fime.com

Enabling nexo standards for payments

May 27, 2020

fime.com

This document is proprietary to FIME and has been furnished on a confidential and restricted basis. FIME expressly reserves all rights, without waiver, election or other limitation to the full extent permitted by law, in and to this material and the information contained herein.

Any reproduction, use or display or other disclosure or dissemination, by any method now known or later developed, of this material or the information contained herein, in whole or in part, without the prior written consent of FIME is strictly prohibited.

FIME accepts no liability for any errors or omissions in this document.

© 2020 FIME. All rights reserved.

FIME within the nexo organization

FIME as Principal Memberparticipates in the work of the organization, with voting rights.

has access to the organization’s deliverables, working documents and reports.

Arnaud Crouzet, FIME VP Consulting,is member of the Board of Directors of nexo organization

450+Experts

9Labs

2Development

centers

40+Industry

accreditations

3000+Customers

18Locations

180Countries

Big enough to be globalsmall enough to be reactive

FIME is a global leader inpayment consulting andsecure transaction testing

We enable our customers to bringuser friendly, reliable and secure solutionsto the Payment and Transport markets.

We are a Trusted Adviser.

We do that by combining our global expertise with disruptive testing.

We go beyond testing.

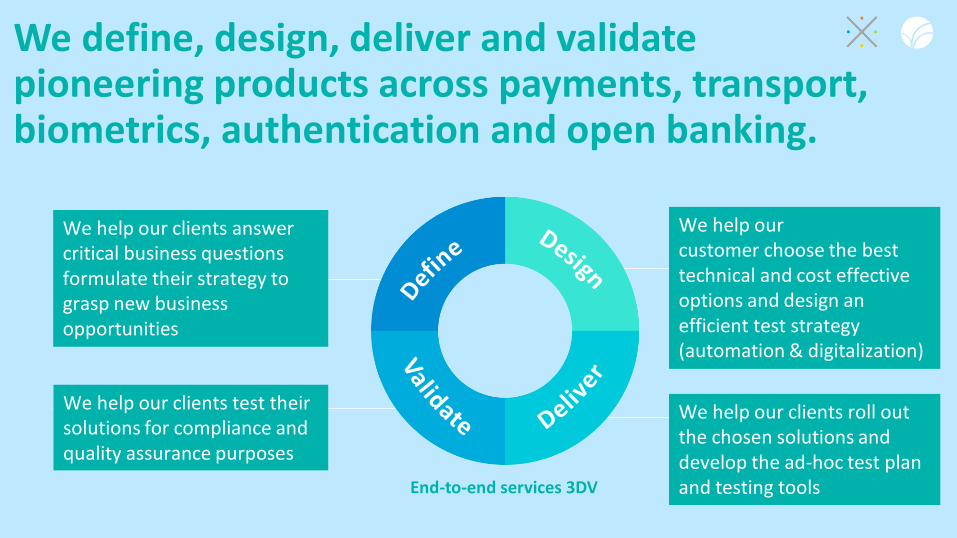

We help our clients answer critical business questions formulate their strategy to grasp new business opportunities

We help our customer choose the best technical and cost effective options and design an efficient test strategy (automation & digitalization)

We help our clients test their solutions for compliance and quality assurance purposes

We help our clients roll out the chosen solutions and develop the ad-hoc test plan and testing tools End-to-end services 3DV

We define, design, deliver and validate pioneering products across payments, transport, biometrics, authentication and open banking.

Welcome from

Claude BrunChairman of nexo standards

nexo standards webinarSPEAKERS PANEL

Ecosystem stakeholders . User experience . Standards . Collaborative . Payments . Acceptors . Processors . Vendors . PSP . Card Schemes . International . ISO20022 . Interoperability . POI . TMS . POS . Acquirer . Foster Innovations .

Arnaud CrouzetVP Consulting

Gomathi Shankar U.Technical PM

Nadine KanaanSenior Consultant

& nexo SME

Sylvain FromagerProject Manager

nexo organization in a nutshell

Benefits for the ecosystem

nexo specifications overview

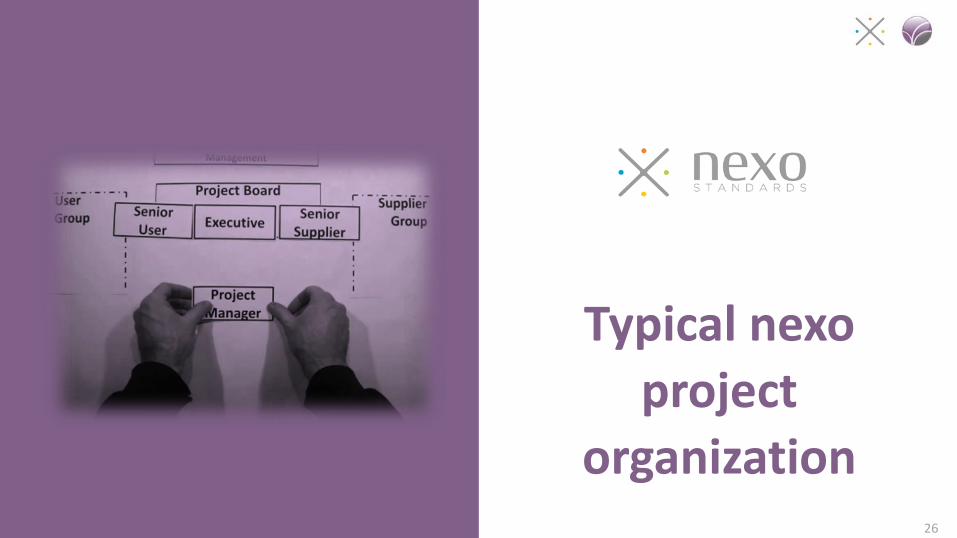

Typical nexo project organization

Case studies

Q&A

Agenda

Creating an international ecosystem for harmonized and interoperable payments

ENABLING GLOBAL INTEROPERABILITY IN PAYMENT ACCEPTANCE

NEXO STANDARDS

• nexo is a not-for-profit, open association; its membership represents the full spectrum of payment stakeholders.

• nexo standards is the association dedicated to removing the barriers present in today’s fragmented global payment acceptance ecosystem.

• It enables fast, borderless and global payments acceptance by standardizing the exchange of data between all payment acceptance stakeholders.

• The nexo specifications and messaging protocols adhere to ISO 20022 standards, are universally applicable and fully open.

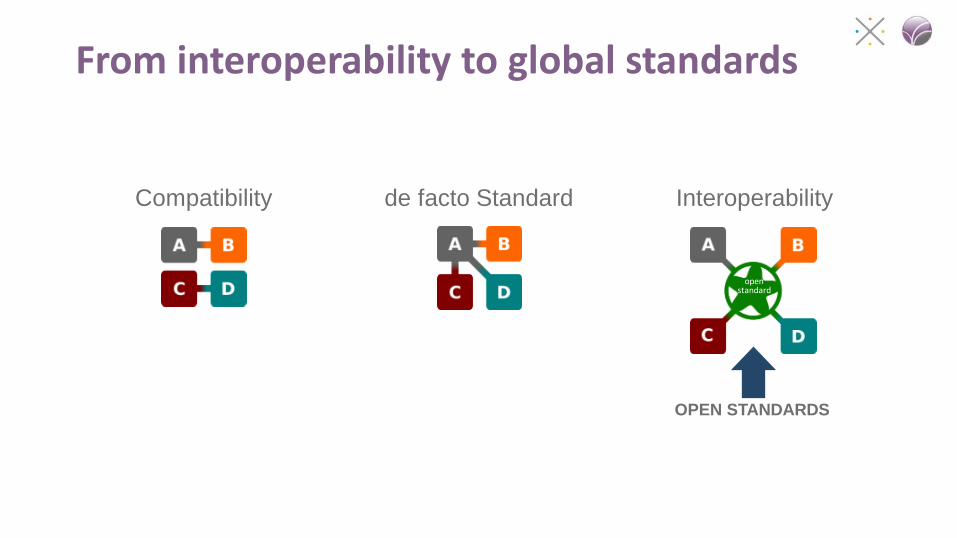

From interoperability to global standards

Compatibility de facto Standard Interoperability

OPEN STANDARDS

openstandard

A worldwide collaborative ecosystem is crucial to representing and addressing the needs of the market

The collaborative ecosystem

nexo members represent the full spectrum of card payment stakeholdersincluding acceptors, processors, vendors, payment service providers and card schemes.

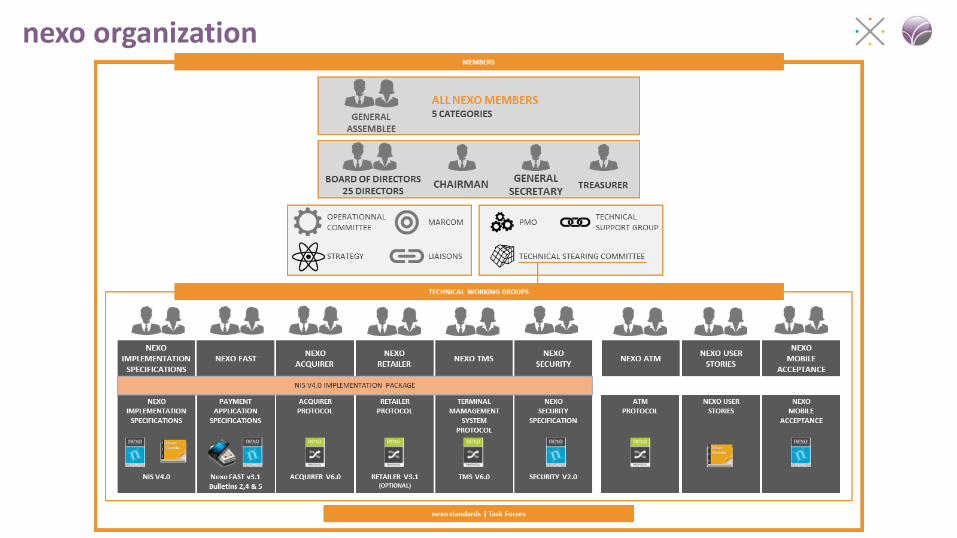

nexo organization

nexo benefits for the

ecosystem

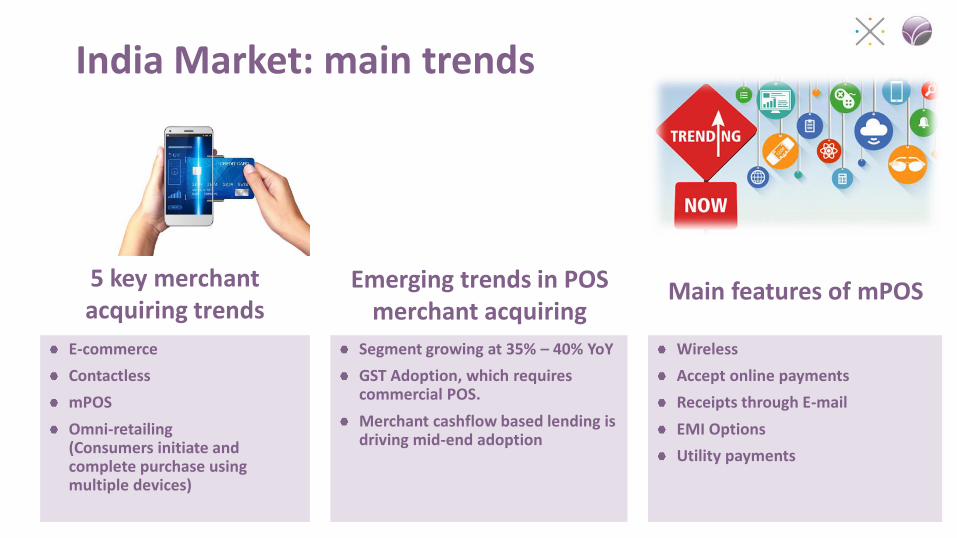

India Market: main trends

E-commerce

Contactless

mPOS

Omni-retailing(Consumers initiate and complete purchase using multiple devices)

Segment growing at 35% – 40% YoY

GST Adoption, which requires commercial POS.

Merchant cashflow based lending is driving mid-end adoption

Wireless

Accept online payments

Receipts through E-mail

EMI Options

Utility payments

5 key merchant acquiring trends

Emerging trends in POS merchant acquiring

Main features of mPOS

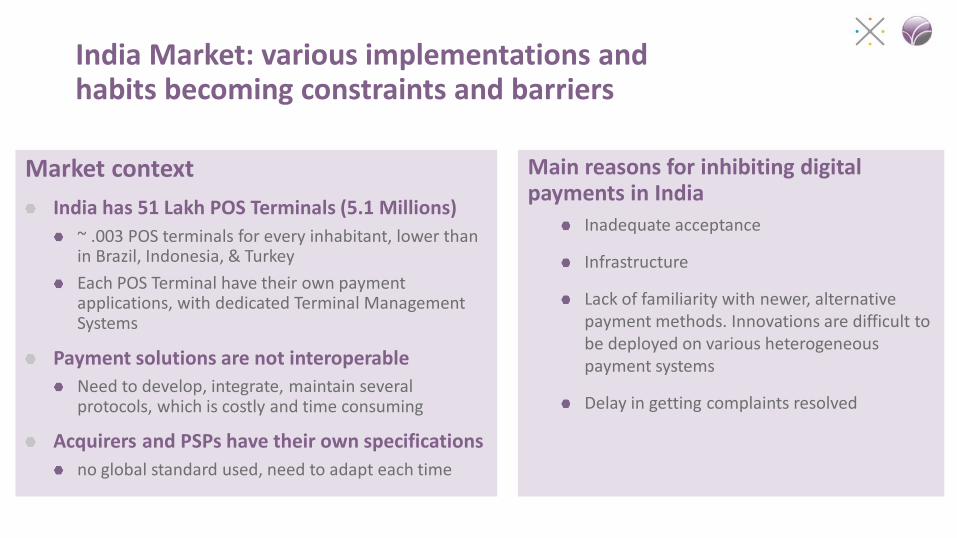

Market context

India has 51 Lakh POS Terminals (5.1 Millions)

~ .003 POS terminals for every inhabitant, lower than in Brazil, Indonesia, & Turkey

Each POS Terminal have their own payment applications, with dedicated Terminal Management Systems

Payment solutions are not interoperable

Need to develop, integrate, maintain several protocols, which is costly and time consuming

Acquirers and PSPs have their own specifications

no global standard used, need to adapt each time

India Market: various implementations and habits becoming constraints and barriers

Main reasons for inhibiting digital payments in India

Inadequate acceptance

Infrastructure

Lack of familiarity with newer, alternative payment methods. Innovations are difficult to be deployed on various heterogeneous payment systems

Delay in getting complaints resolved

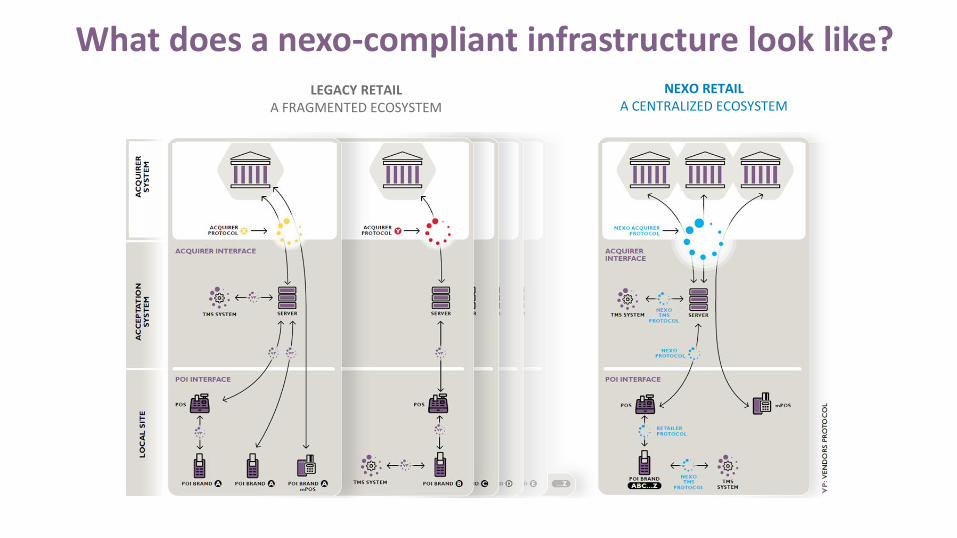

LEGACY RETAILA FRAGMENTED ECOSYSTEM

NEXO RETAILA CENTRALIZED ECOSYSTEM

What does a nexo-compliant infrastructure look like?

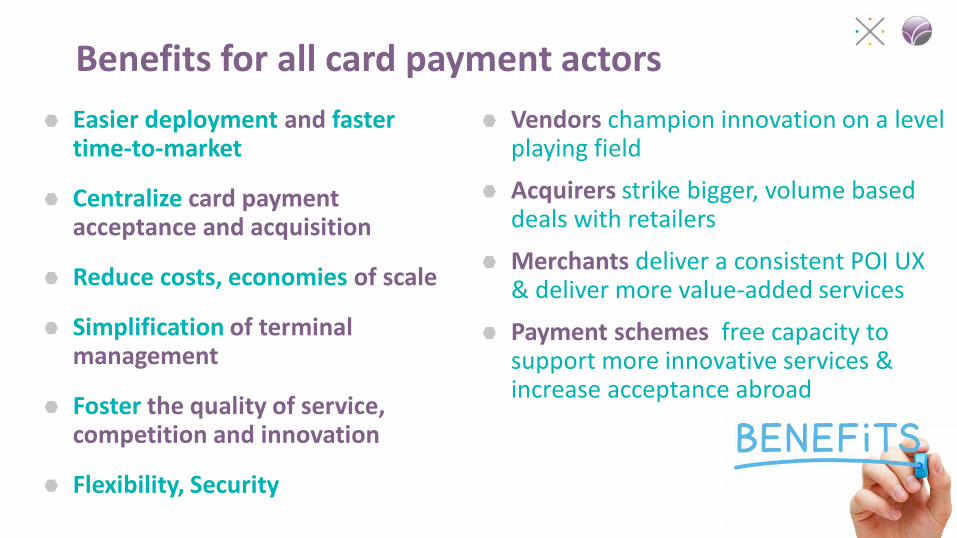

Easier deployment and faster time-to-market

Centralize card payment acceptance and acquisition

Reduce costs, economies of scale

Simplification of terminal management

Foster the quality of service, competition and innovation

Flexibility, Security

Benefits for all card payment actors

Vendors champion innovation on a level playing field

Acquirers strike bigger, volume based deals with retailers

Merchants deliver a consistent POI UX & deliver more value-added services

Payment schemes free capacity to support more innovative services & increase acceptance abroad

22

nexo specifications

overview

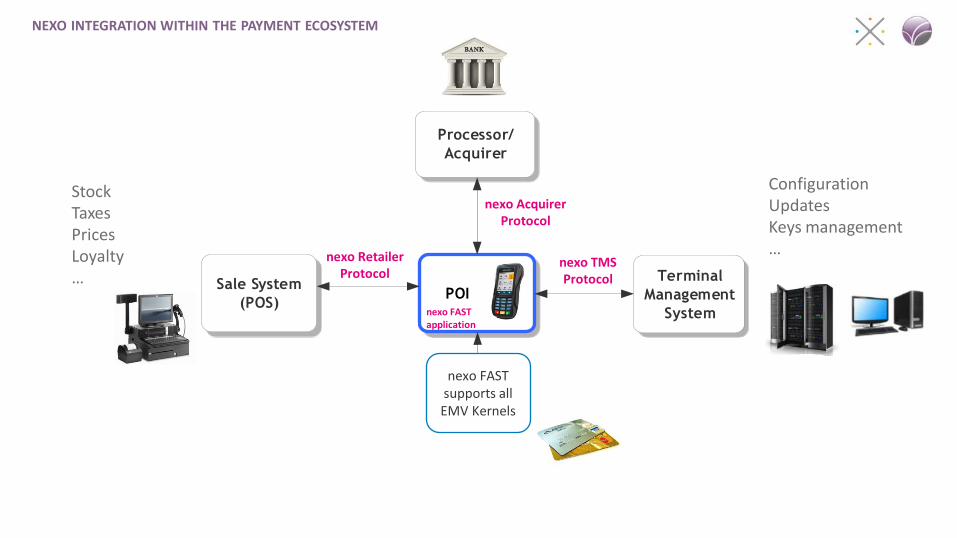

Sale System

(POS) POI

Processor/

Acquirer

Terminal

Management

System

Generic EMV

SDK

Payment

Peripheral

NEXO INTEGRATION WITHIN THE PAYMENT ECOSYSTEM

StockTaxesPricesLoyalty…

Configuration UpdatesKeys management…nexo Retailer

Protocolnexo TMS Protocol

nexo Acquirer Protocol

nexo FAST application

nexo FAST supports all EMV Kernels

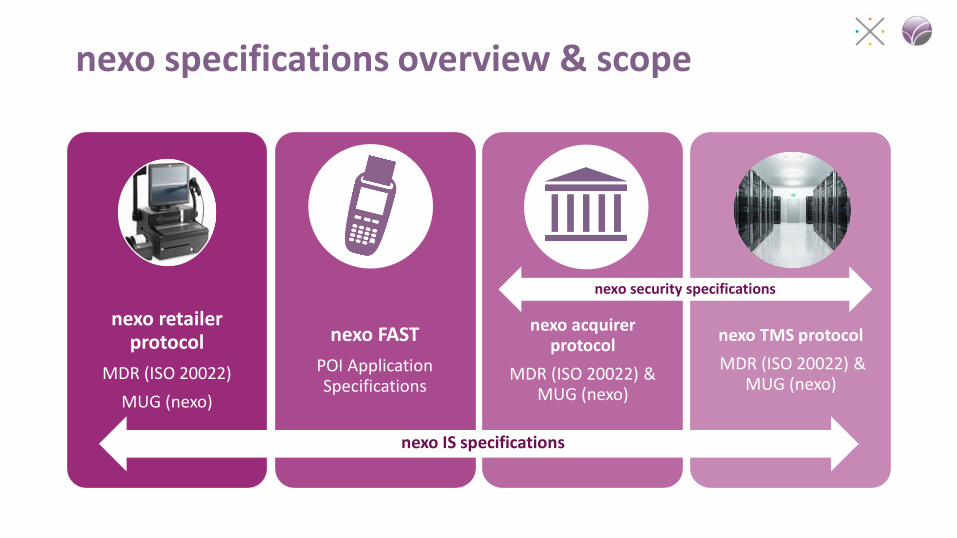

nexo specifications overview & scope

nexo retailer protocol

MDR (ISO 20022)

MUG (nexo)

nexo FAST

POI Application Specifications

nexo acquirer protocol

MDR (ISO 20022) & MUG (nexo)

nexo TMS protocol

MDR (ISO 20022) & MUG (nexo)

nexo IS specifications

nexo security specifications

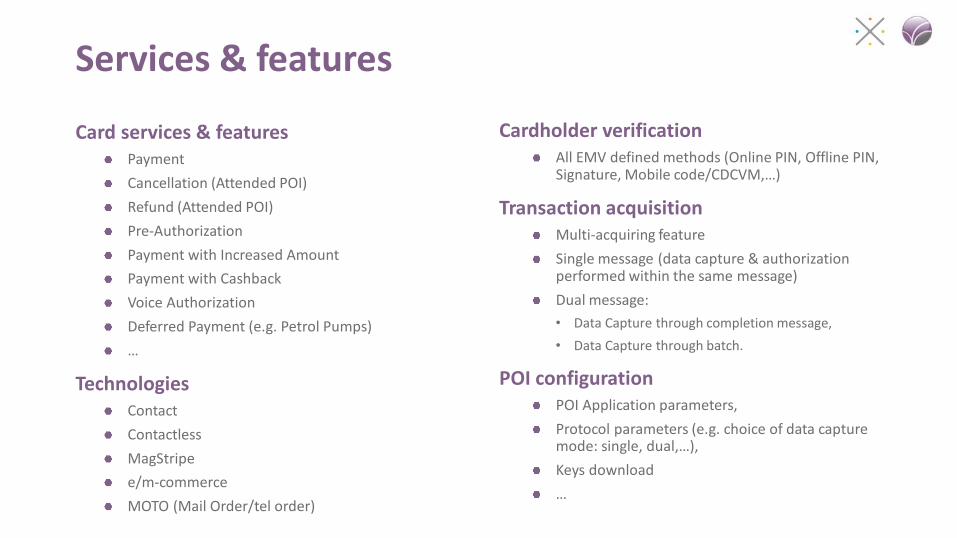

Card services & featuresPayment

Cancellation (Attended POI)

Refund (Attended POI)

Pre-Authorization

Payment with Increased Amount

Payment with Cashback

Voice Authorization

Deferred Payment (e.g. Petrol Pumps)

…

TechnologiesContact

Contactless

MagStripe

e/m-commerce

MOTO (Mail Order/tel order)

Services & features

Cardholder verificationAll EMV defined methods (Online PIN, Offline PIN, Signature, Mobile code/CDCVM,…)

Transaction acquisitionMulti-acquiring feature

Single message (data capture & authorization performed within the same message)

Dual message:

• Data Capture through completion message,

• Data Capture through batch.

POI configurationPOI Application parameters,

Protocol parameters (e.g. choice of data capture mode: single, dual,…),

Keys download

…

26

Typical nexo project

organization

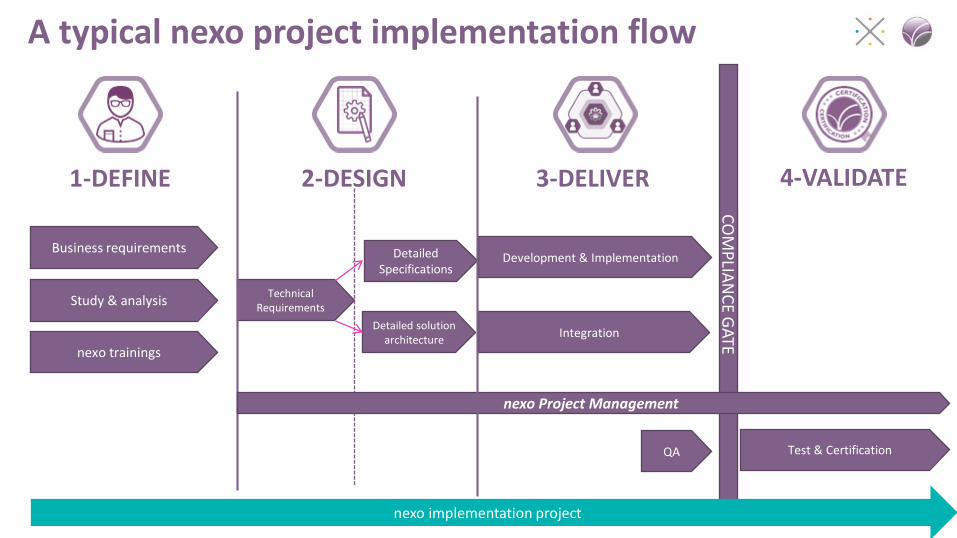

1-DEFINE

Study & analysis

4-VALIDATE

CO

MP

LIAN

CE G

ATE

Test & Certification

nexo implementation project

Business requirements

nexo trainings

A typical nexo project implementation flow

2-DESIGN

Technical Requirements

Detailed Specifications

Detailed solution architecture

3-DELIVER

QA

nexo Project Management

Development & Implementation

Integration

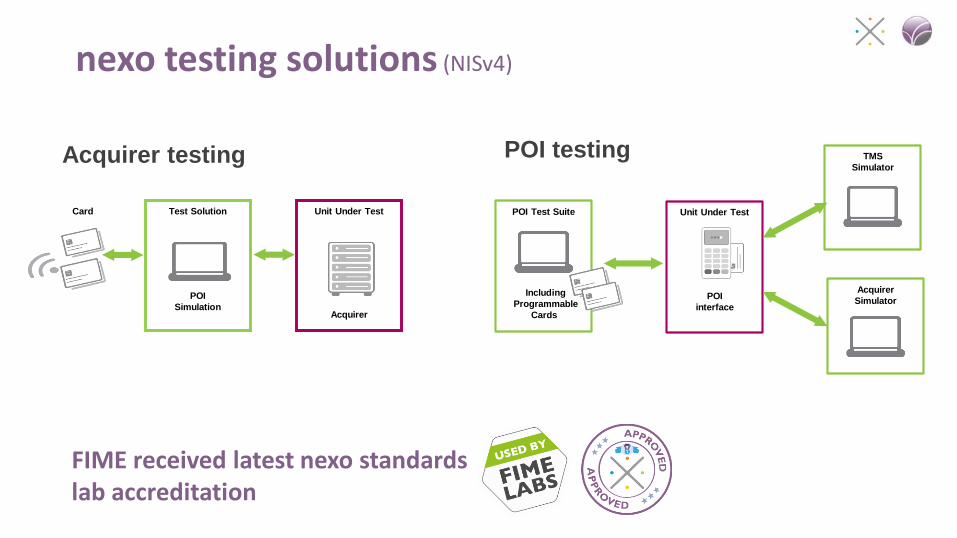

nexo testing solutions (NISv4)

Acquirer testing POI testing

Card Unit Under Test

Acquirer

Test Solution

POI

Simulation

Acquirer

Simulator

Unit Under Test

POI

interface

POI Test Suite

Including

Programmable

Cards

TMS

Simulator

FIME received latest nexo standards lab accreditation

29

Cases studies

nexo case studies

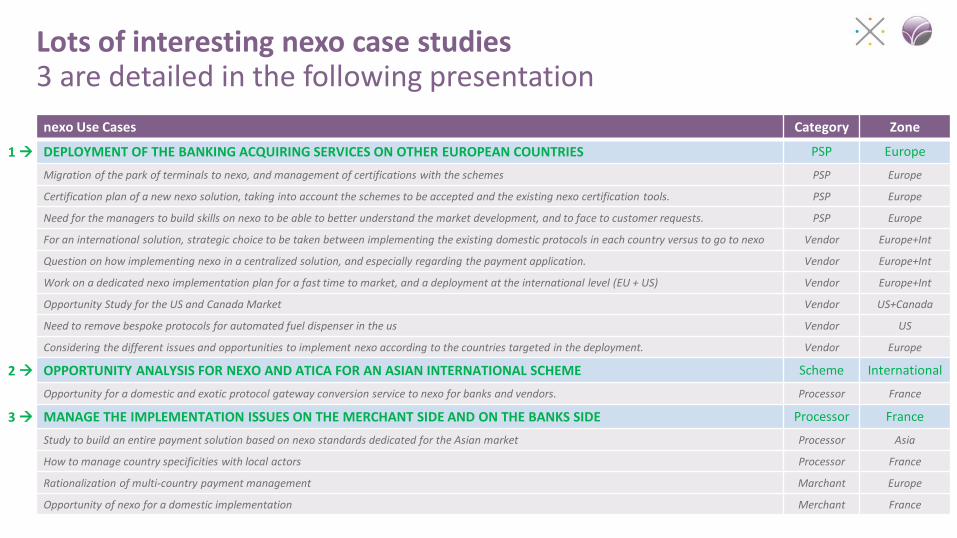

Lots of interesting nexo case studies3 are detailed in the following presentation

nexo Use Cases Category Zone

1 DEPLOYMENT OF THE BANKING ACQUIRING SERVICES ON OTHER EUROPEAN COUNTRIES PSP Europe

Migration of the park of terminals to nexo, and management of certifications with the schemes PSP Europe

Certification plan of a new nexo solution, taking into account the schemes to be accepted and the existing nexo certification tools. PSP Europe

Need for the managers to build skills on nexo to be able to better understand the market development, and to face to customer requests. PSP Europe

For an international solution, strategic choice to be taken between implementing the existing domestic protocols in each country versus to go to nexo Vendor Europe+Int

Question on how implementing nexo in a centralized solution, and especially regarding the payment application. Vendor Europe+Int

Work on a dedicated nexo implementation plan for a fast time to market, and a deployment at the international level (EU + US) Vendor Europe+Int

Opportunity Study for the US and Canada Market Vendor US+Canada

Need to remove bespoke protocols for automated fuel dispenser in the us Vendor US

Considering the different issues and opportunities to implement nexo according to the countries targeted in the deployment. Vendor Europe

2 OPPORTUNITY ANALYSIS FOR NEXO AND ATICA FOR AN ASIAN INTERNATIONAL SCHEME Scheme International

Opportunity for a domestic and exotic protocol gateway conversion service to nexo for banks and vendors. Processor France

3 MANAGE THE IMPLEMENTATION ISSUES ON THE MERCHANT SIDE AND ON THE BANKS SIDE Processor France

Study to build an entire payment solution based on nexo standards dedicated for the Asian market Processor Asia

How to manage country specificities with local actors Processor France

Rationalization of multi-country payment management Marchant Europe

Opportunity of nexo for a domestic implementation Merchant France

CASE STUDY Deployment of the banking acquiring services on other countries

Processor

Acquiring bank with two main activities:• Direct POS terminal management• Acquiring services

Willingness to expand their services in other countries

For those who discover nexo for the first time, it may not be easy to well understand the standards (several nexo components, Lot of technical specifications).

• The initial training allowed managers to understand nexo, in a concrete and updated way, with key business objectives.

• Additional expertise to support the bank's technical experts, and to write adapted specifications to their own needs for implementation.

• Step 1: To take a step back and to identify the main activities that are interesting to develop outside of their country + educational support & training

• Step 2: Analysis with action plan to shorten time to market and to faster responses

• Step 3: Decision -> Two steps implementationThe implementation of the nexo acquirer FIRST.The POS terminal will be upgraded to nexo later.

Return of experienceActions

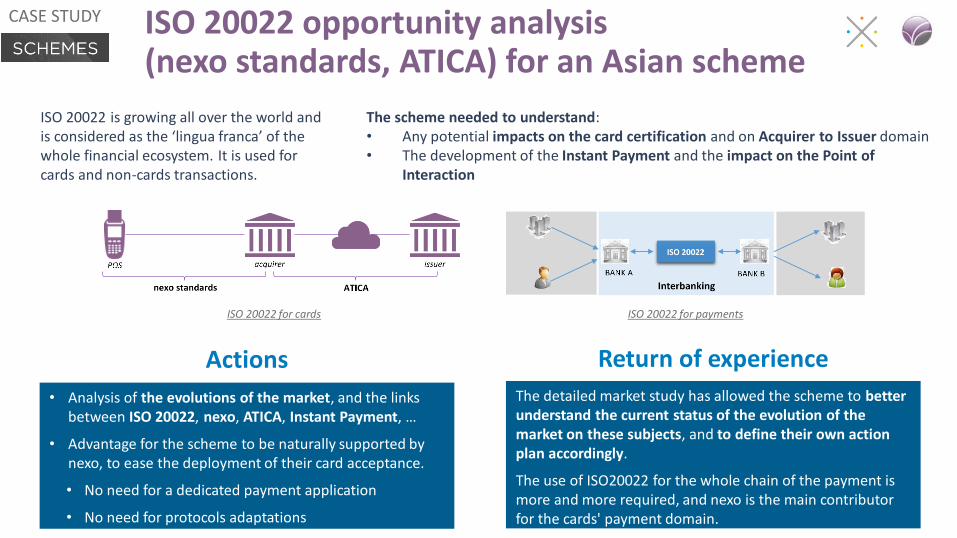

ISO 20022 opportunity analysis(nexo standards, ATICA) for an Asian scheme

ISO 20022 is growing all over the world and is considered as the ‘lingua franca’ of the whole financial ecosystem. It is used for cards and non-cards transactions.

The detailed market study has allowed the scheme to better understand the current status of the evolution of the market on these subjects, and to define their own action plan accordingly.

The use of ISO20022 for the whole chain of the payment is more and more required, and nexo is the main contributor for the cards' payment domain.

• Analysis of the evolutions of the market, and the links between ISO 20022, nexo, ATICA, Instant Payment, …

• Advantage for the scheme to be naturally supported by nexo, to ease the deployment of their card acceptance.

• No need for a dedicated payment application

• No need for protocols adaptations

Return of experienceActions

ISO 20022 for cards ISO 20022 for payments

The scheme needed to understand:• Any potential impacts on the card certification and on Acquirer to Issuer domain• The development of the Instant Payment and the impact on the Point of

Interaction

CASE STUDY

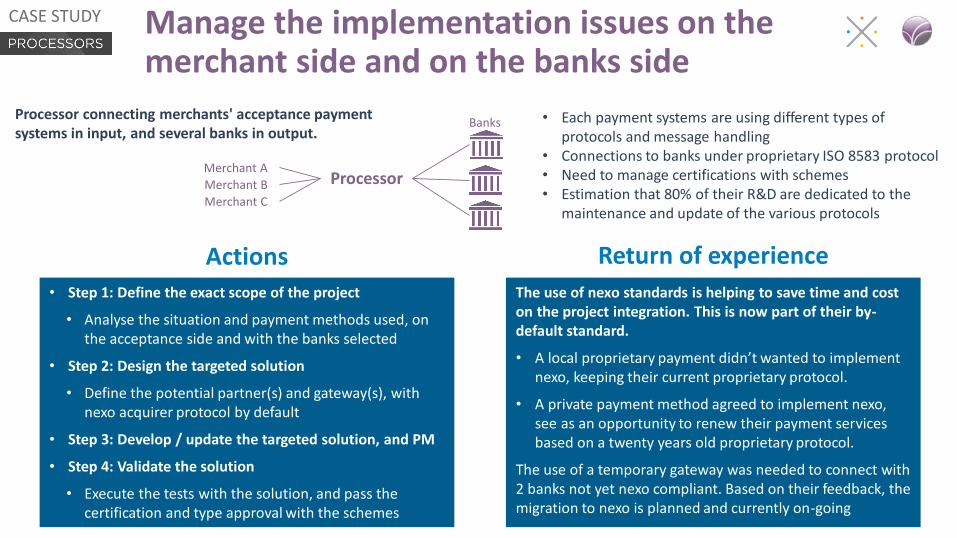

Manage the implementation issues on the merchant side and on the banks side

ProcessorMerchant A

Merchant B

Merchant C

Banks • Each payment systems are using different types of protocols and message handling

• Connections to banks under proprietary ISO 8583 protocol• Need to manage certifications with schemes• Estimation that 80% of their R&D are dedicated to the

maintenance and update of the various protocols

The use of nexo standards is helping to save time and cost on the project integration. This is now part of their by-default standard.

• A local proprietary payment didn’t wanted to implement nexo, keeping their current proprietary protocol.

• A private payment method agreed to implement nexo, see as an opportunity to renew their payment services based on a twenty years old proprietary protocol.

The use of a temporary gateway was needed to connect with 2 banks not yet nexo compliant. Based on their feedback, the migration to nexo is planned and currently on-going

• Step 1: Define the exact scope of the project

• Analyse the situation and payment methods used, on the acceptance side and with the banks selected

• Step 2: Design the targeted solution

• Define the potential partner(s) and gateway(s), with nexo acquirer protocol by default

• Step 3: Develop / update the targeted solution, and PM

• Step 4: Validate the solution

• Execute the tests with the solution, and pass the certification and type approval with the schemes

Return of experienceActions

Processor connecting merchants' acceptance payment systems in input, and several banks in output.

CASE STUDY

Return on experience

nexo standards implementations are successful and are more and more requested in various part of the world

Europe, India, Asia, Africa, US, Canada, Russia

nexo is not just a technical approach,it's mostly a business one.

As nexo specifications are very technical, it is important to understand the business requirements of the customer to define the adapted strategic plan for the nexo deployment.

Thank you

Recommended