Corporate R&D and firms’ efficiency: Evidence from Europe’s top R&D investors

Subal KumbhakarState University of New York at Binghamton / USA

Raquel Ortega-Argilés IN+ Centre for Innovation, Technology and Policy Research, Instituto Superior Técnico, Lisbon / Portugal

Lesley Potters Utrecht School of Economics / NL

Marco VivarelliCatholic University, Milan / Italy & Max-Planck Institute of Economics, Jena / Germany

Peter VoigtEuropean Commission, Joint Research Centre – Institute for Prospective Technological Studies, Seville / Spain

Main research questions

How evident is the link of R&D to productivity? Significant across sectors? If so, what are the differences in the magnitudes of these effects?

What pays off more in terms of productivity: leveraging corporate R&D activities in high- or in low-tech sectors?

Is productivity affected systematically by the amount of deployed physical capital and/or by the accumulated knowledge? Differences across sectors?

Can existing (technical) inefficiencies be empirically attributed to an inappropriate capital accumulation (capacities) or to insufficient spending on R&D (capabilities); or eventually to both?

Evidence suggest: conducting R&D may help enhancing a firm's productivitysee e.g. the seminal article by GRILICHES, 1979 – introducing the ‘knowledge production function’ approach; see also for more recent contributions: KLETTE and KORTUM, 2004; JANZ, LÖÖF and PETERS, 2004; ROGERS, 2006; LÖÖF and HESHMATI, 2006

Most studies focus either on cross-country analyses or on one specific sector, (mainly dealing with high-tech industries, e.g. pharma, ICT, …). However, considerably less attention has been devoted to determining whether the productivity gains resulting from R&D may differ across industrial sectors.

Indeed, technological opportunities and appropriability conditions are quite different across sectors (see FREEMAN, 1982; PAVITT, 1984; WINTER, 1984; DOSI, 1997; MALERBA, 2004)

Most of the previous studies rely on cross sectional methodology (no panel)

Background & literature

From a methodological point of view, 2 strands:

1. Relies on Production Functions that assume efficient use of the given inputs.If this assumption does not hold true, the parameter estimates for any marginal effects of inputs might be biased.

2. Follows the logic of two-stage approach: cross-sectional or cross-firm productivity estimates are retrieved as a residual from a production function and subject to (regression on) a set of potential determinants of productivity growth.

Background & literatureR&D-firm performance

R&D and productivity: empirical evidence

General consensus at country, sector and firm level is that there is a positive link between R&D and productivity (see e.g. Mairesse and Sassenou, 1991; Griliches 1995 and 2000; Mairesse and Mohnen, 2001)

Estimated elasticities range from 0.05 to 0.25 Wakelin (2001)

170 UK quoted firms over the period 1988-92R&D expenditure had a positive and significant role on productivity growth"net users of innovations" have a higher return on R&D

Rincon and Vecchi (2003)CompuStat micro-data over the period 1991-2001R&D-reporting firms were more productive than their non-R&D-reporting

counterparts Tsai and Wang (2004)

Panel of 156 large Taiwanese firms over the period 1994-2000R&D investment had a significant and positive impact on firm’s productivity

(elasticity ~ 0.18)Greater impact for high-techs (0.30) than for other firms (0.07)

•

• Wakelin (2001) 170 UK quoted firms over the period 1988-92 R&D expenditure had a positive and significant role on productivity growth "net users of innovations" have a higher return on R&D

• Rincon and Vecchi (2003) CompuStat micro-data over the period 1991-2001 R&D-reporting firms were more productive than their non-R&D-reporting counterparts

• Tsai and Wang (2004) Panel of 156 large Taiwanese firms over the period 1994-2000 R&D investment had a significant and positive impact on firm’s productivity (elasticity ~

0.18) Greater impact for high-techs (0.30) than for other firms (0.07)

There is a comprehensive literature dealing with empirical analyses of firm’s efficiency, based either on parametric or non-parametric frontier approaches.

Examples of R&D on firms’ inefficiency:

Sanders et al. (2007) based on firms’ life cycle where firms have the choice to achieve quality improvements or invest in R&D to achieve efficiency gains. The findings show that young firms opt for quality instead of efficiency improvements, whereas more mature firms will do both.

Bos et al. (2007 and 2008) account for inefficient use of resources and differences in the production technology across countries/ industries. Technological change, efficiency and effects implied by the input set determine endogenously technology clubs or country groups.

R&D and firm efficiency: empirical evidence

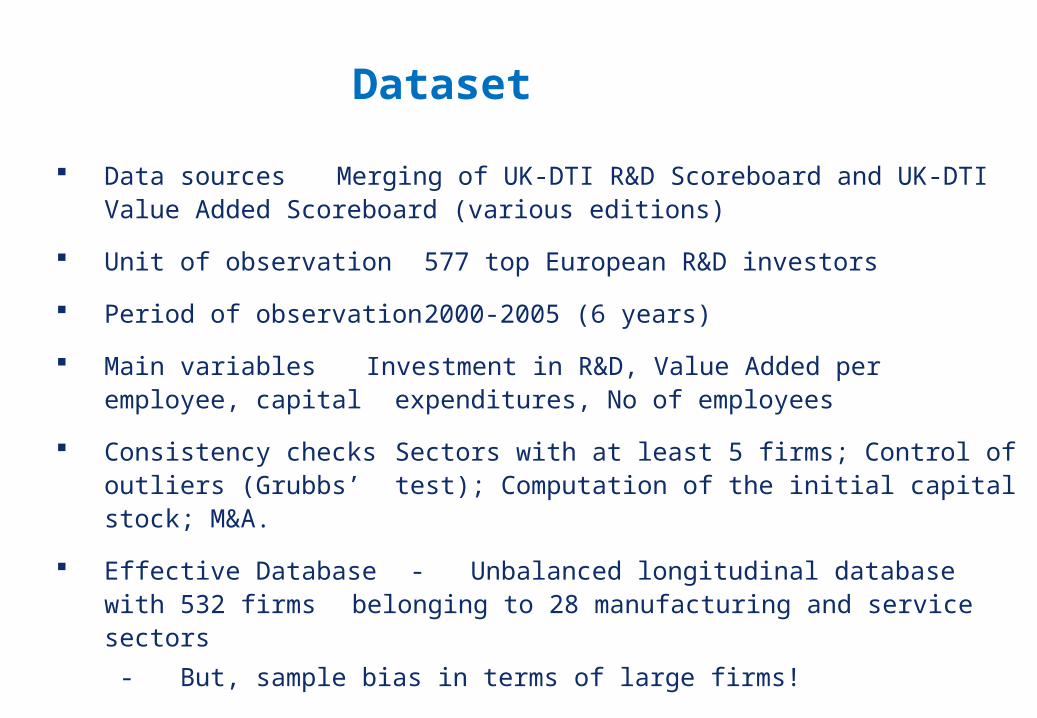

Data sources Merging of UK-DTI R&D Scoreboard and UK-DTI Value Added Scoreboard (various editions)

Unit of observation 577 top European R&D investors

Period of observation 2000-2005 (6 years)

Main variables Investment in R&D, Value Added per employee, capital expenditures, No of employees

Consistency checks Sectors with at least 5 firms; Control of outliers (Grubbs’ test); Computation of the initial capital stock; M&A.

Effective Database - Unbalanced longitudinal database with 532 firms belonging to 28 manufacturing and service sectors

- But, sample bias in terms of large firms!

Dataset

Descriptive statistics

Variable All firms High-tech Medium-tech Low-tech

Mean SD Mean SD Mean SD Mean SD

VA/E 0.068 0.062 0.063 0.037 0.053 0.024 0.095 0.100

R&D/E 0.032 0.049 0.062 0.069 0.021 0.026 0.012 0.013

C/E 0.473 1.756 0.158 0.400 0.135 0.176 1.280 3.091

E 36120 62434 40626 73890 22736 38350 48258 69635

Low-tech industries appear to be highly productive (labour productivity)

But this certainly is not because of R&D accumulation rather than due to …

higher capital intensity and scale economies

Methodology SFA (Stochastic Frontier Analysis) with time and sector dummies (PF) thus controlling for

the effects of R&D and capital stocks, time (time trend) and sector specifics on firms technical inefficiency >>> K/E is used as the pivotal impact variable. Furthermore, marginal effects were calculated to allow detailed investigation of the impact of external factors on inefficiency.

To compare: POLS (Preliminary pooled OLS) with time and sector dummies Random effects (RE) model rather than fixed effects for various reasons:

• unbalanced short panel (average of 3.4 observations available per firm) severely affects within-firm variability ;

• the within-firm component of the variability of the dependent variable is overwhelmed by the between-firms component (0.15 vs 0.58);

• the Hausman selection test (Chi-squared=4.65, p-value=0.79) clearly rejected fixed effects model;

• in the fixed effects model time-invariant regressors, such as the two-digit sectoral dummies, are automatically wiped-out.

ii uvEECEKEVA )ln()/ln()/ln()/ln( 3210

MethodologyLog-linear Production Function:

all variables in natural logarithms and deflated according to the different national GDP deflators during the 6 year period

VA/E = labour productivity

K/E = R&D stock per employee

C/E = (physical) capital stock per employee

E = employment (company size control)

vi - ui = compound error term

Note: Time (alternatively time trend) and two-digit sector dummies used in order to control for market / macroeconomic shocks (learning curve effects ) and sectoral peculiarities

with: i = 1…532; t = 2000…2005; u and ν as the error term components

Methodology: Stock variables• Calculating R&D and capital stocks: Perpetual Inventory Method

00

,( )t

ts c j

FLOWSTOCK

g

with: s = 1,…, 28 c = 1,…,14 j = 1,2,3 t0 = 2000

tjtt FLOWSTOCKSTOCK )1(1 with: t = 2000,…,2005

FLOW = actual expenditures

OECD ANBERD and OECD STAN databases for growth rates (g) per sector (s) and country (c) over the period 1990-1999

Different depreciation rates (δ) depending on sector group (j):

R&D stock [see e.g. Hall, 2007]

20% in case of high-tech firms, 15% for medium-techs, 12% for low-techs

Capital stock [see e.g. Nadiri and Prucha, 1996]

8% in case of high-tech firms, 6% for medium-techs, 4% for low-techs

Results (model comparison)

Model Specifics POLS RE SFA POLS RE SFA POLS RE SFA POLS RE SFA

ln(K/E) 0.123 0.125 0.087 0.180 0.160 0.162 0.138 0.146 0.102 0.048 0.068 0.051

(0.014) (0.015) (0.009) (0.018) (0.029) (0.018) (0.012) (0.026) (0.012) (0.014) (0.021) (0.013)

ln(C/E) 0.122 0.117 0.075 -0.011 0.014 0.035 0.133 0.137 0.132 0.23 0.21 0.105

(0.013) (0.018) (0.011) (0.019) (0.025) (0.020) (0.018) (0.029) (0.014) (0.020) (0.031) (0.017)

ln(E) -0.063 -0.092 -0.043 -0.036 -0.074 -0.007 -0.061 -0.072 -0.035 -0.084 -0.113 -0.087

(0.007) (0.013) (0.006) (0.010) (0.019) (0.009) (0.012) (0.022) (0.009) (0.014) (0.022) (0.010)

Constant -0.189 0.096 -2.015 -1.863 -1.571 -1.792 -1.412 -1.231 -1.326 -0.598 -1.443 -0.306

(0.183) (0.220) (0.086) (0.149) (0.221) (0.151) (0.149) (0.309) (0.141) (0.188) (0.252) (0.211)

Inefficiency term

R&D intensity1 -3.992 -7.66 -0.694 ---

(0.830) (2.285) (0.192) ---

Capital intensity1 -12.715 0.675 --- -0.424

(2.887) (0.295) --- (0.190)

Constant --- --- --- 1.040

--- --- --- (0.345)

Noise term

No. of employees -0.255 -0.295 -0.454 -0.714

(0.004) (0.012) (0.061) (0.081)

Constant --- --- 1.176 3.93

--- --- (0.548) (0.721)

Wald: time-D's (jtl.) 8.8 95.28 53.51 3.3 29.53 7.89 3.66 32.22 20.69 7.17 58.15 55.2

P-value 0.000 0.000 0.000 0.006 0.000 0.162 0.003 0.000 0.001 0.000 0.000 0.000

Wald: sector-D's (PF) 46.62 368.21 1455.85 38.07 54.76 95.15 14.89 19.49 136.22 45.51 186.66 858.23

P-value 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.003 0.000 0.000 0.000 0.000

Wald: sector-D's (TE) 75.9 79.64 59.22 75.45

P-value 0.000 0.000 0.000 0.000

firms 1787 600 671 516

observations 532 170 196 166

Note1 Intensity refers to calculated R&D (capital) stocks per employee, standardized by the sample mean.Robust standard errors in parenthesis; all coefficients are significant at 95% confidence level (unless those that are underlined)

Sample as a whole High-tech Medium-tech Low-tech

Results (SFA)

Whole Sample High-tech Med-high Low-tech

Model Specification coefficient P-Value** coefficient P-Value** coefficient P-Value** coefficient P-Value**

ln(Knowledge stock/Employee)ln(Capital stock/Employee)ln(E) [workforce]timeConstant sector dummies*

0.08700.0744-0.04310.0330-2.05201462.41

0.0000.0000.0000.0000.0000.000

0.1536------

0.0288-1.9007

145.15

0.0000.1620.6130.0000.0000.000

0.1038 0.1307-0.03730.0176-1.2650134.40

0.0000.0000.0000.0030.0000.000

---0.1584-0.09660.0486

---1292.92

0.4990.0000.0000.0000.1110.000

U(het): [Inefficiency term] R&D intensityCapital intensitytimeyear dummies*

sector dummies*

Constant

-3.992-12.700

------

75.86---

0.000 0.0000.2650.7070.0000.838

-5.5144---------

87.50---

0.001 0.0830.4790.6230.0000.984

-0.6861---------

61.64---

0.000 0.1770.2890.0970.0000.216

-0.4683---------

135.311.9146

0.0000.1920.4000.3420.0000.000

V(het): No. of employeesConstant

-0.2545---

0.0000.975

-0.3020---

0.0000.636

-0.4448 1.1138

0.0000.042

-0.84854.7825

0.0000.000

Wald (overall) / prob > chi2 2639.39 0.000 441.61 0.000 545.48 0.000 27755.95 0.000

Log likelihood -449.441 -140.4168-35.599

-146.69

firms 1787 600 671 516

observations 532 170 196 166

Note * Significance of all variables belonging to the corresponding group was tested jointly (joint Wald-test) Note** Variables not found to be significant at α 0.05 have been removed from the estimation (though the corresponding P-values were kept and are reported in the table in italics

in order to demonstrate the level of insignificance / to justify the removal).

SFA: dependent variable VA/E, HN-distribution of inefficiencies

Results: Firm level inefficiencies

Efficiency (TE) obs MeanStd.

deviation Min Max

overall sample 1787 0.822 0.1597 0.145 1.000

high-tech sectors 600 0.819 0.1473 0.161 1.000

medium-techs 671 0.870 0.1182 0.284 1.000

low-techs 516 0.732 0.2086 0.041 0.970

Marginal effects on efficiency obs Mean

Std. deviation Min Max

overall sample 1787 -0.033 0.0290 -0.131 0.000

high-tech sectors 600 -0.040 0.0304 -0.132 0.000

medium-techs 671 -0.052 0.0465 -0.264 0.000

low-techs 516 -0.092 0.0848 -0. 473 -0.011

02

46

810

Den

sity

0 .2 .4 .6 .8 1ef

all companies high-tech industriesmedium-tech industries low-tech industries

R&D intensity groupsEfficiency

-.5

-.4

-.3

-.2

-.1

0

R&D intensity groupsMarginal effects of R&D-intensity on firms' ineffeciency

all companies high-tech industriesmedium-tech industries low-tech industries

Summary of empirical results

In general, corporate R&D affects company performance positively! toehold for R&D policy

However, at firm level there are two effects to be distinguished both leveraging productivity…

1) advancing technology, shifting the frontier (technological progress) increase in prod. possibilities2) creating (tacit) knowledge, which helps avoiding / reducing waste increase in firms’ efficiency

high / medium-tech industries : (1) + (2)low-tech industries : (1)

Accordingly, returns to an additional investment in R&D tend to be higher in high-tech industries compared to low-techs due to the double edge effect of R&D. For capital accumulation it is vice versa! (because embodied TCH is more important for low-techs than for high-tech industries remind TCH…!)

Nevertheless, corporate R&D has a positive impact on company performance in all industries!What is about sector specifics in terms of the effect of R&D on efficiency?Evidence of underinvestment in R&D?

Target sectors for R&D policiesTE estimates

marginal effect of R&D-intensity on firms' Technical Efficiency

R&D intensity firms observations mean min max mean min max

High-tech 0.21 170 600 0.819 0.161 1.000 -0.040 0.000 -0.132

Technology hardware & equipment 0.41 22 77 0.604 0.161 0.885 -0.103 -0.050 -0.132

Pharmaceuticals & biotechnology 0.28 30 120 0.863 0.708 0.943 -0.026 -0.012 -0.035

Leisure goods 0.25 7 25 0.693 0.362 0.906 -0.070 -0.062 -0.074

Aerospace & defence 0.20 21 82 1.000 1.000 1.000 0.000 0.000 0.000

Automobiles & parts 0.16 37 140 0.812 0.565 0.957 -0.038 -0.027 -0.040

Software & computer services 0.16 21 56 0.899 0.863 0.960 -0.019 -0.010 -0.021

Electronic & electrical equipment 0.15 32 100 0.779 0.401 0.909 -0.047 -0.021 -0.051

Medium-high-tech 0.08 196 671 0.870 0.284 1.000 -0.052 0.000 -0.264

Chemicals 0.12 42 154 0.895 0.716 0.996 -0.039 -0.001 -0.063

Industrial engineering 0.08 58 209 0.918 0.771 0.966 -0.030 -0.011 -0.038

Health care equipment & services 0.08 14 43 0.754 0.477 0.930 -0.098 -0.030 -0.141

Household goods 0.06 18 51 0.729 0.414 0.945 -0.112 -0.041 -0.132

General industrials 0.05 20 69 1.000 1.000 1.000 0.000 0.000 0.000

Food producers 0.05 31 105 0.858 0.659 0.936 -0.055 -0.022 -0.063

Media 0.05 13 40 0.640 0.284 0.961 -0.173 -0.044 -0.264

Low-tech 0.02 166 516 0.732 0.041 0.970 -0.092 -0.011 -0.473

Fixed line telecommunications 0.03 14 43 0.783 0.321 0.947 -0.064 -0.041 -0.080

Industrial metals 0.02 14 39 0.837 0.654 0.943 -0.046 -0.025 -0.059

Electricity 0.02 13 43 0.720 0.371 0.911 -0.106 -0.033 -0.146

Oil equipment, services & distribution 0.02 7 22 0.134 0.041 0.206 -0.386 -0.181 -0.473

General retailers 0.02 9 29 0.800 0.588 0.932 -0.055 -0.039 -0.064

Support services 0.02 22 67 0.703 0.297 0.898 -0.090 -0.034 -0.112

Construction & materials 0.02 15 65 0.931 0.821 0.965 -0.017 -0.014 -0.019

Banks 0.02 6 6 0.647 0.411 0.930 -0.414 -0.364 -0.446

Gas, water & multiutilities 0.01 23 75 0.694 0.359 0.954 -0.088 -0.039 -0.103

Oil & gas producers 0.01 13 48 0.787 0.530 0.970 -0.058 -0.028 -0.081

Mobile telecommunications 0.01 6 17 0.550 0.167 0.955 -0.161 -0.011 -0.199

Industrial transportation 0.01 11 23 0.848 0.568 0.943 -0.044 -0.018 -0.052

Beverages 0.01 8 20 0.752 0.481 0.927 -0.073 -0.057 -0.082

Mining 0 5 19 0.471 0.190 0.913 -0.199 -0.186 -0.212

Total 0.09 532 1787 0.822 0.041 1.000 -0.033 0.000 -0.473

Remark: The highest marginal effects of R&D-intensity on inefficiency were found for sectors that have a rather low mean TE, suggesting underinvestment in R&D and a toehold for R&D policy. In turn, in some sectors almost no marginal effect of R&D-intensity on TE could be found (suggesting an already almost optimal R&D-intensity…).

Policy relevant messages

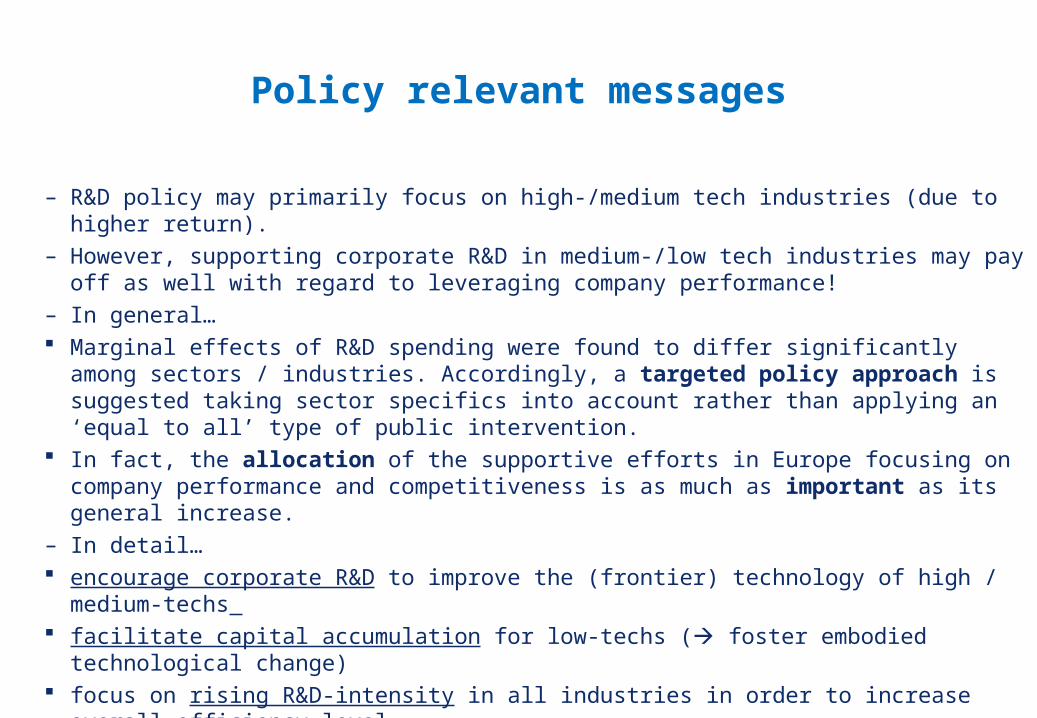

– R&D policy may primarily focus on high-/medium tech industries (due to higher return).– However, supporting corporate R&D in medium-/low tech industries may pay off as well with

regard to leveraging company performance!– In general… Marginal effects of R&D spending were found to differ significantly among sectors / industries.

Accordingly, a targeted policy approach is suggested taking sector specifics into account rather than applying an ‘equal to all’ type of public intervention.

In fact, the allocation of the supportive efforts in Europe focusing on company performance and competitiveness is as much as important as its general increase.

– In detail… encourage corporate R&D to improve the (frontier) technology of high / medium-techs facilitate capital accumulation for low-techs ( foster embodied technological change) focus on rising R&D-intensity in all industries in order to increase overall efficiency level

Recommended