Management Going Concern Reporting: Impact on Investors and Auditors

Jagan Krishnan [email protected]

Jayanthi Krishnan [email protected]

Eunju (Ivy) Lee [email protected]

Temple University Department of Accounting

Fox School of Business 1801 Liacouras Walk

Philadelphia, PA 19122

Revised: September 2018

Preliminary version We appreciate the comments of workshop participants at Temple University.

1

Management Going Concern Reporting: Impact on Investors and Auditors

ABSTRACT The Financial Accounting Standards Board (FASB)’s Accounting Standards Update (ASU) 2014-15 required, effective for fiscal years ending after December 15, 2016, managements to evaluate whether there is substantial doubt about the firm’s ability to continue as a going concern, and provide disclosures in financial statement footnotes. Prior to this, information about a firm’s going concern status came from its auditor, which issues a going concern modified (AGC) or “clean” audit opinion on the financial statements. We examine two research questions. First, is the new information provided by management valued by investors? We find that the earnings response coefficients for firms with clean audit opinions (including those that disclose going concern issues), but not for firms with AGCs, increased in the first year of the standard. Second, we examine whether there was a change in auditors’ reporting strategy. We find, after controlling for changes in client characteristics, that auditors became more conservative in the issuance of AGCs in the first year of the standard. Keywords: ASU 2014-15, FASB, Going Concern, Audit Opinion

2

I. INTRODUCTION

Information about a company’s future survivability is important for investors and the

financial markets. Unless liquidation is imminent, US GAAP requires that corporate financial

statements be prepared under the “going concern presumption” that the company will continue to

operate.1 However, even if liquidation is not imminent, a firm can face going concern

uncertainties that would be of interest to investors. Until recently, the firm’s managers played a

relatively passive role in disclosing such uncertainties. Auditing standards require the firm’s

independent auditor to evaluate whether there is substantial doubt about its client’s going

concern ability and, in the event of an affirmative assessment, issue a going concern modified

audit opinion (henceforth AGC) (AS 2415, PCAOB 2017). When such an opinion is issued, the

SEC requires the firm to disclose the associated financial difficulties. In 2014, the Financial

Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2014-15,

introducing an important change to firms’ going concern reporting. Management must now

evaluate whether there is substantial doubt about the firm’s ability to continue as a going

concern, and provide disclosures in financial statement footnotes.

We examine the impact of this standard in the first year of adoption.2 The FASB expects

the standard to improve financial reporting quality by “reducing diversity in the timing and

content of existing footnote disclosures for all entities” (emphasis added). Our first research

question, motivated by the FASB’s expectation, is the following: do investors perceive earnings

1 ASU 2014-15 does not define the concept of “going concern presumption.” In its 2013 Exposure draft for the standard, the Board defined it as the presumption that an entity “will continue to operate such that it will be able to realize its assets and meet its obligations in the ordinary course of business” (FASB 2013). 2 ASU 2014-15 applies to public and private entities. We focus on public entities only.

3

of companies to be more credible in the first year of adoption of ASU 2014-15 (which included

both auditor and management evaluations) compared with the previous year (which included

only auditor evaluations)? We then examine a second question: did the new standard change the

auditor’s behavior in issuing an AGC? Although the FASB’s main focus in implementing this

standard is on the benefits to users of financial statements, the auditor will need to assess these

new client disclosures about going concern, while also making its own AGC decision (PCAOB

2014, Staff Audit Practice Alert No. 13). We posit therefore that auditor behavior can also be

affected by the standard. Further motivation for this research question is provided by

commenters on the exposure draft that preceded the new standard, many of whom analyzed the

potential effect on auditors. Also, the PCAOB is now reviewing and considering revisions to the

auditing standards for the going concern opinion, in light of the new FASB accounting standard.

The going concern evaluation requires considerable judgement (Carcello, Hermanson,

and Huss 1995; DeFond, Raghunandan, and Subramanyam 2002; Knechel and Vanstraelen

2007; DeFond and Zhang 2014). The FASB articulates two sources of benefits to investors from

ASU 2014-15. First, management can provide additional information about the entity’s going

concern status than that provided by auditors, particularly when the auditor does not issue a

going concern opinion in the presence of mitigating factors. To the extent that this is new

information which investors can use, it can influence investor perceptions about the companies

reporting such information. The second benefit can arise for all companies as noted in the FASB

quote above. ASU 2014-15 defines management’s responsibility to evaluate its going concern

status and provides guidance about the evaluation and disclosures. Management has private

information about the company operations, its strategy, its negotiation with lenders, and other

critical matters, which are relevant to such evaluation. The FASB expects that, because of the

4

judgment needed in the GC assessment, firms may need to “implement and document underlying

processes and controls” (FASB 2014, 31). Thus, regardless of the final outcome of the going

concern judgments by the auditor, the working of the standard can engender positive investor

perceptions of change in firms’ financial reporting quality for all firms.

Under ASU 2014-15, management performs an active role in the evaluation and public

disclosure of going concern issues, compared with its previous passive role of responding behind

the scenes to its auditor’s inquiries about such issues.3 Two factors are relevant here. First, such

active involvement likely means that management is more rigorous than before in its assessment.

Since management has superior private information about the firm, this can potentially provide

both investors and auditors with greater confidence than before in their own assessments. For

investors, while the auditor’s opinion on the firm’s going concern is informative, another layer of

information provided by management can enhance the information environment.

Second, while ASU 2014-15 incorporates many of the disclosure considerations in the

auditing standard, it introduces some important differences. These include, as we discuss in more

detail later, a formal definition of “substantial doubt,” a longer forward-looking window than

that used by auditors, and the requirement that, unlike auditors, management must disclose

relevant information even when the initial substantial doubt is expected to be alleviated by

mitigating factors. Investors, who previously knew only the auditor’s binary going concern

assessment, are now provided more details about the company’s going concern status. An

example of such additional details is provided in a recent much-publicized Form 10-K filing by

3 In addition, SEC rules require disclosures by management when the auditor issues a going concern opinion. More relevant to our analyses, some managers with no auditor going concern modified opinions also disclosed going-concern-related issues prior to the new standard, in the Management, Discussion, and Analysis (MD&A) (Mayew, Sethuraman, and Venkatachalam 2015) and Risk Factors sections of their 10-Ks, but these disclosures were voluntary in nature.

5

Sears for the fiscal year ended January 28, 2017. Sears disclosed that conditions suggesting

substantial doubt about going concern were mitigated by management plans. This disclosure was

accompanied by a clean audit report from Sears’ auditors, Deloitte (Steele 2017).

We hand-collect data on management disclosures for firm-years before and after the

effective date of the standard. Not surprisingly, there is considerable overlap between auditors’

and managements’ going concern assessments when the auditor issues a going concern opinion.

However, there is variation in managements’ disclosures about going concern for “clean” firms

that have not received going concern opinions from their auditors. In most cases, clean firms

have no disclosures relating to going concern (suggesting the absence of any adverse issues), or

state explicitly that they have no going concern issues. We expect that this provides a dual

assurance about clean firms, the auditor’s clean opinion being confirmed by management. This is

different from the pre-standard period when disclosures were voluntary and therefore, their

absence did not necessarily indicate the absence of going concern problems. Some firms disclose

(under ASU 2014-15) issues relating to going concern even in the absence of an auditor’s going

concern report. These provide information about management plans and factors that mitigate

initial substantial doubt judgments.

We compare investors’ responsiveness to earnings – measured by the response of stock

returns to earnings surprises (the earnings response coefficient, ERC) - in the pre-standard year

(henceforth the “PRE period”) and the post-standard year (the “POST period”). We document

the following findings. First, there is no change in the ERCs for firms with going concern audit

opinions. This is consistent with the conjecture that, due to the SEC disclosure requirements for

AGC firms, the ASU 2014-15 disclosures do not provide new information. Second, ERCs for

firms with clean audit reports (i.e., no AGC) and with management confirmation of the absence

6

of going concern issues, increase in the POST period. We conjecture that this is due to the “dual

assurance” being offered in the POST period, as opposed to the single (auditor) assurance that

was offered in the PRE period. Third, we also find, interestingly, an increase in ERC for the

clean (audit opinion) firms whose management discloses going concern-related issues in the 10-

K. This suggests that investors find the information to be useful in interpreting earnings even

though the information indicates that there was an initial assessment about substantial doubt. One

potential explanation is the usefulness of information about management’s plans. ASU 2014-15

requires management to disclose plans that alleviate the initial substantial doubt about going

concern. The FASB asserts that information about management’s plans could give financial

statement users the opportunity to “evaluate the likely success of those plans in mitigating the

conditions or events that raised substantial doubt” (FASB 2014, BC36). The increase in ERC we

note above seems to support this conjecture.

In our second research question, we examine whether auditors change their going

concern reporting strategy after the adoption of ASU 2014-15. Following Francis and Krishnan

(2002) and Geiger, Raghunandan, and Rama (2005), we decompose the change in probability of

issuing a going concern opinion from the PRE to POST periods into two components: the change

attributable to auditors’ reporting strategy and change attributable to client risk characteristics.4

We find an average increase of 1.22% in the probability of auditors’ issuance of a going concern

report. However, we are interested in whether auditors’ reporting strategy changed from the PRE

to POST periods. Decomposition of the overall change in probability into its two components

4 This methodology (i.e., the decomposition of a change in probability into components) is drawn from studies in labor economics (e.g., Farber 1990).

7

reveals that there is a 0.16% increase on average due to change in auditors’ reporting strategy,

after controlling for changes in client characteristics. This suggests that auditors became more

conservative in issuing a going concern report.5 Moreover, the number is economically

significant, given a going concern rate of 5.5% in the PRE period. Interestingly, this increased

conservatism is more marked for firms with no management assertions about going concern

issues. We offer two explanations for this increased conservatism: (a) auditors face more scrutiny

from regulators and more attention from financial statement users in the first year of adoption of

the standard, and (b) auditors have less pressure to avoid issuing a going concern opinion to keep

the client when management is also responsible for going concern disclosures.

Overall, we conclude that ASU 2014-15 increased the informativeness of reported

earnings but also induced greater conservatism in auditors. The standard appears to have been

effective in the first year of adoption at least in terms of providing useful information to the

market. However, the change in auditor’s reporting strategy seems to be an unexpected

consequence of the new policy. At this point, it is unclear whether the increased conservatism of

auditors suggests more accurate going concern assessments or overly conservative decisions.

Our study makes the following contributions. First, we provide detailed descriptive

analyses of managements’ disclosure pursuant to the new standard. Second, we provide some

preliminary assessments of the impact of the standard. We contribute specifically to the debate

on the potential usefulness of mandating management going concern assessments by

documenting increase in earnings informativeness, and to the more general subject of the

5 This is based on the full sample of all firms. We also conduct a similar analysis for financially distressed firms. For the distressed sample, we find a 3.26% overall increase in the probability of issuance of a going concern opinion, 0.40% due to change in auditor reporting strategy and 2.86% due to change in client risk characteristics.

8

usefulness of FASB’s standards (Khan, Li, Rajgopal, and Venkatachalam 2017). Third, we

contribute to the literature on the auditor’s going concern decision (Mutchler, Hopwood and

McKeown 1997; Behn, Kaplan, and Krumwiede 2001; Myers, Schmidt, and Wilkins 2014) by

suggesting that the management’s disclosure may become an important input into the decision.

We note one caveat to our study. In 2015, the PCAOB introduced a new regulation

requiring auditors to disclose the names of engagement partners on audits in a new Form AP

(PCAOB’s Release No. 2015-008, PCAOB 2015). This rule became effective for audit reports

issued on or after January 31, 2017. The PCAOB expects these disclosures to increase

“transparency and accountability for key participants in the audit.” Because the timing of the

Form AP rule coincides with that of ASU 2014-15, we must consider its potential confounding

effects for our analyses. A priori it is not clear that the first-time partner disclosures could affect

overall investor perceptions about financial reporting. These disclosures are expected to become

useful over time as a partner’s past performance becomes available.6 It seems unlikely therefore

that our investor perception results are affected by the new partner disclosures. However, if the

expectation of disclosure of their names causes engagement partners to become conservative in

their going concern decisions, our conservatism results could reflect the joint effect of ASU

2014-15 and the Form AP disclosures. While we acknowledge this possibility, the differences in

our results for different types of management disclosures suggests that ASU 2014-15 has some

effects that are separate from those of Form AP.

The next section discusses background and hypotheses development. Sections 3 and 4

6 At the time of the release of the final rule, PCAOB Board member Jay Hanson remarked “… over time, coupled with information about the partners' experience and history, making [partner identity information] available to investors may incrementally increase their ability to make judgments about audit quality, and, by extension, the credibility of financial statements.”

9

present research design and results of our first and second research questions, respectively. Our

conclusions appear in section 5.

II. BACKGROUND AND HYPOTHESES DEVELOPMENT

The Auditor’s Going Concern Opinion

An auditor’s going concern opinion decision follows several steps. Auditing Standard

2415 (SAS No. 59 prior to reorganization by the PCAOB) requires auditors to first evaluate,

based on the audit procedures conducted during the audit, whether there is “substantial doubt”

about the client’s ability to continue as a “going concern” within a reasonable period not to

exceed one year from the date of the financial statements. The concern about substantial doubt

arises if the auditor identifies negative conditions and events (for example, work stoppages and

legal proceedings) which, when viewed in aggregate, raise the possibility that the client may not

survive beyond 12 months from the year end.7

If the evaluation suggests that there could be substantial doubt, the auditor obtains

management plans to address the doubts about survival. If, again in the auditor’s assessment, the

management’s stated plans can be effectively implemented and might alleviate the concerns

about substantial doubt, the auditor would not issue a going concern modified opinion, but

“should consider the need for disclosure of the principal conditions and events that initially

caused him to believe there was substantial doubt” (AS 2415). In practice, auditors have not

typically included disclosures when not issuing an AGC. In the absence of such perceived

alleviation, the auditor issues a going concern modified opinion, which is an audit report

7 See Carson, Fargher, Geiger, Lennox, Raghunandan, and Willekens (2013) for a research synthesis of going concern literature.

10

including an explanatory paragraph, containing the phrases that includes the terms "substantial

doubt” and “going concern.”

Management’s Responsibility to Assess Going Concern Status

In 2014, the FASB instituted ASU 2014-15. This new standard was a culmination of

repeated attempts by the FASB to include “guidance on the preparation of financial statements as

a going concern and on management’s responsibility to evaluate and disclose uncertainties about

an entity’s ability to continue as a going concern” in US GAAP (FASB 2014). The ASU 2014-15

requirements, while generally similar to the requirements in the auditing standard for the AGC,

nevertheless have some new features. ASU 2014-15 requires management to consider whether

there is substantial doubt about survival and, if the initial assessment suggests the possibility of

substantial doubt, to assess if management plans could be implemented effectively and could

alleviate the substantial doubt. While this is similar to the auditing standards, there are two

important differences. First, the period for the assessment is 12 months beyond the date of

issuance, or date available for issuance, of the financial statements. This is longer than the

auditor’s look-forward period, 12 months beyond the balance sheet date. Second, the auditing

standard does not have a clear definition of substantial doubt. ASU 2014-15 states that

substantial doubt exists when “it is probable that an entity will be unable to meet its obligations

as they become due within one year after the date that the financial statements are issued” (FASB

2014; Booker and Booker 2016). The definition of “probable” (i.e., a future event is likely to

occur) is intended to be consistent with ASC 450, Contingencies.

If the plans are determined to not alleviate the substantial doubt, management must

disclose that there is substantial doubt about survival, its evaluation about conditions and plans,

and whether financial statements are prepared on a going concern basis (FASB 2014). However,

11

even if the plans are determined to alleviate substantial doubt, ASU 2014-15 requires extensive

disclosures that are not required for the auditor: the principal conditions or events that raised

substantial doubt, management’s evaluation of the significance of those conditions or events in

relation to the entity’s ability to meet its obligations, and the plans that are expected to alleviate

the doubt.

Investors’ Response to the New Standard

Because ASU 2014-15 is a FASB standard, its direct target is financial reporting quality

and not audit quality. FASB standards have the general goal of improving “financial accounting

and reporting standards to provide useful information to investors and other users of financial

reports.” Specifically, for ASU 2014-15, the goal is to improve financial reporting quality by

ensuring that the entity’s adoption of the going concern presumption is appropriate, and that

appropriate disclosures about going concern issues are provided.

Although a majority of the attention on the standard has focused on the disclosures by

entities with substantial doubt concerns, the standard applies to all entities. In its discussion of

the standard, the FASB describes two benefits for all entities. First, the standard describes

management’s responsibility to evaluate and disclose “uncertainties about an entity’s ability to

continue as a going concern,” which is a critical presumption for preparing financial statements

under GAAP for all entities. Second, by providing a definition for “substantial doubt,” the

standard is expected to reduce diversity in the “timing and content of existing footnote

disclosures for all entities.” Although viewed as a cost of implementing the standard, the Board

also expects that, because of the significant judgments involved in the evaluation, entities may

12

need to implement and document underlying processes and controls.8 This too can add to the

effectiveness of management assessments of going concern.

Thus, financial reporting quality can improve for all entities because their management

has systematically evaluated the going concern presumption, possibly instituting new controls,

procedures and monitoring.9 Although the FASB does not discuss implications for auditing,

comments on the ASU 2014-15 exposure draft suggest that an additional layer of rigor can also

occur because the auditor must in turn audit these changes to the reporting process and footnote

disclosures. Further, although auditors are not required to audit the MD&A, they must read the

new information arising from the standard, to ensure consistency with the information in the

financial statements (Cohen, Gaynor, Holder-Webb, Montague 2008).

We examine whether the market perceives an improvement in financial reporting quality,

thus responding more positively to earnings surprises in the POST period compared with the

PRE period. Earnings reports are valued by investors when the reported numbers “more

accurately reflect true economic value” (Teoh and Wong 1993). Other things equal, the earnings

response coefficient, is positively associated with the precision in the earnings number

(Holthausen and Verrecchia 1988). Thus, financial reporting changes that can be expected to

signal greater precision in the earnings number can increase the earnings response coefficient

8 The accounting firm Ernst & Young notes that, management will need to “evaluate whether it has adequate processes and internal controls in place to comply with the going concern requirements” (EY 2017). 9 Some commenters provided similar views. For example, “… we support the proposed amendments and believe that they will improve the quality of financial reporting about going concern matters. As a result, we believe users of financial statements will have access to more timely and decision-useful information” (BDO). “… we believe the users of financial statements will be provided a clearer understanding of the events or conditions that may impact an entity’s ability to continue as a going concern as well as management’s plans to mitigate those conditions and events at an earlier stage than under the current auditor driven model” (McGladrey).

13

(Teoh and Wong 1993; Hackenbrack and Hogan 2002). Hackenbrack and Hogan (2002) argue,

for example, that certain types of auditor changes can signal greater precision, engendering a

higher ERC after the auditor change. Similarly, Chen, Krishnan, Sami, and Zhou (2013) find that

there was an increase in ERC in the first year of implementation of internal control audits for

firms that did not have internal control material weaknesses. The inference is that the market

perceived the internal control audits as having improved the quality of financial information

presented by the firm. The critical question is whether investors perceive ASU 2014-15 as

generating a higher quality of information. We distinguish between firms that receive AGCs and

clean opinions from their auditors.

AGC Firms

For AGC firms, the auditor follows auditing standards to conclude that there is

substantial doubt about survivability that is not alleviated by management plans. Management is

required by Securities and Exchange Commission (SEC) rules, but not (prior to ASU 2014-15)

by the FASB, to provide disclosures when the auditor issues an AGC.10 The filings including the

AGC should also include “appropriate and prominent disclosure of the financial difficulties

giving rise to that uncertainty” and a discussion of a viable plan that has the “capability of

removing the threat to the continuation of the business” and can “enable the issuer to remain

viable for at least the 12 months following the date of the financial statements being reported on

must be included” (SEC 2017). The FASB believes that the lack of guidance in GAAP led to

10 The SEC’s Financial Reporting Manual (SEC 2017) states the following: “Filings that include reports having going concern modifications must also include appropriate and prominent disclosure of the financial difficulties giving rise to that uncertainty. Discussion of a viable plan that has the capability of removing the threat to the continuation of the business must be included. The plan may include a “best efforts” offering so long as the amount of minimum proceeds necessary to remove the threat is disclosed. The plan should enable the issuer to remain viable for at least the 12 months following the date of the financial statements being reported on.”

14

considerable diversity in whether, when, and how an entity discloses the relevant conditions and

events in its footnotes.

As discussed, ASU 2014-15 provides more detailed guidance than the SEC about firm

disclosures. Thus any change in investors’ perceptions due to the new standard depends on

whether it provides new information in the first year compared with the previous year. The

FASB notes that the new standard may not “result in new information in many audited financial

statements because the amendments are similar to current U.S. auditing standards” (emphasis

added). This may be particularly true for AGC firms because of the SEC-mandated disclosures

discussed above which were in place in the pre-ASU 2014-15 period. Effectively, the ERC for

the PRE period is based on the AGC and SEC-mandated disclosures, while the ERC in the POST

period is based on the AGC, the SEC-mandated disclosures, and any new disclosures arising

from ASU 2014-15. Because of the existence of some mandated disclosures in the PRE period,

we state our first hypothesis in null form:

H1: ERCs for firms with going concern opinions will not be different in the first post-ASU2014-15 year from that in the previous year.

Non-AGC Firms

For the clean opinion firms, the absence of an AGC in the PRE period provided assurance

of the absence of going concern problems. Under ASU 2014-15, investors have, in addition,

management’s proactive assessment of going concern, possibly after institution of

processes/controls to facilitate this assessment. Such assessment provides an increase in

information which may be viewed positively because it reduces information asymmetry. If so,

the ERC can increase in the post-ASU 2014-15 year. However, the content of the information

15

can also influence investor response. Consequently, we develop two hypotheses below for firms

with clean audit opinions.

ASU 2014-15 requires detailed disclosures when the initial assessment raises concern

about substantial doubt that are subsequently found to be alleviated by management plans. As we

discuss in the next section, the non-AGC companies fall into two broad categories, those that (1)

have no going concern disclosures or state explicitly that they have no going concern issues and

(2) describe the nature of the substantial doubt, management plans, and the basis for judging that

the substantial doubt is alleviated. In contrast, clean companies in the PRE period were not

required to make any disclosures. Consequently, there were relatively few voluntary disclosures

by clean companies regarding going concern issues in the PRE period.

For group (1), investors are essentially provided a double assurance in the POST period

that the firm is “clean” because the auditor did not issue a going concern opinion and the

management confirms the absence of going concern issues in the near future. In contrast, only

the auditor provided the assurance in the PRE period. Therefore, we posit that investors are more

confident that clean firms are in fact free of going concern uncertainties. The double assurance

can increase the precision of the earnings number (Teoh and Wong 1993). As a result, we expect

the earnings of these clean firms to be more informative in the POST period. Our second

hypothesis is as follows:

H2: ERCs for firms with no auditor going concern opinions and with no negative management disclosures regarding going concern will be higher in the first post-ASU 2014-15 year than in the previous year.

We acknowledge however that there are counter arguments. First, the evaluation of

whether there is substantial doubt involves significant judgement because it is based on

qualitative and quantitative factors. Thus managers may not disclose going concern issues

16

because they regard a potentially significant problem as not significant. Second, managers have

incentives to hide or delay bad news due to career concerns (Kothari, Leone, and Wasley 2005).

For example, the empirical evidence from Canada and U.K., where management is required to

disclose going concern issues, indicates that the proportion of firms that report going concern

uncertainties is quite small, and the information disclosed by the management is not

incrementally useful (Uang et al. 2006; Ontario Securities Commission 2010). If the market

considers it likely that firms would not disclose all the relevant information even when required

to do so, the new policy may not change the market’s perception of earnings informativeness,

and there would be no change in ERC in the POST period. Third, the threshold requiring the

disclosure about going concern uncertainty only when it is probable (i.e., the future event or

events is likely to occur) may be too high to reveal any new information about the uncertainty as

investors are likely to have already known about it.11

For group (2) above, disclosures in the POST period provide information relating to

going concern problems. In the PRE period, investors knew only the outcome of the auditor’s

going concern evaluation process. If the auditor decided to not issue a going concern opinion

after incorporating management’s plans, investors simply saw the absence of a going concern

opinion without knowing the underlying contextual details, unless management provided

voluntary disclosures. Mayew et al. (2015) document that some firms discussed going concern

issues in their MD&As, and this disclosure has incremental predictive ability for bankruptcy

11 Board Member Thomas Linsmeier voted against the ASU 2014-15 proposal, arguing that “by requiring disclosure only when it is probable that an entity will be unable to meet its obligations as they become due within one year after the date the financial statements are issued (or available to be issued), the guidance in this Update will provide information about going concern uncertainties that is too late to be of significant benefit to users of financial statements” (FASB 2014).

17

even after controlling for the auditor opinion.12 Therefore, if firms have already disclosed

sufficient information in their MD&As or elsewhere in the 10-K, ASU 2014-15 may not provide

new information. However, the proportion of voluntary going concern disclosures in the MD&A

for clean companies in Mayew et al. (2015) is small. Because the disclosures are now mandatory

(rather than voluntary), and the new policy would likely have legal consequences if management

does not comply with it, it is reasonable to expect that firms are more likely to disclose going

concern information in the POST period than in the PRE period.

Even if management’s disclosures provide new information, the “bad news” nature of

these disclosures might lower ERC. For example, Choi and Jeter (1992) and Dong, Robinson,

and Robinson (2015) document lower ERCs for firms with qualified/going concern audit

opinions. Therefore, although we expect the new policy to provide new information to the

market, whether this information would change market’s valuation of non-AGC firms’ earnings

is an empirical question. Accordingly, our third hypothesis is in null form:

H3: For the firms whose managements discuss going concern issues when the auditor does not issue a going concern opinion, there is no change in ERCs in the first post-ASU2014-15 year from the previous year.

Auditors’ Response to the New Standard

The auditor’s going concern opinion decision is complex, and characterized by grey areas

requiring judgment (Carcello and Neal 2000; Goh, Krishnan, and Li 2013; Carson et al. 2013).

Specifically, auditors can be viewed as determining a range of financial distress over which an

AGC can be issued, and choosing a “threshold” above which to issue it. Researchers have argued

12 Specifically, the proportion of voluntary disclosures in Mayew et al. (2015) is only about 0.2 percent when the auditor does not issue a going concern opinion. In our sample, 2.6% of firms with no AGCs in the POST period disclosed going concern issues.

18

that, given the judgement needed in the process, auditors may move the threshold in response to

different factors. Lowering (raising) the threshold would result in a higher (lower) probability of

issuing a going concern opinion, other things equal. Francis and Krishnan (1999) argue that

uncertainties relating to estimating accruals causes a lowering of the threshold engendering

“reporting conservatism.” Similarly, Goh et al. (2013) argue that the existence of internal control

material weaknesses increases the auditor’s uncertainty surrounding the substantial doubt

assessment, causing it to lower its threshold for the going concern opinion, other things equal.

Blay (2010) argues that the fear of losing a client, other things equal, makes the auditor less

conservative. In addition to responding to uncertainties surrounding the required assessments,

auditors may also move the threshold in response to regulatory changes. For example, the

passage of the Private Securities Litigation Reform Act of 1995 relieved litigation pressure on

auditors, possibly making them less conservative than before (Francis and Krishnan 2002;

Geiger and Raghunandan 2002).

Prior to ASU 2014-15, management plans were incorporated in the auditor’s going

concern decision, but the plans were proffered to the auditor in response to the latter’s expressed

concerns about substantial doubt. The important question is whether the active role forced on

management by the new standard is likely to affect the auditor’s going concern opinion decision.

We posit that several forces may be at work. First, auditors are aware that management must

assess its going concern status, and report it. This can result in greater faith in the information

provided by management, thus moving the threshold to the right (i.e., less conservatism).

Second, auditors will face more scrutiny from regulators (i.e., SEC, PCAOB) and more attention

from the financial statement users in the first year of adoption of a new standard. It is likely that

standard setters will pay more attention to going concern assessments to evaluate the efficacy of

19

the standard and to ensure that firms are applying the new standard appropriately. Such

heightened scrutiny could cause auditors to become more conservative. Further, some

commenters responding to 2013 exposure draft expressed the concern that the new management

disclosures can increase auditors’ litigation exposure. Third, we conjecture that auditors now

have less pressure to avoid issuing a going concern opinion for fear of losing the client because

managements are also responsible for disclosing going concern issues. That is, auditors that may

have delayed disclosing bad news (i.e., issuing a going concern opinion) to please the client

would feel free to issue a going concern opinion without worrying about losing the client

particularly if the client is forced to disclose problems on its own. This would increase reporting

conservatism.

Given the conflicting predictions, we state our fourth hypothesis in the null form.

H4: After controlling for change in client characteristics, auditors’ reporting conservatism is not different in the first post-ASU2014-15 year compared with the previous year.

III. INVESTOR PERCEPTIONS IN THE PRE- AND POST-PERIODS

Management Disclosures pertaining to Going Concern

ASU 2014-15 became effective for fiscal years ending after December 15, 2016, and for

annual periods and interim periods thereafter. We assemble a sample of PRE and POST firm-

year observations using December 15, 2016 as the cutoff. Because of the fairly intense data

coding that is required, we confine our sample to observations that were available on the date

that we started the process, July 1, 2017. We started with all observations that were available for

year ends from November 1, 2015 to January 31, 2017. Fiscal years ending between November

1, 2015 and December 15, 2016 comprise the PRE period, and fiscal years ending between

December 16, 2016 and January 31, 2017 comprise the POST period.

20

Table 1 presents our sample selection procedure. We start with 12,282 firm-year

observations available in Audit Analytics for the PRE and POST periods. We then eliminate (1)

1,419 observations that relate to funds or trusts, use non-U.S. GAAP, or have missing SIC Codes

and (2) 6,252 observations due to unavailability of data on Compustat, CRSP, and/or IBES. This

results in 4,611 firm-year observations comprising 2,328 observations for the PRE period and

2,283 observations for the POST period.

Next, we hand-collected data on management disclosures about going concern from 10-K

filings for every firm-year in the sample. While the POST period had mandatory disclosure

requirements, Mayew et al. (2015) document that managers provided voluntary disclosures

relating to going concern (during 1995-2012) in the MD&A sections of their Form 10-K filings.

Because our empirical models are intended to capture changes in investor perceptions from the

PRE to the POST periods, we examine 10-K filings in both periods to document the disclosures.

Using Python, we conducted keyword searches for phrases such as “substantial doubt” and

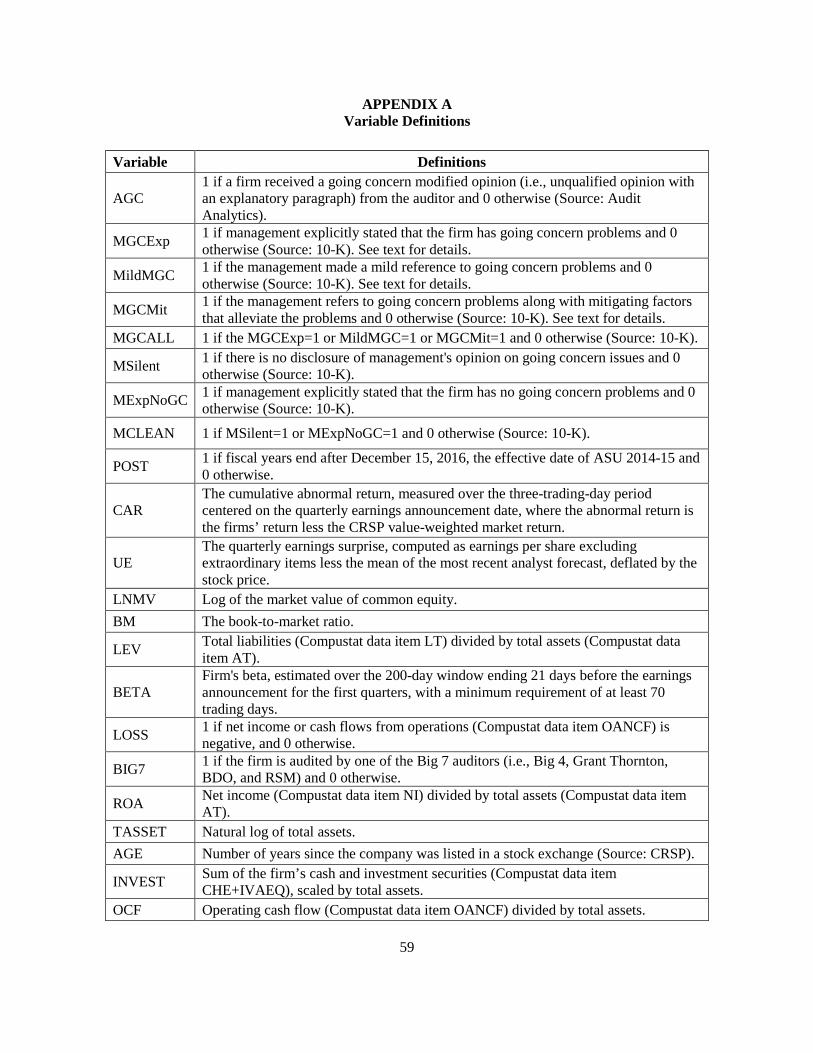

“going concern.”13 We classified the observations into five groups, those with (1) explicit

statements that they had no GC issues (MExpNoGC), (2) no explicit statement about the

presence or absence of going concern issues, which we interpret as indicating the absence of GC

issues (MSilent)14, (3) “mild” suggestions of GC problems (MildMGC), (4) discussions about

13 Two authors were involved in coding the disclosures. We read each paragraph that contained the phrase “going concern.” Many of these paragraphs did not in fact pertain to going concern problems. For example, many companies use the phrase “going concern” when referring to the new standard. Consequently, a large number of “going concern” phrases were eventually not used in the coding of going concern assessments by management. Where there were differences between the authors in coding, they were reconciled through discussion. 14 A number of firms mention ASU 2014-15 and state that its adoption had no material effect on their financial statements. Since this is not an explicit statement about the absence or presence of going concern issues, we code these observations as silent.

21

GC concerns and mitigating factors (MGCMit) that alleviate the substantial doubt, and (5)

explicit statements about substantial doubt relating to going concern (MGCExp).15 A “mild”

suggestion of GC arises when a firm uses modal words (e.g., “may” or “could”) or conditional

sentences in stating its going concern issues.16

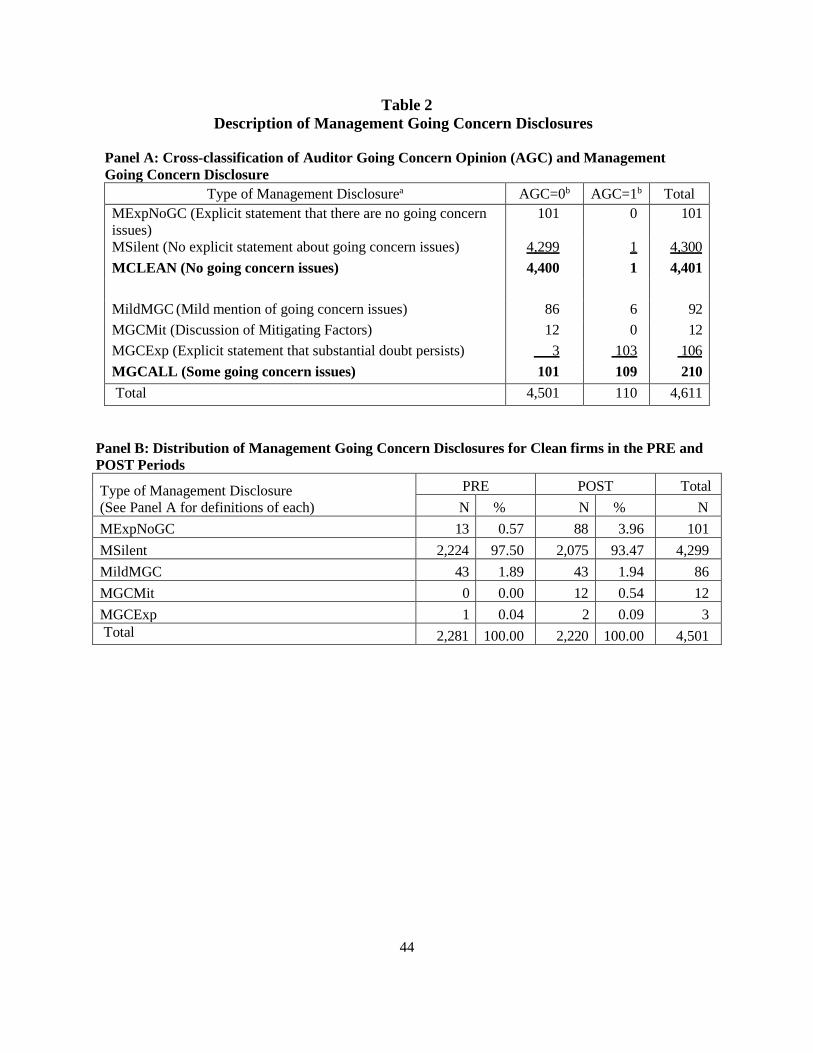

Table 2, Panel A shows the frequency of the management disclosure groups, cross-

classified by AGC, for the combined sample of PRE and POST period firm-years. Not

surprisingly, managements’ explicit statements about substantial doubt overlaps almost

completely with auditors’ issuance of AGCs. Of the 110 firms with auditors’ AGCs, the

management of 103 firms also explicitly acknowledge going concern problems. Of the remaining

seven firms, six acknowledge going concern issues somewhat mildly (MildMGC) and one

(which belongs to the PRE period) had no comments about going concern (MSilent).

Among the 4,501 clean firm-year observations that did not receive an auditor’s going

concern opinion, managements’ disclosures vary. A majority (4,299) of them fall in the

“MSilent” group, and 101 firms belong to the MExpNoGC group, stating explicitly that the firm

has no going concern issues. We find 86 firms with mild acknowledgment of going concern

15 MGCExp firms: “These raise substantial doubt regarding our ability to continue as a going concern”; “There is substantial doubt about its ability to continue as a going concern.” The structure and content of going concern statement made by the management is almost identical to the going concern statements included in the auditor’s report. 16 Some examples of MildGC: “If the condition were to persist for any appreciable period of time, our viability as a going concern could be threatened.”; “Our ability to continue as a going concern is dependent upon our ability to obtain additional equity or debt financing.”

22

problems, and 12 firms disclosing going concern problems but with mitigating plans to alleviate

the problems.17 Three explicitly mention going concern problems.18

In Table 2, Panel B, we focus on clean firms, (AGC=0) and present the distribution of

management going concern disclosures for the PRE and POST periods separately. Although the

individual numbers are small, the changes from the PRE to POST years reflect the effect of the

new standard. First, the MSilent category decreased from 97.5% to 93.5%.19 Although this

category dominates in both years, the introduction of ASU 2014-15 provides a different

interpretation for MSilent in the PRE and POST periods. In the PRE period, investors were not

able to draw any inferences from the lack of disclosure about the going concern issues in the 10-

Ks. In the POST period, however, management is required to assess going concern and disclose

where needed. Thus, no disclosure in the POST period actively implies the absence, in

management’s judgment, of going concern issues.

Second, although the number of observations with any kind of management going

concern disclosure is not large, the standard elicited specific statements, for example about the

17 ASU 2014-15 says: “If, after considering management’s plans, substantial doubt is alleviated as a result of management’s plans, management must disclose conditions that raised substantial doubt as well as management’s plans that alleviated substantial doubt in the footnotes” (205-40-50-12); “If, after considering management’s plans, substantial doubt is not alleviated, management must include a statement in the footnotes indicating that there is substantial doubt about the entity’s ability to continue as a going concern” (205-40-50-13). Therefore, some firms may have mitigating plans which are not sufficient enough to alleviate adverse conditions and thus still state going concern problems. These firms will fall within the MGCExp group rather than within “MGC with Mitigating Factors.” 18 The three firms include the following sentences in their 10-Ks: (1) “Our recurring losses from operations have raised substantial doubt regarding our ability to continue as a going concern”; (2) “our planned operations raise doubt about our ability to continue as a going concern”; (3) “the company’s planned operations raise doubt about its ability to continue as a going concern.” 19 We considered whether the observations including some form of going concern disclosures were the result of early adoption of the standard. Five firms mention that they adopt the standard early. Others made no mention of early adoption of the standard, making it likely that they are voluntary disclosures.

23

absence of going concern issues, or about management plans and mitigating factors, which were

not available in the PRE period. Overall, these specific disclosures increased from 2.5% to 6.5%.

The proportion of firms explicitly stating the absence of going concern increased from 0.57% to

3.96%, and the proportion of firms explicitly disclosing some going concern issues (mild, with

mitigation, or unalleviated substantial doubt) increased from 1.93% in the PRE period to 2.57%

in the POST period. The proportion of disclosures for “MGC with mitigating factors” (MGCMit)

increased significantly after ASU 2014-15 became effective (from 0 to 0.54%), and we

conjecture that this is a major change introduced by the new policy.20 Unfortunately, the small

number of observations restricts our ability to conduct meaningful statistical tests for each

category. Consequently, in the regressions reported later, we combine these three groups into one

group (MGCALL).

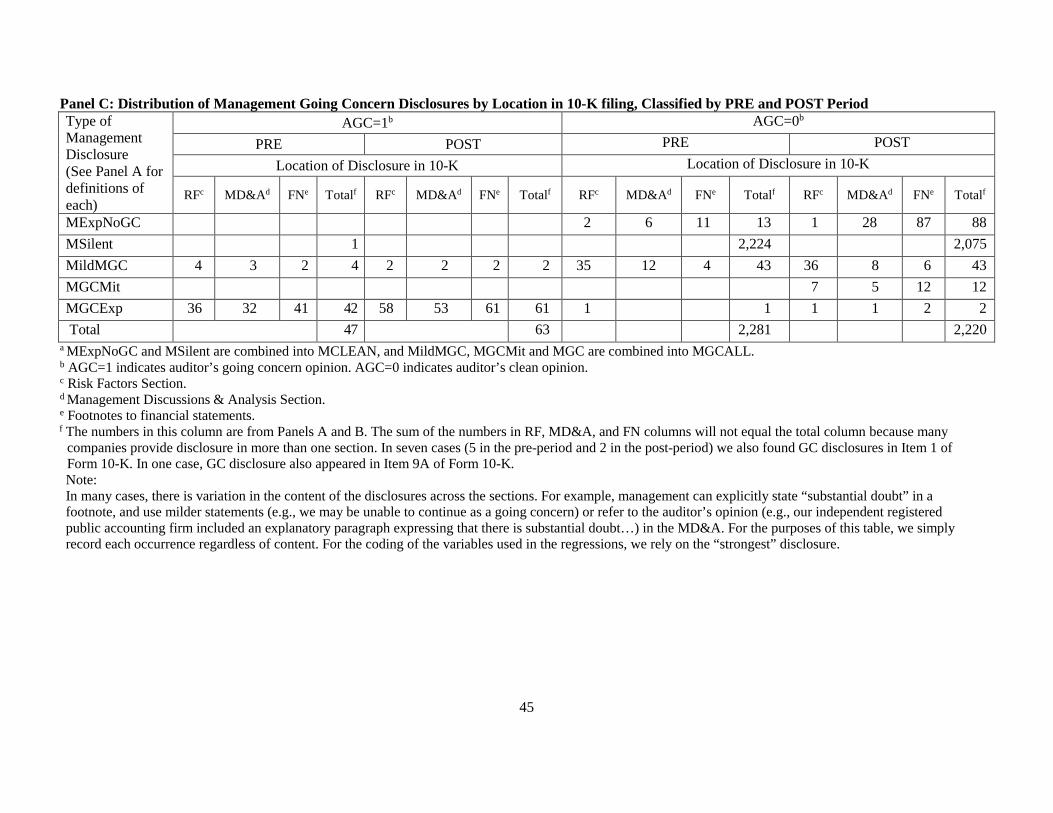

Location of Disclosure

ASU 2014-15 requires disclosure about going concern problems in the footnotes.

However, information about going concern issues also appear in other sections of Form 10-K,

especially in the Risk Factors and MD&A sections.21 Table 2, Panel C provides information

about the location of the disclosures. For the companies with auditor going concern opinion

20 The Sears example discussed earlier falls in the “MGC with Mitigating Factors” (MGCMit) group. “…We believe that the actions discussed above are probable of occurring and mitigating the substantial doubt raised by our historical operating results and satisfying our estimated liquidity needs 12 months from the issuance of the financial statements.” Sears’ auditor, Deloitte, did not issue an AGC, possibly because the substantial doubt was alleviated. Thus, management disclosure provides additional information to investors. 21 The FASB included question 7 in its 2013 exposure draft for ASU 2014-15, specifically seeking comments about the location of the disclosures in the 10-K: “For SEC registrants, would the proposed footnote disclosure requirements about going concern uncertainties have an effect on the timing, content, or communicative value of related disclosures about matters affecting an entity’s going concern assessment in other parts of its public filings with the SEC (such as risk factors and MD&A)? Please explain.”

24

(AGC=1), footnote disclosures dominate in both periods (91.5% and 100% in the PRE and

POST periods respectively) possibly because of the SEC requirement. However, among AGC=0

companies, there is a distinct increase in footnote disclosures in the POST period. Where

management explicitly states that there are no going concern problems, 84.6% of the disclosures

in the PRE period and 99% in the POST period appear in the footnotes. Among the clean

(AGC=0) companies with some going concern problems, 9.1% provide footnote disclosure in the

PRE period. The corresponding percentage for the POST period is 35.1%.

Empirical Model

We examine if the adoption of ASU 2014-15 enhanced investors’ perceptions about

financial reporting quality, leading them to re-evaluate the quality of reported earnings. We

estimate the earnings response coefficient (ERC), the market’s responsiveness to earnings

announcements by the slope coefficient in a regression of unexpected returns on unexpected

earnings (see for example, Balsam, Krishnan, and Yang 2003; Francis and Ke 2006; Baber,

Krishnan, and Zhang 2014).

The basic ERC model is as follows:

𝐶𝐶𝐶𝐶𝐶𝐶 = 𝛽𝛽0 + 𝛽𝛽1𝑈𝑈𝑈𝑈 + � 𝛽𝛽𝑘𝑘𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐7

𝑘𝑘=2+ � 𝛽𝛽𝑘𝑘 𝑈𝑈𝑈𝑈 ∗ 𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐

13

𝑘𝑘=8+ 𝜀𝜀 (1)

where CAR is the three-day cumulative abnormal return around the earnings announcement date,

and UE is a measure of earnings surprise.22 The earnings announcement date is for the first

quarter following the 10-K filing in which the management disclosures (voluntary in the PRE

period and mandatory in the POST period) are included. The parameter 𝛽𝛽1 is the coefficient of

22 We use an event study design with three-day cumulative returns rather than a long-term association study design because our goal is to investigate the information content of earnings announcement rather than value-relevance (Collins and Kothari 1989; Hackenbrack and Hogan 2002).

25

interest, namely the earnings response coefficient. CAR is computed as the common stock return

less the value-weighted market return summed over the three-day period centered on the

earnings announcement date UE is earnings per share less the most recent analyst forecast

deflated by the beginning stock price for the first quarter.

Earnings Responsiveness to Auditors’ Going Concern opinion in the PRE and POST Periods

In order to compare the ERCs of going concern firms and clean firms (hypotheses H1), we

extend the model to estimate ERC for each group:

𝐶𝐶𝐶𝐶𝐶𝐶 = 𝛼𝛼0 + 𝛼𝛼1𝑈𝑈𝑈𝑈 ∗ 𝐶𝐶𝐴𝐴𝐶𝐶 + 𝛼𝛼2𝑈𝑈𝑈𝑈 ∗ 𝐶𝐶𝐶𝐶𝑐𝑐𝐴𝐴𝐴𝐴𝑐𝑐 + � 𝛼𝛼𝑘𝑘𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐9

𝑘𝑘=3+ � 𝛼𝛼𝑘𝑘𝑈𝑈𝑈𝑈 ∗ 𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐

15

𝑘𝑘=10+ 𝜐𝜐 (2)

where AGC indicates firm-year observations with auditor going concern opinions. AClean

indicates firm-year observations that did not receive going concern opinions from the auditors.

Control variables are discussed below.

The coefficients 𝛼𝛼1 and 𝛼𝛼2 indicate the mean ERC for the AGC and AClean groups,

respectively. Since our goal is to compare ERCs for the PRE period and POST periods, we

estimate model (2) separately for the PRE and POST periods and examine differences in

coefficients between the two periods.23 Specifically, the difference in 𝛼𝛼1 between the PRE and

POST periods indicates whether the ERC for AGC firms change. Hypothesis H1 predicts no sign

for the difference in 𝛼𝛼1.

Next, to test hypotheses H2 and H3, we examine whether the ERC changes for firms with

different management going concern disclosures. We restrict this analysis to clean firms because,

as discussed, there is an almost-complete overlap between the auditor’s going concern opinion

and management’s substantial-doubt going concern disclosures. We use two types of

23 Thus the model allows all the coefficients to vary across the two periods.

26

classifications for management going concern disclosures for clean firms. First, we classify

management going concern disclosures into two groups: MCLEAN and MGCALL (see Table 2

Panel A). MCLEAN indicates that the management explicitly states that the firm does not have

going concern problems or that the management does not discuss going concern-related issues in

the 10-K. MGCALL indicates firms where the management discloses going concern issues

mildly, in conjunction with mitigating factors, or as an assertion that substantial doubt exists.

The corresponding ERC model is as follows:

𝐶𝐶𝐶𝐶𝐶𝐶 = 𝛿𝛿0 + 𝛿𝛿1𝑈𝑈𝑈𝑈 ∗ 𝑀𝑀𝐶𝐶𝑀𝑀𝑈𝑈𝐶𝐶𝑀𝑀 + 𝛿𝛿2𝑈𝑈𝑈𝑈 ∗ 𝑀𝑀𝐴𝐴𝐶𝐶𝐶𝐶𝑀𝑀𝑀𝑀 + � 𝛿𝛿𝑘𝑘𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐9

𝑘𝑘=3+ � 𝛿𝛿𝑘𝑘 𝑈𝑈𝑈𝑈 ∗ 𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐

15

𝑘𝑘=10+ € (3)

In model (3), 𝛿𝛿1 indicates the mean ERC for the MCLEAN group while 𝛿𝛿2 indicates the mean

ERC for the MGCALL group. As before, we run model (3) separately for the PRE and POST

periods and compare the coefficients on the two interaction terms between the two periods.

Hypothesis H2 predicts a higher 𝛿𝛿1 in the POST period compared with the PRE period, and

Hypothesis H3 yields no prediction for the direction of change in 𝛿𝛿2.

For our second classification, we separate the MCLEAN group into two subgroups,

MExpNoGC, the firms which state explicitly that they have no going concern issues, and

MSilent, the firms that have no going concern disclosures.24 The corresponding ERC model for a

three-way classification is as follows:

𝐶𝐶𝐶𝐶𝐶𝐶 = 𝛾𝛾0 + 𝛾𝛾1𝑈𝑈𝑈𝑈 ∗ 𝑀𝑀𝑈𝑈𝑀𝑀𝑀𝑀𝑀𝑀𝑐𝑐𝐴𝐴𝐶𝐶 + 𝛾𝛾2𝑈𝑈𝑈𝑈 ∗ 𝑀𝑀𝑀𝑀𝑀𝑀𝑐𝑐𝐴𝐴𝑐𝑐𝑐𝑐+𝛾𝛾3𝑈𝑈𝑈𝑈 ∗ 𝑀𝑀𝐴𝐴𝐶𝐶𝐶𝐶𝑀𝑀𝑀𝑀 + � 𝛾𝛾𝑘𝑘𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐11

𝑘𝑘=4

+ � 𝛾𝛾𝑘𝑘𝑈𝑈𝑈𝑈 ∗ 𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐𝑐17

𝑘𝑘=12+ 𝜉𝜉 (4)

24 These include firms that refer to the standard and state that its adoption had no material effects on their financial statements. We refer to them as “silent” to distinguish them from the firms that state explicitly that they do not have any going concern issues.

27

Similar to models (2) and (3), we run model (4) for the PRE and POST periods separately and

compare the ERCs of different management going concern disclosure groups for the two periods.

Based on previous studies, we include the following control variables in the model: book

to market ratio (BM) (Collins and Kothari 1989), firm size, measured by the logarithm of the

market value of common equity (LNMV), firm beta (BETA) to proxy for systematic risk (Baber

et al. 2014), leverage (LEV) measured by the debt to assets ratio (Easton and Zmijiewski 1989),

a dummy variable that indicates clients of large auditors (BIG7), and a dummy variable LOSS

(Hayn 1995; Hackenbrack and Hogan 2002) to indicate either a negative net income or negative

cash flows from operations. We include main effects for control variables and their interactions

with earnings surprise (UE) because the control variables can engender cross-sectional

variability in ERCs.

Empirical Results

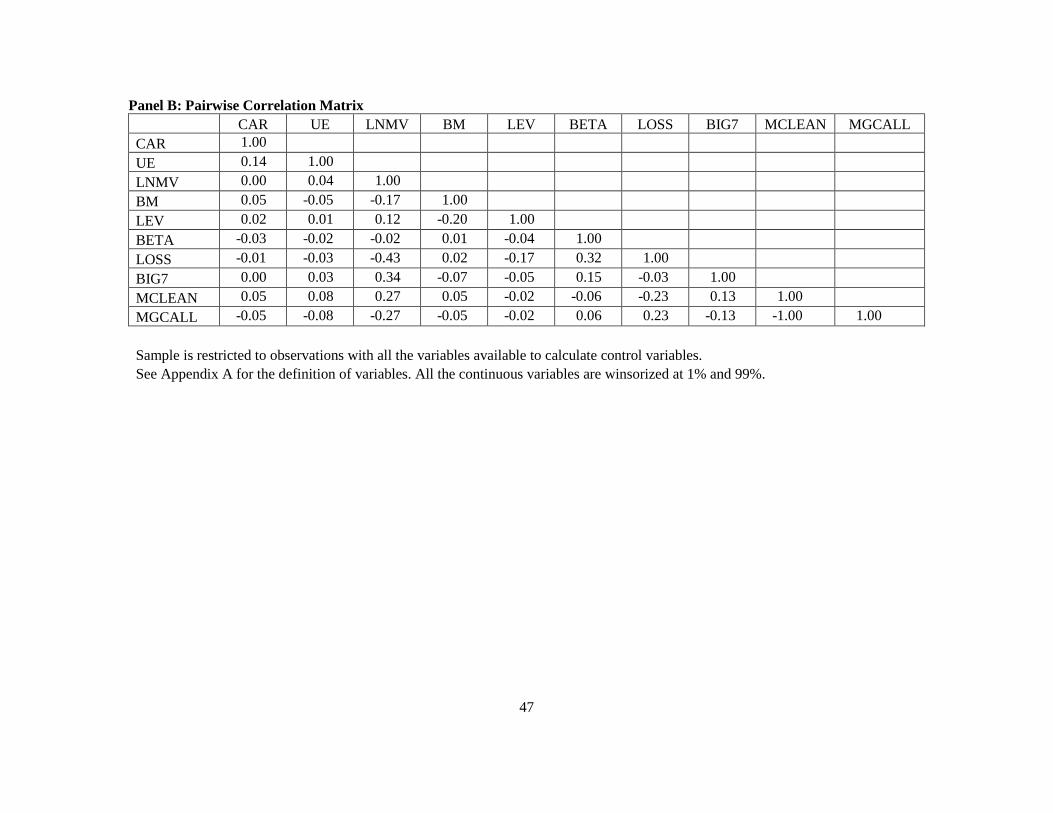

Table 3, Panel A provides descriptive statistics. All continuous variables are winsorized

at the 1 percent and 99 percent levels. Columns 1-2 report the means and medians for the PRE

sample and the POST sample respectively. Column 3 presents statistics for testing differences in

means and medians across the two periods. Our main variables of interest, CAR and UE, do not

show significant change from the PRE to POST periods. The means (medians) for firm size

(LNMV), leverage (LEV) and systematic risk (BETA) are higher in the POST period than in the

PRE period. The book to market ratio (BM) is lower in the POST period than in the PRE period.

Panel B of Table 3 presents pairwise Pearson correlations among the main variables. None of the

correlations exceeds 0.5 (or -0.5).

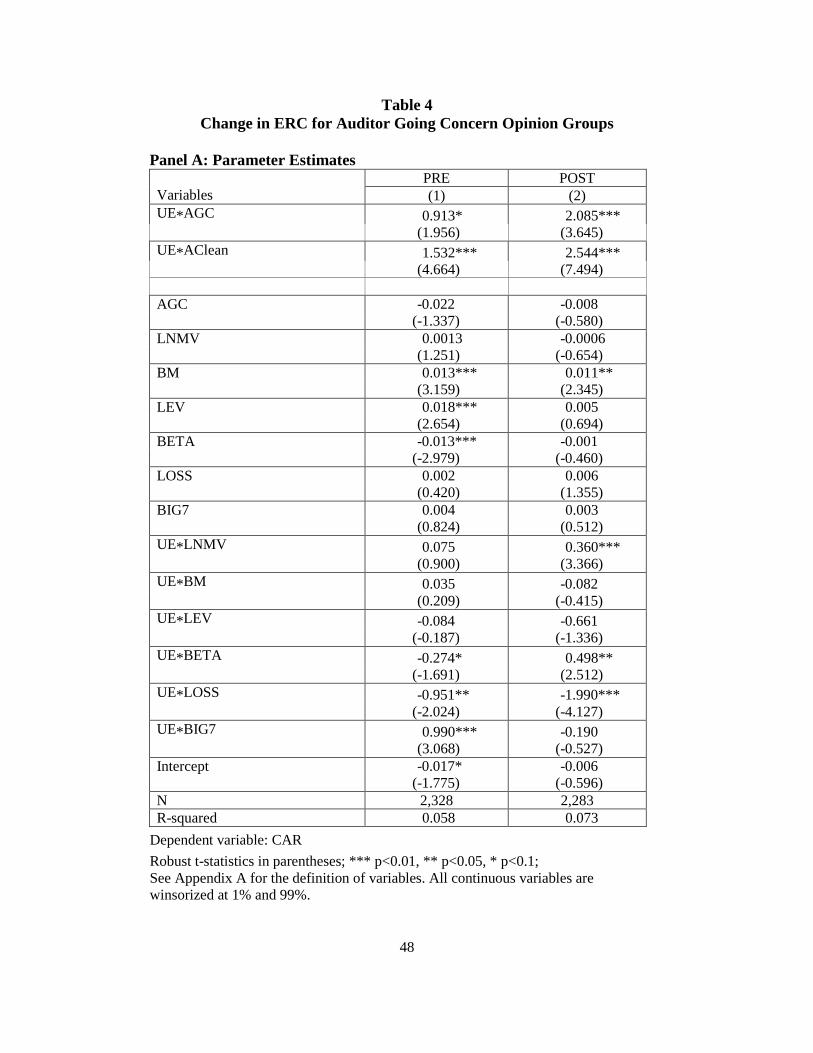

Table 4 reports the results of estimating equation (2) to examine changes in ERC between

the PRE and POST periods for the AGC and AClean firms. Panel A shows the regression

28

estimates, and Panel B shows the resulting (incremental) ERC estimates for subgroups, holding

all other variables constant. Columns (1) and (2) in Panel A show the model estimates for the

PRE and POST periods, respectively. In both periods and for both AGC and AClean firms, ERCs

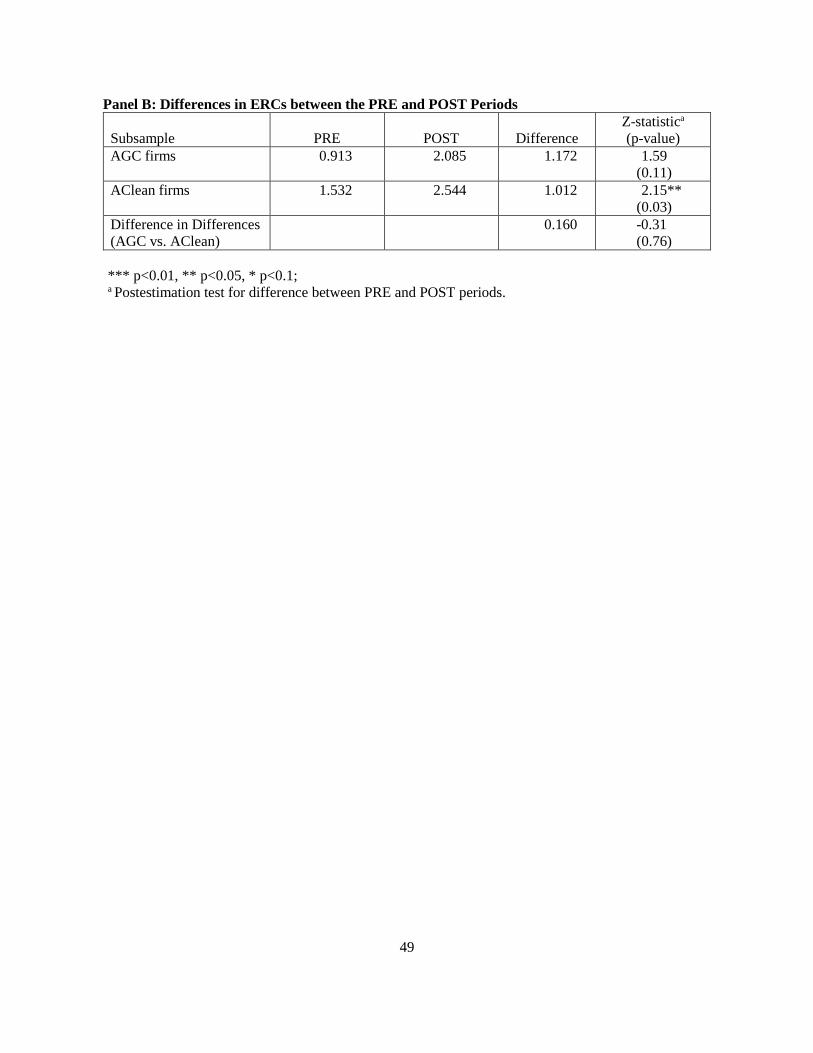

are positive and statistically significant.25 ERC for AGC firms increased from 0.913 to 2.085

between the PRE and the POST periods. As we show in Panel B, this increase is not statistically

significant at conventional levels (p-value 0.11). It seems therefore that the ASU 2014-15

management disclosures for AGC companies in the POST period does not add to the SEC-

mandated disclosures, that were provided in both periods, in influencing investor perceptions.

The ERC for AClean firms increased from 1.532 to 2.544 in the POST period. This

increase is statistically significant with p-value 0.03 (Panel B) indicating that the market

perceives earnings quality to be higher in the POST period than in the PRE period, for firms that

did not receive a going concern opinion from the auditor. However, the difference in the change

in ERC between AGC firms and AClean firms is not significant.26

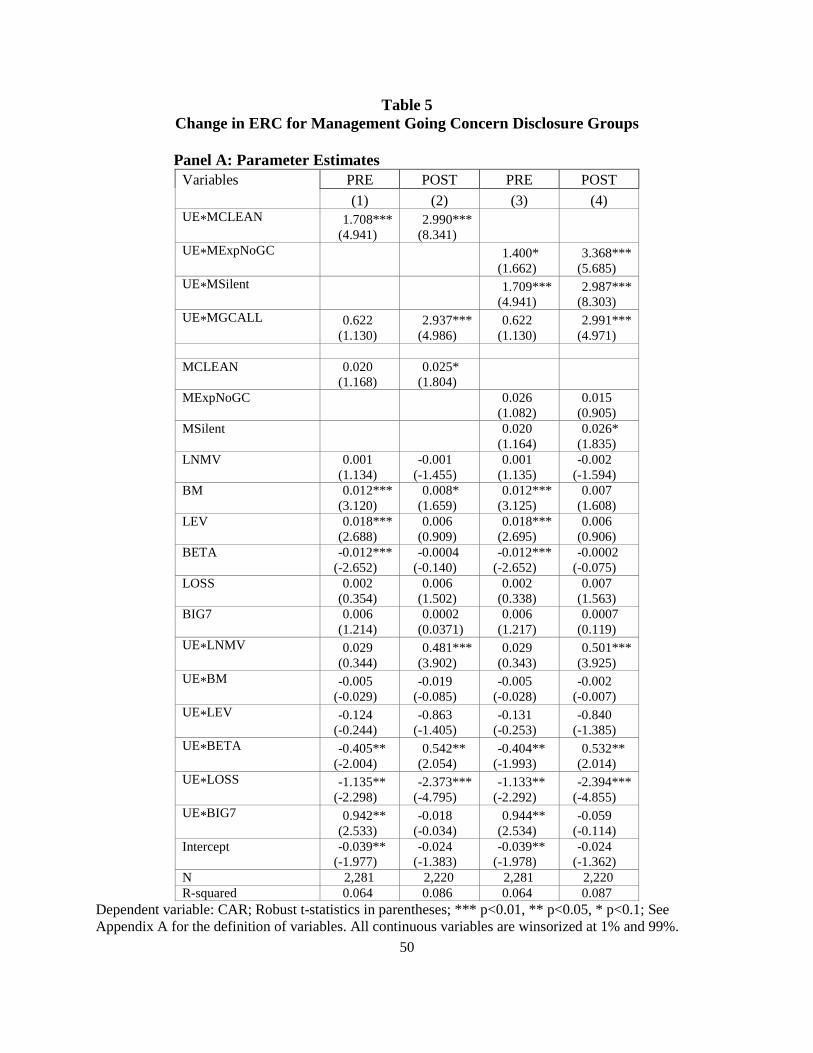

Next, we restrict our sample to clean firms that did not receive going concern opinions

from their auditors, and investigate changes in ERC for firms with different management going

concern disclosures. The results for estimating equations 3 and 4 are presented in Table 5 Panel

A, and the tests for differences in ERCs between groups are shown in Panel B. Columns 1-2 of

Table 5 panel A present results for the PRE and POST periods respectively, using a two-way

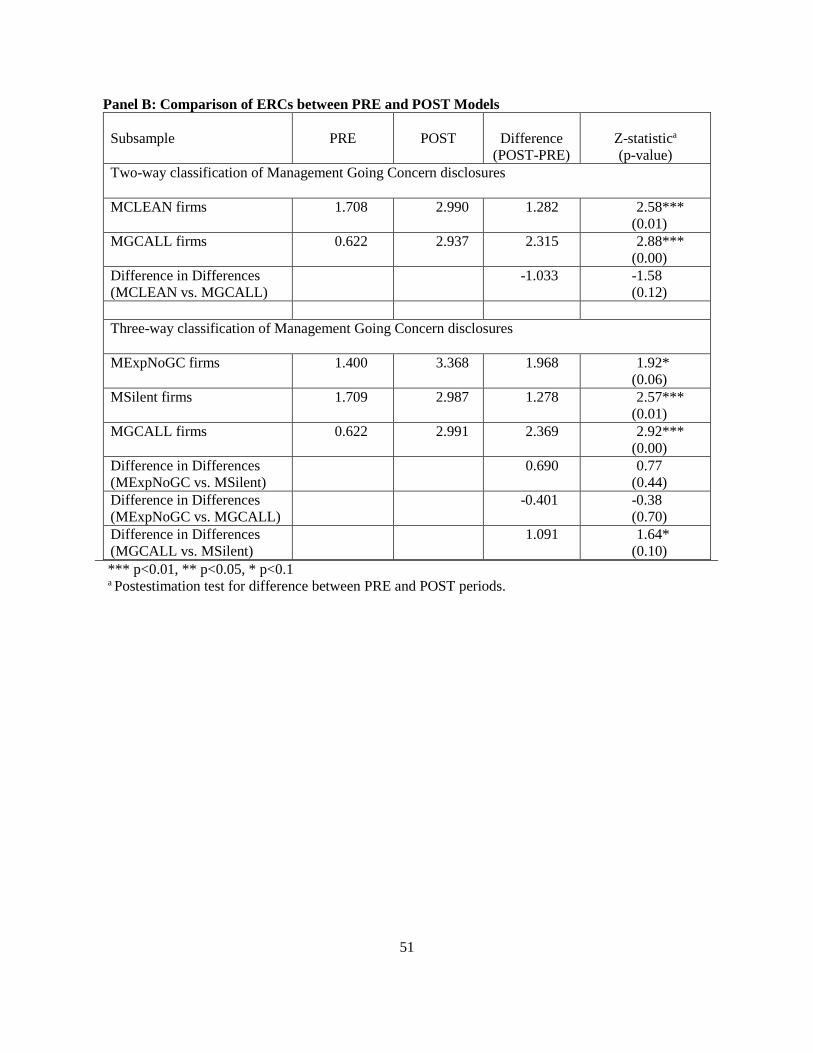

classification of management going concern disclosures. For the MCLEAN group (i.e., firms

with clean audit opinions as well as clean management assessments), the ERC increases,

25 The ERC for the AGC sample is smaller in magnitude than that for the AClean sample in both periods. F-tests indicate that the difference is significant (p-value=.08) for the PRE period but not for the POST period (p-value=.23). 26 We use the lincom command in STATA to examine linear combinations of the coefficient estimates.

29

consistent with H2, from 1.708 in the PRE period to 2.990 in the POST period. The increase in

ERC is statistically significant at the 1% level (Panel B). For the MGCALL group (i.e., firms

with clean audit opinions but with going concern disclosures by management), the ERC

increases from 0.622 in the PRE period to 2.937 in the POST period. Again, the increase is

statistically significant at the 1% level, as shown in Panel B. It seems therefore that, investors

value the increased information offered by these firms, possibly because it reduces asymmetric

information between investors and management, despite the potential negative news conveyed

by the revelation that management had considered the possibility of substantial doubt. The

magnitude of increases for the two groups is not different (p-value= 0.12 in Panel B).

Columns 3-4 in Table 5 Panel A shows the results when a three-way classification of

management going concern disclosures is used. The MCLEAN group is now decomposed into

those with explicit statements of no going concern issues (MExpNoGC) and those that have no

disclosures relating to going concern (MSilent). Tests of difference in ERCs between groups is

shown in Panel B. All three groups show statistically significant increases in ERC, suggesting

that investors value the increased information from the ASU 2014-15 disclosures for firms with

no AGCs. Interestingly, the magnitude of the increase is higher for the two groups with explicit

disclosures than for the silent group. Holding other things constant, the ERC increases by 2.369

and 1.968 respectively for groups with disclosures about going concern issues and explicit

disclosures about the absence of going concern issues. For the silent group, the ERC increases by

1.278. We also examined whether the magnitude of the increases in ERC differed across the

three groups. Pair-wise comparisons are shown in Panel B. The only significant difference is that

between the increase in ERC for the MSilent and MGCALL groups. We conclude that there is

some evidence that the new ASU 2014-15 disclosure are considered useful by investors.

30

In sum, our results indicate the following: (1) investors value the increased information

provided by ASU 2014-15 disclosures by firms without AGCs, but not for firms with AGCs and

(2) among the clean firms, the largest increase is for those that disclose going concern issues

mildly, in conjunction with mitigating factors, or as an assertion that substantial doubt exists.

IV. AUDITOR GOING CONCERN OPINIONS IN THE PRE- AND POST-PERIODS

Empirical Model

Our second research question (hypothesis H4) relates to auditor response to the new

standard. Following the methodology in Francis and Krishnan (2002) and Geiger et al. (2005),

we use coefficients from estimating AGC models to examine changes in conservatism from the

PRE to POST period.

The probability of a going concern audit report depends on client characteristics (X) and

the weight the auditor attaches to each characteristic (β). Specifically, the probability of a going

concern opinion for client i in year t can be described as:

P(𝐶𝐶𝐴𝐴𝐶𝐶𝑖𝑖𝑖𝑖 = 1)=F(𝑋𝑋𝑖𝑖𝑖𝑖 ∙ 𝛽𝛽𝑖𝑖) (5)

where F(∙) denotes the distribution function of a logistic model.

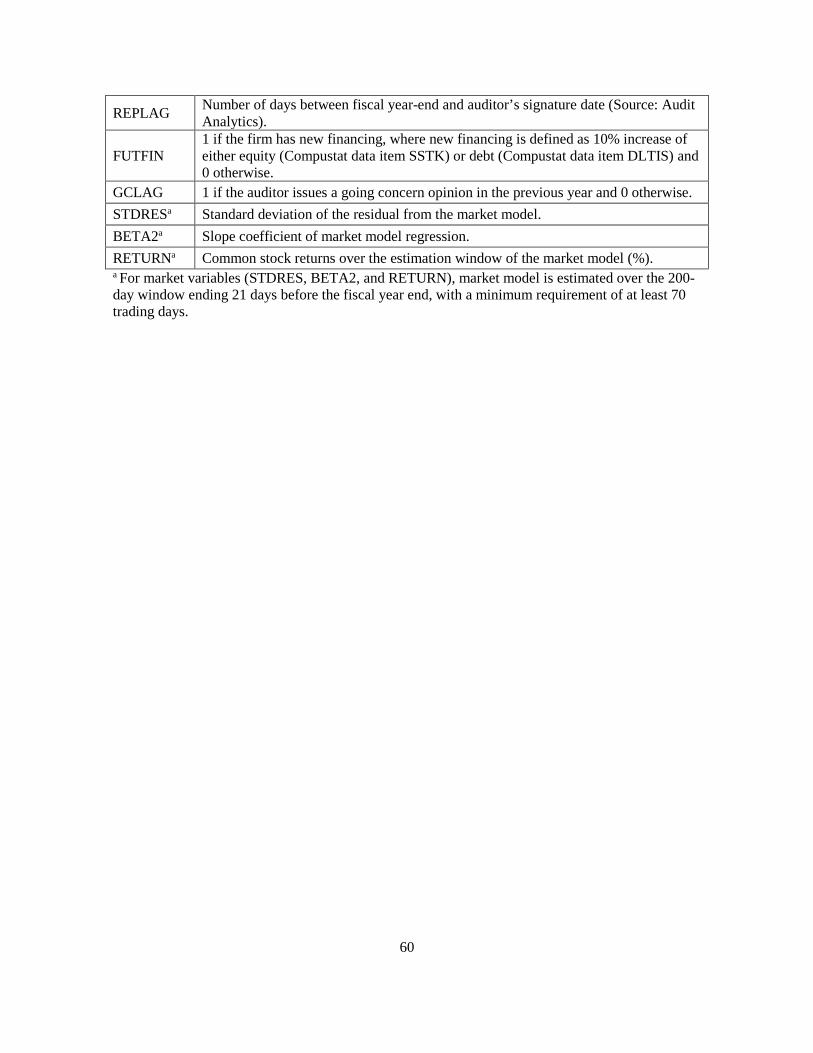

Following prior work, we include financial, market, and other variables in the X vector

(e.g., Francis and Krishnan 1999; DeFond et al. 2002). These variables could also proxy for

“contrary” and “mitigating” factors identified in AS 2415 (DeFond et al. 2002). We include firm

size (TASSET) because smaller firms are more likely than larger firms to receive AGCs. Several

variables capture financial distress: return on assets (ROA), leverage (LEV), and operating cash

flows (OCF). We include the number of years the company has been traded (AGE) as younger

firms are less likely to survive as a going concern (Dopuch, Holthausen, and Leftwich 1987). The

31

ratio of cash and short-term investments to total assets (INVEST) proxy for liquidity. To control

for a firm’s ability to raise funds in the near future, we include a new financing variable (FUTFIN).

We include three market variables, firm returns (RETURN), firm beta (BETA2) and standard

deviation of returns (STDRES), to capture firm performance, systematic risk and firm specific

risk, respectively. The market variables can capture information included in the footnotes and may

be correlated with the auditor’s private information set (Dopuch et al. 1987). We include the lag

between the fiscal year end and the audit report date (REPLAG) because companies that receive

AGC are associated with longer reporting lags (Carcello et al. 1995). Finally, we include the

previous year’s audit opinion, GCLAG, indicating a going concern opinion in the previous year

(Carcello and Neal 2000).

We estimate (5) separately for the PRE and POST periods. Using the estimated coefficients

(�̂�𝛽𝑖𝑖) from (5), we estimate the probability of issuance of a going concern opinion in each period.

The estimated change in predicted probability of a going concern opinion (Δ𝑃𝑃) is given by:

Δ𝑃𝑃 = 𝑃𝑃�𝑋𝑋𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃 , �̂�𝛽𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃� − 𝑃𝑃(𝑋𝑋𝑃𝑃𝑃𝑃𝑃𝑃 , �̂�𝛽𝑃𝑃𝑃𝑃𝑃𝑃) (6)

The change in the probability of issuing a going concern opinion can be due to (i) change in client

risk characteristics (X) or (ii) change in auditors’ reporting strategy which would be reflected in

β. Following Francis and Krishnan (2002), we decompose the change in probability into the two

components as follows: 27

Δ𝑃𝑃 = �𝑃𝑃�𝑋𝑋𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃, �̂�𝛽𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃� − 𝑃𝑃�𝑋𝑋𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃 , �̂�𝛽𝑃𝑃𝑃𝑃𝑃𝑃�� + [𝑃𝑃�𝑋𝑋𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃 , �̂�𝛽𝑃𝑃𝑃𝑃𝑃𝑃� − 𝑃𝑃�𝑋𝑋𝑃𝑃𝑃𝑃𝑃𝑃 , �̂�𝛽𝑃𝑃𝑃𝑃𝑃𝑃�] (7)

The first term in brackets, ∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅, represents the change in probability of a going concern opinion

due to changes in auditors’ reporting strategy. The second term in brackets, ∆𝑃𝑃𝐶𝐶𝑃𝑃𝑖𝑖𝐶𝐶𝑘𝑘, captures

27 Thus we add and subtract the term 𝑃𝑃�𝑋𝑋𝑃𝑃𝑃𝑃𝑃𝑃𝑃𝑃 , �̂�𝛽𝑃𝑃𝑃𝑃𝑃𝑃� to equation (6).

32

the change in probability of a going concern opinion due to change in client risk characteristics.

Thus, we estimate the logistic model for PRE and POST, and compute Δ𝑃𝑃, ∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅, 𝐴𝐴𝑐𝑐𝑎𝑎 ∆𝑃𝑃𝐶𝐶𝑃𝑃𝑖𝑖𝐶𝐶𝑘𝑘.

We then examine whether the changes in the probabilities are statistically significant using t-tests

for the means and Wilcoxon rank-sum tests for medians. Our focus is on ∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅 which captures

the impact of changes in auditor behavior rather than of changes in client characteristics.

Hypotheses 4 does not indicate a sign for ∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅. A positive (negative) ∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅 would indicate that

auditors are more (less) conservative in the POST period compared with the PRE period.

In order to obtain coefficients for the AGC model, we assemble two samples surrounding

the ASU 2014-15 implementation date, one consisting of all firms for which complete data is

available (the “full” sample) and the second consisting of a subset of financially distressed firms

from the full sample (the “distressed” sample). Although the going concern opinion is most

salient for financially distressed firms, we believe that the full sample (consisting of stressed as

well as healthy firms) is useful for our context because the FASB emphasizes that ASU 2014-15

can be beneficial for all entities. However, both samples exclude firms in the financial industry

because the variables used to measure financial distress in the going concern model are not as

applicable to the financial sector (Francis and Krishnan 2002).

The full sample comprises 2,697 observations in the PRE period and 2,640 observations

in the POST period.28 Following prior literature (Reynolds and Francis 2001; DeFond et al.

2002), we define financially stressed firms as those with negative net income and/or negative

28 Since the goal is to obtain coefficients for the GC model to use in the computation of changes in probabilities, we want to retain as large a sample as possible. Thus, these samples are larger than those in the previous section because we do not require availability of IBES data.

33

cash flow from operations. The distressed sample comprises 1,258 observations in the PRE

period and 1,218 observations in the POST period.

Descriptive Statistics

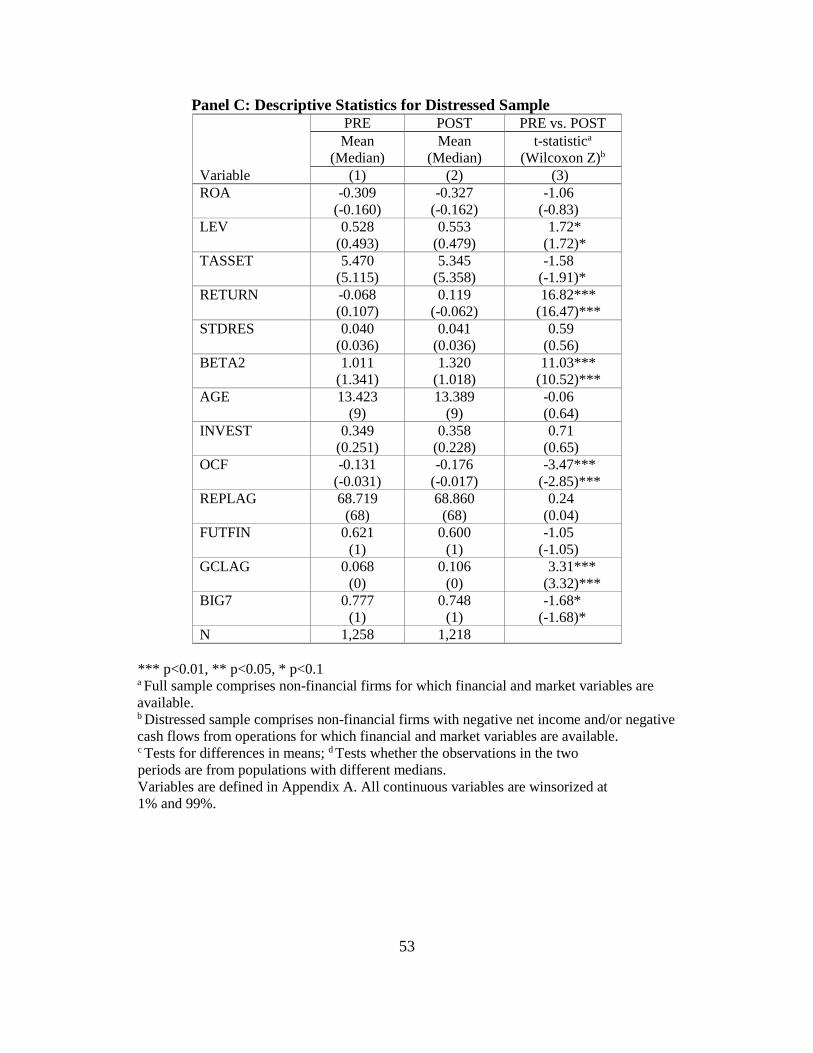

Table 6, Panel A presents auditors’ going concern opinion (AGC) rates for the PRE and

POST periods for the full and distressed samples. For the full sample, the AGC rate increased

from 5.52% to 6.40% from the PRE to POST periods. Not surprisingly, AGC rates are higher for

the distressed sample. The rate increased from 11.53% to 13.63% from the PRE to POST

periods.

Table 6, Panels B and C present descriptive statistics for the full and distressed samples,

respectively. In Panel B, none of the financial variables (with the exception of LEV and OCF) is

significantly different between the PRE and POST periods. Two market based variables, are

significantly different. BETA2 and RETURN have significantly higher values in the POST

period, suggesting higher systematic risk, and higher stock returns on average.29 GCLAG is

higher in the POST period than in the PRE period. For the distressed sample (Panel C), in

addition to the differences noted above for the full sample, there is a decrease in the proportion

of clients audited by the BIG7 and the median firm size (TASSET) is lower in the POST period

compared with the PRE period.

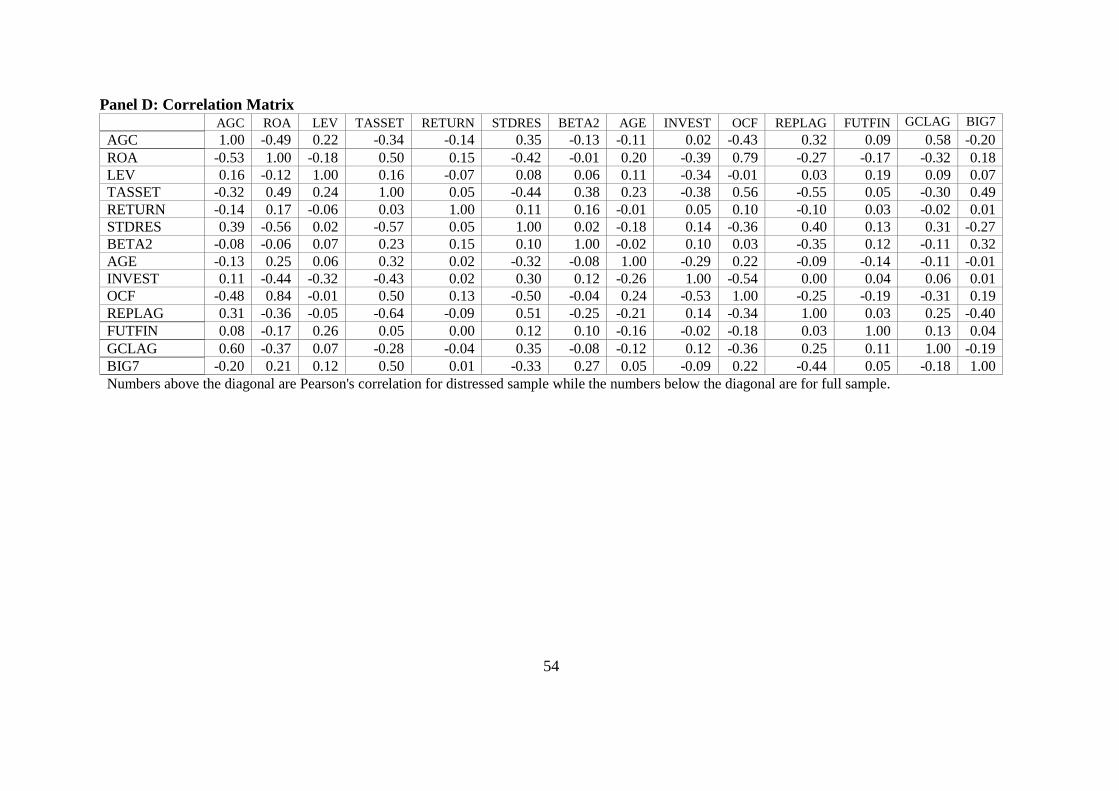

Panel D of Table 6 presents correlations among the variables. We show correlations for

the full sample below the diagonal and correlations for the distressed sample above the diagonal.

29 The market variables are estimated over the 200-day window ending 21 days before the fiscal year end. Consequently, we label the beta variable as BETA2 to distinguish it from the BETA used in the ERC model.

34

The variance inflation factors (VIF) are below 4.5 for all variables, indicating that

multicollinearity is not a concern.

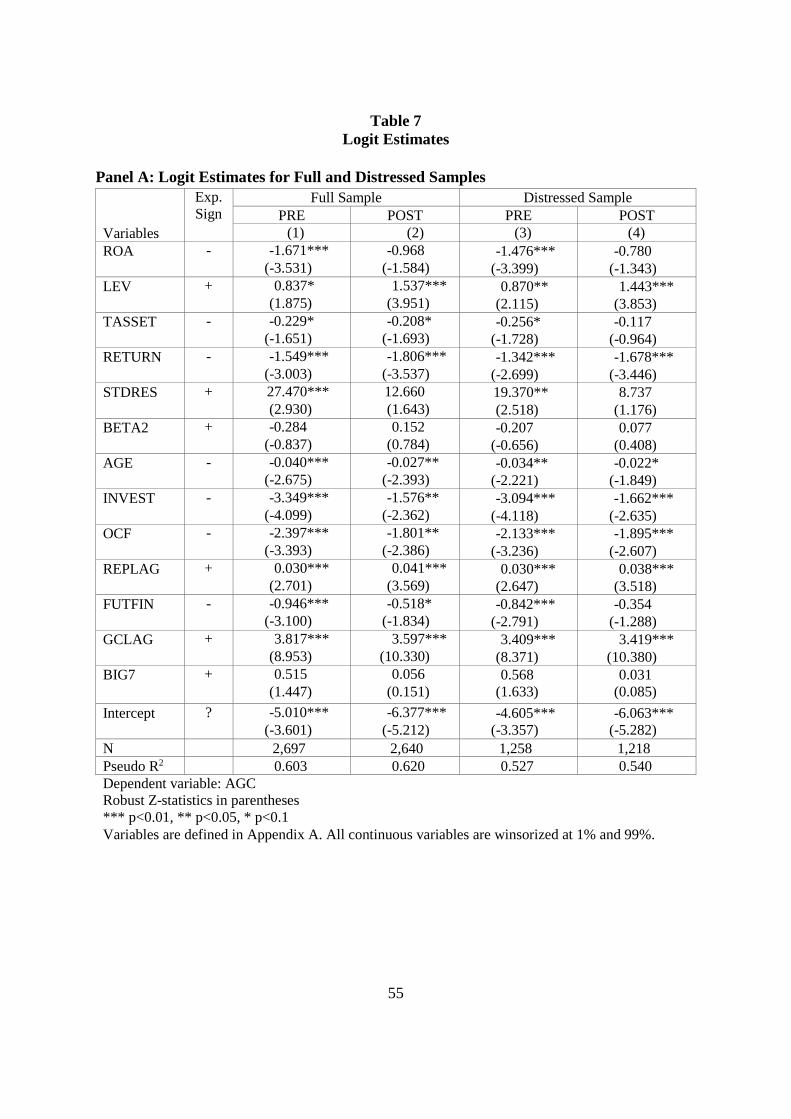

Logit Estimates for PRE and POST Periods

Table 7, Panel A presents estimates for the going concern opinion models for the full

(columns 1-2) and distressed (columns 3-4) samples. The pseudo R-Squared for the four models

vary between 0.52 to 0.62. Overall, the sign of the coefficients on the variables are consistent

with prior work. In addition, most of the variables have the same sign in the PRE and POST

periods, with some differences in their magnitudes and levels of statistical significance.

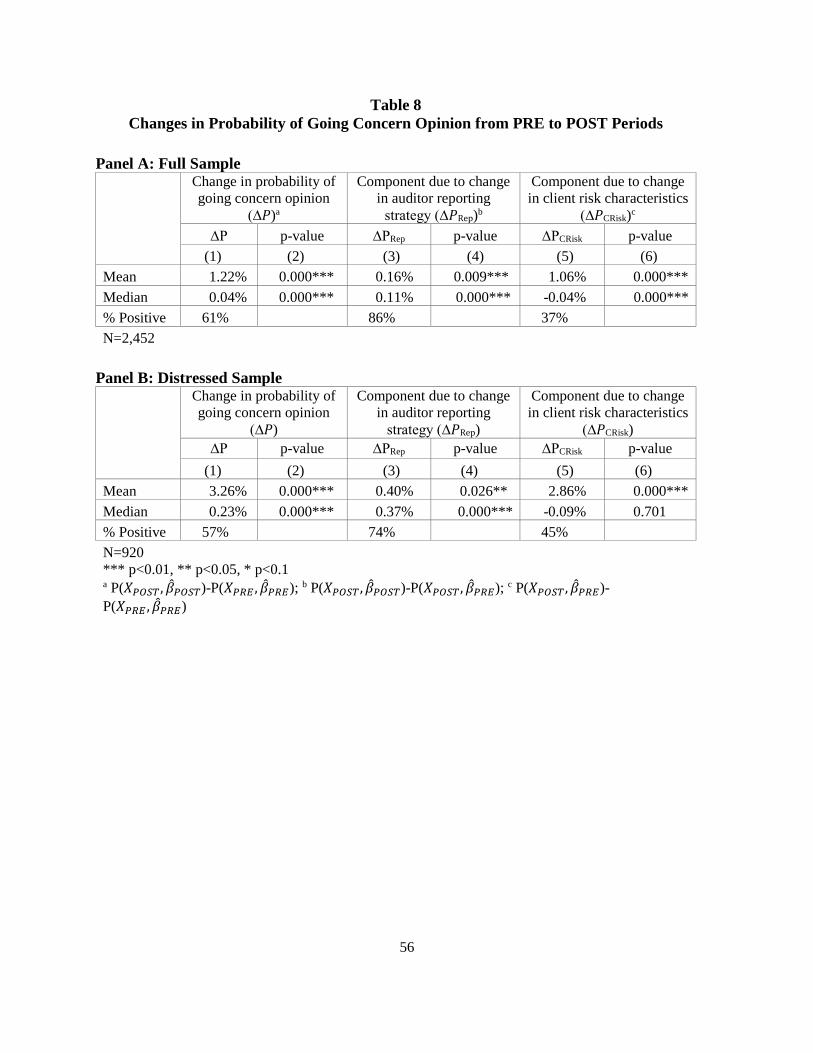

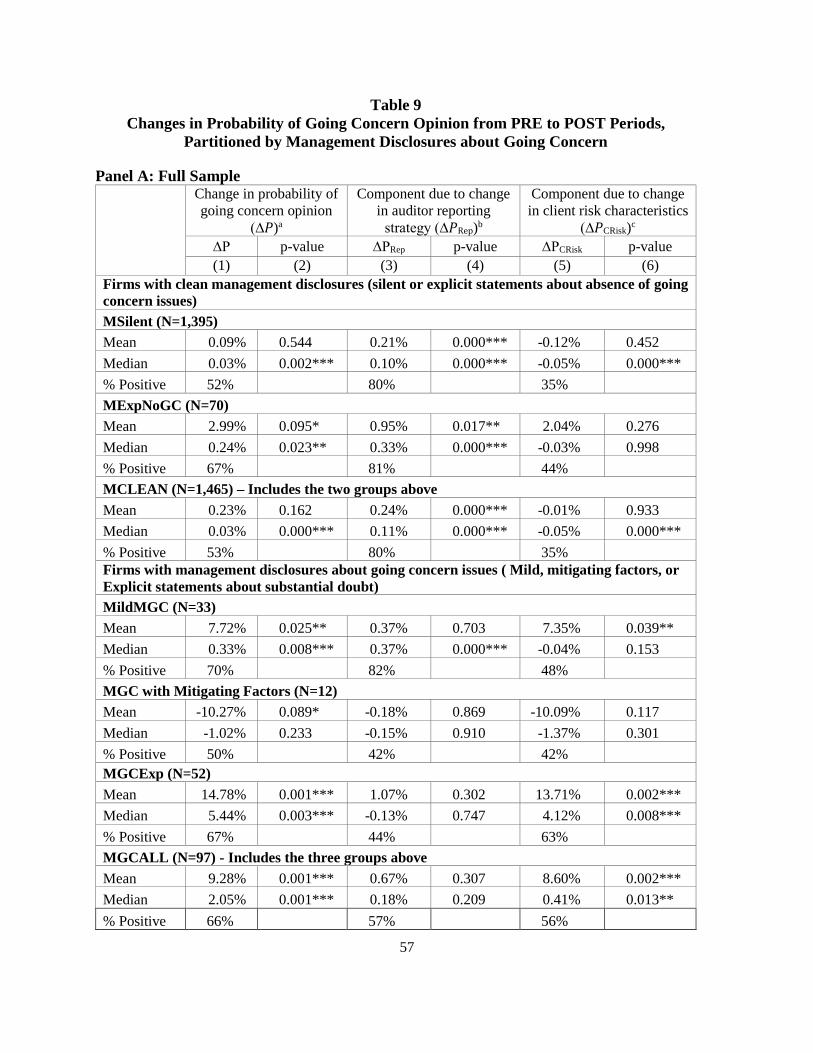

Tests Based on the Decomposition of Going Concern Rates

Table 8 reports changes in going concern reporting probabilities for the PRE and POST

periods. Panels A and B show the results for the full and distressed samples, respectively. Panel

A shows that the mean and median change in the probability of going concern opinion, Δ𝑃𝑃, are

1.22% and 0.04% respectively, and both are significantly different from zero. Columns 3-4 and

columns 5-6 show the mean and medians for the two components of the change, the change in

auditor reporting strategy and change in client risk characteristics. Our focus is on ∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅, the

proxy for changes in auditor reporting strategy. In Panel A, both the mean (0.16%) and median

(0.11%) for ∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅 are positive and significant. Also, 86% of the sample has a positive ∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅.

The change due to change in client risk characteristics ((∆𝑃𝑃𝐶𝐶𝑃𝑃𝑖𝑖𝐶𝐶𝑘𝑘) columns 5-6), for which we

have no a priori expectation, has a positive mean and a negative median. About 37% of the

sample has a positive ∆𝑃𝑃𝐶𝐶𝑃𝑃𝑖𝑖𝐶𝐶𝑘𝑘.

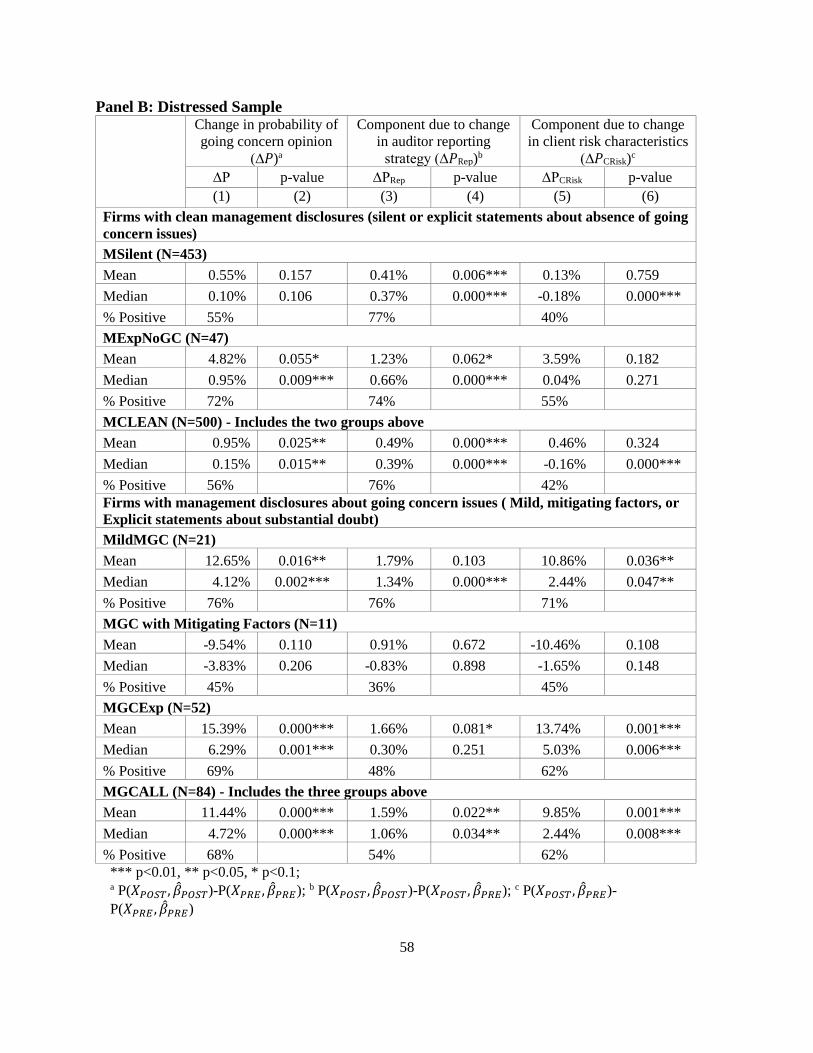

Table 8, Panel B shows similar results for the distressed sample. The mean overall

probability of going concern opinion increases by 3.26% from the PRE to POST periods. The

mean change in probability due to change in auditor reporting strategy �∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅� is 0.40% and is

35

statistically significant. The median change of 0.37% is also significant.30 Also, 74% of the

distressed sample has a positive ∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅. The mean change in probability due to change in client

risk characteristics is 2.86%, and is statistically significant. However, the median is insignificant.

Thus, the new standard seems to have increased auditor reporting conservatism after accounting

for the effect of changes in client characteristics.

Next we report a similar analysis for the sub-sample of firms for which we manually

collected data on management’s assessment of going concern. For this analysis, we merge the

full and distressed samples separately with our sample from Table 4, and compute the change in

probabilities.

Table 9, Panels A and B report the results for the change in probabilities. We continue to

refer to the samples as “full” and “distressed” samples although the sample sizes are different

from those in Table 8. As with our first research question, we separately classify companies into

MCLEAN and MGCALL. We also provide estimates for the sub-categories but the number of

observations for some of the sub-categories are very small.

The numbers in Panels A and B suggest the following. First, all subgroups show an

increase in the overall probability ∆𝑃𝑃 of receiving a going concern opinion (mean, median or

both) with the exception of MSilent for the distressed sample. We ignore the “MGC with

Mitigating Factors” group because it has only 12 (11) observations in the full (distressed)

sample. Second, focusing on the auditor reporting component ∆𝑃𝑃𝑃𝑃𝑅𝑅𝑅𝑅, we find that both the

MSilent and MExpNoGC groups are treated more conservatively in the POST period in both

panels. Among the firms with going concern disclosures, the auditor reporting component is not

30 We use the Wilcoxon Rank Sum test to check whether the median is significantly different from zero.

36

significant in Panel A, except for the median for the MildMGC. In Panel B, the auditor reporting

component is positive and significant for the MGCALL group as a whole. The median for the

MildMGC and mean for the MGCExp groups are positive and significant. However, these tests

should be viewed with some caution, because the sample sizes are small. Third, the client risk

component ∆𝑃𝑃𝐶𝐶𝑃𝑃𝑖𝑖𝐶𝐶𝑘𝑘 is generally positive and significant for the firms with disclosures about

going concern issues (except for MGC with mitigating factors, which has only 12 and 11

observations for the full and distressed sample respectively), but are negative or not significant

for the firms whose managers are not concerned about going concern issues. We note also that

the magnitude of ∆𝑃𝑃𝐶𝐶𝑃𝑃𝑖𝑖𝐶𝐶𝑘𝑘 across the groups gives credibility to our model as well as to our

coding of the disclosures. It is much larger for MGCALL than for MCLEAN. Also, it is larger

for the MGCExp Group than for the MildMGC group.

We conclude that, where management is providing assurance of the absence of going

concern issues, the auditor works harder to possibly ratify this assurance. In contrast, where the

management discloses going concern issues, the auditor does not change reporting strategy.

V. CONCLUSIONS

ASU 2014-15 requires managements of companies to evaluate their going concern status

for a period of one year from the date the financial statements are issued (or become available),

and provide footnote disclosures about the assessments. The rule became effective for fiscal

years ending after December 15, 2016. Prior to this standard, only auditors were required to

make going concern assessments (AS 2415, PCAOB 2017).

The FASB argues that requiring management to evaluate going concern status will

enhance the “timeliness, clarity, and consistency of related disclosures” (FASB 2014). Some

37

accounting firms (including the Big 4) that responded to the FASB’s exposure draft for the

standard supported the proposal, commenting that the management is in a unique position to

make this assessment because of its first-hand knowledge about significant risks, and its plans to

mitigate the risks. Management also has superior information about other relevant factors such as

new product development, strategy, and negotiation with lenders that could affect going concern

status of a company (Hutton, Lee, and Shu 2012).

We examine two research questions: Does the new standard affect market perceptions,

measured by the earnings response coefficient (ERC)? Does it affect auditors’ propensity to issue

a going concern opinion after controlling for changes in client characteristics? Our findings

indicate a significant increase in the ERC for firms with clean audit opinions whose management

also did not disclose going concern issues, indicating that the “double” assurance offered by the

auditor and management that the firm is “clean” is considered informative by investors. In

contrast, companies with AGCs see no change in ERCs. Since companies with AGC have been

required by the SEC to provide relevant disclosures, we conjecture that the market does not

perceive any new information provided by ASU 2014-15 disclosures as being useful.

We further examine whether the nature of the management disclosures by companies

with clean audit opinions differentially affects their ERCs. Clean companies can be silent (i.e.,

make no statement about going concern implying the absence of any issues), make an explicit

statement that there are no going concern issues, or provide disclosures about potential

substantial doubt, management plans and alleviation of the substantial doubt. We find that, while

the ERCs increase for all groups, the two groups with explicit disclosures have a greater increase

than the silent group. However, the difference in the increase in ERC is statistically significant

only between the silent group and the group with some disclosures about going concern. Overall,

38