Crop Insurance 101 & BeyondRisk Management Basics & Strategies for your Operation

Brad Heinrichs, Crop Insurance Specialist & Agent

NFB Crop Insurance Inc.

402-984-6474

About Me

Brad Heinrichs, Agent – NFB Crop Insurance Inc.

Partnered with NFBI to start NFB Crop Insurance, Inc. in 2009

Grew up by Carleton, NE (“The Milo Capital of Nebraska”)

UNL – Agri-business Degree

Worked with Nebraska Soybean Board prior to getting involved

in the crop insurance industry

Been involved with agriculture my whole life.

Row crops & Livestock

Wife, Renae – Daughters Ellie (4) & Sophia (2 ½)

Farmer-Agent – Live it. Know it. Understand the farmer’s

perspective.

Licensed in Crop Insurance since 2009.

Nebraska Farm Business, Inc.

Nebraska Farm Business Inc. provides financial analysis, business planning, tax

planning, and tax preparation.

Started in 1976 as part of the Cooperative Extension through the University of

Nebraska-Lincoln.

In 2002 moved off campus to another location in Lincoln but still works with

UNL on collecting financial data on farming operations.

Financial Analysis, Business Planning, Tax Planning & Tax Preparation Services

NFB Crop Insurance, Inc.

In 2009, NFB Crop Insurance, Inc. was launched to provide a full service crop

insurance agency to farmers across Nebraska.

NFB Crop Insurance, Inc. partnered with Nebraska Farm Business Inc. to work

with clients to develop tailored risk management plans through financial

decision

Can use a client’s financial analysis as a tool to better understand what risk is

covered for clients

Do not need to work with Nebraska Farm Business Inc to be a client of NFB

Crop Insurance.

Our agency only sells crop insurance to better specialize in service to its

customers

A different approach – not your typical crop insurance agency.

Thoughts on Crop Insurance?

What comes to mind when you hear crop insurance?

Have you had experience with crop insurance?

Do creditors need you to carry insurance?

Does your current “Risk Plan” involve insurance coverage?

Why is Crop Insurance Important?

Top Risk Management Tool

Allows farmers to recover from natural disasters & volatile market

fluctuations

Provides confidence to make long-term investments

Thriving Economy is Dependent upon Agriculture Industry Thriving

During 2012 Drought – Crop Insurance saved 20,900 jobs with annual labor income

of 721 Million in IA, NE, SD & WY combined (FCS of America study)

Every 1 in 4 jobs in Nebraska is related to agriculture

5% of the US Economy is Agriculture –10% of all US employment is related to

agriculture

(NCIS)

WHAT DO YOU WANT TO KNOW??

Write your question! We’ll Answer!!

BASICS of PROGRAM

FarmersInsurance Sales Agent

(Responsible for Sales/Premium Collection of Farmer-Paid Portion and processing)

Private Insurance Companies

•15 Companies can sell Federal Crop Insurance

Federal Crop Insurance Corporation

(Managed by USDA/RMA)

What does the Agent do?

Identifies a need for risk management

Explains product options

Sells insurance contract

Collects production and acreage report

Notifies company in case of loss

Informs farmer about changes to the program

Processing of paperwork & policy changes

Local, professional, trusted contact for farmer

What does the Insurance Company do?

Insures crops

Provides agent training for the processing of all paperwork

Contracts agents and independent loss adjusters

Ensures all claims are fairly and promptly paid

Accepts risk on the insurance policies

Interacts with RMA/Agents/Farmers

Trains Agents and Adjusters

What does the Federal Government do? Subsidizes insurance

▪ Pays delivery reimbursement (A&O)

▪ Pays premium subsidy

▪ Offers reinsurance

Sets rates and establishes insurance policy provisions

Regulates insurance companies

Why a Government Program?

▪ Weather tends to impact a large area

▪ Without federal subsidies premiums would be too high for most farmers to

participate

▪ Without federal reinsurance, federal capital requirements would be too

high for most companies to participate

FCIC Premium Subsidy Percentages

Coverage

Level

50/55

CAT50% 55% 60% 65% 70% 75% 80% 85%

Basic Unit 100% 67% .640 .640 .590 .590 .550 .480 .380

Optional

Unit

NA .670 .640 .640 .590 .590 .550 .480 .380

Enterprise

Units

NA .80 .800 .800 .800 .800 .770 .680 .530

Admin

Fee

$300 $30 $30 $30 $30 $30 $30 $30 $30

RMA (Risk Management Agency)

RMA manages the Federal Crop Insurance Corporation (FCIC) which provides

innovative crop insurance products.

Approved Insurance Providers (AIP) sell and service Federal crop insurance

policies through a public private partnership.

RMA has 3 key areas

Insurance Services - Responsible for promoting and supporting sound risk

management solutions for our farmers.

Product Management - Responsible for developing, testing, crop insurance products

Compliance - Responsible for safe guarding the integrity of the program

Types of Crop Insurance Multi-Peril (MPCI)

Federal

YP - Yield Protection - Protects against a production loss

RP - Revenue Protection - Covers weather related causes of

loss, certain other unavoidable perils and price fluctuations.

RPHPE - Revenue Protection Harvest Price Exclusion - RPHPE

coverage excludes the use of the harvest price in the

determination of the revenue protection guarantee

ARP - Area Risk Plan - An area based insurance program that

provides insurance protection against widespread loss of

revenue in a county .

Types of Crop Insurance Cont.

Whole Farm Revenue – Works best with Multiple Crop/Livestock enterprises,

Uses Schedule F, Long Claim Process (Multi-Year)

Margin Protection – Area based plan protecting against fluctuations in Revenue

and Expenses

Pasture, Rangeland, Forest (PRF)

Helps protect loss of forage due to decreased rainfall

Select a time interval (2 months) as well as a grid ID location (17 miles x 17 miles)

70-90% Coverage level

Supplemental Coverages

Crop-Hail

Private Sector

Companion Hail (CP)

Production Plan (CHPP)

Production Plan Enterprise Units

APH – Actual Production History

Actual Production History - a yield history for a farm for a specific crop. The

APH can contain up to 10 years of previous yields.

If a farmer would rotate corn and soybeans every other year. It would be

possible to have yields up to 20 years old in the APH database.

Unit Structure

Enterprise Units

Optional Units

Basic Units

How does it affect my losses?

Cost differences?

Most Popular?

Risk Tolerance?

Enterprise Unit An enterprise unit combines all the acres of an insured crop in the county into one

county-wide unit, regardless of ownership, share or rental arrangement. A varying premium discount will apply, based on the number of planted acres of the crop insured. In order to qualify, an enterprise unit must contain all of the insurable acreage of the same insured crop in:

Two or more sections, if optional units are available by sections;

Two or more section equivalents, if optional units are available by section equivalents;

Two or more FSA farm numbers (FNs), if optional units are available by FSA FNs;

At least two of the sections, section equivalents, FSA FNs must each have planted acreage that constitutes at least the lesser of 20 acres or 20% of the insured crop acreage in the enterprise unit. If there is planted acreage in more than two sections, section equivalents, FSA FNs or units established by written agreement, these can be aggregated to form at least two parcels to meet this requirement.

Enterprise Unit by Practice

Enterprise by Practice

Enterprise units by practice provide for separate coverage by irrigated and

non-irrigated practices. Acreage for each practice will need to meet all the

requirements for enterprise units listed above.

2018 Changes

Optional Unit

Optional units are divisions by sections or section equivalents, by irrigated &

non-irrigated practices.

Typically more expensive than Enterprise Units, but likelihood of collecting if

damage occurs is higher as each unit stands alone.

Basic Unit

A basic unit is all acreage of the crop in the county of which the insured

has 100% ownership or shares with the same person.

Options

Coverage Level by Practice (LP)

Enterprise by Practice (EP)

Trend Adjustment (TA)

Yield Adjustment (YA)

Yield Exclusion (YE)

Yield Cup (YC)

Prevent Plant Plus 5% (PF)

V6 Corn – 6/15/2017 Hail Damage – Clay County, Nebraska

(Photo by Jennifer Reese, Nebraska Extension cropwatch.unl.edu)

Knee High Crop prior to Hail

6/4/2014 – Saline County, Nebraska (ketv.com)

6/3/2014 – Dodge County, Nebraska

(Photo by Nathan Mueller, Nebraska Extension cropwatch.unl.edu)

www.aganytime.com

Hail Risk and Managing that Risk (Video)

Production Plan Hail

Coverage Level in Conjunction with Multi-Peril Policy

Covers the top portion of the crop revenue not covered by your Revenue

Protection.

Can Insure up to 120% of your yield

No deductible wind and hail

Some can now quote you Production Plan Enterprise Units

Less cost than Companion – Rates are Cheaper but tend to have more

coverage per acre

WATCH YOUR PREMIUMS

Production Plan Example

220 APH (with Trend) * 120% = 264

Bushels

Protection under RP Multi-Peril:

220 * 70% = 154 Bushels * $3.95 = $608

Total PP + RP Coverage: 264 * $3.95 =

$1,043

$1,043 - $608 = $435 Limit of Insurance

Production Plan

Example

Adjusts at wind/hail loss 30%

264 * 30% = 79 Bushel loss * $3.95 = $312

Take to harvest

Harvest 200 Bushels/Acre

264 Bu - 200 Bu = 64 Bushel Production loss * $3.95 (Spring Price)= $253

Amount Payable would be the production deficiency. Take the lesser of the two. Not to exceed limit of insurance.

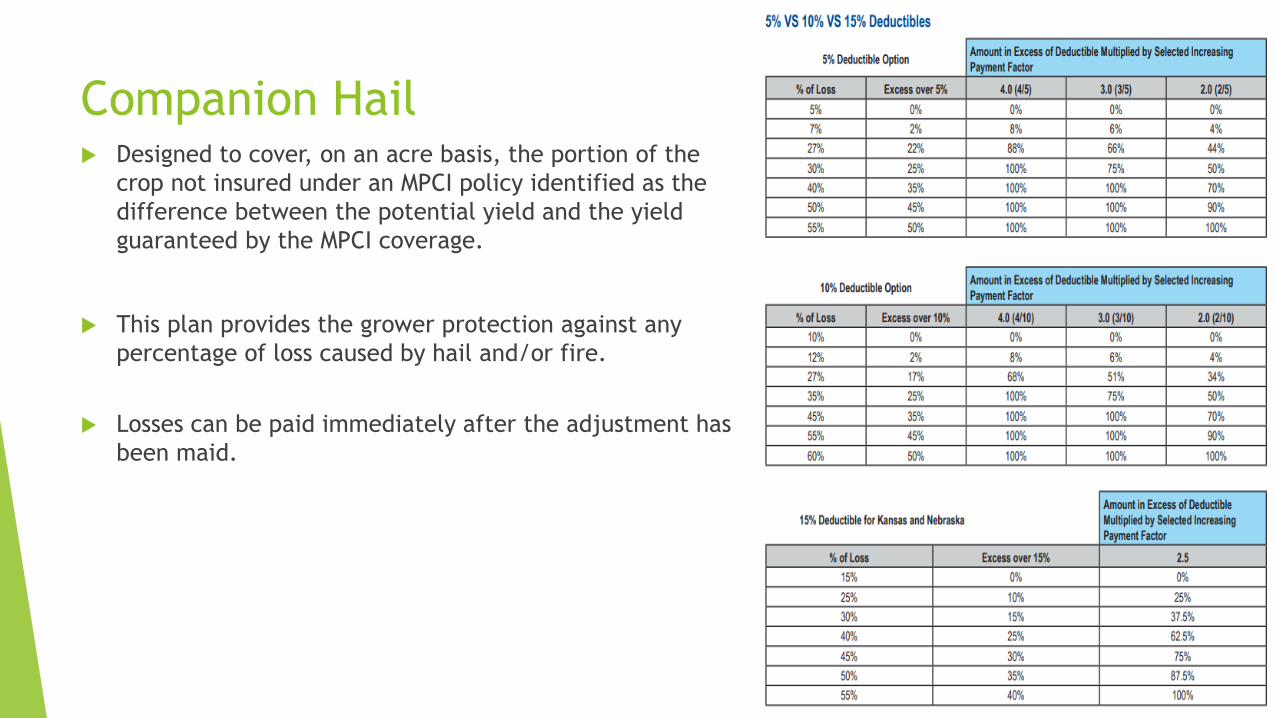

Companion Hail Designed to cover, on an acre basis, the portion of the

crop not insured under an MPCI policy identified as the

difference between the potential yield and the yield

guaranteed by the MPCI coverage.

This plan provides the grower protection against any

percentage of loss caused by hail and/or fire.

Losses can be paid immediately after the adjustment has

been maid.

Who shoulders the risk?

Share the Risk

Farm Bill Ahead

Farmers

• Pay Premium

• Deductibles

Crop Ins. Providers

• Pay Indemnities on own for most claims

• Typically incur Underwriting Losses

Federal Government

• Reinsurance Carrier

• If incur Underwriting Losses, they also can receive gains in good years

Deadlines. Deadlines. Deadlines.

Many crop insurance procedures are focused upon DEADLINES

Hail Policies do not have the March 15/October 1 deadlines or sales, however

they do need to be in place before the weather event occurs. Typically 3+

hours.

Sales Closing (MPCI)

March 15 - Spring Seeded Crops

October 2 – Fall Seeded Crops (ie wheat)

November 15 - PRF

When you can change a policy, cancel a policy, transfer coverage from one agent to

another, write a new policy

Deadlines Cont.

Acreage Reporting

July 16 – Spring Seeded Crops

November 15 – Fall Seeded Crops (ie wheat)

November 15 – Pasture Range Forage PRF

Record Acreage data for planted acres for valid coverage

Production Reporting

April 30 – Spring Seeded Crops (for previous crop year bushels)

November 14 – Fall Seeded Crops (ie wheat)

Record bushels for APH purposes or for claim purposes

Sales Closing

Application Process

What does this information

mean?

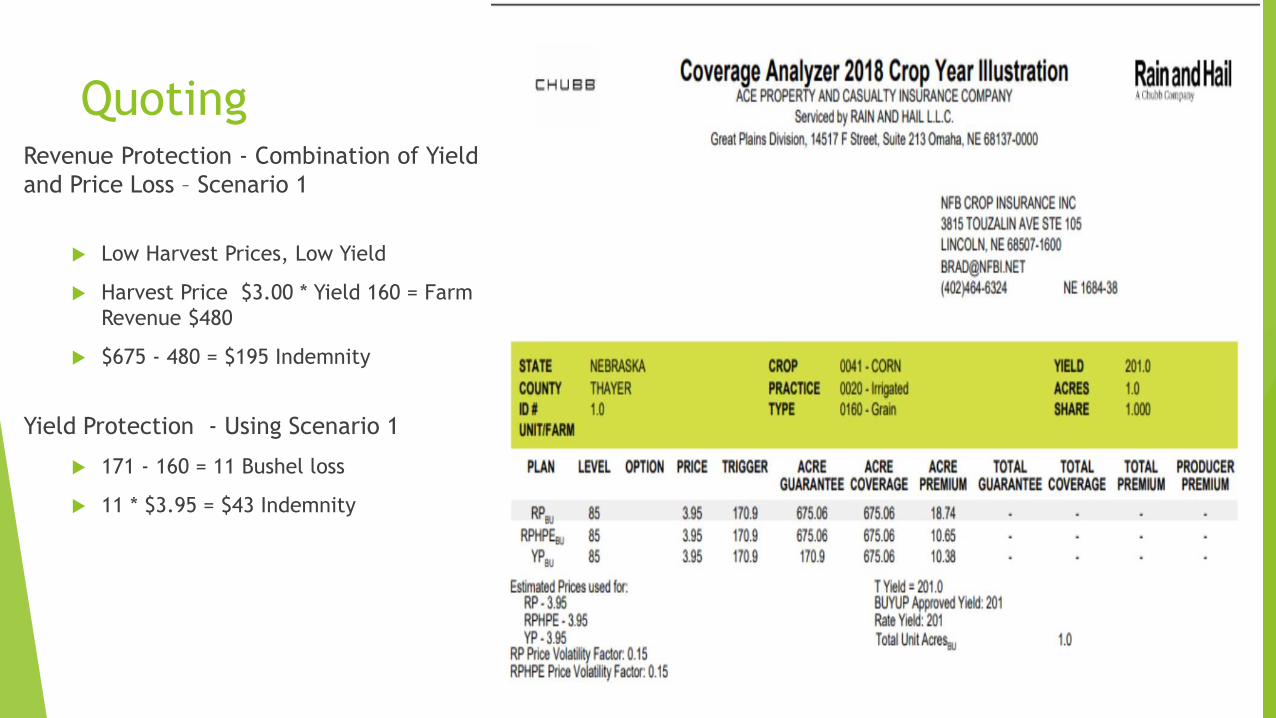

QuotingRevenue Protection - Combination of Yield

and Price Loss – Scenario 1

Low Harvest Prices, Low Yield

Harvest Price $3.00 * Yield 160 = Farm

Revenue $480

$675 - 480 = $195 Indemnity

Yield Protection - Using Scenario 1

171 - 160 = 11 Bushel loss

11 * $3.95 = $43 Indemnity

QuotingRevenue Protection – Scenario 2

Low Prices, Average Yield (Revenue

Loss)

Harvest Price 3.00 * Yield 201 (APH) =

$603

$675 - $603 = $72 Indemnity

Quoting

RPHPE - Does not re figure guarantee

– Using Scenario 3

$675 - $675 = $0 No indemnity

Acreage Reporting How it works?

What to look for when reporting acres?

Be sure to carefully review information

Cross reference Planting Data

If you provide information to FSA first, ensure it matches actual planting data

Will be billed based upon what is submitted

Make sure all persons sharing is accurate

Problems with Acreage Reports

Cannot go back & change easily

Ties into Crop-Hail policy

When reporting production, farmer wants to change acreage

Summary of Coverage

Review, Review, Review

Guarantee How is it figured? Prices and Yield?

If finding error on SOC later in season would have to be inspected, verify

with FSA mapping, increasing liability, late reporting and could be uninsurable

ifloss

Summary of Coverage

Production Reporting

April 30th for previous crop years bushels

Why does a high/low aph matter?

Report IRR and NONIRR separate if you have separate units

Problems

Production Reporting

2. The Yield line will show an “I” next to the year when the yield was imposed (and actual production was not subsequently submitted).

3. Be sure to report production figures on all yield lines with acres! If there is a loss on a policy the insured must report production on all non-loss units by PRD.

What happens when the storm comes?

Claims/Losses? Notify your agent immediately

No cost to have an adjuster look at your crops if you think you have

damage

If you are not sure you have a revenue loss - submit the claim, get

load summary sheets from harvest available, adjust any necessary

bins

Difficult to know if you have an enterprise unit (Practice) loss.

Can miss a claim if you determine a loss and report production

after the claim filing deadline. This happens shortly after

harvest.

If thinking a claim is present prior to replanting or harvesting, be sure

to contact your agent/adjuster. Be sure to leave:

4 rows wide by the length of the field for the first 20 acres

10-foot strip for every 40 acres after that

Is Replanting feasible? Turn in a claim as soon as damage has ocurred.

Determine replant date relative to final planting

dates and late planting period.

Practical to Replant

Is it physically possible to replant acreage

Is seed germination, emergence & formation

of healthy plant likely

It would be practical to replant through the

10th day after the Final Planting Period if the

crop has a LPP of 10 days or more

Is Replanting feasible? cont.

Initial Planting Dates:

Corn April 10th

Soybeans April 25th

Final Planting Dates:

Corn May 25th

Late Planting Period 20 Days after Final Planting Date

Soybeans June 10th

Late Planting Period 25 Days after Final Planting Period

Corn replant payment 8 Bushels * Projected Price 3.95 = $31.60 per

acre

Soybean replant payment 3 Bushels * Projected Price $10.12 =$30.36

per acre

Additional Replant payments with Companion Plan but not Production

Plan

Important that you get approval from the adjuster before you replant

the crops. Could get denied a claim if a farmer replants and doesn't

get approval

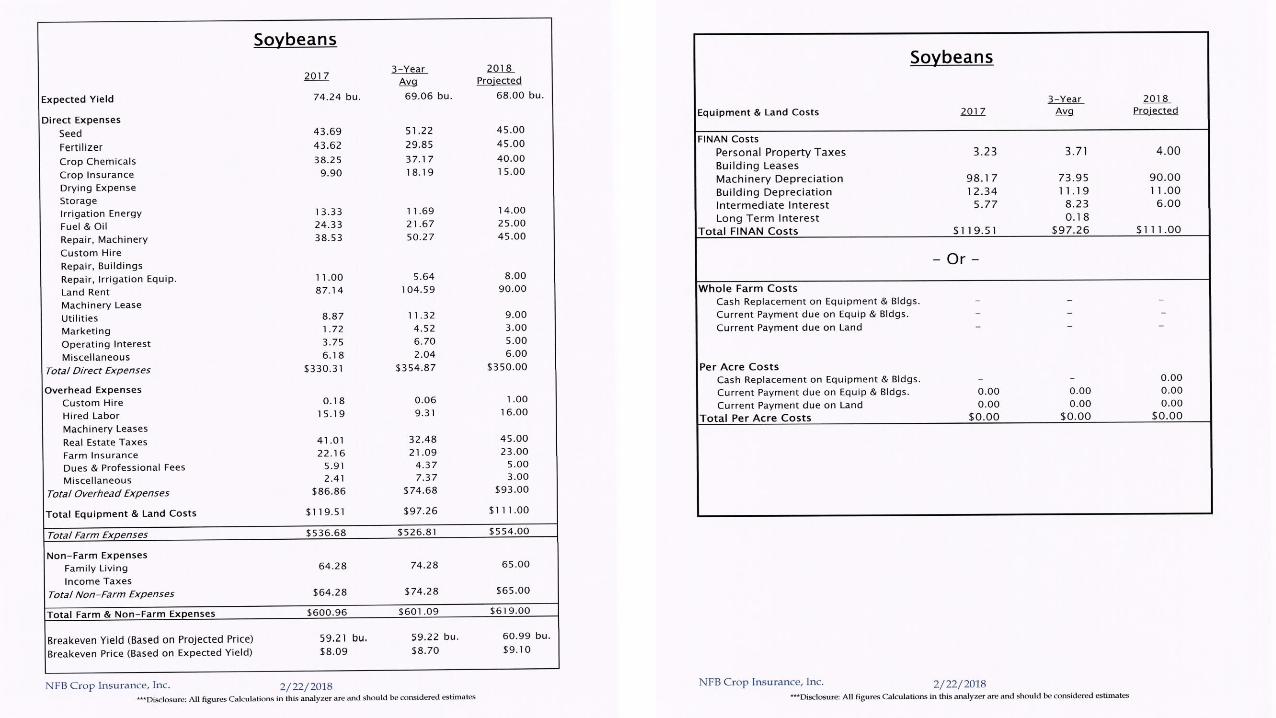

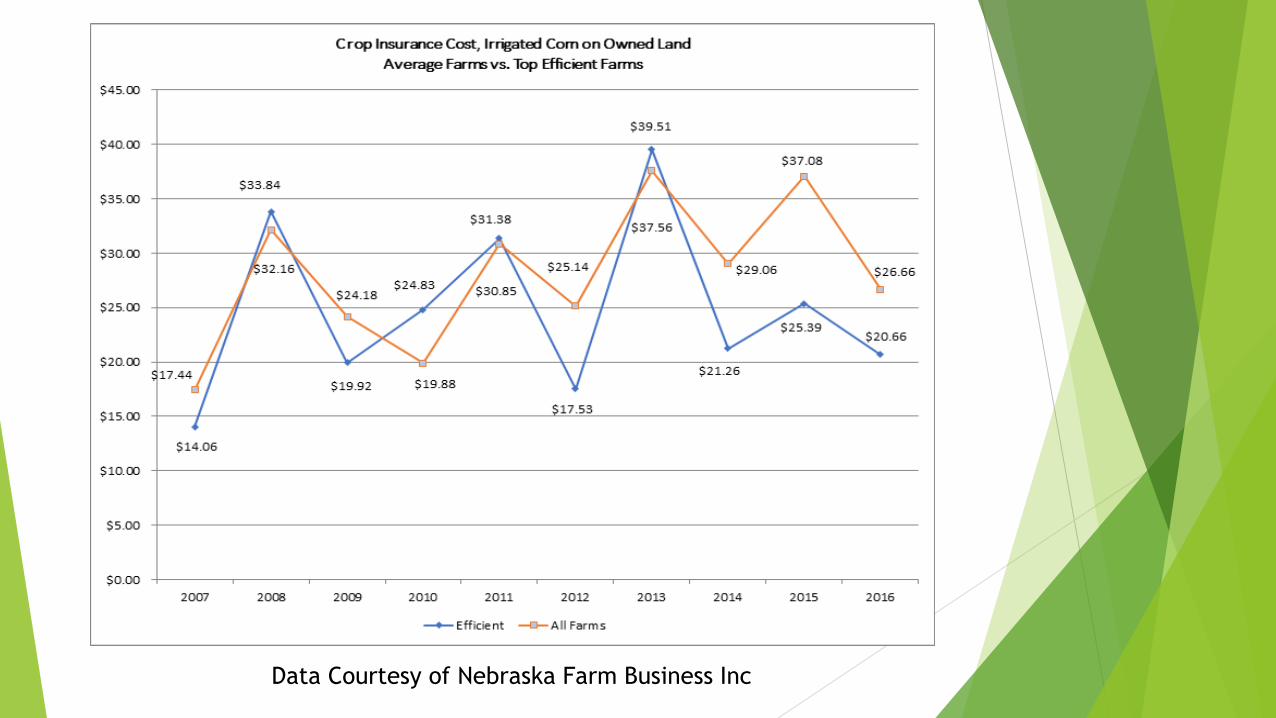

Risk Tolerance

Find out your risk tolerance to find what type of

coverage you want

Utilize a “Crop Insurance Analyzer” at NFB Crop

Insurance with Farm Analysis Information through

NFBI

Data Courtesy of Nebraska Farm Business Inc

2018 Changes to crop insurance

Unit Structure Update

Insured may select an enterprise unit for either Irrigated or non-irrigated practice and choose a different unit structure on the other practice. The insured must meet all the qualifications for the elected unit structure. Example: A producer may have enterprise unit on irrigated ground and optional unit on non-irrigated ground.

Chemical Damage & Crop Insurance

Chemical damage/drift is considered an Unavoidable Uninsurable Cause of Loss. There is no indemnity paid for losses. In 2018 if you receive damage due to chemical or chemical drift the production and acres affected will not be included in the APH database but premium will be assessed. Allows a farmer's APH to not be affected/lowered by the damage. Submit your claim immediately and production from affected area cannot be commingled.

Yield Cup (YC) Option

New to have the option on your policy. It guarantees all insureds will have the maximum APH available for the 2018 Crop Year. Automatically added to NFB Crop Insurance policies

Common Problems

(from the Insurance company perspective)

Ensure interest % are correct when reporting acres

IRR & NON IRR acres correct

Ensure SBI information is correct

POA and Tenant is accurate

Have AD-1026 on file with FSA

Many times “hands are tied” as it is Federally Regulated by RMA

Can only cancel by Sales Closing Date

If Landlord dies, notify agent/company

If losses paid to landlord, Fed government could void any losses and premium

subsidy Have to pay back as Landlord was not alive

WHAT DO YOU WANT TO KNOW??

Write your question! We’ll Answer!!

Thank You!

Contact me for a FREE Policy Review!

Brad Heinrichs, NFB Crop Insurance

402-984-6474

Recommended