Höegh LNG – The floating LNG services provider

Höegh LNG’s Capital Markets Day 2014 9 December

Norges Rederiforbund

Forward-looking statements

2

This presentation contains certain forward-looking statements concerning future events and our operations, performance and financial condition.

Forward-looking statements include, without limitation, any statement that may predict, forecast, indicate or imply future results, performance or

achievements, and may contain the words “believe,” “anticipate,” “expect,” “estimate,” “project,” “will be,” “will continue,” “will likely result,” “plan,”

“intend” or words or phrases of similar meanings. These statements involve known and unknown risks and are based upon a number of

assumptions and estimates that are inherently subject to significant uncertainties and contingencies, many of which are beyond our control. Actual

results may differ materially from those expressed or implied by such forward-looking statements. Important factors that could cause actual results

to differ materially include, but are not limited to: FSRU and LNG carrier market trends, including hire rates and factors affecting supply and

demand; our anticipated growth strategies; our anticipated receipt of dividends and repayment of indebtedness from our joint ventures; the effect of

the worldwide economic environment; turmoil in the global financial markets; fluctuations in currencies and interest rates; general market

conditions, including fluctuations in hire rates and vessel values; changes in our operating expenses, including drydocking and insurance costs; our

ability to make cash distributions from either Höegh LNG Holdings Ltd. (“HLNG”) or Höegh LNG Partners LP (“HMLP”) and the amount of any

borrowings that may be necessary to make such distributions; our ability to comply with financing agreements and the expected effect of restrictions

and covenants in such agreements; the future financial condition of our existing or future customers; our ability to make additional borrowings and

to access public equity and debt capital markets; planned capital expenditures and availability of capital resources to fund capital expenditures; the

exercise of purchase options by our customers; our ability to maintain long-term relationships with our customers; our ability to leverage the

relationship between HLNG and HMLP; our reputation in the shipping industry; the ability of HMLP to purchase vessels from HLNG in the future,

including the FSRU Independence and HLNG’s three FSRU newbuildings; our continued ability to enter into long-term, fixed-rate charters; our

ability to maximize the use of our vessels, including the redeployment or disposition of vessels no longer under long-term charters; expected pursuit

of strategic opportunities, including the acquisition of vessels; our ability to compete successfully for future chartering and newbuilding

opportunities; timely acceptance of our vessels by their charterers; termination dates and extensions of charters; the expected cost of, and our

ability to comply with, governmental regulations and maritime self-regulatory organization standards, as well as standard regulations imposed by

our charterers applicable to our business; expected demand in the LNG shipping sector in general and the demand for vessels in particular;

availability of skilled labor, vessel crews and management; our incremental general and administrative expenses as a publicly traded limited

partnership and our fees and expenses payable under the ship management agreements, the technical information and services agreement and

the Administrative Services Agreements; the anticipated taxation of Höegh LNG Partners LP and distributions to our unitholders; estimated future

maintenance and replacement capital expenditures; our ability to retain key employees; customers’ increasing emphasis on environmental and

safety concerns; potential liability from any pending or future litigation; potential disruption of shipping routes due to accidents, political events,

piracy or acts by terrorists; future sales of our common units in the public market; our business strategy and other plans and objectives for future

operations; and other factors listed from time to time in the reports and other documents that we file with the Oslo Børs or the U.S, Securities and

Exchange Commission, including our Registration Statement on Form F-1 for the initial public offering of HMLP, which was declared effective on

August 7, 2014. All forward-looking statements included in this presentation are made only as of the date hereof. We do not intend to release

publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in our expectations with respect thereto

or any change in events, conditions or circumstances on which any such statement is based.

Preparing for next growth phase

Presented by

Sveinung J.S. Støhle – CEO & President

3

Introduction

Agenda

4

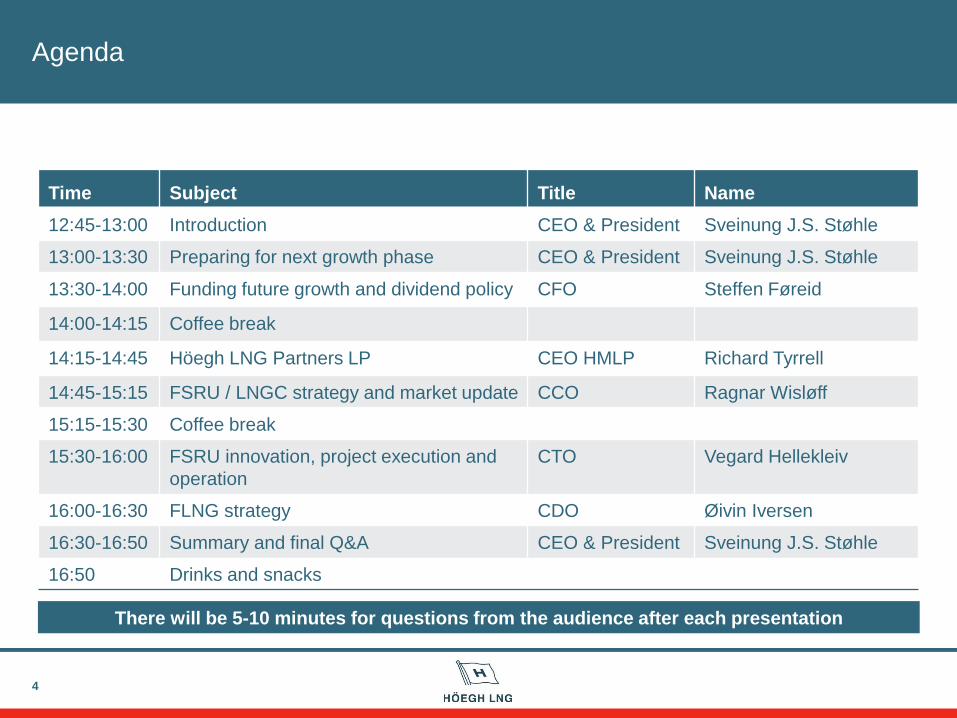

Time Subject Title Name

12:45-13:00 Introduction CEO & President Sveinung J.S. Støhle

13:00-13:30 Preparing for next growth phase CEO & President Sveinung J.S. Støhle

13:30-14:00 Funding future growth and dividend policy CFO Steffen Føreid

14:00-14:15 Coffee break

14:15-14:45 Höegh LNG Partners LP CEO HMLP Richard Tyrrell

14:45-15:15 FSRU / LNGC strategy and market update CCO Ragnar Wisløff

15:15-15:30 Coffee break

15:30-16:00 FSRU innovation, project execution and

operation

CTO Vegard Hellekleiv

16:00-16:30 FLNG strategy CDO Øivin Iversen

16:30-16:50 Summary and final Q&A CEO & President Sveinung J.S. Støhle

16:50 Drinks and snacks

There will be 5-10 minutes for questions from the audience after each presentation

Why invest in Höegh LNG?

5

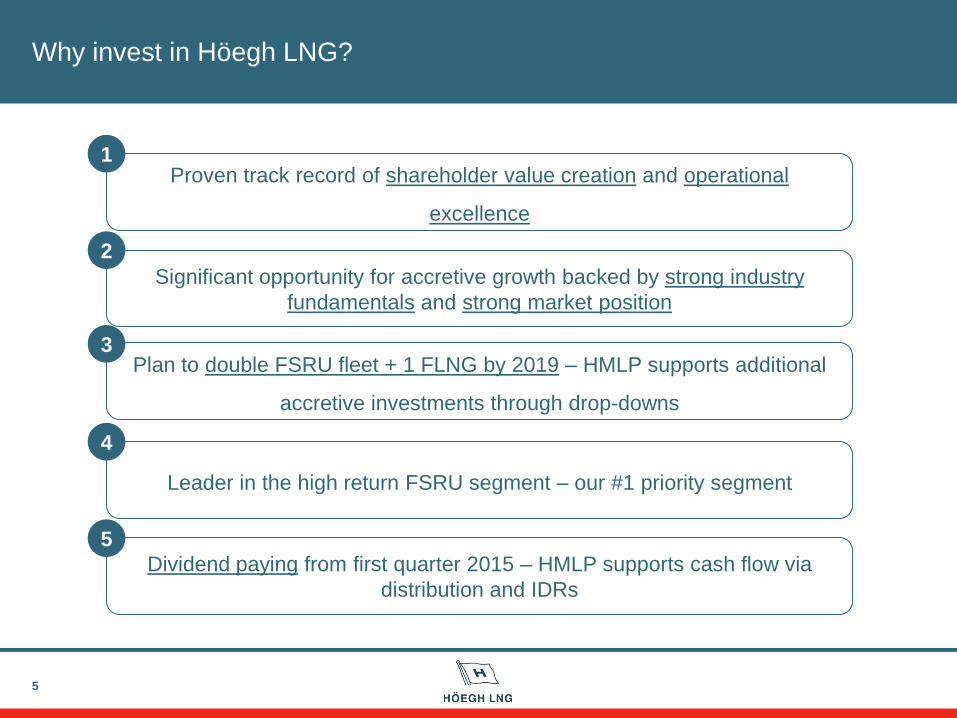

Significant opportunity for accretive growth backed by strong industry

fundamentals and strong market position

Leader in the high return FSRU segment – our #1 priority segment

Proven track record of shareholder value creation and operational

excellence

Plan to double FSRU fleet + 1 FLNG by 2019 – HMLP supports additional

accretive investments through drop-downs

Dividend paying from first quarter 2015 – HMLP supports cash flow via

distribution and IDRs

1

3

4

5

2

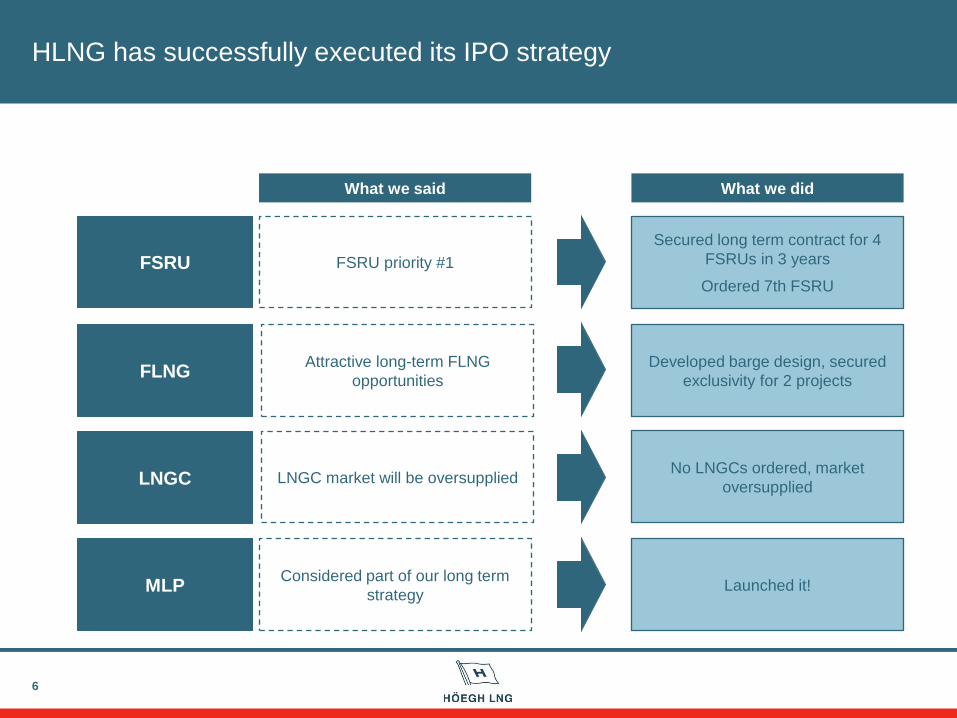

HLNG has successfully executed its IPO strategy

6

FSRU

FLNG

FSRU priority #1

Attractive long-term FLNG

opportunities

Secured long term contract for 4

FSRUs in 3 years

Ordered 7th FSRU

Developed barge design, secured

exclusivity for 2 projects

What we did What we said

LNGC

MLP

LNGC market will be oversupplied

Considered part of our long term

strategy

No LNGCs ordered, market

oversupplied

Launched it!

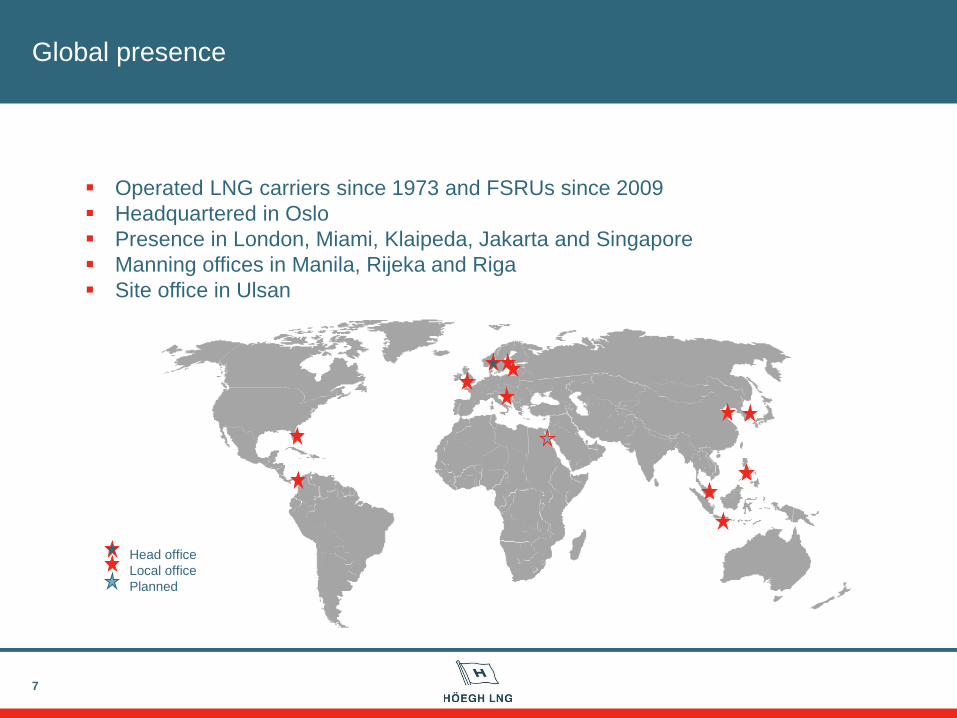

Global presence

7

Operated LNG carriers since 1973 and FSRUs since 2009

Headquartered in Oslo

Presence in London, Miami, Klaipeda, Jakarta and Singapore

Manning offices in Manila, Rijeka and Riga

Site office in Ulsan

Head office

Local office

Planned

Our objective is to achieve best risk-adjusted return by allocating capital in

the optimal order of priority…

8

Order before contract

Modern fleet, latest technology

In-house technical resources

Long term contracts

Order after contract award

Low cost barge design

Experienced EPCIC contractor

Strong contract counterpart

+ May be accretive for MLP

÷ Low barriers to entry

÷ Competitive

÷ Industrial returns

FSRU LNG carriers FLNG 1

Business

model

+ Barriers to entry

+ High risk adjusted return

+ Long-term contracts

+ Strong growth prospects

+ High barriers to entry

+ High returns

+ Long-term contracts

÷ Technical risk and capital

intensive

Order only after contract award

In- house technical resources

Newbuilding only

No spot exposure

Strategic

rationale

3 2

Growth

strategy

1 per year (if accretive for

HMLP)

Capital to be raised by HMLP

1-2 per year

Double FSRU fleet by 2019

through firm+options strategy

1 - 2 by 2019

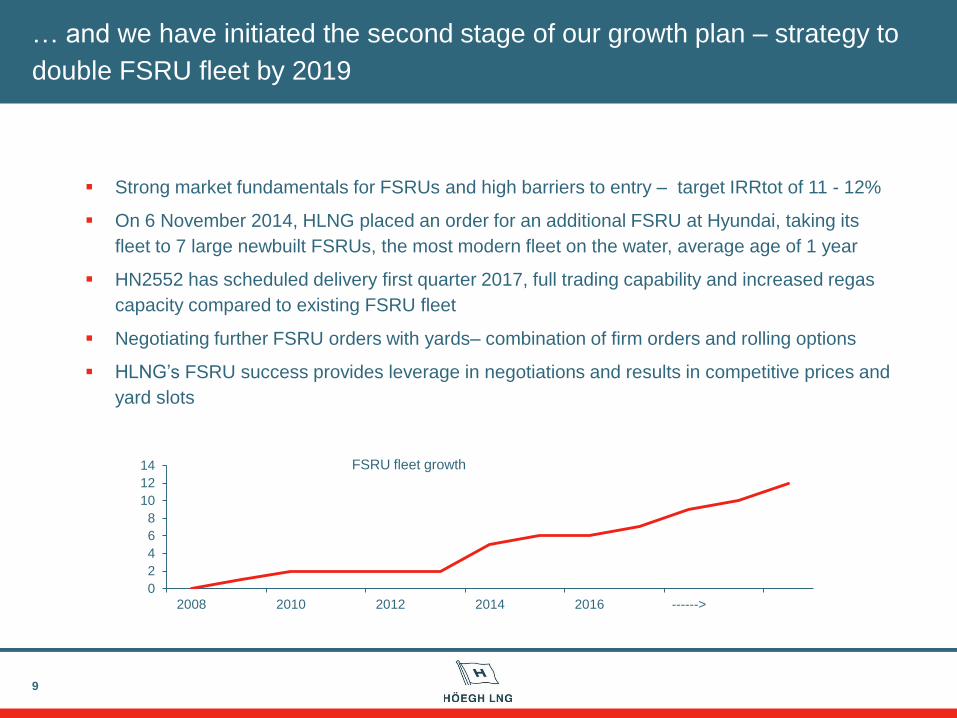

… and we have initiated the second stage of our growth plan – strategy to

double FSRU fleet by 2019

9

Strong market fundamentals for FSRUs and high barriers to entry – target IRRtot of 11 - 12%

On 6 November 2014, HLNG placed an order for an additional FSRU at Hyundai, taking its

fleet to 7 large newbuilt FSRUs, the most modern fleet on the water, average age of 1 year

HN2552 has scheduled delivery first quarter 2017, full trading capability and increased regas

capacity compared to existing FSRU fleet

Negotiating further FSRU orders with yards– combination of firm orders and rolling options

HLNG’s FSRU success provides leverage in negotiations and results in competitive prices and

yard slots

0

2

4

6

8

10

12

14

2008 2010 2012 2014 2016 ------>

FSRU fleet growth

Recent company highlights

10

Successful listing

of MLP

HN2552

Dividend policy in

place

EGAS contract

Colombia contract

Government sponsored project to cover the country’s gas deficit

Start-up and technical specification fits well with Höegh Gallant

MLP candidate with 5 year contract

Government sponsored project to ensure energy security

Established natural gas and electricity market

MLP candidate with 20 years contract

Best priced maritime MLP IPO ever

Funding vehicle for parent’s growth in place

Parent provides the MLP with a visible pipeline of dropdown candidates

Launch of FSRU expansion phase #2

Competitive price offers confirms HLNG’s leading position in the FSRU segment

Increased regasification capacity, storage capacity and speed

Policy: Stability, predictability and growth over time

Dividend payments from 1st quarter 2015

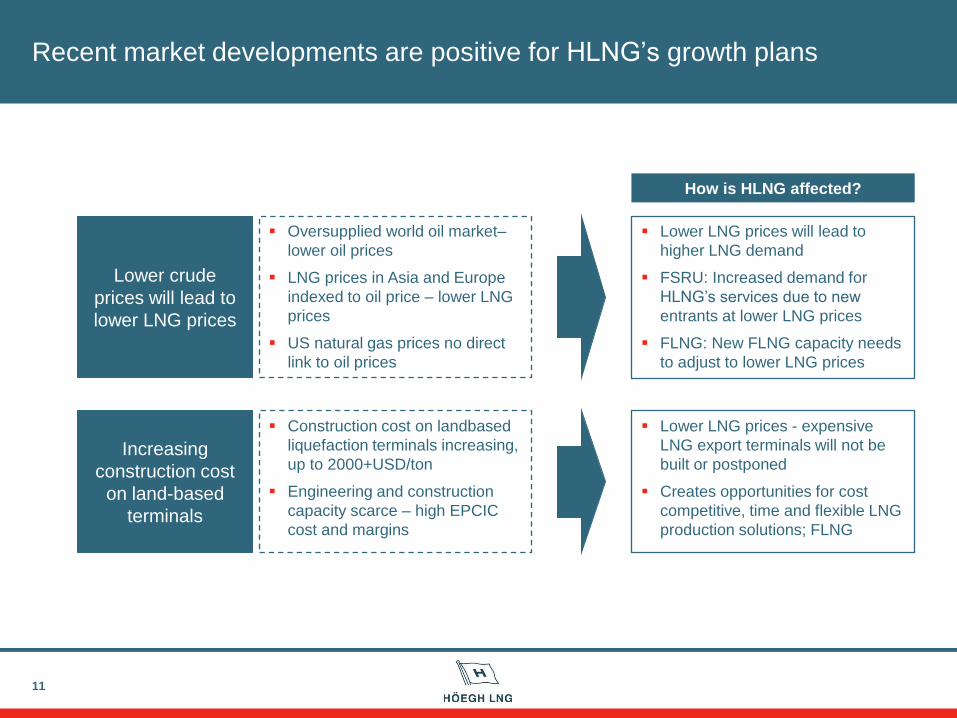

Recent market developments are positive for HLNG’s growth plans

11

Lower crude

prices will lead to

lower LNG prices

Increasing

construction cost

on land-based

terminals

Oversupplied world oil market–

lower oil prices

LNG prices in Asia and Europe

indexed to oil price – lower LNG

prices

US natural gas prices no direct

link to oil prices

Construction cost on landbased

liquefaction terminals increasing,

up to 2000+USD/ton

Engineering and construction

capacity scarce – high EPCIC

cost and margins

Lower LNG prices will lead to

higher LNG demand

FSRU: Increased demand for

HLNG’s services due to new

entrants at lower LNG prices

FLNG: New FLNG capacity needs

to adjust to lower LNG prices

Lower LNG prices - expensive

LNG export terminals will not be

built or postponed

Creates opportunities for cost

competitive, time and flexible LNG

production solutions; FLNG

How is HLNG affected?

12

Funding future growth and dividend policy

Presented by

Steffen Føreid – CFO

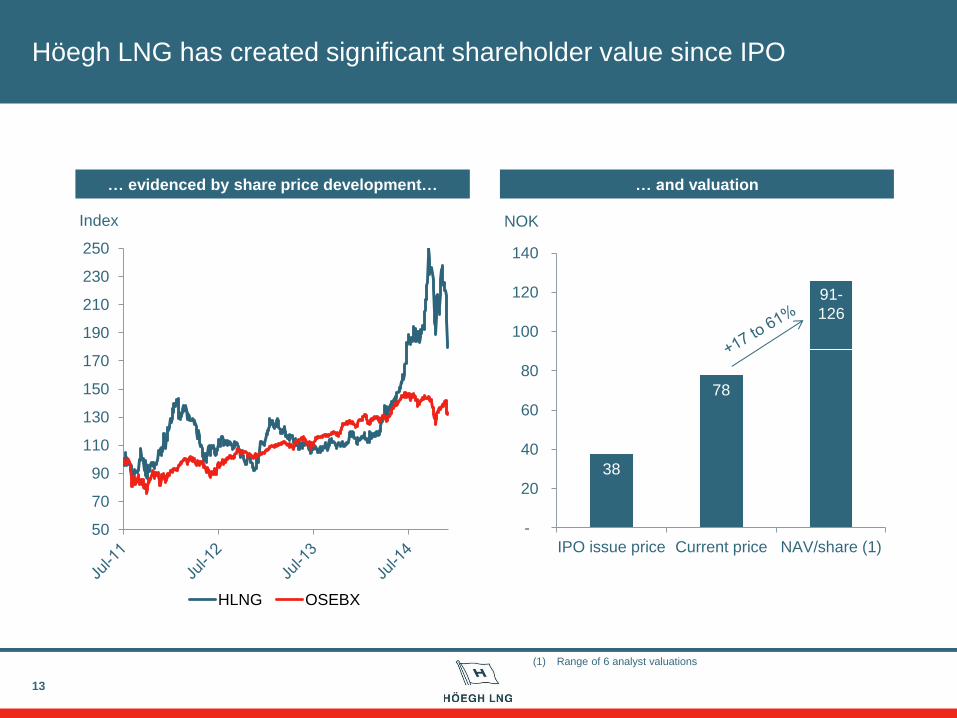

Höegh LNG has created significant shareholder value since IPO

13

38

78

-

20

40

60

80

100

120

140

IPO issue price Current price NAV/share (1)

NOK

… evidenced by share price development… … and valuation

50

70

90

110

130

150

170

190

210

230

250

Index

HLNG OSEBX

(1) Range of 6 analyst valuations

91-

126

91-

126

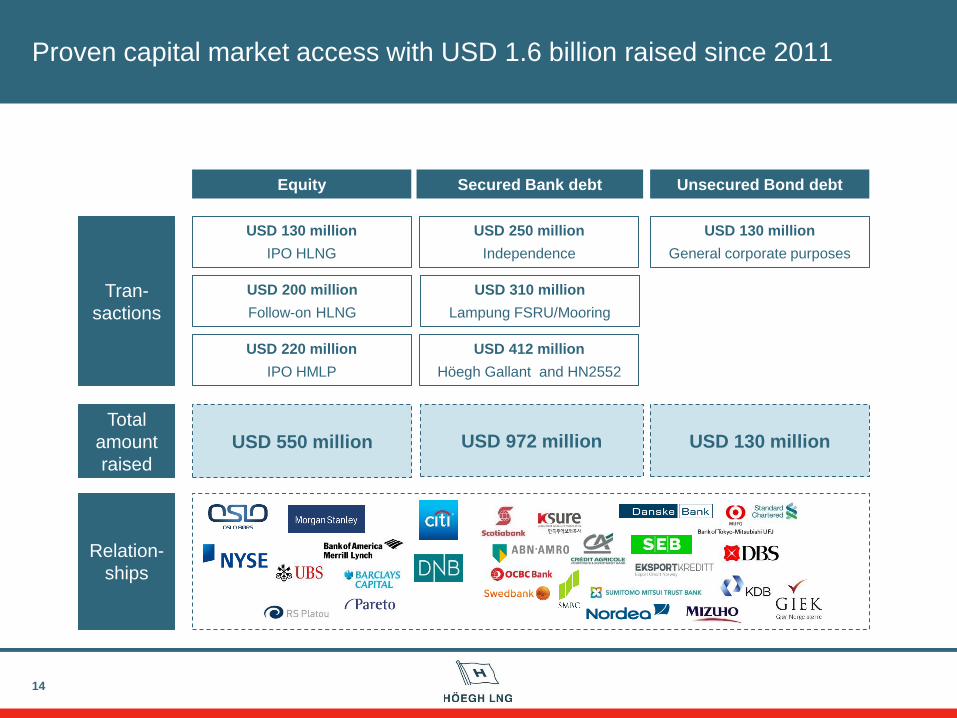

Proven capital market access with USD 1.6 billion raised since 2011

14

USD 550 million USD 972 million

Equity Unsecured Bond debt Secured Bank debt

Total

amount

raised

USD 130 million

IPO HLNG

USD 130 million

Tran-

sactions

Relation-

ships

USD 200 million

Follow-on HLNG

USD 220 million

IPO HMLP

USD 250 million

Independence

USD 310 million

Lampung FSRU/Mooring

USD 412 million

Höegh Gallant and HN2552

USD 130 million

General corporate purposes

-

200

400

600

800

1 000

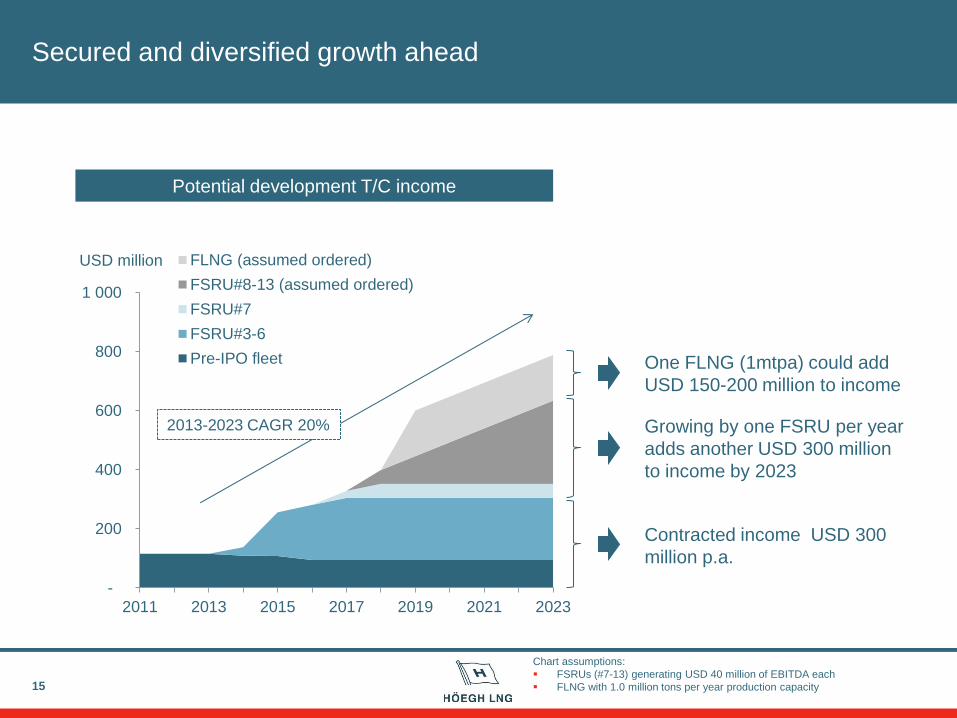

2011 2013 2015 2017 2019 2021 2023

USD million FLNG (assumed ordered)

FSRU#8-13 (assumed ordered)

FSRU#7

FSRU#3-6

Pre-IPO fleet

Secured and diversified growth ahead

Potential development T/C income

2013-2023 CAGR 20%

Chart assumptions:

FSRUs (#7-13) generating USD 40 million of EBITDA each

FLNG with 1.0 million tons per year production capacity

Contracted income USD 300

million p.a.

Growing by one FSRU per year

adds another USD 300 million

to income by 2023

One FLNG (1mtpa) could add

USD 150-200 million to income

15

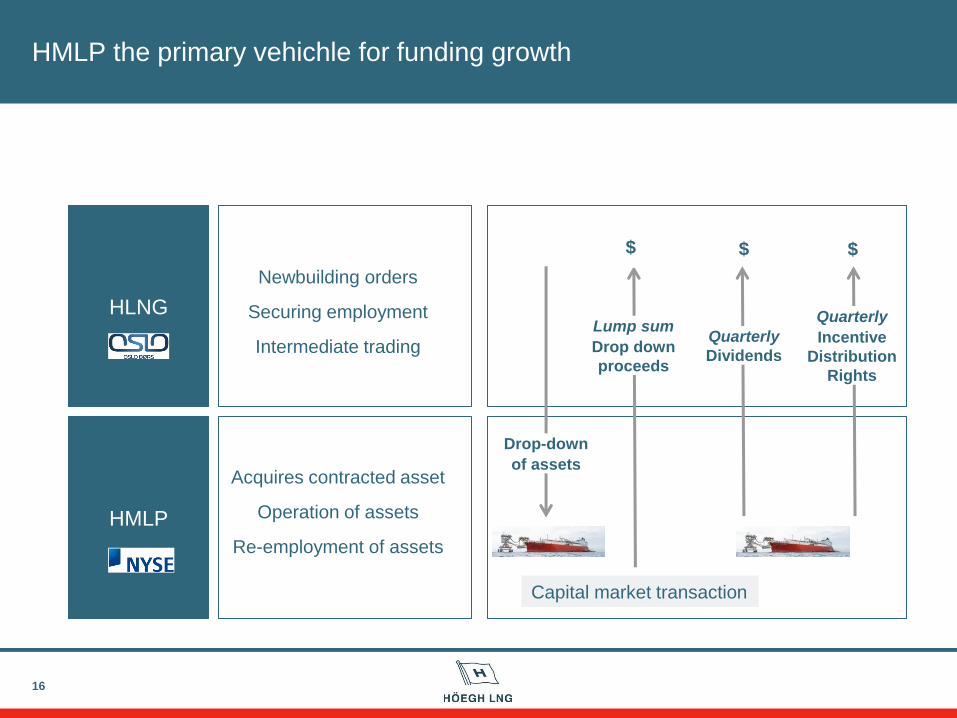

HMLP the primary vehichle for funding growth

16

HLNG

HMLP

HLNG

HMLP

Newbuilding orders

Securing employment

Intermediate trading

Acquires contracted asset

Operation of assets

Re-employment of assets

HLNG

HMLP

Drop-down

of assets

Lump sum

Drop down

proceeds

$ $ $

Quarterly

Dividends

Quarterly

Incentive

Distribution

Rights

Capital market transaction

Newbuildingmultiple (1)

HLNG tradingmultiple (2)

Drop-downmultiple (3)

HMLP tradingmultiple (3)

17

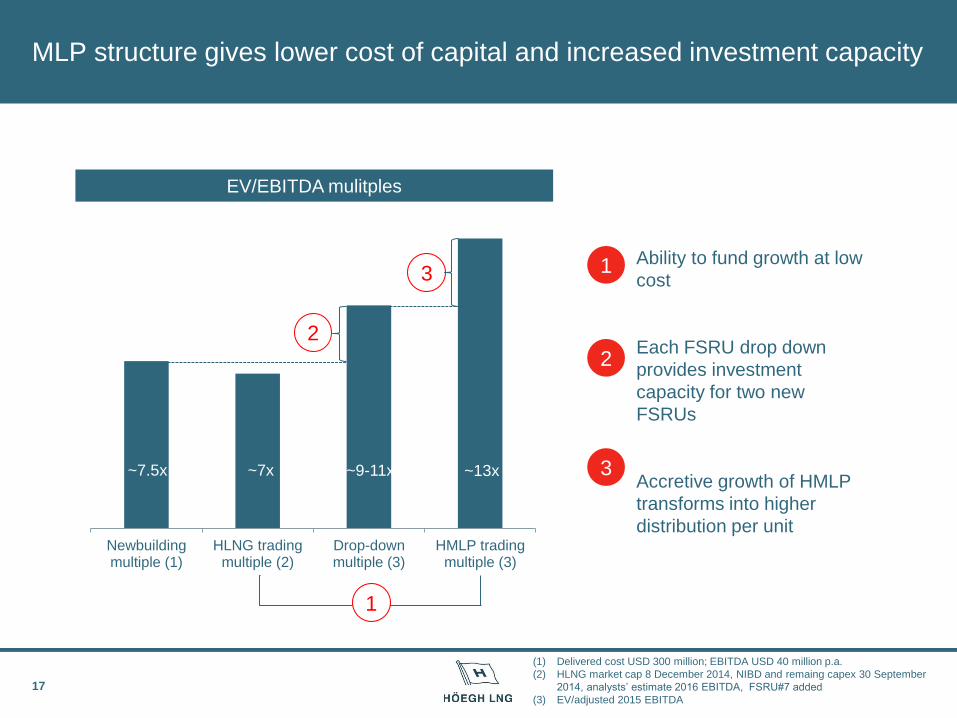

MLP structure gives lower cost of capital and increased investment capacity

• Ability to fund growth at low

cost

• Each FSRU drop down

provides investment

capacity for two new

FSRUs

Accretive growth of HMLP

transforms into higher

distribution per unit

EV/EBITDA mulitples

~9-11x ~13x ~7.5x ~7x

1

2

2

3

(1) Delivered cost USD 300 million; EBITDA USD 40 million p.a.

(2) HLNG market cap 8 December 2014, NIBD and remaing capex 30 September

2014, analysts’ estimate 2016 EBITDA, FSRU#7 added

(3) EV/adjusted 2015 EBITDA

1

3

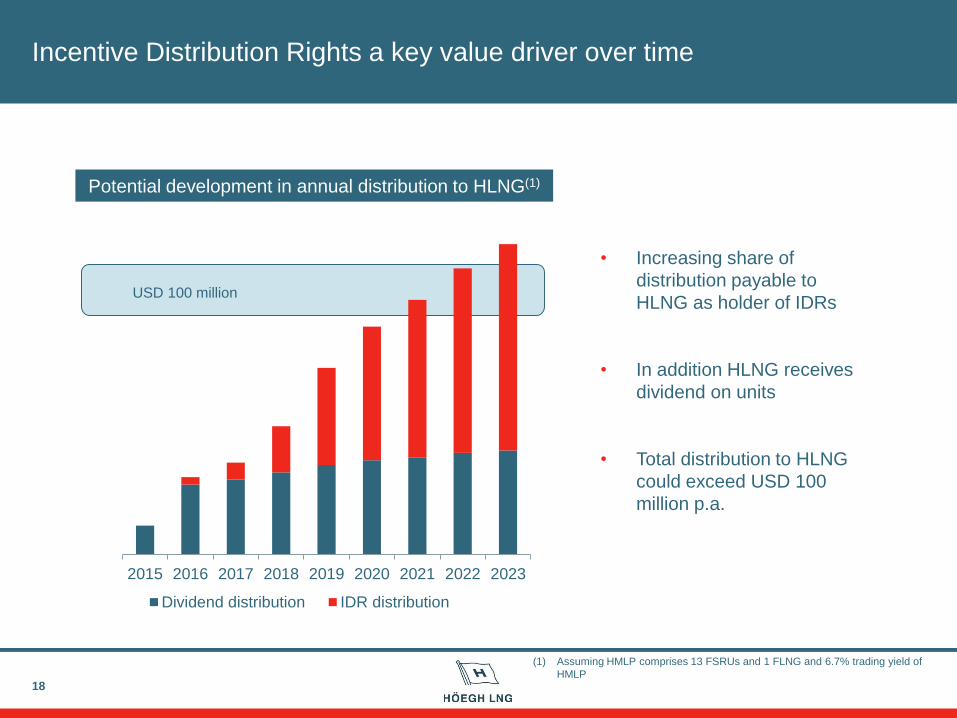

Incentive Distribution Rights a key value driver over time

18

Potential development in annual distribution to HLNG(1)

2015 2016 2017 2018 2019 2020 2021 2022 2023

Dividend distribution IDR distribution

USD 100 million

(1) Assuming HMLP comprises 13 FSRUs and 1 FLNG and 6.7% trading yield of

HMLP

• Increasing share of

distribution payable to

HLNG as holder of IDRs

• In addition HLNG receives

dividend on units

• Total distribution to HLNG

could exceed USD 100

million p.a.

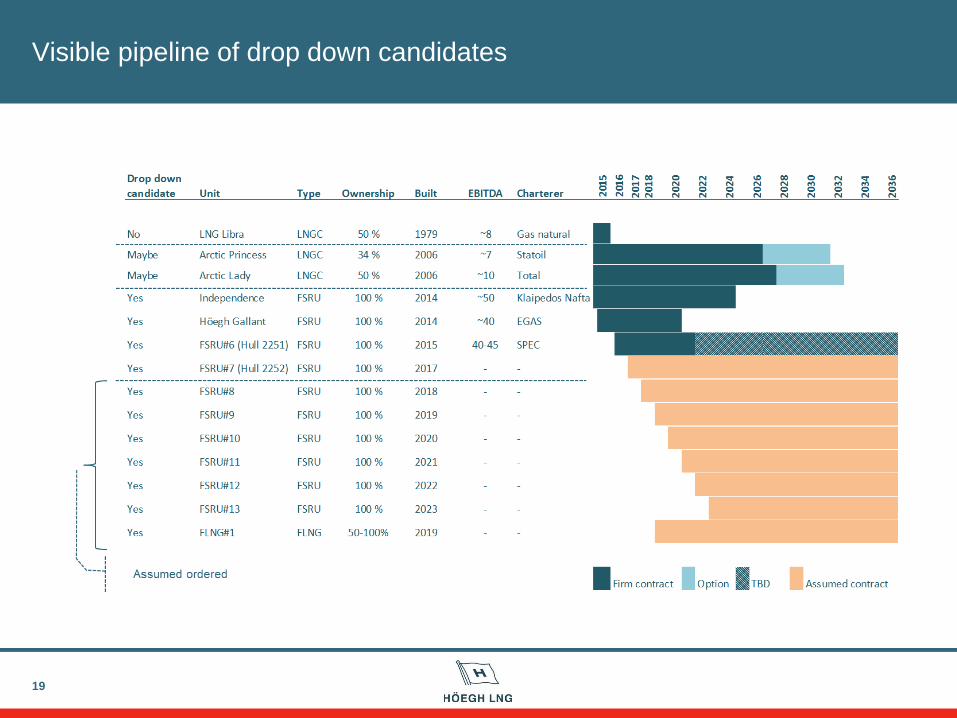

Visible pipeline of drop down candidates

19

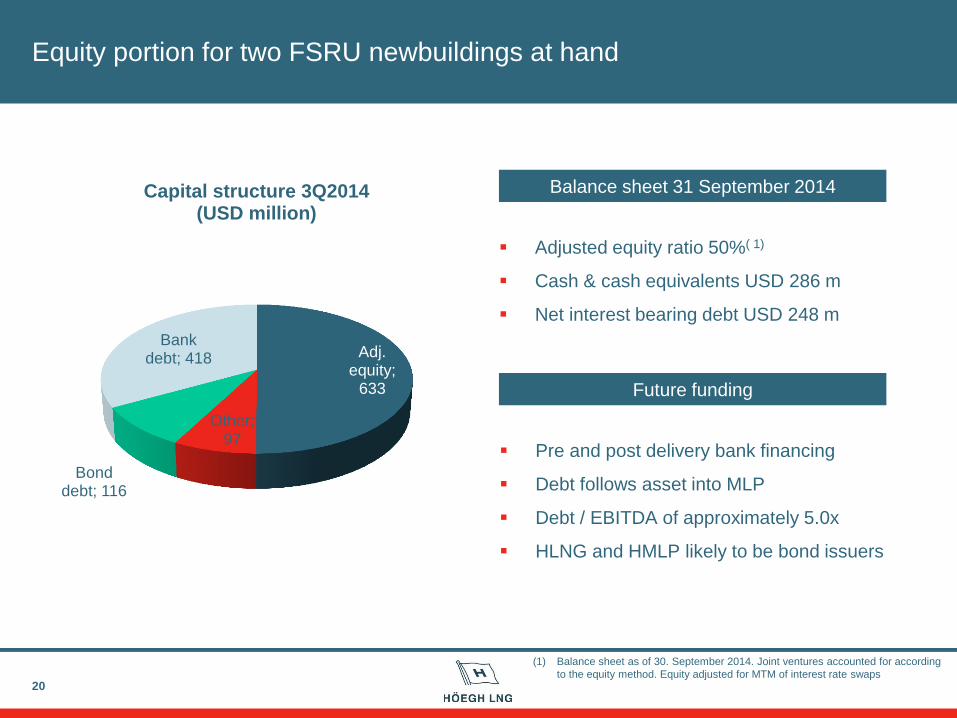

Equity portion for two FSRU newbuildings at hand

20

Adjusted equity ratio 50%( 1)

Cash & cash equivalents USD 286 m

Net interest bearing debt USD 248 m

Balance sheet 31 September 2014

Future funding

Pre and post delivery bank financing

Debt follows asset into MLP

Debt / EBITDA of approximately 5.0x

HLNG and HMLP likely to be bond issuers

Adj. equity;

633

Other; 97

Bond debt; 116

Bank debt; 418

Capital structure 3Q2014 (USD million)

(1) Balance sheet as of 30. September 2014. Joint ventures accounted for according

to the equity method. Equity adjusted for MTM of interest rate swaps

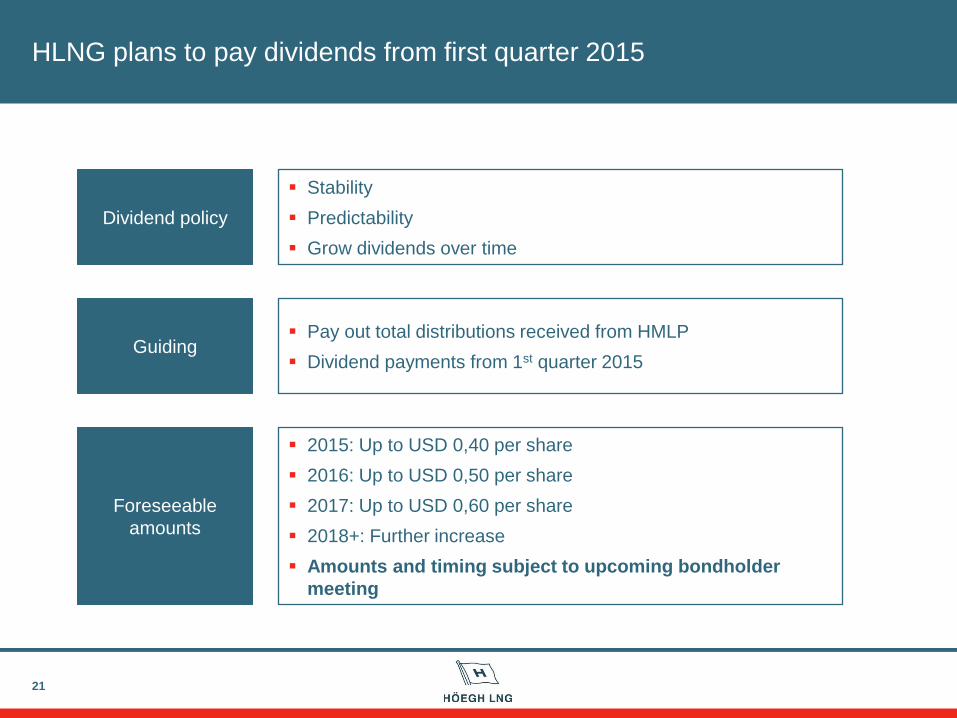

HLNG plans to pay dividends from first quarter 2015

21

Dividend policy

Guiding

Stability

Predictability

Grow dividends over time

Pay out total distributions received from HMLP

Dividend payments from 1st quarter 2015

Foreseeable

amounts

2015: Up to USD 0,40 per share

2016: Up to USD 0,50 per share

2017: Up to USD 0,60 per share

2018+: Further increase

Amounts and timing subject to upcoming bondholder

meeting

Summary

22

Significant shareholder value created since IPO

Proven capital market access

HMLP facilitating growth

Strong balance sheet

Dividend policy in place

23

Höegh LNG Partners LP

Presented by

Richard Tyrrell – CEO HMLP

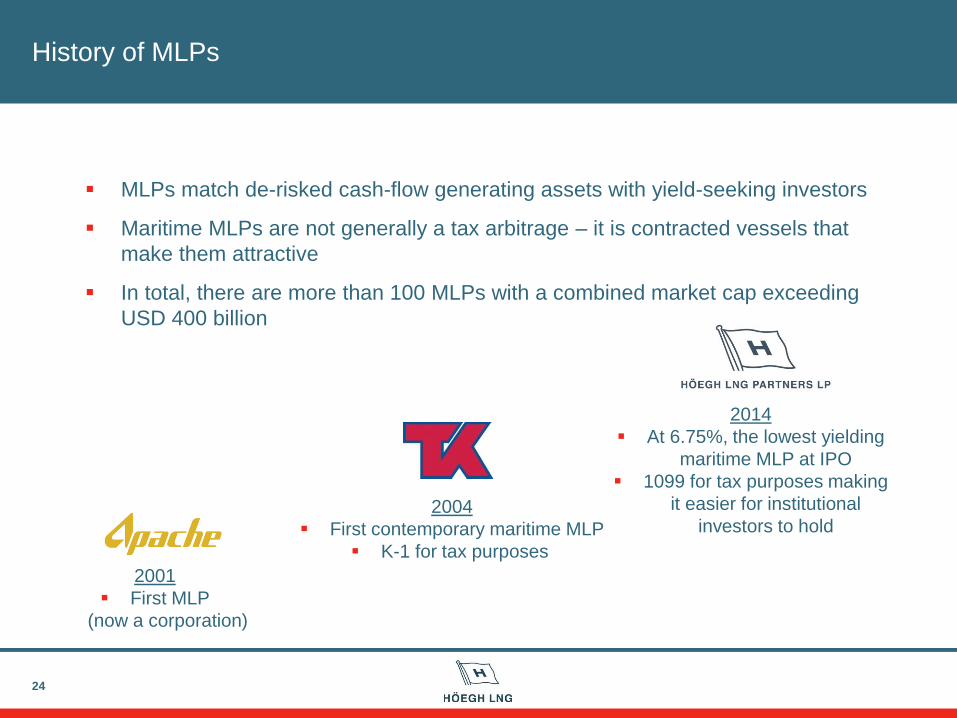

History of MLPs

24

MLPs match de-risked cash-flow generating assets with yield-seeking investors

Maritime MLPs are not generally a tax arbitrage – it is contracted vessels that

make them attractive

In total, there are more than 100 MLPs with a combined market cap exceeding

USD 400 billion

2001

First MLP

(now a corporation)

2004

First contemporary maritime MLP

K-1 for tax purposes

2014

At 6.75%, the lowest yielding

maritime MLP at IPO

1099 for tax purposes making

it easier for institutional

investors to hold

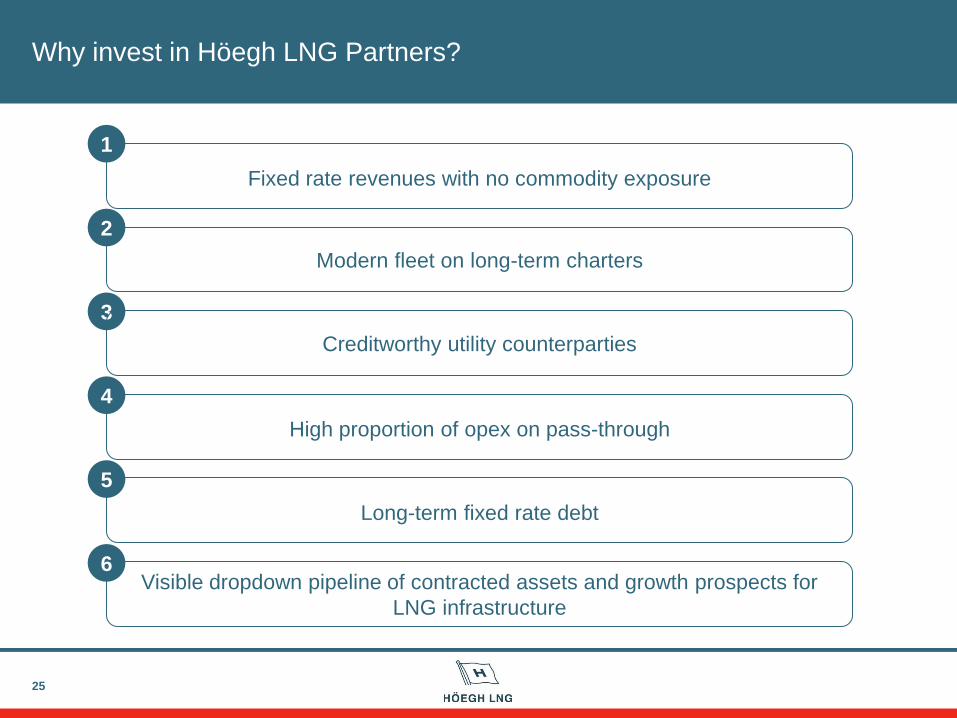

Why invest in Höegh LNG Partners?

25

Modern fleet on long-term charters

Long-term fixed rate debt

Fixed rate revenues with no commodity exposure

High proportion of opex on pass-through

Visible dropdown pipeline of contracted assets and growth prospects for

LNG infrastructure

1

3

4

5

2

Creditworthy utility counterparties

6

26

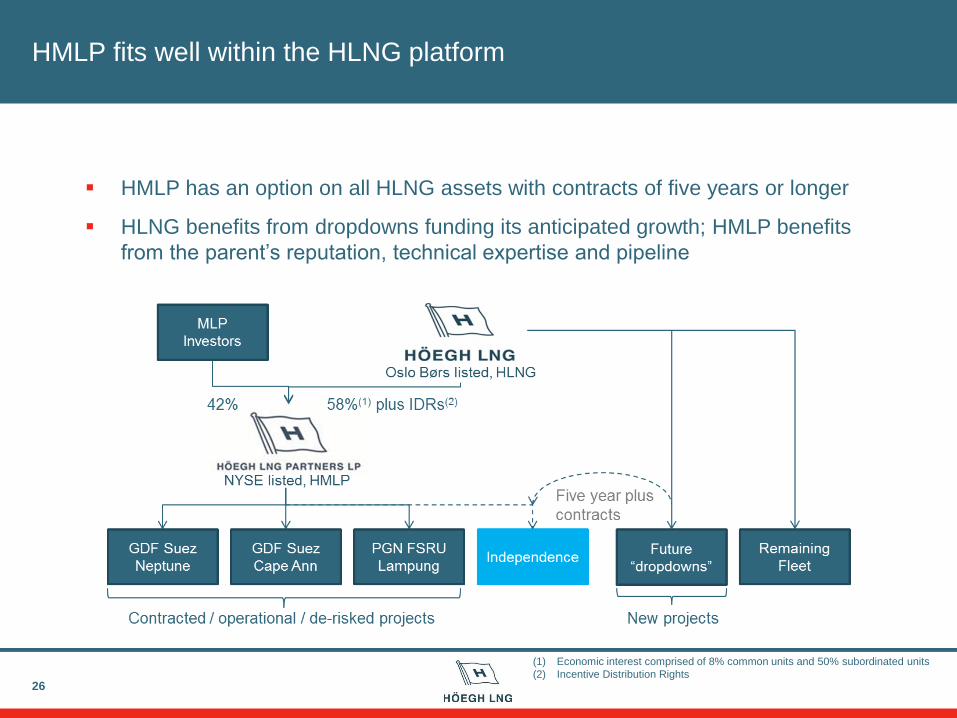

HMLP has an option on all HLNG assets with contracts of five years or longer

HLNG benefits from dropdowns funding its anticipated growth; HMLP benefits

from the parent’s reputation, technical expertise and pipeline

(1) Economic interest comprised of 8% common units and 50% subordinated units

(2) Incentive Distribution Rights

HMLP fits well within the HLNG platform

HMLP is the best priced maritime MLP IPO ever…

27

Issuer Höegh LNG Partners LP (NYSE:HMLP)

Offering Size 11,040,000 Common units after exercise of over-allotment

Price $20.00 (mid-point of range)

Proceeds $220.8 million (gross) / $203.5 million (net)

Implied Yield 6.75%

One-on-One “Hit Rate” 69%

Institutional Coverage 6.6x

# Institutions Allocated 129

Price to First Day Close +11.3%

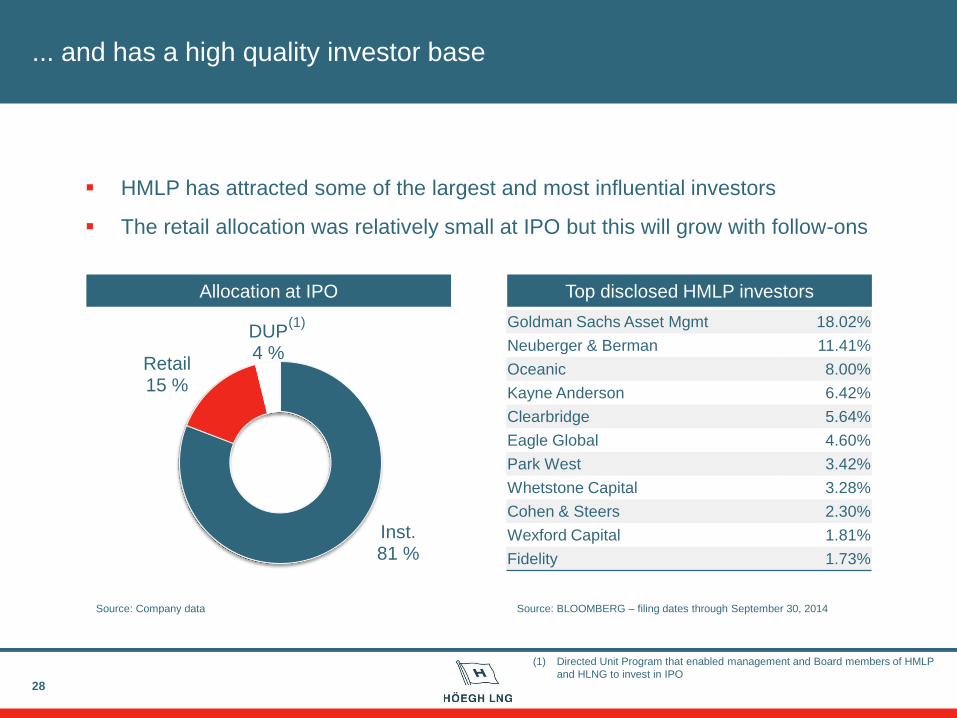

... and has a high quality investor base

28

Top disclosed HMLP investors

Goldman Sachs Asset Mgmt 18.02%

Neuberger & Berman 11.41%

Oceanic 8.00%

Kayne Anderson 6.42%

Clearbridge 5.64%

Eagle Global 4.60%

Park West 3.42%

Whetstone Capital 3.28%

Cohen & Steers 2.30%

Wexford Capital 1.81%

Fidelity 1.73%

Source: BLOOMBERG – filing dates through September 30, 2014

Inst. 81 %

Retail 15 %

DUP 4 %

Source: Company data

Allocation at IPO

(1)

HMLP has attracted some of the largest and most influential investors

The retail allocation was relatively small at IPO but this will grow with follow-ons

(1) Directed Unit Program that enabled management and Board members of HMLP

and HLNG to invest in IPO

HMLP performance since IPO

29

0

50

100

150

200

250

300

350

400

450

500

0

5

10

15

20

25

30

aug sep okt nov

Th

ou

san

ds

Un

it P

rice r

eb

ased

to

HL

NG

Volume

HMLP US Equity

Av. Driller MLPs(1)

Av. Maritime MLPs(2)

HMLP’s common units closed at USD 18.80 on December 5, versus an IPO price

of USD 20

Correlation with oil price despite no direct link to HMLP’s business; trading

characterized by thin volumes

(1) Average of SDLP, RIGP

(2) Average of GLOP, GLNG, DLNG, TGP, KNOP

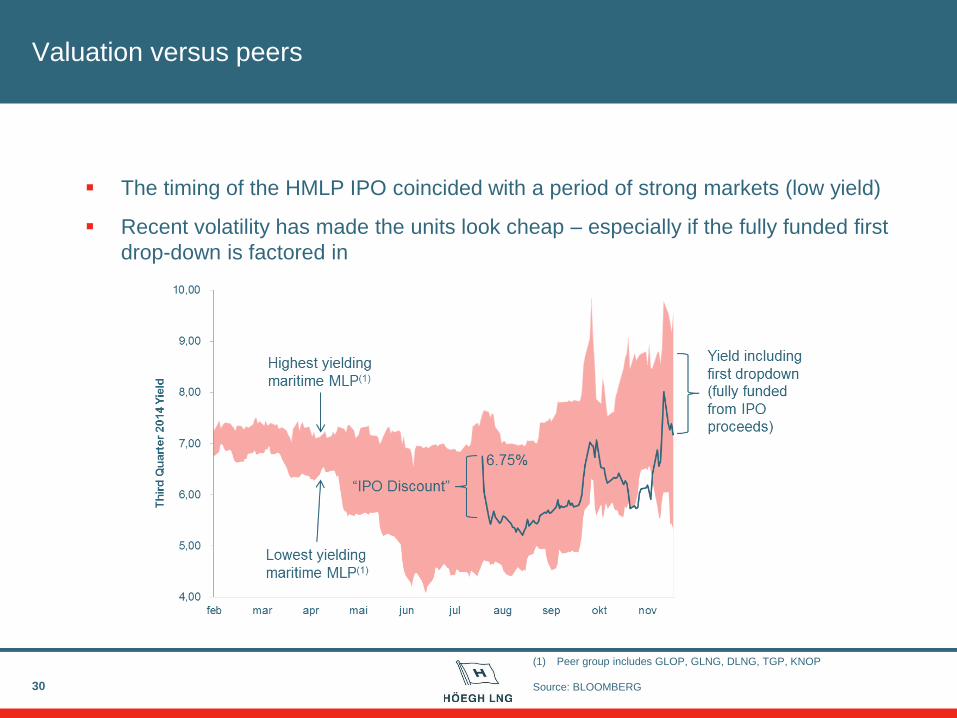

Valuation versus peers

30

The timing of the HMLP IPO coincided with a period of strong markets (low yield)

Recent volatility has made the units look cheap – especially if the fully funded first

drop-down is factored in

(1) Peer group includes GLOP, GLNG, DLNG, TGP, KNOP

Source: BLOOMBERG

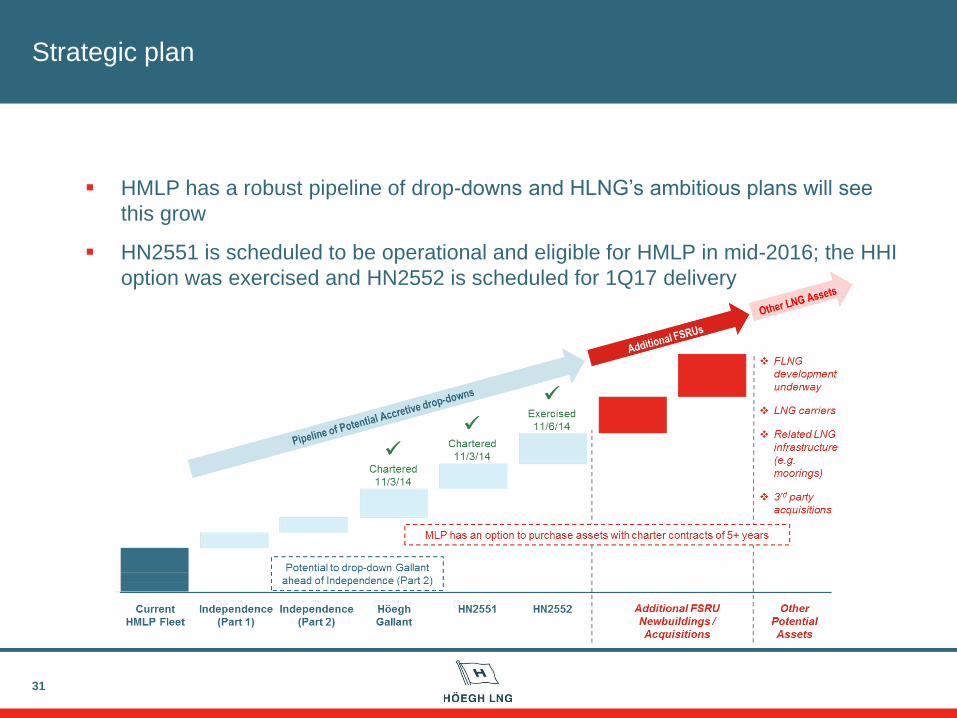

Strategic plan

31

HMLP has a robust pipeline of drop-downs and HLNG’s ambitious plans will see

this grow

HN2551 is scheduled to be operational and eligible for HMLP in mid-2016; the HHI

option was exercised and HN2552 is scheduled for 1Q17 delivery

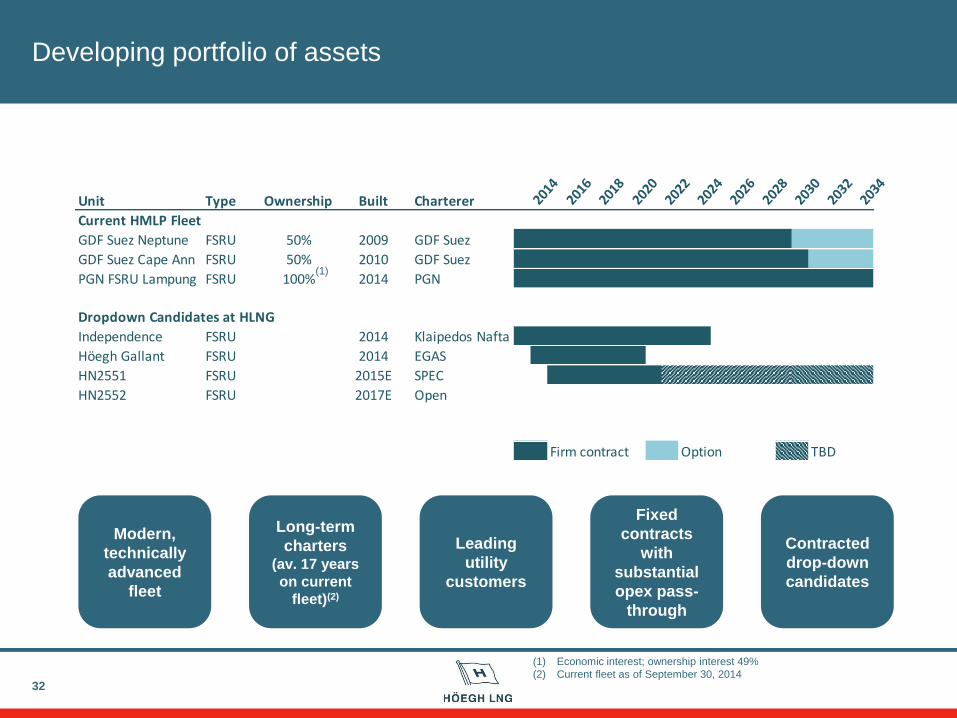

Developing portfolio of assets

32

Modern,

technically

advanced

fleet

Long-term

charters (av. 17 years

on current

fleet)(2)

Leading

utility

customers

Fixed

contracts

with

substantial

opex pass-

through

Contracted

drop-down

candidates

Unit Type Ownership Built Charterer 2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

Current HMLP Fleet

GDF Suez Neptune FSRU 50% 2009 GDF Suez

GDF Suez Cape Ann FSRU 50% 2010 GDF Suez

PGN FSRU Lampung FSRU 100% 2014 PGN

Dropdown Candidates at HLNG

Independence FSRU 2014 Klaipedos Nafta

Höegh Gallant FSRU 2014 EGAS

HN2551 FSRU 2015E SPEC

HN2552 FSRU 2017E Open

Firm contract Option TBD

(1)

(1) Economic interest; ownership interest 49%

(2) Current fleet as of September 30, 2014

Summary

33

Completed the successful IPO of HMLP

Contracts and vessels that are amongst the best suited in the maritime

segment for the asset class

First dropdown (Independence Part 1) funded by IPO proceeds; no follow-

on required

Robust pipeline of accretive dropdown candidates

Parent with ambitious growth plans

34

FSRU / LNGC strategy and market update

Presented by

Ragnar Wisløff – CCO

HLNG will continue to strengthen its position as the leading player in the

FSRU space

35

Order before contract

Modern fleet and latest technology

In-house technical and operational

experience

Long-term contracts

Lower overall cost for the client

Optimize technical design to clients’ needs

Lower residual risk

Business model

Able to bid on fast track / high return

projects

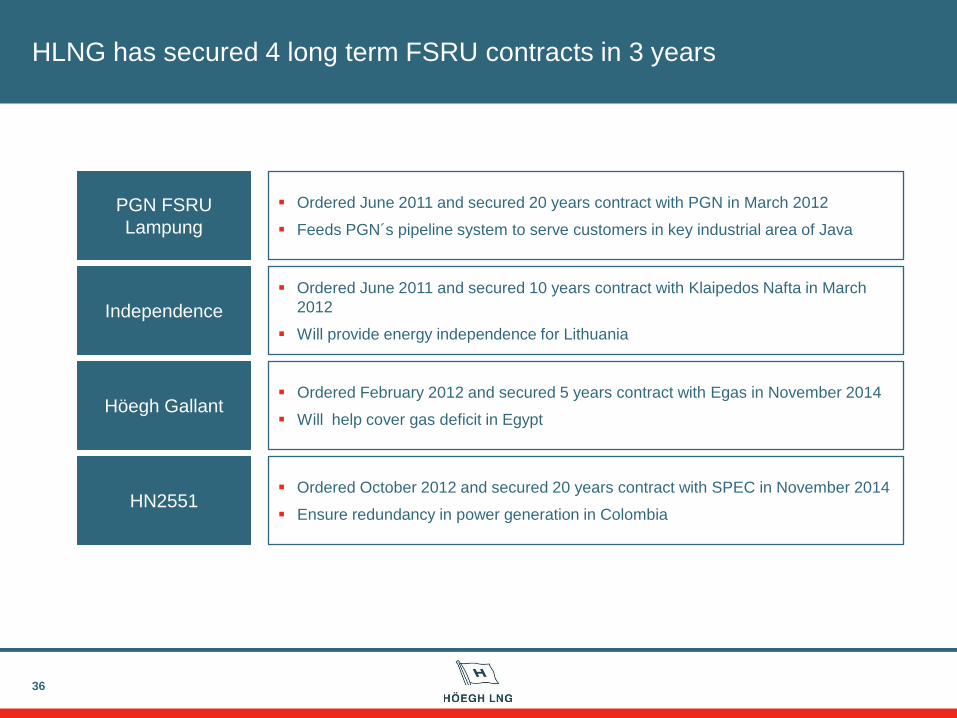

HLNG has secured 4 long term FSRU contracts in 3 years

36

Höegh Gallant

HN2551

PGN FSRU

Lampung

Independence

Ordered June 2011 and secured 20 years contract with PGN in March 2012

Feeds PGN´s pipeline system to serve customers in key industrial area of Java

Ordered June 2011 and secured 10 years contract with Klaipedos Nafta in March

2012

Will provide energy independence for Lithuania

Ordered February 2012 and secured 5 years contract with Egas in November 2014

Will help cover gas deficit in Egypt

Ordered October 2012 and secured 20 years contract with SPEC in November 2014

Ensure redundancy in power generation in Colombia

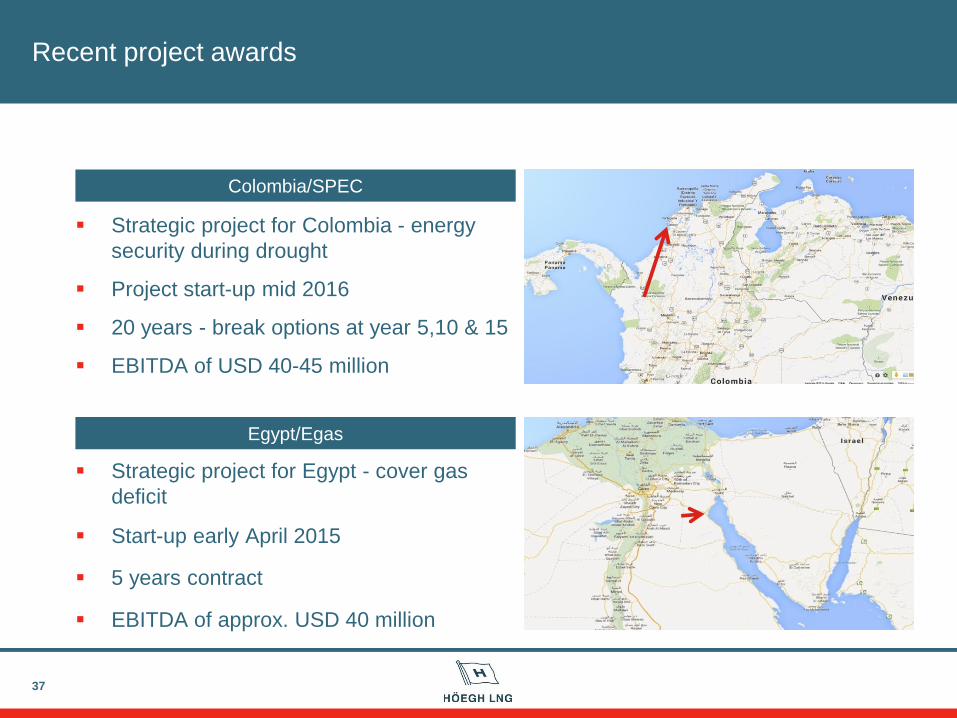

Recent project awards

Strategic project for Colombia - energy

security during drought

Project start-up mid 2016

20 years - break options at year 5,10 & 15

EBITDA of USD 40-45 million

37

Strategic project for Egypt - cover gas

deficit

Start-up early April 2015

5 years contract

EBITDA of approx. USD 40 million

Colombia/SPEC

Egypt/Egas

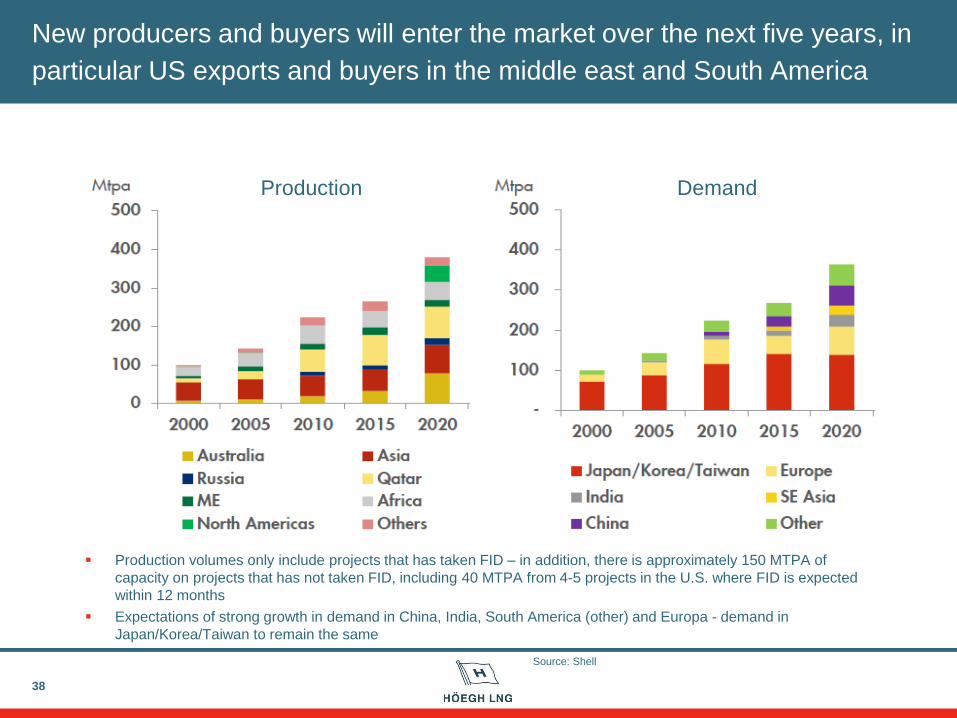

New producers and buyers will enter the market over the next five years, in

particular US exports and buyers in the middle east and South America

38

Production Demand

Production volumes only include projects that has taken FID – in addition, there is approximately 150 MTPA of

capacity on projects that has not taken FID, including 40 MTPA from 4-5 projects in the U.S. where FID is expected

within 12 months

Expectations of strong growth in demand in China, India, South America (other) and Europa - demand in

Japan/Korea/Taiwan to remain the same

Source: Shell

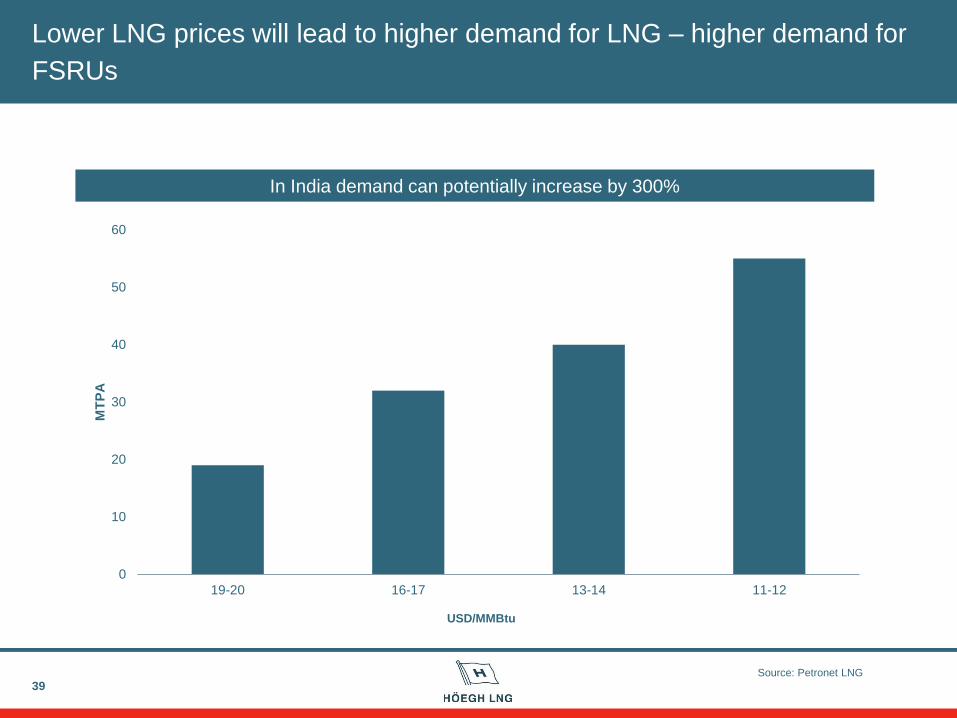

Lower LNG prices will lead to higher demand for LNG – higher demand for

FSRUs

39

In India demand can potentially increase by 300%

Source: Petronet LNG

USD/MMBtu

0

10

20

30

40

50

60

19-20 16-17 13-14 11-12

MT

PA

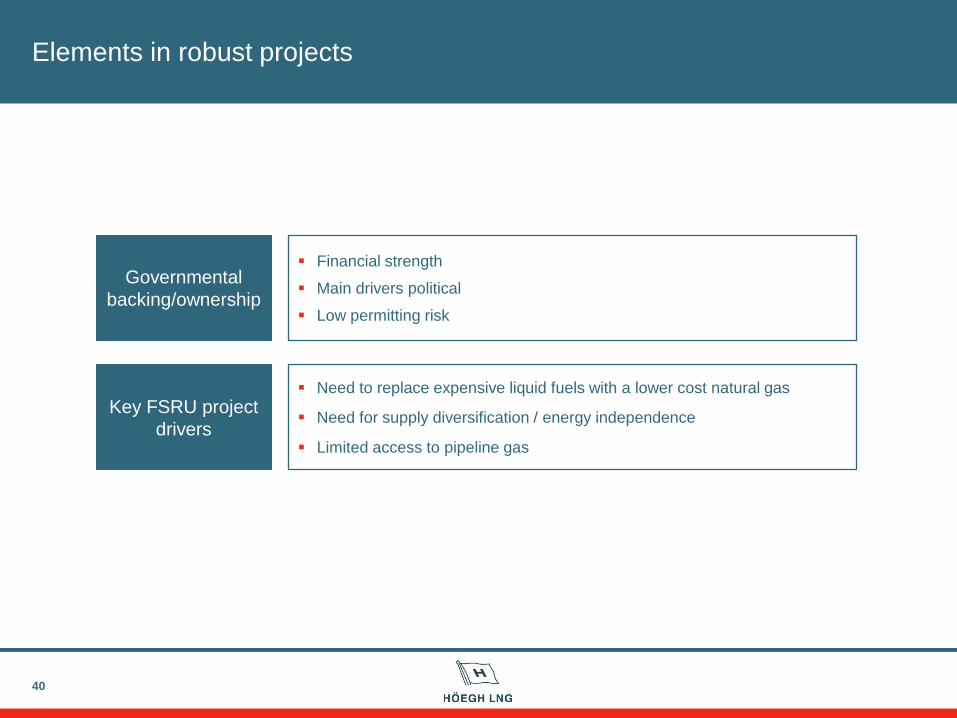

Elements in robust projects

40

Governmental

backing/ownership

Key FSRU project

drivers

Financial strength

Main drivers political

Low permitting risk

Need to replace expensive liquid fuels with a lower cost natural gas

Need for supply diversification / energy independence

Limited access to pipeline gas

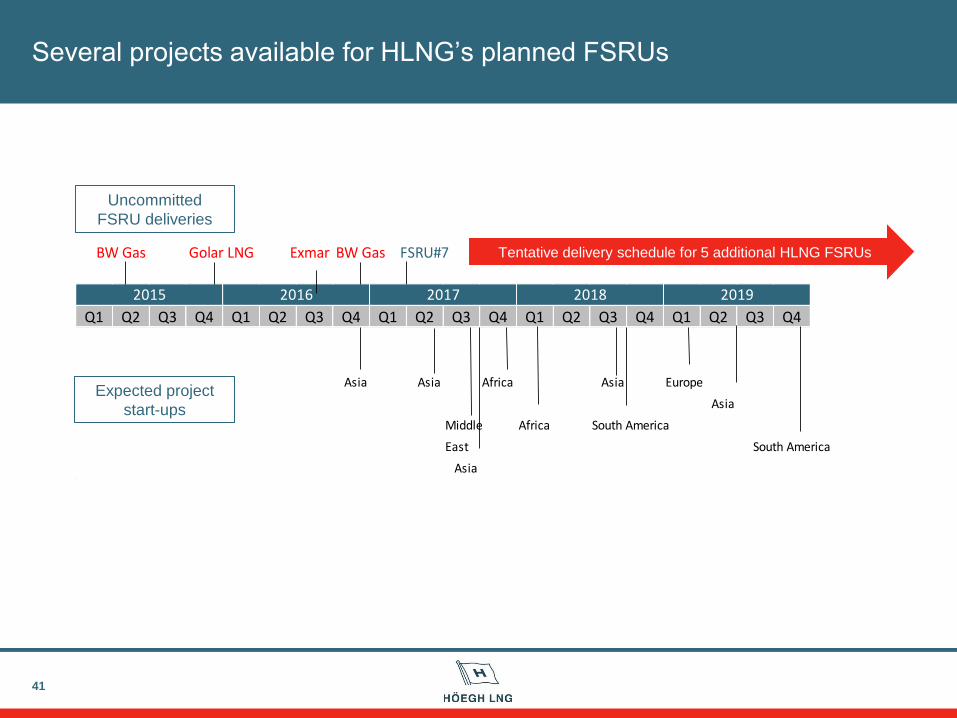

Several projects available for HLNG’s planned FSRUs

41

Uncommitted

FSRU deliveries

BW Gas Golar LNG Exmar BW Gas FSRU#7

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Asia Asia Africa Asia Europe

Asia

Middle Africa South America

East South America

Asia

2015 2017 2018 20192016

Tentative delivery schedule for 5 additional HLNG FSRUs

Expected project

start-ups

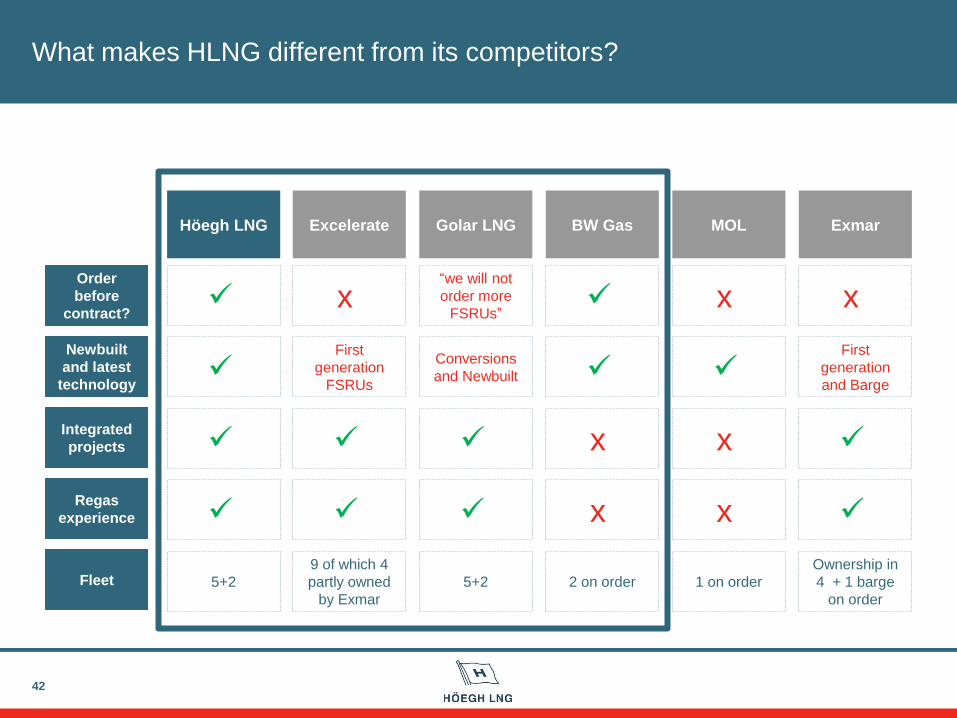

What makes HLNG different from its competitors?

42

i

i

“we will not

order more

FSRUs”

Höegh LNG

Golar LNG

Excelerate

Newbuilt

and latest

technology

i xi Order

before

contract?

Integrated

projects i

First

generation

FSRUs i

xi

Regas

experience i i xi

i

BW Gas

i

xi

xi

Conversions

and Newbuilt

i

MOL

Exmar

xi xi

i

First

generation

and Barge

i i

Fleet 5+2

9 of which 4

partly owned

by Exmar

2 on order 1 on order 5+2

Ownership in

4 + 1 barge

on order

HLNG is considering LNGC deals that will have an accretive impact on

shareholders returns in HMLP

43

Business model

Market update

No speculative orders and no spot exposure

Newbuilding

Latest technology

Short term market is long and will remain so at least until 2016

Little correlation between short term market and medium/long term market

Substantial demand for new tonnage with the right specifications in the next 5 years

due to new export volumes from US and Australia

New buildings will replace existing tonnage due to improved fuel efficiency, size and boil

off

Competition and low barriers to entry

Summary

44

HLNG’s FSRU focus has been a great success – 6 modern FSRUs on long

term contracts

Positive market prospects; increasing demand for FSRUs and entry barriers

continue to be high

HLNG will continue to strengthen its position as the leading player in the

FSRU space

HLNG is considering LNGC deals that will have an accretive impact on

shareholders returns in HMLP

45

FSRU innovation, project execution and operation

Presented by

Vegard Hellekleiv – CTO

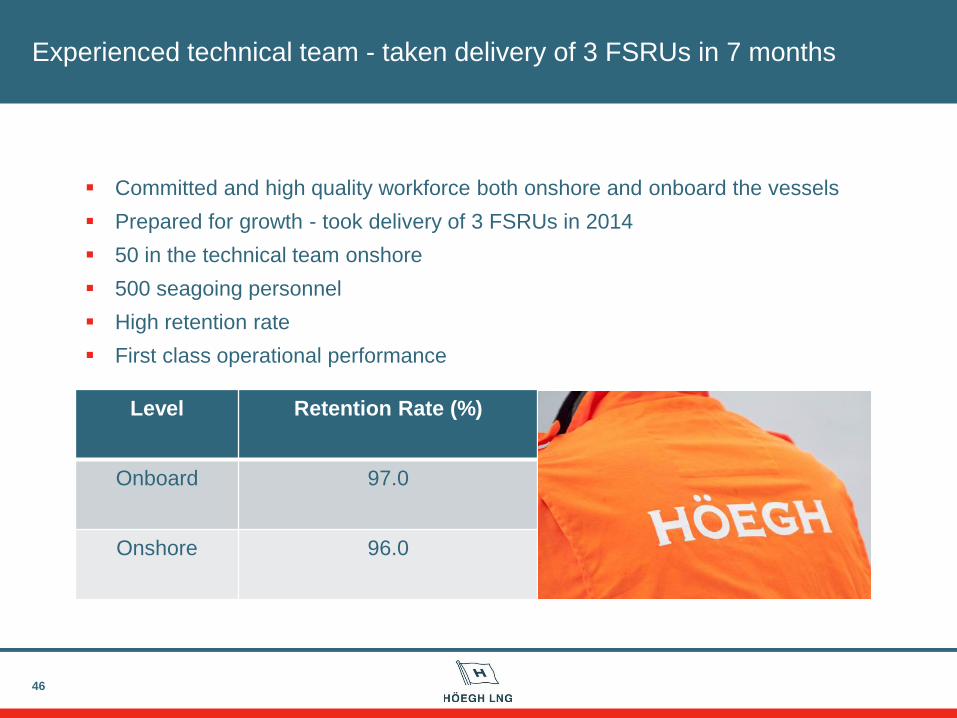

Experienced technical team - taken delivery of 3 FSRUs in 7 months

46

Committed and high quality workforce both onshore and onboard the vessels

Prepared for growth - took delivery of 3 FSRUs in 2014

50 in the technical team onshore

500 seagoing personnel

High retention rate

First class operational performance

Level Retention Rate (%)

Onboard 97.0

Onshore 96.0

Executing USD 1.2 billion construction program

47

Contract signed in June 2011

3 vessels delivered in 2014 and one more coming end of March 2015

Approximately 6 million man-hours for design and construction

Supervision team of 30 people

Zero LTIs to date

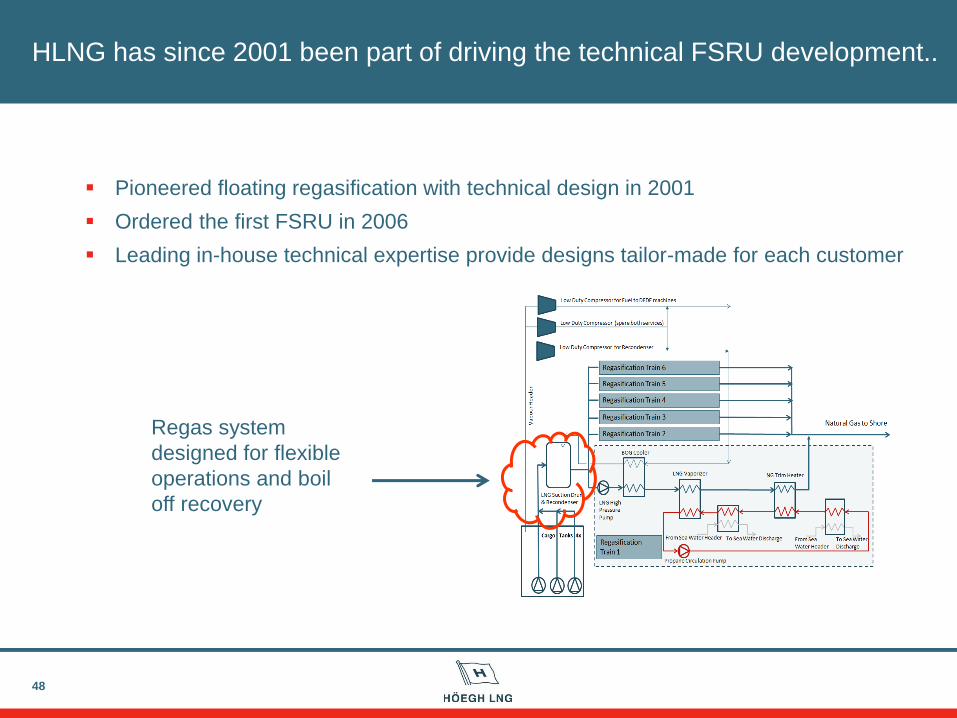

HLNG has since 2001 been part of driving the technical FSRU development..

48

Regas system

designed for flexible

operations and boil

off recovery

Pioneered floating regasification with technical design in 2001

Ordered the first FSRU in 2006

Leading in-house technical expertise provide designs tailor-made for each customer

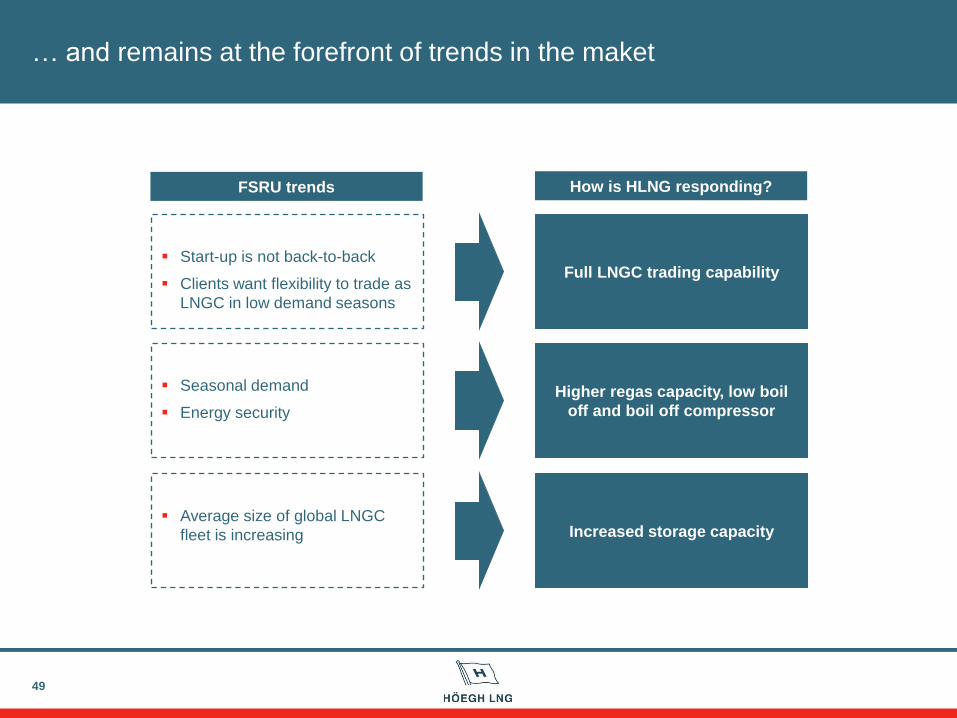

… and remains at the forefront of trends in the maket

49

Full LNGC trading capability

Higher regas capacity, low boil

off and boil off compressor

Start-up is not back-to-back

Clients want flexibility to trade as

LNGC in low demand seasons

Seasonal demand

Energy security

How is HLNG responding?

Increased storage capacity

Average size of global LNGC

fleet is increasing

FSRU trends

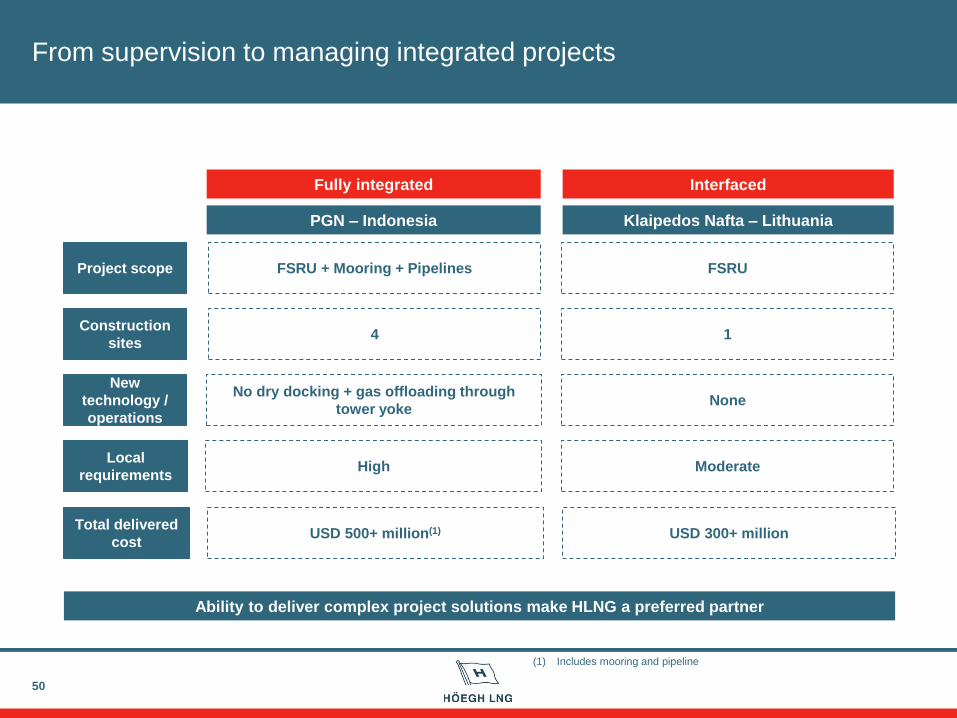

From supervision to managing integrated projects

50

4

None

Construction

sites

FSRU + Mooring + Pipelines FSRU Project scope

New

technology /

operations

No dry docking + gas offloading through

tower yoke

1

Local

requirements High Moderate

Total delivered

cost USD 500+ million(1) USD 300+ million

Ability to deliver complex project solutions make HLNG a preferred partner

Fully integrated Interfaced

PGN – Indonesia Klaipedos Nafta – Lithuania

(1) Includes mooring and pipeline

Summary

51

40 years of LNG experience and 13 years of regas experience

Able to handle growth - took delivery of 3 FSRUs in 2014

Market leading technical competence to optimise designs for the clients

Continously working to develop competitive solutions

52

FLNG strategy

Presented by

Øivin Iversen – CDO

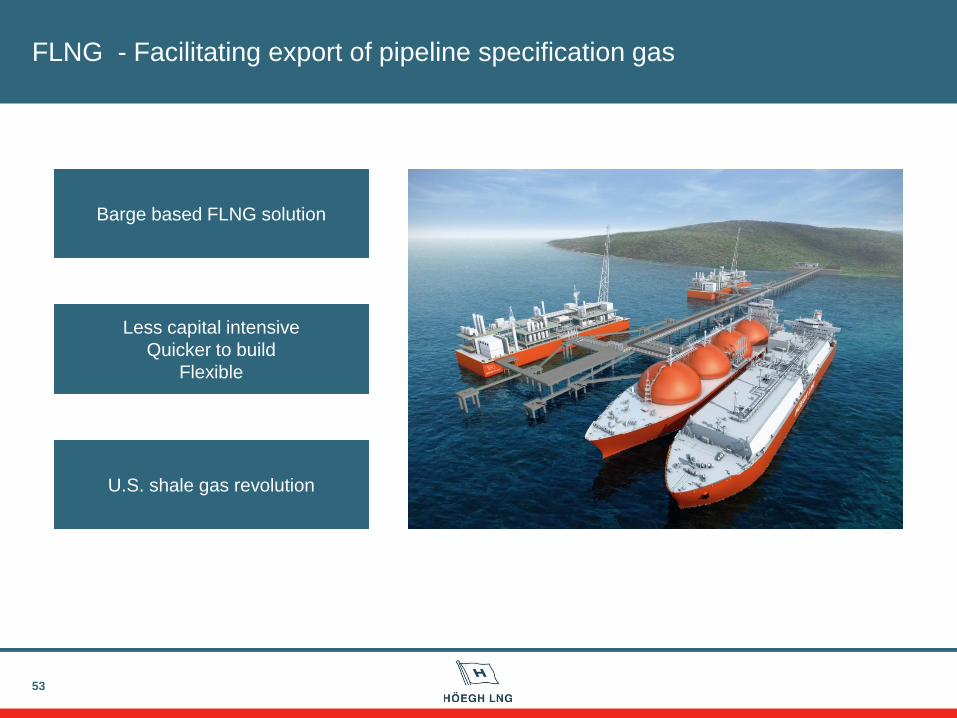

FLNG - Facilitating export of pipeline specification gas

53

U.S. shale gas revolution

Barge based FLNG solution

Less capital intensive

Quicker to build

Flexible

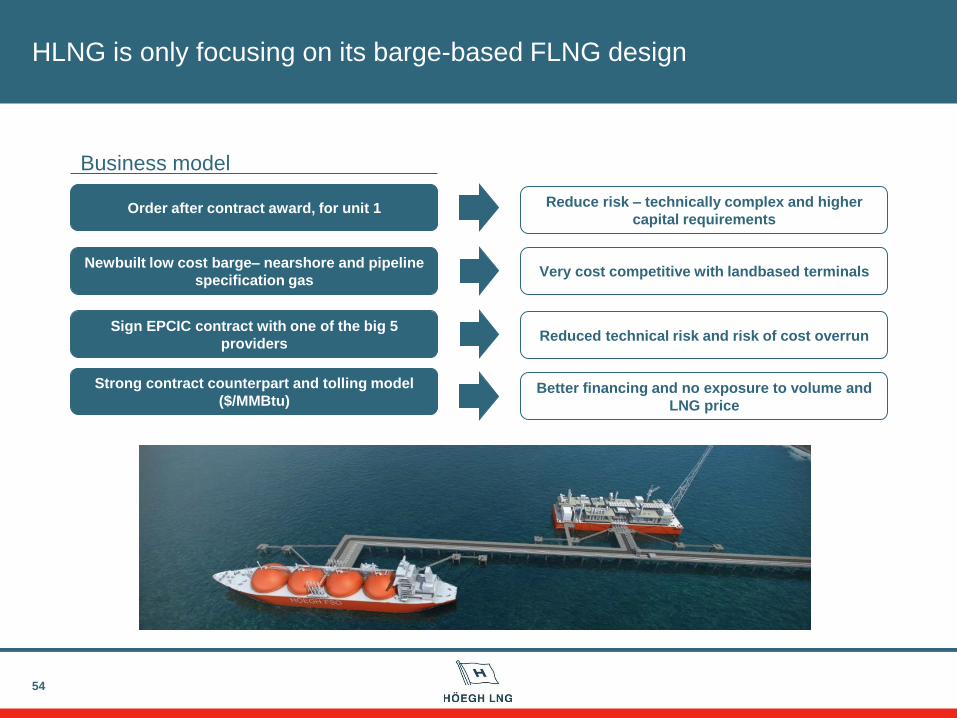

HLNG is only focusing on its barge-based FLNG design

54

Strong contract counterpart and tolling model

($/MMBtu)

Newbuilt low cost barge– nearshore and pipeline

specification gas

Sign EPCIC contract with one of the big 5

providers

Order after contract award, for unit 1

Better financing and no exposure to volume and

LNG price

Very cost competitive with landbased terminals

Reduced technical risk and risk of cost overrun

Reduce risk – technically complex and higher

capital requirements

Business model

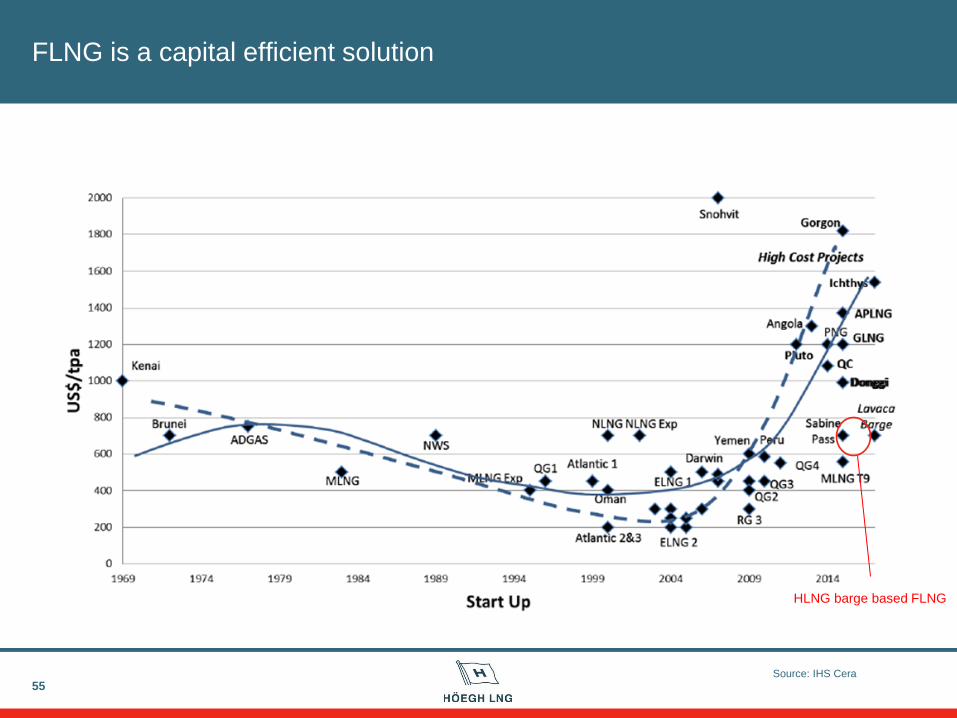

FLNG is a capital efficient solution

55

HLNG barge based FLNG

Source: IHS Cera

Barge FLNG – significantly reduced technical scope

56

Liquefaction volume:

Harsh environment:

Reservoir risk:

Financing and insurance:

Investment level:

Cost per ton:

> 2.5 mmtpa

Yes

Yes

Complex, industrial scheme

4 - 7 billion USD

1 000 – 2 000 USD/ton

Included

Included but limited

Not included

Leads to lower technical risk

and lower cost, also USD/ton

Other

Liquefaction:

Water- and CO2 removal:

Full pre-treatment

Included

Included

Included

< 2.5 mmtpa

No

No

Less complex, marine scheme

1-2 billion USD

550 – 1 000 USD/ton

Technical

specifications

Nearshore FLNG barge Offshore FLNG

57

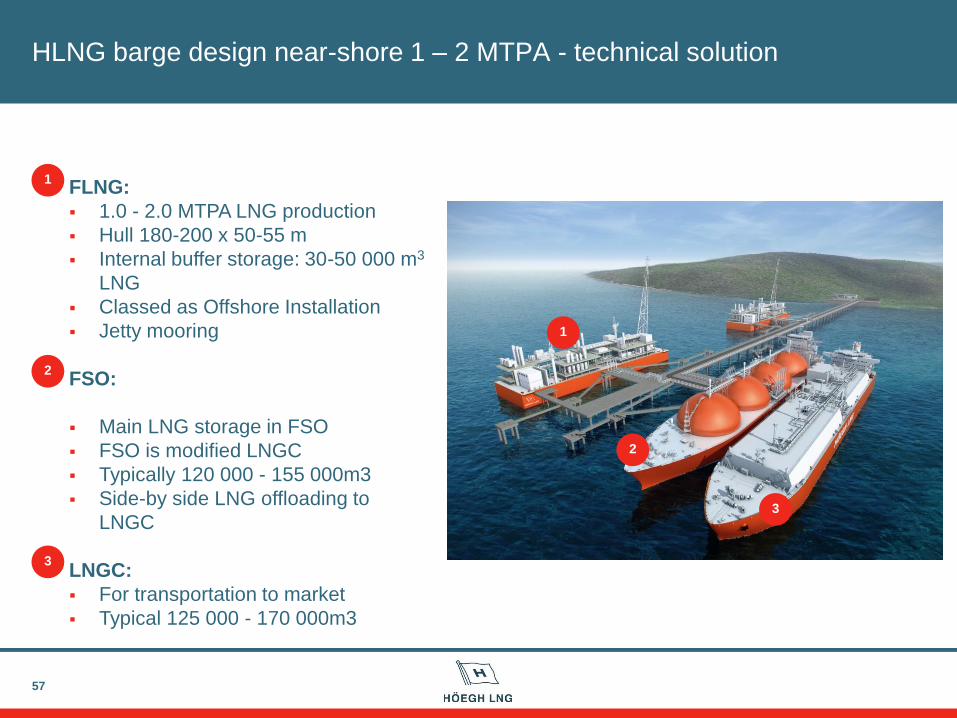

FLNG:

1.0 - 2.0 MTPA LNG production

Hull 180-200 x 50-55 m

Internal buffer storage: 30-50 000 m3

LNG

Classed as Offshore Installation

Jetty mooring

FSO:

Main LNG storage in FSO

FSO is modified LNGC

Typically 120 000 - 155 000m3

Side-by side LNG offloading to

LNGC

LNGC:

For transportation to market

Typical 125 000 - 170 000m3

1

2

2

3

3

HLNG barge design near-shore 1 – 2 MTPA - technical solution

1

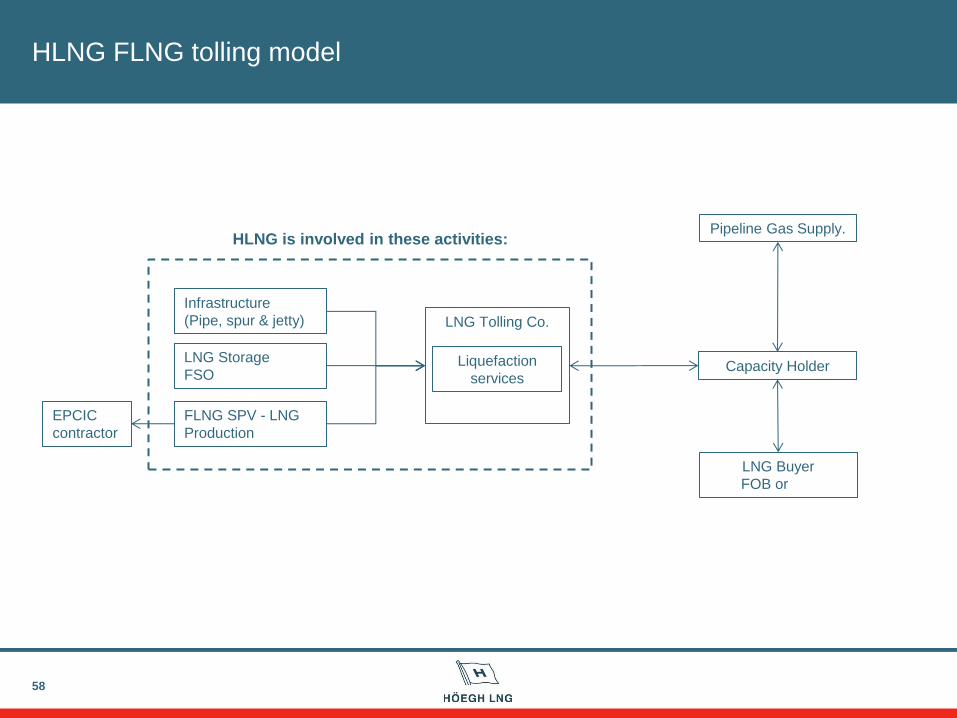

HLNG FLNG tolling model

58

Infrastructure

(Pipe, spur & jetty)

FLNG SPV - LNG

Production

LNG Storage

FSO

LNG Tolling Co.

Liquefaction

services

LNG Buyer

FOB or CIF

Capacity Holder

Pipeline Gas Supply.

EPCIC

contractor

HLNG is involved in these activities:

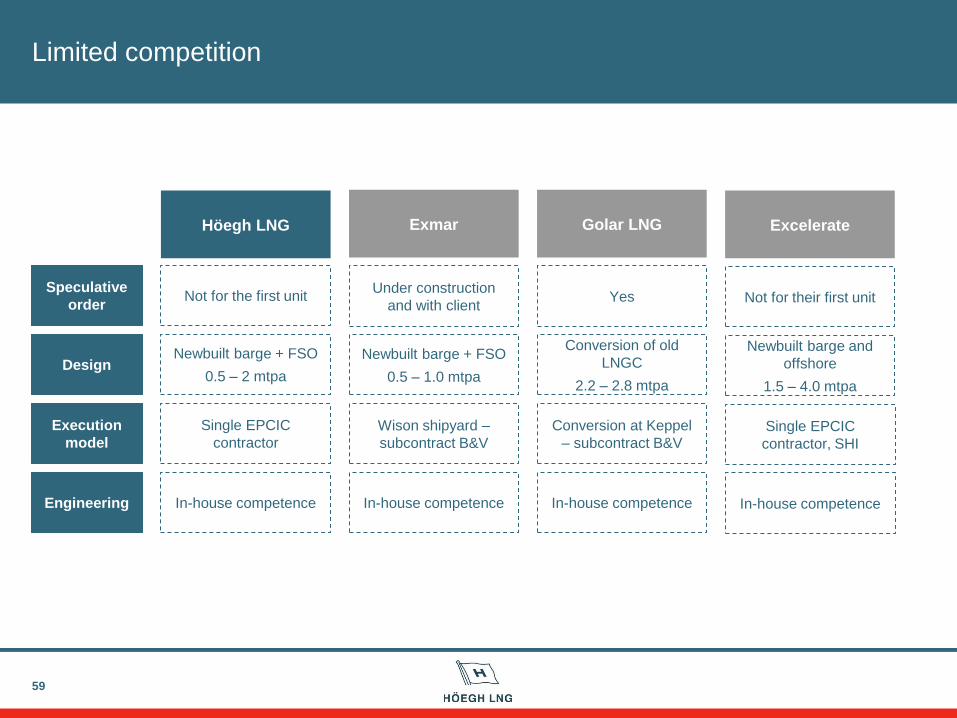

Limited competition

59

Newbuilt barge + FSO

0.5 – 2 mtpa

Wison shipyard –

subcontract B&V

Yes

Höegh LNG

Golar LNG

Exmar

Design

Not for the first unit Under construction

and with client

Speculative

order

Execution

model

Single EPCIC

contractor

Newbuilt barge + FSO

0.5 – 1.0 mtpa

Conversion of old

LNGC

2.2 – 2.8 mtpa

Conversion at Keppel

– subcontract B&V

Engineering In-house competence In-house competence In-house competence

Not for their first unit

Excelerate

Newbuilt barge and

offshore

1.5 – 4.0 mtpa

Single EPCIC

contractor, SHI

In-house competence

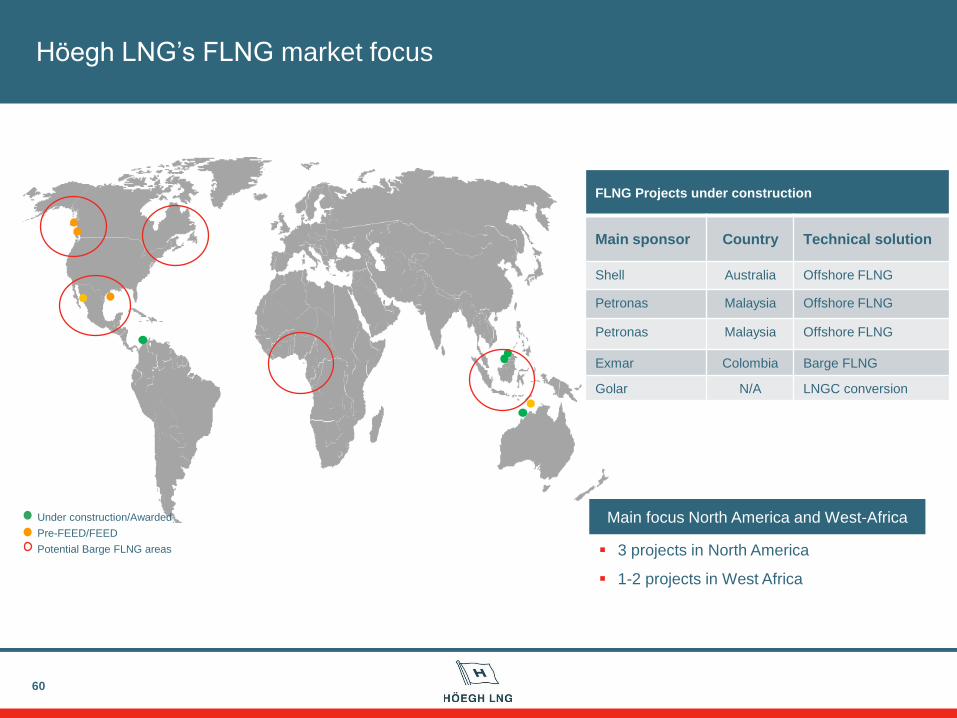

60

FLNG Projects under construction

Main sponsor Country Technical solution

Shell Australia Offshore FLNG

Petronas Malaysia Offshore FLNG

Petronas Malaysia Offshore FLNG

Exmar Colombia Barge FLNG

Golar N/A LNGC conversion

Under construction/Awarded

Pre-FEED/FEED

Potential Barge FLNG areas

Höegh LNG’s FLNG market focus

Main focus North America and West-Africa

3 projects in North America

1-2 projects in West Africa

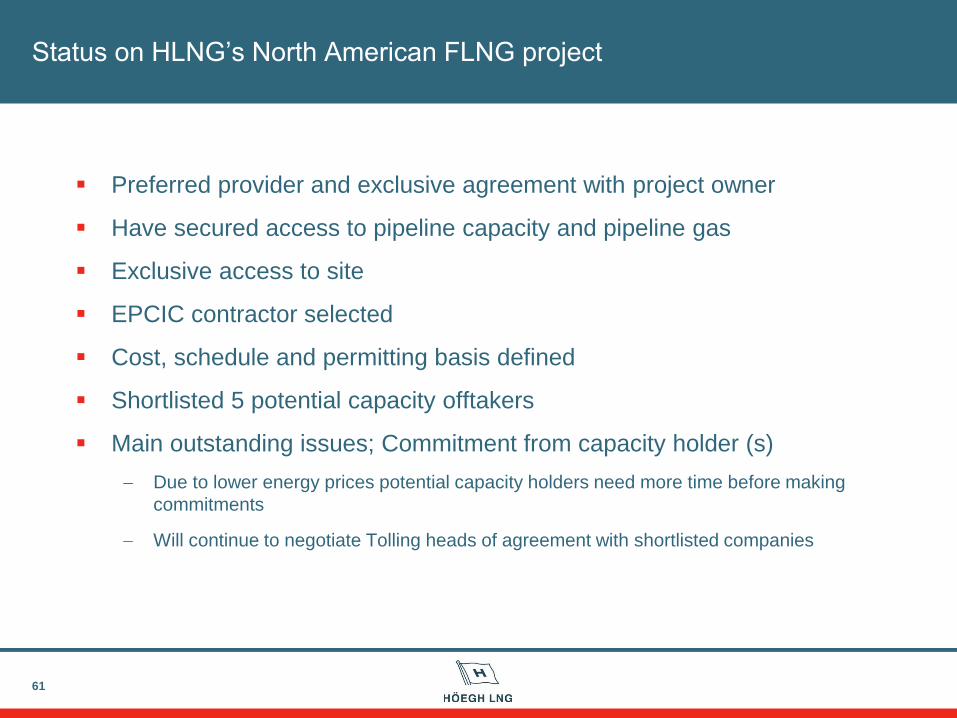

Status on HLNG’s North American FLNG project

Preferred provider and exclusive agreement with project owner

Have secured access to pipeline capacity and pipeline gas

Exclusive access to site

EPCIC contractor selected

Cost, schedule and permitting basis defined

Shortlisted 5 potential capacity offtakers

Main outstanding issues; Commitment from capacity holder (s)

Due to lower energy prices potential capacity holders need more time before making

commitments

Will continue to negotiate Tolling heads of agreement with shortlisted companies

61

Status on key opportunities

62

Sponsor Location

Initial Size

(MTPA) Status

Financial North America 1.8 Existing development agreement

Financial North America 2 x 2 Signed JDA for development phases

HLNG North America 0.5-1.2 Developing the business case

Industrial Africa 1.35+ Completed feasibility study. Client assessing

business case

Industrial North America 2 x 2 Client in process of project due diligence

Summary

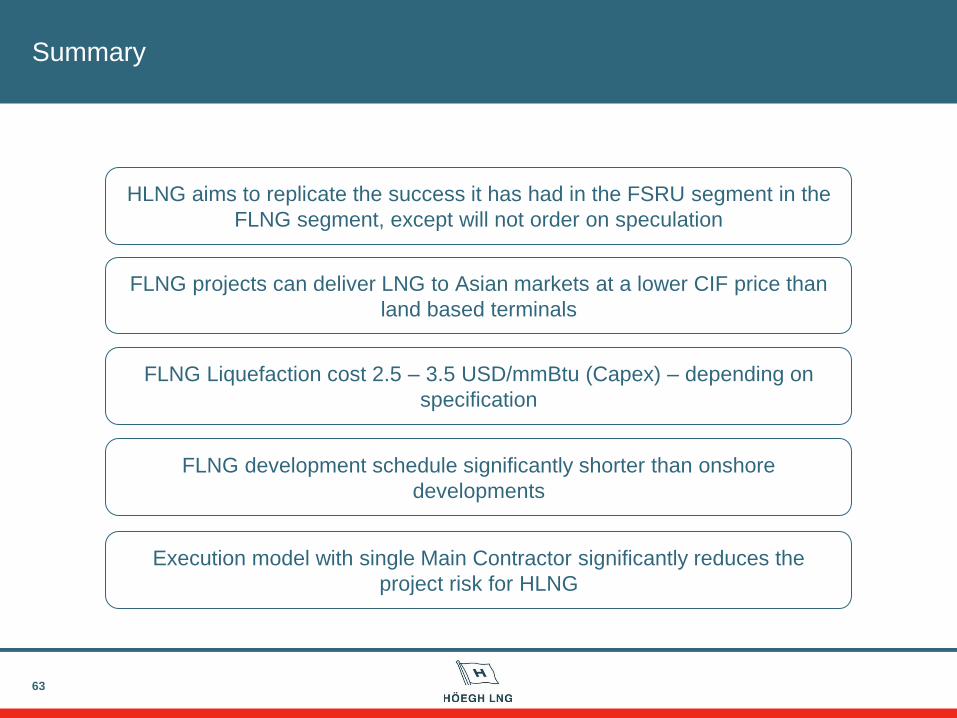

63

HLNG aims to replicate the success it has had in the FSRU segment in the

FLNG segment, except will not order on speculation

FLNG projects can deliver LNG to Asian markets at a lower CIF price than

land based terminals

FLNG Liquefaction cost 2.5 – 3.5 USD/mmBtu (Capex) – depending on

specification

FLNG development schedule significantly shorter than onshore

developments

Execution model with single Main Contractor significantly reduces the

project risk for HLNG

64

Closing remarks

Presented by

Sveinung J.S. Støhle – CEO & President

65

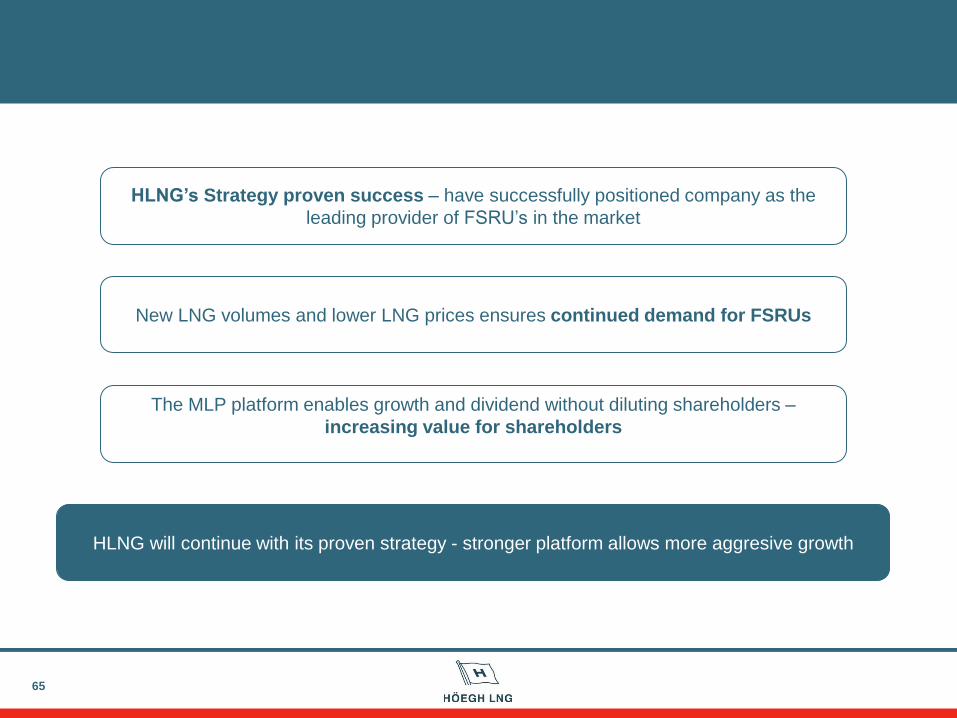

HLNG’s Strategy proven success – have successfully positioned company as the

leading provider of FSRU’s in the market

HLNG will continue with its proven strategy - stronger platform allows more aggresive growth

New LNG volumes and lower LNG prices ensures continued demand for FSRUs

The MLP platform enables growth and dividend without diluting shareholders –

increasing value for shareholders

Recommended