

have been raised on grounds of propriety, they can be dropped from the

Inspection Reports/objection books after these have been included in the Audit

Report for discussion in Public Accounts Committee/ Committee on Public

Undertakings and further action thereon watched through action taken notes and

Reports of Public Accounts Committee/ Committee on Public Undertakings

separately.

Objections on the works side relating to want of estimates, excess over estimates,

want of technical sanction, want of administrative approval, cases of

overpayments, defective agreements, losses of stores and stock shall not be

dropped unless action to regularize them is taken.

Objections relating to want of sanction, receipts and vouchers, detailed

contingent bills and want of reference to bills through which refunds or

repayments have been made also shall normally be pressed and action to settle

the same insisted upon particu1arly in case of want of contingent bills in case of

objection book advances. Regarding other items, while efforts shall be made to

settle the same, a certain amount of discretion can be used in audit where the

matter is so old or petty or where alternative proof is available regarding the

payments made to correct parties etc.

Objections relating to defective sanctions or misapplication of rules can be

reviewed by Audit sue moto and it would be open to Audit to withdraw these

objections and accept the expenditure as regular.

All other objections which are more than five years shall be reviewed by the

Accountant General and may be dropped wherever money is not due for

recovery or where misappropriations and frauds are not likely and wherever they

are technical. It is desirable for this purpose that the powers of waiver are

exercised freely in case of old objections.

If it is considered necessary for valid reasons to pursue an o1d outstanding

objection, the decision to do so shall be taken at the Group Officers level. The

objective should be to formally clear the items more than three years old where

debts due to and by Government are not involved and only minor technical

irregularities are brought out.

20

The half yearly statement of outstanding objections/Inspection Reports in respect

of Public Sector Undertakings which could be settled by the Departments only

shall be sent to the Administrative Ministries concerned.

1.33 Maintenance of objection books in respect of Autonomous bodies set

up under specific Acts of Parliament/State Legislature

In cases where the Accountant General acts as sole auditor for certifying the

accounts of organisations, it is necessary to ascertain various types of money

value of objections as part of the audit. Such objections can broadly fall under

the following categories viz.,

i) Want of stamped receipts or other proof of payment.

ii) Non-recovery of overpayments.

iii) Non-adjustment of advances given.

iv) Expenditure incurred without sanction or with inadequate sanction.

In respect of each of these categories it would be necessary to ensure that the

points of objections are settled before the accounts are certified as correct or if it

is not possible to so settle, to bring the matter to the notice of the organisations

and the Government wherever necessary, so that steps are taken to settle them. If

the objections so raised are of considerable magnitude and/or accumulating over

the years, with due regard to the merit and period of objections it would even be

necessary to incorporate them as a specific paragraph in the concerned separate

Audit Report. If, however, such items are not many and are normally settled in

due course it would be necessary to keep record of such objections a proper place

and in addition to convey the same to the organisations/ Government concerned

through the objection statements or Inspection Reports and watch compliance.

In respect of all cases of money value objections a note should also be kept in the

programme book at an appropriate place and compliance watched.

In addition, in respect of each institution under Audit, a Register of important

results of Audit may be kept, in which a continuous record of the major types of

irregularities noticed in audit is recorded. The entries are to be made in the

register in the form of an epitome of each case duly approved by the Supervising

Officer in charge of the inspection. This register may also be taken by the

inspection parties with them for scrutiny on the spot. No objection book need to

be maintained in respect of autonomous and statutory bodies set up under

specific Acts of Parliament/State legislature and Government Companies. The

objection book and adjustment register in the form M.S.O. (Tech) 127-B, as

amended, shall be maintained in respect of Departmental Commercial

Undertakings.

21

1.34 Calculation of Audit Fees

Audit fee is charged according to daily rates of audit fee worked out by this

office from time to time. The powers to sanction of daily rates of audit fees for

the recovery of cost of audit of non-Government funds are delegated to the

Heads of the Departments by CAG with effect from the revision of daily rates of

audit fee due on 1st September 1968 subject to the following conditions:

1) 'Direct charges' are calculated on the basis of average cost of the particular

post or posts involved, plus the appropriate allowances instead of pay and

allowances of the staff actually engaged on the work on a particular day.

2) ’Indirect charges' are taken as constituting 125% of the direct charges

calculated according to the above method.

3) The figure relating to number of days in a year which is to be adopted for

working out the daily rate would be determined by the Accountant General.

The audit fee is credited to the head of account "O65-A.Other Administrative

Services - C. Other Services. Fee for Government Audit (Central)". .

While calculating the amounts recoverable the instructions contained in the CAG

of India D.O.NO.3164/TA.I/96-64 dt.7th November 1964 shall be kept in view.

The audit fee is to be recovered only for personnel of the party on duty. No

recovery shall be made for a person on casual leave, holidays etc.

Audit fee is leviable for whole days even though only a part of the day may have

been devoted to the audit work.

If a Sunday or holiday is devoted to audit, no audit fee is leviable for that day

unless the Audit actually puts in a full day's work on such Sunday or holiday. It

does not, however, imply that the local officials can be compelled to attend to

Audit on any Sunday or holiday.

Recovery of cost of audit of bodies/authorities taken up under CAG's (Duties,

Powers and Conditions of Service) Act, 1971.

Rules laid down in Section VIII of Appendix-3 of Account Code Volume-I

regulating incidence of expenditure involved in audit conducted by IA &.AD

shall be followed in regard to audit of the accounts of the bodies and authorities

including corporations will be recoverable in all cases in which audit is

undertaken by CAG or any other officer under him as the sole auditor. In cases in

which the audit of the accounts of the body or authority is conducted by another

agency and audit by CAG or an officer under him represents second or

22

superimposed audit undertaken under Sections 14, 15 or 19 as the case may be,

erred from the body or the authority concerned. Audit under Section 20 is

required to be undertaken on such terms and conditions as may be agreed upon

between CAG and the concerned Government. One of the terms to be settled

relates to recovery of cost of audit. The recovery is therefore, to be regulated by

agreement that is arrived in each case. These cases are required to be referred to

the office of the CAG for finalisation of the terms and conditions under which

audit of the accounts of the body or authority concerned may be undertaken

including the question whether cost of audit should be recovered.

23

CHAPTER - 2

AUDIT PROCEDURE – GENERAL

2.1. Types of Audit

The Government Companies, Statutory Corporations and Departmental

Undertakings are subjected to three types of audit, viz., (i) audit of transactions

(ii) audit of Annual accounts and (iii) Performance Audit.

While audit of transactions and audit of Annual accounts is conducted every year

in the case of Statutory Corporations and Departmental Undertakings, the

procedure shall be as follows in respect of Government Companies:

Particulars Audit of

transactions

Audit of accounts

1)Fully owned Government

companies and subsidiary

Companies

Every year Every year (subject to fulfillment of

certain requirements) (details are

dealt with in para)

2)Section 619(B) Companies Every year Every year

Performance Audits are generally taken up on approval of the topic by the

Headquarters Office.

The audits are undertaken under the provisions or various Acts passed by

Parliament to ensure the correctness of the accounts prepared by the individual

organisations and to report to the State Legislature about the functioning of the

Companies/Corporations/Departmental Undertakings along with the analysis of

achievements and/or deficiencies.

Performance Audits are taken up to have an indepth study and a critical analysis

of various activities with reference to the scope of the objectives for which the

organisations were formed and to make a report to the State Legislature through

the Audit Report.

2.2 Audit of Accounts

2.2.1 Audit U/s 619(4) of the Companies Act, 1956

The accounts of the Government Company duly approved by the Board of

Directors and signed by the Directors authorized to do so and certified by

the Statutory Auditors are submitted to the Comptroller and Auditor General of

India for conducting the audit U/s 619(4) of the Companies Act, 1956.As per the

requirement of the Companies Act, 1956 all Government companies are required

24

to finalise their Accounts and lay them before Annual General Meeting of the

Company along with the

auditors’ Reports and CAG’s comments, if any , thereon. While

finalizing/certifying the accounts, the managements /statutory auditors of these

companies are required to keep in view the various requirements of the

Companies Act as well as the Accounting Standards issued by the Institute of

Chartered Accounts of India. The important and apparent requirements of the

Act and Accounting Standards are indicated below:

2.2.2 Statutory Requirement

1. The accounts not prepared in the format prescribed in the Schedule VI to the

Companies Act 1956.

2. The accounts not being signed by the requisite number of Directors as required

in the Act.

3. Balance Sheet abstract and company’s General Business Profile as required

under Part-IV of Schedule-VI of the Companies Act, 1956 is either not attached

or not signed by the Directors/Auditors.

4. Certain disclosure requirements of Schedule VI to the Companies Act not met

with.

5. Adoption of annual accounts in Annual General Meeting without CAG’s

comments under section 619(4) of the Companies Act.

6. Certification of accounts of subsequent year without adoption of accounts of

previous year.

7. Borrowing money in excess of the aggregate of the paid up capital of the

company and its free reserves without approval of shareholders in the general

meeting under Section 293(d).

2.2.3 Accounting Standard

The important Accounting Policies have not been indicated in the Accounts.

2.2.4 Auditors Report

1. The Statutory Auditors have submitted the report in casual manner or not

addressed to the members of the Company.

2. The Statutory Auditors have not complied with various requirements of

Statement of Auditing Practices-such as failure to point out non-compliance of

mandatory Accounting Standard.

3. Improper certification of accounts by Statutory Auditors.

4. Individual and total effect of all qualifications of profit or loss and or state of

affairs of Company is not mentioned in the auditors Report.

5. Compliance to Companies (Auditor’s Report) Order, 2003

25

2.2.5 General

1. The Management has submitted the unauthenticated accounts to AGs for audit.

2. There is totalling error on the fact of the Balance sheet and Profit & Loss

Account.

3. There is typing error in the accounts.

4. Notes to the accounts are in the nature of qualifications of the Statutory Auditors.

5. Notes to accounts are included under the Accounting Policies or vice versa.

6. Previous year’s figures are not updated upto the pervious years.

7. Preparation of annual accounts on the letter head of the Statutory Auditors.

Such types of errors can be avoided by interaction with the

management/statutory auditors before finalization/certification of accounts.

Meetings in this regard may be arranged in the first week of April with the

Company management at the level of Chairman &Managing director/Chief

Finance Executive and the Statutory Auditors and the management as well as

Statutory Auditors may be advised to comply the various requirements of the

Companies Act/Accounting Standards while finalizing/certifying the accounts

and to ensure the assurances given by the managements/statutory auditors to

rectify the mistakes etc at the time of finalization of comments of earlier period

are fulfilled by them. They may also be impressed upon not to submit the

unauthenticated accounts for audit. (Lr.No.284-CA-II/398-99KW dt:12-2-03.)

Periodic meetings may also be taken with the management and statutory auditors

to impress upon them the timely finalization of the accounts as per the provisions

of the Companies Act,1956. Detailed time schedule from the starting of audit by

the statutory auditors till handing over of the signed copy of accounts to the

Accountant General for supplementary audit may be drawn-up in consultation

with the statutory auditors and the management. The time schedule may be

monitored through constant interaction with the statutory auditors and the

management. (DCA’sLr.No.11/A/Rep/28-1/59-60/1379 dt.19.02.1960 in

F.No.82/56/Vol.II). (Lr.No.284-CA-II/398-99KW dated:12-3-03).

On receipt of the authenticated accounts in duplicate along with the Statutory

Auditor's Report and certified copy of the Board Minutes approving the

accounts, it is necessary to ensure that auditors of the company have been

appointed by the Comptroller and Auditor General of India and that the audit

Report has been submitted by such auditor.

Cases involving Litigation/Dispute between the firms of Chartered Accountants

and Public Sector Undertakings:

A case has come to Headquarters notice where a firm of Chartered Accountants

appointed as Statutory Auditors of a Public Sector undertaking under Section

619(2) of Companies Act, had filed a Court

case against that undertaking. Such a situation has obvious implications. If

26

during the course of audit of Public Sector undertakings under our audit control,

any such cases of litigation or dispute between firms of Chartered Accountants

and any of the Public Undertakings and if any case of unbecoming conduct on

the part of firm of auditors come to notice, these may be communicated to

Headquarters office with complete details for information. (Circular No.1 No.

134-CA-V/AO/8-72/Vol.II/KW dt.7. 1. 1984).

2.3 Audit Checks

The following shall be kept in mind during the course of audit under Section

619(4) of the Companies Act, 1956.

Where it is not possible to complete the test audit under Section 619(3)(b) of the

Act, the Report examined generally and comments made on the content or scope

of the Company’s Auditors report or any matters on which we may seriously

differ from the Company Auditor's report, but in our opinion require greater

emphasis.(CAG'S Office . Lr.No.528-Rep/86-57 dt.10.4.1957 in F.No.82/56

Vol.I).

It should be noted that the comments of the Comptroller and Auditor General of

India (as a superimposed auditor) under Section 619(4) of the Companies Act,

1956 should extend beyond the scope of the Statutory Auditors' work and the

review shall not be confined merely to an assessment of the efficiency of the

audit. The issue of a ‘no-remarks’ certificate on the basis of the Statutory

Auditors work within the limited sphere of their duties will give a misleading

impression to the shareholders who should also be made aware of important

objections having substantial financial significance which had been raised with

the Management but not satisfactorily answered before the General Body

Meeting.

It is for the Statutory Auditors to satisfy themselves that the Balance Sheet and

Profit and Loss Account have been approved by the Board of Directors before

they are signed on behalf of the Board in accordance with the provisions of

Section 215(3) of the Act before they are submitted to them for their report

thereon; before their taking up the audit work. The matter should not ordinarily

form part of our comments under Section 619(4) of the Act. If, however, there is

concrete evidence that the procedure adopted is not correct, Audit shall bring it

to the notice of the Company and the Statutory Auditors and comment on it only

after both have refused to act in the manner prescribed. (Lr.No.15/ 56/CL.VI

dt.14.9.1961 of CLB and No.HA/20/18/62/265 dt.15.5.1963 of F.No.IV- 38/60-

61 Vol..I.P.215/c).

The power to approve the accounts as originally prepared or modified

subsequently cannot be delegated by the Board of Directors to a Committee of

Directors. Approval of annual accounts by circulation is permissible. (Authority:

27

D.O.No.965-CA.IV/84-78 from CAG's office addressed to MAB Ex-Officio

DCA, Hyderabad F.No.Circular file Vol.III).

It shall be ensured that Government Companies make appointment of branch

auditors in terms of Section 228 of the Companies Act, 1956 only in respect of

those branches which are not audited by auditors appointed either under the

directives issued by the CAG of India or under the orders of the Central

Government appointing auditors of the Company on the advice of the CAG of

India.

While scrutinising the accounts, it shall be ensured by the audit party that either

the horizontal form or the vertical from of Balance Sheet as given in Part I of

Schedule VI to the Companies Act, 1956 and requirements as to Profit and Loss

Account as enunciated in Part II of Schedule VI to the Companies Act, 1956 are

scrupulously adhered to. The interpretations contained in Part III of Schedule VI

to the Companies Act, 1956 shall also be kept in mind. (No.3.CA/243-64

dt.5.l.1965 P.577 of F.No.82/56/55-56 Vol.II).

Audit of a Government Company ceased to be such during the course of a year

should also be conducted under Section 619(3)&(4) of the Companies Act, 1956.

(343/CA.II/205-69/25.3.80 IV-46/68-69 of Associated Glass Ind. Ltd.)

2.4 Watch on receipt of accounts

A close watch shall be kept on the timely receipt of the authenticated accounts

together with their report thereon by the Statutory Auditors and in case of delays

in the receipt, the matter shall be taken up with the auditors as soon as the

accounts are received (Hqrs. office D.O. No.80/CA.II/l02-79 circular

No.3/CAW/II/State Commercial Audlt-II/80, dt.30.06.1980 P.84/c. of

F.No.IV.17/72-073/Vol.V)

The AG's should complete the supplementary audit and finalise the comments

under section 619(4) of the Companies Act, 1956, within two months of the

receipt of the certified accounts from the Statutory Auditors of the concerned

Government Company. In the context of the overall time limit of six months