0

GOVERNMENT EMPLOYEES PROVIDENT

FUND (GEPF)

ANNUAL OPERATIONS REPORT FOR THE YEAR 2009/2010

April 2010

1

CORPORATE INFORMATION

Board of Management Mrs. M.L. Mwamunyange Chairperson Mr. E.N. Nkuku Mr. L.M. Salema Mr. Mrs. J. Shaidi Mr. R.E. Chalamila Dr. M.I. Nchimbi

Mr. O. Urasa Mr. C. W. Samanyi Mr. D.M. Msangi Secretary

Audit Committee Dr. M.I. Nchimbi Chairperson Mr. L.M. Salema Mr. R.E. Chalamila

Mr. O.M. Urasa

Registered Office Ubungo Plaza 1st Floor, Ubungo Plaza

Morogoro Road P O Box 11492 Dar -es-Salaam

Bankers National Bank of Commerce Limited P.O. Box 9062 Dar-es-salaam

CRDB Bank Plc P.O. Box 71960 Dar-es-Salaam National Micro-finance Bank P.O Box….. Dar-es Salaam

Auditors Deloitte & Touche Certified Public Accountants 10th Floor, PPF Tower Cnr of Ohio Street & Garden Avenue

P O Box 1559 Dar -es-salaam

2

Our Vision

“To be a leading Professional Provident Fund in Tanzania in terms of widest

coverage and customer oriented services”.

Our Mission

“To provide quality and timely social security benefits under Provident Fund System

to non- pension, contractual employees and self employed person in Tanzania

through the use of modern information communication technology”.

Our Core Values

Accountability

Transparency

Behave like owner

Result oriented

Excellence

Integrity

3

TABLE OF CONTENTS

LETTER OF TRANSMITTAL ..........................................................................................................4

CHAIRPERSON’S STATEMENT ....................................................................................................5

THE BOARD OF MANAGEMENT ..................................................................................................7

STATEMENT BY THE CHIEF EXECUTIVE OFFICER ................................................................8

THE MANAGEMENT TEAM.........................................................................................................10

DETAILED PERFORMANCE REVIEW ........................................................................................11

MEMBERSHIP AND BENEFIT PAYMENT .............................................................................. 11

Membership ............................................................................................................................... 11

Members registration ................................................................................................................. 11

Benefit payment ......................................................................................................................... 12

INVESTMENTS AND INVESTMENT INCOMES..................................................................... 12

Investments made....................................................................................................................... 13

Investment Incomes ................................................................................................................... 14

Interest to be Credited to Members ............................................................................................ 16

SERVICES TO MEMBERS .......................................................................................................... 16

ANNUAL GENERAL MEETING (AGM) ................................................................................... 17

Members Recommendations ...................................................................................................... 17

Implementation of Members Recommendations ....................................................................... 18

STAFF DEVELOPMENT AND RECRUITMENT ...................................................................... 18

Staff Development ..................................................................................................................... 19

Staff Recruitment ....................................................................................................................... 19

INDUSTRIAL RELATIONS ........................................................................................................ 19

CORPORATE SOCIAL RESPONSIBILITY ............................................................................... 19

AWARENESS AND PUBLIC RELATIONS ............................................................................... 19

CORPORATE AND INTERNATIONAL RELATIONS ............................................................. 21

BOARD’S STATEMENT ON CORPORATE GOVERNANCE FOR THE YEAR ENDED 30

JUNE 2009 ........................................................................................................................................22

STATEMENT OF BOARD OF MANAGEMENT’S RESPONSIBILITIES ..................................24

INDEPENDENT AUDITORS’ REPORT TO THE CHAIRPERSON OF THE .............................26

BOARD OF MANAGEMENT OF GOVERNMENT EMPLOYEES PROVIDENT FUND .........26

STATEMENT OF CHANGES IN NET ASSETS FOR THE YEAR ENDED 30 JUNE 2009.......28

STATEMENT OF NET ASSETS AS AT 30 JUNE 2009 ...............................................................29

CASHFLOW STATEMENT FOR THE YEAR ENDED 30 JUNE 2009 .......................................30

NOTES TO THE FINANCIAL STATEMENTS .............................................................................31

4

LETTER OF TRANSMITTAL

Mr. Ramadhan Khijah,

Permanent Secretary,

Ministry of Finance and Economic Affairs,

P.O Box 9111,

DAR ES SALAAM.

Permanent Secretary,

I am pleased to present to you on behalf of the Board of Management an Annual Report of

the Government Employees Provident Fund for the financial year ended 30th June 2010.

The report was prepared in accordance with Section 3 of the Government Employees

Provident Fund Act No 52 of 1942, (RE 2002).

The report details a Chairpersons statement, Statement of the Director General, the

Annual Accounts and the Auditor‘s Report.

Yours Sincerely,

Monica L. Mwamunyange

CHAIRPERSON

September, 2010

5

CHAIRPERSON’S STATEMENT

Dear Members,

Having successfully accomplished another year‘s progress, I am delighted to report Fund‘s

Annual Report and Financial Statement for the year ended 30th June 2010. The report will

address, economic performance, operational performance of the Fund, Challenges and

way forward.

In the recovery of the economy, the gross domestic product grew by 6% which is higher

than projection of 5% due to communication and financial intermediation activities.

However, the inflation moved to single digit on February 2010 from double digit in the

previous year in respect to improvement of food supply. The annual inflation decreased to

8.20% by June 2010 from 11.30% in June 2009.

The interest rate decreased as the treasury bills made a record of 2.90% in June 2010

compared to 6.97% in June 2009. The time deposits made a record of declined to 5.78 %

in June 2010 from 6.52% in June 2009. For the 12 months time deposit made a declining

record of 8.67% from 8.98% in the previous year.

Financial Performance

The Fund made an incredible growth despite the economy being in its recovery process.

The Fund‘s net asset grew to 91,260.61 million by June 2010 from TZS 72,549.57 million

reported in June 2009. The growth of 25.79%, this increase was a result of increase in

contribution by 13.50 % and investment income that increase by 40%.

6

Service to Members

Achievement of customer satisfaction has been normal priority of the Fund along the

years. The Fund has strengthened customer services by attending at a minimum possible

time the customer‘s enquiries. Information has been updated in the website for customers

convenient to assess their information including Fund‘s operations. Besides that, there is

also members‘ statement issued for those customers visiting the Fund physically or

through posting.

Response to Members Opinion

During the previous Annual General Meeting, members raised pertinent issues. A special

sub section detailing implementation of such issues is covered under detailed performance

review. I wish to point out that as a response to members‘ comments during the AGM the

Fund has implemented most of their recommendations which include opening offices to

serve customers in the regions. One office has already been opened at Mafinga and

another two are expected to be opened on the Northern Zone and Lake Zone.

Appreciation

Finally, I would like to take this opportunity to place on record our hearty thanks to

members‘, stakeholders and GEPF Staff for the perfect logistic support and guidance that

extended to our sustainable growth. It is my sincere expectations the co-operation will be

strengthen to over record performance in the near future. I assure to our esteemed

members‘ that the Fund will make sure better lives‘ is maintained through quality service

and perfect requirement packages for them.

MONICA L. MWAMUNYANGE

CHAIRPERSON

7

THE BOARD OF MANAGEMENT

Mr. E. M. Nkuku

Vice Chairperson

Mrs. M. L. Mwamunyange

Chairperson

Eng.Ladislaus M. Salema

Member

He joined the Board in May 2003 as

Non Executive Director and became

Deputy Chairperson in May 2006. He

is a lawyer and holder of Post

Graduate Diploma in Human

Resources Management. Currently he

is the Commissioner of Prisons

responsible for Finance and

Administration Division in Tanzania

Prisons Service.

She joined the Board in May 2006.

She is a planner with over 20 years of

public service. She is currently

serving as Commissioner for Budget,

Ministry of Finance and Economic

Afairs and Non- Executive Director,

Mwalimu Nyerere Memorial Academy.

He joined the Board in May 2006. A Former

Manager of National Engineering Company

and Divisional Director in Tanzania Social

Action Fund. He has over 30 years of

experience in techno-managerial in public

service. He is currently the CEO of

MKURABITA.

Dr. Mariam I. Nchimbi

Member

She joined the Board in May 2006.

She is a senior Lecturer and

Director of the University of Dar es

Salaam Enterpreneurship and also

a Non Executive Director of the

Governing Boards of the Tanzania

Investment Centre (TIC) and

Arusha International Conference

Centre (AICC)

8

STATEMENT BY THE DIRECTOR GENERAL

I appreciate the efforts made in 2009-10 in accomplishing the achievement that kept a

record of another successful year. The Fund has been performing well despite the

economy being in the recovery situation.

The annual report of the fund shows the growth in the aspect of membership, members‘

contribution, investments and investment income. The contributions have increased from

TZS 14,723.50 million in June 2009 to TZS 16,719.67 million in June 2010. The increase

in contribution resulted from increase in salaries, close follow up in contribution collection

and increase in membership size.

Investment performance made a good record to an increase from TZS 5,475.04 million in

June 2009 to TZS 7,693.60 million in June 2010. The increase in investment income was a

result from attractive interest rate from fixed deposit, high yields earned from Treasury

bond, dividends and interest from loans issued to companies.

Members have been paid benefits on time within seven working days with the exception of

the some which had problems beyond our control. The benefits paid to members

increased from TZS 1,575.96 million to TZS 3,335.00 million. This increase resulted from

increase in members who have graduated to pension terms and retired members.

9

Voluntary Saving Retirement Scheme (VSRS)

During the year the Fund introduced a new scheme voluntary saving retirement scheme

that suits the need of employed and self - employed. In the interest of widening the

members‘ coverage to reach all people, the VSRS product is in place to cover self-

employed workers in all sectors of the economy. The scheme has progressed very well;

members registered as 30th June 2010 were 1,451 that contributed a sum of TZS 52.45

million. Detailed of operations is presented in the following sections.

I would like to conclude by extending special appreciation to the Board of the Fund,

Employees of the Fund, members, employers, business associates and other stakeholders

for their continued support. Contributions made by all parties were key to the success of

the Fund during the year.

DAUD M. MSANGI

DIRECTOR GENERAL

10

THE MANAGEMENT TEAM

Philemon P. Minga

Manager - Finance and Administration

Mr. Daud M. Msangi DIRECTOR GENERAL

Mr. Festo F. Fute Manager – Investment and

Operations

He joined the Fund in April 2004 as

Manager responsible for finance

and administration. He is a

professional accountant who

previously worked with TTCL as

manager responsible for customer

accounting and later responsible for

financial accounting.

He joined the Fund in June 2004 as

Chief Executive Officer. He is economist

with over 15 years in the field and has

held various positions in the public

sector including the post of Deputy

National Authorizing Officer and

Coordinator of European Development

Fund in Tanzania.

He joined the Fund in June 2004 as

Manager responsible for operations

and investments. He is economist

and has previously worked with the

National Social Security Fund (NSSF)

as principal planning and finance

officer for over ten years before

joining the Fund.

Mr. Hussein I. Kinduu Chief Internal Auditor

Mr. Edgar Shumbusho Chief ICT Officer

He joined the Fund in 2003 as

senior accountant and later

promoted to Chief Internal Auditor

in 2007. He is a professional

accountant who previously worked

with Ministry of Finance and

Economic Affairs and Public

Services Pensions Fund holding

various accounting positions.

He joined the Fund in September

2004 as Information Technology

Officer and later promoted to Chief

Information Technology officer in Jan

2007. He is a Computer Scientist and

has previously worked with the

University of DSM Computing Centre

as head of Consultancy Unit before

joining the Fund.

11

DETAILED PERFORMANCE REVIEW

MEMBERSHIP AND BENEFIT PAYMENT

Membership

The membership of the Fund depends upon the type of employment.

The Fund has two schemes which are the statutory contributory scheme and Voluntary

Saving Retirement Scheme (VSRS). The old Statutory Contributory Scheme is open to all

employees of the Central Government, its agencies, independent departments working

under contracts or operational service. Other eligible employees are those working in

projects and program. While members of VSRS scheme are those who are self employed

workers or pensionable members who would like to contribute voluntarily to add into

retirement gratuity. As at 30th June 2010 the Fund had a total of 35,279 members out of

which 1,451 members were from new registered product namely VSRS.

Voluntary Savings Retirement Scheme (VSRS)

During the year 2009/10, the Fund conducted a study on the possibility of including self

employed workers to the scheme. The result of the study led to introduction of a Voluntary

Saving and Retirement Scheme (VSRS) in January 2010. The overall response has been

very positive as from January to June 2010 the Fund managed to register 1,451 members

and collected TZS 52.45 million from the scheme. The scheme was officially launched

during the second Annual General Meeting held on 21st May 2010.the table 2 below shows

the performance of the scheme since November 2009 to June 2010.

Members registration

The Fund had planned to register 3,352 new members during the year. Providentially, the

Fund registered 5,897 members‘ equivalents to 175.92% of the set target. The members

were registered from the Central Government, agencies, independent departments,

projects and self-employed.

12

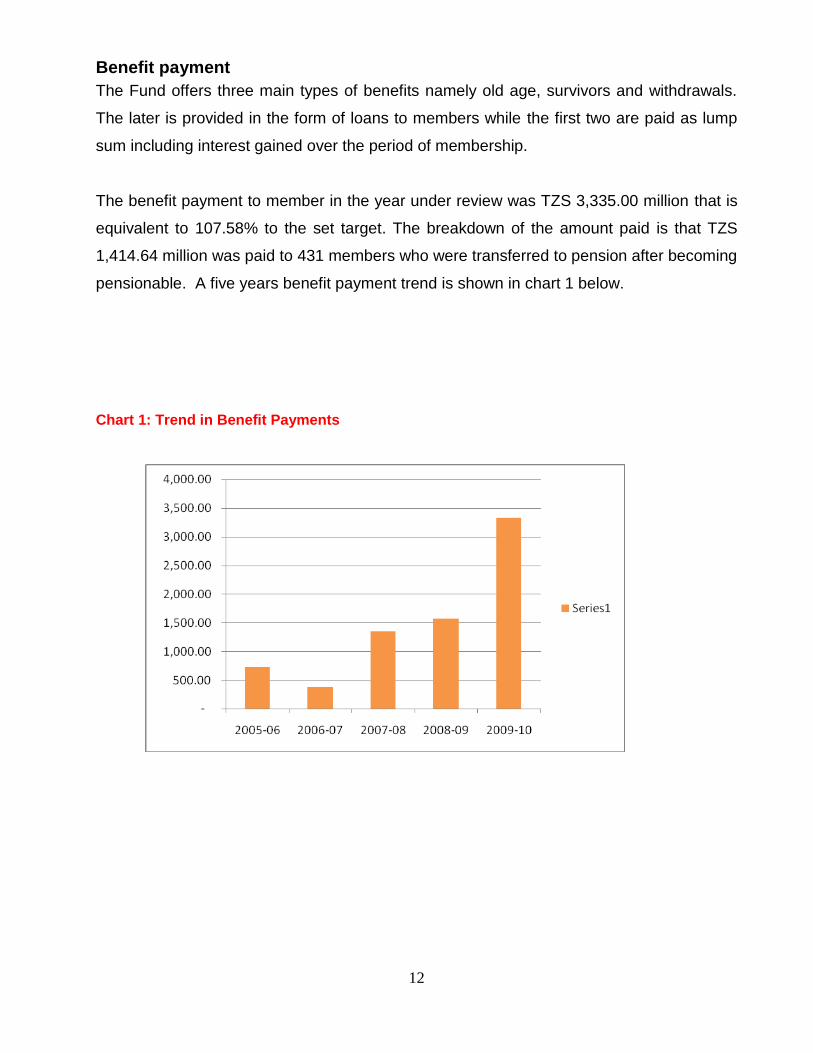

Benefit payment

The Fund offers three main types of benefits namely old age, survivors and withdrawals.

The later is provided in the form of loans to members while the first two are paid as lump

sum including interest gained over the period of membership.

The benefit payment to member in the year under review was TZS 3,335.00 million that is

equivalent to 107.58% to the set target. The breakdown of the amount paid is that TZS

1,414.64 million was paid to 431 members who were transferred to pension after becoming

pensionable. A five years benefit payment trend is shown in chart 1 below.

Chart 1: Trend in Benefit Payments

13

INVESTMENTS AND INVESTMENT INCOMES

Investments made

The Fund collects contributions from members‘ and invests in different secured security to

increase the growth of the Fund. Growth of the Fund through revenue realised increases

the members‘ account value. The investments are made in a highly professional method

through the guidance set out in the investment policy.

The Fund is faced with limited investment avenue in the country. The Fund is The Fund

invested in Government Securities, fixed deposit in commercial bank, corporate bonds,

listed shares in the Dar es Salaam stock exchange, corporate loans and Land Plot. The

Fund is in process of constructing a commercial office complex in the plot acquired along

new Bagamoyo Road.

During the year under review, the Fund‘s investment portfolio increased from TZS

64,935.82 million in June 2009 to TZS 83,773.47 million in June 2010 which is equivalent

to a growth of 29.00%.Table 1 below shows a five year investment portfolio structure, while

chart No. 2 presents a percentage distribution of the portfolio structure in year 2008/09.

Table 1: GEPF Investments Portfolio Structure as at 30th June 2010

(TZS Mil.)

Type of Investment

2005/2006 2006/2007 2007/2008 2008/09 2009/10

Treasury Bills 9,082.73

12,365.55 11,845.49 14,556.60 2,099.94

Treasury Bond 7,183.13

10,974.80 16,727.45 21,787.89 31,230.34

Govt. Stocks 78.35

78.35 4.40 4.40 4.41

Fixed Deposits 4,915.00

10,030.00 15,790.00 20,040.00 37,864.90

Equity/shares 941.14

2,077.63 2,314.96 3,320.94 3,320.94

Corporate Bond 1,000.00

1,000.00 800.00 1,600.00 1,400.00

Loans 0.00

2,000.00 2,000.00 4,100.00

UTT 1,000.00

799.99 799.99 799.99 799.99

Real Estate 0.00

0.00 0.00 826.00 853.00

Total 24,200.35

37,326.32 50,282.2 64,935.82 81,673.52

14

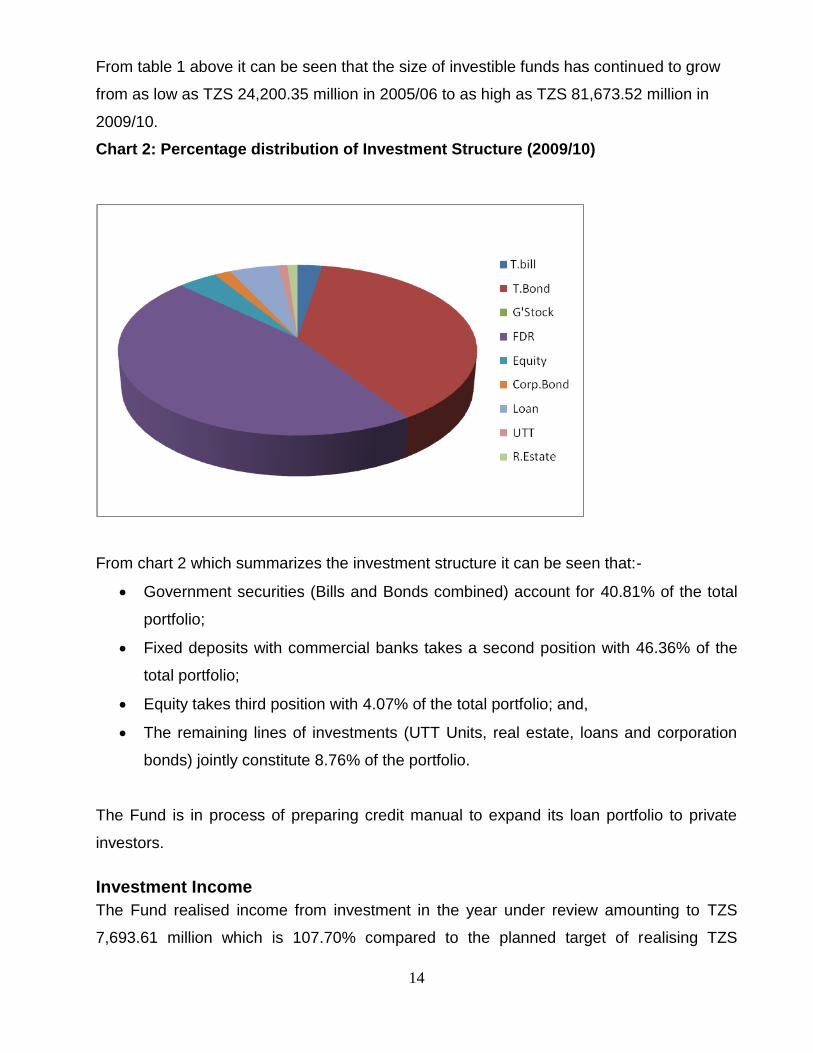

From table 1 above it can be seen that the size of investible funds has continued to grow

from as low as TZS 24,200.35 million in 2005/06 to as high as TZS 81,673.52 million in

2009/10.

Chart 2: Percentage distribution of Investment Structure (2009/10)

From chart 2 which summarizes the investment structure it can be seen that:-

Government securities (Bills and Bonds combined) account for 40.81% of the total

portfolio;

Fixed deposits with commercial banks takes a second position with 46.36% of the

total portfolio;

Equity takes third position with 4.07% of the total portfolio; and,

The remaining lines of investments (UTT Units, real estate, loans and corporation

bonds) jointly constitute 8.76% of the portfolio.

The Fund is in process of preparing credit manual to expand its loan portfolio to private

investors.

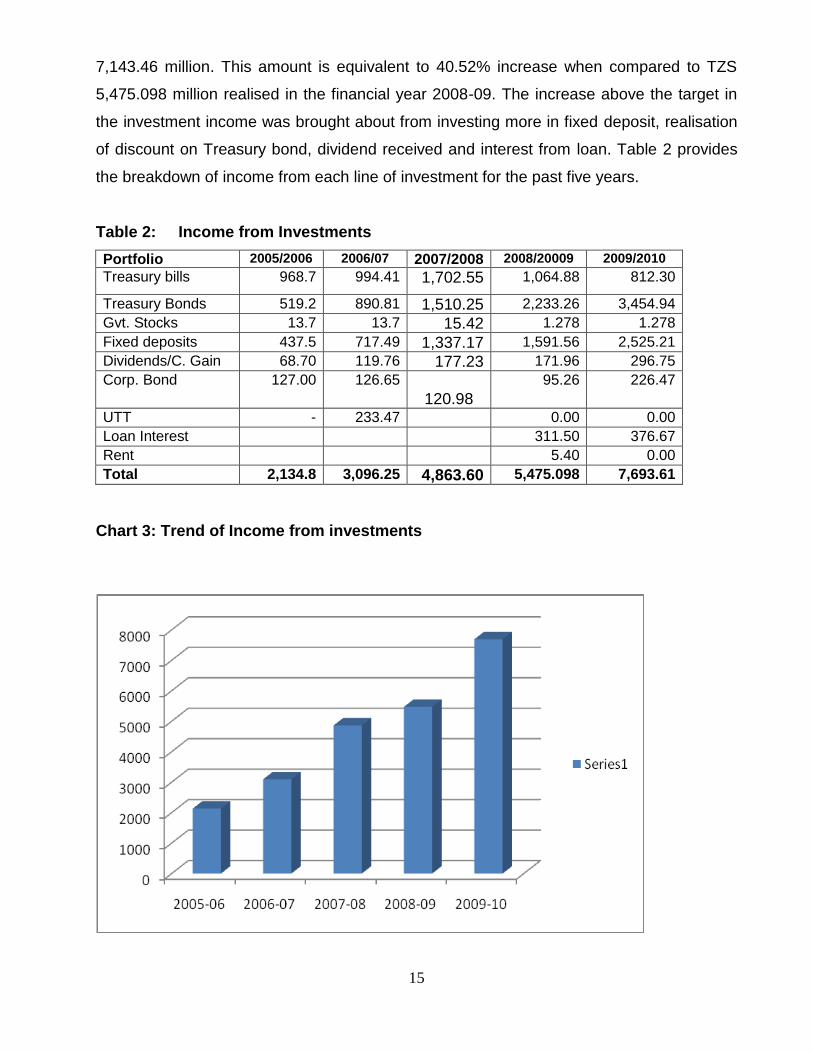

Investment Income

The Fund realised income from investment in the year under review amounting to TZS

7,693.61 million which is 107.70% compared to the planned target of realising TZS

15

7,143.46 million. This amount is equivalent to 40.52% increase when compared to TZS

5,475.098 million realised in the financial year 2008-09. The increase above the target in

the investment income was brought about from investing more in fixed deposit, realisation

of discount on Treasury bond, dividend received and interest from loan. Table 2 provides

the breakdown of income from each line of investment for the past five years.

Table 2: Income from Investments

Portfolio 2005/2006 2006/07 2007/2008 2008/20009 2009/2010

Treasury bills 968.7 994.41 1,702.55 1,064.88 812.30

Treasury Bonds 519.2 890.81 1,510.25 2,233.26 3,454.94

Gvt. Stocks 13.7 13.7 15.42 1.278 1.278

Fixed deposits 437.5 717.49 1,337.17 1,591.56 2,525.21

Dividends/C. Gain 68.70 119.76 177.23 171.96 296.75

Corp. Bond 127.00 126.65 120.98

95.26 226.47

UTT - 233.47 0.00 0.00

Loan Interest 311.50 376.67

Rent 5.40 0.00

Total 2,134.8 3,096.25 4,863.60 5,475.098 7,693.61

Chart 3: Trend of Income from investments

16

Interest to be credited to Members

During the Financial year 2009-10, the national financial market kept on declining not only

resulted from a relaxed monetary policy stance pursed by the Bank of Tanzania but also

resulted from credit crunch that planted fear in credit institutions to discharge loans to

agriculturist. This led the interest rates in the financial market to decline to 2.90% in June

2010 from 5.89% recorded in March 2010, the overall time deposit rate decreased to

5.78% in June 2010 from 6.01% in June 2009. The unchanged market situation from the

financial year 2008-09 affected the Fund investments projections be targeted low.

The low interest rate across various instruments in the money market led interest to be low

credited to members accounts. For the year 2009/10 members‘ accounts will be credited

with 4.90% interest. The same will be used as provisional rate for the year 2009/10.

SERVICES TO MEMBERS

Quality of the service offered to members have been crucial factor that is most considered.

The Fund had maintained the punctuality in benefit payment, information query and

conduct Annual General Meeting that serve to give operational information to

stakeholders.

The Fund participated in different public occasions and site visit to clients that creates

close relationships with members and enables members‘ queries be responded. The Fund

participated in Sabasaba Exhibition, Nanenane Show, and Public Service week. The

participation resulted to fruitful information and suggestion to the Fund.

.

17

An official of the Fund availing members with their statements of account during the Nane Nane Exhibition in Dodoma in 2009.

ANNUAL GENERAL MEETING (AGM)

Members Recommendations

The Fund conducted its third Annual General Meeting on 30th April 2009. The meeting

which was attended by 160 participants was graced by the Minister for Finance and

Economic Affairs, Honourable Mustapha Mkullo. The occasion saw the Minister launching

the Fund‘s new product of Voluntarily Saving Retirement Scheme that aimed to self –

employed worker or employed workers who intend to put additional benefits for their future.

During the first AGM members raised the following issues for consideration:

The Fund should change the name of GEPF to accommodate the meaning of VSRS

as the GEPF name has Government employees that contradicts with VSRS Product

which accommodates self employed and employed regardless of government

employment.

The Fund should open a branch in up-countries to ease service to members around

the place branch.

18

How the Fund has made arrangements in improving welfare of members in informal

sector.

In death benefit payment, the Fund should prepare cheque to all beneficiaries

according to the proportions allocated by the Court than issuing one cheque to the

administrator that leads to family problems at the end.

Implementation of Members Recommendations

Recommendations received from members were given due considerations. All were

implemented except for the following two which had specific reasons:

The change of the name of GEPF to accommodate the meaning of VSRS will take

long time as it involves parliament approval.

19

STAFF DEVELOPMENT AND RECRUITMENT

Staff Development

Training the staff builds the capacity and adds output in the Fund‘s operations. During the

year under review, seven staff participated in short courses covering social security,

investment risk analysis, leadership skills, information technology, advanced financial

management and enhancement of good labour relations during the year. Further during

the same period the Fund conducted in-house training on the labour laws which benefited

28 staff members and a similar approach on computerised financial accounting system for

8 staff. The Fund continued to sponsor two (2) staff to complete studies on advance

accounting and social security‘s on June 2010. One more staff was sponsored on full time

nine months Certificate Course on Record Management.

Staff Recruitment

In the view of improving the Fund‘s strength, three staffs were recruited during the year to

fill the position of Director of Marketing and Operation, Supplies and Procurement Officer

and Assistant Accountant. The Fund established the procurement unit.

INDUSTRIAL RELATIONS

During the year under review the Fund continue to conduct normal relationship among

staffs. The Fund carried monthly meetings for department and staff meeting in every two

months that provide opportunity to staff discuss issues concerning lead in adding Fund‘s

worth and quality.

CORPORATE SOCIAL RESPONSIBILITY

The Fund continued to carry out its social responsibility to the society. During the year

under review the Fund kept supporting the community by donating TZS 10.00 million in

various charitable areas. The donations were channelled during the year to National Youth

Anti- HIV/ Aids Committee, Public Procurement Regulatory Authority, Kimara Ophans,

AWARENESS AND PUBLIC RELATION

As normal custom of the Fund to make sure most members and stakeholder are of

complete knowledge relating the Fund issues. The Fund conducted various programme

such as seminars, advertisements in news papers and televisions, distribution of

promotional materials and physical client visit. Despite these awareness, the Fund also

20

participated Dar es Salaam International Trade Fair and National Agricultural Exhibition

(Nane Nane) held in Dar es Salaam and Dodoma respectively.

21

CORPORATE AND INTERNATIONAL RELATIONS

The Fund cooperates with other social security institution in upgrading different policy

governing the sector. The Fund has registered with East and Central African Social

Security Association (ECASSA) and International Social Security Association (ISSA).

During the year the Fund visited Social Security and National Insurance Trust (SSNIT) of

Ghana for learning on the provision of the social protection to the informal sector. Both

SSNIT and GEPF are members of the ISSA where it is encouraged to share information.

A group picture of GEPF delegation with Management of SISF after brief presentation of the SSNIT Informal Sector

Fund

22

BOARD’S STATEMENT ON CORPORATE GOVERNANCE FOR THE YEAR ENDED 30 JUNE 2009 The Board recognises the importance of good corporate governance in discharging its

responsibilities, protecting and enhancing shareholders' value through various policies.

The Board adopts and applies the principles and best practices as governed by the Social

Security Regulator.

A. Directors

(i) The Board

The Board is primarily responsible for the strategic directions of the Fund and is scheduled

to meet at least eight (8) times a year. However, additional meetings may be convened as

and when deemed necessary as determined by the members of the Board. The Board

make various decisions regarding Fund‘s operations in the interest of the members .

(ii) Board Balance & Composition

The current Board has five (7) members comprising six (6) Non-Executive who have been

nominated by the Ministry of Finance and Economic Affairs. Together, the Directors bring a

wide range of experience relevant to the direction and objectives of the Fund. A brief

description of the background of each Director is presented on pages 7 of this Annual

Report.

AUDIT COMMITTEE

The Audit Committee Charter was formed for the purpose of assisting of directors in

fulfilling its oversight responsibility relating to the integrity of the performance of internal

auditor, the annual independent audit of the company‘s financial statements, the

engagement of the independent auditors and the evaluation of the independent auditors‘

qualifications.In discharging its responsibilities, the Committee is not itself responsible for

the planning or conduct of audits or for any determination that the Company‘s financial

statements are complete and accurate or in accordance with generally accepted

accounting principles. This is the responsibility of management and the independent

auditors.

Members of the Audit Committee during the year 2009-10 were; 1. Dr. M.I. Nchimbi Chairperson

23

2. Mr. L.M. Salema Member 3. Mr. W.G. Gumbu Member The Committee held 2 meetings during the year. The Chief Internal auditor (CIA) is the secretary to the Committee. The Chief Executive Officer and Manager of Finance and Administration attend all meetings.

24

STATEMENT OF BOARD OF MANAGEMENT’S RESPONSIBILITIES

GEPF Act of 1942 and Public Finance Act 2001 (revised 2004) require the Fund to prepare

the Financial Statements for each financial year. It is also requires the Management to

ensure that the Fund keeps proper accounting records of its income, expenditure, assets

and liabilities.

The Board of Management is responsible for the preparation and fair presentation of these

financial statements in accordance with the International Financial Reporting Standards

(IFRS). This responsibility includes: designing, implementing and maintaining internal

controls relevant to the preparation and fair presentation of financial statements that are

free from material misstatement, whether due to fraud or error, selecting and applying

appropriate accounting policies, and making accounting estimates that are reasonable in

the circumstances.

The Board of Management accepts responsibility for the financial statements, which have

been prepared using appropriate accounting policies supported by reasonable and prudent

judgements and estimates, in conformity with International Financial Reporting Standards,

GEPF Act of 1942 and the Public Finance Act 2001 (revised 2004). The Board of

Management are of the opinion that the financial statements give a true and fair view of the

financial transactions of the Fund and of the disposition of its assets and liabilities, other

than liabilities to pay benefits falling due after the end of the year. The Board of

Management further accept responsibility for the maintenance of accounting records which

may be relied upon in the preparation of financial statements, as well as for safeguarding

the assets of the Fund and hence for taking reasonable steps for the prevention of fraud

and other irregularities.

The Board of Management certify that, to the best of their knowledge and belief, the

information furnished to the auditors for the purposes of the audit was correct and

complete in every respect.

25

------------------------------------ ---------------------------------

M. L. Mwamunyange D. M. Msangi

Chairperson Secretary

……………………………. 2010 ………………………2010

26

INDEPENDENT AUDITORS’ REPORT TO THE CHAIRPERSON OF THE

BOARD OF MANAGEMENT OF GOVERNMENT EMPLOYEES PROVIDENT FUND Report on the Financial Statements

1. We have audited the accompanying financial statements of the Government Employees Provident Fund, set out on pages 8 to 31 which comprise the statement of net assets as at 30 June 2009, and the statement of changes in net assets and cash flow statement for the year then ended, and a summary of significant accounting policies and other explanatory notes. Managements’ Responsibility for the Financial Statements

2. The Management are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards and the requirements of the Public Finance Act No. 6 of 2001 (revised 2004), and Cap. 51 as amended by Cap.52 of 1965. This responsibility includes: designing, implementing and maintaining internal controls relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors‘ Responsibility

3. Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on our judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, we considered the internal controls relevant to the Fund‘s preparation and fair presentation of the financial statements in order to design audit procedures that were appropriate in the circumstances, but not for the purpose of expressing an opinion on the Fund‘s internal controls. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our qualified audit opinion.

Unqualified Opinion

In our opinion, the accompanying financial statements give a true and fair view of the state of financial affairs of the company as at 30 June 2009 and of disposition at that date of its assets and liabilities other than liabilities to pay benefits falling due after the year end, in accordance with International Financial Reporting Standards.

27

Report on Other Legal Requirements

4. As required by the Public Finance Act No.6 of 2001, Public Procurement Act No. 21 of 2004 and GEPF Cap.51, as amended by GEPF Cap.52 of 1965, we report to you, based on our audit, that: i) we have obtained all the information and explanations which to the best of our knowledge and

belief were necessary for the purposes of our audit; ii) in our opinion proper books of account have been kept by the Fund, so far as appears from our

examination of those books; iii) the Fund‘s statement of net assets is in agreement with the books of account and iv) In consideration of the procurement transactions and processes we reviewed as part of the audit,

we state that the Fund has generally complied with the Public Procurement Act together with its regulations.

Deloitte & Touche Dar es Salaam Signed by: E A Harunani ……………………… 2010

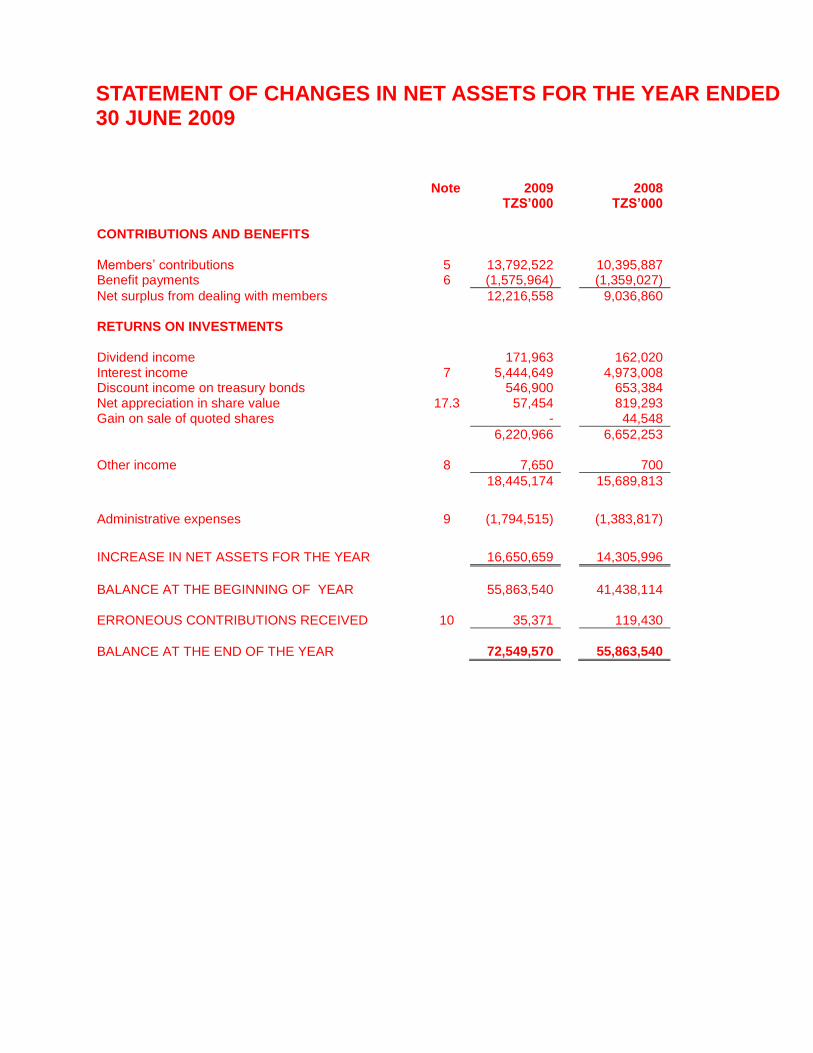

STATEMENT OF CHANGES IN NET ASSETS FOR THE YEAR ENDED 30 JUNE 2009

Note 2009 2008 TZS’000 TZS’000 CONTRIBUTIONS AND BENEFITS

Members‘ contributions 5 13,792,522 10,395,887 Benefit payments 6 (1,575,964) (1,359,027)

Net surplus from dealing with members 12,216,558 9,036,860 RETURNS ON INVESTMENTS Dividend income 171,963 162,020 Interest income 7 5,444,649 4,973,008 Discount income on treasury bonds 546,900 653,384 Net appreciation in share value 17.3 57,454 819,293 Gain on sale of quoted shares - 44,548

6,220,966 6,652,253 Other income 8 7,650 700

18,445,174 15,689,813

Administrative expenses 9 (1,794,515) (1,383,817)

INCREASE IN NET ASSETS FOR THE YEAR 16,650,659 14,305,996

BALANCE AT THE BEGINNING OF YEAR 55,863,540 41,438,114 ERRONEOUS CONTRIBUTIONS RECEIVED 10 35,371 119,430

BALANCE AT THE END OF THE YEAR 72,549,570 55,863,540

STATEMENT OF NET ASSETS AS AT 30 JUNE 2009 2009 2008 Note TZS’000 TZS’000 NON CURRENT ASSETS Property and equipment 11 1,162,322 55,970 Intangible assets 12 146,609 193,179 Members and staff loans 13 868,874 524,524

2,177,805

773,673

INVESTMENTS TANESCO Loan 14 2,000,000 2,000,000 Corporate bond 15 1,600,000 800,000 Treasury bonds 16 22,919,554 17,380,833 Treasury Bills 14,556,605 11,845,499 Government stocks 4,409 4,409 Quoted shares 17.1 4,134,953 3,208,742 Unit Trust of Tanzania 17.2 1,776,138 1,638,922 Short term deposits 18 20,040,000 15,790,000

67,031,659

52,668,405

CURRENT ASSETS Members and staff loans 13 257,770 156,677 Prepayments and other receivables 19 10,696 240,568 Interest receivable 20 1,538,134 1,294,302 Contributions receivable 687,930 391,025 Cash and bank balances 21 921,209 385,895

3,415,739

2,468,467

TOTAL ASSETS 72,625,203 55,910,545

CURRENT LIABILITIES

Benefits and other payables 22 75,633 47,005

NET ASSETS

72,549,570

55,863,540

REPRESENTED BY:

FUND BALANCE

23

72,549,570

55,863,540

The financial statements on pages 12 to 31 were approved by the Board of Management on …………….2010 and signed on its behalf by: -------------------------------------------- ---------------------------------------- M. L. Mwamunyange D. M. Msangi Chairperson Secretary

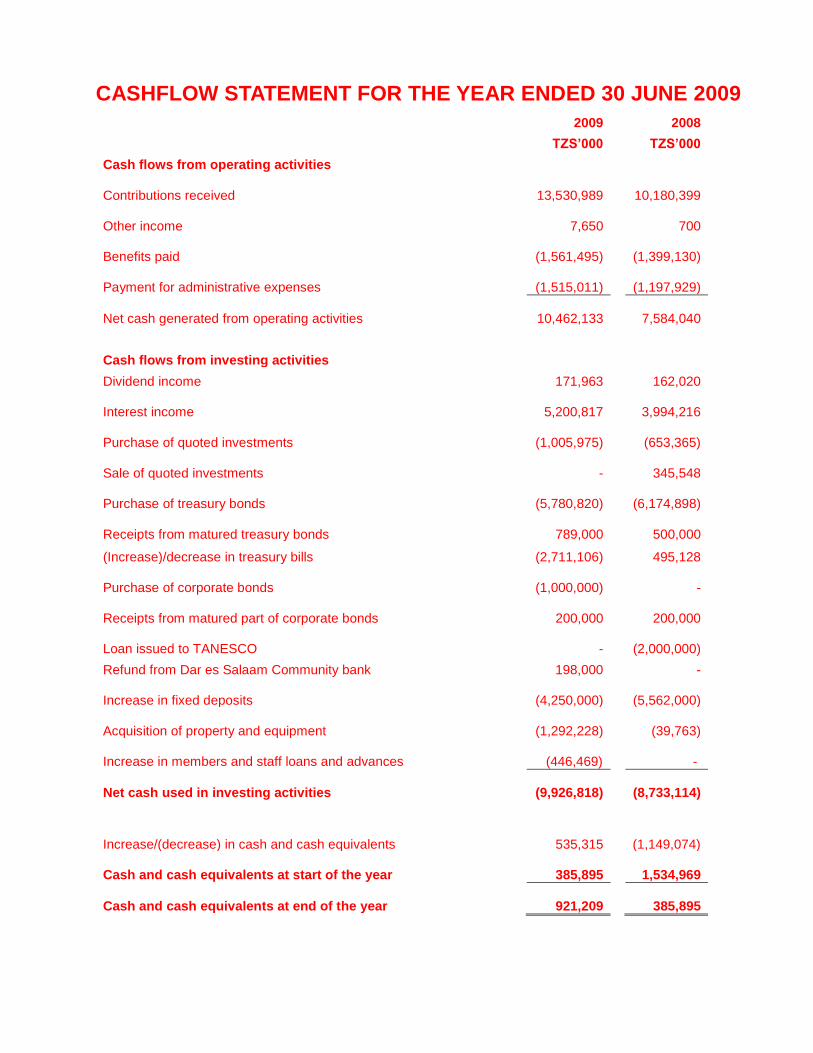

CASHFLOW STATEMENT FOR THE YEAR ENDED 30 JUNE 2009

2009 2008

TZS’000 TZS’000

Cash flows from operating activities

Contributions received

13,530,989

10,180,399

Other income

7,650

700

Benefits paid

(1,561,495)

(1,399,130)

Payment for administrative expenses

(1,515,011)

(1,197,929)

Net cash generated from operating activities 10,462,133

7,584,040

Cash flows from investing activities

Dividend income 171,963 162,020

Interest income

5,200,817

3,994,216

Purchase of quoted investments

(1,005,975)

(653,365)

Sale of quoted investments

-

345,548

Purchase of treasury bonds

(5,780,820)

(6,174,898)

Receipts from matured treasury bonds

789,000

500,000

(Increase)/decrease in treasury bills (2,711,106)

495,128

Purchase of corporate bonds

(1,000,000)

-

Receipts from matured part of corporate bonds

200,000

200,000

Loan issued to TANESCO

-

(2,000,000)

Refund from Dar es Salaam Community bank 198,000 -

Increase in fixed deposits

(4,250,000)

(5,562,000)

Acquisition of property and equipment

(1,292,228)

(39,763)

Increase in members and staff loans and advances

(446,469)

-

Net cash used in investing activities

(9,926,818)

(8,733,114)

Increase/(decrease) in cash and cash equivalents

535,315

(1,149,074)

Cash and cash equivalents at start of the year

385,895

1,534,969

Cash and cash equivalents at end of the year

921,209

385,895

NOTES TO THE FINANCIAL STATEMENTS 1. STATEMENT OF COMPLIANCE

The financial statements have been prepared in accordance with the International Financial Reporting Standards. The principal accounting policies adopted in the preparation of these financial statements are stated below:

Adoption of new and revised standards and interpretations Standards and Interpretations effective in the current period

The following new interpretations issued by the International Financial Reporting Interpretations Committee and revised standard are effective for the current period:

IFRIC 12, Service Concession Arrangements (effective 1 January 2008);

IFRIC 13, Customer Loyalty Programmes (effective 1 July 2008);

IFRIC 14, IAS 19 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their interaction (effective 1 January 2008);

IFRIC 16, Hedges of a Net Investment in a Foreign Operation (effective 1 October 2008).

The adoption of these Interpretations and a revised standard has not led to any changes in the Company‘s accounting policies.

Standards and Interpretations in issue not yet effective

At the date of authorization of these financial statements, the following amendments to Standards and new Interpretations were in issue but not yet effective:

IFRIC 15, Agreements for the construction of Real Estate (effective for accounting periods beginning on or after 1 January 2009);

IFRIC 17, Distributions of Non-cash Assets to Owners (effective for accounting periods on or after 1 January 2009);

IFRIC 18, Transfers of Assets from Customers (effective for accounting periods on or after 1 July 2009);

IFRS 1, First-Time Adoption of International Financial Reporting Standards – Amendment relating to cost of an investment on first-time adoption (effective for accounting periods beginning on or after 1 January 2009);

IFRS2, Share-based Payment — Amendment relating to vesting conditions and cancellations (effective for accounting periods beginning on or after 1 January 2009);

IFRS 3, Business Combinations – Comprehension revision on applying the acquisition method (effective for accounting periods beginning on or after 1 July 2009);

IFRS 7, Financial Instruments: Disclosures, Amendments enhancing disclosures about fair value and liquidity risk (effective for annual periods beginning on or after 1 January 2009);

IFRS 8, Operating Segments (effective for accounting periods beginning on or after 1 January 2009);

IAS 1, Presentation of financial Statements - Comprehensive revision including requiring a statement of comprehensive income and Amendments relating to disclosure of puttable instruments and obligations arising on liquidation (effective for accounting periods on or after 1 January 2009);

IAS 23, Borrowing Costs - Comprehensive revision to prohibit immediate expensing (effective for accounting periods on or after 1 January 2009);

IAS 27, Consolidated and Separate Financial Statements — Amendment relating to cost of an investment on first-time adoption (effective for accounting periods beginning on or after 1 January 2009);

Adoption of new and revised International Financial Reporting Standards (IFRSs) (Continued)

IAS 27, Consolidated and Separate Financial Statements: Consequential amendments arising from amendments to IFRS 3 (effective for accounting periods beginning on or after 1 July 2009);

IAS 28, Investments in Associates: Consequential amendments arising from amendments to IFRS 3 (effective for accounting periods beginning on or after 1 July 2009);

IAS 31, Interests in Joint Ventures: Consequential amendments arising from amendments to IFRS 3 (effective for accounting periods beginning on or after 1 July 2009);

IAS 32, Financial Instruments: Presentation: Amendments relating to puttable instruments and obligations arising on liquidation (effective for accounting periods beginning on or after 1 January 2009);

IAS 39, Financial Instruments: Recognition and Measurement: Amendments for embedded derivatives when reclassifying financial instruments (effective for accounting periods beginning on or after 30 June 2009);

IAS 39, Financial Instruments: Recognition and Measurement: Amendments for eligible hedged items (effective for accounting periods beginning on or after 1 July 2009);

―Improvements to IFRSs‖ were issued in May 2008 and April 2009 and their requirements are effective over a range of dates, with the earliest effective date being for annual periods beginning on or after 1 January 2009. This comprises a number of amendments to IFRSs, which resulted from the IASB‘s annual improvements project. The directors are currently assessing the impact and expected timing of adoption of these amendments on the Company‘s results and financial position.

Adoption of other Standards and Interpretations, when effective, is not expected to have material impact on the financial statements of the company.

2. ACCOUNTING POLICIES

Basis of preparation

The financial statements have been prepared on the historical cost basis except for the revaluation of certain non-current assets and financial instruments. A historical cost is generally based on the fair value of the consideration given in exchange for assets. The principal accounting policies are set out below.

Taxation The Fund is not an approved fund as per Income Tax Act 2004. Management has sought clarification on the fund‘s tax status from Tanzania Revenue Authority and Treasury and is waiting for final decision. No provision for tax liabilities have been made due to the tax status uncertainty.

Property and equipments Property and equipments are held for administration purposes stated in the statement of net assets at cost less accumulated depreciation. Depreciation is recognised so as to write off the cost of assets (other than freehold land and properties under construction) less their residual values over their useful lives, using the straight-line method. The estimated useful lives, residual values and depreciation method are reviewed at each year end, with the effect of any changes in estimate accounted for on a prospective basis.

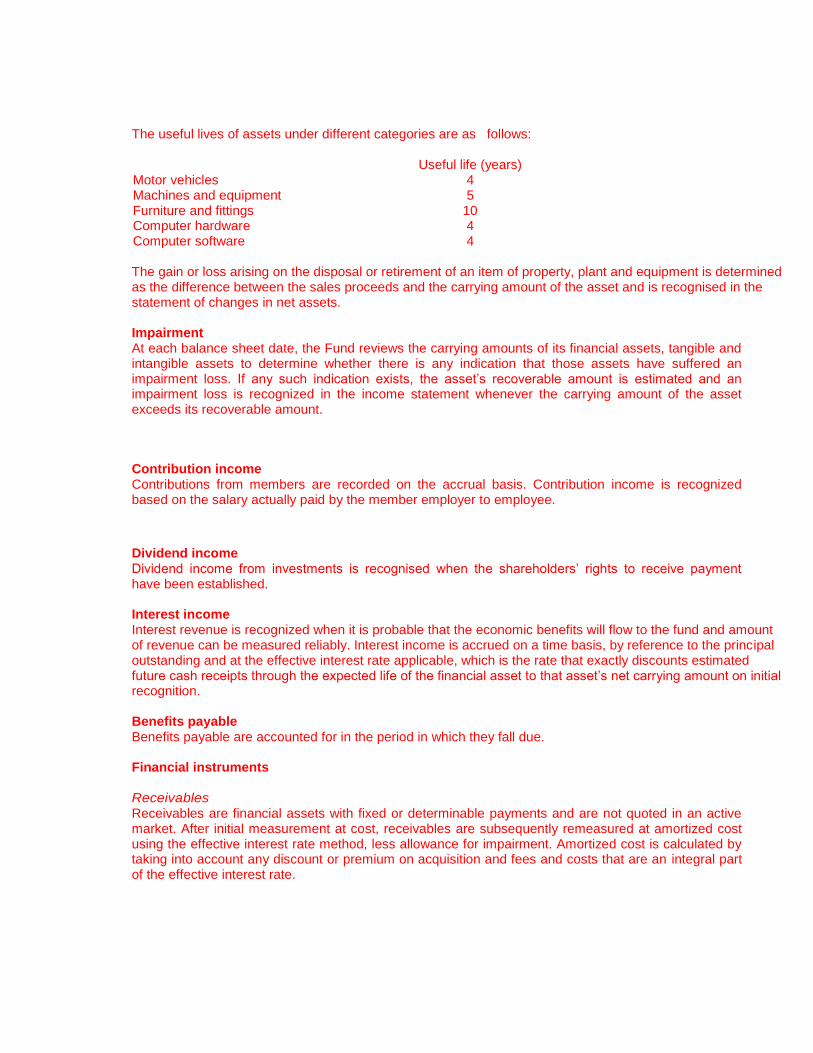

The useful lives of assets under different categories are as follows:

Useful life (years) Motor vehicles 4 Machines and equipment 5 Furniture and fittings 10 Computer hardware 4 Computer software 4 The gain or loss arising on the disposal or retirement of an item of property, plant and equipment is determined as the difference between the sales proceeds and the carrying amount of the asset and is recognised in the statement of changes in net assets.

Impairment At each balance sheet date, the Fund reviews the carrying amounts of its financial assets, tangible and intangible assets to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the asset‘s recoverable amount is estimated and an impairment loss is recognized in the income statement whenever the carrying amount of the asset exceeds its recoverable amount.

Contribution income Contributions from members are recorded on the accrual basis. Contribution income is recognized based on the salary actually paid by the member employer to employee.

Dividend income Dividend income from investments is recognised when the shareholders‘ rights to receive payment have been established.

Interest income Interest revenue is recognized when it is probable that the economic benefits will flow to the fund and amount of revenue can be measured reliably. Interest income is accrued on a time basis, by reference to the principal outstanding and at the effective interest rate applicable, which is the rate that exactly discounts estimated future cash receipts through the expected life of the financial asset to that asset‘s net carrying amount on initial recognition.

Benefits payable Benefits payable are accounted for in the period in which they fall due.

Financial instruments

Receivables Receivables are financial assets with fixed or determinable payments and are not quoted in an active market. After initial measurement at cost, receivables are subsequently remeasured at amortized cost using the effective interest rate method, less allowance for impairment. Amortized cost is calculated by taking into account any discount or premium on acquisition and fees and costs that are an integral part of the effective interest rate.

Financial assets at fair value through profit or loss Financial assets through profit or loss are those which were either acquired for generating a profit from short-term fluctuations in price or dealer's margin, or are securities included in a portfolio in which a pattern of short-term profit-taking exists. Investments held for trading are initially recognised at cost and subsequently re-measured to fair value based on quoted bid prices or dealer price quotations, without any deduction for transaction costs. All related realised and unrealised gains and losses are included in the income statement. Interest earned whilst holding held for trading investments is reported as interest income.

Held to maturity investments Held to maturity financial investments are those which carry fixed or determinable payments and have fixed maturities and which the Fund has the intention and ability to hold to maturity. After initial measurement, held to maturity financial investments are subsequently measured at amortised cost using the effective interest rate method, less allowance for impairment. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees that are an integral part of the effective interest rate. The amortisation and losses arising from impairment of such investments are recognised in the income statement.

Available for sale financial assets Investment securities intended to be held for an indefinite period of time, which may be sold in response to needs for liquidity, or changes in interest rates, exchange rates or equity prices are classified as available for sale and are initially recognised at cost. Available for sale investments are subsequently re-measured at fair value, based on quoted bid prices or amount derived from cash flow models. Unrealised gains and losses arising from changes in the fair value of securities classified as available for sale are recognised directly in statement of net assets until the asset is de-recognised, at which time the cumulative gains or losses previously recognised in statement of net assets shall be recognised in the income statement.

Investment in Quoted equity Investment in Quoted investments are classified as fair value through profit or loss and investment properties are stated at market values as estimated at the balance sheet date. Investments in quoted stocks and shares are stated at market value and any surplus arising there from is recognized at investment income in the statement of change in net assets.

Investments in Unquoted companies

Investments in Unquoted companies are measured at cost less any impairment.

Government securities

Government securities comprise Treasury bills and Treasury bonds, the debt securities of which are issued by the Government of Tanzania. These are investments with fixed maturity that the fund have the intent and ability to hold to maturity are classified as held-to-maturity and are carried at amortised cost.

Corporate bonds

Corporate bonds are classified as financial instruments fair value through profit or loss and are stated at fair value.

Loan to corporate Loan to corporate are classified as financial instruments, the Loan is stated in the balance sheet at fair value.

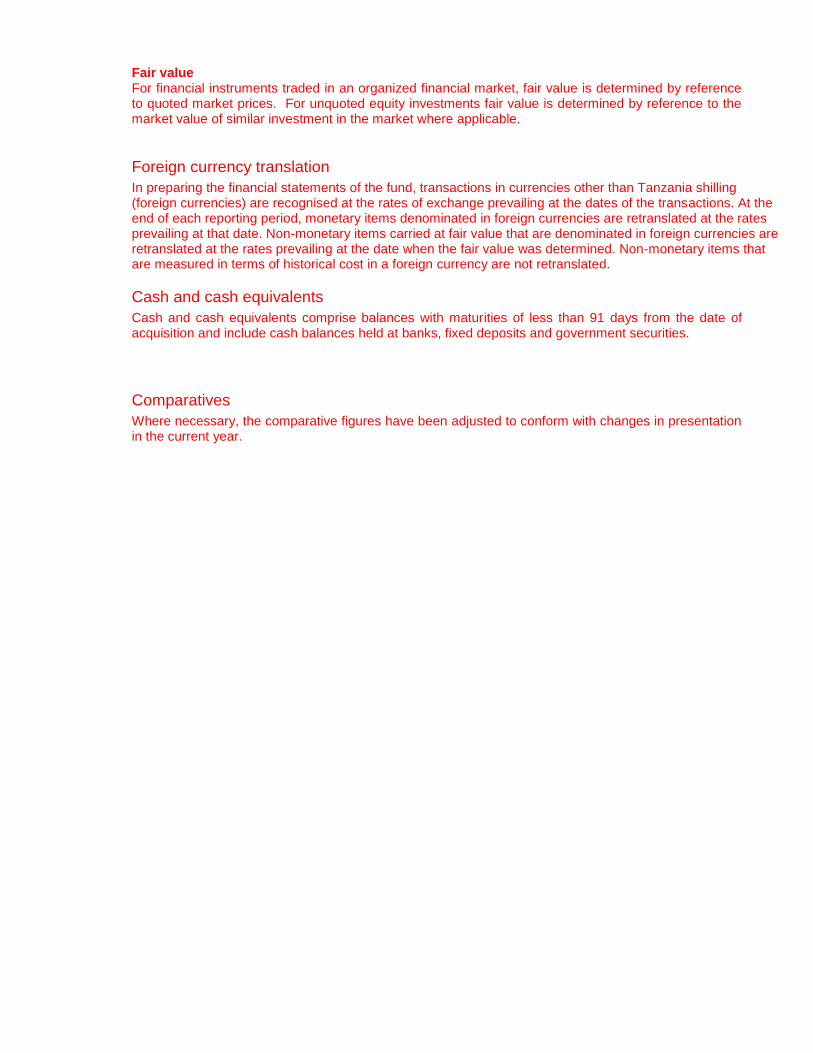

Fair value For financial instruments traded in an organized financial market, fair value is determined by reference to quoted market prices. For unquoted equity investments fair value is determined by reference to the market value of similar investment in the market where applicable.

Foreign currency translation

In preparing the financial statements of the fund, transactions in currencies other than Tanzania shilling (foreign currencies) are recognised at the rates of exchange prevailing at the dates of the transactions. At the end of each reporting period, monetary items denominated in foreign currencies are retranslated at the rates prevailing at that date. Non-monetary items carried at fair value that are denominated in foreign currencies are retranslated at the rates prevailing at the date when the fair value was determined. Non-monetary items that are measured in terms of historical cost in a foreign currency are not retranslated.

Cash and cash equivalents

Cash and cash equivalents comprise balances with maturities of less than 91 days from the date of acquisition and include cash balances held at banks, fixed deposits and government securities.

Comparatives

Where necessary, the comparative figures have been adjusted to conform with changes in presentation in the current year.

3. CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS IN APPLYING THE FUND’S ACCOUNTING POLICIES

In the process of applying the Fund‘s accounting policies, Management has made estimates and assumptions that affect the reported amounts of assets and liabilities within the next financial year. Estimates and judgements are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances. These are dealt with below:

Held -to-maturity investments The Fund follows the guidance of IAS 39 on classifying non-derivative financial assets with fixed or determinable payments and fixed maturity as held-to-maturity. This classification requires significant judgement. In making this judgement, the bank evaluates its intention and ability to hold such investments to maturity. If the Fund fails to keep these investments to maturity other than for the specific circumstances – for example, selling an insignificant amount close to maturity – it will be required to reclassify the entire class as available-for-sale. The investments would therefore be measured at fair value not amortised cost.

Impairment losses on financial assets At each balance sheet date, the Fund reviews the carrying amounts of its financial assets to determine whether there is any indication that these assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated and an impairment loss is recognised in the income statement whenever the carrying amount of the asset exceeds its recoverable amount.

4. FINANCIAL RISK MANAGEMENT

The Fund‘s operations expose it to a variety of financial risks; including credit risk and market risk (price risk, foreign currency exchange rates and interest rates). The Fund‘s overall risk management programme focuses on the unpredictability of financial markets and seeks to minimise potential adverse effects on its financial performance. Risk management is carried out by management on behalf of the Board of Management under the approved policies.

The Management reviews the market trends and information available to evaluate the potential exposures and in the final analysis come up with the strategies to mitigate the market risks. The Board of Management provide guidelines for overall risk management, as well as policies covering specific areas such as foreign exchange risk, interest rate risk, credit risk, use of derivative and non-derivative financial instruments and investing excess liquidity.

Market risk

(i) Price risk

The Fund is exposed to equity securities price risk because of investments in quoted shares classified at fair value through profit and loss. Further the Fund is exposed to the risk that the value of debt securities will fluctuate due to changes in market value. To manage the price risk arising from investing in equity and debt securities, the Fund diversifies its portfolio. For equities, the Fund has invested in companies in different sectors of the economy, while for debt securities; the Fund has invested in bonds of varying maturities. Diversification of the portfolio is done in accordance with statement of investment policy. All quoted shares held by the Fund are traded on the Dar es Salaam Stock Exchange (DSE).

At 30 June 2009, if the price of shares had weakened/strengthened by 5%, all other variables held constant, the impact on pre-tax profit for the year would have been TZS 295,555,000 (2008: TZS 242,383,000) higher/lower.

The carrying amounts of the company's investment in shares that will have an impact on profit or loss when price of shares change as at 30 September 2009 are as follows:

2009 TZS’000

2008 TZS’000

Investment in quoted shares

4,134,953

3,208,742

Investment in Unit Trust of Tanzania 1,776,138 1,638,922

5,911,091

4,847,664

Market risk

(i) Interest rate risk

The Fund‘s interest bearing assets are investments in treasury bonds, loan to corporate, corporate bonds, treasury bills and fixed deposits. All these instruments are at fixed interest rates except corporate loan to Tanzania Electricity Supplies Company Limited which is at floating interest rates which is equal to 182 days treasury bills interest rates plus a margin which ranges from 2% to 0.5% depending on the amount of 182 treasury bills interest rates. There is a remote chance that movement in interest rates of treasury bills will adversely affect the Fund as adverse movement in treasury bills exchange rate is covered by increase in margin that is added to 182 treasury bills interest rates.

The nature of other financial instruments held, that is, fixed interest instruments mitigates risk exposure of the Fund. Fluctuations in interest rates will have an insignificant effect to the Fund.

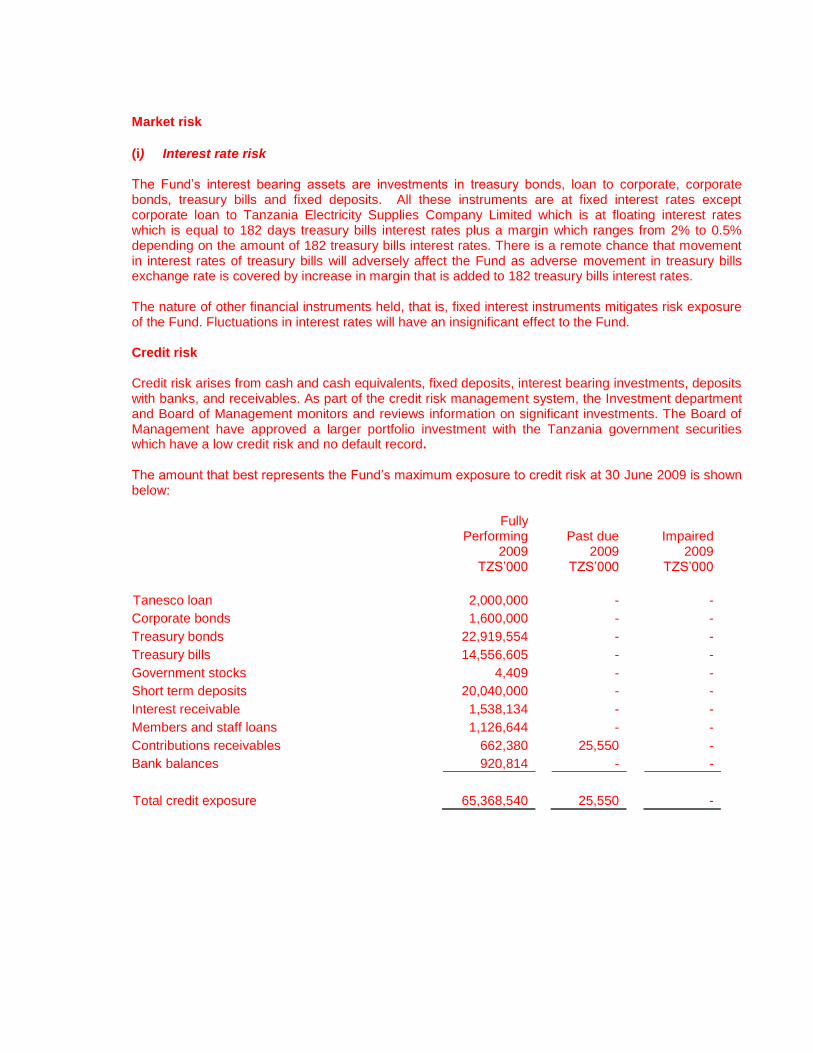

Credit risk

Credit risk arises from cash and cash equivalents, fixed deposits, interest bearing investments, deposits with banks, and receivables. As part of the credit risk management system, the Investment department and Board of Management monitors and reviews information on significant investments. The Board of Management have approved a larger portfolio investment with the Tanzania government securities which have a low credit risk and no default record.

The amount that best represents the Fund‘s maximum exposure to credit risk at 30 June 2009 is shown below:

Fully

Performing

Past due Impaired

2009

TZS‘000 2009

TZS‘000 2009

TZS‘000

Tanesco loan 2,000,000 - -

Corporate bonds 1,600,000 - -

Treasury bonds 22,919,554 - -

Treasury bills 14,556,605 - -

Government stocks 4,409 - -

Short term deposits 20,040,000 - -

Interest receivable 1,538,134 - -

Members and staff loans 1,126,644 - -

Contributions receivables 662,380 25,550 -

Bank balances 920,814 - -

Total credit exposure 65,368,540 25,550 -

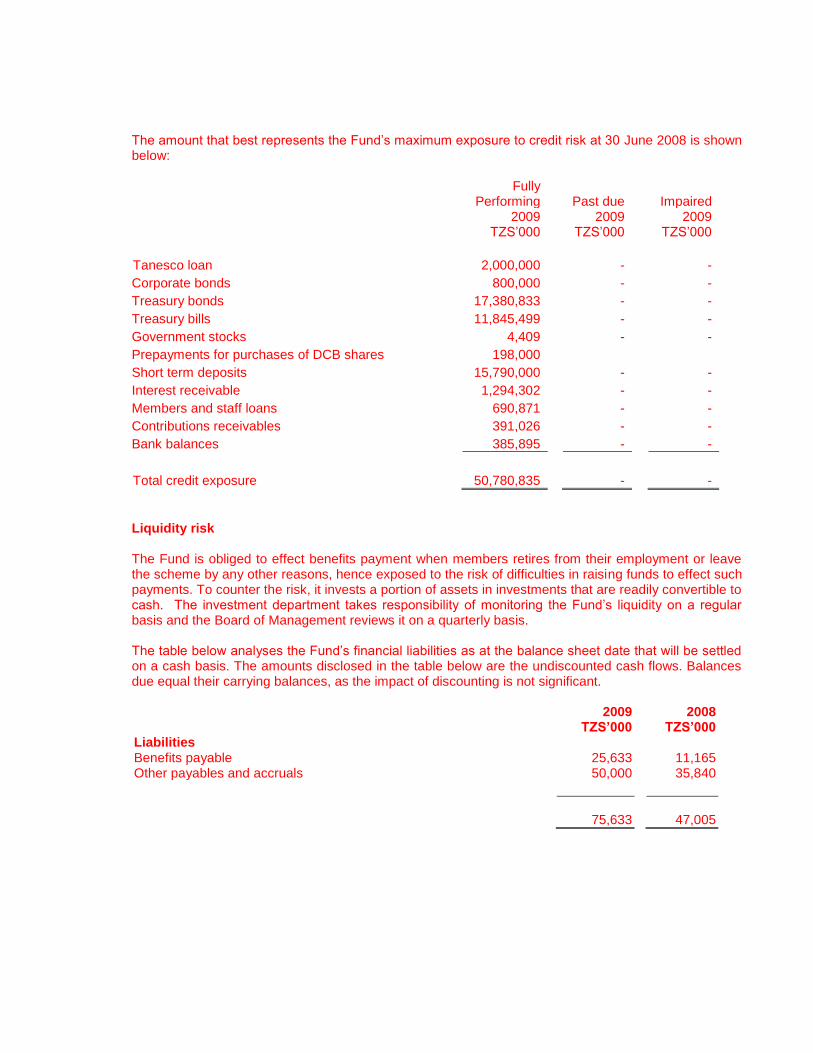

The amount that best represents the Fund‘s maximum exposure to credit risk at 30 June 2008 is shown below:

Fully

Performing

Past due Impaired

2009

TZS‘000 2009

TZS‘000 2009

TZS‘000

Tanesco loan 2,000,000 - -

Corporate bonds 800,000 - -

Treasury bonds 17,380,833 - -

Treasury bills 11,845,499 - -

Government stocks 4,409 - -

Prepayments for purchases of DCB shares 198,000

Short term deposits 15,790,000 - -

Interest receivable 1,294,302 - -

Members and staff loans 690,871 - -

Contributions receivables 391,026 - -

Bank balances 385,895 - -

Total credit exposure 50,780,835 - -

Liquidity risk

The Fund is obliged to effect benefits payment when members retires from their employment or leave the scheme by any other reasons, hence exposed to the risk of difficulties in raising funds to effect such payments. To counter the risk, it invests a portion of assets in investments that are readily convertible to cash. The investment department takes responsibility of monitoring the Fund‘s liquidity on a regular basis and the Board of Management reviews it on a quarterly basis.

The table below analyses the Fund‘s financial liabilities as at the balance sheet date that will be settled on a cash basis. The amounts disclosed in the table below are the undiscounted cash flows. Balances due equal their carrying balances, as the impact of discounting is not significant.

2009 2008

TZS’000 TZS’000 Liabilities Benefits payable 25,633 11,165 Other payables and accruals 50,000 35,840

75,633 47,005

2009 2008 TZS’000 TZS’000

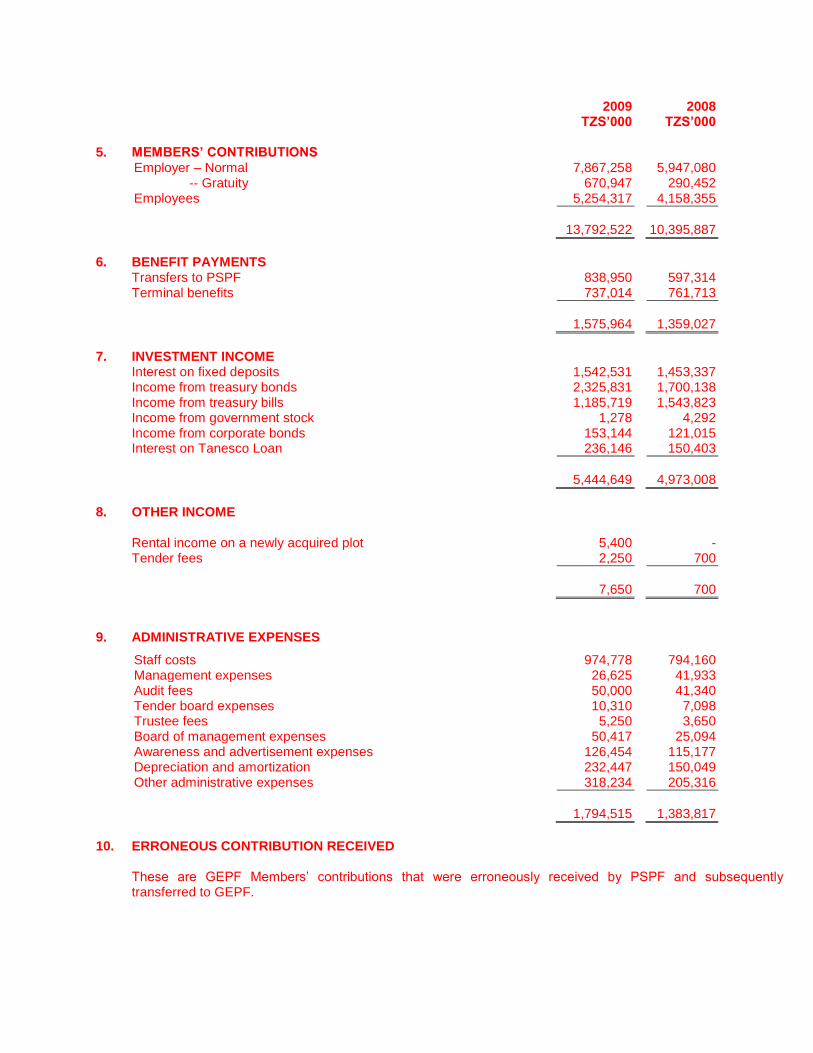

5. MEMBERS’ CONTRIBUTIONS

Employer – Normal 7,867,258 5,947,080 -- Gratuity 670,947 290,452 Employees 5,254,317 4,158,355

13,792,522

10,395,887

6. BENEFIT PAYMENTS

Transfers to PSPF 838,950 597,314 Terminal benefits 737,014 761,713

1,575,964

1,359,027

7. INVESTMENT INCOME

Interest on fixed deposits 1,542,531 1,453,337 Income from treasury bonds 2,325,831 1,700,138 Income from treasury bills 1,185,719 1,543,823 Income from government stock 1,278 4,292 Income from corporate bonds 153,144 121,015 Interest on Tanesco Loan 236,146 150,403

5,444,649

4,973,008

8. OTHER INCOME

Rental income on a newly acquired plot 5,400 - Tender fees 2,250 700

7,650

700

9. ADMINISTRATIVE EXPENSES

Staff costs 974,778

794,160 Management expenses 26,625 41,933 Audit fees 50,000 41,340 Tender board expenses 10,310 7,098 Trustee fees 5,250 3,650 Board of management expenses 50,417 25,094 Awareness and advertisement expenses 126,454 115,177 Depreciation and amortization 232,447 150,049 Other administrative expenses 318,234 205,316

1,794,515

1,383,817

10. ERRONEOUS CONTRIBUTION RECEIVED

These are GEPF Members‘ contributions that were erroneously received by PSPF and subsequently transferred to GEPF.

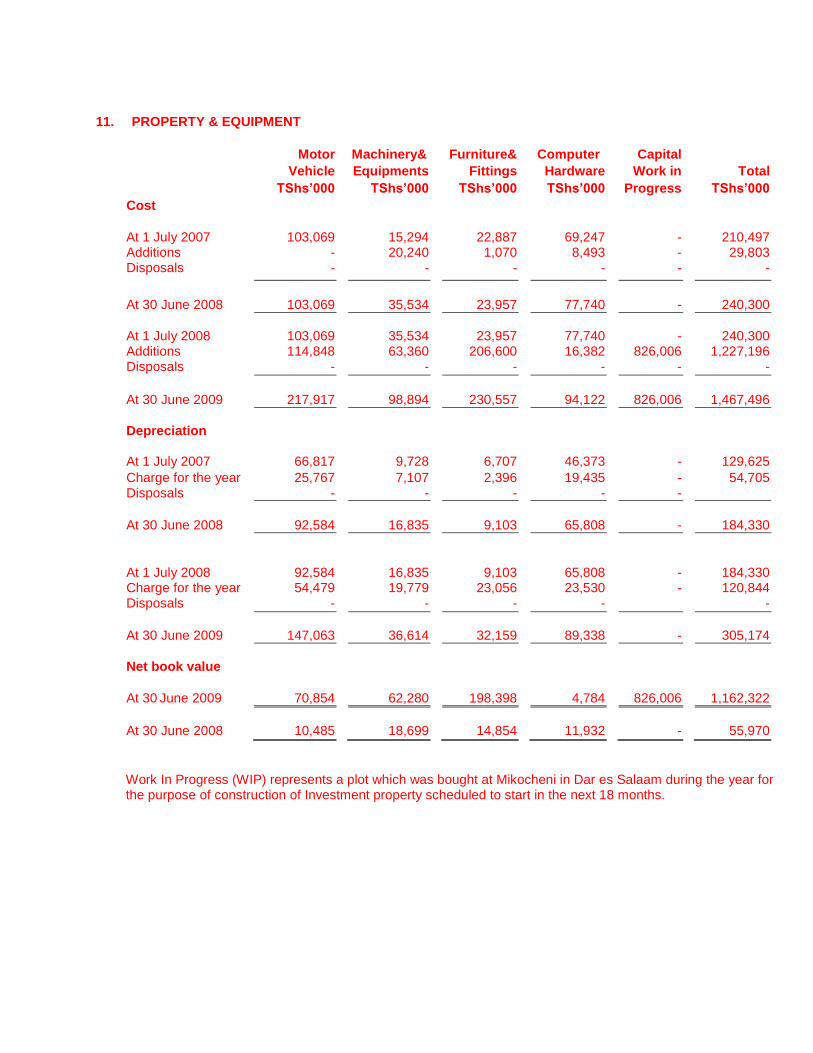

11. PROPERTY & EQUIPMENT

Motor Machinery& Furniture& Computer Capital

Vehicle Equipments Fittings Hardware Work in Total

TShs’000 TShs’000 TShs’000 TShs’000 Progress TShs’000

Cost

At 1 July 2007 103,069 15,294 22,887 69,247 - 210,497 Additions - 20,240 1,070 8,493 - 29,803 Disposals - - - - - -

At 30 June 2008 103,069 35,534 23,957 77,740 - 240,300

At 1 July 2008 103,069 35,534 23,957 77,740 - 240,300 Additions 114,848 63,360 206,600 16,382 826,006 1,227,196 Disposals - - - - - -

At 30 June 2009 217,917 98,894 230,557 94,122 826,006 1,467,496

Depreciation At 1 July 2007 66,817 9,728 6,707 46,373 - 129,625

Charge for the year 25,767 7,107 2,396 19,435 - 54,705 Disposals - - - - -

At 30 June 2008 92,584 16,835 9,103 65,808 - 184,330

At 1 July 2008 92,584 16,835 9,103 65,808 - 184,330 Charge for the year 54,479 19,779 23,056 23,530 - 120,844 Disposals - - - - -

At 30 June 2009 147,063 36,614 32,159 89,338 - 305,174

Net book value

At 30 June 2009 70,854 62,280 198,398 4,784 826,006 1,162,322

At 30 June 2008 10,485 18,699 14,854 11,932 - 55,970

Work In Progress (WIP) represents a plot which was bought at Mikocheni in Dar es Salaam during the year for the purpose of construction of Investment property scheduled to start in the next 18 months.

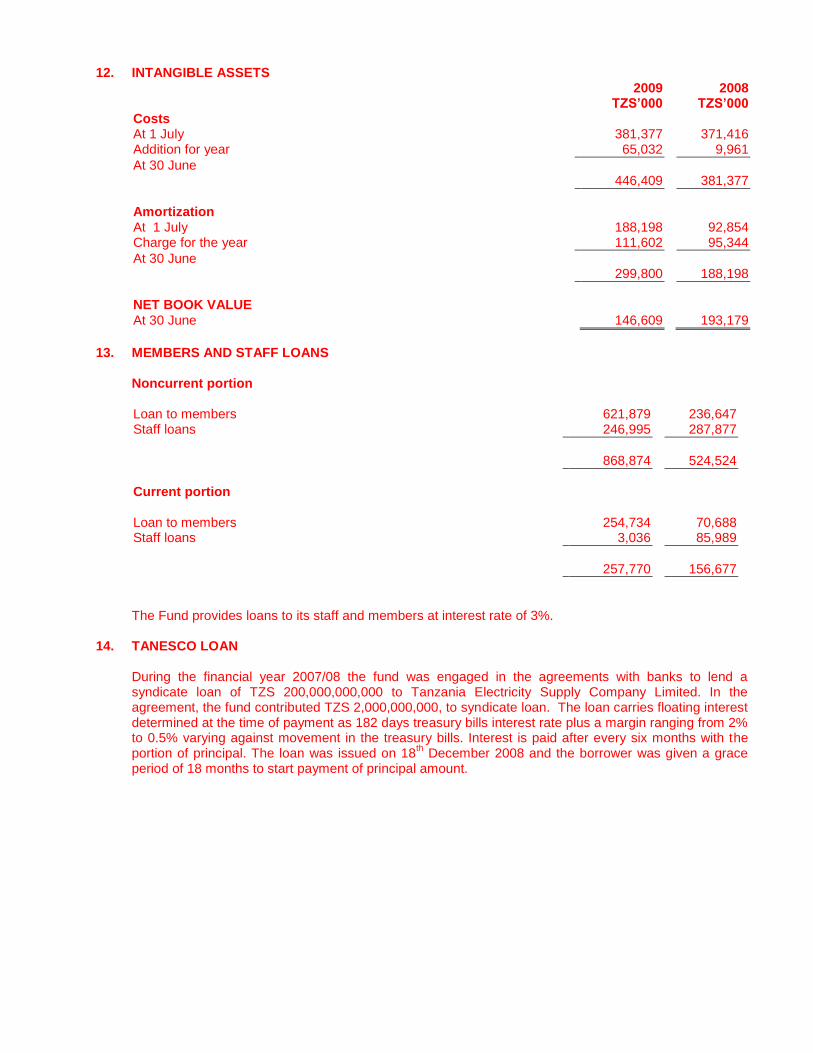

12. INTANGIBLE ASSETS 2009 2008 TZS’000 TZS’000 Costs At 1 July 381,377 371,416 Addition for year 65,032 9,961

At 30 June 446,409

381,377

Amortization At 1 July 188,198 92,854 Charge for the year 111,602 95,344

At 30 June 299,800

188,198

NET BOOK VALUE At 30 June 146,609 193,179

13. MEMBERS AND STAFF LOANS

Noncurrent portion Loan to members 621,879 236,647 Staff loans 246,995 287,877

868,874

524,524

Current portion

Loan to members 254,734 70,688 Staff loans 3,036 85,989

257,770

156,677

The Fund provides loans to its staff and members at interest rate of 3%.

14. TANESCO LOAN

During the financial year 2007/08 the fund was engaged in the agreements with banks to lend a syndicate loan of TZS 200,000,000,000 to Tanzania Electricity Supply Company Limited. In the agreement, the fund contributed TZS 2,000,000,000, to syndicate loan. The loan carries floating interest determined at the time of payment as 182 days treasury bills interest rate plus a margin ranging from 2% to 0.5% varying against movement in the treasury bills. Interest is paid after every six months with the portion of principal. The loan was issued on 18

th December 2008 and the borrower was given a grace

period of 18 months to start payment of principal amount.

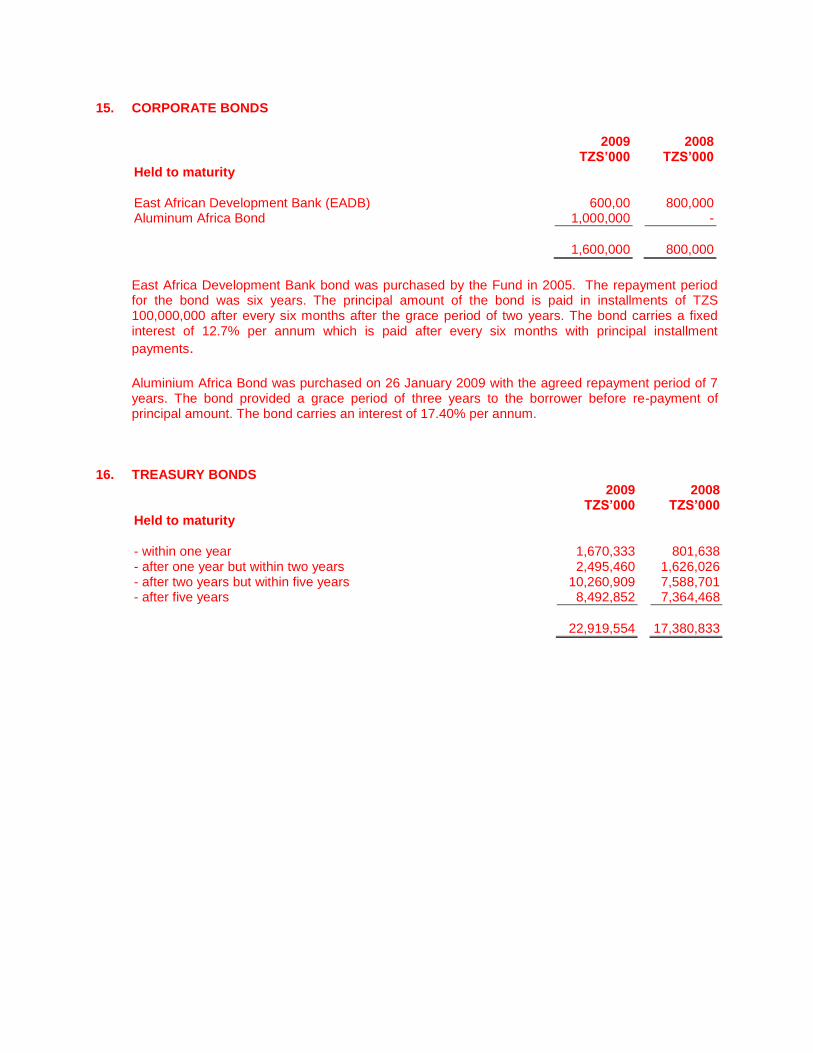

15. CORPORATE BONDS

2009 2008 TZS’000 TZS’000 Held to maturity

East African Development Bank (EADB) 600,00 800,000 Aluminum Africa Bond 1,000,000 -

1,600,000

800,000

East Africa Development Bank bond was purchased by the Fund in 2005. The repayment period for the bond was six years. The principal amount of the bond is paid in installments of TZS 100,000,000 after every six months after the grace period of two years. The bond carries a fixed interest of 12.7% per annum which is paid after every six months with principal installment

payments.

Aluminium Africa Bond was purchased on 26 January 2009 with the agreed repayment period of 7 years. The bond provided a grace period of three years to the borrower before re-payment of principal amount. The bond carries an interest of 17.40% per annum.

16. TREASURY BONDS 2009 2008 TZS’000 TZS’000 Held to maturity - within one year 1,670,333 801,638 - after one year but within two years 2,495,460 1,626,026 - after two years but within five years 10,260,909 7,588,701 - after five years 8,492,852 7,364,468

22,919,554

17,380,833

17.1 INVESTMENT IN QUOTED SHARES UNITS Amounts (TZS’000)

At 1 July

2008 Additions Disposal At 30 June

2009 At 1 July

2008 Additions Disposal Gain/(Loss)

in Fair value as at 30/06/2009

Market value at

30.06.2009

Market value at

30.06.2008

DAHACO (SWISSPORT)

301,957

-

-

301,957

208,350

-

-

(33,215)

175,135

208,350

Simba Cement Co. Ltd

221,617

-

-

221,617

381,181

-

-

22,161

403,343

381,181

Tanzania Cigarette Co. Ltd

207,674

-

207,674

336,432

-

-

24,921

361,354

336,432

Tanzania Breweries Co. ltd

400,000

-

-

400,000

824,000

-

-

(104,000)

720,000

824,000

Twiga Cement Co. Ltd

588,205

-

-

588,205

858,779

-

-

52,938

911,719

858,779

NICOL

2,000,000

-

-

2,000,000

600,000

-

-

(40,000)

560,000

600,000

NMB Bank - 986,773 - 986,773 - 795,824 - (65,612) 730,212 - CRDB Bank Plc - 1,400,975 - 1,400,975 - 210,146 - 63,044 273,190 -

Total

3,719,453

2,387,748

-

6,107,201

3,208,742

1,005,970

-

(79,763)

4,134,953

3,208,742

17.2 INVESTMENT IN UNIT TRUST OF TANZANIA (UTT)

UNITS Amounts (TZS’000)

At 1 July

2008 Additions Disposal At 30 June

2009 At 1 July

2008 Additions Disposal Gain/(Loss)

in Fair value as at 30/06/2009

Market value at

30.06.2009

Market value at

30.06.2008

11,428,570

-

-

11,428,570

1,638,922

-

-

137,215

1,776,138

1,638,922

17.3 GAIN ON VALUATION OF INVESTMENTS 2009

TZS’000 2008

TZS’000 Net (loss)/gain on quoted shares (79,763) 531,114 Gain on valuation of UTT units 137,215 288,179

57,454

819,293

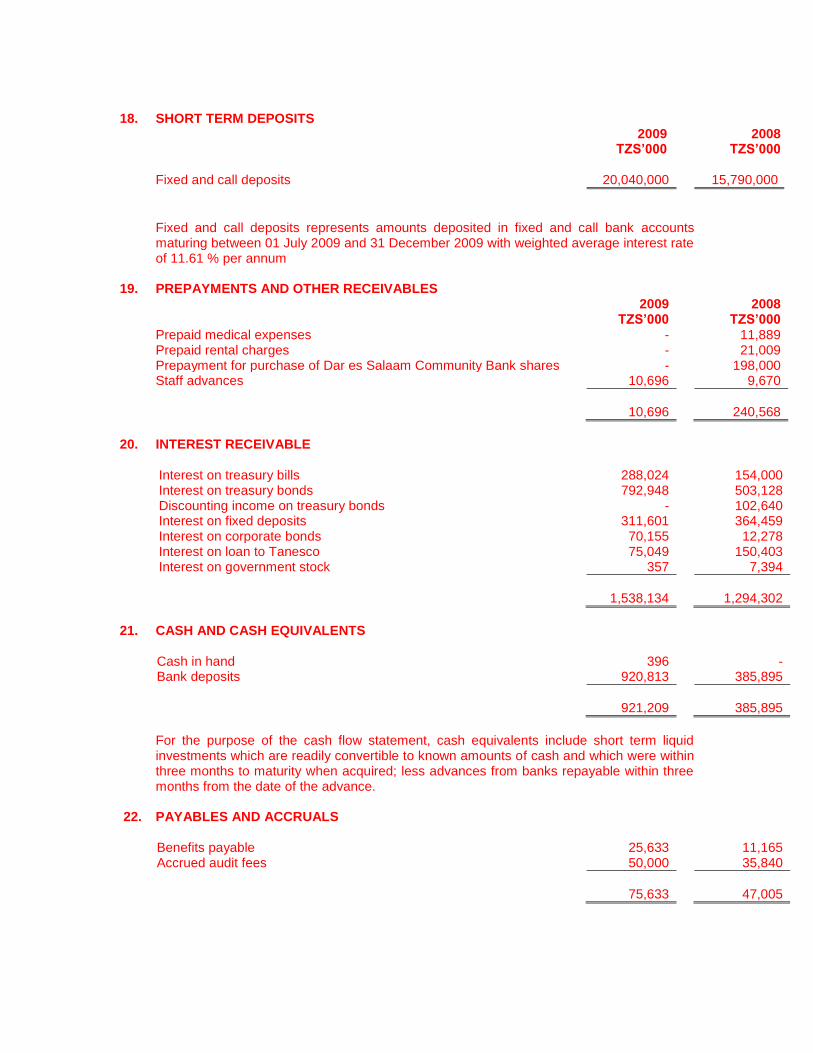

18. SHORT TERM DEPOSITS

2009 2008 TZS’000 TZS’000

Fixed and call deposits 20,040,000 15,790,000

Fixed and call deposits represents amounts deposited in fixed and call bank accounts maturing between 01 July 2009 and 31 December 2009 with weighted average interest rate of 11.61 % per annum

19. PREPAYMENTS AND OTHER RECEIVABLES

2009 2008 TZS’000 TZS’000 Prepaid medical expenses - 11,889 Prepaid rental charges - 21,009 Prepayment for purchase of Dar es Salaam Community Bank shares - 198,000 Staff advances 10,696 9,670

10,696

240,568

20. INTEREST RECEIVABLE

Interest on treasury bills 288,024 154,000 Interest on treasury bonds 792,948 503,128 Discounting income on treasury bonds - 102,640 Interest on fixed deposits 311,601 364,459 Interest on corporate bonds 70,155 12,278 Interest on loan to Tanesco 75,049 150,403 Interest on government stock 357 7,394

1,538,134

1,294,302

21. CASH AND CASH EQUIVALENTS

Cash in hand 396 - Bank deposits 920,813 385,895

921,209

385,895

For the purpose of the cash flow statement, cash equivalents include short term liquid investments which are readily convertible to known amounts of cash and which were within three months to maturity when acquired; less advances from banks repayable within three months from the date of the advance.

22. PAYABLES AND ACCRUALS

Benefits payable 25,633 11,165 Accrued audit fees 50,000 35,840

75,633

47,005

2009 2008 TZS’000 TZS’000

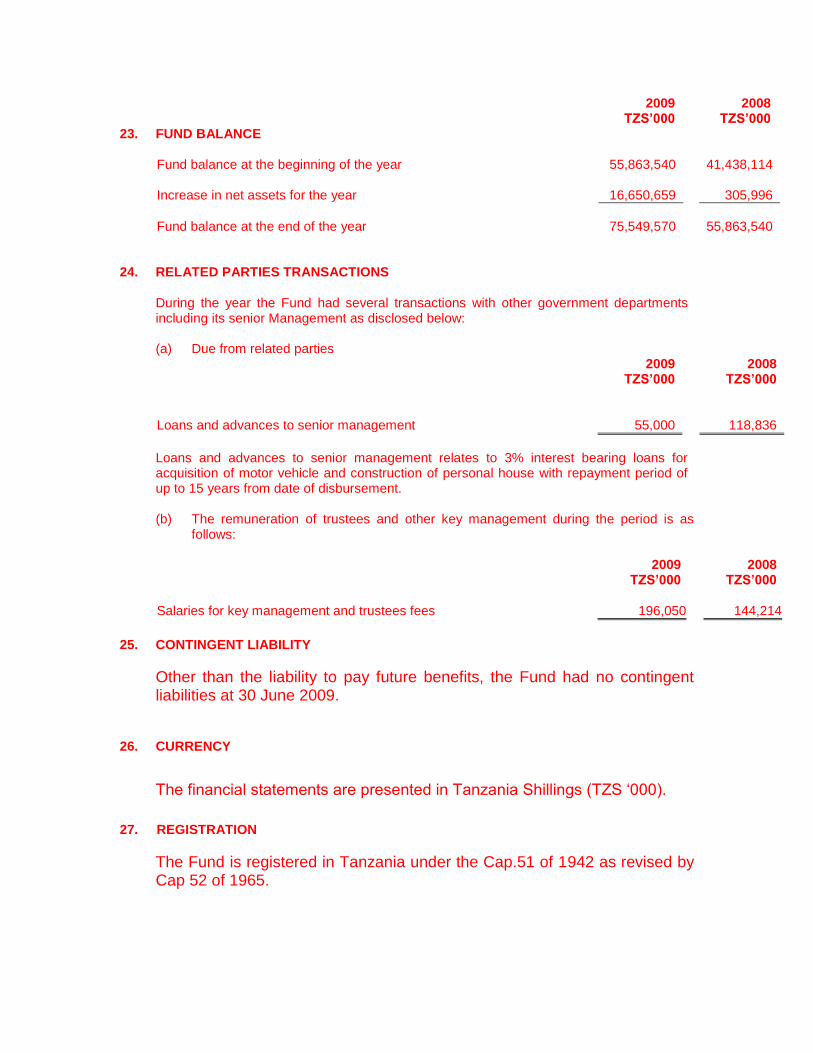

23. FUND BALANCE Fund balance at the beginning of the year 55,863,540 41,438,114 Increase in net assets for the year 16,650,659 305,996

Fund balance at the end of the year

75,549,570

55,863,540

24. RELATED PARTIES TRANSACTIONS

During the year the Fund had several transactions with other government departments including its senior Management as disclosed below:

(a) Due from related parties 2009 2008 TZS’000 TZS’000 Loans and advances to senior management 55,000 118,836

Loans and advances to senior management relates to 3% interest bearing loans for acquisition of motor vehicle and construction of personal house with repayment period of up to 15 years from date of disbursement.

(b) The remuneration of trustees and other key management during the period is as

follows:

2009

2008 TZS’000 TZS’000

Salaries for key management and trustees fees 196,050 144,214

25. CONTINGENT LIABILITY

Other than the liability to pay future benefits, the Fund had no contingent liabilities at 30 June 2009.

26. CURRENCY

The financial statements are presented in Tanzania Shillings (TZS ‗000).

27. REGISTRATION

The Fund is registered in Tanzania under the Cap.51 of 1942 as revised by Cap 52 of 1965.

Recommended

![EMPLOYEES' PROVIDENT FUND C!>RGANISATION · employees' provident fund c!>rganisation newdelhi finance and investment commi1"fee [central board oftrustees, employees' provident fund]](https://img.pdfslide.net/doc/110x75/5d22657b88c993722e8d8033/employees-provident-fund-crganisation-employees-provident-fund-crganisation.jpg)