HVS.com HVS | 6th Floor, Building 8-C, DLF Cyber City, Phase – II, Gurgaon 122 002, INDIA

HVS HOTEL MANAGEMENT CONTRACT SURVEY

Manav Thadani, MRICS

Chairman – Asia Pacific

Juie S. MobarAssociate Director – Special Projects

AUGUST 2014

EXCERPTSUSA | EUROPE | APAC

PAGE 2 | EXCERPTS: USA | EUROPE | APAC – HVS HOTEL MANAGEMENT CONTRACT SURVEY

ForewordbyJanA.deRoos

WhydoesthisSurveyaddtoourUnderstandingoftheHotelIndustry?

Neverhastherebeenamorediversesetofhotelmanagementagreementsinuse.Managementagreementswereoriginallyborn

ofadesiretoallowfinancialorpassiveownerstoparticipateintheownershipofhotelrealestatewhilecontractingwith

brandedmanagerstooperatethehotelontheowners'behalf.Thisdesirehasevolvedintoaverysophisticatedmarketinwhich

ownersoftherealpropertycontractwithownersofintellectualcapitalovertheuse,branding,andlong-termcontrolofhotel

assets.Itisclearthattwofundamentalforcesdrivemanagementcontractnegotiation:theexperiencegainedfromthe

recenteconomicstressesappliedtotheentireindustry,andmattersspecifictoagivenhotelinagivenlocation.Thecurrentand

nextgenerationofcontractsmustanticipatebothforces.

Today'shotelownersincluderealestateinvestmenttrusts(REITs),realestatehedgefunds,realestateprivateequityfunds,

sovereign wealth funds, life insurance companies, pension funds and private wealth clients. Operators include global

corporationswithmultiplebrandsforeachmarket,globalsingle-brandcompanies,andregionaloperators(bothwithand

withoutbrands).Whiletherelativestrengthsofthepartieshaveagreatinfluenceoncontractnegotiations,itisnot

necessarilythecasethatthepartywiththegreatestmarketcapitalisationhasthegreatestpowerinanygivenhotelat

anygiventime.Withsomanypotentialoutcomes,howcanoneseethe“bigpicture”andunderstandacontract'sstrategic

levers?

Fortunately,aworklikethe“HVSHotelManagementContractSurvey”byManavThadaniandJuieMobarprovidesanexcellent

and invaluable survey thathelpsusunderstand the termsand language in contemporaryhotelmanagement agreements

(HMAs).Theirsisthefirstsurveywithatrulyglobalperspectiveonthestructureofmanagementcontracts.

TheauthorspresentandaddresstheuniquefeaturesofHMAsinadirectandcandidwayprovidingowners,investorsand

lenderswithauniqueperspectivethatonlycomesfromhands-onexperienceinthehotelsectoroveralongperiodoftime.This

depthofknowledgecomesfromaconsultingandadvisoryteamthatworkssolelyonhospitalityassets. Theauthorsprovide

insightintothefiveprincipalsectionsofamanagementcontract:termandrenewals,operatormanagementfees,performance

test,budgetandexpenditures,andterminationofthecontractbyowner.

Theauthors'objectiveofprovidinginsightintocontemporaryHMApracticeisfullyrealisedinthisimportantwork.Inaddition,

bymakingthisavailableforpurchaseviatheHVSBookstore,theyhavecommittedtoeducatingabroadaudiencewithrelevant

andcurrentpractice.IcommendThadaniandMobarfortheirexcellentandinvaluablesurvey.

JanA.deRoosIthaca,NewYorkJuly28,2014

JanA.deRoosistheHVSProfessorofHotelFinanceandRealEstateatCornellUniversity'sSchoolofHotelAdministration.Heisco-

author ofTheNegotiationandAdministrationofHotelManagementContracts, long considered to be the industry's leading

referenceonhotelmanagementagreements.Thecurrentfourthedition(2009),co-authoredwithJamesEyster,isavailableat:

[email protected](607)255-2933.

EXCERPTS: USA | EUROPE | APAC – HVS HOTEL MANAGEMENT CONTRACT SURVEY | PAGE 3

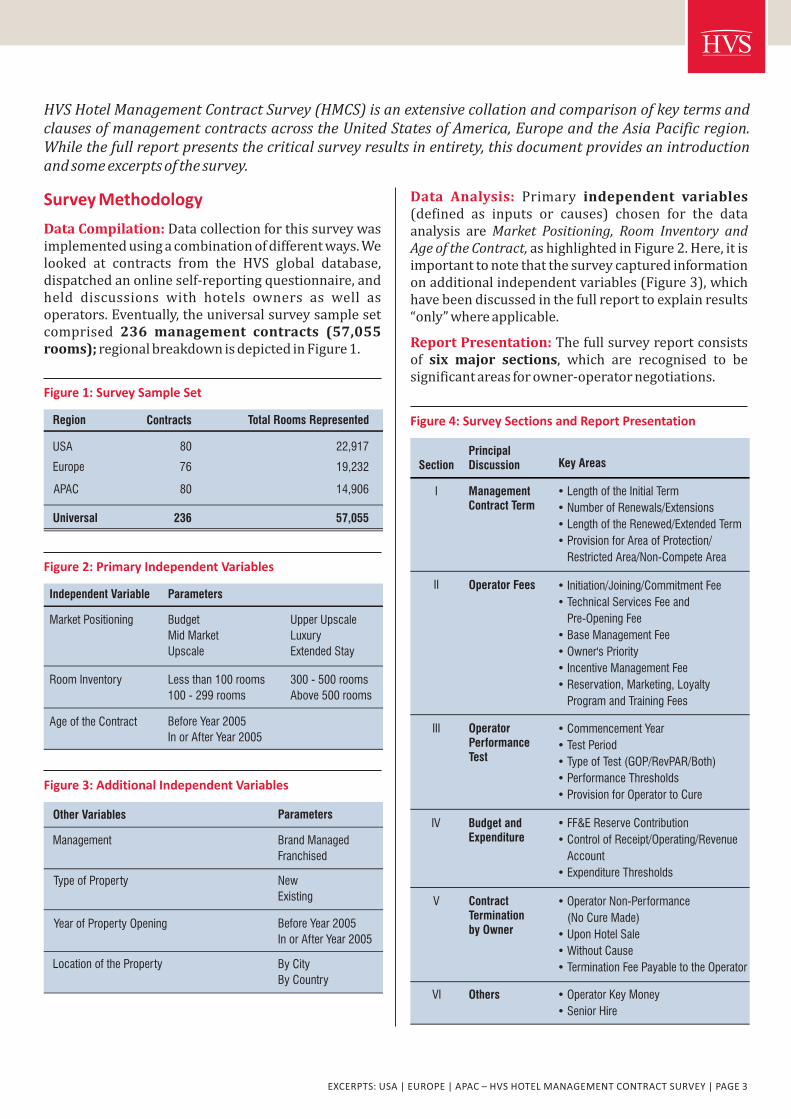

Figure 1: Survey Sample Set

Figure 2: Primary Independent Variables

Figure 3: Additional Independent Variables

Figure 4: Survey Sections and Report PresentationRegion Contracts Total Rooms Represented

USA 80 22,917

Europe 76 19,232

APAC 80 14,906

Universal 236 57,055

Independent Variable

Market Positioning Budget

Mid Market

Upscale

Upper Upscale

Luxury

Extended Stay

Room Inventory Less than 100 rooms

100 - 299 rooms

300 - 500 rooms

Above 500 rooms

Age of the Contract Before Year 2005

In or After Year 2005

Parameters

Other Variables Parameters

Management Brand Managed

Franchised

Type of Property New

Existing

Year of Property Opening Before Year 2005

In or After Year 2005

Location of the Property By City

By Country

SectionPrincipal Discussion Key Areas

I Management Contract Term

• Length of the Initial Term

• Number of Renewals/Extensions

• Length of the Renewed/Extended Term

• Provision for Area of Protection/

Restricted Area/Non-Compete Area

II Operator Fees

III Operator Performance Test

IV Budget and Expenditure

V Contract Termination by Owner

VI Others

• Initiation/Joining/Commitment Fee

• Technical Services Fee and

Pre-Opening Fee

• Base Management Fee

• Owner's Priority

• Incentive Management Fee

• Reservation, Marketing, Loyalty

Program and Training Fees

• Commencement Year

• Test Period

• Type of Test (GOP/RevPAR/Both)

• Performance Thresholds

• Provision for Operator to Cure

• FF&E Reserve Contribution

• Control of Receipt/Operating/Revenue

Account

• Expenditure Thresholds

• Operator Non-Performance

(No Cure Made)

• Upon Hotel Sale

• Without Cause

• Termination Fee Payable to the Operator

• Operator Key Money

• Senior Hire

HVSHotelManagementContractSurvey(HMCS)isanextensivecollationandcomparisonofkeytermsandclausesofmanagementcontractsacrosstheUnitedStatesofAmerica,EuropeandtheAsiaPacificregion.Whilethefullreportpresentsthecriticalsurveyresultsinentirety,thisdocumentprovidesanintroductionandsomeexcerptsofthesurvey.

Data Analysis: Primary independent variables(defined as inputs or causes) chosen for the dataanalysis areMarket Positioning, Room Inventory andAgeoftheContract,ashighlightedinFigure2.Here,itisimportanttonotethatthesurveycapturedinformationonadditionalindependentvariables(Figure3),whichhavebeendiscussedinthefullreporttoexplainresults“only”whereapplicable.

ReportPresentation:Thefullsurveyreportconsistsof six major sections, which are recognised to besignificantareasforowner-operatornegotiations.

Survey Methodology

DataCompilation:Datacollectionforthissurveywasimplementedusingacombinationofdifferentways.Welooked at contracts from the HVS global database,dispatchedanonlineself-reportingquestionnaire,andheld discussions with hotels owners as well asoperators.Eventually,theuniversalsurveysamplesetcomprised 236 management contracts (57,055rooms);regionalbreakdownisdepictedinFigure1.

PAGE 4 | USA | EUROPE | APAC – HVS HOTEL MANAGEMENT CONTRACT SURVEY

Hotel Companies Represented In This Survey

Totally,38 branded hotel companies have been represented in this survey, in addition to a few independentoperatorsandseveralthird-partymanagementcompanies.

Figure 5: Hotel Companies (Branded) Represented in the Survey

Accor

Aman Resorts

Americas Best Value Inn (Vantage)

Banyan Tree Hotels and Resorts

Best Western

Caesars Entertainment

Carlson Rezidor

Choice Hotels

Club Méditerranée

Concept Hospitality

Dusit Hotels and Resorts

Fairmont Rafes Hotels International

Four Seasons Hotels and Resorts

Fortune Hotels and Resorts (ITC)

Hilton Worldwide

Hyatt Hotels Corporation

InterContinental Hotels Group

Jumeirah Group

Kempinski Hotels

La Quinta Inns and Suites

Louvre Hotels

Mandarin Oriental Hotel Group

Marriott International

Minor Hotel Group

Moevenpick Hotels and Resorts

Omni Hotels and Resorts

One&Only Luxury Resorts

Peninsula Hotels (HSH Group)

Premier Inn (Whitbread)

Rosewood Hotels and Resorts

Sarovar Hotels and Resorts

Shangri-La Hotels and Resorts

Six Senses Hotels, Resorts and Spas

Starwood Hotels and Resorts

Taj Group

The Leela Palaces, Hotels and Resorts

Trump International

Wyndham Worldwide

Report Purchase And Ordering Instructions

Thefullsurveyreportcomprisingaround35pagescanbepurchasedforUS$2,000.Toprocurethesame,pleaselogontothe ThereportwillbeavailablebothinPDF(softcopy)aswellasinprint(hardcopy).HVSBookstore.Thepurchaserwillbeallowedtochoosethepreferredformat,postwhichapersonalisedcopyofthereportwillbesentacross.

Fororderinginstructionsoranyotherassistance,pleasecontact:

JuieS.MobarAssociateDirector–SpecialProjectsHVSEmail:[email protected]

Dataconfidentialityhasbeenstrictlymaintainedthroughoutthissurvey,withresultsinthereportbeingpresentedonlyinaggregateandnoindividualcontractdetailsbeingrevealed.

EXCERPT I

Length of the Initial Term

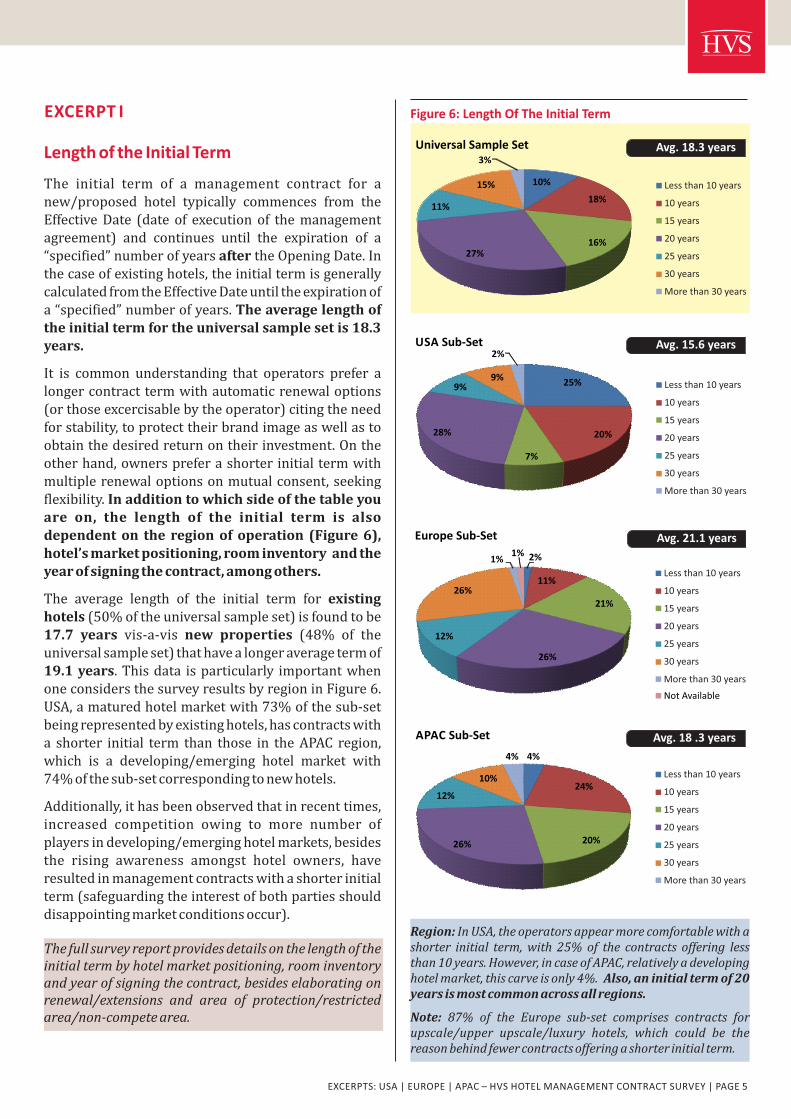

The initial term of a management contract for anew/proposed hotel typically commences from theEffectiveDate (date of executionof themanagementagreement) and continues until the expiration of a“specified”numberofyearsaftertheOpeningDate.Inthecaseofexistinghotels,theinitialtermisgenerallycalculatedfromtheEffectiveDateuntiltheexpirationofa“specified”numberofyears.Theaveragelengthoftheinitialtermfortheuniversalsamplesetis18.3years.

It is common understanding that operators prefer alongercontracttermwithautomaticrenewaloptions(orthoseexcercisablebytheoperator)citingtheneedforstability,toprotecttheirbrandimageaswellastoobtainthedesiredreturnontheirinvestment.Ontheotherhand,ownerspreferashorterinitialtermwithmultiplerenewaloptionsonmutualconsent,seekingflexibility.Inadditiontowhichsideofthetableyouare on, the length of the initial term is alsodependent on the region of operation (Figure 6),hotel’smarketpositioning,roominventoryandtheyearofsigningthecontract,amongothers.

The average length of the initial term for existinghotels(50%oftheuniversalsampleset)isfoundtobe17.7 years vis-a-vis new properties (48% of theuniversalsampleset)thathavealongeraveragetermof19.1years.Thisdata isparticularly importantwhenoneconsidersthesurveyresultsbyregioninFigure6.USA,amaturedhotelmarketwith73%ofthesub-setbeingrepresentedbyexistinghotels,hascontractswitha shorter initial term than those in theAPAC region,which is a developing/emerging hotel market with74%ofthesub-setcorrespondingtonewhotels.

Additionally,ithasbeenobservedthatinrecenttimes,increased competition owing to more number ofplayersindeveloping/emerginghotelmarkets,besidesthe rising awareness amongst hotel owners, haveresultedinmanagementcontractswithashorterinitialterm(safeguardingtheinterestofbothpartiesshoulddisappointingmarketconditionsoccur).

Thefullsurveyreportprovidesdetailsonthelengthoftheinitialtermbyhotelmarketpositioning,roominventoryandyearofsigningthecontract,besideselaboratingonrenewal/extensions and area of protection/restrictedarea/non-competearea.

Figure 6: Length Of The Initial Term

25%

20%

7%

28%

9%9%

2%USA Sub-Set

Less than 10 years

10 years

15 years

20 years

25 years

30 years

More than 30 years

Avg. 15.6 years

Europe Sub-Set

2%

11%

21%

26%

12%

26%

1%1%

Less than 10 years

10 years

15 years

20 years

25 years

30 years

More than 30 years

Not Available

Avg. 21.1 years

4%

24%

20%26%

12%

10%

4%

APAC Sub-Set

Less than 10 years

10 years

15 years

20 years

25 years

30 years

More than 30 years

Avg. 18 .3 years

Region:InUSA,theoperatorsappearmorecomfortablewithashorter initial term,with 25%of the contracts offering lessthan10years.However,incaseofAPAC,relativelyadevelopinghotelmarket,thiscarveisonly4%.Also,aninitialtermof20yearsismostcommonacrossallregions.

Note: 87% of the Europe sub-set comprises contracts forupscale/upper upscale/luxury hotels, which could be thereasonbehindfewercontractsofferingashorterinitialterm.

EXCERPTS: USA | EUROPE | APAC – HVS HOTEL MANAGEMENT CONTRACT SURVEY | PAGE 5

Universal Sample Set

10%

18%

16%27%

11%

15%

3%

Less than 10 years

10 years

15 years

20 years

25 years

30 years

More than 30 years

Avg. 18.3 years

PAGE 6 | USA | EUROPE | APAC – HVS HOTEL MANAGEMENT CONTRACT SURVEY

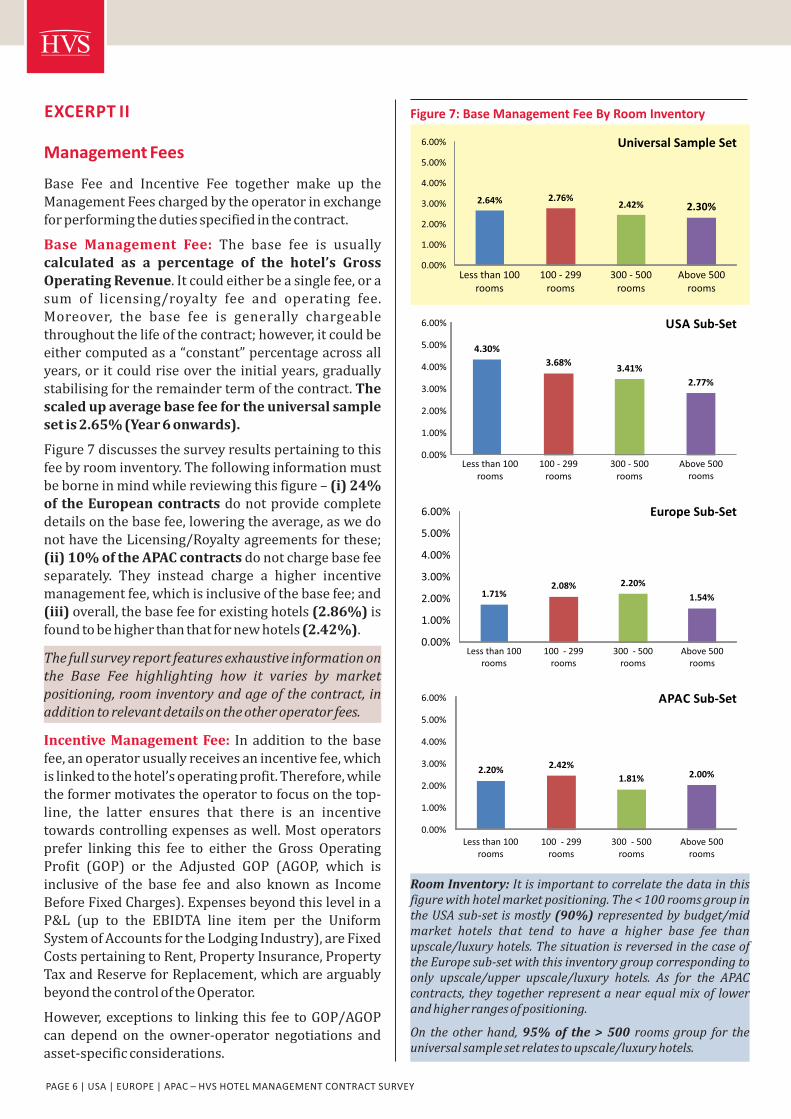

Figure 7: Base Management Fee By Room Inventory

RoomInventory:Itisimportanttocorrelatethedatainthisfigurewithhotelmarketpositioning.The<100roomsgroupintheUSAsub-setismostly(90%)representedbybudget/midmarket hotels that tend to have a higher base fee thanupscale/luxuryhotels.ThesituationisreversedinthecaseoftheEuropesub-setwiththisinventorygroupcorrespondingtoonly upscale/upper upscale/luxury hotels. As for the APACcontracts,theytogetherrepresentanearequalmixoflowerandhigherrangesofpositioning.

On the otherhand,95%of the>500 roomsgroup for theuniversalsamplesetrelatestoupscale/luxuryhotels.

2.64% 2.76%2.42% 2.30%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Less than 100 rooms

100 - 299 rooms

300 - 500 rooms

Above 500 rooms

Universal Sample Set

2.20% 2.42%

1.81% 2.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00% APAC Sub-Set

Less than 100 rooms

100 - 299 rooms

300 - 500 rooms

Above 500 rooms

1.71%2.08% 2.20%

1.54%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Less than 100 rooms

100 - 299 rooms

300 - 500 rooms

Above 500 rooms

Europe Sub-Set

4.30%

3.68%3.41%

2.77%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Less than 100 rooms

100 - 299 rooms

300 - 500 rooms

Above 500 rooms

USA Sub-Set

EXCERPT II

Management Fees

Base Fee and Incentive Fee together make up theManagementFeeschargedbytheoperatorinexchangeforperformingthedutiesspecifiedinthecontract.

Base Management Fee: The base fee is usuallycalculated as a percentage of the hotel’s GrossOperatingRevenue.Itcouldeitherbeasinglefee,orasum of licensing/royalty fee and operating fee.Moreover, the base fee is generally chargeablethroughoutthelifeofthecontract;however,itcouldbeeithercomputedasa“constant”percentageacrossallyears,oritcouldriseovertheinitialyears,graduallystabilisingfortheremaindertermofthecontract.Thescaledupaveragebasefeefortheuniversalsamplesetis2.65%(Year6onwards).

Figure7discussesthesurveyresultspertainingtothisfeebyroominventory.Thefollowinginformationmustbeborneinmindwhilereviewingthisfigure–(i)24%oftheEuropeancontractsdonotprovidecompletedetailsonthebasefee,loweringtheaverage,aswedonothavetheLicensing/Royaltyagreementsforthese;(ii)10%oftheAPACcontractsdonotchargebasefeeseparately. They instead charge a higher incentivemanagementfee,whichisinclusiveofthebasefee;and(iii)overall,thebasefeeforexistinghotels(2.86%)isfoundtobehigherthanthatfornewhotels(2.42%).

Thefullsurveyreportfeaturesexhaustiveinformationonthe Base Fee highlighting how it varies by marketpositioning,roominventoryandageofthecontract,inadditiontorelevantdetailsontheotheroperatorfees.

Incentive Management Fee: Inaddition to thebasefee,anoperatorusuallyreceivesanincentivefee,whichislinkedtothehotel’soperatingprofit.Therefore,whiletheformermotivatestheoperatortofocusonthetop-line, the latter ensures that there is an incentivetowardscontrollingexpensesaswell.Mostoperatorsprefer linking this fee to either the Gross OperatingProfit (GOP) or the Adjusted GOP (AGOP, which isinclusive of the base fee and also known as IncomeBeforeFixedCharges).ExpensesbeyondthislevelinaP&L (up to the EBIDTA line item per the UniformSystemofAccountsfortheLodgingIndustry),areFixedCostspertainingtoRent,PropertyInsurance,PropertyTaxandReserveforReplacement,whicharearguablybeyondthecontroloftheOperator.

However,exceptionsto linkingthis fee toGOP/AGOPcan depend on the owner-operator negotiations andasset-specificconsiderations.

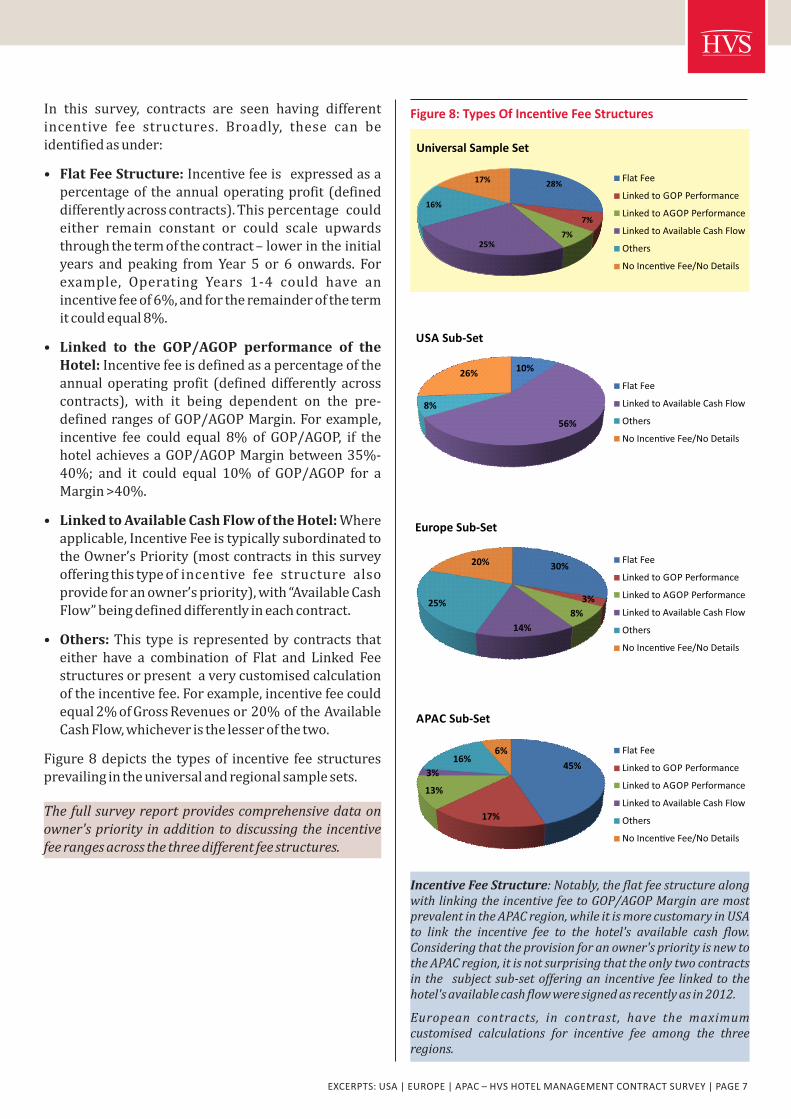

In this survey, contracts are seen having differentincentive fee structures. Broadly, these can beidentifiedasunder:

• Incentivefeeis expressedasaFlatFeeStructure: percentageof theannualoperatingprofit (defined differentlyacrosscontracts).Thispercentage could either remain constant or could scale upwards throughthetermofthecontract–lowerintheinitial years and peaking from Year 5 or 6 onwards. For example, Operating Years 1-4 could have an incentivefeeof6%,andfortheremainderoftheterm itcouldequal8%.

• Linked to the GOP/AGOP performance of the Hotel:Incentivefeeisdefinedasapercentageofthe annual operatingprofit (defineddifferently across contracts), with it being dependent on the pre- definedrangesofGOP/AGOPMargin.Forexample, incentive fee could equal 8% of GOP/AGOP, if the hotelachievesaGOP/AGOPMarginbetween35%- 40%; and it could equal 10% of GOP/AGOP for a Margin>40%.

• WhereLinkedtoAvailableCashFlowoftheHotel: applicable,IncentiveFeeistypicallysubordinatedto theOwner’sPriority(mostcontractsinthissurvey offeringthistypeofincentive fee structure also provideforanowner’spriority),with“AvailableCash Flow”beingdefineddifferentlyineachcontract.

• This type isrepresentedbycontracts thatOthers: either have a combination of Flat and Linked Fee structuresorpresentaverycustomisedcalculation oftheincentivefee.Forexample,incentivefeecould equal2%ofGrossRevenuesor20%oftheAvailable CashFlow,whicheveristhelesserofthetwo.

Figure8depicts the typesof incentive feestructuresprevailingintheuniversalandregionalsamplesets.

Thefullsurveyreportprovidescomprehensivedataonowner'spriorityinadditiontodiscussingtheincentivefeerangesacrossthethreedifferentfeestructures.

Figure 8: Types Of Incentive Fee Structures

IncentiveFeeStructure:Notably,theflatfeestructurealongwithlinkingtheincentivefeetoGOP/AGOPMarginaremostprevalentintheAPACregion,whileitismorecustomaryinUSAto link the incentive fee to the hotel's available cash flow.Consideringthattheprovisionforanowner'spriorityisnewtotheAPACregion,itisnotsurprisingthattheonlytwocontractsinthe subjectsub-setofferinganincentivefee linkedtothehotel'savailablecashflowweresignedasrecentlyasin2012.

European contracts, in contrast, have the maximumcustomised calculations for incentive fee among the threeregions.

Flat Fee

Linked to GOP Performance

Linked to AGOP Performance

Linked to Available Cash Flow

Others

No Incen�ve Fee/No Details

45%

17%

13%

3%

16%6%

APAC Sub-Set

10%

56%

8%

26%

USA Sub-Set

Flat Fee

Linked to Available Cash Flow

Others

No Incen�ve Fee/No Details

30%

3%

8%

14%

25%

20%

Europe Sub-Set

Flat Fee

Linked to GOP Performance

Linked to AGOP Performance

Linked to Available Cash Flow

Others

No Incen�ve Fee/No Details

EXCERPTS: USA | EUROPE | APAC – HVS HOTEL MANAGEMENT CONTRACT SURVEY | PAGE 7

28%

7%

7%25%

16%

17%

Universal Sample Set

Flat Fee

Linked to GOP Performance

Linked to AGOP Performance

Linked to Available Cash Flow

Others

No Incen�ve Fee/No Details

HVS.com HVS | 6th Floor, Building 8-C, DLF Cyber City, Phase – II, Gurgaon 122 002, INDIA

About HVSHVS is the world's leading consulting and services organisation

focused on the hotel, mixed-use, shared ownership, gaming, and

leisure industries. Established in 1980, the company performs 4500+

assignments each year for hotel and real estate owners, operators,

and developers worldwide. HVS principals are regarded as the

leading experts in their respective regions of the globe. Through a

network of more than 30 offices and 450 professionals, HVS provides

an unparalleled range of complementary services for the hospitality

industry. HVS.com

Manav Thadani, MRICS,Chairman,AsiaPacific,HVSfounded the New Delhiofficein1997.Heisactivelyi nvo lved i n op e ra to rs e a r c h /ma n a g eme n tcontract negotiations and

providesstrategicadvicetokeyclients.Headditionally serves as amentor to otherHVSverticalsintheAPACregion,andistheglobal head of HVS Sustainability.Moreover, Manav oversees the planningand implementation of the regionalHVSconferences, including Hotel InvestmentConference–SouthAsia(HICSA);Tourism,Ho te l I nve s tmen t & Ne twork ingConference (THINC) Indonesia; and theChina Hotel Investment Conference(CHIC). On a personal level, Manav co-foundedSAMHIin2011,aleadingIndianhotel investment and development firmwithfocusonownershipofbrandedhotelsin the mid-scale/economy [email protected]

About the Authors

Juie S. Mobar is AssociateDirector - Special ProjectswithHVS'NewDelhioffice.Shehasspentfiveyearswiththe company starting as aConsulting & ValuationAnalyst . In addit ion to

having worked on feasibility studies,v a l u a t i o n s , ma rke t s t u d i e s a ndoperational audits in the past, Juie hasbeenactivelyinvolvedinoperatorsearchand management contract negotiations,research-based assignments and selectwork for HVS Susta inabi l i ty. Shecompleted her Management TraineeProgramwiththeTajGroupin2006,andholds a BA (Hon) in Hotel Managementfrom the Institute of Hotel ManagementAurangabad (University of Huddersfield,UK ) a n d B a c h e l o r s i n B u s i n e s sAdministrat ion from [email protected]

Superior Results through Unrivalled Hospitality Intelligence. Everywhere.

HVS Consulting & Valuation enjoys impeccable worldwide

reputation for credibility, excellence and thoroughness. With offices

strategically located throughout North and South America, Asia,

Europe and the Middle East, our clients benefit from local insights

and international expertise.

Recommended