first investment first investment groupgroup

March 26, 2009March 26, 2009

2009 Economic Update2009 Economic UpdateSteve FrantzSteve Frantz

Senior Managing DirectorSenior Managing DirectorChief Investment OfficerChief Investment Officer

2

Post WWII Recessions Typically Last 10 MonthsDuration of Economic Recessions

0

10

20

30

40

50

60

70

Recession Periods

# o

f M

on

ths

Average back to 1945 = 10 months 2009 = 15 months

Source: National Bureau of Economic Research, Merrill Lynch

3

Recessions Last 18 Months On Average Back to 1855

Duration of Economic Recessions

0

10

20

30

40

50

60

70

1857

-185

8

1960

-186

1

1865

-186

7

1869

-187

0

1873

-187

9

1882

-188

5

1887

-188

8

1890

-189

1

1893

-189

4

1895

-189

7

1899

-190

0

2002

-190

4

1907

-190

8

1910

-191

2

1913

-191

4

1918

-191

9

1920

-192

1

1923

-192

4

1926

-192

7

1929

-193

3

1937

-193

819

45

1948

-194

9

1953

-195

4

1957

-195

8

1960

-196

1

1969

-197

0

1973

-197

519

80

1981

-198

2

1990

-199

120

0120

09

Recession Periods

# o

f M

on

ths

Average back to 1855 = 18 months

Source: National Bureau of Economic Research, Merrill Lynch

4

Stock Market Bottoms 60-70% Of The Way Through A Recession

*Average of 1969-70, 1973-75, 1981-82, 1990-91, and 2001 recessionsShaded area represents recession periodSource: National Bureau of Economic Research, Merrill Lynch

S&P 500 indexed to 100 at start of recession*

110

105

100

95

90

85

80

-52 -39 -26 -13 0 13 26 39 52

Start of recessionEnd of recession

5

Why So Severe?

Source: BEA, JPMorgan Asset Management

6

What Has Been The Primary Driver?

Source: Census Bureau, FactSet, EcoWin, JPMorgan Asset Management Source: (top chart) Census Bureau, FactSet, EcoWin, JPMorgan Asset Management

Source: (bottom chart) Census Bureau, Federal Reserve Board, BEA, JPMorgan Asset Management

7

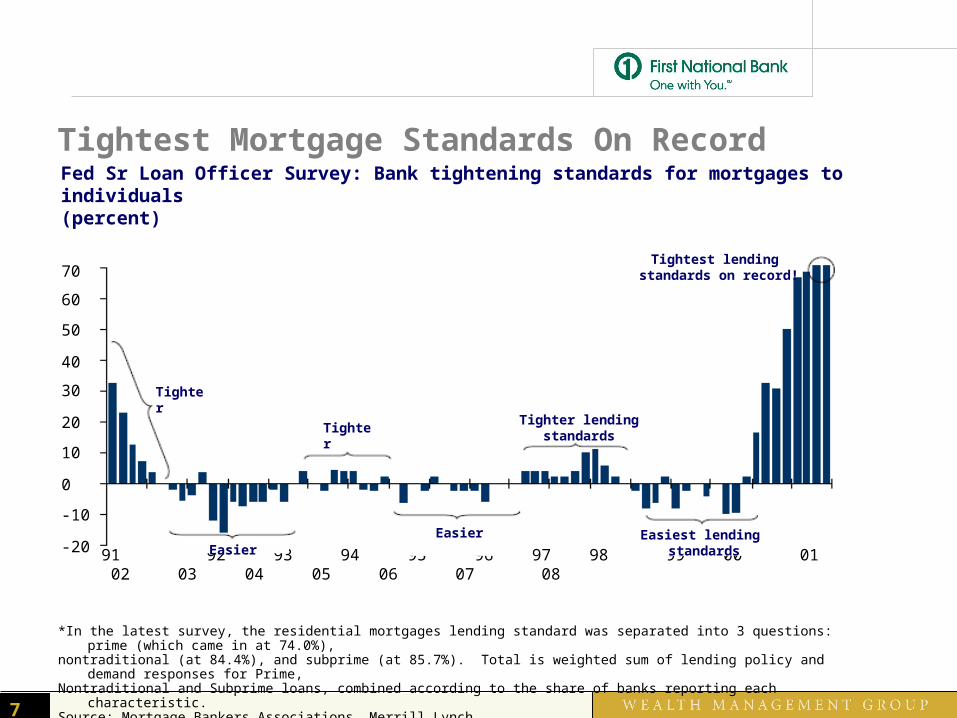

Tightest Mortgage Standards On Record

*In the latest survey, the residential mortgages lending standard was separated into 3 questions: prime (which came in at 74.0%),nontraditional (at 84.4%), and subprime (at 85.7%). Total is weighted sum of lending policy and demand responses for Prime,Nontraditional and Subprime loans, combined according to the share of banks reporting each characteristic.Source: Mortgage Bankers Associations, Merrill Lynch

Fed Sr Loan Officer Survey: Bank tightening standards for mortgages to individuals(percent)

70

60

50

40

30

20

10

0

-10

-20

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Tighter

Tighter

Tighter lending standards

Tightest lending standards on record!

EasierEasier Easiest lending

standards

8

Omaha Housing Market

2008 2007 2006 2005 2004 2003

Avg. List Price Residential Closed

$172,147 $176,412 $178,324 $180,570 $166,738 $164,251

Avg. Sales Price Residential Closed

$166,822 $172,251 $178,578 $177,526 $165,929 $163,235

Avg. Market Time Residential Closed

71 68 70 54 52 52

Avg. Sales Closed as % of Avg. List Price

97% 98% 100% 98% 100% 99%

Total Volume $1.59B $1.93B $1.79B $1.95B $1.74B $1.60B

Source: Omaha Board of Realtors, MLS Data

9

US Debt-To-Income Ration Rose As Much In The Past 7 Years As It Did In The Previous 39 Years

Source: Mortgage Bankers Associations, Merrill Lynch

Household Debt-to-Income Ratio (percent)

140

130

120

110

100

90

80

70

60

50

40

30

52 56 60 64 68 72 76 80 84 88 92 96 00 04 08

1962 = 63%

2001 = 101%

Peak = 139%

10

National Debt as a Percent of GDP

Source: zFacts.com

1950 1960 1970 1980 1990 2000 2010

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

The National Debt as a Percent of

Gross Domestic Product(Data from whitehouse.gov)

2008 OMB

Budget

Prediction

Truman

Ike

Kennedy

LBJ

Nixon

Ford

Bush

Reagan

Clinton

W. Bush

zFacts.com

11

2009 Forecast 1Q GDP Worst for Economy

Modestly Positive GDP by 4Q

Unemployment Peaks 3Q above 8%

Equities – End Year Higher

Treasuries – End Year Lower

Oil Prices Higher by End of Year

Housing Market Bottoms – 2Q/3Q 2009

First Investment Group investment products are: *Not FDIC insured *May go down in value *Not financial institutionguaranteed *Not a deposit *Not insured by any federal government agency.

first investment first investment groupgroup

March 26, 2009March 26, 2009

2009 Economic Update2009 Economic UpdateSteve FrantzSteve Frantz

Senior Managing DirectorSenior Managing DirectorChief Investment OfficerChief Investment Officer

Recommended