1

IFRS for Hospitality and Gaming Industry(Part 1) 25 May 2010

copy 2006-10 Nelson Consulting Limited 1

Nelson LamNelson Lam 林智遠林智遠MBA MSc BBA ACA ACIS CFA CPA(Aust) CPA(US) FCCA FCPA FHKIoD MSCA

Property Plant and Equipment (IAS 16)

Workshop Agenda

P t 1

Updated Practices

Cases amp ExamplesLeases (IAS 17)

I t ibl A t

Revenue(IAS 18)

Part 1This

Evening

Cases amp Examples from Hospitality amp Gaming Industry

copy 2006-10 Nelson Consulting Limited 2

Intangible Assets(IAS 38)

Investment Property (IAS 40)

Part 2Tomorrow

2

Presentation of Financial Statements(IAS 1 Revised in 2007)

copy 2006-10 Nelson Consulting Limited 3

Complete Set of Fin Statements

bull A complete set of financial statements comprisesa) a statement of financial position as at the end of the

period

Previously we call it ldquoBalance Sheetrdquoperiod

b) a statement of comprehensive income for the periodc) a statement of changes in equity for the periodd) a statement of cash flows for the periode) notes comprising a summary of significant accounting

policies and other explanatory information andf) a statement of financial position as at the beginning of

the earliest comparative period

Previously we call it ldquoIncome Statementrdquo

3 yearsrsquo ldquobalance sheetsrdquo

copy 2006-10 Nelson Consulting Limited 4

the earliest comparative periodbull when an entity applies an accounting policy

retrospectively or makes a retrospective restatement of items in its financial statements or

bull when it reclassifies items in its financial statementsbull An entity may use titles for the statements other than

those used in HKAS 1

3

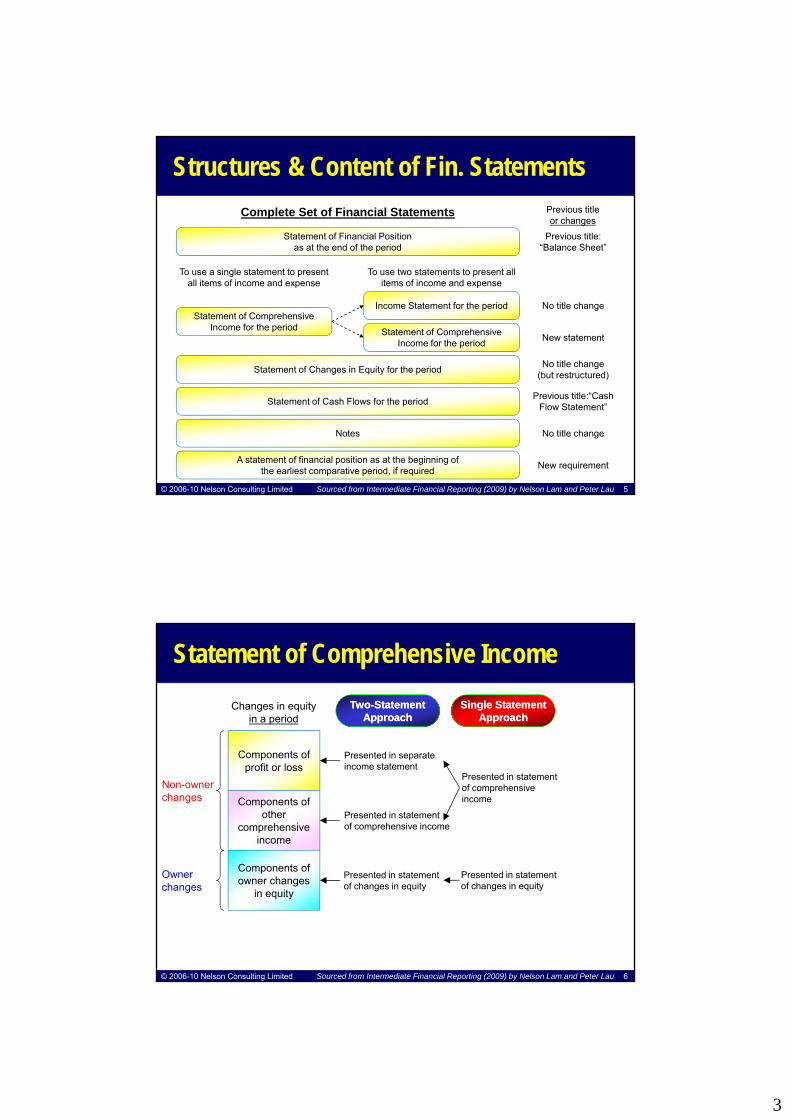

Structures amp Content of Fin Statements

Statement of Financial Position as at the end of the period

Complete Set of Financial Statements Previous titleor changes

Previous title ldquoBalance Sheetrdquo

To use a single statement to present all items of income and expense

Statement of Comprehensive Income for the period

Statement of Changes in Equity for the period

No title change

No title change(but restructured)

New statement

To use two statements to present all items of income and expense

Statement of Comprehensive Income for the period

Income Statement for the period

copy 2006-10 Nelson Consulting Limited 5

Statement of Cash Flows for the period

Notes

A statement of financial position as at the beginning of the earliest comparative period if required

Previous titleldquoCash Flow Statementrdquo

(but restructured)

No title change

New requirement

Sourced from Intermediate Financial Reporting (2009) by Nelson Lam and Peter Lau

Statement of Comprehensive IncomeChanges in equity

in a periodSingle Statement Single Statement

ApproachApproachTwoTwo--Statement Statement

ApproachApproach

Components of profit or loss

Components of other

comprehensive income

Non-owner changes

Presented in separateincome statement

Presented in statementof comprehensive income

Presented in statementof comprehensive income

copy 2006-10 Nelson Consulting Limited 6

Components of owner changes

in equity

Owner changes

Presented in statementof changes in equity

Presented in statementof changes in equity

Sourced from Intermediate Financial Reporting (2009) by Nelson Lam and Peter Lau

4

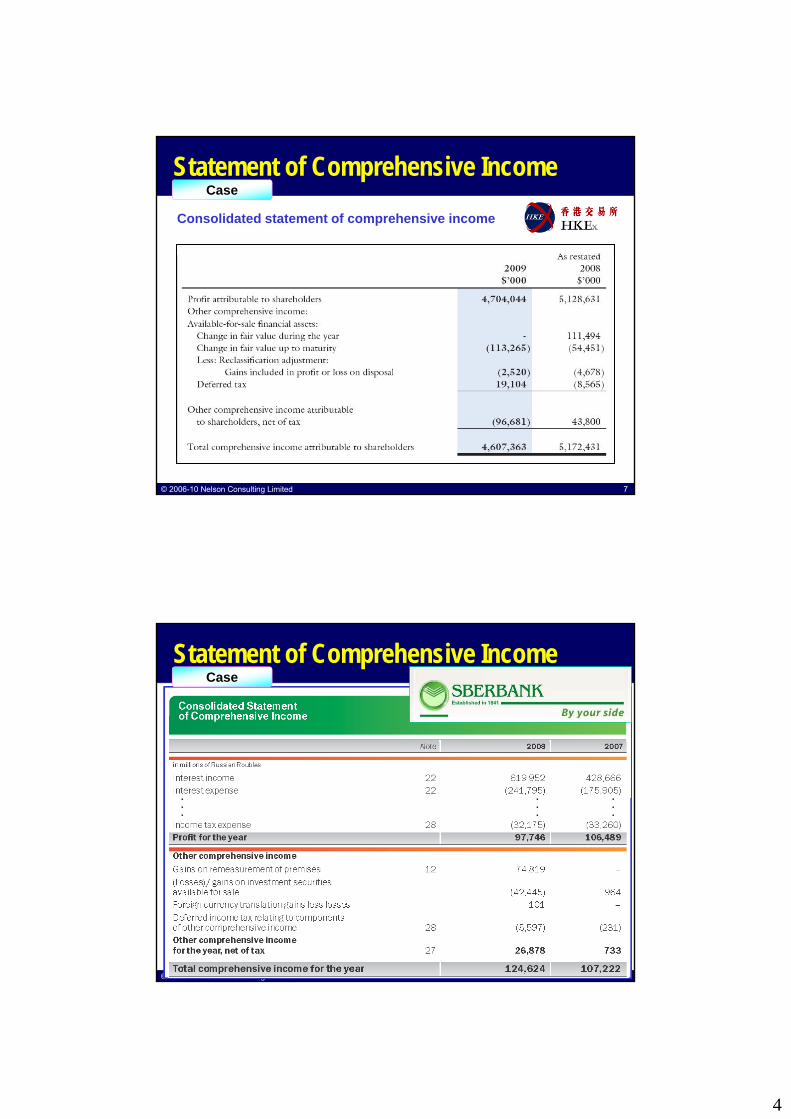

Statement of Comprehensive IncomeCase

Consolidated statement of comprehensive income

copy 2006-10 Nelson Consulting Limited 7

Statement of Comprehensive IncomeCase

copy 2006-10 Nelson Consulting Limited 8

5

Property Plant and Equipment (IAS 16)

copy 2006-10 Nelson Consulting Limited 9

1 Objective and Scope

bull The principal issues in accounting for property plant and equipment (PPE) area) the recognition of the assets Definitionsa) the recognition of the assetsb) the determination of their carrying amounts andc) the depreciation charges and impairment losses

to be recognised in relation to themMeasurement

Recognition

copy 2006-10 Nelson Consulting Limited 10

6

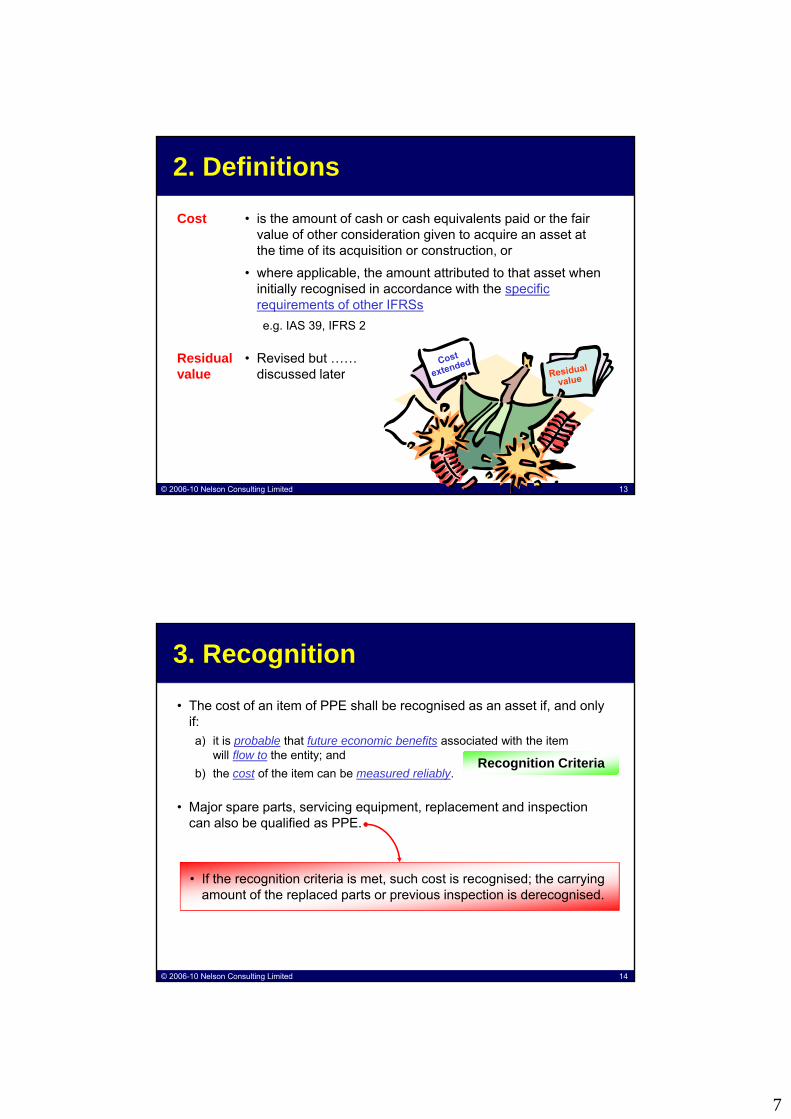

bull Building acquired under an

1 Objective and Scope

What are PPE Are the following PPEWhat are PPE Are the following PPE

Example

IAS 17timesoperating lease

bull Building acquired under finance leases

bull Freehold property used for rental purpose

bull Investment property underre-development

IAS 17

radic

times

times

IAS 40

IAS 40

copy 2006-10 Nelson Consulting Limited 11

pbull Property held for a currently

undetermined future usebull Leasehold land separated

from the leasehold building

times

times

IAS 40

IAS 17

2 Definitions

bull Property plant and equipment (PPE) are tangible items thata) are held for use

ndash in the production or supply of goods or servicesin the production or supply of goods or services ndash for rental to others or ndash for administrative purposes and

b) are expected to be used during more than one period

copy 2006-10 Nelson Consulting Limited 12

7

2 Definitions

Cost bull is the amount of cash or cash equivalents paid or the fair value of other consideration given to acquire an asset at the time of its acquisition or construction orq

bull where applicable the amount attributed to that asset when initially recognised in accordance with the specific requirements of other IFRSseg IAS 39 IFRS 2

Residual value

bull Revised but helliphellip discussed later

copy 2006-10 Nelson Consulting Limited 13

value discussed later

3 Recognition

bull The cost of an item of PPE shall be recognised as an asset if and only ifa) it is probable that future economic benefits associated with the itema) it is probable that future economic benefits associated with the item

will flow to the entity andb) the cost of the item can be measured reliably

bull Major spare parts servicing equipment replacement and inspection can also be qualified as PPE

Recognition CriteriaRecognition Criteria

copy 2006-10 Nelson Consulting Limited 14

bull If the recognition criteria is met such cost is recognised the carrying amount of the replaced parts or previous inspection is derecognised

8

3 RecognitionCase

Wynn Macau Limited(N t t Fi i l St t t 2009)

bull Expenditures incurred after items of property and equipment have been brought into use such as repairs and maintenance are normally charged to the statement of comprehensive income in the period in which they are incurred

bull In situationsndash where it can be clearly demonstrated an expenditure has resulted in

(Notes to Financial Statements 2009)

copy 2006-10 Nelson Consulting Limited 15

ndash where it can be clearly demonstrated an expenditure has resulted in an increase in the future economic benefits expected to be obtained from the use of an item of property and equipment and

ndash where the cost of the item can be measured reliably the expenditure is capitalized as an additional cost of that asset or as a replacement

3 Recognition

Galaxy Entertainment Group Limited(2009 Annual Report)

Case

( p )ndash Subsequent costs are included in the carrying

amount of the asset or recognised as a separate asset as appropriate only when bull it is probable that future economic benefits associated

with the item will flow to the Group andbull the cost of the item can be measured reliably

ndash All other repairs and maintenance costs are

copy 2006-10 Nelson Consulting Limited 16

All other repairs and maintenance costs are expensed in the income statement during the financial period in which they are incurred

9

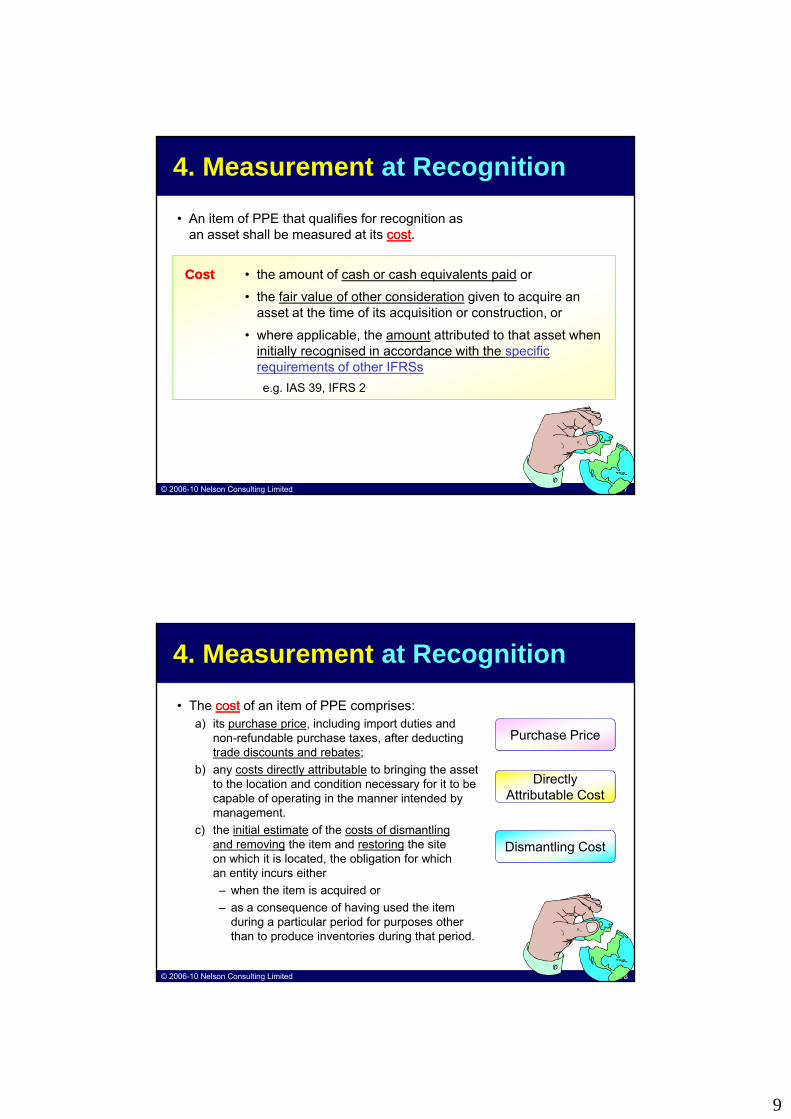

4 Measurement at Recognition

bull An item of PPE that qualifies for recognition as an asset shall be measured at its costcost

CostCost bull the amount of cash or cash equivalents paid or

bull the fair value of other consideration given to acquire an asset at the time of its acquisition or construction or

bull where applicable the amount attributed to that asset when initially recognised in accordance with the specific requirements of other IFRSs

copy 2006-10 Nelson Consulting Limited 17

eg IAS 39 IFRS 2

4 Measurement at Recognition

bull The costcost of an item of PPE comprisesa) its purchase price including import duties and

non-refundable purchase taxes after deducting Purchase Pricep gtrade discounts and rebates

b) any costs directly attributable to bringing the asset to the location and condition necessary for it to be capable of operating in the manner intended by management

c) the initial estimate of the costs of dismantlingand removing the item and restoring the siteon which it is located the obligation for which

Directly Attributable Cost

Dismantling Cost

copy 2006-10 Nelson Consulting Limited 18

on which it is located the obligation for whichan entity incurs eitherndash when the item is acquired orndash as a consequence of having used the item

during a particular period for purposes other than to produce inventories during that period

10

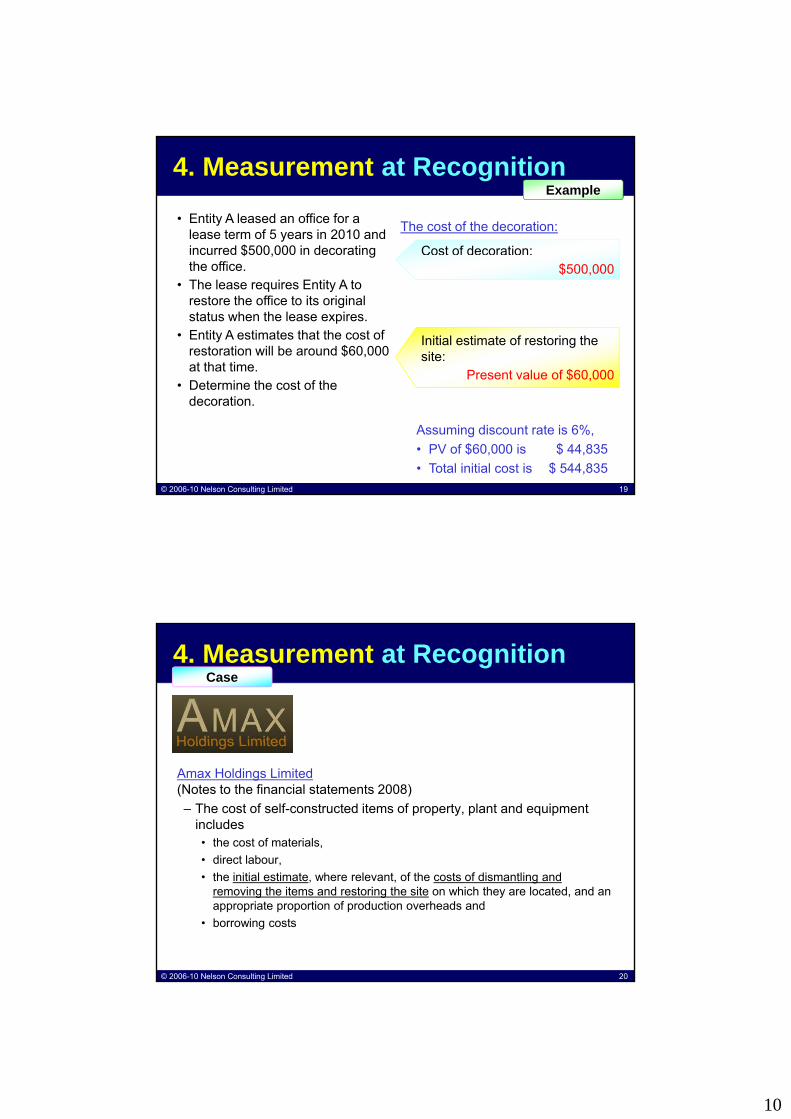

4 Measurement at Recognition

bull Entity A leased an office for a lease term of 5 years in 2010 and incurred $500000 in decorating

The cost of the decoration

Example

Cost of decoration $ gthe office

bull The lease requires Entity A to restore the office to its original status when the lease expires

bull Entity A estimates that the cost of restoration will be around $60000 at that time

$500000

Initial estimate of restoring the site

Present value of $60 000

copy 2006-10 Nelson Consulting Limited 19

bull Determine the cost of the decoration

Present value of $60000

Assuming discount rate is 6bull PV of $60000 is $ 44835bull Total initial cost is $ 544835

4 Measurement at RecognitionCase

Amax Holdings Limited(Notes to the financial statements 2008)ndash The cost of self-constructed items of property plant and equipment

includes bull the cost of materials bull direct labour

copy 2006-10 Nelson Consulting Limited 20

direct labour bull the initial estimate where relevant of the costs of dismantling and

removing the items and restoring the site on which they are located and an appropriate proportion of production overheads and

bull borrowing costs

11

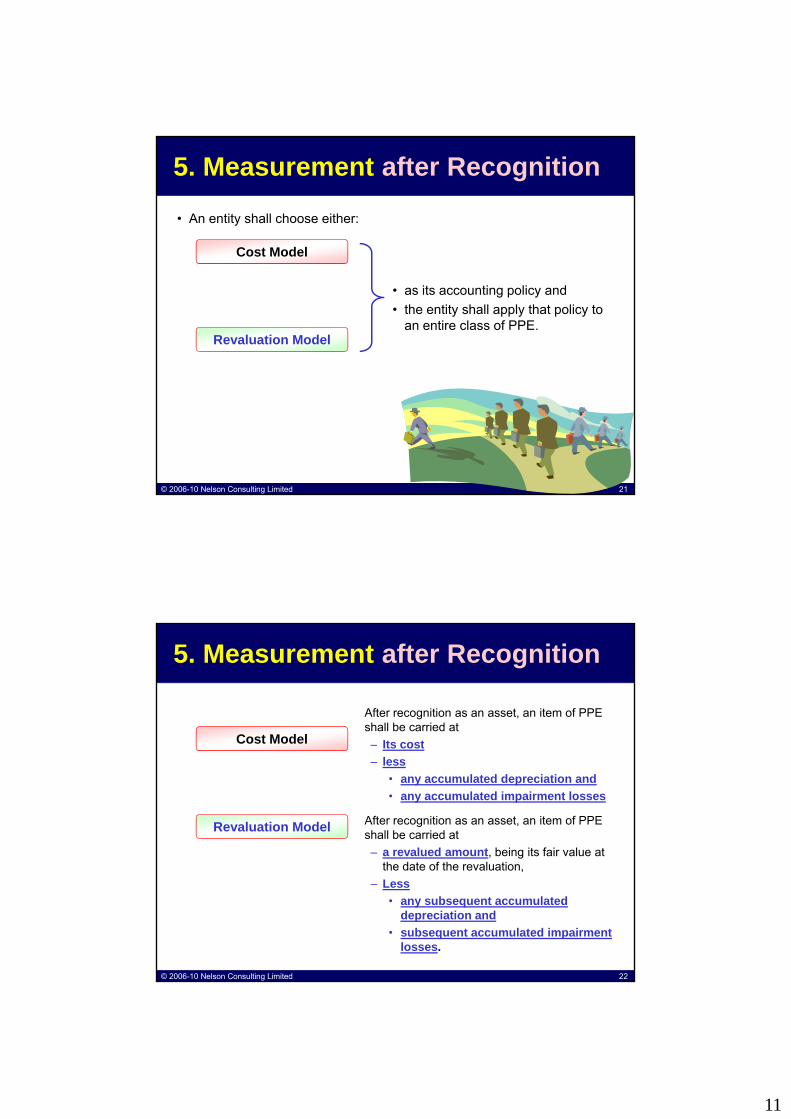

5 Measurement after Recognition

bull An entity shall choose either

Cost ModelCost Model

Revaluation Model

bull as its accounting policy andbull the entity shall apply that policy to

an entire class of PPE

copy 2006-10 Nelson Consulting Limited 21

5 Measurement after Recognition

Cost Model

After recognition as an asset an item of PPE shall be carried at

Its costCost Model

Revaluation Model

ndash Its costndash less

bull any accumulated depreciation and bull any accumulated impairment losses

After recognition as an asset an item of PPE shall be carried atndash a revalued amount being its fair value at

th d t f th l ti

copy 2006-10 Nelson Consulting Limited 22

the date of the revaluation ndash Less

bull any subsequent accumulated depreciation and

bull subsequent accumulated impairment losses

12

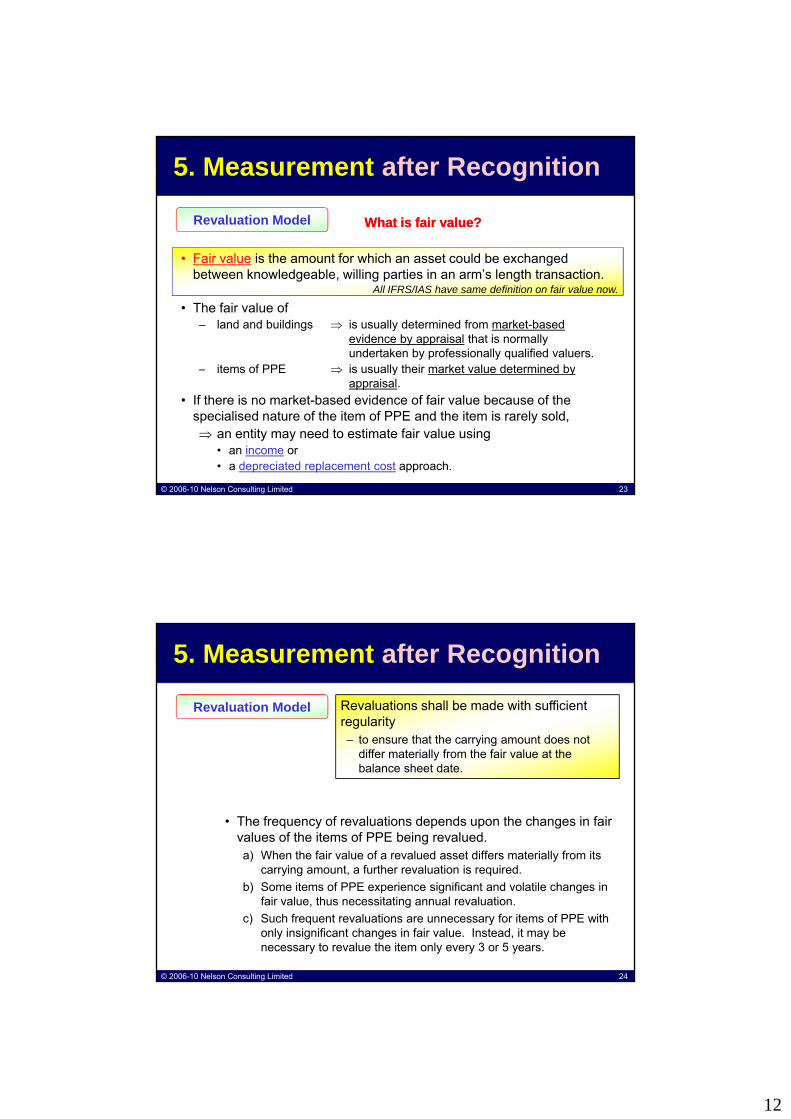

5 Measurement after Recognition

Revaluation Model

F i l i th t f hi h t ld b h d

What is fair valueWhat is fair value

All IFRSIAS have same definition on fair value now

bull Fair value is the amount for which an asset could be exchanged between knowledgeable willing parties in an armrsquos length transaction

bull The fair value ofndash land and buildings rArr is usually determined from market-based

evidence by appraisal that is normally undertaken by professionally qualified valuers

ndash items of PPE rArr is usually their market value determined by

copy 2006-10 Nelson Consulting Limited 23

y yappraisal

bull If there is no market-based evidence of fair value because of the specialised nature of the item of PPE and the item is rarely sold rArr an entity may need to estimate fair value using

bull an income orbull a depreciated replacement cost approach

5 Measurement after Recognition

Revaluation Model Revaluations shall be made with sufficient regularityndash to ensure that the carrying amount does not

bull The frequency of revaluations depends upon the changes in fair values of the items of PPE being revalueda) When the fair value of a revalued asset differs materially from its

to ensure that the carrying amount does not differ materially from the fair value at the balance sheet date

copy 2006-10 Nelson Consulting Limited 24

carrying amount a further revaluation is requiredb) Some items of PPE experience significant and volatile changes in

fair value thus necessitating annual revaluationc) Such frequent revaluations are unnecessary for items of PPE with

only insignificant changes in fair value Instead it may be necessary to revalue the item only every 3 or 5 years

13

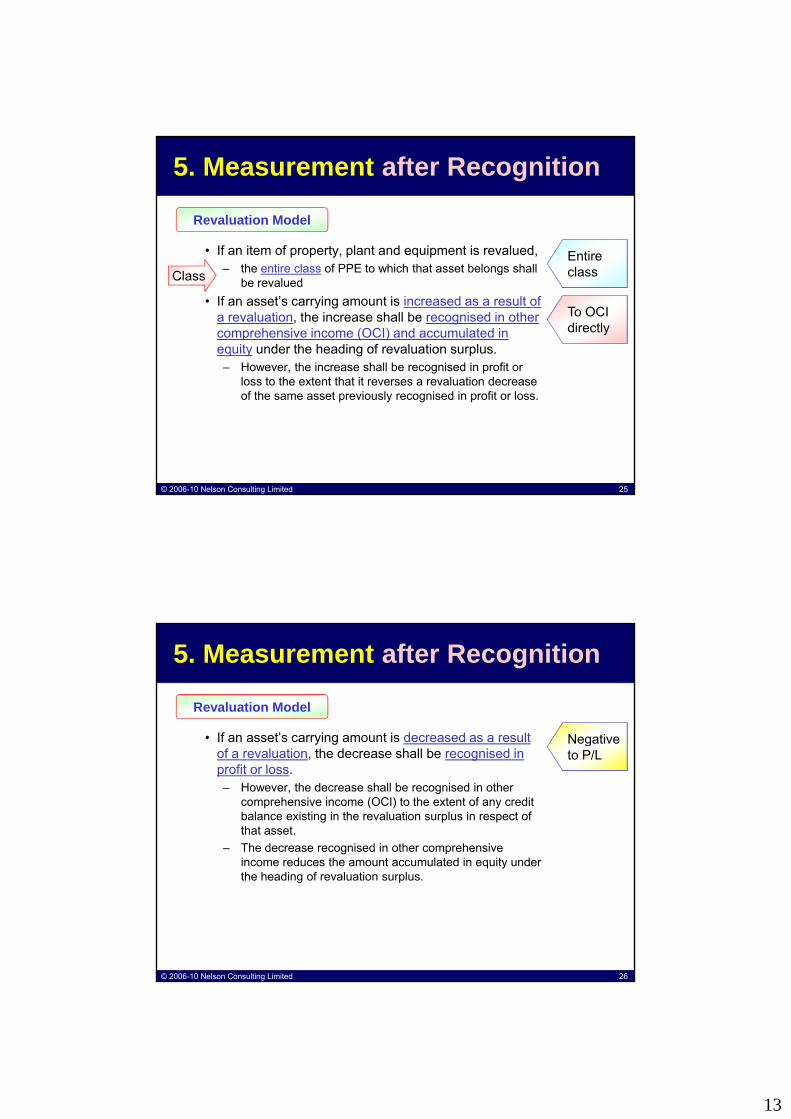

5 Measurement after Recognition

Revaluation Model

bull If an item of property plant and equipment is revalued Entirep p y p q p ndash the entire class of PPE to which that asset belongs shall

be revaluedbull If an assetrsquos carrying amount is increased as a result of

a revaluation the increase shall be recognised in other comprehensive income (OCI) and accumulated in equity under the heading of revaluation surplusndash However the increase shall be recognised in profit or

ClassEntire class

To OCI directly

copy 2006-10 Nelson Consulting Limited 25

loss to the extent that it reverses a revaluation decrease of the same asset previously recognised in profit or loss

5 Measurement after Recognition

Revaluation Model

bull If an assetrsquos carrying amount is decreased as a result Negativey gof a revaluation the decrease shall be recognised in profit or lossndash However the decrease shall be recognised in other

comprehensive income (OCI) to the extent of any credit balance existing in the revaluation surplus in respect of that asset

ndash The decrease recognised in other comprehensive income reduces the amount accumulated in equity under

Negative to PL

copy 2006-10 Nelson Consulting Limited 26

income reduces the amount accumulated in equity under the heading of revaluation surplus

14

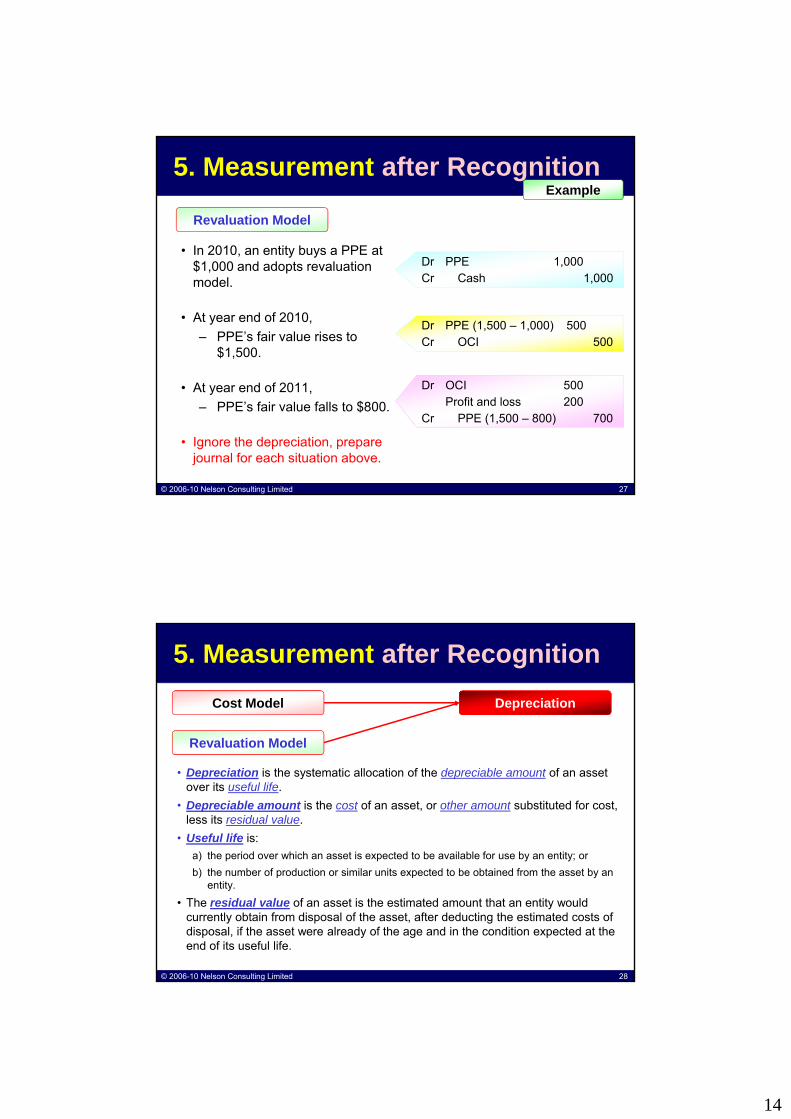

5 Measurement after Recognition

bull In 2010 an entity buys a PPE at

Example

Revaluation Model

y y$1000 and adopts revaluation model

bull At year end of 2010ndash PPErsquos fair value rises to

$1500

Dr PPE 1000Cr Cash 1000

Dr PPE (1500 ndash 1000) 500Cr OCI 500

copy 2006-10 Nelson Consulting Limited 27

bull At year end of 2011ndash PPErsquos fair value falls to $800

bull Ignore the depreciation prepare journal for each situation above

Dr OCI 500Profit and loss 200

Cr PPE (1500 ndash 800) 700

5 Measurement after RecognitionDepreciationCost Model

Revaluation Model

bull Depreciation is the systematic allocation of the depreciable amount of an asset over its useful life

bull Depreciable amount is the cost of an asset or other amount substituted for cost less its residual value

bull Useful life isa) the period over which an asset is expected to be available for use by an entity or

Revaluation Model

copy 2006-10 Nelson Consulting Limited 28

b) the number of production or similar units expected to be obtained from the asset by an entity

bull The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset after deducting the estimated costs of disposal if the asset were already of the age and in the condition expected at the end of its useful life

15

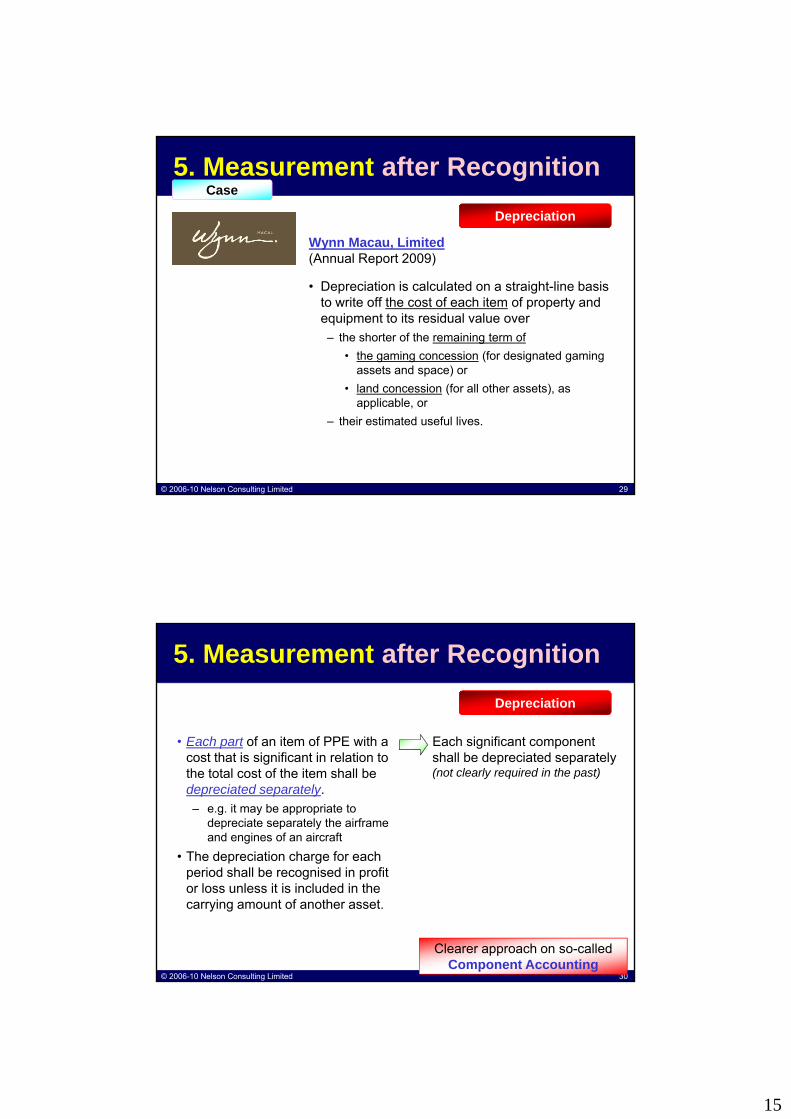

5 Measurement after RecognitionCase

Wynn Macau Limited(A l R t 2009)

Depreciation

bull Depreciation is calculated on a straight-line basis to write off the cost of each item of property and equipment to its residual value over ndash the shorter of the remaining term of

bull the gaming concession (for designated gaming assets and space) or

(Annual Report 2009)

copy 2006-10 Nelson Consulting Limited 29

p )bull land concession (for all other assets) as

applicable or ndash their estimated useful lives

5 Measurement after Recognition

bull Each part of an item of PPE with a

Depreciation

Each significant componentbull Each part of an item of PPE with a cost that is significant in relation to the total cost of the item shall be depreciated separatelyndash eg it may be appropriate to

depreciate separately the airframe and engines of an aircraft

bull The depreciation charge for each

Each significant component shall be depreciated separately (not clearly required in the past)

copy 2006-10 Nelson Consulting Limited 30

p gperiod shall be recognised in profit or loss unless it is included in the carrying amount of another asset

Clearer approach on so-calledComponent Accounting

16

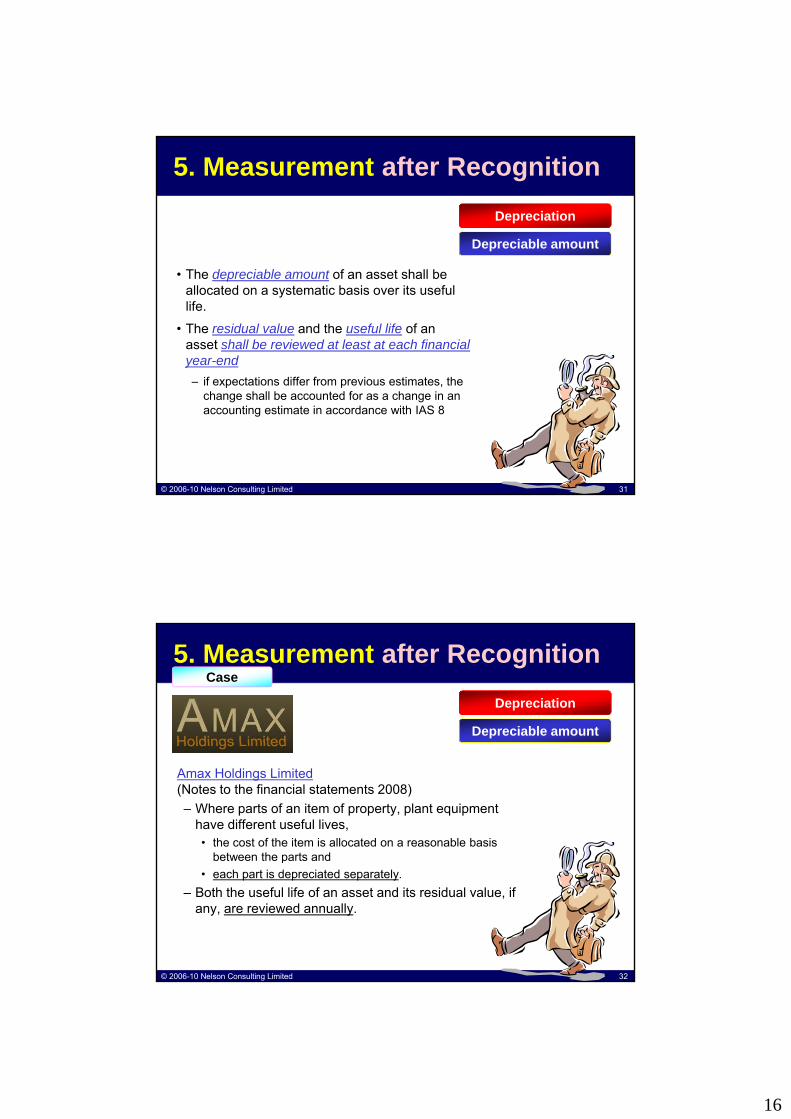

5 Measurement after RecognitionDepreciation

Depreciable amount

bull The depreciable amount of an asset shall be allocated on a systematic basis over its useful life

bull The residual value and the useful life of an asset shall be reviewed at least at each financial year-end

copy 2006-10 Nelson Consulting Limited 31

ndash if expectations differ from previous estimates the change shall be accounted for as a change in an accounting estimate in accordance with IAS 8

5 Measurement after RecognitionCase

Depreciation

Depreciable amount

Amax Holdings Limited(Notes to the financial statements 2008)ndash Where parts of an item of property plant equipment

have different useful livesbull the cost of the item is allocated on a reasonable basis

between the parts and

copy 2006-10 Nelson Consulting Limited 32

pbull each part is depreciated separately

ndash Both the useful life of an asset and its residual value if any are reviewed annually

17

5 Measurement after RecognitionDepreciation

Depreciable amountResidual Value

bull Residual Value is updated as

the estimated amount that an entity would currently obtain from disposal of the asset after deducting the estimated costs of disposal if the assetndash were already of the age andndash in the condition expected at the end

copy 2006-10 Nelson Consulting Limited 33

in the condition expected at the end of its useful life

Inflation may be incorporated in residual value

5 Measurement after Recognition

bull Depreciation of an asset begins when it i il bl f

Depreciation

Depreciable amountis available for usendash ie when it is in the location and condition

necessary for it to be capable of operating in the manner intended by management

bull Depreciation of an asset ceases at the earlier of the date thatndash the asset is classified as held for sale (or

included in a disposal group that is classified as held for sale) in accordance

Implied that depreciation still required even PPEndash becomes idle or

is retired from active use

copy 2006-10 Nelson Consulting Limited 34

classified as held for sale) in accordance with IFRS 5 and

ndash the date that the asset is derecognisedbull Land and buildings are separable assets

and are accounted for separately even when they are acquired together

ndash is retired from active use

18

5 Measurement after Recognition

bull The depreciation method usedndash shall reflect the pattern in which the

assetrsquos future economic benefits are

Depreciation

Depreciable amountasset s future economic benefits are expected to be consumed by the entity

ndash shall be reviewed at least at each financial year-end and

ndash such a change shall be accounted for as a change in an accounting estimate in accordance with IAS 8

bull Other than the above that method is

Depreciation method

copy 2006-10 Nelson Consulting Limited 35

Other than the above that method is applied consistently from period to periodbull unless there is a change in the expected

pattern of consumption of those future economic benefits

5 Measurement after Recognition

bull To determine whether an item of PPE is impaired an entity applies IAS 36

bull Compensation from third parties for items of

Depreciation

Depreciable amountbull Compensation from third parties for items of

property plant and equipment that were impaired lost or given up shall be included in profit or loss when the compensation becomes receivable

Depreciation method

Impairment

copy 2006-10 Nelson Consulting Limited 36

19

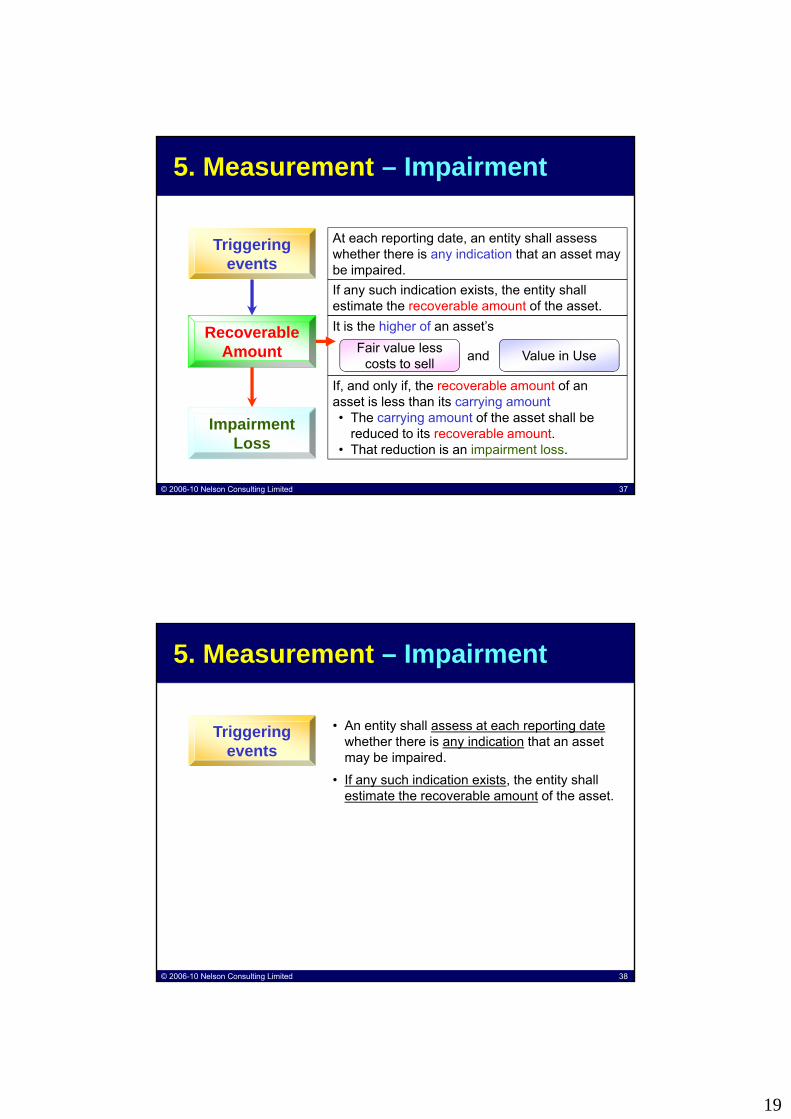

5 Measurement ndash Impairment

Triggering At each reporting date an entity shall assess whether there is any indication that an asset may

It is the higher of an assetrsquos

events

Recoverable Amount

whether there is any indication that an asset may be impairedIf any such indication exists the entity shall estimate the recoverable amount of the asset

andFair value less costs to sell Value in Use

copy 2006-10 Nelson Consulting Limited 37

Impairment Loss

If and only if the recoverable amount of an asset is less than its carrying amountbull The carrying amount of the asset shall be

reduced to its recoverable amountbull That reduction is an impairment loss

bull An entity shall assess at each reporting datewhether there is any indication that an asset

Triggering

5 Measurement ndash Impairment

whether there is any indication that an asset may be impaired

bull If any such indication exists the entity shall estimate the recoverable amount of the asset

events

copy 2006-10 Nelson Consulting Limited 38

20

6 Derecognition

bull The carrying amount of an item of PPE shall be derecogniseda) on disposal ora) on disposal orb) when no future economic benefits are

expected from its use or disposalbull The gain or loss arising from the

derecognition of an item of PPE shall be included in profit or loss when the item is derecognised (unless IAS 17 requires otherwise on a sale and leaseback)

copy 2006-10 Nelson Consulting Limited 39

otherwise on a sale and leaseback)bull Gains shall not be classified as revenue Amended by Annual

Improvement Project 2008

6 Derecognition

IAS 16 Property Plant and Equipmentbull Gain (on derecognition of PPE) shall not be classified as

revenue (IAS 16 68)revenue (IAS 1668)bull Amendment introduces IAS 1668A that

ndash However an entity that in the course of its ordinary activities routinely sells items of PPE that it has held for rental to othersbull shall transfer such assets to inventories at their carrying

amount when they cease to be rented and become held for sale

ndash The proceeds from the sale of such assets shall be recognised as

copy 2006-10 Nelson Consulting Limited 40

p grevenue in accordance with IAS 18 Revenue

ndash IFRS 5 does not apply when assets that are held for sale in the ordinary course of business are transferred to inventories

In some industries entities are in the business of renting and subsequently selling the same assets for example car rental company

21

6 Derecognition

bull Derecognition on disposalndash The disposal of an item of PPE may occur in a variety of

ways (eg by sale by entering into a finance lease or byways (eg by sale by entering into a finance lease or by donation)

ndash In determining the date of disposal of an item an entity applies the criteria in IAS 18 Revenue for recognising revenue from the sale of goods

ndash IAS 17 Leases applies to disposal by a sale and leaseback

copy 2006-10 Nelson Consulting Limited 41

6 DerecognitionCase

Melco Development Limited (新濠國際發展有限公司)Accounting policies for year ended 31122009ndash An item of property plant and equipment is derecognised

bull upon disposal or bull when no future economic benefits are expected to arise from the continued

use of the asset ndash Any gain or loss arising on derecognition of the asset

copy 2006-10 Nelson Consulting Limited 42

Any gain or loss arising on derecognition of the asset bull (calculated as the difference between

ndash the net disposal proceeds and ndash the carrying amount of the asset)

is included in profit or loss in the period in which the asset is derecognised

22

6 Derecognition

bull Derecognition on replacementndash If under the initial recognition principle

bull an entity recognises in the carrying amount of an item of PPE the costbull an entity recognises in the carrying amount of an item of PPE the cost of a replacement for part of the item

bull then it derecognises the carrying amount of the replaced partregardless of whether the replaced part had been depreciated separately

bull The gain or loss arising from the derecognition of an item of PPE shall be determined as the difference between

copy 2006-10 Nelson Consulting Limited 43

ndash the net disposal proceeds if any andndash the carrying amount of the item

Leases (IAS 17)

copy 2006-10 Nelson Consulting Limited 44

23

1 Objective and Scope

bull The objective of IAS 17 Leases

ndash is to prescribe for lessees and lessors the appropriate accounting policies and disclosure to apply in relation to leasespolicies and disclosure to apply in relation to leases

bull A lease

ndash is an agreement whereby the lessor conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period of time

copy 2006-10 Nelson Consulting Limited 45

1 Objective and Scope

bull IAS 17 shall be applied in accounting for all leases other than a) leases to explore for or use minerals oil natural gas and similar

non-regenerative resources andnon regenerative resources andb) licensing agreements for such items as motion picture films video

recordings plays manuscripts patents and copyrights

bull IAS 17 shall not be applied as the basis of measurement fora) property held by lessees that is accounted

for as investment property (see IAS 40)b) investment property provided by lessors

copy 2006-10 Nelson Consulting Limited 46

b) investment property provided by lessorsunder operating leases (see IAS 40)

c) biological assets held by lessees underfinance leases (see IAS 41) or

d) biological assets provided by lessorsunder operating leases (see IAS 41)

24

2 Classification of Leases

The classification of leases adopted in IAS 17 Is based on the extent to which risks and rewards incidental to ownership of a leased asset lie the the lessor or the leseee

Risks and Rewards

FinanceLease

bull A finance leasendash is a lease that transfers substantially all the risks

and rewards incidental to ownership of an asset

ownership of a leased asset lie the the lessor or the leseee

copy 2006-10 Nelson Consulting Limited 47

Operating Lease

pndash Title may or may not eventually be transferred

bull An operating leasendash is a lease other than a finance lease

2 Classification of Leases

Galaxy Entertainment Group Limited(2009 Annual Report)

Case

( p )ndash Leases that substantially transfer to the Group all

the risks and rewards of ownership of assets are accounted for as finance leases hellip

ndash Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases

copy 2006-10 Nelson Consulting Limited 48

25

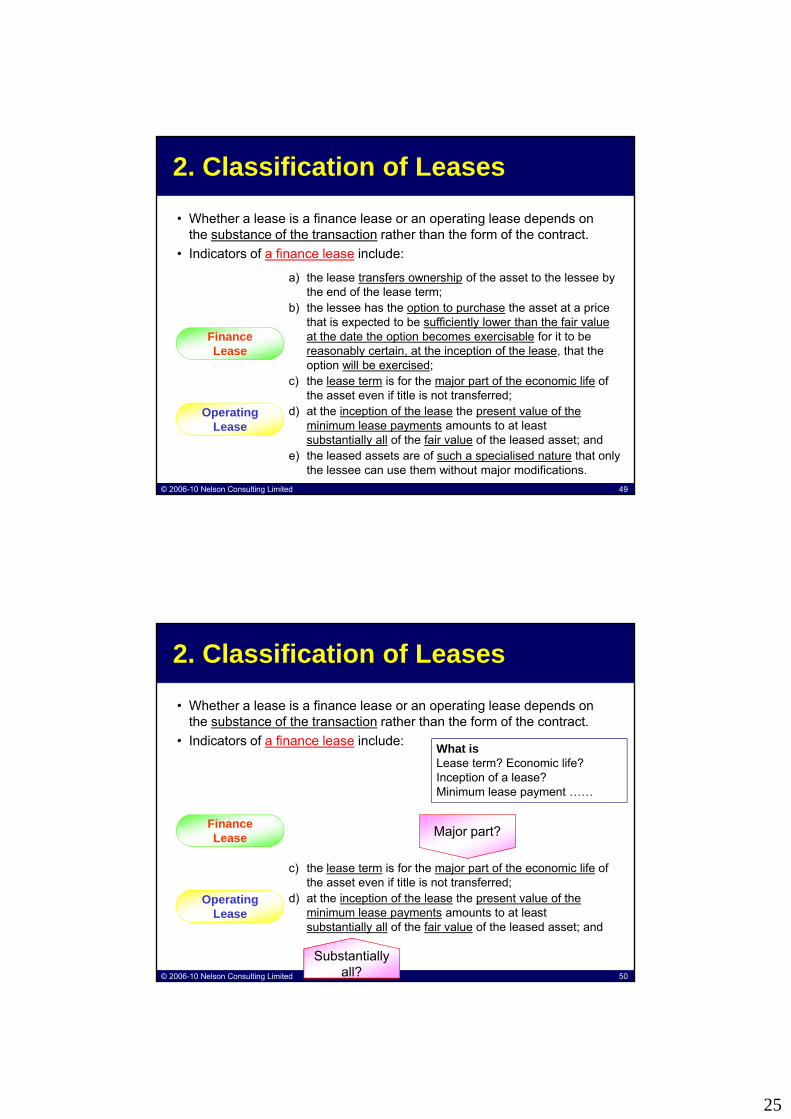

2 Classification of Leases

bull Whether a lease is a finance lease or an operating lease depends on the substance of the transaction rather than the form of the contract

bull Indicators of a finance lease includeIndicators of a finance lease include

FinanceLease

a) the lease transfers ownership of the asset to the lessee by the end of the lease term

b) the lessee has the option to purchase the asset at a price that is expected to be sufficiently lower than the fair value at the date the option becomes exercisable for it to be reasonably certain at the inception of the lease that the option will be exercised

copy 2006-10 Nelson Consulting Limited 49

Operating Lease

c) the lease term is for the major part of the economic life of the asset even if title is not transferred

d) at the inception of the lease the present value of the minimum lease payments amounts to at leastsubstantially all of the fair value of the leased asset and

e) the leased assets are of such a specialised nature that only the lessee can use them without major modifications

2 Classification of Leases

bull Whether a lease is a finance lease or an operating lease depends on the substance of the transaction rather than the form of the contract

bull Indicators of a finance lease includeIndicators of a finance lease include

FinanceLease Major part

What isLease term Economic lifeInception of a leaseMinimum lease payment helliphellip

copy 2006-10 Nelson Consulting Limited 50

Operating Lease

c) the lease term is for the major part of the economic life of the asset even if title is not transferred

d) at the inception of the lease the present value of the minimum lease payments amounts to at least substantially all of the fair value of the leased asset and

Substantially all

26

2 Classification of Leases

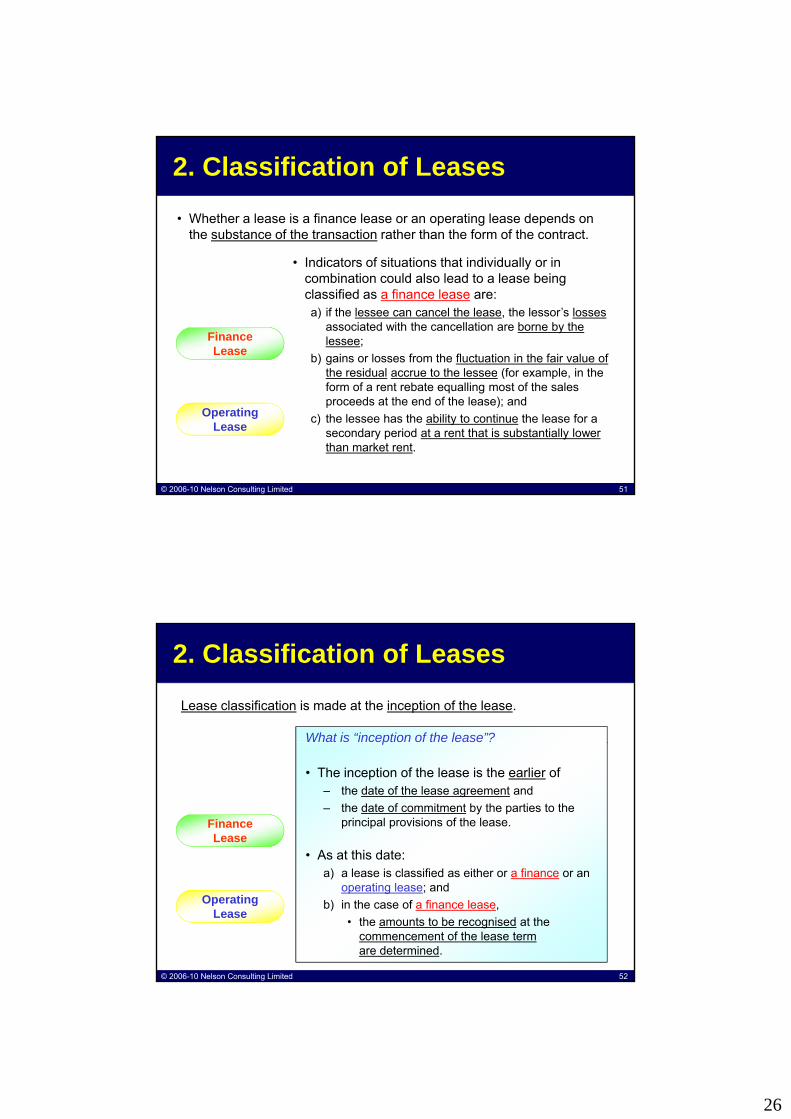

bull Whether a lease is a finance lease or an operating lease depends on the substance of the transaction rather than the form of the contract

FinanceLease

bull Indicators of situations that individually or in combination could also lead to a lease being classified as a finance lease area) if the lessee can cancel the lease the lessorrsquos losses

associated with the cancellation are borne by the lessee

b) gains or losses from the fluctuation in the fair value of the residual accrue to the lessee (for example in the

copy 2006-10 Nelson Consulting Limited 51

Operating Lease

the residual accrue to the lessee (for example in the form of a rent rebate equalling most of the sales proceeds at the end of the lease) and

c) the lessee has the ability to continue the lease for a secondary period at a rent that is substantially lower than market rent

2 Classification of Leases

Lease classification is made at the inception of the lease

What is ldquoinception of the leaserdquo

FinanceLease

p

bull The inception of the lease is the earlier ofndash the date of the lease agreement andndash the date of commitment by the parties to the

principal provisions of the lease

bull As at this date

copy 2006-10 Nelson Consulting Limited 52

Operating Lease

a) a lease is classified as either or a finance or an operating lease and

b) in the case of a finance leasebull the amounts to be recognised at the

commencement of the lease termare determined

27

2 Classification of Leases

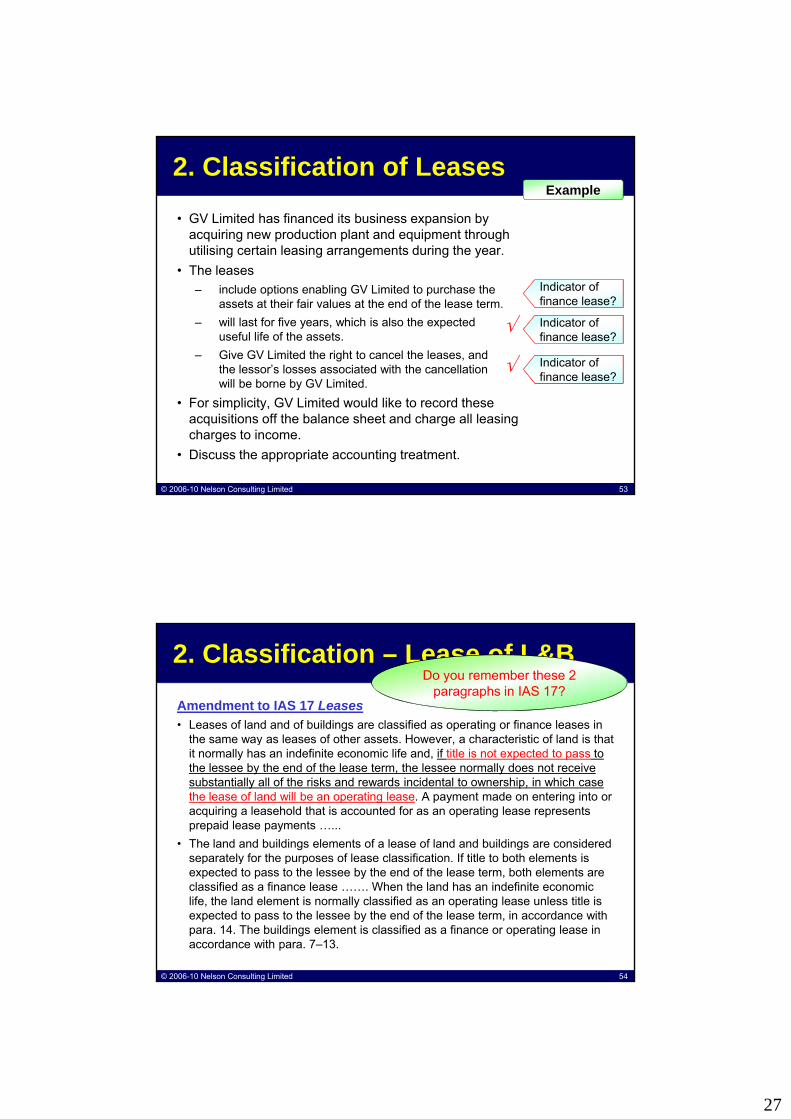

bull GV Limited has financed its business expansion by acquiring new production plant and equipment through utilising certain leasing arrangements during the year

Example

g g g g ybull The leases

ndash include options enabling GV Limited to purchase the assets at their fair values at the end of the lease term

ndash will last for five years which is also the expecteduseful life of the assets

ndash Give GV Limited the right to cancel the leases andthe lessorrsquos losses associated with the cancellation

Indicator of finance lease

Indicator of finance lease

Indicator of finance lease

radic

radic

copy 2006-10 Nelson Consulting Limited 53

will be borne by GV Limited bull For simplicity GV Limited would like to record these

acquisitions off the balance sheet and charge all leasing charges to income

bull Discuss the appropriate accounting treatment

finance lease

2 Classification ndash Lease of LampB

Amendment to IAS 17 Leasesbull Leases of land and of buildings are classified as operating or finance leases in

the same way as leases of other assets However a characteristic of land is that

Do you remember these 2 paragraphs in IAS 17

the same way as leases of other assets However a characteristic of land is that it normally has an indefinite economic life and if title is not expected to pass to the lessee by the end of the lease term the lessee normally does not receive substantially all of the risks and rewards incidental to ownership in which case the lease of land will be an operating lease A payment made on entering into or acquiring a leasehold that is accounted for as an operating lease represents prepaid lease payments hellip

bull The land and buildings elements of a lease of land and buildings are considered separately for the purposes of lease classification If title to both elements is

copy 2006-10 Nelson Consulting Limited 54

p y p pexpected to pass to the lessee by the end of the lease term both elements are classified as a finance lease helliphellip When the land has an indefinite economic life the land element is normally classified as an operating lease unless title is expected to pass to the lessee by the end of the lease term in accordance with para 14 The buildings element is classified as a finance or operating lease in accordance with para 7ndash13

28

2 Classification ndash Lease of LampB

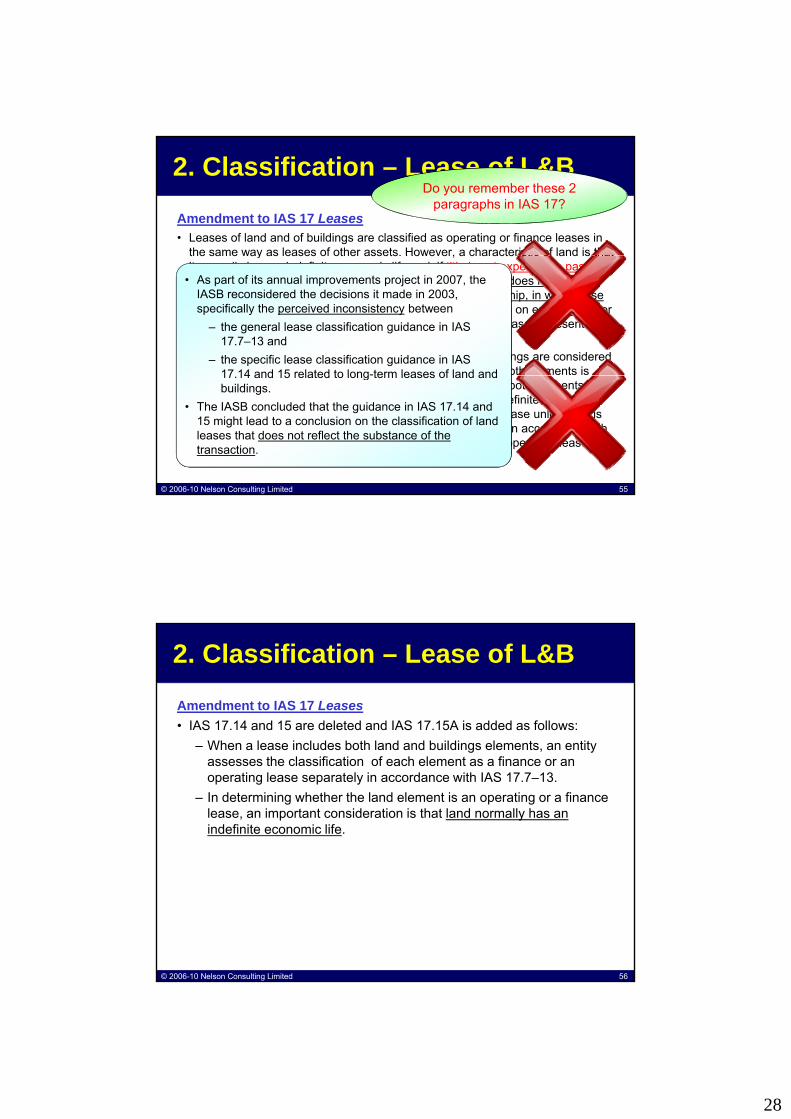

Amendment to IAS 17 Leasesbull Leases of land and of buildings are classified as operating or finance leases in

the same way as leases of other assets However a characteristic of land is that

Do you remember these 2 paragraphs in IAS 17

the same way as leases of other assets However a characteristic of land is that it normally has an indefinite economic life and if title is not expected to pass to the lessee by the end of the lease term the lessee normally does not receive substantially all of the risks and rewards incidental to ownership in which case the lease of land will be an operating lease A payment made on entering into or acquiring a leasehold that is accounted for as an operating lease represents prepaid lease payments hellip

bull The land and buildings elements of a lease of land and buildings are considered separately for the purposes of lease classification If title to both elements is

bull As part of its annual improvements project in 2007 the IASB reconsidered the decisions it made in 2003 specifically the perceived inconsistency between ‒ the general lease classification guidance in IAS

177ndash13 and‒ the specific lease classification guidance in IAS

17 14 and 15 related to long-term leases of land and

copy 2006-10 Nelson Consulting Limited 55

p y p pexpected to pass to the lessee by the end of the lease term both elements are classified as a finance lease helliphellip When the land has an indefinite economic life the land element is normally classified as an operating lease unless title is expected to pass to the lessee by the end of the lease term in accordance with para 14 The buildings element is classified as a finance or operating lease in accordance with para 7ndash13

1714 and 15 related to long-term leases of land and buildings

bull The IASB concluded that the guidance in IAS 1714 and 15 might lead to a conclusion on the classification of land leases that does not reflect the substance of the transaction

2 Classification ndash Lease of LampB

Amendment to IAS 17 Leasesbull IAS 1714 and 15 are deleted and IAS 1715A is added as follows

Wh l i l d b th l d d b ildi l t titndash When a lease includes both land and buildings elements an entity assesses the classification of each element as a finance or an operating lease separately in accordance with IAS 177ndash13

ndash In determining whether the land element is an operating or a finance lease an important consideration is that land normally has an indefinite economic life

copy 2006-10 Nelson Consulting Limited 56

29

2 Classification ndash Lease of LampBExample

bull IASB describes in IAS 17BC8B and BC8C thatndash For example consider a 999-year lease of land and buildings

bull In this situation significant risks and rewards associated with the land during the lease term would have been transferred to the lessee despite there being no transfer of title

bull The Board noted that the lessee in leases of this type will typically be in a position economically similar to an entity that purchased the land and buildings

bull The present value of the residual value of the property in a lease with a term of several decades would be negligible

bull The Board concluded that the accounting for the land element as a

copy 2006-10 Nelson Consulting Limited 57

The Board concluded that the accounting for the land element as a finance lease in such circumstances would be consistent with the economic position of the lessee

Unclear how long the lease term must Unclear how long the lease term must be for the IASB to conclude that a be for the IASB to conclude that a

lessee and a purchaser are in the same lessee and a purchaser are in the same economic positioneconomic position

2 Classification ndash Lease of LampB

Galaxy Entertainment Group Limited(2009 Annual Report)

Case

( p )ndash The Group has early adopted HKAS 17

(Amendment) Leases which is mandatory for accounting periods beginning on and after 1 January 2010 hellip

ndash HKAS 17 (Amendment) requires the Group to reassess the classification of leasehold land as finance or operating lease

copy 2006-10 Nelson Consulting Limited 58

p gbull Upon adoption the opening balances have been

assessed and classified accordingly bull Current year addition to leasehold land has been

classified based on the underlying criteria of HKAS 17

30

2 Classification ndash Lease of LampBCase

bull Note 2 states (for early adoption of Amendment to HKAS 17 in 2009)

Financial Statements 2009

ndash The early adoption of the amendment to HKAS 17 has resulted in a change in accounting policy for the classification of leasehold land of the Group

ndash Previously leasehold land was classified as an operating lease and stated at cost less accumulated amortisation

ndash In accordance with the amendment leasehold land is classified as a finance lease and stated at cost less accumulated depreciation if substantially all risks and rewards of the leasehold land have been transferred to the Group bull As the present value of the minimum lease payments (ie the transaction

copy 2006-10 Nelson Consulting Limited 59

As the present value of the minimum lease payments (ie the transaction price) of the land held by the Group amounted to substantially all of the fair value of the land as if it were freehold

the leasehold land of the Group has been classified as a finance lease The amendment has been applied retrospectively to unexpired leases at the date of adoption of the amendment on the basis of information existing at the inception of the leases The amendment does not apply to the leasehold land disposed of by the Group in prior years

3 Lesseesrsquo Financial Statements

bull At lease commencement lessees shall recognise finance leases as assets and liabilities in their statements of financial position at amounts equal to

Initial Recognition and Measurement statements of financial position at amounts equal to

a) the fair value of the leased property orb) if lower the present value of the minimum lease

paymentseach determined at the inception of the lease

bull The discount rate to be used in calculating the present value of the minimum lease payments isndash the interest rate implicit in the lease if this is

FinanceLease

Measurement

copy 2006-10 Nelson Consulting Limited 60

the interest rate implicit in the lease if this is practicable to determine

ndash if not the lessees incremental borrowing rate shall be used

bull Any initial direct costs of the lessee are added to the amount recognised as an asset

31

3 Lesseesrsquo Financial Statements

bull Minimum lease payments shall be apportioned betweena) the finance charge and

Subsequent Measurement

a) the finance charge andb) the reduction of the outstanding liability

bull Finance charge allocated to each period during the leasendash so as to produce a constant periodic rate of interest

on the remaining balance of the liabilitybull Contingent rents charged as expenses in the

periods in which they are incurred

FinanceLease

copy 2006-10 Nelson Consulting Limited 61

periods in which they are incurred

bull Contingent rent is that portion of the lease paymentsndash that is not fixed in amountndash but is based on the future amount of a factor that changes other than with

the passage of timeeg percentage of future sales amount of future use future price indices future market rates of interest

3 Lesseesrsquo Financial Statements

bull A finance lease gives rise tondash depreciation expense for depreciable assets as

well as

Subsequent Measurement

well asndash finance expense for each accounting period

bull The depreciation policy for depreciable leased assetsndash consistent with that for depreciable assets that

are owned andndash the depreciation recognised shall be calculated

in accordance with IAS 16 and IAS 38

FinanceLease

copy 2006-10 Nelson Consulting Limited 62

bull If there is no reasonable certainty that the lessee will obtain ownership by the end of the lease termndash the asset shall be fully depreciated over the

shorter ofbull the lease term andbull its useful life

32

3 Lesseesrsquo Financial StatementsCase

Wynn Macau Limited

bull Finance leases which transfer to the Group substantially all the risks and benefits incidental to ownership of the leased item are capitalized at the inception of the leasendash at the fair value of the leased property or ndash if lower at the present value of the minimum

lease payments

y (Prospectus ndash Accountantsrsquo Report 2009)

Dr AssetsCr Liabilities

copy 2006-10 Nelson Consulting Limited 63

bull Lease payments are apportioned betweenndash the finance charges and ndash reduction of the lease liability

so as to achieve a constant rate of interest on the remaining balance of the liability

bull Finance charges are reflected in profit or loss

Dr LiabilitiesPL ndash Finance charge

Cr Cash

3 Lesseesrsquo Financial Statements

bull In addition to meeting the requirements of IAS 32 the following disclosures for finance leasesa) for each class of asset the net carrying amount at the

Disclosures

) y gend of the reporting period

b) a reconciliation between the total of future minimum lease payments at the end of the reporting period and their present value In addition an entity shall disclose the total of future minimum lease payments at the end of the reporting period and their present value for each of the following periods

i) not later than one yearii) later than one ear and not later than fi e ears

FinanceLease

copy 2006-10 Nelson Consulting Limited 64

ii) later than one year and not later than five yearsiii) later than five years

c) contingent rents recognised as an expense in the periodd) the total of future minimum sublease payments expected

to be received under non-cancellable subleases at the end of the reporting period

e) a general description of the lesseersquos material leasing arrangements

33

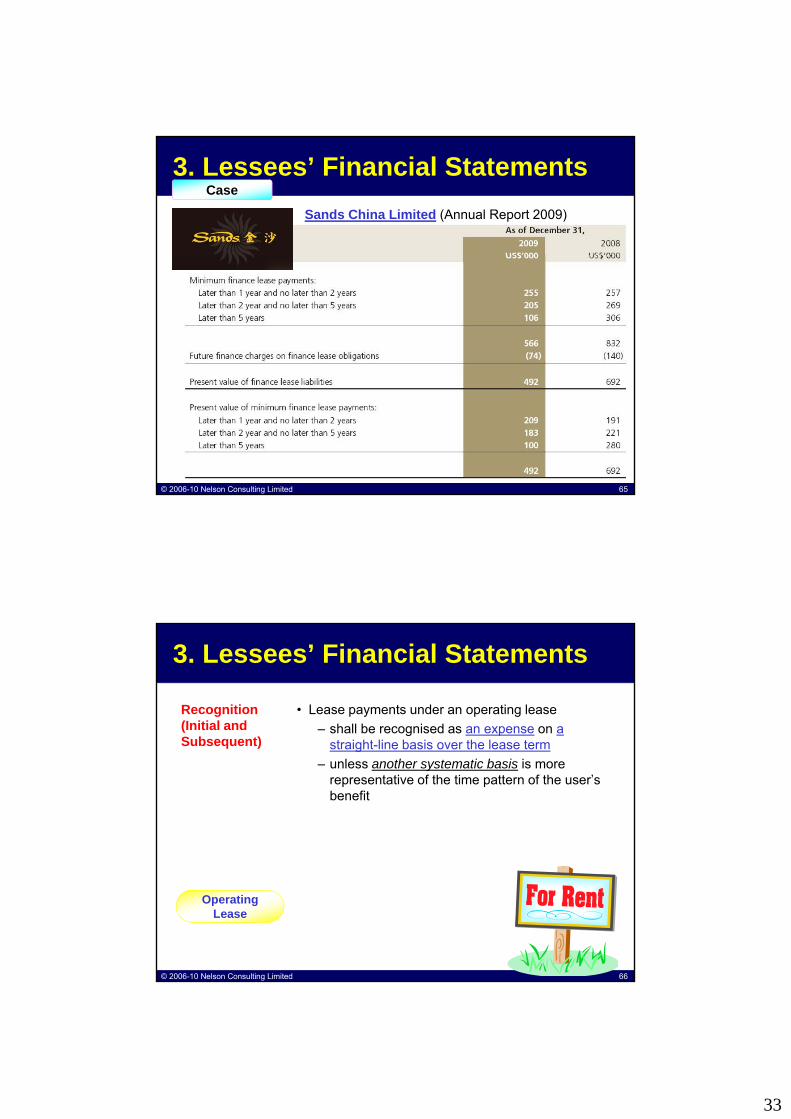

3 Lesseesrsquo Financial StatementsCase

Sands China Limited (Annual Report 2009)

copy 2006-10 Nelson Consulting Limited 65

3 Lesseesrsquo Financial Statements

bull Lease payments under an operating leasendash shall be recognised as an expense on a

straight line basis over the lease term

Recognition (Initial and Subsequent) straight-line basis over the lease term

ndash unless another systematic basis is more representative of the time pattern of the userrsquos benefit

Subsequent)

copy 2006-10 Nelson Consulting Limited 66

Operating Lease

34

3 Lesseesrsquo Financial Statements

bull Lessees shall in addition to meeting the requirements of IAS 32 make the following disclosures for operating leasesa) the total of future minimum lease payments under non-

Disclosures

a) the total of future minimum lease payments under non-cancellable operating leases for each of the following periods

i) not later than one yearii) later than one year and not later than five yearsiii) later than five years

b) the total of future minimum sublease paymentsexpected to be received under non-cancellable

copy 2006-10 Nelson Consulting Limited 67

Operating Lease

subleases at the end of the reporting periodc) lease and sublease payments recognised as an

expense in the period with separate amounts for minimum lease payments contingent rents and sublease payments

d) a general description of the lesseersquos significant leasing arrangements

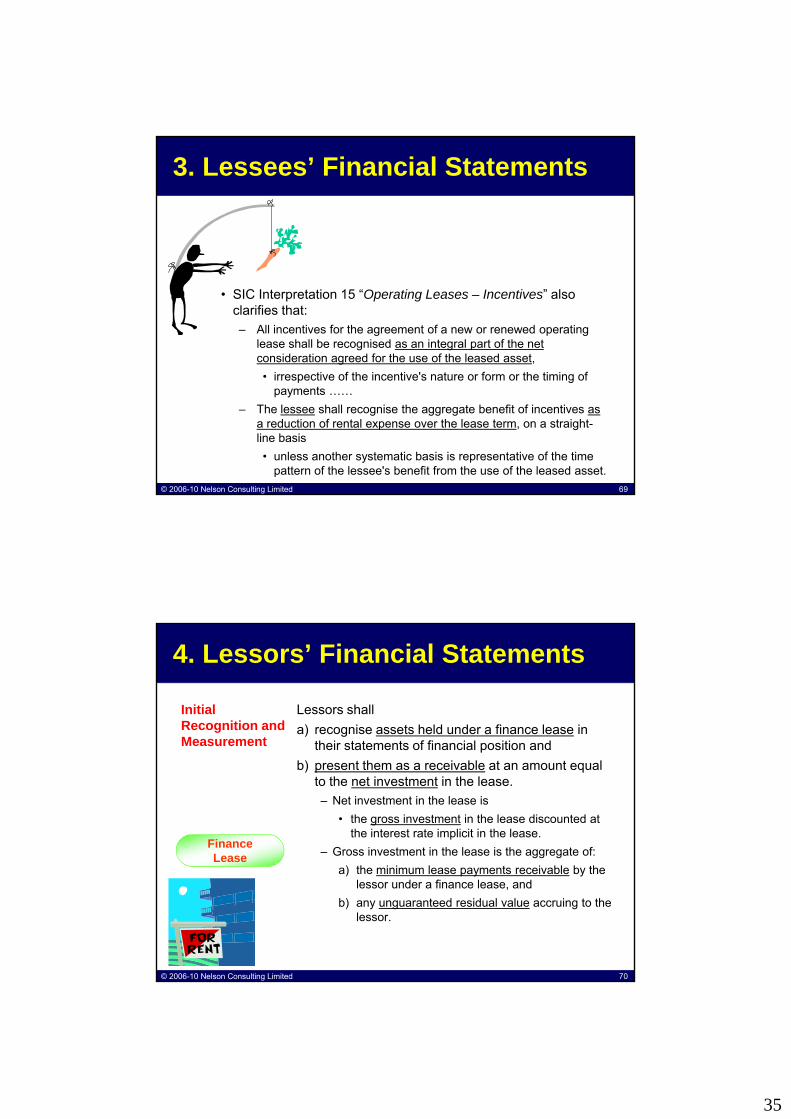

3 Lesseesrsquo Financial StatementsCase

Sands China Limited (Annual Report 2009)

copy 2006-10 Nelson Consulting Limited 68

35

3 Lesseesrsquo Financial Statements

bull SIC Interpretation 15 ldquoOperating Leases ndash Incentivesrdquo also clarifies thatndash All incentives for the agreement of a new or renewed operating

lease shall be recognised as an integral part of the net consideration agreed for the use of the leased asset bull irrespective of the incentives nature or form or the timing of

copy 2006-10 Nelson Consulting Limited 69

bull irrespective of the incentive s nature or form or the timing of payments helliphellip

ndash The lessee shall recognise the aggregate benefit of incentives as a reduction of rental expense over the lease term on a straight-line basisbull unless another systematic basis is representative of the time

pattern of the lessees benefit from the use of the leased asset

4 Lessorsrsquo Financial Statements

Lessors shalla) recognise assets held under a finance lease in

th i t t t f fi i l iti d

Initial Recognition and Measurement their statements of financial position and

b) present them as a receivable at an amount equal to the net investment in the lease ndash Net investment in the lease is

bull the gross investment in the lease discounted at the interest rate implicit in the lease

ndash Gross investment in the lease is the aggregate of

Measurement

FinanceLease

copy 2006-10 Nelson Consulting Limited 70

a) the minimum lease payments receivable by the lessor under a finance lease and

b) any unguaranteed residual value accruing to the lessor

36

4 Lessorsrsquo Financial Statements

bull The recognition of finance incomendash shall be based on a pattern reflecting a constant

periodic rate of return on the lessors net

Subsequent Measurement

periodic rate of return on the lessors net investment in the finance lease

FinanceLease

copy 2006-10 Nelson Consulting Limited 71

4 Lessorsrsquo Financial Statements

bull Manufacturer or dealer lessorsndash shall recognise selling profit or loss in the period

in accordance with the policy followed by the

Leases for Manufacturer or Dealer Lessors in accordance with the policy followed by the

entity for outright salesbull If artificially low rates of interest are quoted

ndash selling profit shall be restricted to that which would apply if a market rate of interest were charged

bull Costs incurred by manufacturer or dealer lessors in ti ith ti ti d i l

Dealer Lessors

FinanceLease

copy 2006-10 Nelson Consulting Limited 72

connection with negotiating and arranging a leasendash shall be recognised as an expense when the

selling profit is recognised

37

4 Lessorsrsquo Financial Statements

bull CampP Inc was used to sell its self-manufactured motor car at $500000 at cash price and the cost of the car was about $280000

bull In order to boom its sale CampP Inc offers 2 plans of instalment sale to

Example

In order to boom its sale CampP Inc offers 2 plans of instalment sale to its customers1 Customers can buy the car at $550000 and repay the consideration in 12

equal instalment over a year at zero interest2 Customers can buy the car at $500000 and then arrange a 48-month

instalment plan with the subsidiary of CampP Inc and the interest rate is 10 per annum on the outstanding balance

bull Discuss the implication on the selling profit to CampP Inc

copy 2006-10 Nelson Consulting Limited 73

bull The outright profit on the sale is still $220000 ($500000 - $280000)bull Even for plan 1 the selling profit should still be restricted to $220000

ndash Since no interest (ie an artificially low rate of interest) is quoted selling profit shall be restricted to that which would apply if a market rate of interest were charged

ndash The excess of selling profit is an compensation on the loss of interest

4 Lessorsrsquo Financial Statements

Lessors shall in addition to meeting the requirements in IAS 32 disclose the following for finance leasesa) a reconciliation between the gross investment in the lease

Disclosures

a) a reconciliation between the gross investment in the lease at the end of the reporting period and the present value of minimum lease payments receivable at the end of the reporting period In addition an entity shall disclose the gross investment in the lease and the present value of minimum lease payments receivable at the end of the reporting period for each of the following periods

i) not later than one yearii) later than one year and not later than five yearsiii) later than five years

FinanceLease

copy 2006-10 Nelson Consulting Limited 74

iii) later than five yearsb) unearned finance incomec) the unguaranteed residual values accruing to the benefit

of the lessord) the accumulated allowance for uncollectible minimum

lease payments receivablee) contingent rents recognised as income in the periodf) a general description of material leasing arrangements

38

4 Lessorsrsquo Financial Statements

bull Lessors shall present assets subject to operating leases in their statements of financial position according to the nature of the asset

Recognition (Initial and Subsequent) according to the nature of the asset

bull Lease income from operating leasesndash shall be recognised in income on a straight-line basis

over the lease termndash unless another systematic basis is more representative

of the time pattern in which use benefit derived from the leased asset is diminished

Subsequent)

copy 2006-10 Nelson Consulting Limited 75

Operating Lease

4 Lessorsrsquo Financial Statements

bull Initial direct costs incurred by lessorsndash shall be added to the carrying amount of the leased

asset and

Recognition (Initial and Subsequent) asset and

ndash recognised as an expense over the lease term on the same basis as the lease income

bull Depreciation policy for depreciable leased assetsndash shall be consistent with the lessorrsquos normal

depreciation policyndash depreciation shall be calculated in accordance with IAS

16 and 38

Subsequent)

copy 2006-10 Nelson Consulting Limited 76

Operating Lease

39

4 Lessorsrsquo Financial Statements

bull Lessors shall in addition to meeting the requirements of IAS 32 disclose the following for operating leasesa) the future minimum lease payments under non

Disclosures

a) the future minimum lease payments under non-cancellable operating leases in the aggregate and for each of the following periodsi) not later than one yearii) later than one year and not later than five yearsiii) later than five years

b) total contingent rents recognised as income in the period

copy 2006-10 Nelson Consulting Limited 77

c) a general description of thelessorrsquos leasing arrangements

Operating Lease

4 Lessorsrsquo Financial StatementsCase

Sands China Limited (Annual Report 2009)

copy 2006-10 Nelson Consulting Limited 78

40

Revenue (IAS 18)

copy 2006-10 Nelson Consulting Limited 79

1 Objective of IAS 18

bull Incomendash is defined in the Framework for the Preparation and Presentation of

Financial Statements asFinancial Statements asbull increases in economic benefits during the accounting period in the form

of inflows orbull enhancements of assets or decreases of liabilities that result in increases

in equitybull other than those relating to contributions from equity participants

ndash Income encompasses both revenue and gains

copy 2006-10 Nelson Consulting Limited 80

bull Revenue is income that ndash arises in the course of ordinary activities of an entity and is referred

to by a variety of different names including sales fees interest dividends and royalties

41

1 Objective of IAS 18

bull The primary issue in accounting for revenue isndash determining when to recognise revenue

bull Revenue is recognised whenbull Revenue is recognised whenndash it is probable that future economic benefits will

flow to the entity andndash these benefits can be measured reliably

bull IAS 18 identifies the circumstances in which these criteria will be met and therefore revenue will be recognised

copy 2006-10 Nelson Consulting Limited 81

2 Scope of IAS 18

bull IAS 18 shall be applied in accounting for revenue arising from the following transactions and eventsSale of goodsSale of goodsa) the sale of goodsb) the rendering of services andc) the use by others of entity assets

yielding interest royalties and dividends

Sale of goodsSale of goods

Rendering of Rendering of servicesservices

Interest royalties Interest royalties and dividendand dividend

copy 2006-10 Nelson Consulting Limited 82

42

2 Scope of IAS 18

IAS 18 does not deal with revenue arising froma) lease agreements (see IAS 17 Leases)b) dividends arising from investments which are accounted for under theb) dividends arising from investments which are accounted for under the

equity method (see IAS 28 Investments in Associates)c) insurance contracts within the scope of IFRS 4 Insurance Contractsd) changes in the fair value of financial assets and financial liabilities or their

disposal (see IAS 39 Financial Instruments Recognition and Measurement)e) changes in the value of other current assetsf) initial recognition and from changes in the fair value of biological assets

related to agricultural activity (see IAS 41 Agriculture)

copy 2006-10 Nelson Consulting Limited 83

related to agricultural activity (see IAS 41 Agriculture)g) initial recognition of agricultural produce (see IAS 41) andh) the extraction of mineral ores

3 What is Revenue

bull Revenue isndash the gross inflow of economic benefits

during the periodndash arising in the course of the ordinary

activities of an entityndash when those inflows result in increases

copy 2006-10 Nelson Consulting Limited 84

in equityndash other than increases relating to

contributions from equity participants

43

3 What is Revenue

bull Revenue includesndash only the gross inflows of economic benefits received and receivable

by the entity on its own accountby the entity on its own accountbull Amounts collected on behalf of third parties such as sales taxes goods

and services taxes and value added taxesndash are not economic benefits which flow to the entity andndash do not result in increases in equity

Therefore they are excluded from revenuebull Similarly in an agency relationship the gross inflows of economic

b fit i l d t ll t d b h lf f th i i l d hi h

copy 2006-10 Nelson Consulting Limited 85

benefits include amounts collected on behalf of the principal and which do not result in increases in equity for the entity

The amounts collected on behalf of the principal are not revenueInstead revenue is the amount of commission

4 Measurement of Revenue

bull Revenue shall be measured at the fair value of the consideration received or receivablendash Fair value is the amount for which an asset could be exchanged or aFair value is the amount for which an asset could be exchanged or a

liability settled between knowledgeable willing parties in an arms length transaction

ndash The amount of revenue arising on a transaction is usually determined by agreement between the entity and the buyer or user of the asset

ndash It is measured atbull the fair value of the consideration received or receivable

copy 2006-10 Nelson Consulting Limited 86

the fair value of the consideration received or receivablebull taking into account the amount of any trade discounts and volume

rebates allowed by the entityndash In most cases the consideration is in the form of cash or cash

equivalents and the amount of revenue is the amount of cash or cash equivalents received or receivable

44

4 Measurement of RevenueCase

Wynn Macau Limited

bull Revenue ndash is recognized to the extent that it is probable that

the economic benefits will flow to the Group and the revenue can be reliably measured

bull Revenue is measured at the fair value of the consideration

y (Prospectus ndash Accountantsrsquo Report 2009)

copy 2006-10 Nelson Consulting Limited 87

ndash is measured at the fair value of the consideration received excluding discounts rebates and other sales taxes or duties

5 Identification of the Transaction

bull The recognition criteria in IAS 18 is usually applied separately to each transaction

bull However there are situations that thebull However there are situations that the recognition criteria is1 Applied to separately identifiable

components of a single transaction2 Applied to two or more transactions

together

Separately identifiable component of a single transaction

Two or moretransactions together

copy 2006-10 Nelson Consulting Limited 88

45

5 Identification of the Transaction

bull In certain circumstances it is necessary to apply the recognition criteria to the separately identifiable components of a single transaction in order to reflect the substance of the transaction

Example

Separately identifiable component of a single transaction

bull For examplendash when the selling price of a product

includes an identifiable amount for subsequent servicing

copy 2006-10 Nelson Consulting Limited 89

subsequent servicingbull that amount is deferred and

recognised as revenue over the period during which the service is performed

5 Identification of the Transaction

bull Conversely the recognition criteria are applied to two or more transactions together when they are linked in such a way that the commercial effect cannot be understood without reference to the series

Example

of transactions as a whole

bull For examplendash an entity may sell goods and at the

same time enter into a separate agreement to repurchase the goods at a later date

Two or moretransactions together

copy 2006-10 Nelson Consulting Limited 90

at a later datebull thus negating the substantive

effect of the transaction in such a case the two transactions are dealt with together

46

5 Identification of the TransactionCase

Wynn Macau Limited

bull Casino revenues ndash are measured by the aggregate net difference

between gaming wins and losses ndash with liabilities recognized for funds deposited by

customers before gaming play occurs and for chips in customersrsquo possession

y (Prospectus ndash Accountantsrsquo Report 2009)

copy 2006-10 Nelson Consulting Limited 91

pbull Revenues are recognized net of certain sales

incentives bull Accordingly the Grouprsquos casino revenues

ndash are reduced by discounts commissions and points earned in customer loyalty programs

Customer Loyalty Programmes (IFRIC Interpretation 13)

copy 2006-10 Nelson Consulting Limited 92

47

Background

bull Customer loyalty programmes are used by entitiesto provide customers with incentives to buy their goods or services

ndash If a customer buys goods or services the entity grants the customer award credits (often described as points)

ndash The customer can redeem the award credits for awards such as free or discounted goods or services

bull The programmes operate in a variety of waysndash Customers may be required to accumulate a specified minimum number or

value of award credits before they are able to redeem them

copy 2006-10 Nelson Consulting Limited 93

value of award credits before they are able to redeem them ndash Award credits may be linked to individual purchases or groups of

purchases or to continued custom over a specified period ndash The entity may operate the customer loyalty programme itself or

participate in a programme operated by a third party ndash The awards offered may include goods or services supplied by the entity

itself andor rights to claim goods or services from a third party

Scope

bull IFRIC Interpretation 13 applies to customer loyalty award credits thata) an entity grants to its customers as part of a salesa) an entity grants to its customers as part of a sales

transaction ie a sale of goods rendering of services or use by a customer of entity assets and

b) subject to meeting any further qualifying conditions the customers can redeem in the future for free or discounted goods or services

bull The Interpretation addresses accounting by the entity that grants award credits to its customers

copy 2006-10 Nelson Consulting Limited 94

48

Issues

bull Whether the entityrsquos obligation to provide free or discounted goods or services (awards) in the future should be recognised and measured byg yi) allocating some of the consideration received or

receivable from the sales transaction to the award credits and deferring the recognition of revenue(applying IAS 1813) or

ii) providing for the estimated future costs of supplying the awards (applying IAS 1819) and

bull If consideration is allocated to the award creditsi) h h h ld b ll t d t th

copy 2006-10 Nelson Consulting Limited 95

i) how much should be allocated to themii) when revenue should be recognised andiii) if a third party supplies the awards how revenue

should be measured

Conclusions ndash Separation

bull An entity shall ndash apply IAS 1813 and

account for award credits as a separately

Separately Identifiable Componentndash account for award credits as a separately

identifiable component of the sales transaction(s) in which they are granted (the initial sale)

bull The fair value of the consideration received or receivable in respect of the initial sale shall be allocated between

the award credits and

Component

Award Credit

Fair Value

copy 2006-10 Nelson Consulting Limited 96

ndash the award credits and ndash the other components of the sale Components

Other Components

Supplied by Supplied by the Entity Itselfthe Entity Itself

Supplied by Supplied by the Third Partythe Third Party

49

Conclusions ndash Fair Value

bull The consideration allocated to the award credits shall be measured by reference to their fair value

ndash i e the amount for which the award credits couldie the amount for which the award credits could be sold separately

bull If the fair value is not directly observable it must be estimated

bull An entity may estimate the fair value of award credits by reference to

ndash the fair value of the awards for which they could be redeemed

Award Credit

Fair Value

copy 2006-10 Nelson Consulting Limited 97

be redeemed

Supplied by Supplied by the Entity Itselfthe Entity Itself

Supplied by Supplied by the Third Partythe Third Party

Conclusions ndash Fair Value

bull The fair value of the awards (for which they could be redeemed) would be reduced to take into accounta) the fair value of awards that would be offered toa) the fair value of awards that would be offered to

customers who have not earned award credits from an initial sale and

b) the proportion of award credits that are not expected to be redeemed by customers

bull If customers can choose from a range of different awards the fair value of the award credits will reflect

th f i l f th f il bl dAward Credit

Fair Value

copy 2006-10 Nelson Consulting Limited 98

ndash the fair values of the range of available awards weighted in proportion to the frequency with which each award is expected to be selected

Supplied by Supplied by the Entity Itselfthe Entity Itself

Supplied by Supplied by the Third Partythe Third Party

50

Conclusions ndash Recognition

bull If the entity supplies the awards itself it shall recognise the consideration allocated to award credits as revenue when

ndash award credits are redeemed andndash it fulfils its obligations to supply awards

bull The amount of revenue recognised shall be based on

ndash the number of award credits that have been redeemed in exchange for awards

No of Award Credits Redeemed in Exchange

divide

copy 2006-10 Nelson Consulting Limited 99

ndash relative to the total number expected to be redeemed

Supplied bySupplied bythe Entity Itselfthe Entity Itself

Total No of Award Credits Expected to be Redeemed

Conclusions ndash Recognition

bull If a third party supplies the awards the entity shall assess whether it is collecting the consideration allocated to the award credits

ndash on its own account(ie as the principal in the transaction) or

ndash on behalf of the third party(ie as an agent for the third party)

On its Own Account

On Behalf of the Third Party

copy 2006-10 Nelson Consulting Limited 100

Supplied by Supplied by the Third Partythe Third Party

51

Conclusions ndash Recognition

bull If the entity is collecting the consideration on its own account it shall ndash measure its revenue as the grossndash measure its revenue as the gross

consideration allocated to the award creditsand

ndash recognise the revenue when it fulfils its obligations in respect of the awards

On its Own Account

copy 2006-10 Nelson Consulting Limited 101

Supplied by Supplied by the Third Partythe Third Party

Conclusions ndash RecognitionExample

bull A grocery retailer operates a customer loyalty programme‒ It grants programme members loyalty points when they

spend a specified amount on groceries p p g‒ Programme members can redeem the points for further

groceries ‒ The points have no expiry date

bull In one period the entity grants 100 points (assume sales of $2000) ‒ Management expects 80 of these points to be redeemed ‒ Management estimates the fair value of each loyalty point to

copy 2006-10 Nelson Consulting Limited 102

g y y pbe one currency unit ($1) and defers revenue of $100

Dr Cash $ 2000Cr Revenue $ 1900

Deferred income 100

52

Conclusions ndash RecognitionExample

Year 1bull At the end of the first year 40 points (pts) have been redeemed in exchange for

groceries ie half of those expected to be redeemed g pbull The entity recognises revenue of (40 80 pts) times $100 = $50

Dr Deferred income $ 50Cr Revenue $ 50

Year 2bull In the second year management revises its expectations and now expects 90

points to be redeemed altogetherbull During the second year 41 points are redeemed bringing the total number

copy 2006-10 Nelson Consulting Limited 103

During the second year 41 points are redeemed bringing the total number redeemed to 40 + 41 = 81 points

bull The cumulative revenue that the entity recognises is (81 90 pts) times $100 = $90 bull The entity has recognised revenue of $50 in the first year so it recognises $40

in the second yearDr Deferred income $ 40Cr Revenue $ 40

Conclusions ndash RecognitionExample

Year 3bull In the third year a further nine points are redeemed taking the total number of

points redeemed to 81 + 9 = 90 points p pbull Management continues to expect that only 90 points will ever be redeemed ie

that no more points will be redeemed after the third year bull So the cumulative revenue to date is (90 points 90 points) times $100 = $100 bull The entity has already recognised $90 of revenue ($50 in the first year and $40

in the second year) bull So it recognises the remaining $10 in the third year bull All of the revenue initially deferred has now been recognised

copy 2006-10 Nelson Consulting Limited 104

y gDr Deferred income $ 10Cr Revenue $ 10

53

Conclusions ndash Recognition

bull If the entity is collecting the consideration on behalf of the third party it shalli) measure its revenue as the net amount retained on its own account i e thei) measure its revenue as the net amount retained on its own account ie the

difference between bull the consideration allocated to the award credits andbull the amount payable to the third party for supplying

the awards andii) recognise this net amount as revenue when the

third party becomes obliged to supply the awardsand entitled to receive consideration for doing so

On Behalf of the Third Party

copy 2006-10 Nelson Consulting Limited 105

bull These events may occur as soon as the award credits are grantedbull Alternatively if the customer can choose to claim awards from either

the entity or a third party these events may occur only when the customer chooses to claim awards from the third party

Supplies by Supplies by the Third Partythe Third Party

Conclusions ndash RecognitionCase

bull A retailing amp real estate group stated in its annual report 2009Th G h li d IFRIC 13 C L l P

Casino Guichard-Perrachon

ndash The Group has applied IFRIC 13 ndash Customer Loyalty Programmes as of 1 January 2009 bull This standard sets out the accounting treatment for award credits

granted to customers upon an initial sale transaction for use against a future sale transaction

ndash Award credits are recognised as a separately identifiable component of the initial sales transaction and their fair value at inception is deducted from the revenue generated by the sale

copy 2006-10 Nelson Consulting Limited 106

ndash When the award credit is used by the customerbull the revenue deferred at inception is recognised and bull the cost of the award credit is either deducted

ndash from the cost of goods sold (in the case of exchange vouchers) or ndash from revenue (in the case of money vouchers)

54

Conclusions ndash RecognitionCase

bull A retailing amp real estate group stated in its annual report 2009Th G h f l l l d b IFRIC 13

Casino Guichard-Perrachon

ndash The Group has two types of loyalty plan covered by IFRIC 13bull plans that award points to customers when they purchase goods in Group

stores which may be cashed in for money vouchers or gift vouchersbull a money voucher plan

ndash The Group previously recognised a provision for the costs incurred in granting award credits to its customers

ndash Under IFRIC 13 the Group now accounts for the fair value of the award credits granted (that is the fair value to the customer) as

copy 2006-10 Nelson Consulting Limited 107

award credits granted (that is the fair value to the customer) as opposed to their cost

ndash Consequently the impact of customer loyalty plans is now presentedbull in the balance sheet as deferred income rather than provisions and bull in the income statement as a deduction from revenue or in the cost of

goods sold as applicable rather than in marketing costs

IFRS for Hospitality and Gaming Industry(Part 1) 25 May 2010

copy 2006-10 Nelson Consulting Limited 108

Nelson LamNelson Lam 林智遠林智遠nelsonnelsoncpacomhkwwwNelsonCPAcomhkwwwFacebookcomNelsonCPA

55

IFRS for Hospitality and Gaming Industry(Part 1) 25 May 2010

QampA SessionQampA SessionQampA SessionQampA Session

copy 2006-10 Nelson Consulting Limited 109

Nelson LamNelson Lam 林智遠林智遠nelsonnelsoncpacomhkwwwNelsonCPAcomhkwwwFacebookcomNelsonCPA

2

Presentation of Financial Statements(IAS 1 Revised in 2007)

copy 2006-10 Nelson Consulting Limited 3

Complete Set of Fin Statements

bull A complete set of financial statements comprisesa) a statement of financial position as at the end of the

period

Previously we call it ldquoBalance Sheetrdquoperiod

b) a statement of comprehensive income for the periodc) a statement of changes in equity for the periodd) a statement of cash flows for the periode) notes comprising a summary of significant accounting

policies and other explanatory information andf) a statement of financial position as at the beginning of

the earliest comparative period

Previously we call it ldquoIncome Statementrdquo

3 yearsrsquo ldquobalance sheetsrdquo

copy 2006-10 Nelson Consulting Limited 4

the earliest comparative periodbull when an entity applies an accounting policy

retrospectively or makes a retrospective restatement of items in its financial statements or

bull when it reclassifies items in its financial statementsbull An entity may use titles for the statements other than

those used in HKAS 1

3

Structures amp Content of Fin Statements

Statement of Financial Position as at the end of the period

Complete Set of Financial Statements Previous titleor changes

Previous title ldquoBalance Sheetrdquo

To use a single statement to present all items of income and expense

Statement of Comprehensive Income for the period

Statement of Changes in Equity for the period

No title change

No title change(but restructured)

New statement

To use two statements to present all items of income and expense

Statement of Comprehensive Income for the period

Income Statement for the period

copy 2006-10 Nelson Consulting Limited 5

Statement of Cash Flows for the period

Notes

A statement of financial position as at the beginning of the earliest comparative period if required

Previous titleldquoCash Flow Statementrdquo

(but restructured)

No title change

New requirement

Sourced from Intermediate Financial Reporting (2009) by Nelson Lam and Peter Lau

Statement of Comprehensive IncomeChanges in equity

in a periodSingle Statement Single Statement

ApproachApproachTwoTwo--Statement Statement

ApproachApproach

Components of profit or loss

Components of other

comprehensive income

Non-owner changes

Presented in separateincome statement

Presented in statementof comprehensive income

Presented in statementof comprehensive income

copy 2006-10 Nelson Consulting Limited 6

Components of owner changes

in equity

Owner changes

Presented in statementof changes in equity

Presented in statementof changes in equity

Sourced from Intermediate Financial Reporting (2009) by Nelson Lam and Peter Lau

4

Statement of Comprehensive IncomeCase

Consolidated statement of comprehensive income

copy 2006-10 Nelson Consulting Limited 7

Statement of Comprehensive IncomeCase

copy 2006-10 Nelson Consulting Limited 8

5

Property Plant and Equipment (IAS 16)

copy 2006-10 Nelson Consulting Limited 9

1 Objective and Scope

bull The principal issues in accounting for property plant and equipment (PPE) area) the recognition of the assets Definitionsa) the recognition of the assetsb) the determination of their carrying amounts andc) the depreciation charges and impairment losses

to be recognised in relation to themMeasurement

Recognition

copy 2006-10 Nelson Consulting Limited 10

6

bull Building acquired under an

1 Objective and Scope

What are PPE Are the following PPEWhat are PPE Are the following PPE

Example

IAS 17timesoperating lease

bull Building acquired under finance leases

bull Freehold property used for rental purpose

bull Investment property underre-development

IAS 17

radic

times

times

IAS 40

IAS 40

copy 2006-10 Nelson Consulting Limited 11

pbull Property held for a currently

undetermined future usebull Leasehold land separated

from the leasehold building

times

times

IAS 40

IAS 17

2 Definitions

bull Property plant and equipment (PPE) are tangible items thata) are held for use

ndash in the production or supply of goods or servicesin the production or supply of goods or services ndash for rental to others or ndash for administrative purposes and

b) are expected to be used during more than one period