Computer FraudPertemuan XVIII

Matakuliah : F0184/Audit atas KecuranganTahun : 2007

Bina Nusantara

• Mahasiswa diharapkan dapat mengidentifikasi metode-metode kecurangan berbasis komputer

• Mahasiswa diharapkan mampu mengetahui pengendalian yang diperlukan untuk mengatasi kecurangan berbasis komputer

Learning Outcomes

3

Bina Nusantara

• Computer fraud category • Computer Fraud Theory• Nature of Computer Fraud• Type of Computer Fraud• Internal Control for Computer Fraud

Outline Materi

4

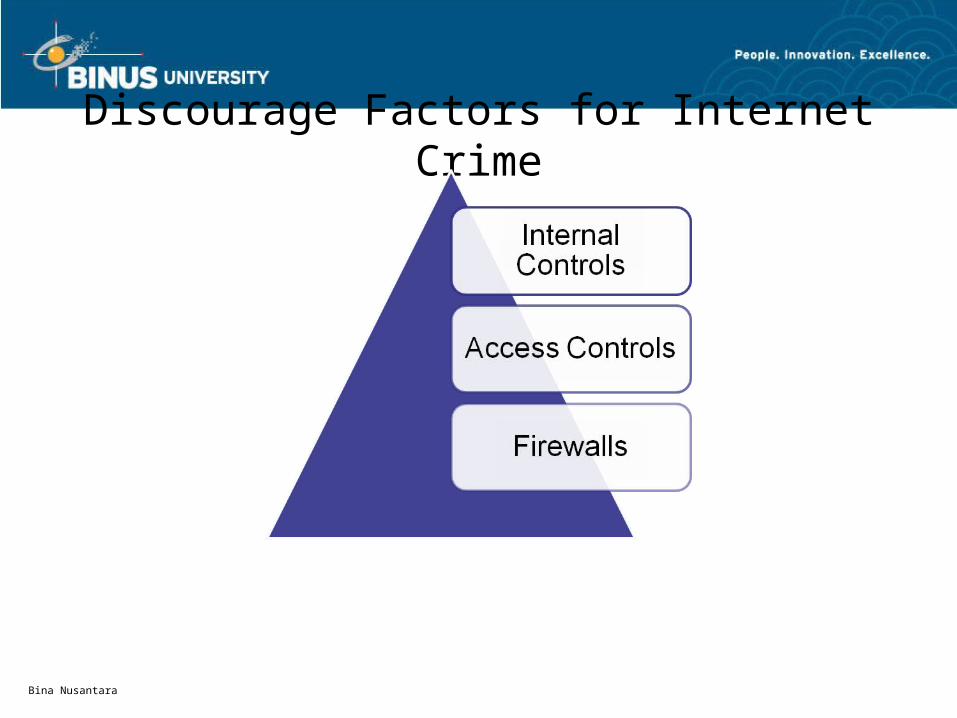

Potential Issues• Most prevention efforts focus on building more

accounting, access, or physical security controls• It is vital to recognize that there are limits to

technological and procedural controls• Some factors in the business environment are

likely to encourage computer crime and other discourage it

Bina Nusantara

Discourage Factors for Internet Crime

Bina Nusantara

Internal Controls• Separation and rotation of duties• Periodic audit• Absolute insistence that control policies and

procedures be documented in writing• Dual signatures authorities, monetary authorization

limit, expired date for signatures, and check amount limit

• Offline controls and limits• Feedback mechanism

Bina Nusantara

Access Controls• Authentication and identification controls• Compartmentalization• Encryption

Bina Nusantara

Measures to Detect Attempt• A system of logging and follow up exceptions should

be designed and implemented to log unusual activities• Logging and following up on variances should be able

to indicate a problem may have occurred or is occurring

• General logging should be in place• Awareness of employee attitudes and satisfaction

levels should be developed and maintained• Sensitivity should be developed and maintained to

reports that particular individuals are having problems• Newly developed intrusion detection systems should

be used

Bina Nusantara

IT Controls based on COSO

Bina Nusantara

General Controls

Bina Nusantara

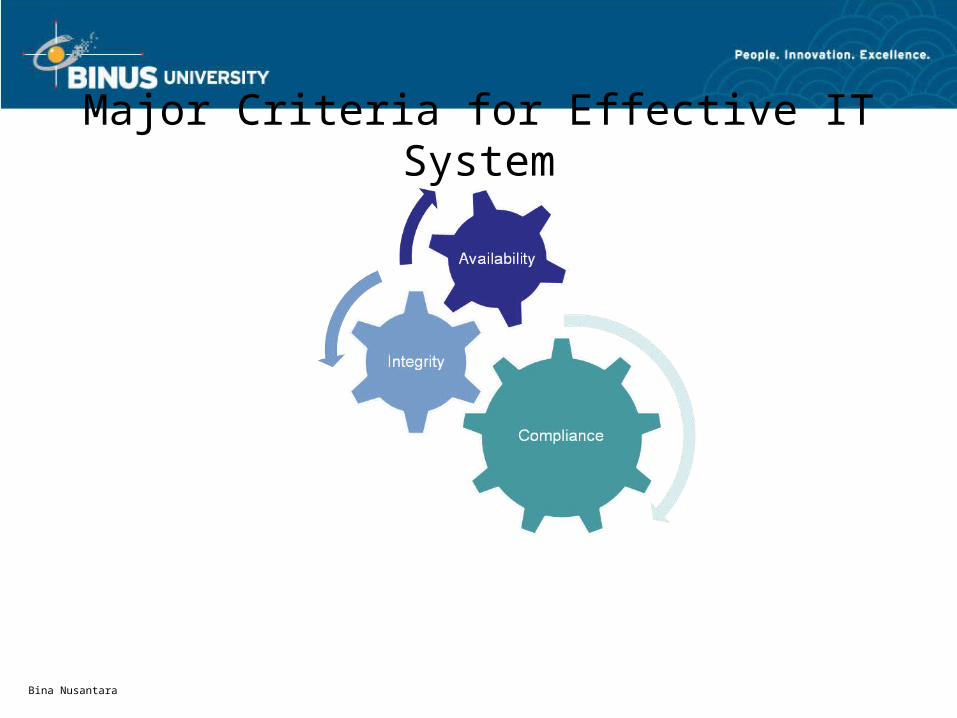

Major Criteria for Effective IT System

Bina Nusantara

Sub Criteria for Effective IT System

Bina Nusantara

Recommended