SHADOW BANKING AND FINTECH:

BRIEF PRESENTATION

Dominique C H E S N E A U

Managing partner TRESORISKCONSEIL

Member of the ITC IAFEI

GROWTH RATE

BANK CREDIT IS NOT SUFFICIENT.

SAVINGS AND RISK APPETITE NEED NEW

DISTRIBUTION/ALLOCATION CHANNELS

3,6%

1,2%

6,8%

5,2%

1,3%

4,9%

3,3%

1,4%

6,3%

5,3%

2,3%

5,2%

Etats-Unis Zone euro Chine ASEAN-5 Amérique latineet Caraïbes

Afriquesubsaharienne

2015

2016

SHADOW BANKING VS BANK?

Borrowers

Institutional Investors

SPV Conduits

Short term liabilities

investissors

LENDERS SHAREHOLDERSE

TC.

LONG TERM SAVINGS

SHORT TERM SAVINGS

BANK CREDIT Transformation

Information assymetry Market funding and Private placement

Limited Transformation of maturity and liquidity Transparency

Indirect funding/Shadow banking Lack o iinformation and lack of transprency

SHADOW BANKING : SUNDRIES, PRODUCTS, EMERGING MARKETS

MARKETS • Shadow banking: a sustainable

alternative to the bank credit model

• From crowd funding to bitcoin

• Shadow banking : towards a « fair

securitization »

• Securitization

• Asset Backed Securities

• US PP,EURO PP

• Factoring

• Covered bonds

• Repos

• Developed countries

• Emerging markets:

- China

- India

- Brazil

• Many divergences

• Many convergences

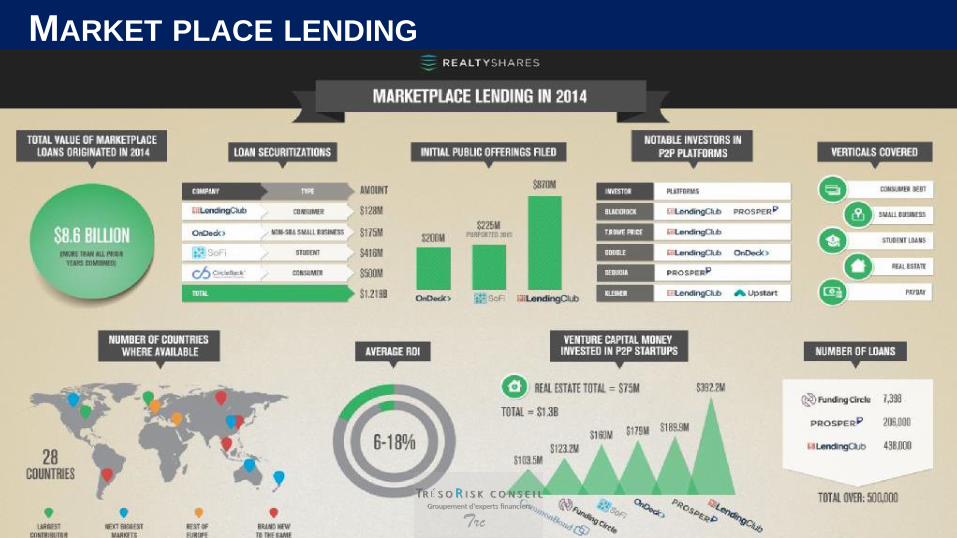

MARKET PLACE LENDING

5

FINTECH

MAJOR FUNCTIONS IN THE FINTECH INDUSTRY

Aggregators

Integrators

Disruptors

FINTECH: CREDIT INSURANCE INTEGRATOR

FUTURE OF THE FINTECH CORPORATES: ORGANISATION

F A C T S 1. New private and corporate consumers appear 2. Hyper-connectivity 3. New “digital” business models 4. Virtual Currencies 5. Barriers 6. Enrichment of contents 7. Growing importance of the data 8. New eco-systems . 2 T Y P E S O F S E R V I C E S

1. Provider of Basic services: bank accounts, credit cards, e-portfolio, money transfers

2. Broker of other services (investment, trading, brokerage, wealth management, sophisticated funding products, crowdfunding, insurance, guarantees, payement…) via Apple and Google Apps

5 B U 1. Banking platform 2. Interface platform 3. Compliance procedures and processes 4. Central bank agreement 5. CRM

• Beyond automatisation: the client experience

• Substitution of product/services/ open innovation and open

development

• Opportunities and limits of big data inTreasury

• Major implication for the Treasurers

• ...

FUTURE OF THE FINTECH CORPORATES: OPEN QUESTIONS

Recommended