Kent Housing Group10th September 2013

Terrie AlafatDirector, Housing Growth and Affordable Housing Department for Communities and Local Government

2

A Housing Strategy to increase supply

Supporting demand • Recognition of aspiration of home

ownership• Increasing demand for rented

homes

Increase housing supply• Across all tenures – addressing

barriers

Underpinned by systemic reform • Planning• Greater land availability

Getting house building moving again is crucial for economic growth – having a direct impact on economic output, averaging at 3% of the GDP in the last decade.

3

The Challenge: Barriers to supply

4

The Challenge: Barriers to demand

• From 2000-2007, annual mortgage lending increased by 200%

• Lending broadly flat sinceMortgage Lending

• Sharp fall in annual mortgage lending in 2007-8.

• First time buyers particularly hit as deposit requirements soared

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

110.0

Jan-

02

May

-02

Sep

-02

Jan-

03

May

-03

Sep

-03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep

-05

Jan-

06

May

-06

Sep

-06

Jan-

07

May

-07

Sep

-07

Jan-

08

May

-08

Sep

-08

Jan-

09

May

-09

Sep

-09

Jan-

10

May

-10

Sep

-10

Jan-

11

May

-11

Sep

-11

Jan-

12

May

-12

Sep

-12

Jan-

13

Month

%

First Time Buyers – Deposits as % of Income

• Demand for private rented housing is growing - the sector now houses 3.8 million households in England, compared to 2.0 million in 2000..

5

Supporting Home Ownership NewBuy Right to Buy

Expanding Rented Sector

Unlocking Housing Development

Help to Buy: Equity

Loan

Affordable Homes

Programme

Build to rent

Debt Guarantees

PRS taskforce

Local Infrastructure

Fund

Get Britain Building

Public sector land

Growing Places Fund

£3.5bn, £1bn

Guarantee75,000 plus transactions

Nearly £6bn, £10bn

GuaranteesUp to

210,000homes

£1.6bnUnlocking

capacity for over 120,000

homes - 11,000 started

on site

Delivery to 2015

PLANNING REFORM

6

2013 has shown the most positive signs to date of recovery in housing market activity

Quarterly housing starts & completions(seasonally adjusted)

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1990

1

1991

2

1992

3

1993

4

1995

1

1996

2

1997

3

1998

4

2000

1

2001

2

2002

3

2003

4

2005

1

2006

2

2007

3

2008

4

2010

1

2011

2

2012

3

Quarter

Starts

Completions

Quarterly housing starts hit their highest point since 2010

BUT starts and completions are down on the long term average

The flow of residential planning approvals in Q1 2013 7% higher than a year ago.

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2008 2009 2010 2011 2012 2013 Q1only

7

This is driven by improved demand and consumer confidence

•Value of mortgage lending up 29% from a year ago. Strongest lending since October 2008.30% increase in number of loans to FTB in year to June 2013. Quarterly lending to first-time buyers was at its highest since 2007.

Net reservations per site

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Jan '08 Jan '09 Jan '10 Jan '11 Jan '12 Jan '13

And reservations on site are moving ahead of seasonal trends.

UK FTB loans as proportion of total mortgages (CML data)

30

40

50

Oct-08 Feb-09 Jun-09 Oct-09 Feb-10 Jun-10 Oct-10 Feb-11 Jun-11 Oct-11 Feb-12 Jun-12 Oct-12 Feb-13 Jun-13

Month

% o

f all

mor

tgag

es

8

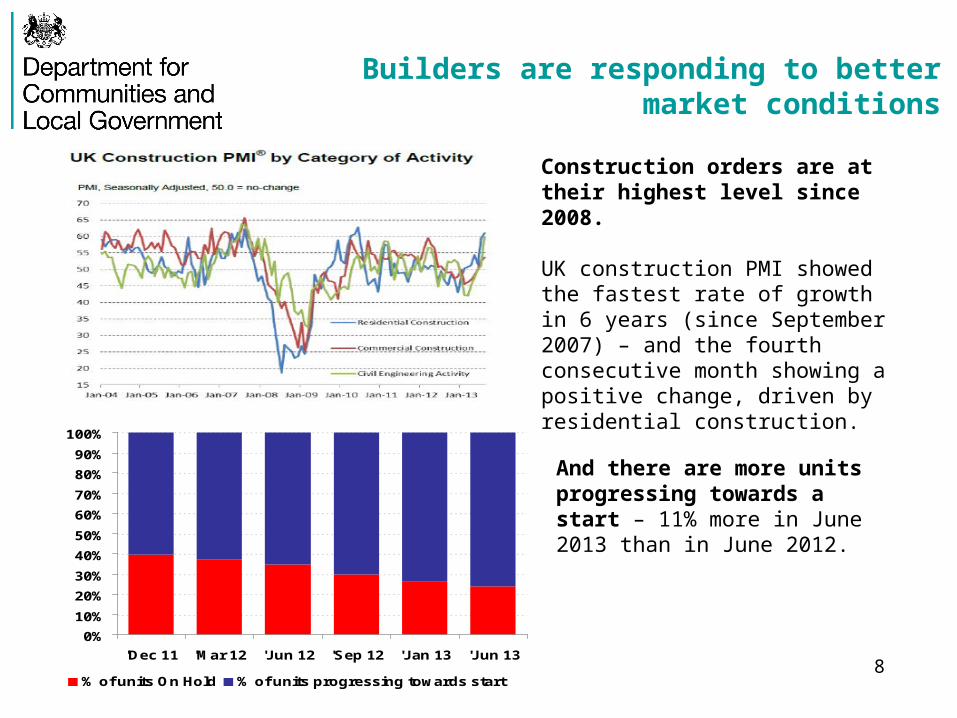

Builders are responding to better market conditions

Construction orders are at their highest level since 2008.

UK construction PMI showed the fastest rate of growth in 6 years (since September 2007) – and the fourth consecutive month showing a positive change, driven by residential construction.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

'Dec 11 'Mar 12 'Jun 12 'Sep 12 'Jan 13 'Jun 13

% of units On Hold % of units progressing towards start

And there are more units progressing towards a start – 11% more in June 2013 than in June 2012.

9

Spending Round: housing package

DEMAND • Help to Buy: Equity Loan £1.3bn in 15/16• Help to Buy: Mortgage Guarantee

LAND• £102 million to unlock large sites• Strategic review to identify Government surplus land and set disposal target • HCA will be Land Disposal Agency

AFFORDABLE HOMES• Affordable Homes programme £3.3bn, plus Guarantees• Rent certainty CPI + 1%• New £400m Rent to Buy programme

PRIVATE RENTED SECTOR• Build to Rent £300m 15/16• Guarantees

LOCAL GROWTH

• £2bn/yr local growth pot • local transport investment

10

Spending Round: Affordable Homes Delivery

• £3.3bn package for 165,000 new affordable homes over 3 years from 2015-16.

• Stronger focus on driving out efficiencies and managing assets actively.

• Rent certainty - rents in the social sector will increase annually by CPI + 1%, for ten years, from 2015/16.

• £400m to pilot a new approach to affordable housing in ‘Affordable Rent to Buy’.

11

Spending Round: Local Authority assets

• £100m for stock transfer in 2015/16 with strong value-for-money and tenant support.

• £160m for Decent Homes targeted at authorities to reduce greatest backlog.

• Aim to ensure no authority will have more than 10% of stock non-decent by 2016.

12

What will this deliver?

• Aiming for 55,000 affordable housing starts a year, the highest rate of new build affordable housing for at least 20 years

• Current programme demonstrated the sector’s ability to drive efficiency and deliver more with less public subsidy

• New programme provides the long term investment framework landlords asked for. In return, we will look for:

• Continuing focus on efficiency and value for money• Opportunities to make more of the asset base – including

the range of options on re-let• Non-developers and under-developers to consider their

capacity to start building

13

Homelessness

Recognise pressures arising from:• Affordability (linked to supply)• Welfare Reform

Government maintaining support to VCS and LAs - £470m over the current SR

Gold Standard for homelessness services – includes commitment to limit B&B for families.

;

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1998199920002001200220032004200520062007200820092010201120122013

Seasonally adjusted Non Seasonal

Statutory Homelessness Acceptances and use of Temporary Accommodation still well below 2003 peak - though increasing.

14

Where next?

• How will housing associations use flexible tenure, rent certainty and increased efficiency to drive investment in affordable homes?

• Will Affordable Rent to Buy offer new opportunities to meet housing need in Kent?

• What more can local authorities do with their land and assets to support supply?

• Will housing be a key part of your LEP’s draft local growth strategy due in the autumn?

Recommended