Please see important disclosures at the end of this report

Global Thematic Research September 18, 2018

Considering ESG Factors in Fixed Income Investing A guide for asset owners

Much has been written about the strategies, theoretical and practical, that can be employed by asset managers to integrate Environmental, Social and Governance (ESG) factors into fixed income portfolios. Less has been written about the challenges facing asset owners—including individuals and families, foundations and endowments—as they try to incorporate an ESG perspective into the fixed income allocation of their portfolios.

Cornerstone Capital’s tactical allocation for a typical portfolio includes an allocation to fixed income in the range of 20-40% depending on market conditions. In that context, this report is intended to provide a guide to sustainable fixed income vehicles that are currently available to asset owners.

“Fixed income” is a term generally used to refer to debt instruments that provide a return on investment in the form of fixed periodic payments, and the repayment of the original investment at the end of a defined time period. The focus of this report is on fixed income instruments backed both by public (e.g., governments and municipalities, supranational development finance institutions) and private (e.g., corporate, NGOs) issuers that are associated with flows of capital to various sustainable activities.

In many respects, integration of ESG into fixed income is less mature than it is in equities. However, given that fixed income investors take the perspective of managing risk more than opportunity—in contrast to equity investors—fixed income ESG analysis likely has a greater role to play in the investment process than is widely perceived. There are a growing number of opportunities for asset owners to invest in fixed income vehicles and securities that provide funding for impactful projects or sustainable companies, and that also offer competitive yields.

Michael Geraghty Strategist Craig Metrick, CAIA Head of Institutional Consulting Jennifer Leonard, CFA Asset Manager Due Diligence

2

Table of Contents

Table of Contents .............................................................................................................................................. 2

Motivations of Fixed Income ESG Investors ..................................................................................................... 3

Fixed Income Versus Equity Investing: Key Differences for Asset Owners in Considering ESG ...................... 4

Sustainable Fixed Income Issuers ..................................................................................................................... 5

Sustainable Bonds ............................................................................................................................................. 6

Global Green Bonds and U.S. Muni Green Bonds ........................................................................................................................... 7

Social Bonds .................................................................................................................................................................................... 9

Sustainability Bonds ..................................................................................................................................................................... 10

Social Impact Bonds ...................................................................................................................................................................... 10

Corporate Bonds Meeting ESG Criteria ......................................................................................................................................... 10

Sustainable Fixed Income Investment Vehicles .............................................................................................. 11

Sustainable Bond Funds ................................................................................................................................................................ 11

Fixed Income Notes....................................................................................................................................................................... 12

Private Debt Funds ....................................................................................................................................................................... 13

Community Development Financial Institutions (CDFIs) ............................................................................................................... 13

Conclusion ....................................................................................................................................................... 14

3

Motivations of Fixed Income ESG Investors There are a number of factors that may lead investors to incorporate an ESG perspective into the fixed income allocation of their portfolios. Three of the most common are values alignment; investing for a quantifiable impact; and achieving risk-adjusted returns. These factors are, of course, not mutually exclusive.

Values alignment. Investors can align their investments with their values by incorporating ESG factors into their fixed income investment decisions. The motivations might be ethical, religious or other norms and standards, e.g., a focus on human rights, labor conditions, or corruption. One way that values alignment can be accomplished is to apply screens, whether “negative” or “positive.” So, for example, an investor may apply negative screens to exclude certain investments from their portfolio – for instance, bonds issued by companies that produce tobacco, firearms or alcohol, or that operate private prisons. Alternatively, an investor might screen for corporate issuers that meet certain positive ESG criteria, such as good relations with unions.

Investing for a quantifiable impact. Impact investing has a dual goal: to generate a financial return (ranging from market-rate to concessionary), and to achieve a positive social and/or environmental impact that can be measured. For example, investors who support private debt financing for the construction of a solar power facility can measure the impact of the project through the amount of energy generated and the reduction in emissions achieved by replacing diesel generators. Investments can also be made in funds or through notes that finance microfinance institutions, which make loans to individuals, cooperatives, and small businesses in emerging and frontier markets.

Enhancing risk-adjusted returns. There is academic evidence that companies with better ESG characteristics have lower borrowing costs.1 So, fixed income investors can utilize ESG analysis not only to maximize social or environmental impact, but also to maximize risk-adjusted return and minimize downside exposure. For example, an investor might compare two bonds with similar characteristics issued by two different energy companies and determine that the issuer with stronger governance practices and a superior environmental track record is the better investment.

Multiple goals can often be attained via a single fixed income instrument. For example, a green bond issued by a supranational institution may exhibit characteristics of values alignment, quantifiable impact, and risk-adjusted returns.

1 https://www.sciencedirect.com/science/article/pii/S037842661300407X

Multiple goals can often be attained via a single fixed income instrument

4

Fixed Income Versus Equity Investing: Key Differences for Asset Owners in Considering ESG From an asset owner’s perspective, there are several key differences between fixed income and equity ESG investments:

A relatively small market. The dollar value of sustainable bonds — green, social, and sustainability bonds — outstanding at the end of 2017 was $385 billion2. By way of comparison, Apple’s equity market capitalization recently reached $1 trillion.

Relatively small issuances. According to the Climate Bonds Initiative3, most green bond issuances fall into the $10 - $100 million bracket. In addition, there are still only a limited number of issuers of sustainable bonds of all types.

Relatively few fixed income ESG managers. Not surprisingly, there are relatively few fixed income managers focused on ESG, in comparison to a significant number of ESG equity managers. An MSCI analysis4 of more than 89,000 funds indicated that ESG equity funds outnumber ESG bond funds by three-to-one globally, a disparity that rises above four-to-one in the United States.

Fewer opportunities for corporate engagement. The purchase of an equity conveys ownership in a firm whereas fixed income issuances are debt obligations. As lenders of capital, bondholders generally have fewer opportunities than shareholders to materially engage with companies — two of the most important rights of shareholders are voting and speaking at annual shareholder meetings. Bondholders’ interaction with issuers has traditionally been restricted to attending bond roadshows and influencing and enforcing terms of bond covenants. However, some ESG investors have been engaging with issuers. For example, there have been efforts to integrate ESG performance into the covenants of issues, as well as longer-term efforts to address sustainability matters with issuers.

2 This does not include values-alignment bonds discussed in the previous section. 3 https://www.climatebonds.net/resources/reports/bonds-and-climate-change-state-market-2017 4 2018 ESG Trends to Watch, MSCI ESG Research, January 2018

There have been efforts to integrate ESG performance into the covenants of bond issues, as well as longer-term efforts to address sustainability matters with issuers

5

Sustainable Fixed Income Issuers Sustainable bond issues were once dominated by supranational development banks, but other organizations have since emerged as significant issuers. Currently, major issuers of sustainable fixed income instruments fall into six categories, four of which are public: supranational development finance institutions; sovereign countries; governments and municipalities; agencies. The two other major categories are corporations and issuers of asset-backed securities.

Supranational development finance issuers. Supranational development finance institutions — such as the World Bank, International Bank for Reconstruction and Development, International Finance Corporation, Asian Development Bank, European Investment Bank, and European Bank for Reconstruction and Development — regularly issue bonds to finance development–related initiatives. Bonds issued have funded a variety of projects, including solar and wind installation, as well as the construction of energy-efficient buildings.

Sovereign issuers. Poland became the first country to issue a green sovereign bond, with a €750 million bond financing a range of climate-related projects including renewable energy generation and clean transportation. Poland generates more than 80% of its electricity from coal, highlighting that even fossil fuel-reliant countries are looking to alternative energy sources.

Government and municipal issuers. Local governments issue municipal bonds to fund projects for the public good. While not all municipal bonds generate positive social and environmental impact — e.g., bonds to finance prison construction or coal-burning power plants — some municipal bonds are associated with sustainable activities, e.g., to finance clean water infrastructure. Moreover, even after it was announced that the U.S. would withdraw from the Paris Climate Accord, state and local level climate change plans have remained ambitious, further supporting green bond issuance by municipalities.

Issuers of agency securities. Affordable housing mortgages from Fannie Mae and Freddie Mac are considered impact bonds by some asset owners.

Corporate issuers. A growing number of corporations are issuing “green bonds.” These are fixed income instruments whose proceeds are used exclusively to finance “green projects,” defined as any initiative that promotes progress on environmentally sustainable activities, such as renewable energy. Green bonds are a good way for almost any corporation to raise capital for environmental or energy-efficiency projects. For example, in February 2016 Apple issued a $1.5 billion green bond to finance renewable energy, energy storage, and energy efficiency projects throughout its global operations. According to Apple’s vice president of environment, policy and social initiatives, the issuance “will allow investors to show they will put their money where their hearts and concerns are.”

Even after the U.S. withdrawal from the Paris Climate Accord, state and local level climate change plans have remained ambitious, further supporting green bond issuance by municipalities

6

Issuers of asset-backed securities. Securities backed by assets such as car loans for Tesla vehicles and hybrid autos are considered sustainable by some asset owners. There are also for-profit firms and nonprofit organizations that issue debt (often in structured note form) to support renewable energy projects, other green infrastructure projects, and community development and housing.

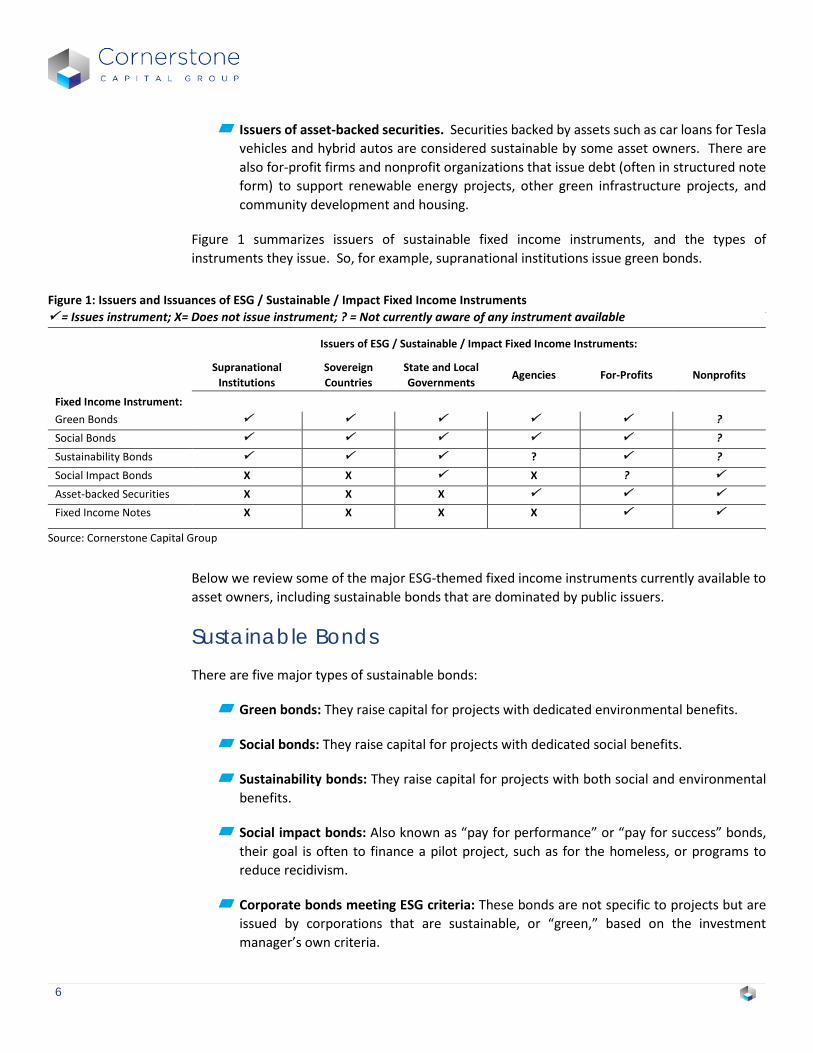

Figure 1 summarizes issuers of sustainable fixed income instruments, and the types of instruments they issue. So, for example, supranational institutions issue green bonds.

Figure 1: Issuers and Issuances of ESG / Sustainable / Impact Fixed Income Instruments = Issues instrument; X= Does not issue instrument; ? = Not currently aware of any instrument available

Issuers of ESG / Sustainable / Impact Fixed Income Instruments:

Supranational Institutions

Sovereign Countries

State and Local Governments

Agencies For-Profits Nonprofits

Fixed Income Instrument:

Green Bonds ? Social Bonds ? Sustainability Bonds ? ? Social Impact Bonds X X X ? Asset-backed Securities X X X Fixed Income Notes X X X X

Source: Cornerstone Capital Group

Below we review some of the major ESG-themed fixed income instruments currently available to asset owners, including sustainable bonds that are dominated by public issuers.

Sustainable Bonds There are five major types of sustainable bonds:

Green bonds: They raise capital for projects with dedicated environmental benefits.

Social bonds: They raise capital for projects with dedicated social benefits.

Sustainability bonds: They raise capital for projects with both social and environmental benefits.

Social impact bonds: Also known as “pay for performance” or “pay for success” bonds, their goal is often to finance a pilot project, such as for the homeless, or programs to reduce recidivism.

Corporate bonds meeting ESG criteria: These bonds are not specific to projects but are issued by corporations that are sustainable, or “green,” based on the investment manager’s own criteria.

7

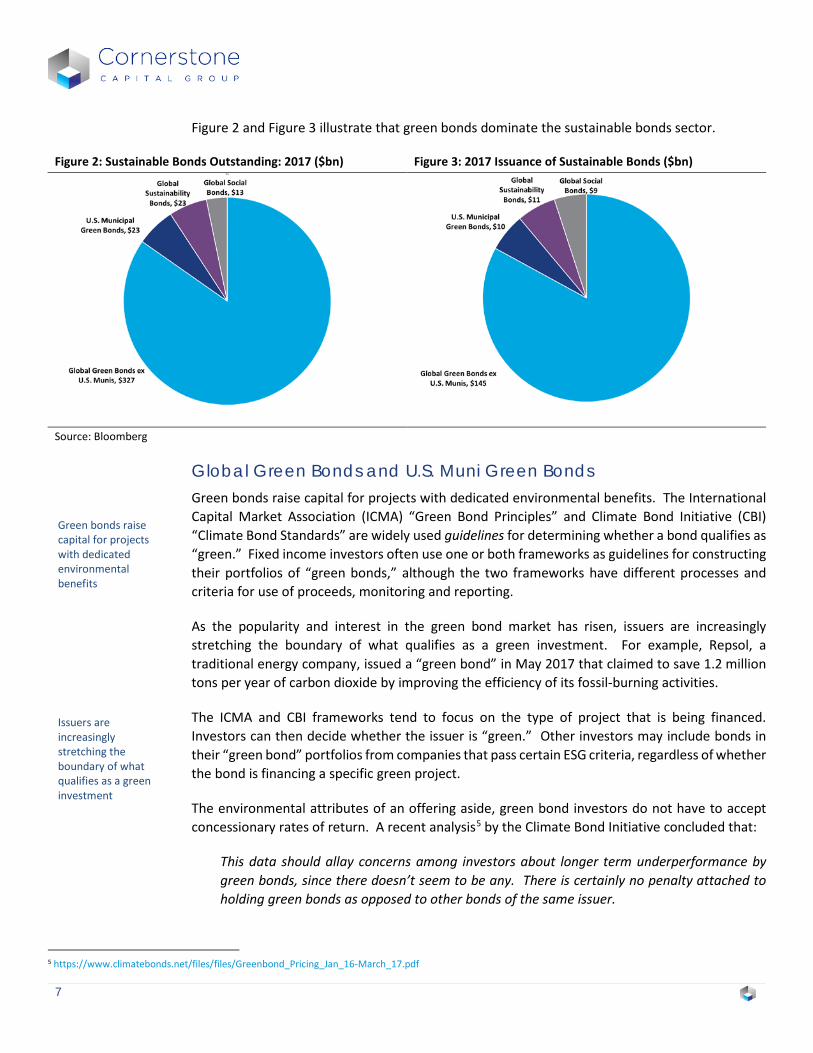

Figure 2 and Figure 3 illustrate that green bonds dominate the sustainable bonds sector.

Figure 2: Sustainable Bonds Outstanding: 2017 ($bn) Figure 3: 2017 Issuance of Sustainable Bonds ($bn) Ta

Source: Bloomberg

Global Green Bonds and U.S. Muni Green Bonds Green bonds raise capital for projects with dedicated environmental benefits. The International Capital Market Association (ICMA) “Green Bond Principles” and Climate Bond Initiative (CBI) “Climate Bond Standards” are widely used guidelines for determining whether a bond qualifies as “green.” Fixed income investors often use one or both frameworks as guidelines for constructing their portfolios of “green bonds,” although the two frameworks have different processes and criteria for use of proceeds, monitoring and reporting.

As the popularity and interest in the green bond market has risen, issuers are increasingly stretching the boundary of what qualifies as a green investment. For example, Repsol, a traditional energy company, issued a “green bond” in May 2017 that claimed to save 1.2 million tons per year of carbon dioxide by improving the efficiency of its fossil-burning activities.

The ICMA and CBI frameworks tend to focus on the type of project that is being financed. Investors can then decide whether the issuer is “green.” Other investors may include bonds in their “green bond” portfolios from companies that pass certain ESG criteria, regardless of whether the bond is financing a specific green project.

The environmental attributes of an offering aside, green bond investors do not have to accept concessionary rates of return. A recent analysis5 by the Climate Bond Initiative concluded that:

This data should allay concerns among investors about longer term underperformance by green bonds, since there doesn’t seem to be any. There is certainly no penalty attached to holding green bonds as opposed to other bonds of the same issuer.

5 https://www.climatebonds.net/files/files/Greenbond_Pricing_Jan_16-March_17.pdf

Green bonds raise capital for projects with dedicated environmental benefits

Issuers are increasingly stretching the boundary of what qualifies as a green investment

8

In other words, most green bonds trade no differently than non-green bonds by the same issuer. (The study looked at 31 dollar-denominated and 31 euro-denominated green bonds issued over a 15-month period between 2016 and 2017.)

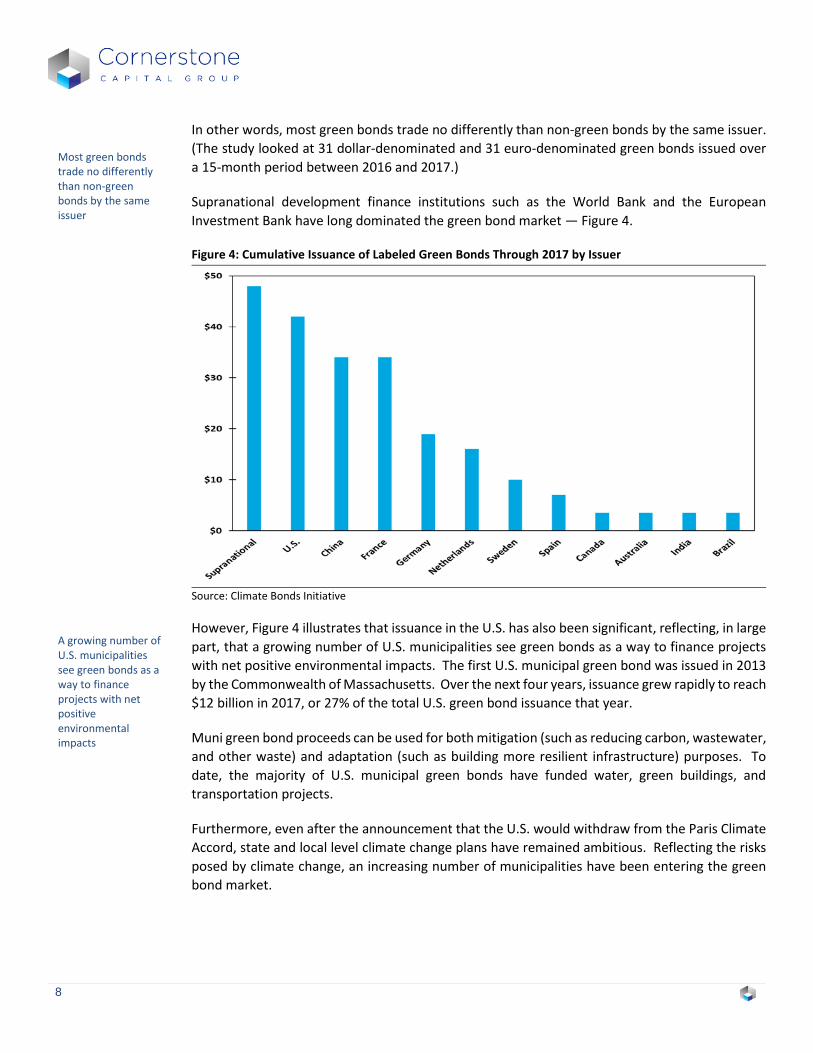

Supranational development finance institutions such as the World Bank and the European Investment Bank have long dominated the green bond market — Figure 4.

Figure 4: Cumulative Issuance of Labeled Green Bonds Through 2017 by Issuer

Source: Climate Bonds Initiative

However, Figure 4 illustrates that issuance in the U.S. has also been significant, reflecting, in large part, that a growing number of U.S. municipalities see green bonds as a way to finance projects with net positive environmental impacts. The first U.S. municipal green bond was issued in 2013 by the Commonwealth of Massachusetts. Over the next four years, issuance grew rapidly to reach $12 billion in 2017, or 27% of the total U.S. green bond issuance that year.

Muni green bond proceeds can be used for both mitigation (such as reducing carbon, wastewater, and other waste) and adaptation (such as building more resilient infrastructure) purposes. To date, the majority of U.S. municipal green bonds have funded water, green buildings, and transportation projects.

Furthermore, even after the announcement that the U.S. would withdraw from the Paris Climate Accord, state and local level climate change plans have remained ambitious. Reflecting the risks posed by climate change, an increasing number of municipalities have been entering the green bond market.

Most green bonds trade no differently than non-green bonds by the same issuer

A growing number of U.S. municipalities see green bonds as a way to finance projects with net positive environmental impacts

9

Social Bonds Social Bonds are very similar in concept to green bonds, differing only in terms of their use of proceeds: They raise capital for projects that seek to achieve positive social outcomes for underserved communities. Potential projects include:

Affordable basic infrastructure such as water, sanitation, transport.

Basic services such as health and education.

Access to finance.

Access to affordable housing.

As an example, Spain’s Instituto de Credito, a state-owned bank, issued the first formal social bond offering in January 2015. The purpose of the transaction was to help finance small and medium-sized enterprises (SME) in economically depressed regions of Spain. The bond offering supported loans at favorable rates and terms to SMEs; companies deemed to be unsustainable from a socially responsible perspective were excluded.

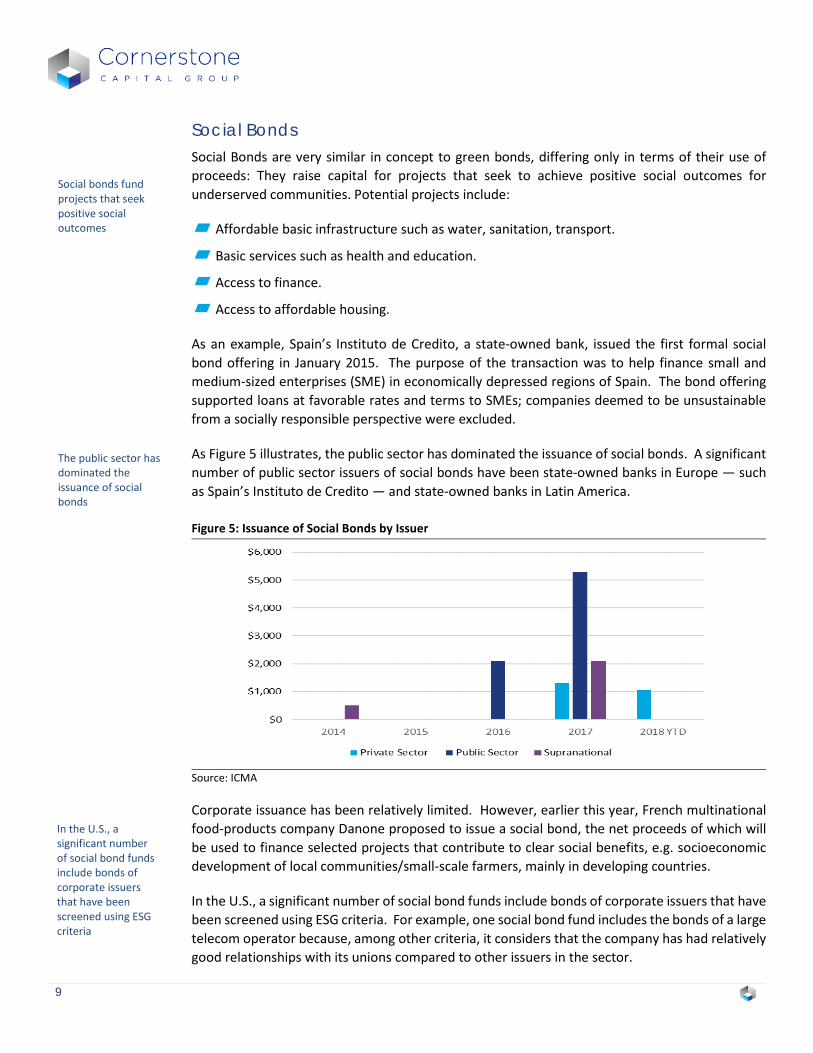

As Figure 5 illustrates, the public sector has dominated the issuance of social bonds. A significant number of public sector issuers of social bonds have been state-owned banks in Europe — such as Spain’s Instituto de Credito — and state-owned banks in Latin America.

Figure 5: Issuance of Social Bonds by Issuer

Source: ICMA

Corporate issuance has been relatively limited. However, earlier this year, French multinational food-products company Danone proposed to issue a social bond, the net proceeds of which will be used to finance selected projects that contribute to clear social benefits, e.g. socioeconomic development of local communities/small-scale farmers, mainly in developing countries.

In the U.S., a significant number of social bond funds include bonds of corporate issuers that have been screened using ESG criteria. For example, one social bond fund includes the bonds of a large telecom operator because, among other criteria, it considers that the company has had relatively good relationships with its unions compared to other issuers in the sector.

Social bonds fund projects that seek positive social outcomes

The public sector has dominated the issuance of social bonds

In the U.S., a significant number of social bond funds include bonds of corporate issuers that have been screened using ESG criteria

10

Sustainability Bonds Sustainability bonds raise capital for projects with a mix of social and environmental benefits. Previous issuances by the public sector have included energy-efficient buildings for disadvantaged people, and clean energy public transport that includes bicycle lanes.

While the public sectors in Europe and South America have been the primary issuers, sustainability bonds also offer corporations a way to signal their core values. Starbucks issued the first-ever U.S. corporate sustainability bond in 2016. Proceeds from the $500 million bond were dedicated to sourcing coffee that meets the company’s standards for coffee certified against the Coffee and Farmer Equity (C.A.F.E.) practices, a third-party verified set of standards that Starbucks developed in 2004 to measure environmental and social practices of its suppliers.

In addition, Starbucks set aside funding for loans to coffee farmers, in an acknowledgement that many coffee farmers lack access to traditional financial products needed to help them fund their businesses.

Social Impact Bonds These bonds are not investable for most investors and they are still rare, but interest is growing rapidly. Also known as “pay for performance” or “pay for success” bonds, these are highly structured arrangements, typically between foundations, other institutional investors and a government agency. The goal of these bonds is often to finance a pilot project, such as services for homelessness, or programs to reduce recidivism.

Investors finance the implementation of the project, results are tracked, and investors get paid a certain rate if the program meets goals that are defined in advance. One example of a social impact bond in Denver, still ongoing, is available here6.

Corporate Bonds Meeting ESG Criteria This type of bond selection is similar to the way ESG criteria can be used to select publicly traded stocks for investing. These bonds may be referred to as “sustainable,” “green,” or “socially responsible,” but the proceeds for the issuance are not tied to any specific project.

Investment managers can use proprietary sets of criteria, usually supported by third-party data sources, to determine whether a company’s debt is suitable for a “sustainability-branded” portfolio. Often the criteria are a combination of negative and positive screens, which will result in certain business exclusions (tobacco, weapons), and the inclusion of companies that exhibit better ESG policies, practices and performance.

Using these types of securities in a bond portfolio allows the portfolio to exhibit characteristics more typical of corporate bond portfolios, or the corporate portion of core bond portfolios, which usually include government and corporate securities.

6 http://www.payforsuccess.org/project/denver-housing-health-initiative

Starbucks issued the first-ever U.S. corporate sustainability bond in 2016

Investment managers can use proprietary sets of criteria to determine whether a company’s debt is suitable for a “sustainability-branded” portfolio

11

Sustainable Fixed Income Investment Vehicles In the sections above, we reviewed some of the major ESG-themed fixed income instruments. We now turn to vehicles through which asset owners can gain access to the various instruments:

Sustainable bond funds: These are fixed income funds managed by investment professionals that allow investors to gain exposure to a range of sustainable instruments including green and social bonds.

Fixed income notes: These are investments directly into a note structure specified for a defined period of time, usually with a fixed rate of return.

Private debt funds: These are “evergreen” funds (i.e., perpetually open to new subscriptions) that typically have some sort of “lock-up” or notice period prior to the withdrawal of capital.

Community Development Financial Institutions (CDFIs): Asset owners can support job creation and affordable housing in local communities by investing in deposits at private, community-oriented financial institutions.

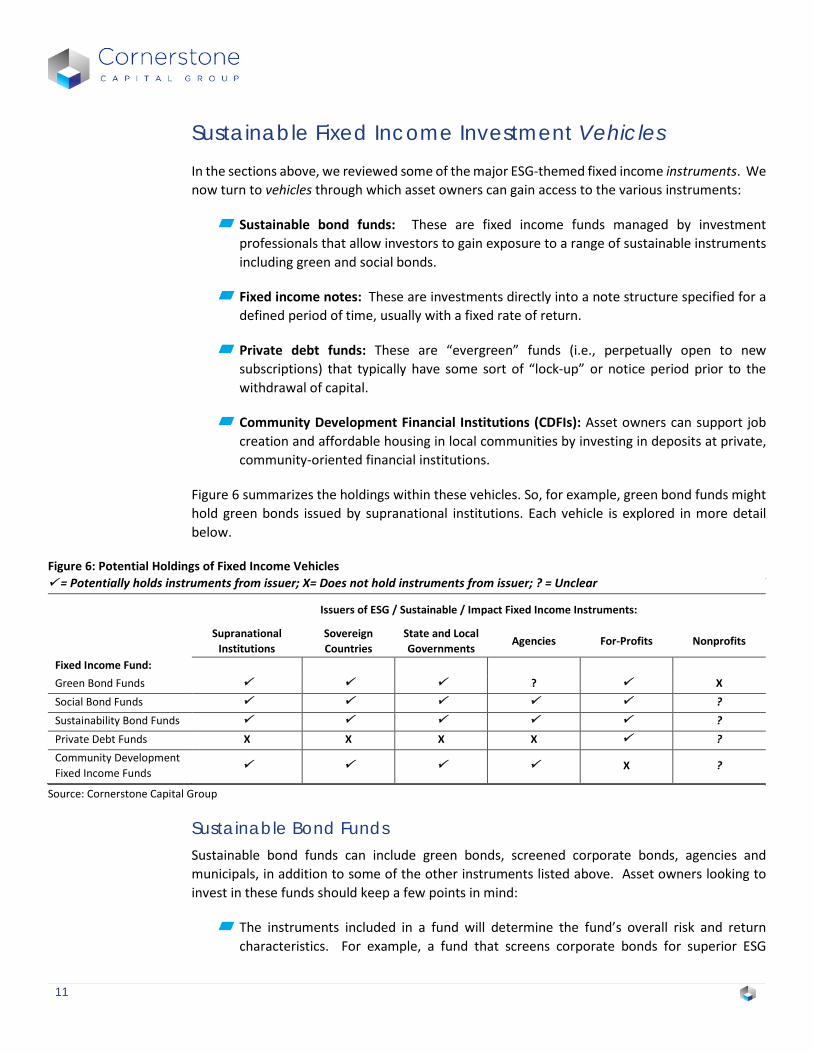

Figure 6 summarizes the holdings within these vehicles. So, for example, green bond funds might hold green bonds issued by supranational institutions. Each vehicle is explored in more detail below.

Figure 6: Potential Holdings of Fixed Income Vehicles = Potentially holds instruments from issuer; X= Does not hold instruments from issuer; ? = Unclear

Issuers of ESG / Sustainable / Impact Fixed Income Instruments:

Supranational Institutions

Sovereign Countries

State and Local Governments

Agencies For-Profits Nonprofits

Fixed Income Fund: Green Bond Funds ? X Social Bond Funds ? Sustainability Bond Funds ? Private Debt Funds X X X X ? Community Development Fixed Income Funds

X ?

Source: Cornerstone Capital Group

Sustainable Bond Funds Sustainable bond funds can include green bonds, screened corporate bonds, agencies and municipals, in addition to some of the other instruments listed above. Asset owners looking to invest in these funds should keep a few points in mind:

The instruments included in a fund will determine the fund’s overall risk and return characteristics. For example, a fund that screens corporate bonds for superior ESG

12

performance should, in theory, have a lower risk profile than a fund that doesn’t perform such a screen (and that contains corporate bonds of similar quality and duration). By way of example, one way the risk profile of a fund could be reduced is if the bonds of energy companies are screened for those at risk of major oil spills.

While a bond fund may offer a higher potential return than another sustainable fixed income vehicle, such as a private debt fund, an asset owner may be willing to accept the concessionary return of a private debt fund in return for the quantified impact of their investment.

Asset owners investing in a bond fund need to “do their homework” to understand the true characteristics of the fund. As noted above, Repsol, a traditional energy company, issued a “green bond” in May 2017 that claimed to save 1.2 million tons a year of carbon dioxide by improving the efficiency of its fossil-burning activities. Some asset owners may question the decision of an asset manager to include a so-called “green bond” in the holdings of a self-proclaimed green bond fund.

Fixed Income Notes In the parlance of the fixed income market, “bonds” have maturities of more than 10 years, while “notes” have maturities of between one and ten years. Fixed income note investments are structured for a defined time frame, usually with a fixed rate of expected return; there may also be structured notes where the rate of return floats relative to a benchmark, e.g. LIBOR. In the ESG or impact space, notes typically represent a pool of loans to social enterprises, for-profits or nonprofits, offered at maturities and rates of return that resemble Certificates of Deposit (CDs).

By way of example, asset owners can invest in fixed income notes that fund:

Loans to a variety of social enterprises, for-profits and nonprofits that are dedicated to social and environmental impact. Themed notes are sometimes available (e.g. Gender Equity).

Loans to smallholder farmers in Africa and Latin America.

Microfinance, which supports lending to rural areas and small SMEs in emerging and frontier markets.

Renewable energy or energy efficiency projects.

Reflecting the mission-driven focus of many of the organizations that issue such notes (some of them being not-for-profit), these notes can have CD-like characteristics. Some offer multiple-year terms and returns of 1-3% depending on the term. However, there are also higher-returning notes supporting these same types of impacts.

Asset owners investing in a bond fund need to “do their homework” to understand the true characteristics of the fund

In the impact space, notes typically represent a pool of loans to social enterprises, for-profits or nonprofits, offered at maturities and rates of return that resemble Certificates of Deposit

13

Private Debt Funds Similarly, there are a variety of private debt funds that finance a wide range of ESG-oriented activities. These are often considered to be “market-rate” investments although, depending on the fund and the sector it is invested in, returns and risks may be higher or lower than some mainstream (i.e., non ESG-oriented) private debt funds.

Generally, these funds operate similarly to private equity funds, with a management fee plus a performance fee when, or if, the fund reaches a certain threshold of return. These are illiquid strategies, with investor assets sometimes being “locked up” for a few years. Some examples of private debt funds include:

Funds that invest in certain pools of loans on online lending platforms. The platforms and the loans must meet impact criteria, i.e., they must benefit underserved populations and communities.

Funds that invest in small and medium-sized enterprises in emerging markets to support business growth and/or short-term trade financing.

Funds that purchase debt of companies in developed markets to help improve the companies’ growth prospects, as well as their ESG policies and performance.

Funds that finance renewable energy or other environmentally beneficial projects. These funds may also make equity investments but are often considered in this asset class because of their overall risk, return, and cash-flow characteristics.

Community Development Financial Institutions (CDFIs) Asset owners can support local communities by investing in deposits or other programs at Community Development Financial Institutions (CDFIs). These are private financial institutions dedicated to providing affordable lending for small businesses, microenterprises, nonprofit organizations, and low-income housing development.

There are more than 1,000 CDFIs in the U.S. Some CDFIs are focused on business services, and others on individuals. Many have programs allowing investors to purchase CDs or sign up for full banking services, which allows the CDFI to use those funds to achieve its mission of local economic development.

Community Development Funds and Community Venture Funds are also included under the definition of CDFIs. They invest in businesses that have a positive impact on the community; these can be for-profit or nonprofit funds. These funds are not open to investors directly, but by depositing assets in a CDFI, investors can enhance its ability to have a positive impact on low income and minority communities.

Private debt funds operate similarly to private equity funds

CDFIs are private financial institutions dedicated to providing affordable lending for small businesses, microenterprises, nonprofit organizations, and low income housing development

14

Conclusion Fixed income investing for impact and ESG integration is relatively new in many respects, especially when compared with public equity investing. However, given that fixed income investors take the perspective of managing risk more than opportunity — in contrast to equity investors — fixed income ESG analysis likely has a greater role to play in the investment process than is widely perceived.

Cornerstone is witnessing a rapid uptake in investment strategies and vehicles designed for investors with different motivations for incorporating ESG into their fixed income portfolio. Investors should be aware that the labels of “ESG,” “sustainable,” “green,” “socially responsible,” and “impact” can be used interchangeably in the industry. Working with an informed advisor can help identify the specific instruments and investment strategies that are best aligned with an investor’s financial and ESG objectives.

Michael Geraghty is Cornerstone’s Strategist. He has over three decades of experience in the financial services industry. Michael has worked as an investment strategist at a number of leading firms. At PaineWebber, he was a Senior Vice President and member of an Institutional Investor ranked U.S. Portfolio Strategy team. At UBS, he was an Executive Director and senior member of the global equity strategy team responsible for regional and sector allocations. At Citi Investment Research & Analysis, Michael was the global themes strategist. Michael holds a Master’s degree in Economics and an MBA in Finance from Columbia University. [email protected]

Craig Metrick, CAIA is Managing Director, Institutional Consulting and Research at Cornerstone Capital Group, where he oversees the firm’s manager review process and provides investment advisory services for our foundation, endowment and family office clients. Previously, Craig was Principal and US Head of Responsible Investment at Mercer; for nearly 15 years, he has consulted on implementing responsible investment principles and mandates. Craig serves as the Chair of the Board of the US Forum for Sustainable and Responsible Investment (US SIF). [email protected]

Jennifer Leonard, CFA is Director, Asset Manager Due Diligence at Cornerstone Capital Group. In a career spanning microfinance, institutional financial services and impact investing, Jennifer has developed a unique skill-set in working to deploy capital for social and financial returns. Previously, she was vice president of impact investing at The CAPROCK Group, where she co-led the firm’s impact practice and helped clients build customized, impact-mandated portfolios. From 2009-13, she was a Latin America equity research analyst at Morgan Stanley. [email protected]

15

For more information on this report or our services, please contact our Investment Advisory team:

Phil Kirshman, CFA, CFP® Chief Investment Officer +1 646-650-2234 Alison R. Smith Managing Director, Head of Business Development +1 646-808-3666 M. Randall Strickland Director, Client Relationship Management +1 646-650-2175

1180 Avenue of the Americas, 20th Floor, New York, NY 10036 | +1 212 874 7400 www.cornerstonecapinc.com | [email protected] Follow us on Twitter, @Cornerstone_Cap

Important disclosures Cornerstone Capital Inc. doing business as Cornerstone Capital Group (“Cornerstone”) is a Delaware corporation with headquarters in New York, NY. The Cornerstone Flagship Report (“Report”) is a service mark of Cornerstone Capital Inc. All other marks referenced are the property of their respective owners. The Report is licensed for use by named individual Authorized Users, and may not be reproduced, distributed, forwarded, posted, published, transmitted, uploaded or otherwise made available to others for commercial purposes, including to individuals within an Institutional Subscriber without written authorization from Cornerstone. The views expressed herein are the views of the individual authors and may not reflect the views of Cornerstone or any institution with which an author is affiliated. Such authors do not have any actual, implied or apparent authority to act on behalf of any issuer mentioned in this publication. This publication does not take into account the investment objectives, financial situation, restrictions, particular needs or financial, legal or tax situation of any particular person and should not be viewed as addressing the recipients’ particular investment needs. Recipients should consider the information contained in this publication as only a single factor in making an investment decision and should not rely solely on investment recommendations contained herein, if any, as a substitution for the exercise of independent judgment of the merits and risks of investments. This is not an offer or solicitation for the purchase or sale of any security, investment, or other product and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations to purchase or sell such securities. Investing in securities and other financial products entails certain risks, including the possible loss of the entire principal amount invested. You should obtain advice from your tax, financial, legal, and other advisors and only make investment decisions on the basis of your own objectives, experience, and resources. Information contained herein is current as of the date appearing herein and has been obtained from sources believed to be reliable, but accuracy and completeness are not guaranteed and should not be relied upon as such. Cornerstone has no duty to update the information contained herein, and the opinions, estimates, projections, assessments and other views expressed in this publication (collectively “Statements”) may change without notice due to many factors including but not limited to fluctuating market conditions and economic factors. The Statements contained herein are based on a number of assumptions. Cornerstone makes no representations as to the reasonableness of such assumptions or the likelihood that such assumptions will coincide with actual events and this information should not be relied upon for that purpose. Changes in such assumptions could produce materially different results. Past performance is not a guarantee or indication of future results, and no representation or warranty, express or implied, is made regarding future performance of any security mentioned in this publication. Cornerstone accepts no liability for any loss (whether direct, indirect or consequential) occasioned to any person acting or refraining from action as a result of any material contained in or derived from this publication, except to the extent (but only to the extent) that such liability may not be waived, modified or limited under applicable law. This publication may provide addresses of, or contain hyperlinks to, Internet websites. Cornerstone has not reviewed the linked Internet website of any third party and takes no responsibility for the contents thereof. Each such address or hyperlink is provided for your convenience and information, and the content of linked third party websites is not in any way incorporated herein. Recipients who choose to access such third-party websites or follow such hyperlinks do so at their own risk. Copyright 2018.

Recommended