7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 1/15

IAB L 3FINANCIAL STATEMENTS FOR SOLE

TRADERS

1

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 2/15

This book was prepared for Home iLearn Ltd.

It is part of a series of chapters developed for the course on ACCA F6 and is published by Home iLearn

Ltd.

Home iLearn Ltd

6! "ath #oad

Cranford$ HounslowT%& '()

www.homeilearn.com

* Home iLearn +!,-

All rihts reserved. /o part of this work may be reproduced in any form$ or by any means$ without

permission in writin from the author.

2

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 3/15

Table of Contents

9 FINANCIAL STATEMENTS FOR SOLE TRADERS 4

SOLE TRADERS..........................................................................4

FINANCIAL STATEMENTS FOR SOLE TRADER................................4

OTHER ITEMS IN FINANCIAL STATEMENTS....................................7

SUMMARY OF YEAR END ADJUSTMENTS FOR FINANCIAL

STATEMENTS...........................................................................

!RE!ARIN" FINANCIAL STATEMENT FROM THE E#TENDED TRIAL

$ALANCE.................................................................................%

3

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 4/15

9 FINANCIAL STATEMENTS FOR SOLETRADERS

O&ER&IE'

This chapter is about preparing fnancial statements or a single

owner o a business, called a sole trader.

SOLE TRADERS

A sole trader is a business in which there is onl one owner who has

complete control o!er the business and its management.

The legal ownership structure does not di"erentiate between the

owner and the business entit #although rom an accounting

perspecti!e it does$. All the profts, losses, assets and liabilities are

thus the direct responsibilit and entitlement o the owner. This

means that an liabilit o the business is also the responsibilit o

the owner #unli%e a compan$.

AD&ANTA"ES DISAD&ANTA"ES

• &ase o ormation and

dissolution

• 'imple to run

• Low start(up costs

• Low operational o!erheads

• )ewer regulations

• *ontrol o!er the business

operations

• +wnership o all profts

• nlimited liabilit- +wners are

personall responsible or the

obligations and liabilities o

the business

• +wner is liable or the actions

o emploees representing

the business

• Limited lie- I the owner dies,

the business dies too

• suall it is dicult or the

owner to raise unds or

e/pansion

FINANCIAL STATEMENTS FOR SOLE TRADER

The fnancial accounts or sole traders comprise o the ollowing

statements-

0

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 5/15

• Income 'tatement

• 'tatement o )inancial osition

e introduced these statements in the pre!ious unit, Accounts

reparation. e will now ta%e a closer loo% at each o them.

THE INCOME STATEMENT

The Income 'tatement shows the proft and loss o a business o!er

an accounting period. It is tpicall prepared on an annual, uarterl

or monthl basis.

An e/ample o an Income 'tatement is shown below-

In(o)e State)ent fo* Yea* En+e+ , De( %-#%Sales /0--+pening in!entor 1,044urchases 02,544*losing in!entor #2,444$Less- *ost o sales #01,644$"*oss 1*o2t 30-ages #07,444$Insurance #6,444$8epreciation e/pense #3,544$Irreco!erable debts #3,044$

Net loss fo* ea* 54307-6

Note: the Income Statement relates to a period e.g. sales

and profts or a whole month or a whole year

Co)1onents of an In(o)e State)ent

• Sales- the cash generated b a business through sales o goods.

Also called re!enues.

• Cost of oo+s sol+8 cost o sales comprise opening in!entor

plus purchases less closing in!entor. urchases comprise goods

directl related to what is being sold #e.g. boo%s that are bought

b a boo% retailer rom a supplier$.

• "*oss 1*o2t8 the di"erence between sales and cost o goods

sold.

• E1enses8 whereas cost o sales relates directl to what is being

sold, e/penses relate to all other e/penditure and o!erheads

#rent, rates, oce costs, emploee costs, insurance etc$.

• Net 1*o2t8 9et proft shows the o!erall proftabilit o the

business. It is eual to :sales less cost o sales less e/penses;.

5

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 6/15

STATEMENT OF FINANCIAL !OSITION

The 'tatement o )inancial osition summarises the assets and

liabilities o a business. This includes both non(current #o!er a ear$

and current #under a ear$ assets and liabilities.

A 'tatement o )inancial osition is shown below-

State)ent of F:nan(:al !os:t:on at , De( %-#%

Non;(<**ent assets

8eli!er !ans 4%0--

C<**ent assets

In!entor Trade recei!ables

Less allowance or doubtul debts

repaments

*ash

2,44414,044

#3,344$

1,444

15,544%03--

Total assets 3/0--

C<**ent l:ab:l:t:es

Trade paables

Accruals

#6,354$

#12,444$5%0,-6

Non;(<**ent l:ab:l:t:es

Ban% loan 5%0--6Total l:ab:l:t:es 5430/-6

Net assets %0%-

*apital < at beginning o ear =6,444roft>loss or ear

8rawings

#0=,754$

#1,444$Ca1:tal %0%-

Note: the Statement o Financial Position relates to a

particular point/day in time (NO a period!

Liabilities are subtracted rom assets to gi!e a business?s :net

assets; #top hal o statement$. This euals :capital" #shown b

the bottom hal o this statement$ which is the amount o mone

in!ested b the owner #includes profts that the owner has earned

reduced b drawings ta%en out b the owner$.

This is summarised in the Accounting &uation-

Assets = L:ab:l:t:es > Ca1:tal 5t?:s also e@<als Net Assets6

=

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 7/15

Assets = L:ab:l:t:es > Ca1:tal !*o2t = D*aB:ns

ASSETS

• Non;(<**ent assets8 Assets that are used primaril or carring

out business acti!ities and are not e/pected to be con!erted into

cash, irrespecti!e o their !alue, in the due course o time.

suall held or greater than 1 ear e.g. plant, machiner,

computers, urniture, building, land, !ehicles.

• C<**ent assets8 These are short term assets, which can be

readil con!erted to cash within 1 ear e.g. cash, in!entor,

accounts recei!ables.

LIA$ILITIES

The obligation o paing a debt that a compan owes to an e/ternal

part is %nown as liabilities. The e/ternal parties are usuall the

sta%eholders li%e ban%s and creditors #also called paables$.

Liabilities are usuall show up in the orm o unpaid bills>in!oices or

loans that a compan is bound to pa. *lassifcation o liabilities is

as ollows-

•

C<**ent l:ab:l:t:es8 'hort term liabilities that are paable within1 ear eg. +!er drat, accounts paable, accruals.

• Non;(<**ent l:ab:l:t:es8 Long term liabilities that are due in

greater than 1 ear e.g. ban% loans.

O'NERS EUITY OR CA!ITAL

This shows the amount o in!estment that the owner has made in

the business. As shown abo!e in the Accounting &uation, it is a

combination o the amount that the owner has in!ested in the

business #opening capital$ plus profts less drawings #amounts

withdrawn b the owner$.

OTHER ITEMS IN FINANCIAL STATEMENTS

There are a number o other double entr balances that ma ha!e

to be transerred into the income statement. These include-

7

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 8/15

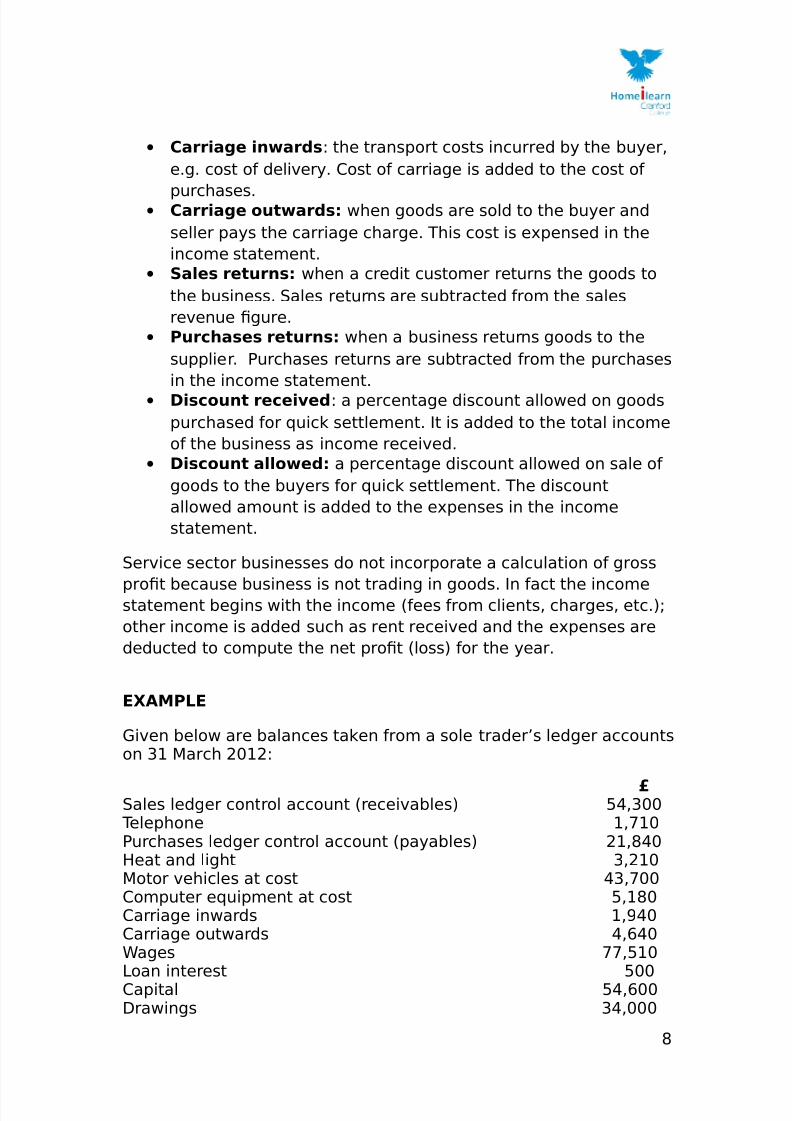

• Ca**:ae :nBa*+s- the transport costs incurred b the buer,

e.g. cost o deli!er. *ost o carriage is added to the cost o

purchases.• Ca**:ae o<tBa*+s8 when goods are sold to the buer and

seller pas the carriage charge. This cost is e/pensed in the

income statement.

• Sales *et<*ns8 when a credit customer returns the goods to

the business. 'ales returns are subtracted rom the sales

re!enue fgure.

• !<*(?ases *et<*ns8 when a business returns goods to the

supplier. urchases returns are subtracted rom the purchases

in the income statement.

• D:s(o<nt *e(e:e+- a percentage discount allowed on goods

purchased or uic% settlement. It is added to the total income

o the business as income recei!ed.

• D:s(o<nt alloBe+8 a percentage discount allowed on sale o

goods to the buers or uic% settlement. The discount

allowed amount is added to the e/penses in the income

statement.

'er!ice sector businesses do not incorporate a calculation o gross

proft because business is not trading in goods. In act the incomestatement begins with the income #ees rom clients, charges, etc.$@

other income is added such as rent recei!ed and the e/penses are

deducted to compute the net proft #loss$ or the ear.

E#AM!LE

i!en below are balances ta%en rom a sole trader?s ledger accountson 31 arch 2412-

'ales ledger control account #recei!ables$ 50,344 Telephone 1,714urchases ledger control account #paables$ 21,C04Deat and light 3,214otor !ehicles at cost 03,744*omputer euipment at cost 5,1C4*arriage inwards 1,604*arriage outwards 0,=04ages 77,514Loan interest 544*apital 50,=448rawings 30,444

C

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 9/15

Allowance or doubtul debts 5C4Ban% o!erdrat 0,704urchases 23=,744

ett cash =4'ales 022,454Insurance 0,5=4Accumulated depreciation < motor !ehicles 13,244Accumulated depreciation < computer euipment 3,404'toc% at 1 April 2447 20,544Loan C,144Eent 35,=04

INCOME STATEMENT

In(o)e state)ent fo* M:lton Te(?nolo:es fo* t?e ea*

en+e+ ,st Ma*(? %-%

'ales

Less- *ost o sales

+pening 'toc%

*arriage inwards

urchases

Less- *losing stoc%

ross roft

Less- &/penses

Telephone

Deat and light

*arriage outwards

ages

Loan interest

Insurance

Eent

8epreciation(otor !ehicles

8epreciation(*omputer euipment

Irreco!erable debts

Allowance or doubtul debt

adFustment

Total e/penses

Net !*o2t

20,544

1,604

23=,7442=3,104

#15,C44$

1,C64

3,214

0=04

77,514544

3,624

35,=04

12,074

644

544

124

022,454

207,304

170,714

101344

,,04-

6

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 10/15

STATEMENT OF FINANCIAL !OSITION

$alan(e S?eet of M:lton Te(?nolo:es as at , Ma*(? %-%Cost A((<)<late+

De1*e(:at:on

Net booG

&al<e

F:e+ Assets

otor !ehicles 03,744 20,C74 1C,C34*omputer euipment 5,1C4 3,604 1,204

0C,CC4 2C,C14 24,474

C<**ent Assets'toc% 15,C448ebtors 53,=44Less allowance or

doubtul debts

#734$ =C,=74

repaments 564ett cash =4 =6,324C<**ent L:ab:l:t:es 5;6Ban% o!erdrat 0,704*reditors 21,C04Accruals 7,44 27,2C4

*urrent assets 02,404Net C<**ent Assets

#Total assets less

current liabilities$

=2,114

Long term liabilit-Loan #C,144$Net assets 40--Ca1:tal+pening capital 50=449et proft or the

ear

33,014

CC,414Less drawings #30,444$!*o1*:eto*s f<n+s 40--

SUMMARY OF YEAR END ADJUSTMENTS FOR

FINANCIAL STATEMENTS

ADJUSTMENTS FINANCIAL STATEMENTClos:n :nento* *losing in!entor is deducted rom purchases

14

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 11/15

in the income statement and classifed as

current asset in the statement o fnancial

position

A((*<e+ e1enses Accrued e/penses are e/pensed in the income

statement and classifed as current liabilit in

the statement o fnancial position!*e1a:+ e1enses repaid e/penses are deducted rom the total

e/penses in the income statement and

classifed as current asset in the statement o

fnancial positionA((*<e+ :n(o)e Accrued income is added to the income o the

business and shown as current asset in the

statement o fnancial position

!*e1a:+ :n(o)e repaid income is deducted rom income o thebusiness and shown as current liabilit in the

statement o fnancial positionDe1*e(:at:on an+

a((<)<late+

+e1*e(:at:on

8epreciation charge is e/pensed in the income

statement and accumulated depreciation

reduces the cost o non current asset to gi!e

carring amountD:s1osal of non

(<**ent assets

ain #loss$ on disposal is treated as income

#e/pense$ in the income statement and

disposal reduces the amount o non current

assetsI**e(oe*able +ebts These are treated as an e/pense and the trade

recei!ables fgure is reduced b the amount o

irreco!erable debtC*eat:on:n(*ease :n

alloBan(e fo* +o<btf<l

+ebts

Increase in allowance or doubtul debts is

treated as an e/pense and trade recei!able

fgure is reduced b the total amount o

allowanceDe(*ease :n alloBan(e

fo* +o<btf<l +ebts

8ecrease in allowance or doubtul debts is

treated as an income and trade recei!able

fgure is reduced b the total amount o

allowanceD*aB:ns 8rawings are deducted rom purchases in the

income statement and added to Gdrawings? in

the statement o fnancial position

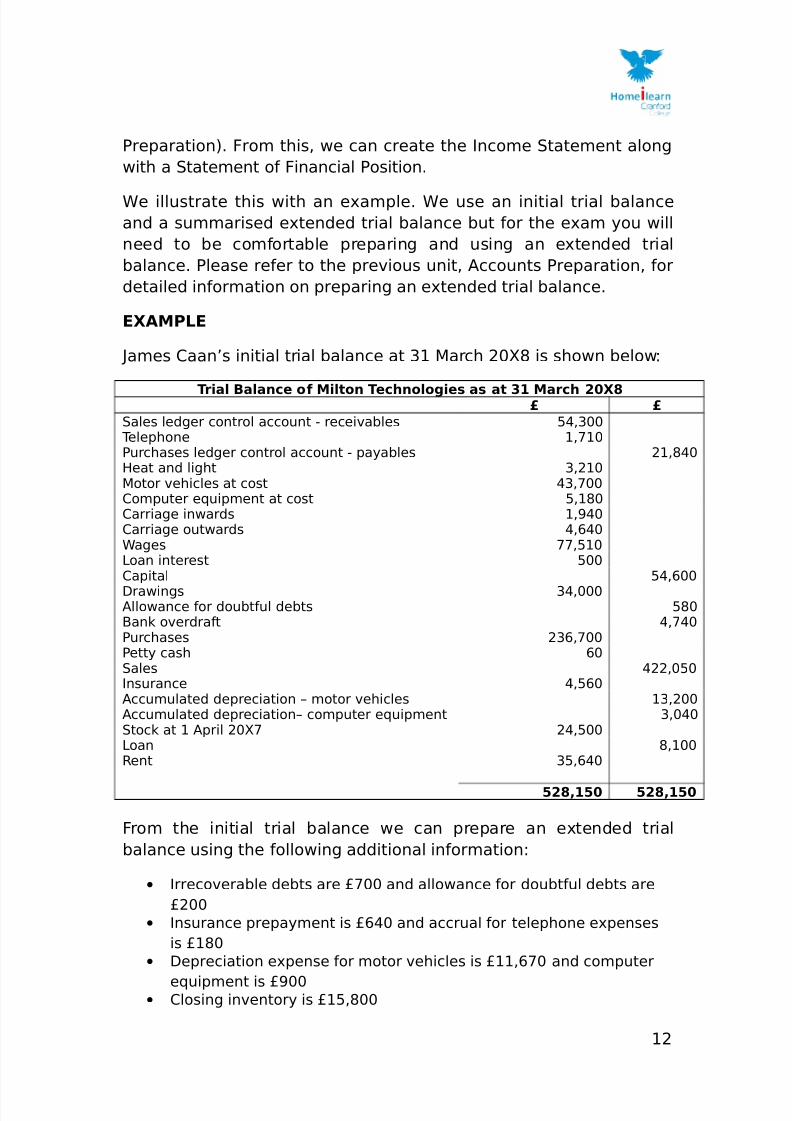

!RE!ARIN" FINANCIAL STATEMENT FROM THE

E#TENDED TRIAL $ALANCE

The fnal accounts o a sole trader in!ol!e the preparation o an

e/tended trial balance #as we co!ered in the unit, Accounts

11

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 12/15

reparation$. )rom this, we can create the Income 'tatement along

with a 'tatement o )inancial osition.

e illustrate this with an e/ample. e use an initial trial balance

and a summarised e/tended trial balance but or the e/am ou will

need to be comortable preparing and using an e/tended trial

balance. lease reer to the pre!ious unit, Accounts reparation, or

detailed inormation on preparing an e/tended trial balance.

E#AM!LE

Hames *aan?s initial trial balance at 31 arch 24C is shown below-

T*:al $alan(e of M:lton Te(?nolo:es as at , Ma*(? %-#/

'ales ledger control account ( recei!ables 50,344 Telephone 1,714urchases ledger control account ( paables 21,C04Deat and light 3,214otor !ehicles at cost 03,744*omputer euipment at cost 5,1C4*arriage inwards 1,604*arriage outwards 0,=04ages 77,514Loan interest 544*apital 50,=44

8rawings 30,444Allowance or doubtul debts 5C4Ban% o!erdrat 0,704urchases 23=,744ett cash =4'ales 022,454Insurance 0,5=4Accumulated depreciation < motor !ehicles 13,244Accumulated depreciation< computer euipment 3,404'toc% at 1 April 247 20,544Loan C,144Eent 35,=04

%/0- %/0-

)rom the initial trial balance we can prepare an e/tended trial

balance using the ollowing additional inormation-

• Irreco!erable debts are J744 and allowance or doubtul debts are

J244

• Insurance prepament is J=04 and accrual or telephone e/penses

is J1C4

• 8epreciation e/pense or motor !ehicles is J11,=74 and computer

euipment is J644• *losing in!entor is J15,C44

12

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 13/15

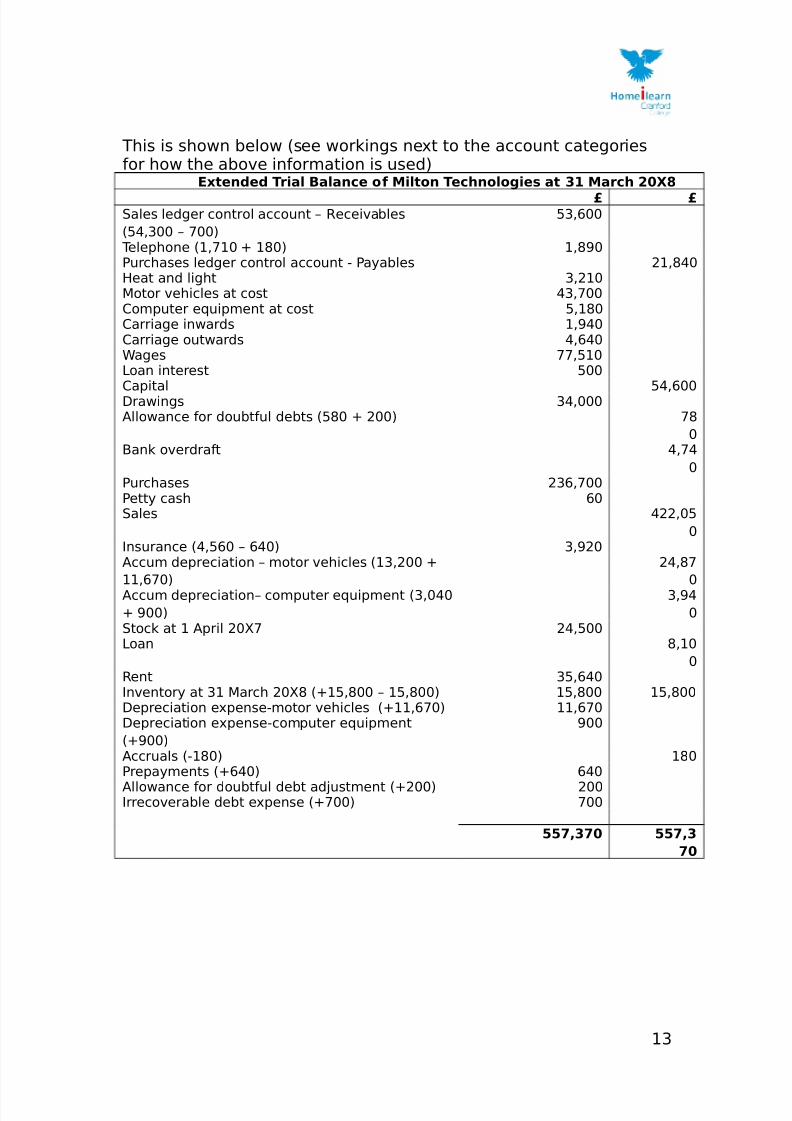

This is shown below #see wor%ings ne/t to the account categoriesor how the abo!e inormation is used$

Eten+e+ T*:al $alan(e of M:lton Te(?nolo:es at , Ma*(? %-#/

'ales ledger control account < Eecei!ables

#50,344 < 744$

53,=44

Telephone #1,714 K 1C4$ 1,C64urchases ledger control account ( aables 21,C04Deat and light 3,214otor !ehicles at cost 03,744*omputer euipment at cost 5,1C4*arriage inwards 1,604*arriage outwards 0,=04ages 77,514Loan interest 544

*apital 50,=448rawings 30,444Allowance or doubtul debts #5C4 K 244$ 7C

4Ban% o!erdrat 0,70

4urchases 23=,744ett cash =4'ales 022,45

4Insurance #0,5=4 < =04$ 3,624Accum depreciation < motor !ehicles #13,244 K

11,=74$

20,C7

4Accum depreciation< computer euipment #3,404

K 644$

3,60

4'toc% at 1 April 247 20,544Loan C,14

4Eent 35,=04In!entor at 31 arch 24C #K15,C44 < 15,C44$ 15,C44 15,C448epreciation e/pense(motor !ehicles #K11,=74$ 11,=748epreciation e/pense(computer euipment

#K644$

644

Accruals #(1C4$ 1C4repaments #K=04$ =04

Allowance or doubtul debt adFustment #K244$ 244Irreco!erable debt e/pense #K744$ 744

70,7- 70,

7-

13

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 14/15

)inancial statements can then be prepared rom the e/tended trialbalance as ollows-

INCOME STATEMENT

In(o)e State)ent fo* M:lton Te(?nolo:es fo* t?e ea* en+e+ ,st

Ma*(? %-#/

Sales

Less- *ost o sales

+pening in!entor

*arriage inwards

urchases

Less- *losing in!entor

"*oss 1*o2t

Less- &/penses

Telephone

Deat and light

*arriage outwards

ages

Loan interest

InsuranceEent

8epreciation(otor !ehicles

8epreciation(*omputer euipment

Irreco!erable debts

Allowance or doubtul debt

adFustment

Net !*o2t

20,544

1,604

23=,744

2=3,104

#15,C44$

1,C64

3,214

0,=04

77,514

544

3,62435,=04

11,=74

644

744

244

4%%0--

#207,304$

7407-

#104,7C4$

,,09,-

10

7/18/2019 Financial statements for sole traders

http://slidepdf.com/reader/full/financial-statements-for-sole-traders 15/15

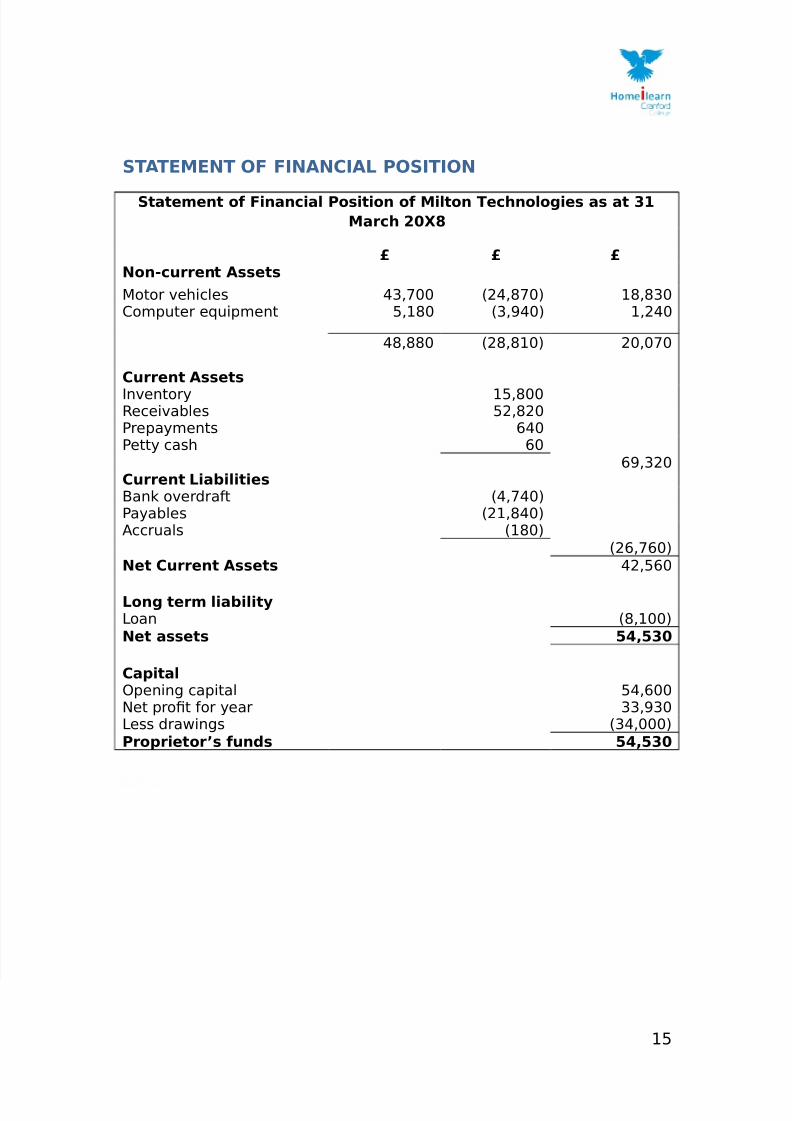

STATEMENT OF FINANCIAL !OSITION

State)ent of F:nan(:al !os:t:on of M:lton Te(?nolo:es as at ,

Ma*(? %-#/

Non;(<**ent Assets

otor !ehicles 03,744 #20,C74$ 1C,C34*omputer euipment 5,1C4 #3,604$ 1,204

0C,CC4 #2C,C14$ 24,474

C<**ent Assets

In!entor 15,C44Eecei!ables 52,C24repaments =04ett cash =4

=6,324C<**ent L:ab:l:t:esBan% o!erdrat #0,704$aables #21,C04$Accruals #1C4$

#2=,7=4$Net C<**ent Assets 02,5=4

Lon te*) l:ab:l:tLoan #C,144$Net assets 40,-

Ca1:tal+pening capital 50,=449et proft or ear 33,634Less drawings #30,444$!*o1*:eto*s f<n+s 40,-

15

Recommended