Consumer Driven Health Plans:

Empirical evidence of take-up, cost and utilization and HSA policy implications.Stephen T Parente, Roger Feldman, Jon B Christianson

Presentation to the National Association of Business Economics (NABE), Washington, DC, March 13, 2006

Sponsored by the Robert Wood Johnson Foundation’s Health Care Financing & Organization Initiative (HCFO) and the U.S. Department of Health and Human Services

Presentation Overview

What is a Consumer Drive Health Plan (CDHP)?

Policy Questions National CDHP Take-up Cost & Utilization Comparisons Over

Time National HSA Simulation Policy Implications

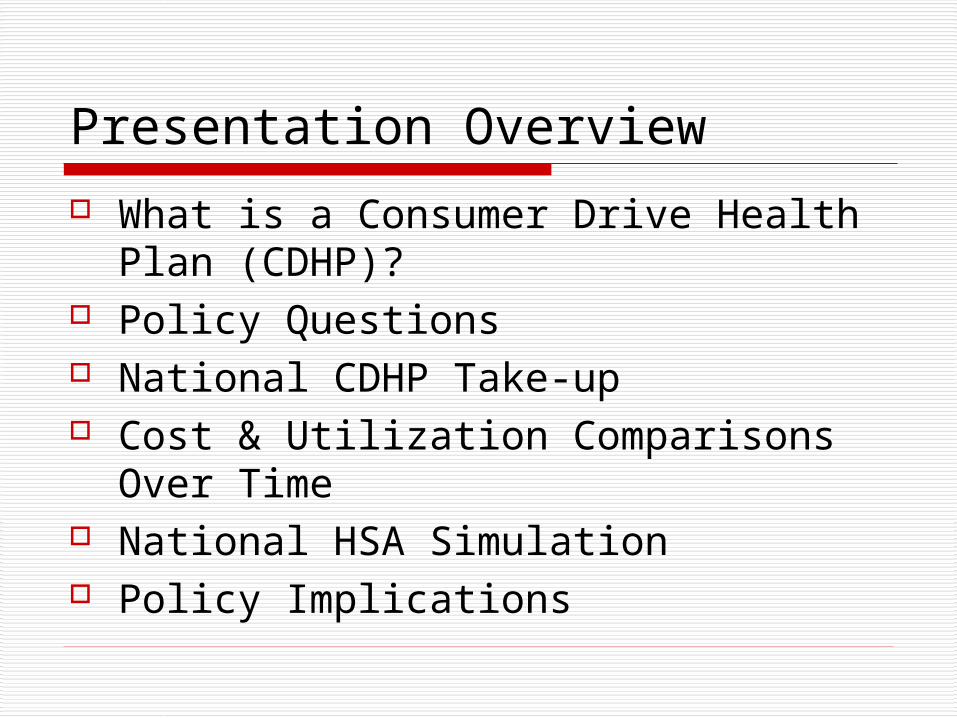

‘Classic’ CDHP Model – Definity Health

Definity Definity HealthHealthCareCare

AdvantageAdvantage

Web- and Web- and Phone-Phone-Based Based ToolsTools

Health ToolsHealth Toolsand Resourcesand Resources

Health Tools and Resources• Care management

program• Internet enabled

Health Coverage• Preventive care covered

100%• Annual deductible• Expenses beyond the

HRA

Health Reimbursement Account (HRA)• Employer allocates HRA1

• Member directs HRA• Roll over at year-end • Apply toward deductible2

Annual Annual DeductibleDeductible

Annual Annual DeductibleDeductible

Pre

ven

tive

Care

10

0%

Pre

ven

tive

Care

10

0%

Health Health CoverageCoverage

An

nu

al

Ded

uct

ible

1 Employer selects which expense apply toward the Health Coverage annual deductible.2 Paid out of employer’s general assets.

HRAHRAHRAHRA

$$

CDHP Version 2.0: The Health Savings Account (HSA)

HSAs legislated in

MMA 2003.

Pretty similar to

Definity Health HRA

Design except

the consumers owns

the account.

Annual Annual DeductibleDeductible

Annual Annual DeductibleDeductible

Pre

ven

tive C

are

P

reven

tive C

are

1

00

%1

00

%

Health Health CoverageCoverage

An

nu

al

Ded

uct

ible

HSAHSAHSAHSA

$$

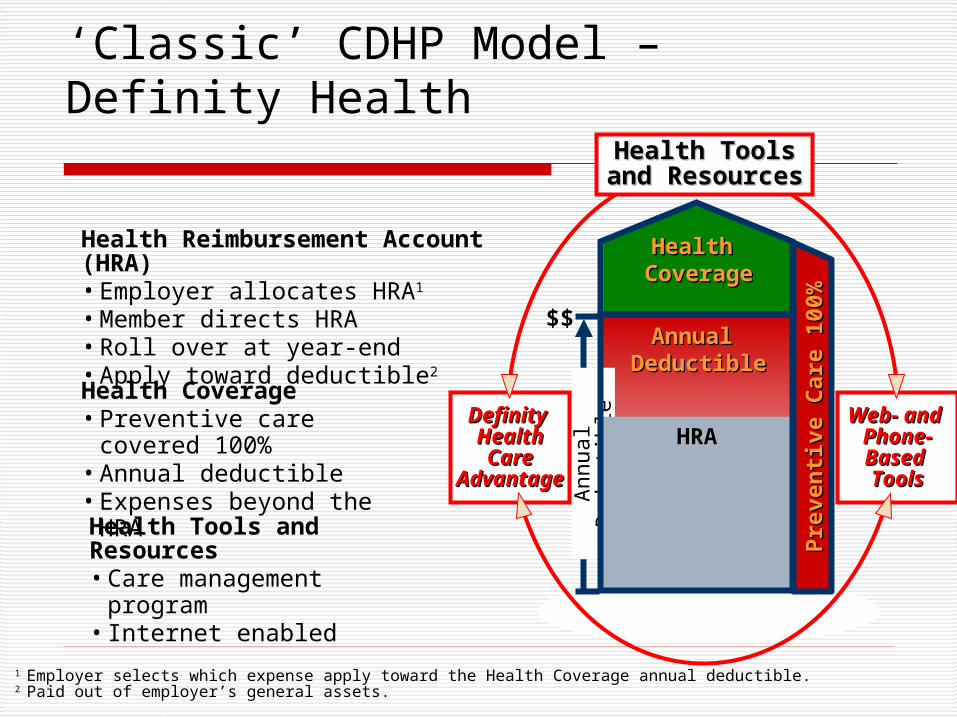

Conceptual Model of CDHPMoney

Medical Care

CDHP Budget

CoinsurancePlan Budget

b

a

c

Low Use Medium Use High Use

Policy Questions to be Addressed Do CDHPs (in the form of HRAs) have

national appeal? What are the longer-run cost & use

consequences of CDHPs? Where do they save money? What is the impact on pharmacy services, where

consumers can act in a ‘directed’ fashion? Do HSAs have potential national appeal? Are HSAs a viable approach to addressing

the problem of the uninsured?FYI: We are just approaching the half-way point of our research.

Nearly National Appeal of HRAs: States where the study employers’ 1st year CDHP take-up was >5%

>5%

0.1 - 5%

0%

Take-up

Employer-based Analysis Overview Analysis started in 2002 with six employers Combined population drawn from 50 states Total covered lives represented: ~250,000 Collect primarily employer HR data and

insurance claims data for all plans. New HCFO grant will create a study panel

with six total years of CDHP experience 2001-2006.

What is the impact of CDHPs on cost & use? Study Design:

First results reported in 2004, August, Health Services Research.

Look at CDHP/PPO/POS cohorts within one large employer for employees over time to see ‘longer run’ impact of CDHP in 2001 - 2003.

Control for several factors to ADJUST cost & use estimates: Health status/illness burden/health shocks

(cancer, catastrophic accident) Income Family size and dependents Age, gender

Study Setting Large employer that offered HMO and PPO in 2000-

2003 and introduced CDHP in 2001 Variation in cost sharing by contract Take-up of CDHP approximately 15% Smaller account/deductible gap, 0% co-insurance on

catastrophic General caveat: ANY Employer’s experience can be

quite different due to: Alternatives offered Plan design Communications with employees Sponsor’s objectives for the plan

New Results: Impact of CDHP and PPO on Cost Compared to POS

NOTES: These are results from a restricted continuously enrolled sample of 26% of the total employee population and are not a reflection of the plans’ expenditures. Bolded numbers are significant at p<.05.

All Annual Plan Effects Using POS Plan as baseline.

2000 Model 2001 2002Health Plan Cohorts Mean Stage Plan Effects Plan Effects Plan Effects

CDHP Cohort N=429Total Expenditure 4,037$ Probit -0.111 0.269 0.187

GLM 4.1% 26.0% 22.6%

Employer Expenditure 3,627$ Probit -0.077 0.222 0.222

GLM 11.2% 38.9% 30.1%Employee Expenditure 410$ Probit -2.083 -2.149 -1.723

GLM 43.0% 36.8% 39.6%

PPO Cohort N=1,025Total Expenditure 4,661$ Probit -0.082 -0.087 -0.161

GLM 8.3% 16.8% 9.5%

Employer Expenditure 4,172$ Probit -0.104 -0.127 -0.183

GLM 11.2% 20.0% 12.4%Employee Expenditure 490$ Probit -0.041 -0.003 -0.060

GLM -7.0% -3.3% -9.6%

Notes:

Regressions adjusted by annual trends, health plan choice, health plan choice interactedwith annual trends, age gender, income, number of covered lives in contract, use of an healthcare flexible spending account.

2003

NOTE: These are results from a restricted continuously enrolled sample of 27% of the total employee population and are not a reflection of the plans’ full prescription drug experience.

Impact of CDHP and PPO on Physician, Hospital and Pharmacy Cost Compared to POS

NOTE: These are results from a restricted continuously enrolled sample of 26% of the total employee population and are not a reflection of the plans’ expenditures.

All Annual Plan Effects Using POS Plan as baseline.

2000 Model 2001 2002Health Plan Cohorts Mean Stage Plan Effects Plan Effects Plan Effects

CDHP Cohort N=429Hospital Expenditure 1,332$ Probit -0.109 0.069 -0.050

GLM 60.8% 119.7% 75.5%

Physician Expenditure 1,891$ Probit -0.089 0.311 -0.007

GLM 10.7% 20.2% 25.1%Pharmacy Expenditure 814$ Probit -0.086 -0.061 0.256

GLM -14.7% -5.1% -3.9%

PPO Cohort N=1,025Hospital Expenditure 1,669$ Probit 0.109 0.106 -0.091

GLM 23.8% 24.4% 29.0%

Physician Expenditure 1,958$ Probit -0.105 -0.055 -0.174

GLM 5.9% 10.2% 6.7%Pharmacy Expenditure 1,034$ Probit -0.029 -0.096 0.047

GLM 8.3% 22.7% 9.9%

Notes:

Regressions adjusted by annual trends, health plan choice, health plan choice interactedwith annual trends, age gender, income, number of covered lives in contract, use of an healthcare flexible spending account.

2003

NOTE: These are results from a restricted continuously enrolled sample of 27% of the total employee population and are not a reflection of the plans’ full prescription drug experience.

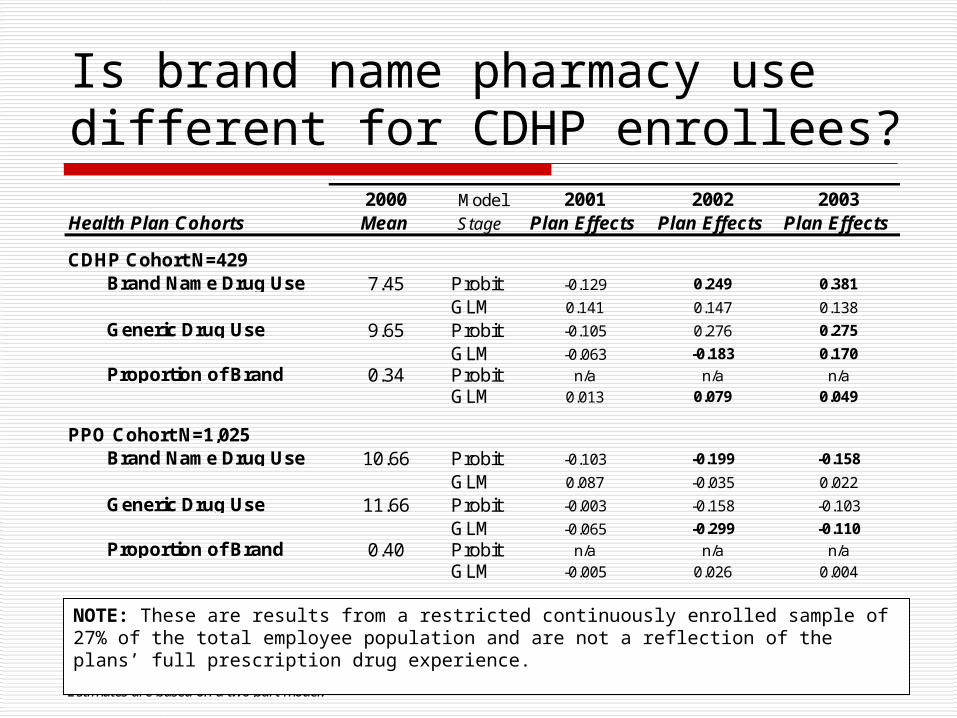

Is brand name pharmacy use different for CDHP enrollees?

2000 Model 2001 2002Health Plan Cohorts Mean Stage Plan Effects Plan Effects Plan Effects

CDHP Cohort N=429Brand Name Drug Use 7.45 Probit -0.129 0.249 0.381

GLM 0.141 0.147 0.138

Generic Drug Use 9.65 Probit -0.105 0.276 0.275

GLM -0.063 -0.183 0.170Proportion of Brand 0.34 Probit n/a n/a n/a

GLM 0.013 0.079 0.049

PPO Cohort N=1,025Brand Name Drug Use 10.66 Probit -0.103 -0.199 -0.158

GLM 0.087 -0.035 0.022

Generic Drug Use 11.66 Probit -0.003 -0.158 -0.103

GLM -0.065 -0.299 -0.110Proportion of Brand 0.40 Probit n/a n/a n/a

GLM -0.005 0.026 0.004

Notes:

Regressions adjusted by annual trends, health plan choice, health plan choice interactedwith annual trends, age gender, income, number of covered lives in contract, use of an healthcare flexible spending account.Estimates are based on a two part model.

2003

NOTE: These are results from a restricted continuously enrolled sample of 27% of the total employee population and are not a reflection of the plans’ full prescription drug experience.

Is there a difference in pharmacy use for CDHP patients with chronic conditions?

NOTE: These are results from a restricted continuously enrolled sample of 27% of the total employee population and are not a reflection of the plans’ full prescription drug experience.

2001 Model 2001 2002 2003Health Plan Cohorts Mean Stage Plan Effects Plan Effects Plan Effects

CDHP Cohort N=429Chronic Medical Rx Use 9.68 Probit -0.037 0.294 0.176 68.00

GLM -0.052 -0.179 0.171Chronic Psych Rx Use 6.90 Probit -0.037 0.294 0.176 88.00

GLM -0.052 -0.179 0.171Non-Chronic Rx Use 7.41 Probit 0.015 -0.063 0.031 108.00

GLM 0.065 0.010 0.222

PPO Cohort N=1,025Chronic Medical Rx Use 14.51 Probit 0.020 0.060 -0.087 71.00

GLM -0.013 -0.274 -0.138

Chronic Psych Rx Use 10.00 Probit -0.066 0.052 -0.023 91.00

GLM -0.032 -0.312 -0.170Non-Chronic Rx Use 7.81 Probit -0.070 -0.121 0.005 111.00

GLM -0.021 -0.237 -0.035

Notes:

Regressions adjusted by annual trends, health plan choice, health plan choice interactedwith annual trends, age gender, income, number of covered lives in contract, use of an healthcare flexible spending account.Estimates are based on a two part model.

NOTE: These are results from a restricted continuously enrolled sample of 27% of the total employee population and are not a reflection of the plans’ full prescription drug experience.

Overall Cost & Use Results Summary

CDHP plan did not have the lowest cost and utilization across all plans.

CDHP best (lowest) cost result was for pharmacy.

CDHP worse (highest) cost result was for hospital expenditures (inpatient & outpatient). – partially explained by pent-up demand for elective procedures & provider pricing differences across years.

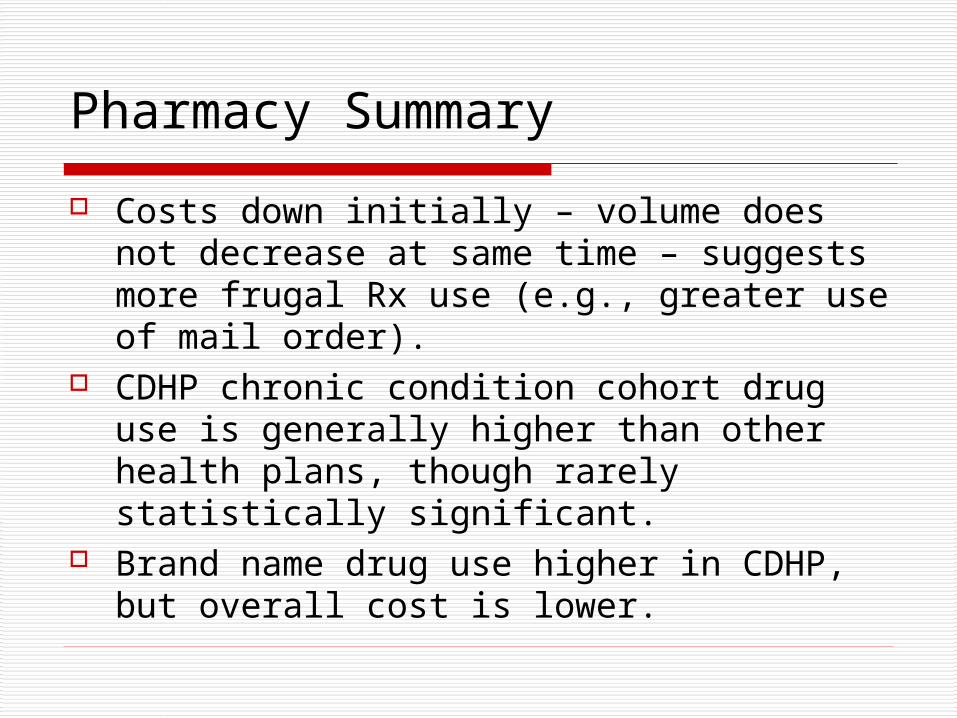

Pharmacy Summary

Costs down initially – volume does not decrease at same time – suggests more frugal Rx use (e.g., greater use of mail order).

CDHP chronic condition cohort drug use is generally higher than other health plans, though rarely statistically significant.

Brand name drug use higher in CDHP, but overall cost is lower.

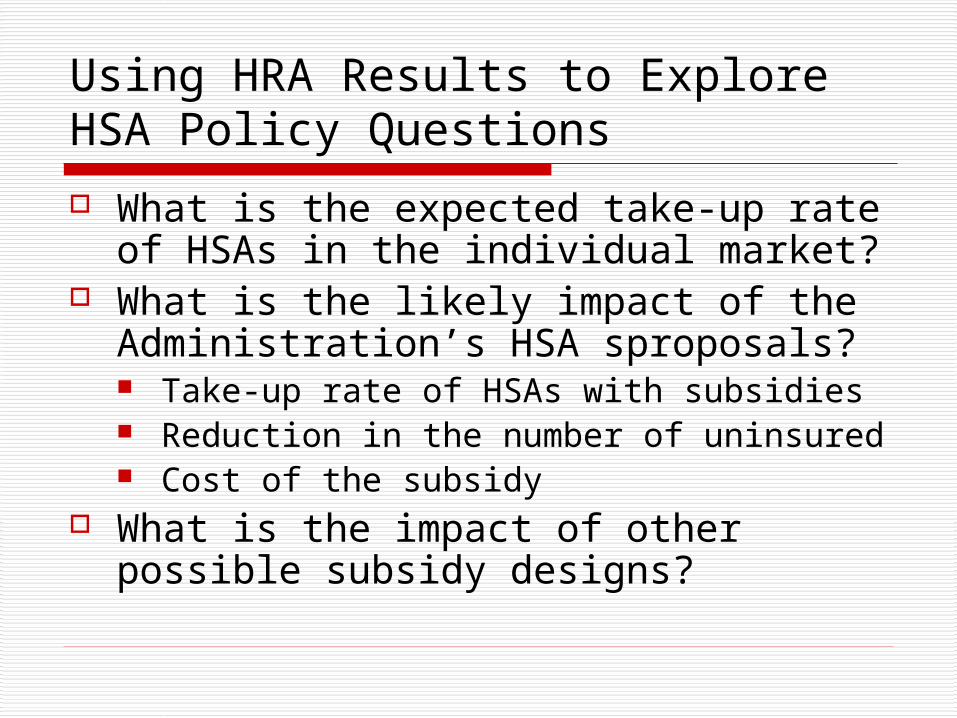

Using HRA Results to Explore HSA Policy Questions

What is the expected take-up rate of HSAs in the individual market?

What is the likely impact of the Administration’s HSA sproposals? Take-up rate of HSAs with subsidies Reduction in the number of uninsured Cost of the subsidy

What is the impact of other possible subsidy designs?

Data Sources

2002 health plan choice data from 3 large employers participating in a Robert Wood Johnson Foundation funded study on CDHPs Employee premium, deductible, coinsurance,

worker’s age, gender, wage income, single/family coverage

2001 Medical Expenditure Panel Survey (MEPS) Household Component Linked Insurance Component

eHealthinsurance.com Individual HSA plan information

Plan Choice Model Analytic Approach Plan Choices: HMO, 3 PPOs (low, medium, high), 2

CDHPs with Health Reimbursement Accounts (low and high)

Utility-maximization assumption where Uhj = j + Zj + Xhj + ehj

Estimate a conditional logit model of plan choice using the pooled, employer data

Explanatory variables Plan attributes (Z)

Annual tax-adjusted employee premium ($1000s dollars) Savings/reimbursement account size ($1000s dollars) Donut hole: difference between annual deductible and

account size ($1000s dollars) Coinsurance rate (i.e., .10 = 10% coinsurance)

Interactions between employee and plan attributes (X) Age, female, wage income, family contract

Plan-specific constants (j )

Price elasticity estimates from the plan choice model

PriceVariable Elasticity

Tax adjusted Employee Premium in $1,000 -0.9213

Employee's Health Account in $1,000 0.0885

∆ Between Deductible and Health Account in $1,000 -0.2430

Coinsurance (e.g., 15% = .15) -0.5405

Policy Simulations Baseline take-up of HSAs from the Medicare

Modernization Act of 2003

Simulation (1): Bush Administration’s 2004 proposal Refundable tax credit up to 90% of premium;

maximum of $1000/adult, $500/child (up to two) Subsidy for singles with no dependents phased out

at $30,000 adjusted gross income and $60,000 for families

Simulation (2): 2006 State of the Union Proposal

Simulation (3): Level the Playing Field

Simulation (4): Full subsidy of HSA premium

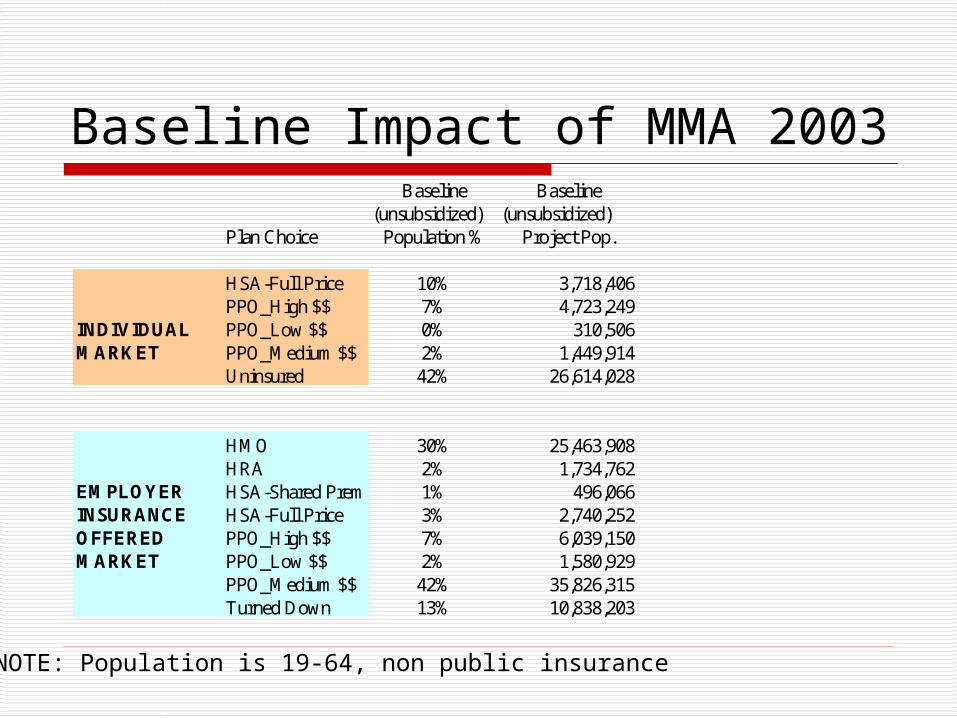

Baseline Impact of MMA 2003

NOTE: Population is 19-64, non public insurance

Baseline Baseline(unsubsidized) (unsubsidized)

Plan Choice Population % Project Pop.

HSA-Full Price 10% 3,718,406PPO_High $$ 7% 4,723,249

INDIVIDUAL PPO_Low $$ 0% 310,506MARKET PPO_Medium $$ 2% 1,449,914

Uninsured 42% 26,614,028

HMO 30% 25,463,908HRA 2% 1,734,762

EMPLOYER HSA-Shared Prem 1% 496,066INSURANCE HSA-Full Price 3% 2,740,252OFFERED PPO_High $$ 7% 6,039,150MARKET PPO_Low $$ 2% 1,580,929

PPO_Medium $$ 42% 35,826,315Turned Down 13% 10,838,203

HSA Summary & Next Steps HSA Plan design matters – We find a

greater take-up from a reduction in the donut hole than an increase in the account size.

Administration proposals to tax advantage HSAs will increase their take-up and reduce the number of uninsured, at the margin.

Look at HSA take-up versus retirement saving choice is a new frontier to examine.

Thank You!

For more information on our research, please visit:

www.ehealthplan.org

Stephen T. Parente, Ph.D., M.P.H., M.S.Assistant Professor, Department of FinanceDeputy Director, Medical Industry Leadership InstituteCarlson School of ManagementUniversity of Minnesota321 19th Ave. South, Room 3-149Minneapolis, MN 55455612-624-1391 (v)[email protected]://www.tc.um.edu/~paren010

Recommended