Seaborne Coal Markets to 2030

Pittsburgh, PASeptember 20-21, 2012

This material was used by McKinsey & Company during an oral presentation; it is not a complete record of the discussion.

Platts Coal Marketing Days

G L O B A L C O A L O U T L O O K

1|McKinsey & Company

Seaborne Coal has a healthy future …

▪ Seaborne trade is growing faster than total demand

Energy coal

▪ India will need an extra 250-350 mtpa by 2020 and

China 500-1,000 mtpa by 2030.

▪ Few countries can supply at >100 mtpa scale – Australia– Indonesia– US– Russia

Met coal

▪ Steel demand growth will slow, but seaborne met coal demand will accelerate

▪ Best positioned suppliers:

– Australia

– US/Canada

– Mozambique

▪ Supply/demand balance remains unstable.

2|McKinsey & Company

India is at an inflection point

SOURCE: McKinsey India Coal Model

Inconceivable for the coal and power sectors to continue on the current business-

as-usual trajectories

▪ Domestic coal supply: Production from CIL and captive blocks will fall severely short

of demand

▪ Power and coal demand: Fulfilling power demand even at a modest GDP growth of

~6% will imply higher reliance on imported coal, most of which is not viable at current

power purchase prices (PPAs)

▪ Ports and railways infrastructure: Even at modest levels of coal import, the port and

rail infrastructure in the eastern region will bottleneck supplies

We expect discontinuities in several of these drivers, with significant implications

for imported coal

▪ A step change in power price realization (either through PPAs, merchant prices or cost

pass-through pricing), enabling a much higher imported coal component

▪ A significant (and with lead time) ramp-up in domestic coal supply partially mitigating

the imported coal dependence

▪ Significant power shortage, hampering India’s growth

3|McKinsey & Company

230 to 340 mtpa of Indian import need by 2020

* At 9,400 BTU/lb

SOURCE: McKinsey India Coal Model

Domestic supply scenarios

Mtpa @ 6,300 BTU/lb

▪ Minor

improvement in

CIL/SCCL policy

and execution

S1

▪ CIL/SCCL

mechanize

▪ ~ 50 pending

blocks into prod.

S2

▪ Coal supply declared ‘crisis’

▪ Accelerated development of 80 blocks

S3

Demand scenarios, Mtpa @ 6,300 BTU/lb

▪156 GW new plants

▪185 GW inland plants

delayed without coal

▪720 Mtps needed

D2

▪223 GW new plants

▪116 GW plants without

equipt. orders delayed

▪1,020 Mtpa needed

D1

430 Mtpa

import need*230

340 130

250 40

650

350300

520

300 220

380

230 150

Govt Private Total

Govt Private Total

Govt Private Total

Most

likely

4|McKinsey & Company

China is a real unknown – may need 500-1,000 mtpaof imports by 2030

0

500

1,000

1,500

2,000

2,500

3,000

China generation capacityGW

Coal

Hydro/nuke/other

Gas

302520151005

7.0

EIA Outlook

0

500

1,000

1,500

2,000

2,500

3,000

China generation capacityGW

Coal

Hydro/nuke/other

Gas

302520151005

‘30 coal consumptionBillion tonnes, 5800 kcal/kJ

Wood Mackenzie forecast

SOURCE: US Energy Information Administration, Wood Mackenzie, World Energy Council, McKinsey analysis

‘30 Reserve/production ratio(excludes imports, discoveries)

~5

‘30 coal consumptionBillion tonnes, 5800 kcal/kJ

4.6

‘30 Reserve/production ratio(excludes imports, discoveries)

~10

2010-30 CAGRPercent

3%

4%

2%

2010-30 CAGRPercent

7%

7%

4%

5|McKinsey & Company

Few countries could increase exports by 100+ mtpa

SOURCE: McKinsey analysis

▪ Incremental Australian and Russian supply face medium-risk transportation constraints

▪ Beyond 150 Mtpa, Indonesian supply is highly uncertain– Rapidly growing

domestic demand– Government limits

and taxes on exports

▪ Incremental US supply remains highly uncertain given the political constraints on new Pacific port construction

2030

2.2

Other

0.1

Russia

0.2

US

0.3

Indonesia

0.3

Australia

0.5

2012

0.7

Low uncertainty

Medium uncertainty

High uncertainty

Incremental seaborne energy coal supply capacity (2012 – 2030)Billion tonnes / year

6|McKinsey & Company

Steel demand to slow to ~4% as per capita consumption starts to peak

0

100

200

300

400

500

600

700

800

2050403020102000

Western Europe

NAFTA

China

Japan, Korea, Taiwan

Forecast

SOURCE: McKinsey analysis

Potential peak levels of 600-650 kg finished steel per capita,

resulting in finished steel consumption of ~850-900 mt Long term maturity

levels of 450-550 kg per capita, or ~630-770 mtof steel consumption

China finished steel demand, kg/capita

7|McKinsey & Company

As China steel consumption begins to peak, demand growth shifts to India and other developing markets

1 CIS, MENA, Latin America, Subsaharan Africa, Other Asia

136

129

129

128

98

127

144

151

154

181

199

203

China

ROW 1

India

Developed Asia

North America

Europe

25

2,180

886

597

217

20

1,931

815

485

160

3.4% p.a.

1,640

718

383

102

15

1,315

586

280

62

2010

Apparent demand for finished steel productsMillion metric tons

CAGR

2010 - 15 2015 - 20 2020 - 25

6.310.5 9.3

0.43.2 1.9

1.05.2 2.6

-0.2-0.9 -0.1

4.26.5 4.8

1.74.2 2.6

4.5 3.3 2.5Global

BASE CASE

SOURCE: World Steel Association; McKinsey Integrated Steel Making Raw Materials Demand model

8|McKinsey & Company

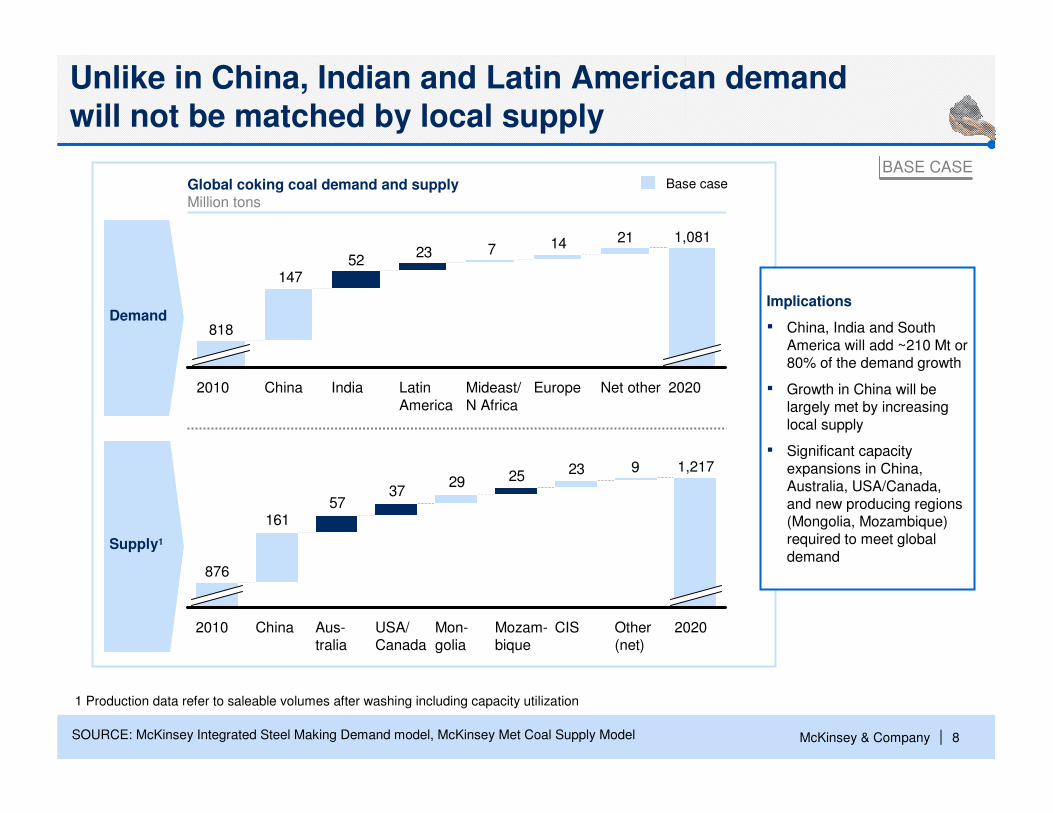

211472352

147

2020

1,081

Net otherEuropeMideast/

N Africa

Latin

America

IndiaChina2010

818

923252937

57161

2020

1,217

Other (net)

CISMozam-bique

Mon-golia

USA/Canada

Aus-tralia

China2010

876

Base case

Unlike in China, Indian and Latin American demand will not be matched by local supply

1 Production data refer to saleable volumes after washing including capacity utilization

Implications

▪ China, India and South

America will add ~210 Mt or 80% of the demand growth

▪ Growth in China will be largely met by increasing

local supply

▪ Significant capacity

expansions in China, Australia, USA/Canada,

and new producing regions (Mongolia, Mozambique) required to meet global

demand

Demand

Supply1

Global coking coal demand and supplyMillion tons

BASE CASE

SOURCE: McKinsey Integrated Steel Making Demand model, McKinsey Met Coal Supply Model

9|McKinsey & Company

CA

N-T

3

0

CA

N-T

1

AU

S-T

5

AU

S-T

3

NZ

IND

O

VE

NC

OL

MO

Z

AU

S-T

2

RU

S

AU

S-T

1

50

200

250

0

AU

S-T

4

100

150

CA

N-T

2

10 4020 30 8050 7060 22090 110100 210120 140130 200150 190160 180170

Seaborne cost curve steep and unstable, with high prices when high cost US coal required to close the market

Brownfield pricing regime

+5/+25% premium over C90 seaborne cash cost of U.S.

Greenfield pricing regime

+25/+45% premium over C90 seaborne cash cost of U.S.

SupplyMtpy

Washed seaborne coking coal cost curveCash cost, USD / metric tonne FOB

90th percentile

cash cost

SOURCE: McKinsey Met Coal Supply Model

Mining cash cost

Inland freight

(rail/barge and port)

Quality discount to

HCC benchmark

US producers:

10|McKinsey & Company

Appendix

11|McKinsey & Company

Steel demand to slow to ~4%

Low case

Base case

High case

25

2,200

2,800

2030

7.0% pa

2,400

2,600

2,000

1,800

1,600

1,400

1,200

1,000

800

600

0

1.2% pa

2015

1,391

100520009590851981

Apparent demand for finished steel productsMillion metric tons, CAGRs 1981 - 2000, 2000 - 08

Historical Forecast

6.3%

4.5%

2.6%

3.3%

3.3%

3.2%

‘10-'15

CAGR, Percent

'15-'20

Financial crisis – sharp break from previous trend, demand growing again but from a lower base

Inflection point – rise of emerging market industrialization, led by China

SOURCE: World Steel Association; McKinsey Integrated Steel Making Raw Materials Demand model

12|McKinsey & CompanySOURCE: McCloskey; China customs

OtherChina

2532

30

2011

211

166

5

2005

211

171

187

06

179

07

182

152

08

183

179

3

09

179

10

176

3173

170

3

3 1 2 2 17

▪ Historically coking coal demand in China was mostly satisfied by domestic supply and had limited impact on seaborne export market

▪ In 2009, driven by lower price, coastal/riverside steel mills (Baosteel, Wugang, Angang, Hebei Iron & Steel, Shagang), started to import metallurgical coal

▪ Given better quality of imported met coal, these imports were “sticky”throughout 2011 but started declining as the share of overland imports increased

China became a significant seaborne coking coal importer in 2009and but reduced seaborne imports again in 2011

15

Seaborne coking coal demand (excl. imports from Mongolia)Million tons

11

% China share

13|McKinsey & CompanySOURCE: McCloskey; China customs

68 54 50 47 68 55

▪ Strong increase of coking coal imports in 2009 substantially driven by seaborne imports from Australia

▪ Starting in 2010 and even stronger in 2011, seaborne imports from Australia were replaced particularly by non-seaborne imports from Mongolia and seaborne imports from North America

In 2011, seaborne imports into China were largely substituted bynon-seaborne imports from Mongolia

88

Chinese coking coal importsMillion tons

% Seaborne share

8

3

7

20

15

0

5

10

15

20

25

30

35

40

45

50

5

2002

2005

7

3102

2011

45

10

8

10

47

17

06 09

34

23

4

4

4

08

7

1114

07

6

201

7

Non-sea-borne

Sea-borne

1 Russia, Indonesia, New Zealand and other

Australia

Canada + US

Other seaborne1

Mongolia

14|McKinsey & CompanySOURCE: China Customs; McKinsey analysis

20 25

2418 22

1413

29

5262

131510000

112

17

2

126

10

111

09

86

10

08

33

201107

41

22

06

3120

7

2005

1622

7

0 21 5

5

102

Chinese seaborne1 thermal coal import

Mtpa (@ 6000 kcal/kg)

1 Excludes road/rail imports from Mongolia and North Korea

2 Primary export destinations (both historical and forecast) are Japan, S Korea and Taiwan

CHINA THERMAL AND COKING COAL TRADE EVOLUTION

Others

Russia

Australia

Vietnam

Indonesia

Import

share

%

4.2 4.9 5.10.9 1.6 2.2 1.4

Exports2

Mtpa

22 18 1166 59 51 42

Net import

Mtpa

64 93 115(50) (28) (9) (9)

China coal imports reached ~125 mt in 2011 and have shown strong growth since 2008 but still represent just 5% of China’s thermal demand

▪ In 2009, imports tripled,

with significant imports

from Australia for the

first time

▪ China moved from a net

export position to large

net seaborne imports in

one year

▪ Rapid rise in imports

because of freight

differentials and

delivered price arbitrage

15|McKinsey & Company

Continued yr-on-yr declining power demand growth has contributed to

increasing inventories both in ports and at power plants

SOURCE: CCTD; Sxcoal; McKinsey

8

10

12

14

16

18

20

22

24

26

28

30

J F M DNOSAJJMA

Coal inventory in 7 key Northern portsMillion metric ton

-30

-20

-10

0

10

20

30

40

50

60

70

80

-30

-20

-10

0

10

20

30

40

50

60

70

80

Coal demand growthPercent YoY

Power generation growthPercent YoY

JS MM S N JJ N JMJJ J SJM S MNJN MMM MM J20092008 2010

Thermal power generation monthly growth

Coal app. demand monthly growth

CHINA THERMAL COAL DEMAND - INVENTORIES

▪ Inventory in key ports e.g., Qinhuangdao, Tianjin, have reached record highs in July; warehouses are so full that

incoming trains cannot unload coal and are forced to stay idle with coal on board

▪ Coal inventories at power plants level are also at record high levels, there are only very few buyers for the record stockpile of coal

2012

2011

2010

2009

2008

20122011

16|McKinsey & Company

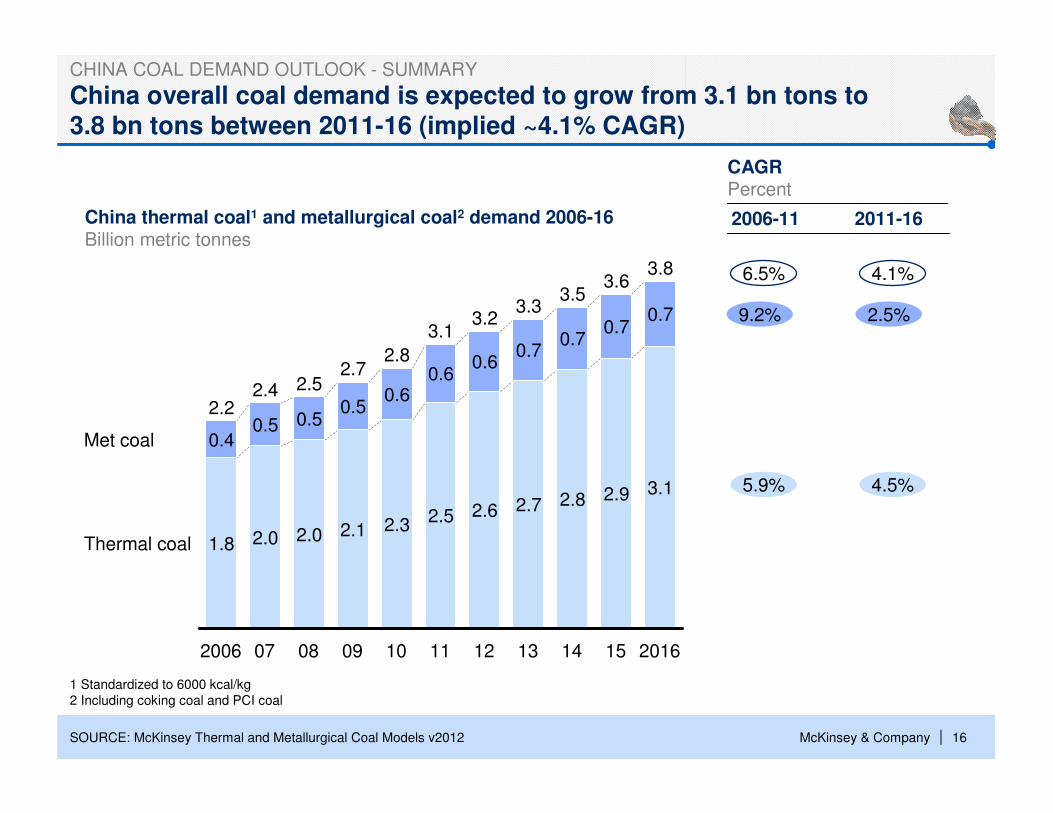

China overall coal demand is expected to grow from 3.1 bn tons to 3.8 bn tons between 2011-16 (implied ~4.1% CAGR)

China thermal coal1 and metallurgical coal2 demand 2006-16Billion metric tonnes

CHINA COAL DEMAND OUTLOOK - SUMMARY

2.8

0.7

13

3.3

2.7

0.7

12

3.2

2.6

0.6

11

3.1

2.9

Thermal coal

Met coal

2016

3.8

3.1

0.7

15

3.6

0.7

14

2.5

0.6

10

2.8

2.3

0.6

3.5

2.7

2.1

0.5

08

2.5

2.0

0.5

09

2.4

2.0

0.5

2006

2.2

1.8

0.4

07

SOURCE: McKinsey Thermal and Metallurgical Coal Models v2012

2.5%

4.5%

CAGRPercent

2011-162006-11

4.1%

9.2%

5.9%

6.5%

1 Standardized to 6000 kcal/kg

2 Including coking coal and PCI coal

17|McKinsey & Company

Southern Africa has seven significant coal deposits, with thelargest located in South Africa

Mozambique

Angola

Malawi

Zambia

Namibia

Lesotho

Zimbabwe

Botswana

South Africa

Swaziland

Madagascar

8

67

5

4

21

SOURCE: Team analysis

Location of major coal reserves in Southern Africa

DepositsReservestons, billion

Qualitykcal/kg

Thermal % Deposits

Reservestons, billion

Qualitykcal/kg

Thermal %

1 Witbank 17 5900-6200 85 6 Zambezi basin 26 5800-6926 60

2 Waterberg 6 5900-6200 100 7 Maamba

deposits

0.7 6100-6300 100

4 Moatzie basin 23 5300-7800 408 Imaloto

coal basin0.7 4200 100

5 Mmamabula coal deposits

200 4700-6448 100 9 Aranos coal basin

0.4 - -

9

PRELIMINARY

3 South Africa other 8 5900-6200 -

3

18|McKinsey & Company

Steel intensity for selected economies

1 Crude steel equivalent

SOURCE: WSA; Global Insight; IMF; USGS; McKinsey

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000

Steel consumption1

kg/capita

Real GDP (2000)USD/capita

India (1970 - 2011)

Taiwan (1970 - 2011)

USA (1900 - 2011)

Japan (1955 - 2011)

South Korea (1970 - 2011)

EU-15 (1948 - 2011)

Germany (1946 - 2011)

Heavy

industryexport

economies

Developedand

diversified

economies

China

(1970 –

2011)

Russia (1994 –

2011)

Low asset

intensityeconomies

Mexico (1967 - 2011)

Recommended

![2+* /-,4176 a P|Gw]Tki8Nqn9CE+d.QPn9 YC C O? nK ;?](https://img.pdfslide.net/doc/110x75/5e59e615d5302a300c3f40ed/2-4176-a-pgwtki8nqn9cedqpn9-yc-c-o-nk-.jpg)