LANDSCAPE OF DONOR ACTIVITY IN MICROINSURANCE

Henk van Oosterhout, Interim Executive Director, Microinsurance Network

Study: Liz McGuiness, LMG Consulting, for the Microinsurance Network

The global multi-stakeholder platform for microinsurance industry & experts

80 institutional members > 40 countries

www.microinsurancenetwork.org

Connect. Participate. Influence

The Microinsurance Network

www.microinsurancenetwork.org

www.microinsurancenetwork.org

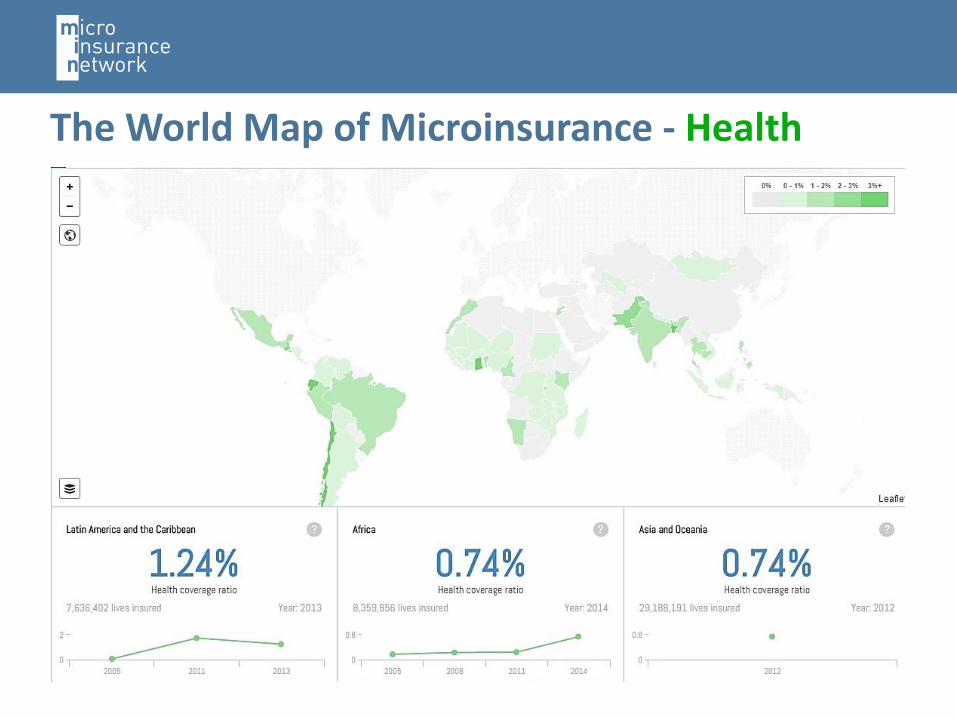

The World Map of Microinsurance - Health

www.microinsurancenetwork.org

The World Map of Microinsurance - Agriculture

www.microinsurancenetwork.org

1. Identify interventions with details since 2011

2. Place interventions in terms of objective, method, funding, and development areas

3. Establish patterns and trends in this landscape

4. Suggest key areas of focus emerging from these patterns

5. Identify global trends

6. Identify donors who are interested in collaborating to develop new donor guidelines on microinsurance

Objectives of the donor landscape study

www.microinsurancenetwork.org

Background information survey

20

98

141112

8

0

20

40

60

80

100

120

Members Non-Members

Nu

mb

er o

f In

stit

uti

on

s

Invited Responded Completed

• 118 donor institutions were contacted

• 20 Donors completed survey

PORTFOLIOS

www.microinsurancenetwork.org

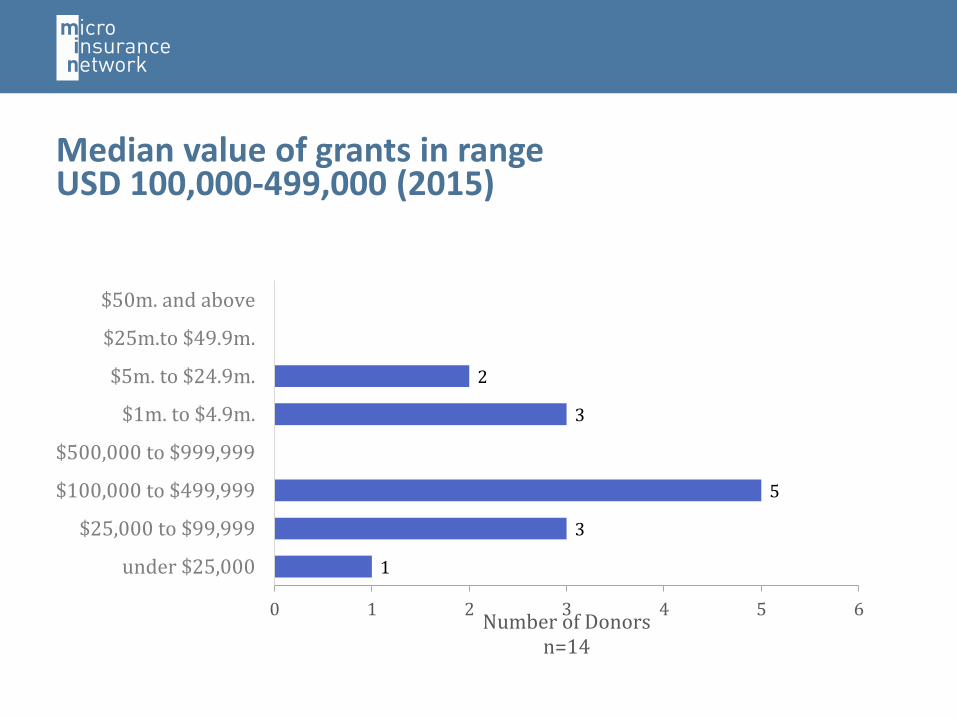

Median value of grants in range USD 100,000-499,000 (2015)

1

3

5

3

2

0 1 2 3 4 5 6

under $25,000

$25,000 to $99,999

$100,000 to $499,999

$500,000 to $999,999

$1m. to $4.9m.

$5m. to $24.9m.

$25m.to $49.9m.

$50m. and above

Number of Donorsn=14

www.microinsurancenetwork.org

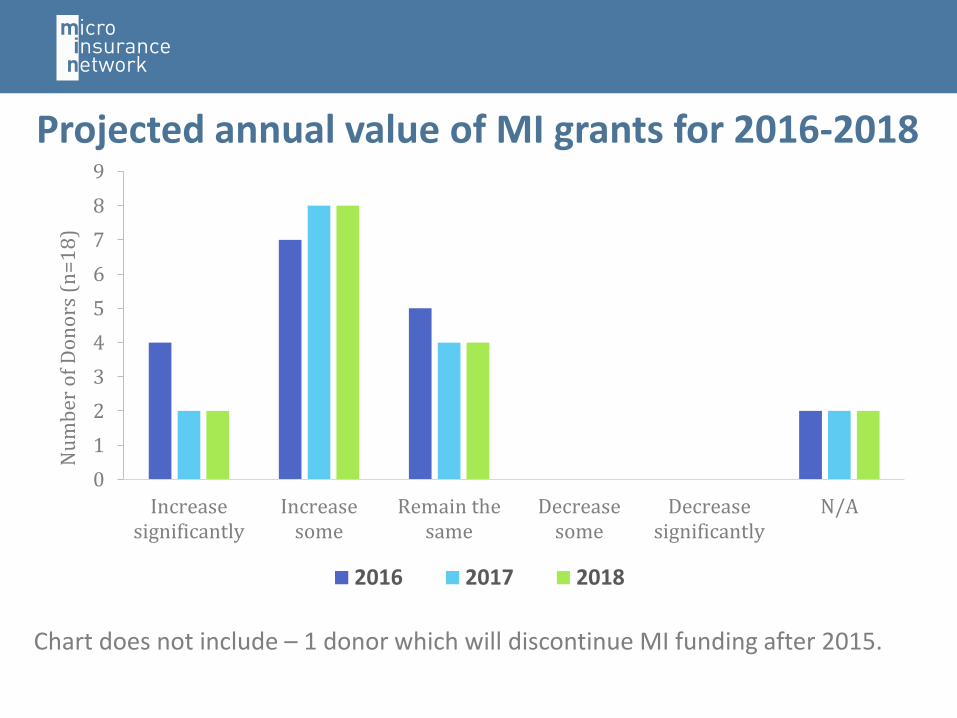

Projected annual value of MI grants for 2016-2018

0

1

2

3

4

5

6

7

8

9

Increasesignificantly

Increasesome

Remain thesame

Decreasesome

Decreasesignificantly

N/A

Nu

mb

er o

f D

on

ors

(n

=1

8)

2016 2017 2018

Chart does not include – 1 donor which will discontinue MI funding after 2015.

REGIONS, PARTNER ORGANIZATIONS AND SECTORS RECEIVING DONOR

SUPPORT

www.microinsurancenetwork.org

Geographical areas receiving donor support

0

2

4

6

8

10

12

14

Nu

mb

er o

f R

esp

on

den

ts

Actual 2011 to 2015 Expected 2016 to 2018

www.microinsurancenetwork.org

Partner organizations receiving donor support

0

2

4

6

8

10

12

14

16

Nu

mb

er o

f R

esp

on

den

ts

Actual 2011 and 2015 Planned 2016 through 2018

www.microinsurancenetwork.org

0

2

4

6

8

10

12

14

Nu

mb

er o

f R

esp

on

den

ts

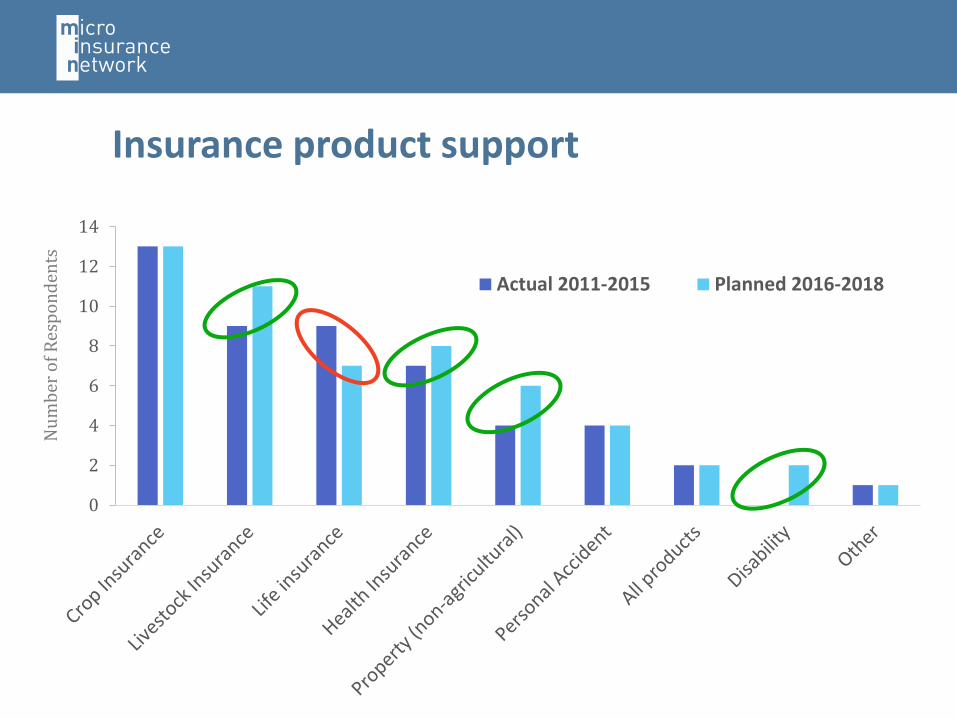

Actual 2011-2015 Planned 2016-2018

Insurance product support

OBJECTIVES OF DONOR INVOLVEMENT

www.microinsurancenetwork.org

Donors’ objectives in supporting MI

5.88

6.88

6.626.83

6.93

5.00

4

5

6

7

8

Stimulatedemand for MI

Encourage supplyof MI

Build the marketinfrastructure for

MI

Advance enabling& protective

policyenvironments

Promote research& evidence

building for MI

Provide global orregional

coordination forMI

Ran

kin

g o

f O

bje

ctiv

e

2011-2015

www.microinsurancenetwork.org

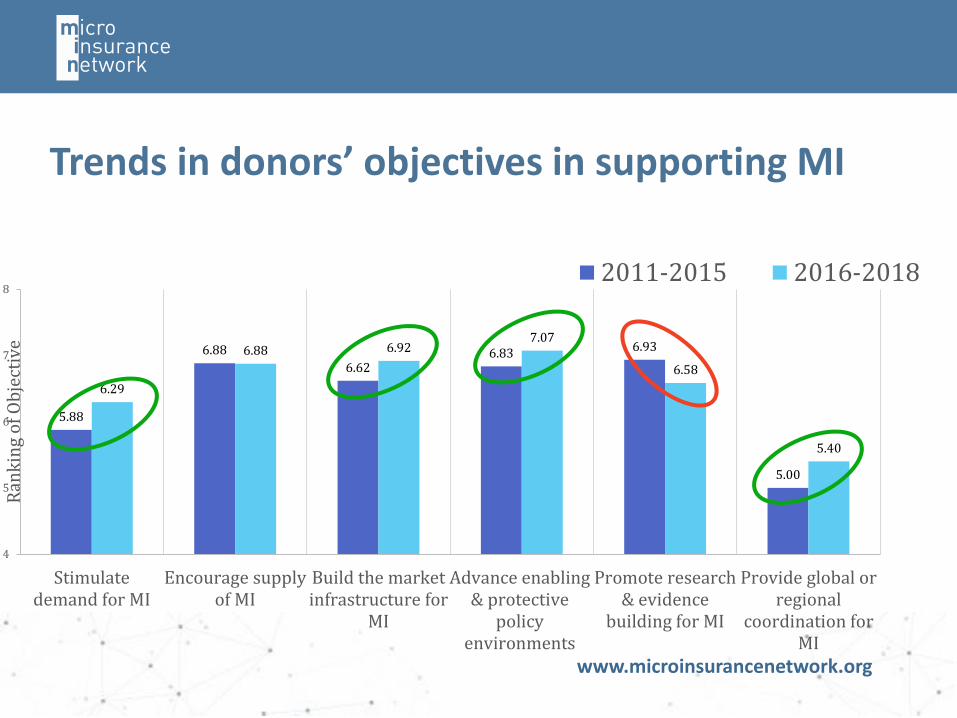

Trends in donors’ objectives in supporting MI

5.88

6.88

6.626.83 6.93

5.00

6.29

6.88 6.927.07

6.58

5.40

4

5

6

7

8

Stimulatedemand for MI

Encourage supplyof MI

Build the marketinfrastructure for

MI

Advance enabling& protective

policyenvironments

Promote research& evidence

building for MI

Provide global orregional

coordination forMI

Ran

kin

g o

f O

bje

ctiv

e

2011-2015 2016-2018

www.microinsurancenetwork.org

Donor’s perception of their role in MI

2

4

4

4

6

7

8

12

Other

Market infrastructure for microinsurance

Research and evidence building for…

Global or regional coordination for…

Enabling and protective policy environments

Demand for microinsurance

Supply of microinsurance

Market systems approach or broad support

Number of Donors (n=16)

www.microinsurancenetwork.org

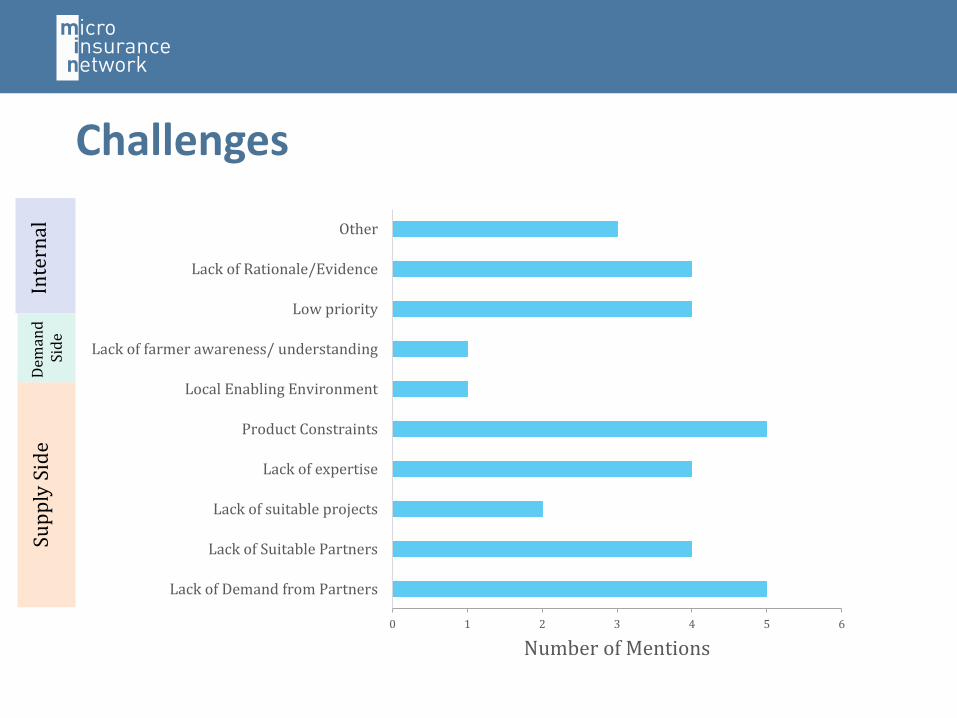

0 1 2 3 4 5 6

Lack of Demand from Partners

Lack of Suitable Partners

Lack of suitable projects

Lack of expertise

Product Constraints

Local Enabling Environment

Lack of farmer awareness/ understanding

Low priority

Lack of Rationale/Evidence

Other

Number of Mentions

Inte

rnal

Sup

ply

Sid

eD

eman

d

Sid

e

Challenges

PRIORITY SECTORS AND PRODUCTS

www.microinsurancenetwork.org

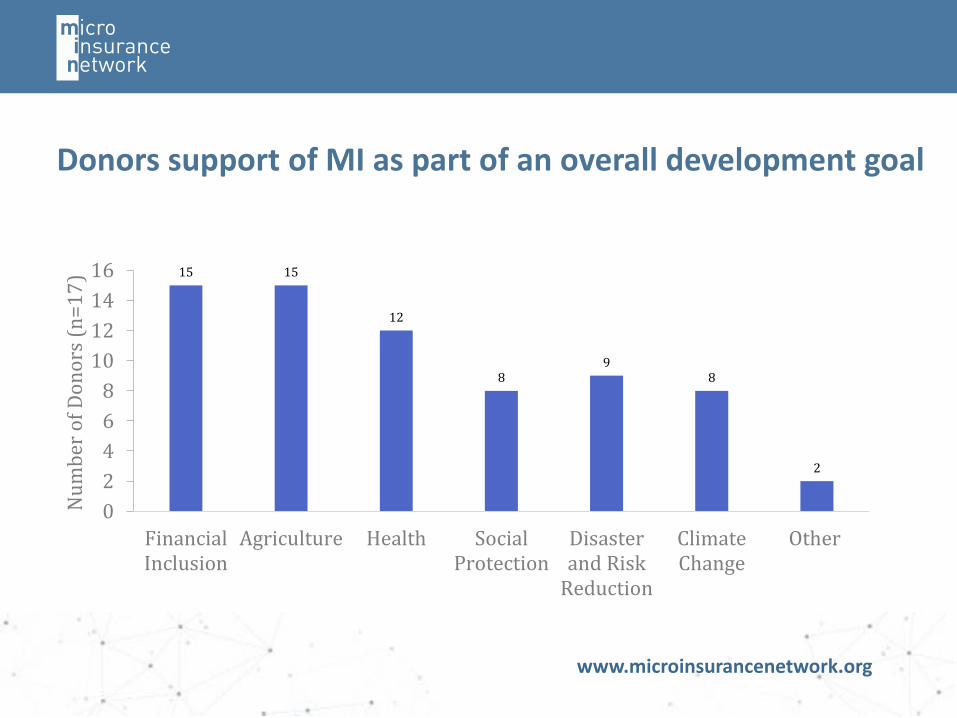

Donors support of MI as part of an overall development goal

15 15

12

89

8

2

0

2

4

6

8

10

12

14

16

FinancialInclusion

Agriculture Health SocialProtection

Disasterand Risk

Reduction

ClimateChange

Other

Nu

mb

er o

f D

on

ors

(n

=1

7)

www.microinsurancenetwork.org

Projected donor support in MI as part of an overall development goal between 2015 and 2018

15 15

12

89

8

2

15 15

9

67

8

3

0

2

4

6

8

10

12

14

16

FinancialInclusion

Agriculture Health SocialProtection

Disaster andRisk

Reduction

ClimateChange

Other

Nu

mb

er o

f D

on

ors

www.microinsurancenetwork.org

TRENDS “Inclusion of Agriculture as a

core sector … means that we expect greater attention to this area.”

“There are increasing concerns about adaptation to climate change amongst our partners …” (AFD)

“Strong (political) focus on climate risk insurance.” (GIZ)

2.22.0

3.73.4

3.9

3.3

4.5

3.0

2011-2015 2016-2018

1.01.0

Health

Climate Change

Development sectors of increasing importance in next 3 years

Note: The lower the number the higher the rank

Agriculture

Disaster & RR

www.microinsurancenetwork.org

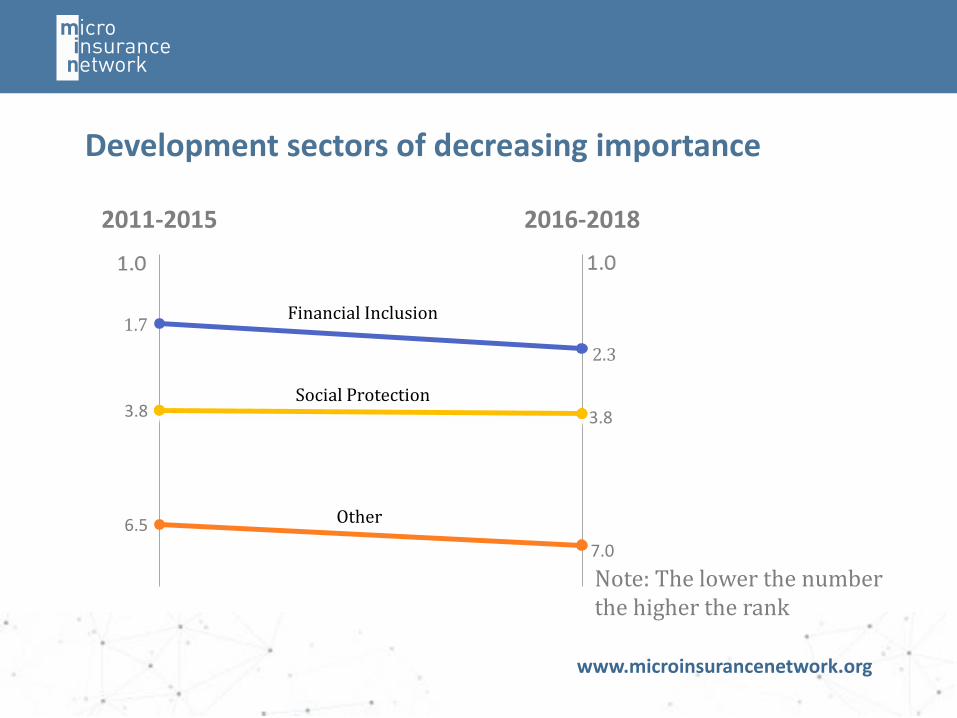

1.7

2.3

3.8 3.8

6.5

7.0

2011-2015 2016-2018

Financial Inclusion

Social Protection

Other

Development sectors of decreasing importance

Note: The lower the number the higher the rank

www.microinsurancenetwork.org

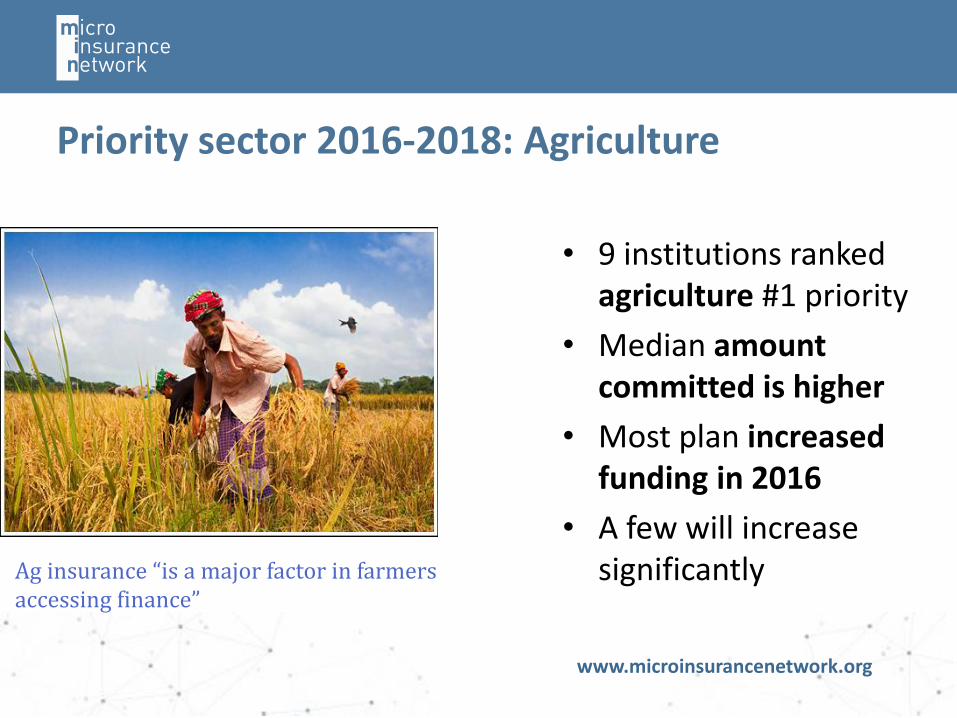

Priority sector 2016-2018: Agriculture

• 9 institutions ranked agriculture #1 priority

• Median amount committed is higher

• Most plan increased funding in 2016

• A few will increase significantlyAg insurance “is a major factor in farmers

accessing finance”

www.microinsurancenetwork.org

Priority sector 2016-2018: Financial inclusion

• 3 institutions ranked FI #1 priority

• MI portfolios tend to be smaller

• Funding flat this year, will increase some in 2017 & 2018

www.microinsurancenetwork.org

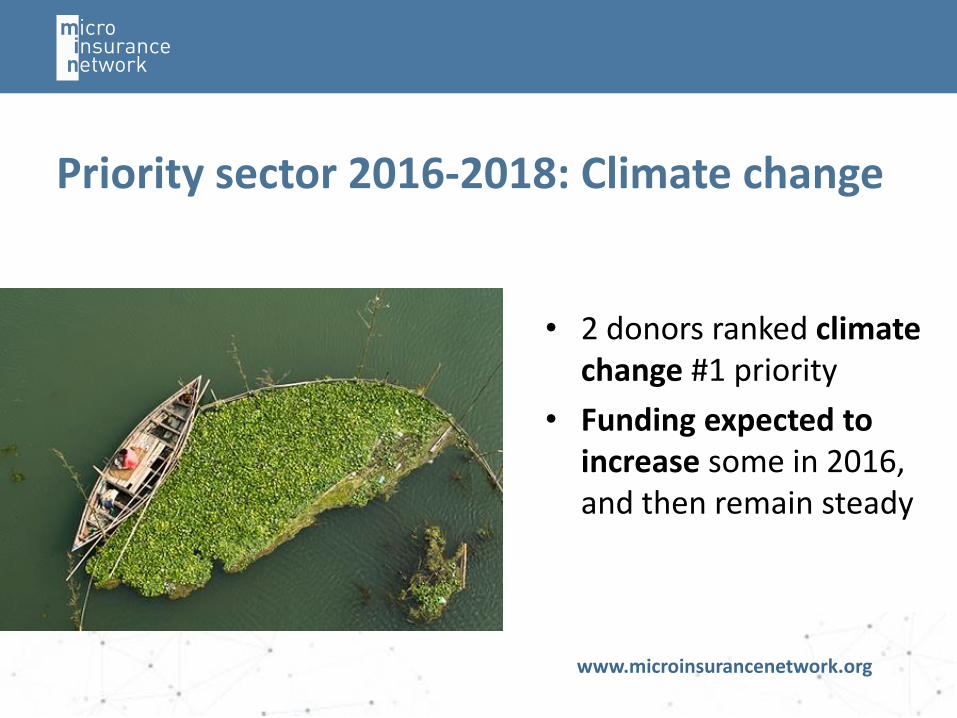

Priority sector 2016-2018: Climate change

• 2 donors ranked climate change #1 priority

• Funding expected to increase some in 2016, and then remain steady

www.microinsurancenetwork.org

Areas of opportunity:

Regulatory and

Supervision Support 5

Scaling 2

Other 5Agricultural Insurance 7

Livestock 1

Index Ins. 3

MI General 1

Health 4

Property 1Disaster Risk Finance 1Climate Change 2

Digital Insurance 2

Products

n=34

www.microinsurancenetwork.org

Key takeaways

Donor landscape: dynamic and growing

Donor objectives: shifting from (1) supporting supply and (2) promoting research & evidence building

(1) advancing the policy and protective policy environments and (2) building market infrastructure

Donor strategies: Movement toward market system development strategy

Caveat: Low response rate & absence of some important donors.

www.microinsurancenetwork.org

Key takeaways• Sectors with increasing support: agriculture, climate change, disaster and

risk reduction and health. However, financial inclusion will still be #2 sector

• Products with increasing support: Livestock, health, property, and disability.

• Lower income countries increasingly emphasized. Selected African nations - prioritized by donors with country specific strategy.

• Donor funding for MI poised to increase.

• Agricultural Insurance will be the most dynamic area: Crop, livestock, index insurance, etc.

THANK YOU

Connect. Participate. Influence

Microinsurance Network

@NetworkFlash

Microinsurance-Network

www.microinsurancenetwork.org

Recommended