1

MARKET TRENDS AND GROWTH SECTORS IN THE

BALKAN TELECOM MARKETS

Stela Bokun, Senior Analyst, EMEA

Pyramid Research

April 2011

© 2008 Pyramid Research

2

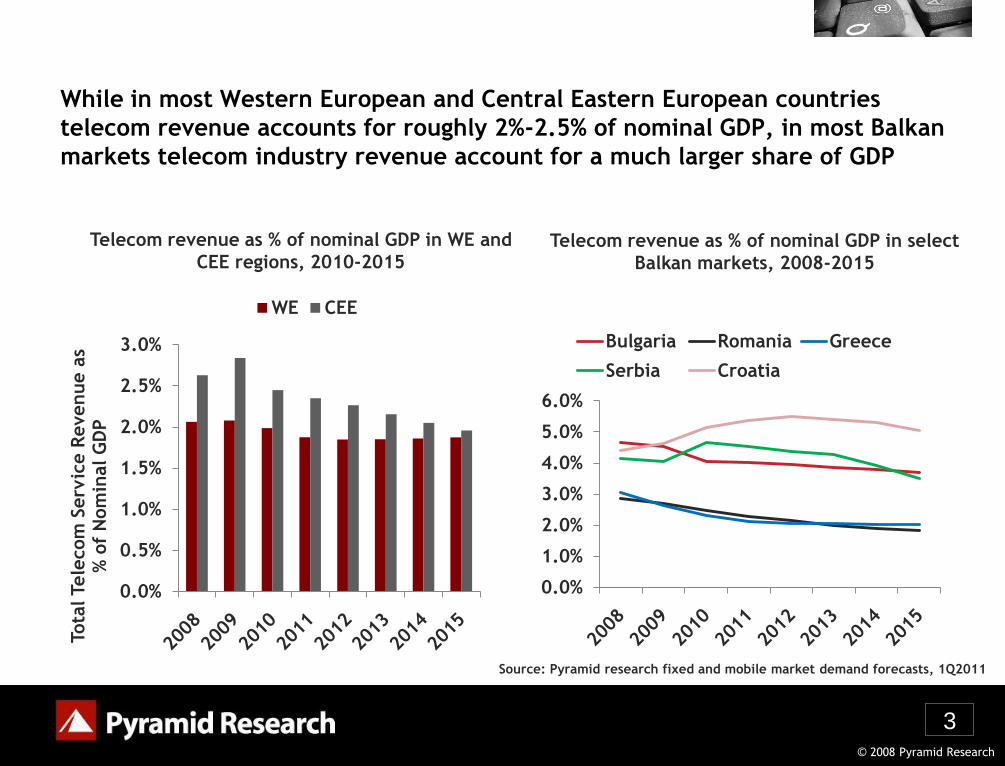

While in most Western European and Central Eastern European countries telecom revenue accounts for roughly 2%-2.5% of nominal GDP, in most Balkan markets telecoms account for a much larger share of GDP – in some cases exceeding 5%.

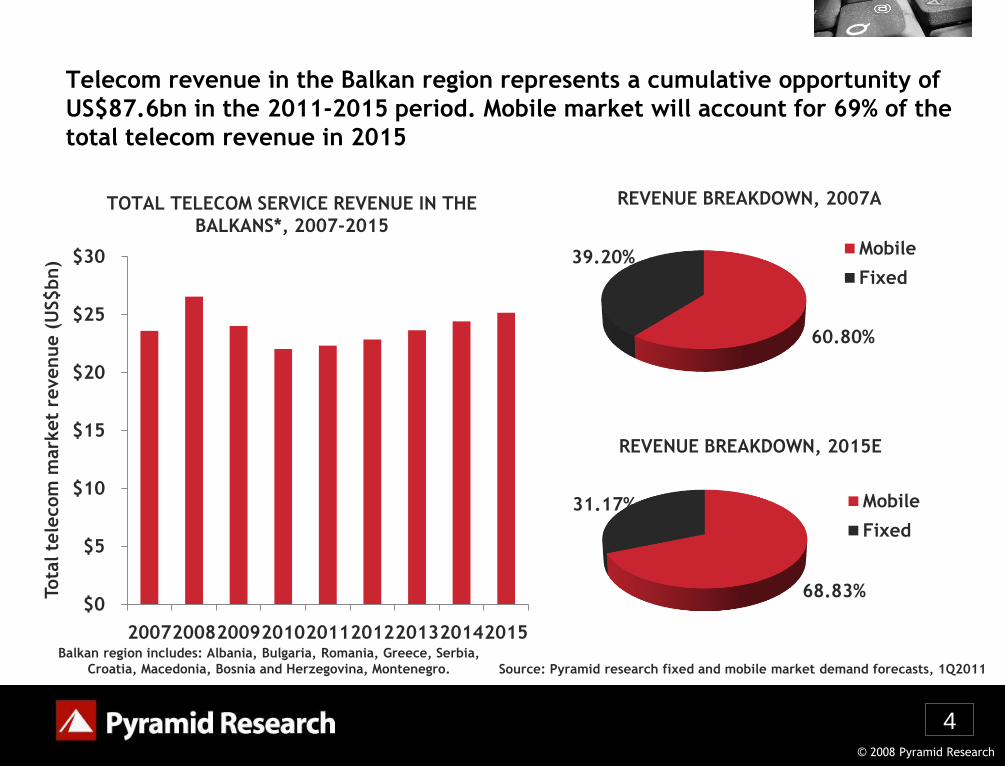

Telecom service revenue in the Balkan region represents a cumulative opportunity of US$87.6bn in the 2011-2015 period. Mobile market will account for 69% of the total telecom revenue in 2015.

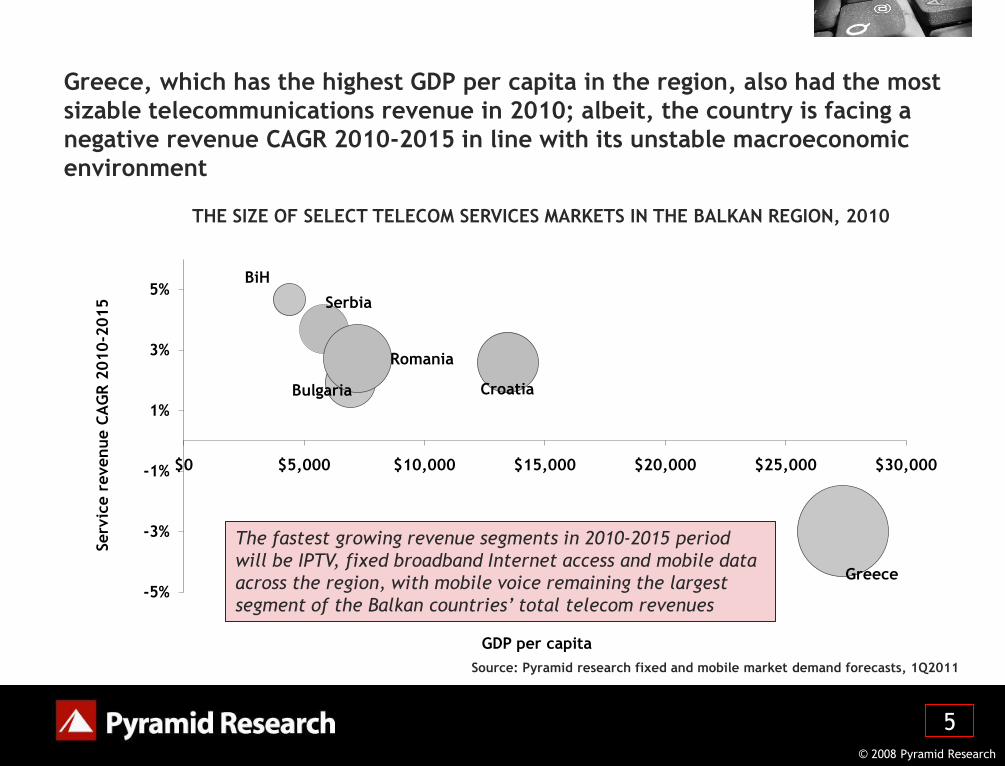

Greece, which has the highest GDP per capita in the region, also had the most sizable telecommunications revenue in 2010; albeit, the country is facing a negative revenue CAGR 2010-2015 in line with its unstable macroeconomic environment.

Fastest growing revenue segments in 2010-2015 period will be IPTV, fixed broadband Internet access and mobile data across most markets, with mobile voice remaining the largest segment of the regions’ total telecom revenues.

While fixed broadband will continue expanding, attractive device financing schemes, thirst for mobility and growing access speeds will result in a more pronounced growth of mobile broadband in most Balkan markets

Most Balkan markets will see growing investments in new access technologies in both fixed and mobile segments; however, the uptake of high-speed access technologies in both fixed and mobile segments will continue to fall behind when compared to WE countries and some most advanced CEE markets too.

Executive Summary

© 2008 Pyramid Research

While in most Western European and Central Eastern European countries

telecom revenue accounts for roughly 2%-2.5% of nominal GDP, in most Balkan

markets telecom industry revenue account for a much larger share of GDP

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Tota

l Tele

com

Serv

ice R

evenue a

s %

of

Nom

inal G

DP

WE CEE

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Bulgaria Romania Greece

Serbia Croatia

3

Telecom revenue as % of nominal GDP in WE and

CEE regions, 2010-2015Telecom revenue as % of nominal GDP in select

Balkan markets, 2008-2015

Source: Pyramid research fixed and mobile market demand forecasts, 1Q2011

© 2008 Pyramid Research

Telecom revenue in the Balkan region represents a cumulative opportunity of

US$87.6bn in the 2011-2015 period. Mobile market will account for 69% of the

total telecom revenue in 2015

$0

$5

$10

$15

$20

$25

$30

200720082009201020112012201320142015

Tota

l te

lecom

mark

et

revenue (

US$bn)

60.80%

39.20% Mobile

Fixed

4

TOTAL TELECOM SERVICE REVENUE IN THE

BALKANS*, 2007-2015

Balkan region includes: Albania, Bulgaria, Romania, Greece, Serbia,

Croatia, Macedonia, Bosnia and Herzegovina, Montenegro.

68.83%

31.17% Mobile

Fixed

REVENUE BREAKDOWN, 2007A

REVENUE BREAKDOWN, 2015E

Source: Pyramid research fixed and mobile market demand forecasts, 1Q2011

© 2008 Pyramid Research

Greece, which has the highest GDP per capita in the region, also had the most

sizable telecommunications revenue in 2010; albeit, the country is facing a

negative revenue CAGR 2010-2015 in line with its unstable macroeconomic

environment

5

Serbia

Bulgaria

Romania

Greece

Croatia

BiH

-5%

-3%

-1%

1%

3%

5%

$0 $5,000 $10,000 $15,000 $20,000 $25,000 $30,000

Serv

ice r

evenue C

AG

R 2

010-2

015

GDP per capita

THE SIZE OF SELECT TELECOM SERVICES MARKETS IN THE BALKAN REGION, 2010

The fastest growing revenue segments in 2010-2015 period

will be IPTV, fixed broadband Internet access and mobile data

across the region, with mobile voice remaining the largest

segment of the Balkan countries’ total telecom revenues

Source: Pyramid research fixed and mobile market demand forecasts, 1Q2011

6

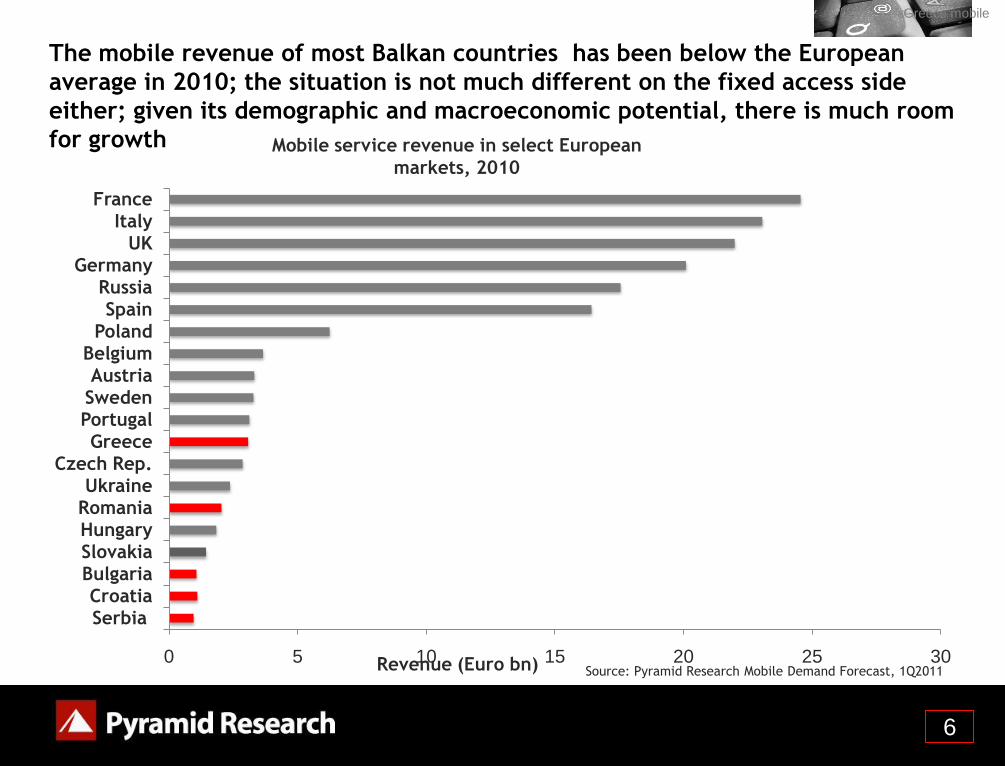

Greece mobile

The mobile revenue of most Balkan countries has been below the European

average in 2010; the situation is not much different on the fixed access side

either; given its demographic and macroeconomic potential, there is much room

for growth

0 5 10 15 20 25 30

Serbia

Croatia

Bulgaria

Slovakia

Hungary

Romania

Ukraine

Czech Rep.

Greece

Portugal

Sweden

Austria

Belgium

Poland

Spain

Russia

Germany

UK

Italy

France

Revenue (Euro bn) Source: Pyramid Research Mobile Demand Forecast, 1Q2011

Mobile service revenue in select European

markets, 2010

© 2008 Pyramid Research

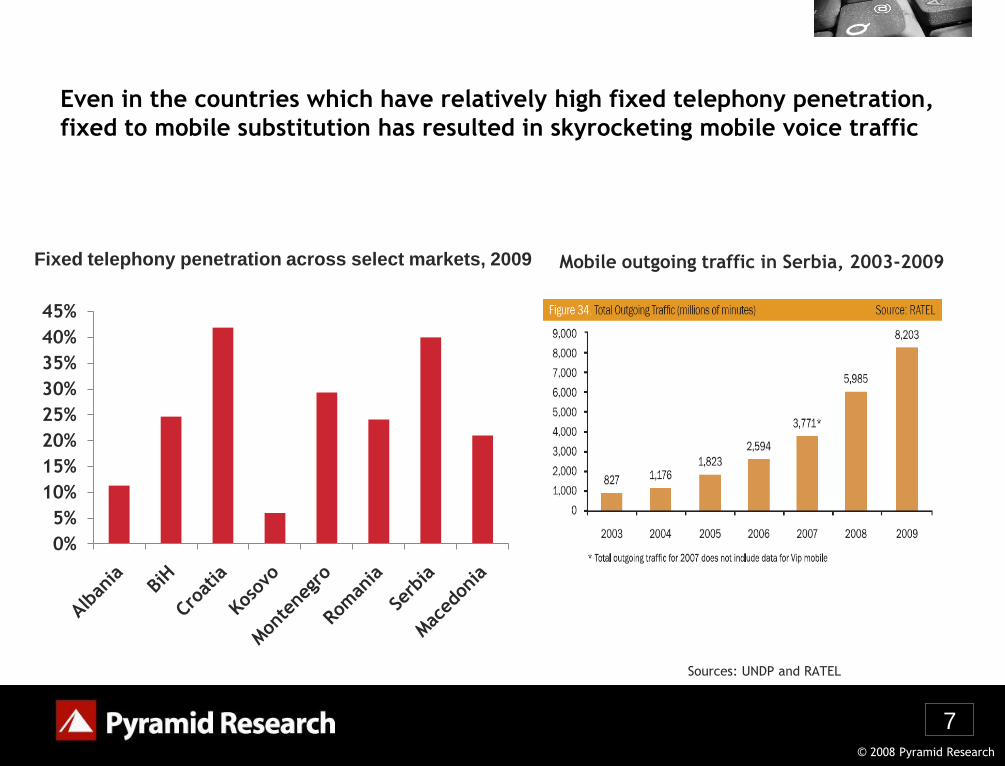

Even in the countries which have relatively high fixed telephony penetration,

fixed to mobile substitution has resulted in skyrocketing mobile voice traffic

7

Fixed telephony penetration across select markets, 2009 Mobile outgoing traffic in Serbia, 2003-2009

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Sources: UNDP and RATEL

© 2008 Pyramid Research

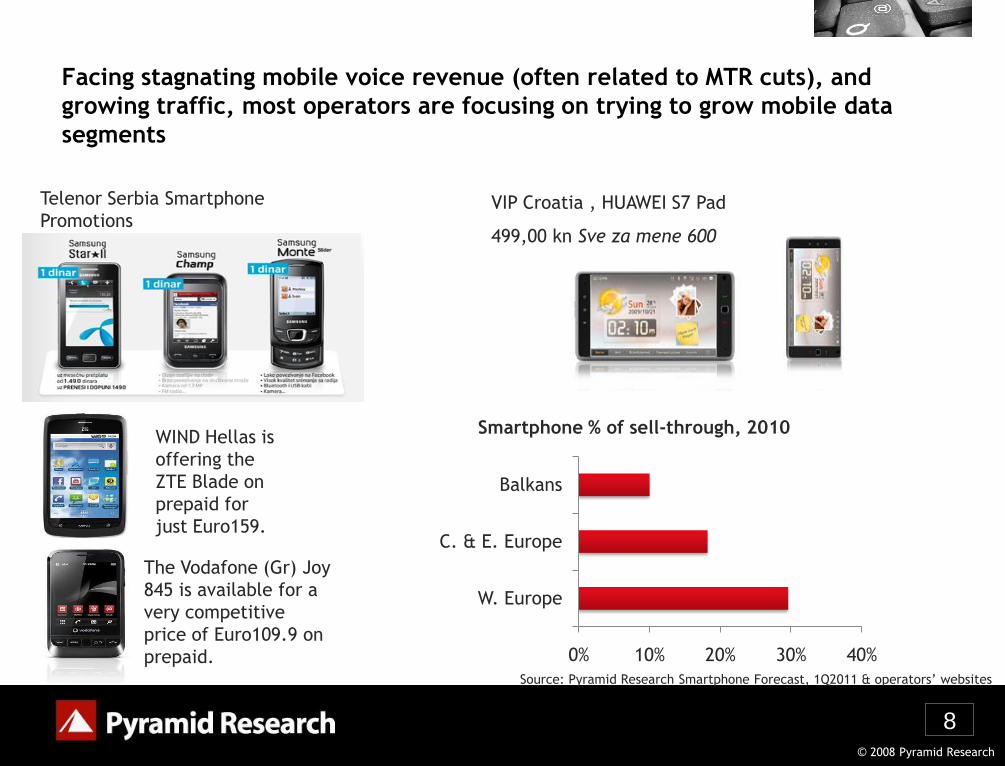

Facing stagnating mobile voice revenue (often related to MTR cuts), and

growing traffic, most operators are focusing on trying to grow mobile data

segments

8

VIP Croatia , HUAWEI S7 Pad

499,00 kn Sve za mene 600

Telenor Serbia Smartphone

Promotions

WIND Hellas is

offering the

ZTE Blade on

prepaid for

just Euro159.

The Vodafone (Gr) Joy

845 is available for a

very competitive

price of Euro109.9 on

prepaid. 0% 10% 20% 30% 40%

W. Europe

C. & E. Europe

Balkans

Smartphone % of sell-through, 2010

Source: Pyramid Research Smartphone Forecast, 1Q2011 & operators’ websites

9

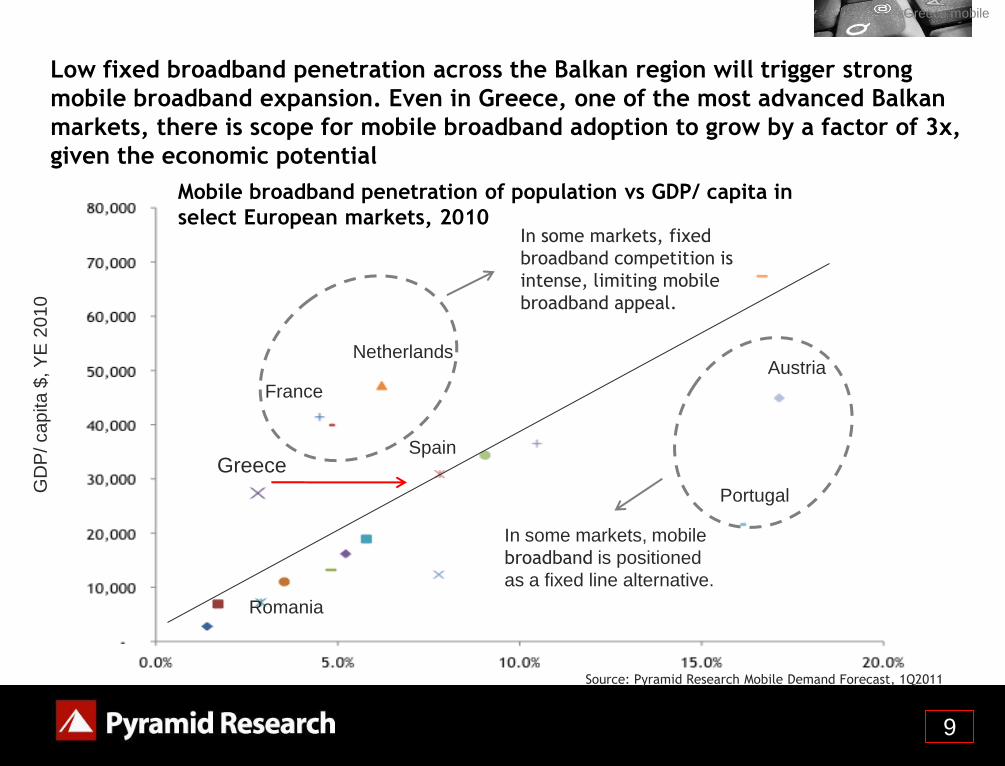

Low fixed broadband penetration across the Balkan region will trigger strong

mobile broadband expansion. Even in Greece, one of the most advanced Balkan

markets, there is scope for mobile broadband adoption to grow by a factor of 3x,

given the economic potential

Greece mobile

Greece

Portugal

AustriaNetherlands

France

Spain

Romania

In some markets, mobile

broadband is positioned

as a fixed line alternative.

In some markets, fixed

broadband competition is

intense, limiting mobile

broadband appeal.

GD

P/ ca

pita

$, Y

E 2

01

0

Mobile broadband penetration of population vs GDP/ capita in

select European markets, 2010

Source: Pyramid Research Mobile Demand Forecast, 1Q2011

© 2008 Pyramid Research

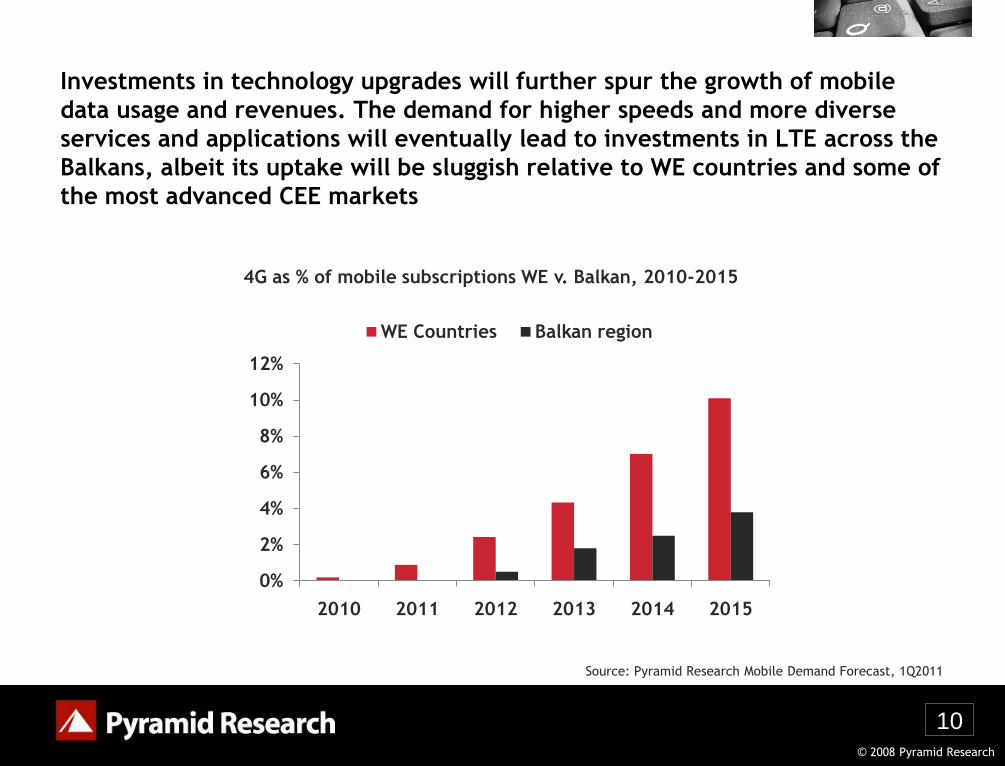

Investments in technology upgrades will further spur the growth of mobile

data usage and revenues. The demand for higher speeds and more diverse

services and applications will eventually lead to investments in LTE across the

Balkans, albeit its uptake will be sluggish relative to WE countries and some of

the most advanced CEE markets

10

0%

2%

4%

6%

8%

10%

12%

2010 2011 2012 2013 2014 2015

WE Countries Balkan region

4G as % of mobile subscriptions WE v. Balkan, 2010-2015

Source: Pyramid Research Mobile Demand Forecast, 1Q2011

11

Poland fixed

In the fixed arena, bundling is becoming a market norm in some Balkan markets,

with operators competing on speed as well as Value Added Services

Bulgaria blizoo offering Romtelecom fiber offering

SBB Serbia offering

BH Telecom offering

12

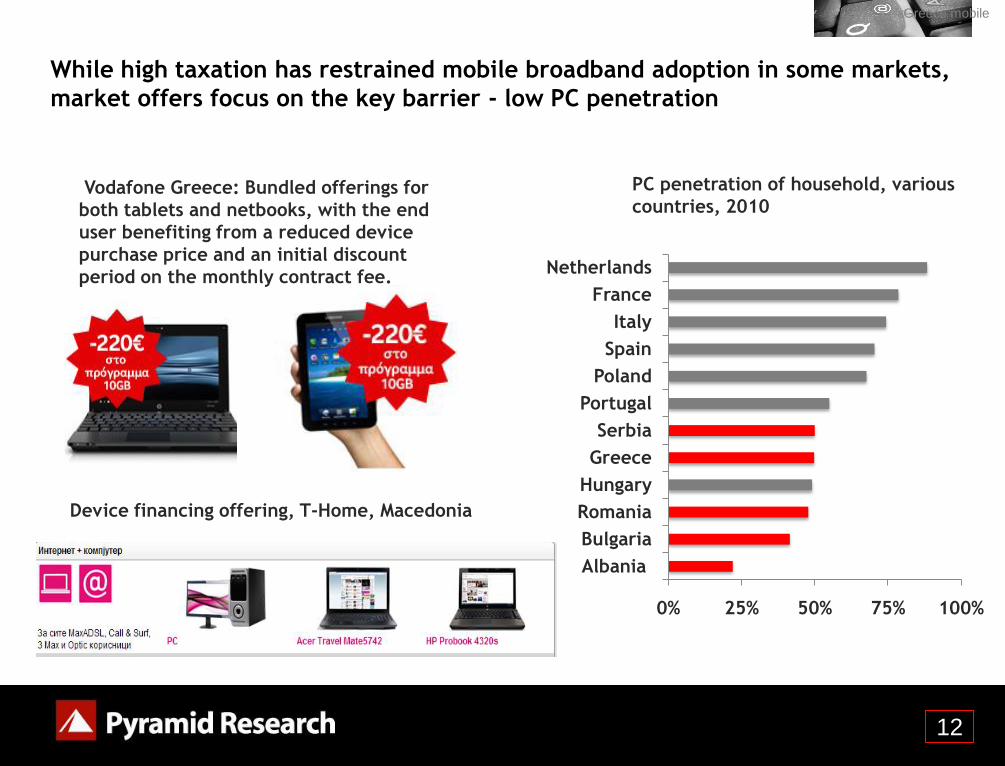

While high taxation has restrained mobile broadband adoption in some markets,

market offers focus on the key barrier - low PC penetration

Greece mobile

0% 25% 50% 75% 100%

Albania

Bulgaria

Romania

Hungary

Greece

Serbia

Portugal

Poland

Spain

Italy

France

Netherlands

PC penetration of household, various

countries, 2010Vodafone Greece: Bundled offerings for

both tablets and netbooks, with the end

user benefiting from a reduced device

purchase price and an initial discount

period on the monthly contract fee.

Device financing offering, T-Home, Macedonia

13

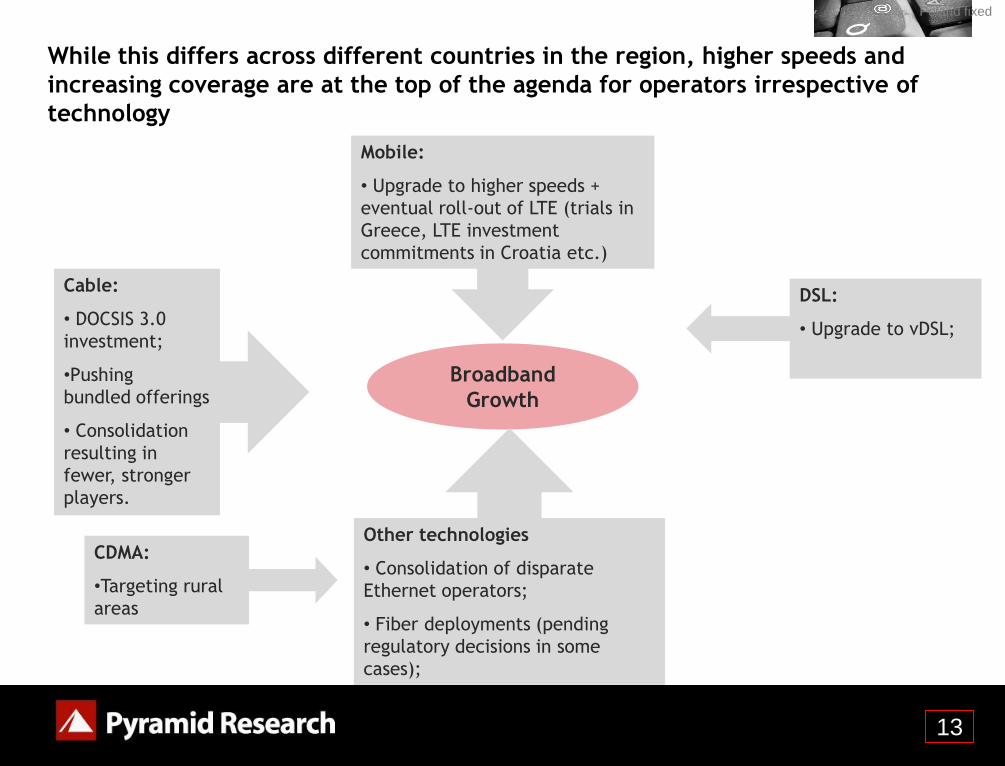

Poland fixed

While this differs across different countries in the region, higher speeds and

increasing coverage are at the top of the agenda for operators irrespective of

technology

Broadband

Growth

Cable:

• DOCSIS 3.0

investment;

•Pushing

bundled offerings

• Consolidation

resulting in

fewer, stronger

players.

DSL:

• Upgrade to vDSL;

Other technologies

• Consolidation of disparate

Ethernet operators;

• Fiber deployments (pending

regulatory decisions in some

cases);

Mobile:

• Upgrade to higher speeds +

eventual roll-out of LTE (trials in

Greece, LTE investment

commitments in Croatia etc.)

CDMA:

•Targeting rural

areas

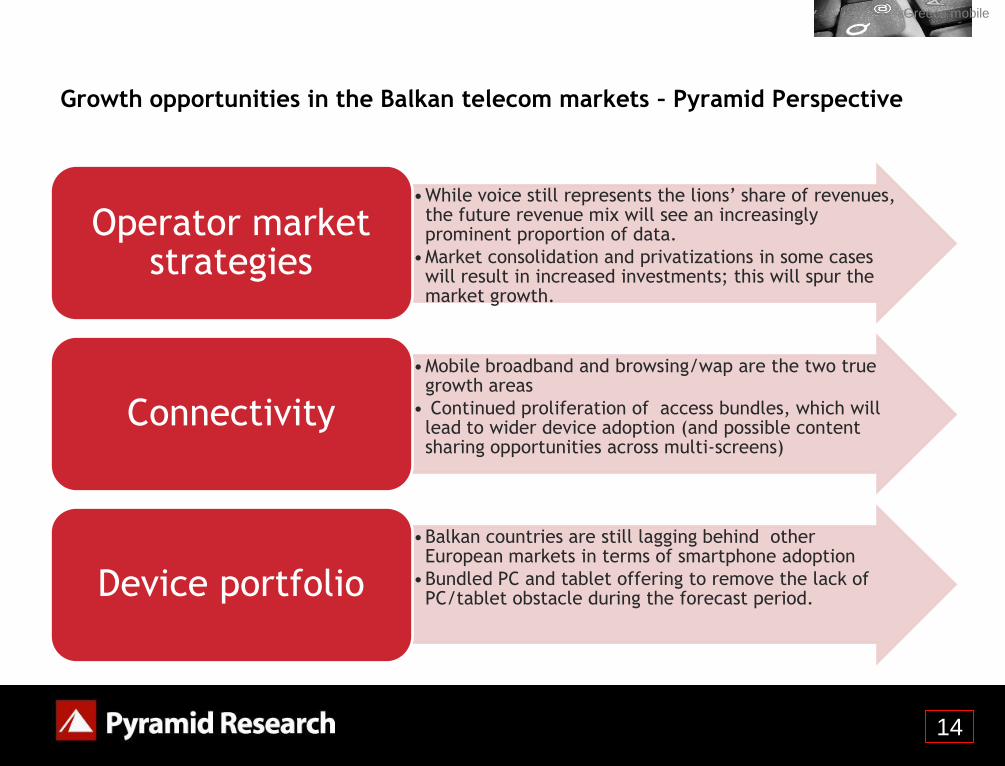

•While voice still represents the lions’ share of revenues, the future revenue mix will see an increasingly prominent proportion of data.

•Market consolidation and privatizations in some cases will result in increased investments; this will spur the market growth.

Operator market strategies

•Mobile broadband and browsing/wap are the two true growth areas

• Continued proliferation of access bundles, which will lead to wider device adoption (and possible content sharing opportunities across multi-screens)

Connectivity

•Balkan countries are still lagging behind other European markets in terms of smartphone adoption

•Bundled PC and tablet offering to remove the lack of PC/tablet obstacle during the forecast period. Device portfolio

Growth opportunities in the Balkan telecom markets – Pyramid Perspective

14

Greece mobile

15

Stela Bokun, Senior Analyst, Europe

Recommended