www.pwc.ru/

IFRS 15: Implementation challenges

29 July 2014

Christoph Cruss Partner, PwC Germany

PwC

Agenda

Revenue Impacts the Entire Organization

Impact Study of various Industries

Key aspects to consider implementing IFRS 15

Slide 2

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Revenue Impacts the Entire Organization

Accounting is only the tip of the iceberg

Slide 3

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Accounting & Reporting • Changes to revenue model

- Number of things to track

- Allocation of revenue

- Timing of recognition

• Changes beyond revenue

- collectibility; time value of

money; sales commissions

• Judgment & estimates

• Additional disclosures

• Transition considerations

Process & Systems • Impacts across quote-to-cash cycle

• Involvement of IT is paramount

• Likely to accelerate trend of revenue

automation (replacing Excel and

manual processes)

• Potentially IT 3-5 year

roadmaps

• Significant Cost trigger

Cross-functional Impacts Business Changes

Revenue Impacts the Entire Organization Is it a main operational change

• Executive management

• Audit Committee

• Investor Relations

• Financial Planning & Analysis

• Sales

• Legal

• HR

• Tax

• Accounting and IT Functions

• Changing business models

- Organic changes

- M&A activity

• Opportunity to structure and

go-to-market differently

• Pricing strategy

• Impact on compensation

• Executive communication and awarenes

Slide 4

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Impact Study of various Industries

It really depends on your business models

Slide 5

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Impact Study of various Industries It really depends on your business models

Review of all contracts is required

Disclosures are affected

Staff training and education

needed

Assessment of collectability, time value of money, …

•Subsidized services/warranties

•Tooling and products

Automotive

• Licenses

• Multiple element arrangements

• Variable consideration

Software

•Subsidized services/products

•Licenses

•Milestone payments

•Multiple element arrangements

Healthcare & Pharma

•Licenses

•Variable consideration

•Multiple element arrangements

•Subsidized hardware

Media

• Variable consideration

Energy

• Multiple element arrangements

• Collectability • Contract cost

Telecommunication

•Repurchase agreements

•Variable consideration

•Time value of money •Contract costs

Real Estate

•Milestone payments

•Variable consideration

•Warranties, •Time value of money

Construction/ Engineering

• Material rights (Gift cards)

• Right of return

Retail

• Combination of contracts

• Milestone payments

Transportation & Logistics

Slide 6

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Key Aspects to consider implementing IFRS 15

Slide 7

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Key Aspects to consider implementing IFRS 15 Overview

• Full retro-perspective

• Partially retro-perspective

• Accounting options

o Contract-by-Contract

o Portfolio Approach

• IT aspects

o Data Sources

o Calculation Engine

o Interface to G/L

• Pilot entity to confirm analysis and probe detailed approach

• Cluster option for entities

• Complexity driven by heterogeneity

• External Reporting

• Management Reporting / Controlling

• Future business models

• Extent and scope internal and external involvement

• Auditor‘s involvement

Organi-sational

Scope Transition

Imple-mentation

Project Setup

Rollout Strategy

Slide 8

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

2016 2017

Effective date = 1 Jan 2017

Option 1 – Full

retrospective (Apply IAS 8)

NEW IFRS 15

NEW IFRS 15

Cumulative effect at 1 Jan 2016

Reliefs

For completed contracts: • No adjustment for interims • Hindsight allowed for variable

consideration

Option 2– Partially

retrospective

OLD GAAP NEW

IFRS 15

Cumulative effect at 1 Jan 2017

No reliefs

Disclose OLD GAAP

It depends.

Transition and implementation Transition timeline

Slide 9

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Exposure Draft Final Standard (28.05.14) Effective date (2017)

Phase I: Assessment

Phase II: Implementation

Phase III: Embedding

• Project plan & governance • As-is analysis • Cross functional impact

assessment • Training & education • Determination of implementation

approach and roadmap

• Data gathering • Accounting and IT concepts • System changes and upgrades • Adoption planning

• Testing • Go live & business as usual • Training • Reporting updates • Disclosure modifications • Stakeholder communication • On-going monitoring

Assess impact and determine strategy

Establish policies and prepare result

Embed the new standard

Implementation methodology and timeline

Have you started now?

Revenue recognition tomorrow

Revenue recognition

today Project management, communication, knowledge transfer &

preparation

Slide 10

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Transition and implementation Implementation challenges and success factors

Challenges

• Technical accounting

application • Increased management

judgement • Project management • Maintaining dual GAAP • Operational process and

system changes • Data gathering & analysis • Communications • Changing business models

Success factors

Start preparing now to figure out how

the standard affects your financial picture, your investors, and the way you do business

Develop an approach that effectively leverages the transition period–measured approach

Establish robust governance structure Agree project management and

change management protocol Document as you go–maintain an

audit trail

Slide 11

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Transition and implementation Portfolio approach may be an option

Generally the contract-by-contract approach shall be applied

In general IFRS 15 specifies the accounting for an individual contract with a

customer.

However, as a practical expedient, an entity may apply this Standard to a portfolio of contracts (or performance obligations)

• with similar characteristics • if the entity reasonably expects that the effects on the financial statements of

applying this Standard to the portfolio would not differ materially from applying this Standard to the individual contracts (or performance obligations) within that portfolio.

Slide 12

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Transition and implementation Contract-by-contract approach vs. portfolio approach

With Contract-by-Contract Approach With Portfolio Approach

iPhone 500 € 5483

S4 450 € 5484

HTC One 400 € 5485

… … …

System 1 Hardware

5484 Tariff1 20 € p.m.

5483 Tariff1 20 € p.m.

5485 Tariff2 40 € p.m.

… … …

System 2 Services

iPhone 500 €

S4 450 €

HTC One 400 €

… …

System 1 Hardware

Tariff1 20 € p.m.

Tariff1 20 € p.m.

Tariff2 40 € p.m.

… …

System 2 Services

Link between different systems necessary to identify performance obligation on a contract by contract basis: • Unique ID over system borders necessary, • Data granularity in different systems must match.

Key Figure Selection Criteria: - sold with service - minimum contract term:

24 month - month: February - new contract

Key Figure Selection Criteria: - sold with hardware - minimum contract term:

24 month - month: February - new contract

𝐻𝑎𝑟𝑑𝑤𝑎𝑟𝑒 15 𝑀𝑖𝑜 € 𝑆𝑒𝑟𝑣𝑖𝑐𝑒 5 𝑀𝑖𝑜 €

≙

Contract 1: iPhone Tariff 1 Hardware 500€ Service: 480€

Contract 2: HTC One Tariff 2 Hardware 400€ Service 960 €

Slide 13

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Imp

lem

en

tio

n c

os

t

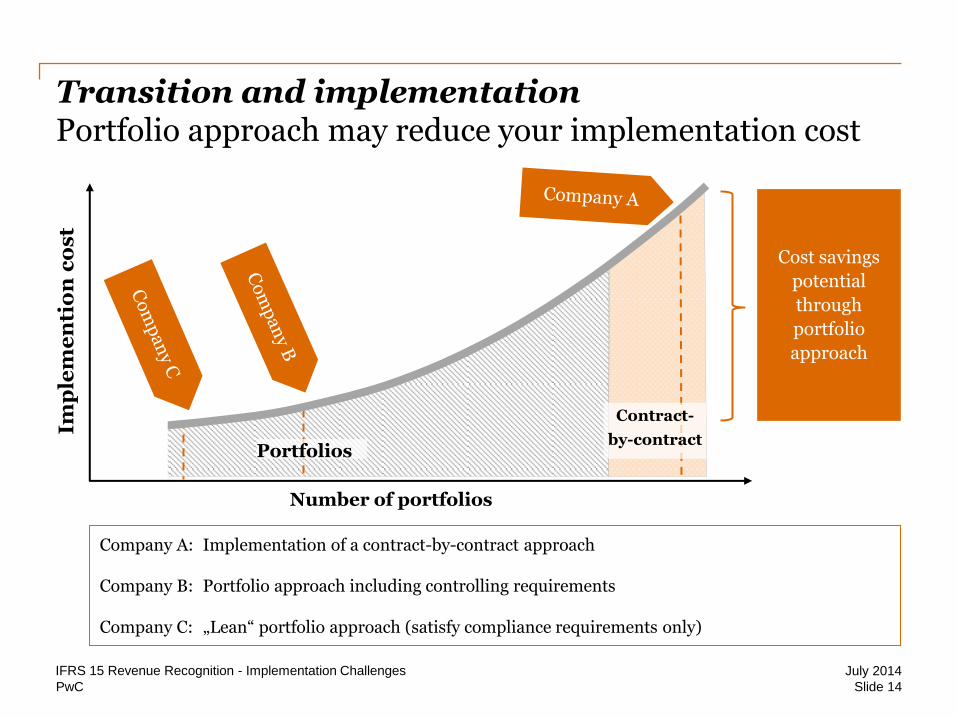

Cost savings

potential

through

portfolio

approach

Company A: Implementation of a contract-by-contract approach

Company B: Portfolio approach including controlling requirements

Company C: „Lean“ portfolio approach (satisfy compliance requirements only)

Portfolios

Contract-

by-contract

Number of portfolios

Transition and implementation Portfolio approach may reduce your implementation cost

Slide 14

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Rollout Strategy Pilot Project and Cluster Option

Cluster 3

Cluster 2

Cluster 1

Pilot Project

Project phases

Clu

ste

rs

January 2015

January 2016

December 2016

Impact Study and Analysis

Preparation & Decision IT Project

IT Realization Planning Phase

September 2014

Slide 15

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Project Setup PwC project approach

Impact study and analysis

Implementation Preparation and decision

• Analysis of processes and systems used

• Analysis of contracts, business models and products

• Definition of technical requirements as well as system requirements

• Identification of interfaces

• Preparation and performance of workshops involving different departments (accounting, controlling, sales, business development, etc.)

• Design of future revenue recognition process

• Identification of data gaps

• Assure accordance with future compliance requirements

• Decision on appropriate software solution

• Adjustment of internal & external reporting

• Consolidation and prioritization of requirements of different departments

• Data collection and migration of current data

• Implementation, customization , testing and Integration of software solution into the existing systems

• Accounting policies & reporting updates

• Roll-out & communication

• Coaching and support during the period of familiarization

Project management, communication and knowledge transfer

Slide 16

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

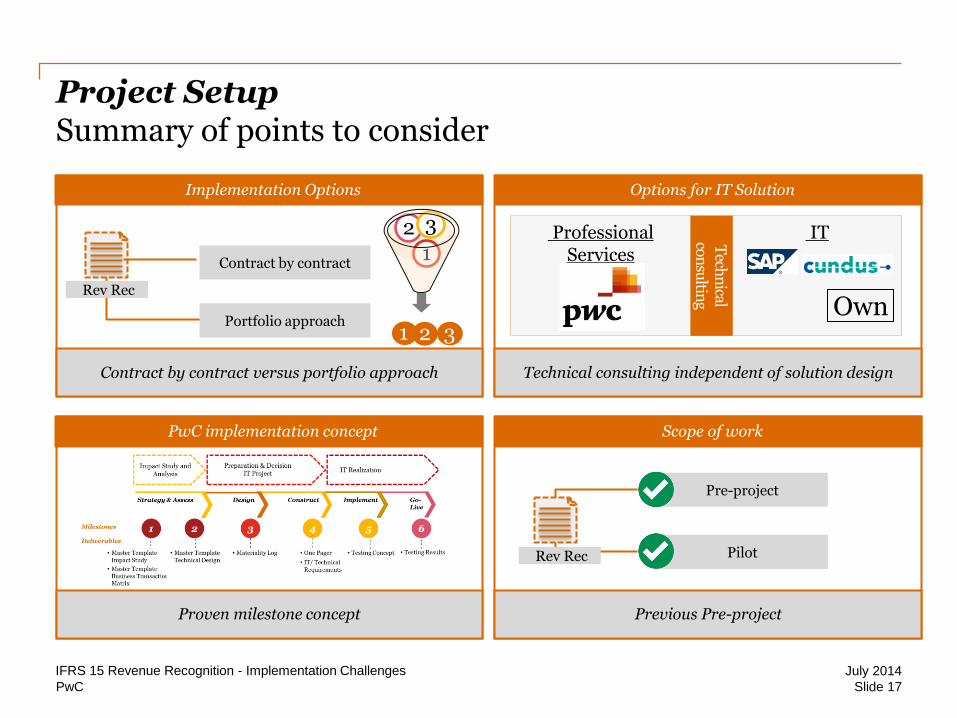

Project Setup Summary of points to consider

Implementation Options

Contract by contract versus portfolio approach

Options for IT Solution

Technical consulting independent of solution design

PwC implementation concept

Proven milestone concept

Scope of work

Previous Pre-project

Professional Services

IT Tech

nical

con

sultin

g

Pre-project

Pilot

Contract by contract

Rev Rec

Rev Rec

1 2 3

1 2 3 Own

Portfolio approach

Slide 17

July 2014 IFRS 15 Revenue Recognition - Implementation Challenges

PwC

Question for voting

IFRS 15, Revenue from Contracts with Customers, will be mandatory for annual periods starting on 1 January 2017. When do you plan to assess the impact of the new standard on your company?

2

1. In 2017

2. In 2016

3. “Today", as we may need to adjust business processes and/or IT systems

Thank you!

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, [insert legal name of the PwC firm], its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

PwC Russia (www.pwc.ru) provides industry-focused assurance, tax, legal and advisory services. Over 2,600 professionals working in PwC offices in Moscow,

St Petersburg, Ekaterinburg, Kazan, Novosibirsk, Rostov-on-Don, Krasnodar, Voronezh, Yuzhno- Sakhalinsk and Vladikavkaz share their thinking, experience

and solutions to develop fresh perspectives and practical advice for our clients. The global network of PwC firms brings together more than 184,000 people in

157 countries.

* PwC refers to PricewaterhouseCoopers Russia B.V. or, as the context requires, other member firms of PricewaterhouseCoopers International Limited, each of

which is a separate legal entity.

© 2014 PricewaterhouseCoopers Russia B.V. All rights reserved.

Recommended