Indian Income Tax

A Birds Eye ViewGeneral Structure for Laymen

By Kamal Bhandari

Five Heads of Income (or Losses)

1. Salary ( Net)

2. Income from House Property (Net)

3. Income From Business / Profession (Net)

4. Capital Gains / Losses (Net)

5. Other Income (Net)– Bank Interest, Windfall Gains etc.

• Each of the above Income heads have special deductions / adjustments from Actual Income

By Kamal Bhandari

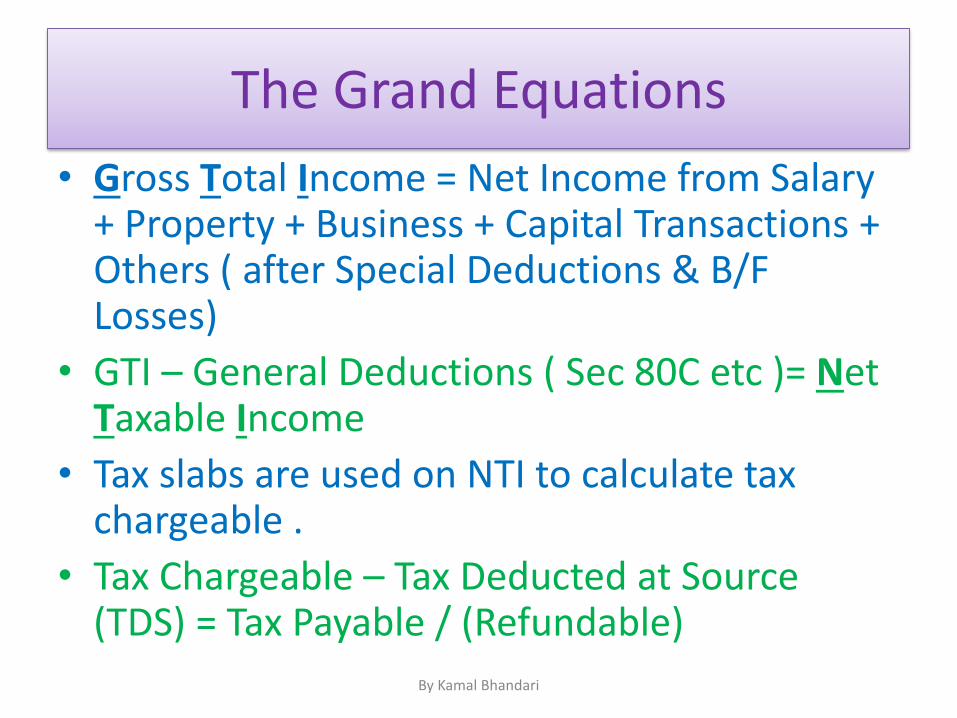

The Grand Equations

• Gross Total Income = Net Income from Salary + Property + Business + Capital Transactions + Others ( after Special Deductions & B/F Losses)

• GTI – General Deductions ( Sec 80C etc )= Net Taxable Income

• Tax slabs are used on NTI to calculate tax chargeable .

• Tax Chargeable – Tax Deducted at Source (TDS) = Tax Payable / (Refundable)

By Kamal Bhandari

Exempt Income

• Income which do not enter the GTI calculation

– Tax Free bonds, PPF interest

– LT Gains on Equity and Equity Funds

– Life Insurance payouts

– Other specified items

By Kamal Bhandari

When & Who is Taxed ?

• Income is taxed for each Previous Year (April 2013 - March 2014)– Returns filed in Assessment Year (2014-15) by 31st

July

• Type of Residency: Non Resident, Not Ordinarily Resident or Resident– Non Resident are at least 182 days out of India in PY. Only

Income arising in India is taxable.

• Type of Person: Individual, HUF, Company, Firm etc– Different tax rates apply. Any “Person” can be non-resident

By Kamal Bhandari

Income from Salaries

• Basic Salary and Allowances

• Fees, Commission and Bonus

• All Perquisites or subsidized services, Loans

• Retirement Benefits

• Deduct: Exempt portion of HRA, Professional Tax paid, LTA etc

By Kamal Bhandari

Income From Property

• The higher of actual rent or notional rental value is taken as “Annual Value”. – Only one self-occupied property is treated as zero AV

– Determination of Notional Rent is a bit tricky involving Fair Rent, Municipal Rent, Std. Rent and Actual Rent comparisons.

• (AV-Property tax)* (1-30% ) = Net AV

• Net AV - Interest on Property Loan ( Limits apply) = Taxable income

By Kamal Bhandari

Income from Business & Prof.

• Tax code is complex and varied on this issue with many exemptions and limitations relating to income arising out of running a business or profession.

• Profit / Loss from Option & Forward trading falls under this head instead of Capital Gains even for individuals who have no business setup

By Kamal Bhandari

Income from Capital Gains

• Gain on sales of Funds, Equity, Securities, Property, Bullion, Art, Business etc come under this head

• Long Term Gain is usually any gain on sales after holding an asset for 3 years (one year only for Equity or Equity funds). There are special tax saving strategies available.

• LT Gain on Equity & Eq funds are fully exempt.• Short Term gain is anything which is not long

term and has no special tax treatment except Equity & Eq funds is taxed at 15% PTO

By Kamal Bhandari

Income from Capital Gainscontd

• LT Gains are computed after scaling up the actual cost by the cost inflation index ratio

• LT Gain = Sales – Indexed cost

• Indexed LT gain is taxed at 20% (NRI can opt for Non-indexed LT gain and be taxed at 10% )

• Cost Includes Cost of Improvement too.

• Sales means Net sales Proceeds after direct expenses incurred on selling. PTO

By Kamal Bhandari

Income from Capital Gainscontd

• LT Gains from Sale of House Property: There are many different sops available for saving tax on such gains. Mostly by investing the proceeds in another property within a period of couple of years from the sale or one year prior to sale.

• By investing entire proceeds in specified GovtBonds, tax on LT Gain can be saved up to 100%

By Kamal Bhandari

Income from Other Sources

• This head is the residual section to catch all income not defined under other specific heads before e.g. Bank Interest, Awards, Windfall gains, Lottery and gambling etc– Bank Interest attracts a small exemption upto Rs

10,000

• Interest on NRE & FCNR accounts and fixed deposits are fully exempted.

• NRO accounts and NRO deposits are fully taxable

By Kamal Bhandari

General Deductions from GTI

• Some investments e.g. ELSS, PPF, EPF, NSC, 5 yr Post Office Deposit, Housing Loan Principal payment etc upto Rs 150,000 (Section 80C)

• Medical Ins Premium upto 15,000 (80D)

• Medical Treatment Rs 40,000 (80DDB)

• Interest on Edu Loan for 8 years (80E)

• Charitable donations to recognisedInstitutions – 50% / 100% (80G) PTO

By Kamal Bhandari

General Deductions from GTI

• Rent paid upto Rs 2000 pm max (80GG)

• Donation to Political Party (80GGC)

• Disabilities 50,000 or 100,000 (80U)

• Saving Bank Interest Rs 10,000 (80TTA)

By Kamal Bhandari

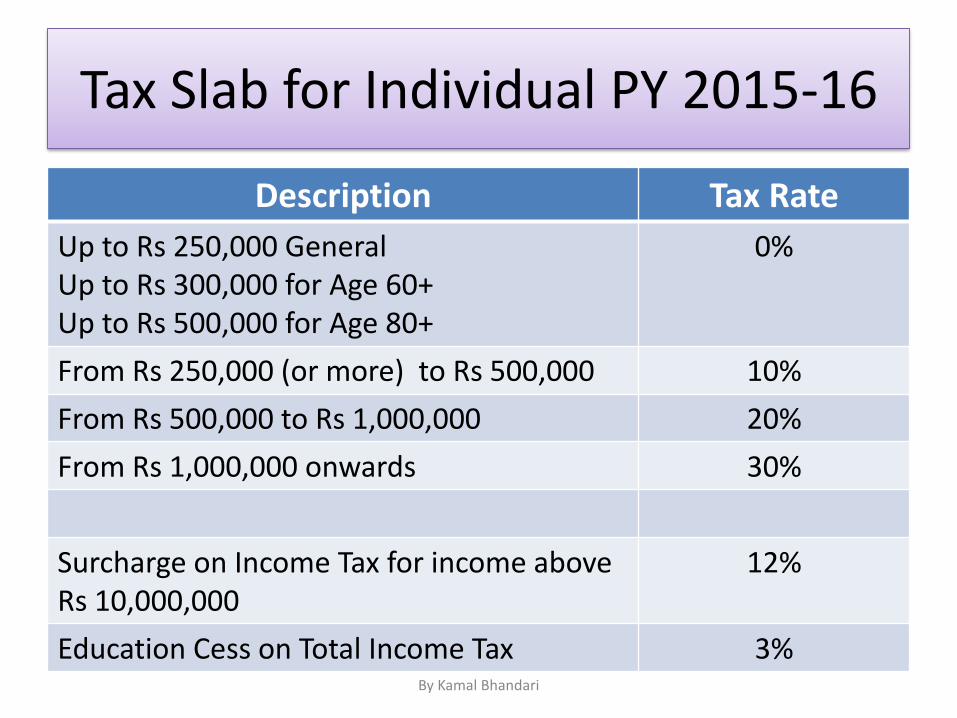

Tax Slab for Individual PY 2015-16

Description Tax Rate

Up to Rs 250,000 GeneralUp to Rs 300,000 for Age 60+Up to Rs 500,000 for Age 80+

0%

From Rs 250,000 (or more) to Rs 500,000 10%

From Rs 500,000 to Rs 1,000,000 20%

From Rs 1,000,000 onwards 30%

Surcharge on Income Tax for income above Rs 10,000,000

12%

Education Cess on Total Income Tax 3%By Kamal Bhandari

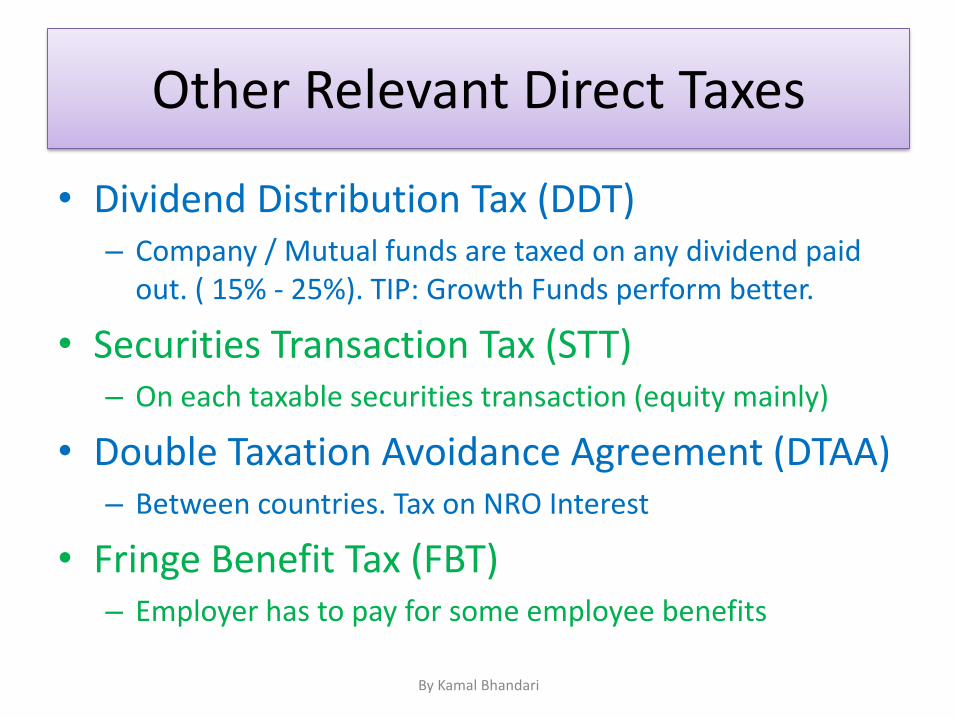

Other Relevant Direct Taxes

• Dividend Distribution Tax (DDT)– Company / Mutual funds are taxed on any dividend paid

out. ( 15% - 25%). TIP: Growth Funds perform better.

• Securities Transaction Tax (STT)– On each taxable securities transaction (equity mainly)

• Double Taxation Avoidance Agreement (DTAA)– Between countries. Tax on NRO Interest

• Fringe Benefit Tax (FBT)– Employer has to pay for some employee benefits

By Kamal Bhandari

THANK YOUEND

FOR BEING PATIENT …..

By Kamal Bhandari

Recommended

![Indian Accounting Standard [AS] -22 Tax on Income](https://img.pdfslide.net/doc/110x75/55b82c4dbb61eb680f8b47dc/indian-accounting-standard-as-22-tax-on-income.jpg)