1 / 30

Multinational Banks∗

Jose L. FillatFederal Reserve Bank of Boston

Stefania GarettoBoston University

Martin GotzGoethe Universitat

December 4, 2013

∗The views expressed in this paper are the authors’ only and not those of the Federal Reserve Bankof Boston or the Federal Reserve System.

Introduction

Objective

Literature

Data

Model

Calibration

Results

Conclusions

2 / 30

The Boston Globe, October 26th 2013

“Spanish-based Santander (...) acquired Sovereign Bank in 2009 as thespringboard for its US ambitions, [establishing] 700 branches andATMs across nine northeastern states.”

“Santander is the fourth-largest bank by deposits in Massachusetts andhas 1.7 million US customers. Emilio Botin, chairman of the parentcompany, said last week during a visit to the United States that hehopes to see profits for the American business double in three years to$2 billion.”

This Paper

Introduction

Objective

Literature

Data

Model

Calibration

Results

Conclusions

3 / 30

Why and how banks expand internationally?We develop a structural model of entry in the foreign bankingmarket.

• The model is a “good description” of the foreign banking sector inthe US:

– assumptions motivated by institutional details of the sector;– model designed to replicate empirical patterns on the activities

of foreign banking institutions in the US:

⊲ differences in presence, size and activities of branches versussubsidiaries of foreign institutions.

• Structural model is amenable to counterfactual analysis to study:

– the risk implications of foreign banking;– the efficiency properties of the proposed regulation or regulation

in place.

Related Literature

Introduction

Objective

Literature

Data

Model

Calibration

Results

Conclusions

4 / 30

• Empirical analysis of foreign banking:

Goldberg (2007, 2009), Cetorelli and Goldberg (2010, 2012 JF andAER PP)

• Models of Trade and FDI in the Banking Sector:

Eaton (1994), De Blas and Russ (2012), Niepmann (2012, 2013),Bremus et al. (2013)

• To build our model:

– Micro-founded Models of Banking:

Klein (1971), Monti (1972)

– Models of investment under uncertainty:

Dixit (1989), Fillat and Garetto (2012)

Data Description and Sources

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

5 / 30

• Regulatory reporting data filed by US domestic banks, USsubsidiaries of foreign banks, and U.S. branches/agencies of foreignbanks (Call Reports - FFIEC 002, 031,041)

• Foreign owned institutions :

– U.S. branches and agencies of foreign banks, and– U.S. banks of which more than 25% is owned by a foreign

banking organization or where the relationship is reported asbeing a controlling relationship.

• Sample period: 1995-2010.

⇒ History of Banking Regulation

How do Foreign Banks Enter the US Market?

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

6 / 30

Home Country Foreign Country

BHC

BHC

Branch Subs

BHC

Subs

Offices Offices

Subs

BHC

BHC

Subs

Subs

Bank

Offices Offices

Subs

Offices Offices

Offices Offices

Offices Offices

Subs

Offices Offices Offices Offices

Domestic institutions

FBOs

Example: Royal Bank of Scotland

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

7 / 30

U.S. U.K.

CFG

BofA,

Corp

RBS

Securities

BofA

BHC

BofA

NA

M.L.

RBSG,

Plc

RBS,

Plc

RBS

Bank

Lloyd’s

Bank of

Utica

Offices Offices

Citizens

Offices Offices RBS

Fund

Offices

Domestic institutions

FBOs

RBS

Int’l

Bank of

Scotland

NY Branch

How do Foreign Banks Enter the US Market?

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

8 / 30

• Subsidiary Banks:

– 64 banks, total assets approx $1tn;– subject to US regulation and capital requirements;– give loans and accept both wholesale and retail deposits (with

deposit insurance);– arm’s length relationship with the parent.

• Branches and Agencies:

– 215 branches and agencies, total assets approx $2tn,;– subject to US regulation but NOT to capital requirements;– give loans and accept only wholesale deposits (they cannot

accept insured deposits);– display large intrafirm flows with the foreign parent.

• Other: Edge and Agreement Corporations, Representative officesand Non-depository trusts.

Foreign Banking Institutions: Total Flows

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

9 / 30

1015

2025

30S

hare

1995q4 1998q4 2001q4 2004q4 2007q4 2010q4

% of Foreign C&I Loans

1015

2025

30S

hare

1995q4 1998q4 2001q4 2004q4 2007q4 2010q4

% of Foreign Loans

1015

2025

30S

hare

1995q4 1998q4 2001q4 2004q4 2007q4 2010q4

% of Foreign Total Assets

1015

2025

30S

hare

1995q4 1998q4 2001q4 2004q4 2007q4 2010q4

% of Foreign Deposits

[Data source: Federal Reserve Board of Governors, U.S. Share Data for U.S.Offices of Foreign Banking Organizations.]

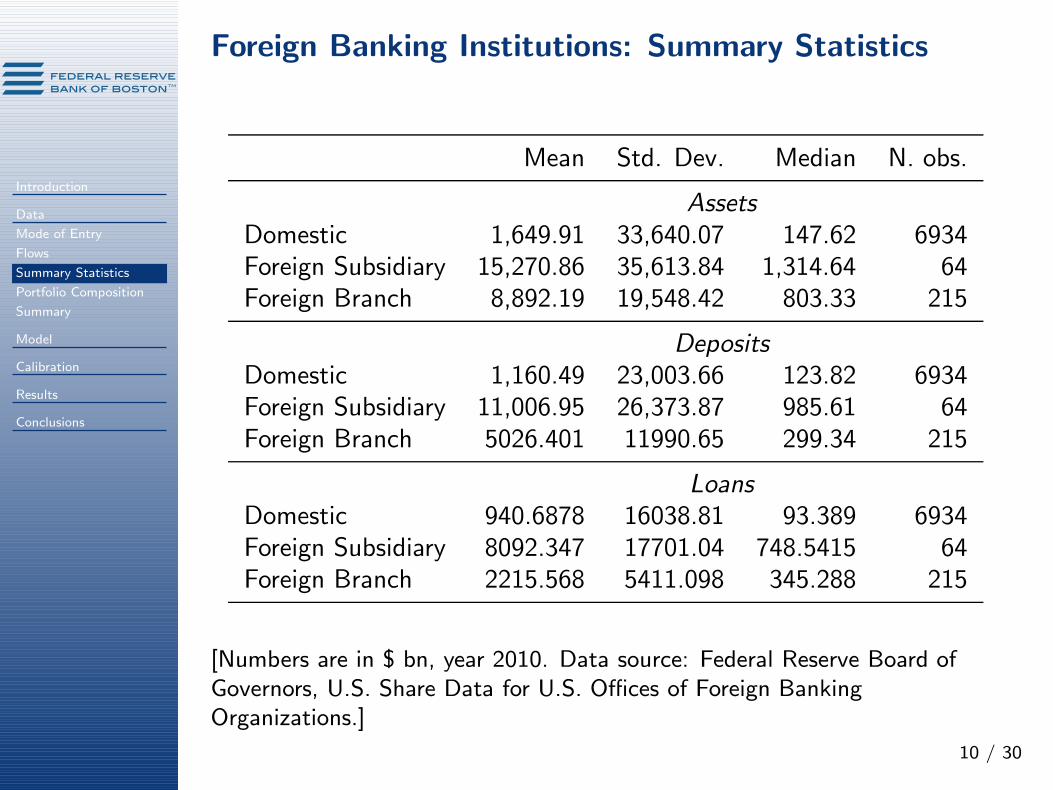

Foreign Banking Institutions: Summary Statistics

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

10 / 30

Mean Std. Dev. Median N. obs.

AssetsDomestic 1,649.91 33,640.07 147.62 6934Foreign Subsidiary 15,270.86 35,613.84 1,314.64 64Foreign Branch 8,892.19 19,548.42 803.33 215

DepositsDomestic 1,160.49 23,003.66 123.82 6934Foreign Subsidiary 11,006.95 26,373.87 985.61 64Foreign Branch 5026.401 11990.65 299.34 215

LoansDomestic 940.6878 16038.81 93.389 6934Foreign Subsidiary 8092.347 17701.04 748.5415 64Foreign Branch 2215.568 5411.098 345.288 215

[Numbers are in $ bn, year 2010. Data source: Federal Reserve Board ofGovernors, U.S. Share Data for U.S. Offices of Foreign BankingOrganizations.]

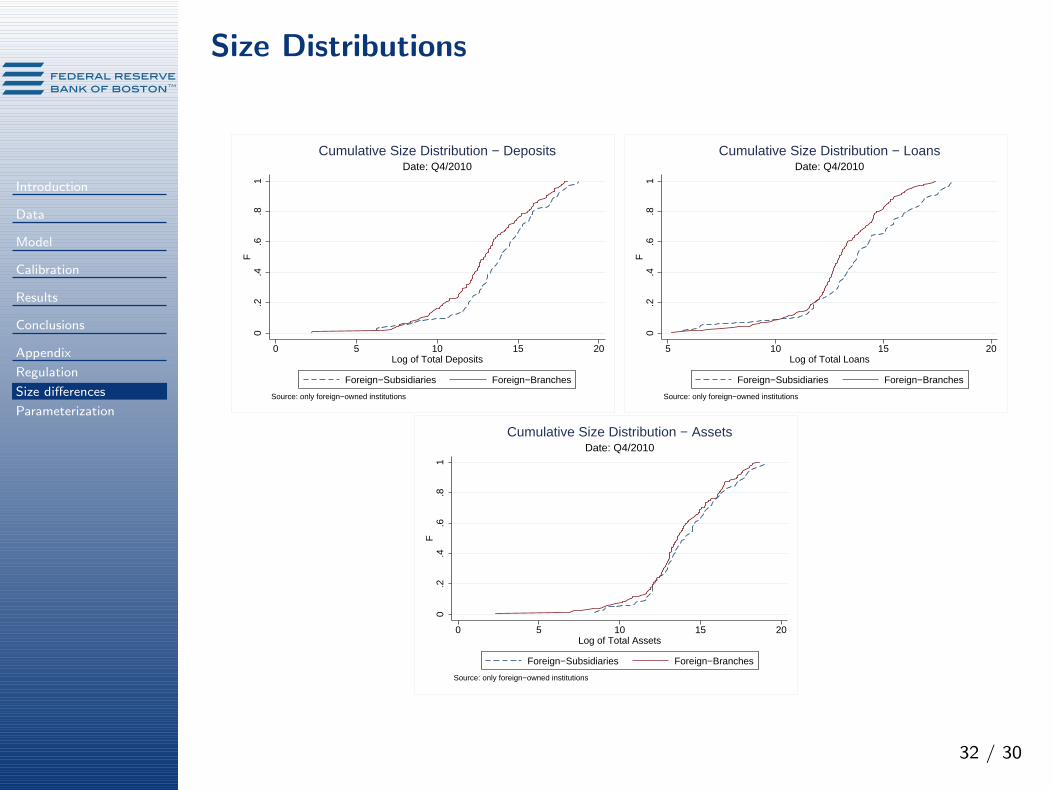

Size Differences: Assets

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

11 / 30

05

1015

bn $

1995q4 1997q4 1999q4 2001q4 2003q4 2005q4 2007q4 2009q4

foreign−branch foreign−branch (+due from related institutions)

foreign−subsidiary domestic bank

Average Assets

⇒ Size distributions

Intra-firm Flows

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

12 / 30

−1

01

23

bn $

1995q1 2000q1 2005q1 2010q1

Net Due From Head Office Net Due To Head Office

Intrafirm Balances (Average)

Portfolio Composition: Loans-to-Assets Ratio

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

13 / 30

.2.3

.4.5

.6bn

$

1995q4 1997q4 1999q4 2001q4 2003q4 2005q4 2007q4 2009q4

foreign−branch foreign−subsidiary

domestic bank

Loans / Assets

Portfolio Composition: Loan Types

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

14 / 30

020

4060

8010

0

Domestic Bank Foreign−Subsidiary Foreign−Branch

Loan Portfolio

Commercial & Industrial Real Estate

Other

Stylized Facts

Introduction

Data

Mode of Entry

Flows

Summary Statistics

Portfolio Composition

Summary

Model

Calibration

Results

Conclusions

15 / 30

• Foreign banking in the US is a large phenomenon.

• Foreign banks are larger than domestic incumbents: evidence ofselection.

• Subsidiaries of foreign banks are larger than foreign branches,and more similar to the domestic incumbents in their activities.

• Foreign branches appear to be a source of funding to theirparents.

A good structural model of foreign banking must be

• consistent with these facts• be able to answer the question of why and how banks expand• explain what risks international expansion poses to them and the

system.• allow us to run conterfactuals and help design optimal regulatory

policies

The Environment of the Model

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

16 / 30

• Two countries, Home and Foreign (denoted by ∗).

• Time is continuous.

• Each country is populated by a large mass of national banks:

– each bank offers one-period loans (L), makes investments (I) andaccepts deposits (D);

– each bank has some market power in the loans market (start withmonopolistic competition to rule out strategic considerations).

• Study the decision of banks from the Home country to enter theForeign country:

– each bank enters if it can make positive profits in the Foreigncountry;

– the rationale for entry is given by differentiation (spatial or product);– a bank can enter a market either as a branch or as a subsidiary.

The Environment of the Model (contd.)

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

17 / 30

• Banks are heterogeneous in their ability a of managing loans,investments and deposits:

– Each bank has management costs a · C(D,L, I), where C(D,L, I) isa convex function;

– When a bank enters the Foreign market, it transfers his efficiency a tothe subsidiary or branch.

• There are sunk costs of entry, depending on the organizational formof the foreign affiliate: Fs > Fb > 0.

• Loans and investments are risky (on aggregate).

⇓The solution of the optimal entry problem is a bank-specific policyfunction that determines a bank’s entry decision and mode of entry asa function of bank-level characteristics and aggregate variables(aggregate loan demand and return on investments).

Why THIS model?

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

18 / 30

• Broader research agenda on the risk implications of foreignactivities, building on Fillat and Garetto (2012), Fillat, Garetto andOldenski (2013):

– aggregate, country-specific shocks and sunk costs of entrygenerate hysteresis in firms’ decisions;

– entry after a series of positive shocks may not be followed byexit when shocks revert (Dixit 1989, Baldwin and Krugman1989);

– possible “optimal losses” are a source of risk to the firm.

• This model:

– allows us to quantify the risk arising from banks’ foreignactivities associated with different kinds of shocks;

– can be used to perform counterfactual exercises where wemodify institutional features of the sector and evaluate theirconsequences for risk exposure.

Why THIS model?

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

18 / 30

• Broader research agenda on the risk implications of foreignactivities, building on Fillat and Garetto (2012), Fillat, Garetto andOldenski (2013):

– aggregate, country-specific shocks and sunk costs of entrygenerate hysteresis in firms’ decisions;

– entry after a series of positive shocks may not be followed byexit when shocks revert (Dixit 1989, Baldwin and Krugman1989);

– possible “optimal losses” are a source of risk to the firm.

• This model:

– allows us to quantify the risk arising from banks’ foreignactivities associated with different kinds of shocks;

– can be used to perform counterfactual exercises where wemodify institutional features of the sector and evaluate theirconsequences for risk exposure.

• What we CANNOT talk about (yet):

– Maturity mismatch. Liquidity issues are TBA.– Drivers of aggregate shocks in the banking sector.

Intra-temporal Problem: National Banks

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

19 / 30

Determine the optimal per-period profits of a bank given its foreignstatus.

• A national bank chooses the optimal amounts of loans L, depositsD, investment I, interbank borrowing M , and equity E tomaximize its profits πN :

maxL,I,D,M,E

πN = prL(L) · L− (1− p)L+ rII − rDD − rMM − ...

aC(D,L, I)− fp ·D

s.t. M +D + E = L+ I (resource constraint)

E

ωLL+ ωII≥ k (capital requirement).

where p is the probability of loan repayment, fp is the deposit insurancepremium, k is the capital requirement, and ωL, ωI are weights.rL(L) is a downward-sloping demand for loans, while rI , rD, and rM

are taken as given by the bank.

Intra-temporal Problem: Parent + Foreign Sub Pair

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

20 / 30

• In a parent + subsidiary pair, the profit maximization problem ofthe parent in the home country is identical to the problem of anational bank. The foreign subsidiary is operated as an independententity to maximize its profits πS :

maxL∗,I∗,D∗,M∗,E∗

πS = pr∗L(L∗) · L∗ − (1− p)L∗ + rII

∗ − rDD∗ − ...

rMM∗ − aC(D∗, L∗, I∗)− fp ·D∗ − FS

s.t. M∗ +D∗ + E∗ = L∗ + I∗ (resource constraint)

E∗

ωLL∗ + ωII∗≥ k (capital requirement).

Intra-temporal Problem: Parent + Foreign Branch Pair

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

21 / 30

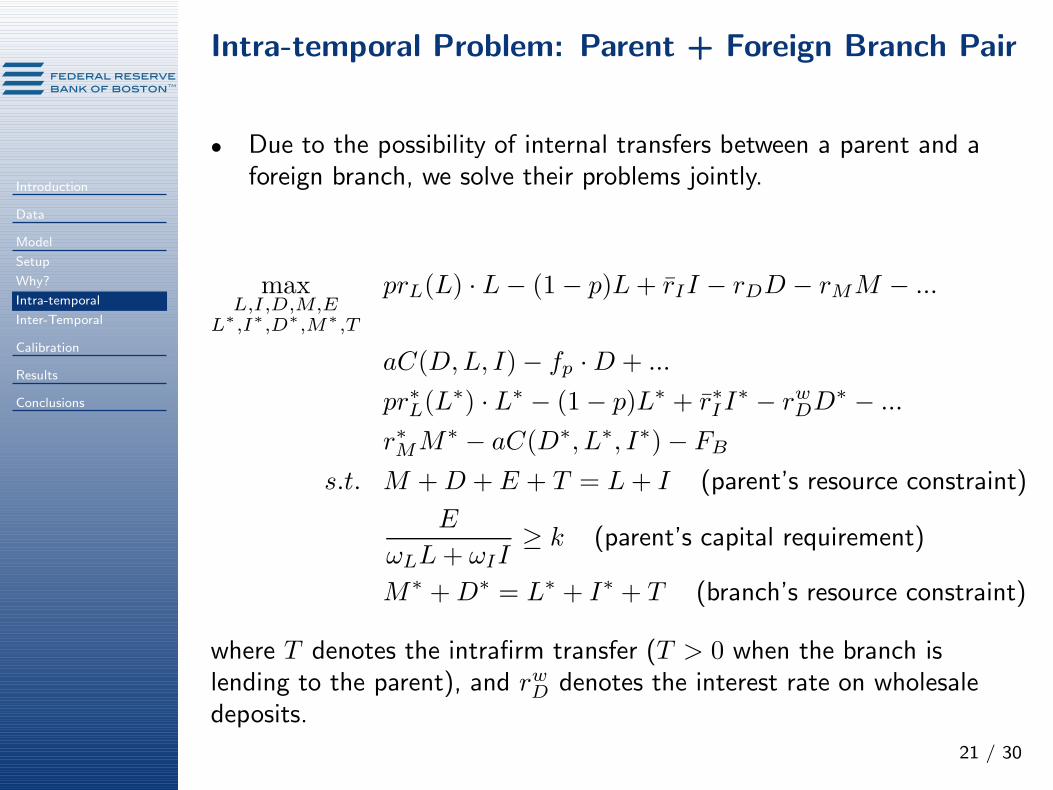

• Due to the possibility of internal transfers between a parent and aforeign branch, we solve their problems jointly.

maxL,I,D,M,E

L∗,I∗,D∗,M∗,T

prL(L) · L− (1− p)L+ rII − rDD − rMM − ...

aC(D,L, I)− fp ·D + ...

pr∗L(L∗) · L∗ − (1− p)L∗ + r∗I I

∗ − rwDD∗ − ...

r∗MM∗ − aC(D∗, L∗, I∗)− FB

s.t. M +D + E + T = L+ I (parent’s resource constraint)

E

ωLL+ ωII≥ k (parent’s capital requirement)

M∗ +D∗ = L∗ + I∗ + T (branch’s resource constraint)

where T denotes the intrafirm transfer (T > 0 when the branch islending to the parent), and rwD denotes the interest rate on wholesaledeposits.

Intra-temporal Problem: Matching Cross-Sectional Facts

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

22 / 30

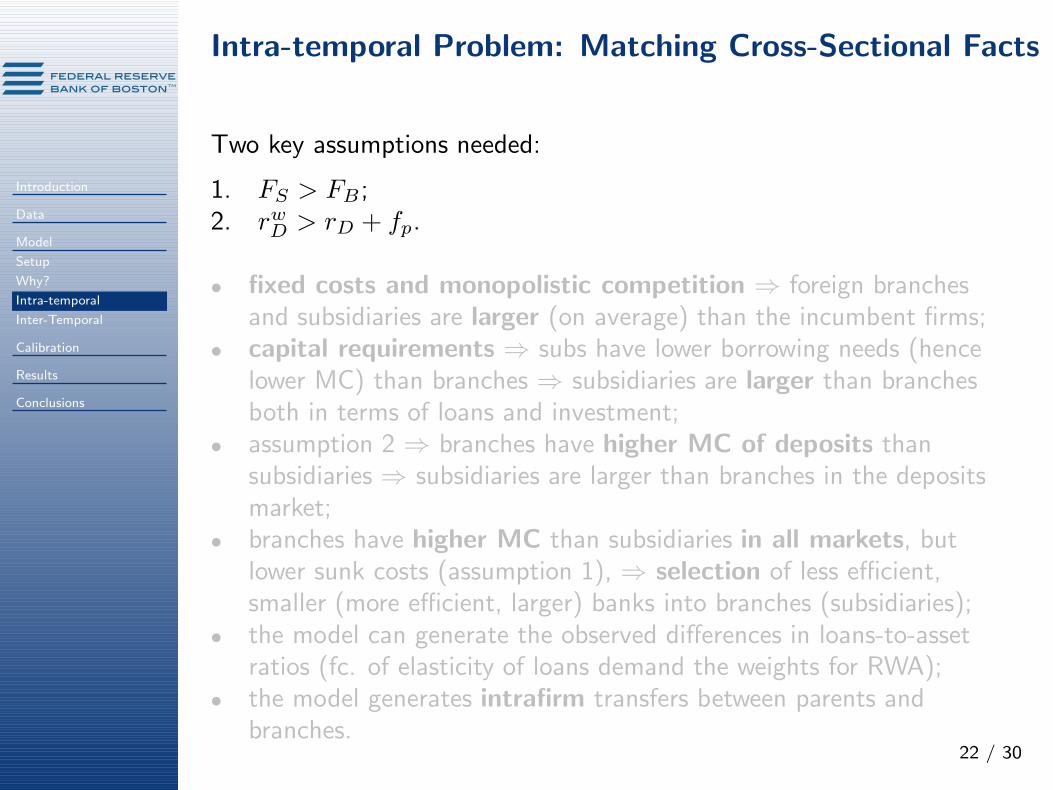

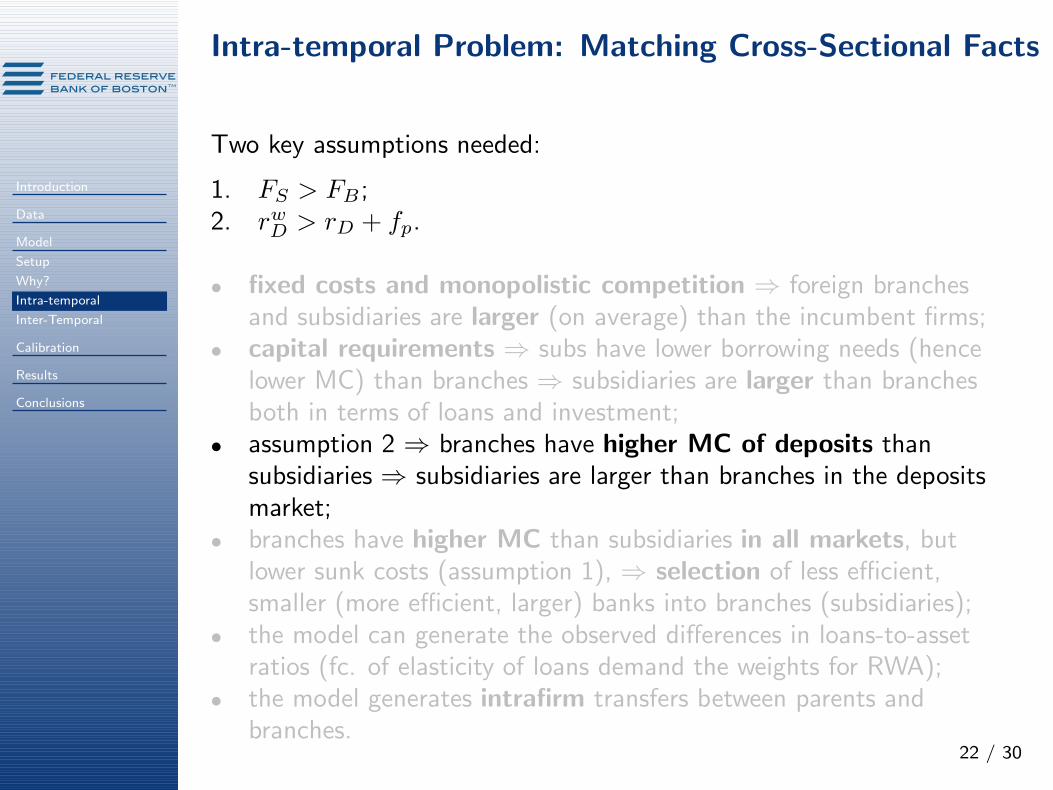

Two key assumptions needed:

1. FS > FB;2. rwD > rD + fp.

• fixed costs and monopolistic competition ⇒ foreign branchesand subsidiaries are larger (on average) than the incumbent firms;

• capital requirements ⇒ subs have lower borrowing needs (hencelower MC) than branches ⇒ subsidiaries are larger than branchesboth in terms of loans and investment;

• assumption 2 ⇒ branches have higher MC of deposits thansubsidiaries ⇒ subsidiaries are larger than branches in the depositsmarket;

• branches have higher MC than subsidiaries in all markets, butlower sunk costs (assumption 1), ⇒ selection of less efficient,smaller (more efficient, larger) banks into branches (subsidiaries);

• the model can generate the observed differences in loans-to-assetratios (fc. of elasticity of loans demand the weights for RWA);

• the model generates intrafirm transfers between parents andbranches.

Intra-temporal Problem: Matching Cross-Sectional Facts

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

22 / 30

Two key assumptions needed:

1. FS > FB;2. rwD > rD + fp.

• fixed costs and monopolistic competition ⇒ foreign branchesand subsidiaries are larger (on average) than the incumbent firms;

• capital requirements ⇒ subs have lower borrowing needs (hencelower MC) than branches ⇒ subsidiaries are larger than branchesboth in terms of loans and investment;

• assumption 2 ⇒ branches have higher MC of deposits thansubsidiaries ⇒ subsidiaries are larger than branches in the depositsmarket;

• branches have higher MC than subsidiaries in all markets, butlower sunk costs (assumption 1), ⇒ selection of less efficient,smaller (more efficient, larger) banks into branches (subsidiaries);

• the model can generate the observed differences in loans-to-assetratios (fc. of elasticity of loans demand the weights for RWA);

• the model generates intrafirm transfers between parents andbranches.

Intra-temporal Problem: Matching Cross-Sectional Facts

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

22 / 30

Two key assumptions needed:

1. FS > FB;2. rwD > rD + fp.

• fixed costs and monopolistic competition ⇒ foreign branchesand subsidiaries are larger (on average) than the incumbent firms;

• capital requirements ⇒ subs have lower borrowing needs (hencelower MC) than branches ⇒ subsidiaries are larger than branchesboth in terms of loans and investment;

• assumption 2 ⇒ branches have higher MC of deposits thansubsidiaries ⇒ subsidiaries are larger than branches in the depositsmarket;

• branches have higher MC than subsidiaries in all markets, butlower sunk costs (assumption 1), ⇒ selection of less efficient,smaller (more efficient, larger) banks into branches (subsidiaries);

• the model can generate the observed differences in loans-to-assetratios (fc. of elasticity of loans demand the weights for RWA);

• the model generates intrafirm transfers between parents andbranches.

Intra-temporal Problem: Matching Cross-Sectional Facts

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

22 / 30

Two key assumptions needed:

1. FS > FB;2. rwD > rD + fp.

• fixed costs and monopolistic competition ⇒ foreign branchesand subsidiaries are larger (on average) than the incumbent firms;

• capital requirements ⇒ subs have lower borrowing needs (hencelower MC) than branches ⇒ subsidiaries are larger than branchesboth in terms of loans and investment;

• assumption 2 ⇒ branches have higher MC of deposits thansubsidiaries ⇒ subsidiaries are larger than branches in the depositsmarket;

• branches have higher MC than subsidiaries in all markets, butlower sunk costs (assumption 1), ⇒ selection of less efficient,smaller (more efficient, larger) banks into branches (subsidiaries);

• the model can generate the observed differences in loans-to-assetratios (fc. of elasticity of loans demand the weights for RWA);

• the model generates intrafirm transfers between parents andbranches.

Intra-temporal Problem: Matching Cross-Sectional Facts

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

22 / 30

Two key assumptions needed:

1. FS > FB;2. rwD > rD + fp.

• fixed costs and monopolistic competition ⇒ foreign branchesand subsidiaries are larger (on average) than the incumbent firms;

• capital requirements ⇒ subs have lower borrowing needs (hencelower MC) than branches ⇒ subsidiaries are larger than branchesboth in terms of loans and investment;

• assumption 2 ⇒ branches have higher MC of deposits thansubsidiaries ⇒ subsidiaries are larger than branches in the depositsmarket;

• branches have higher MC than subsidiaries in all markets, butlower sunk costs (assumption 1), ⇒ selection of less efficient,smaller (more efficient, larger) banks into branches (subsidiaries);

• the model can generate the observed differences in loans-to-assetratios (fc. of elasticity of loans demand the weights for RWA);

• the model generates intrafirm transfers between parents andbranches.

Intra-temporal Problem: Matching Cross-Sectional Facts

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

22 / 30

Two key assumptions needed:

1. FS > FB;2. rwD > rD + fp.

• fixed costs and monopolistic competition ⇒ foreign branchesand subsidiaries are larger (on average) than the incumbent firms;

• capital requirements ⇒ subs have lower borrowing needs (hencelower MC) than branches ⇒ subsidiaries are larger than branchesboth in terms of loans and investment;

• assumption 2 ⇒ branches have higher MC of deposits thansubsidiaries ⇒ subsidiaries are larger than branches in the depositsmarket;

• branches have higher MC than subsidiaries in all markets, butlower sunk costs (assumption 1), ⇒ selection of less efficient,smaller (more efficient, larger) banks into branches (subsidiaries);

• the model can generate the observed differences in loans-to-assetratios (fc. of elasticity of loans demand the weights for RWA);

• the model generates intrafirm transfers between parents andbranches.

Intra-temporal Problem: Matching Cross-Sectional Facts

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

22 / 30

Two key assumptions needed:

1. FS > FB;2. rwD > rD + fp.

• fixed costs and monopolistic competition ⇒ foreign branchesand subsidiaries are larger (on average) than the incumbent firms;

• capital requirements ⇒ subs have lower borrowing needs (hencelower MC) than branches ⇒ subsidiaries are larger than branchesboth in terms of loans and investment;

• assumption 2 ⇒ branches have higher MC of deposits thansubsidiaries ⇒ subsidiaries are larger than branches in the depositsmarket;

• branches have higher MC than subsidiaries in all markets, butlower sunk costs (assumption 1), ⇒ selection of less efficient,smaller (more efficient, larger) banks into branches (subsidiaries);

• the model can generate the observed differences in loans-to-assetratios (fc. of elasticity of loans demand the weights for RWA);

• the model generates intrafirm transfers between parents andbranches.

Inter-temporal Model: Aggregation and Shocks

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

23 / 30

Shocks to aggregate loans demand:

dL

L= µdt+ σdz

dL∗

L∗= µ∗dt+ σ∗dz∗

where µ, µ∗ ≥ 0, σ, σ∗ > 0 and dz, dz∗ are the increments of twostandard Wiener processes with correlation ρ ∈ [−1, 1].

Aggregation:

L =

(∫

L1−1/ηdL

)η/(η−1)

where η > 1 is also the elasticity of demand of each individual loantype.

[“Technical” role of these assumptions: ensure that interest rates on loans

are independent of L, and that each bank’s optimal profits in a country are a

linear affine function of L.]

Inter-temporal Model: Bellman Equations

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

24 / 30

Let Vi(a,L,L∗) denote the value of a bank with efficiency a with

international status i (i ∈ {N,B, S}), when aggregate loan demand inthe two markets is described by (L,L∗):

Vi(a,L,L∗) = S(a,L) + Vi(a,L

∗)

where S(a,L) is the expected p.d.v. of domestic profits (independentof i), and Vi(a,L

∗) is the expected p.d.v. of foreign profits for a bankin status i.

Bellman equations:

S(a,L) = πN (a,L) + E[S(a,L′)|L]

VN (a,L∗) = max{

E[VN (a,L∗′)|a,L∗] ; VB(a,L∗)− FB ; ...

VS(a,L∗)− FS}

VB(a,L∗) = max

{

πB(a,L∗) + E[VB(a,L

∗′)|L∗] ; VN (a,L∗)}

VS(a,L∗) = max

{

πS(a,L∗) + E[VS(a,L

∗′)|L∗] ; VN (a,L∗)}

Inter-temporal Model: Value Functions

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

25 / 30

In the continuation regions:

S(a,L) =πN (a,L)

rM

VN (a,L∗) = AN (a)L∗α +BN (a)L∗β

VB(a,L∗) = AB(a)L

∗α +BB(a)L∗β +

πB

r∗M

VS(a,L∗) = AS(a)L

∗α +BS(a)L∗β +

πS

r∗M

where α and β are the roots of: 12σ

∗2ξ2 + (µ∗ − 12σ

∗2)ξ − rM = 0(α < 0, β > 1).

Value-matching and smooth pasting conditions deliver the parametersAi(a) and Bi(a) (i ∈ {N,B, S}) and the thresholds in aggregate loandemand that induce banks to enter or exit the foreign market (thepolicy function).

What does the Simulated Model Do?

Introduction

Data

Model

Setup

Why?

Intra-temporal

Inter-Temporal

Calibration

Results

Conclusions

26 / 30

• Parameterize the model and generate an economy with a largenumber of domestic banks.1

• Simulate the stochastic process describing aggregate loan demandin each country.

• Every period, the model delivers:

1. banks’ endogenous decisions of foreign entry (by type);2. banks’ endogenous decisions of exit from the foreign market (by

type);3. banks’ domestic and foreign flows of deposits, loans,

investment, interbank borrowing, and intrafirm transfers;4. banks’ domestic and foreign profits depending on the mode of

entry;5. banks’ domestic and foreign risk exposure (computed

theoretically as the covariance of a bank’s profits with domesticloan demand).

1Functional form assumptions: C(D,L, I) ≡ βLL+ βII2

2+ βDD2

2and manage-

ment efficiency x ≡ 1/a distributed according to G(x) = 1− bϑx−ϑ.

Calibration

Introduction

Data

Model

Calibration

SMM

Results

Conclusions

27 / 30

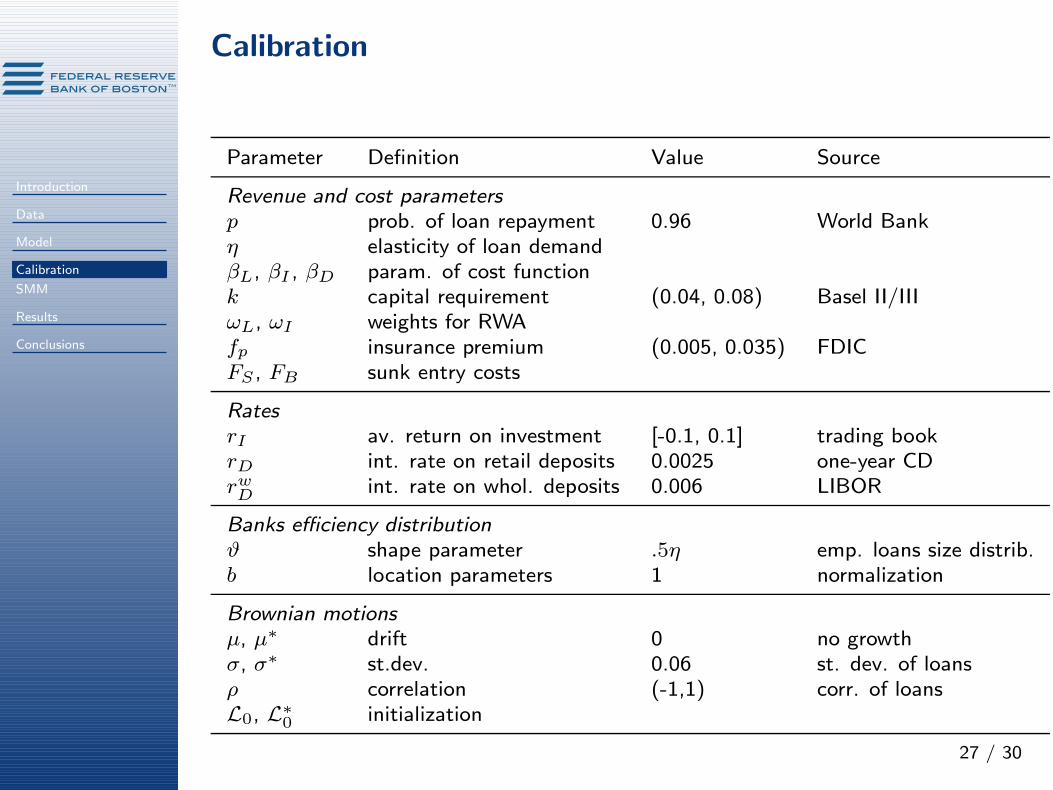

Parameter Definition Value Source

Revenue and cost parameters

p prob. of loan repayment 0.96 World Bankη elasticity of loan demandβL, βI , βD param. of cost functionk capital requirement (0.04, 0.08) Basel II/IIIωL, ωI weights for RWAfp insurance premium (0.005, 0.035) FDICFS , FB sunk entry costs

Rates

rI av. return on investment [-0.1, 0.1] trading bookrD int. rate on retail deposits 0.0025 one-year CDrwD

int. rate on whol. deposits 0.006 LIBOR

Banks efficiency distribution

ϑ shape parameter .5η emp. loans size distrib.b location parameters 1 normalization

Brownian motions

µ, µ∗ drift 0 no growthσ, σ∗ st.dev. 0.06 st. dev. of loansρ correlation (-1,1) corr. of loansL0, L∗

0initialization

Calibration: SMM (ongoing)

Introduction

Data

Model

Calibration

SMM

Results

Conclusions

28 / 30

• Direct calibration of p, k, fp, rI , rD, rwD, ϑ, b, µ, µ∗, σ, σ∗, ρ.

• Remaining 10 parameters: η, βL, βI , βD, ωL, ωI , FS , FB, L0, L∗

0

calibrated jointly to match moments from the data:

– average interest rates on loans (1 moment);– relative size of deposits and loans in branches compared to

subsidiaries (2 moments);– relative loans-to-assets ratios in branches compared to

subsidiaries (1 moment);– percentages of branches and subsidiaries in the total number of

banks in the US (2 moments);– entry and exit dynamics: average share of national banks that

become branches (subsidiaries) each year, and average share ofbranches (subsidiaries) exiting each year (4 moments).

Results and Extensions

Introduction

Data

Model

Calibration

Results

Conclusions

29 / 30

Use the model to evaluate the following counterfactual scenarios:

• changes in deposit insurance and capital requirements rules;• extending interbank transfers to subsidiaries;• elimination of the possibility of opening branches or subsidiaries.

Extensions:

• stochastic rates of return on investments;• shocks to deposits supply.

Conclusions

Introduction

Data

Model

Calibration

Results

Conclusions

30 / 30

• Growing interest (and literature!) on the operations ofmultinational banks.

• In this paper we provide a structural model that is designed toreproduce features of the foreign banking sector, includingendogeneity of entry decisions and the choice of the mode of entry.

• The model has the potential to become a laboratory to conductpolicy analysis.

History of Banking Regulation

Introduction

Data

Model

Calibration

Results

Conclusions

Appendix

Regulation

Size differences

Parameterization

31 / 30

• 1927 – McFadden Act prohibits interstate banking.

• 1978 – International Banking Act:

– brings foreign banks within the federal regulatory framework,– requires deposit insurance for branches of foreign banks engaged

in retail deposit taking in the U.S.

• 1991 – FBSEA (Foreign Bank Supervision Enhancement Act), partof FDICIA (Federal Deposit Insurance Corporation ImprovementAct):

– eliminates deposit insurance for branches of foreign banks.

• 1994 – Riegle-Neal Interstate Banking and Branching EfficiencyAct:

– adequately capitalized and managed Bank Holding Companies(BHCs) are permitted to acquire banks in any state. The law isthe same for both domestic and international banks.

Size Distributions

Introduction

Data

Model

Calibration

Results

Conclusions

Appendix

Regulation

Size differences

Parameterization

32 / 30

0.2

.4.6

.81

F

0 5 10 15 20Log of Total Deposits

Foreign−Subsidiaries Foreign−Branches

Source: only foreign−owned institutions

Date: Q4/2010Cumulative Size Distribution − Deposits

0.2

.4.6

.81

F

5 10 15 20Log of Total Loans

Foreign−Subsidiaries Foreign−Branches

Source: only foreign−owned institutions

Date: Q4/2010Cumulative Size Distribution − Loans

0.2

.4.6

.81

F

0 5 10 15 20Log of Total Assets

Foreign−Subsidiaries Foreign−Branches

Source: only foreign−owned institutions

Date: Q4/2010Cumulative Size Distribution − Assets

On Modeling Deposit Insurance

Introduction

Data

Model

Calibration

Results

Conclusions

Appendix

Regulation

Size differences

Parameterization

33 / 30

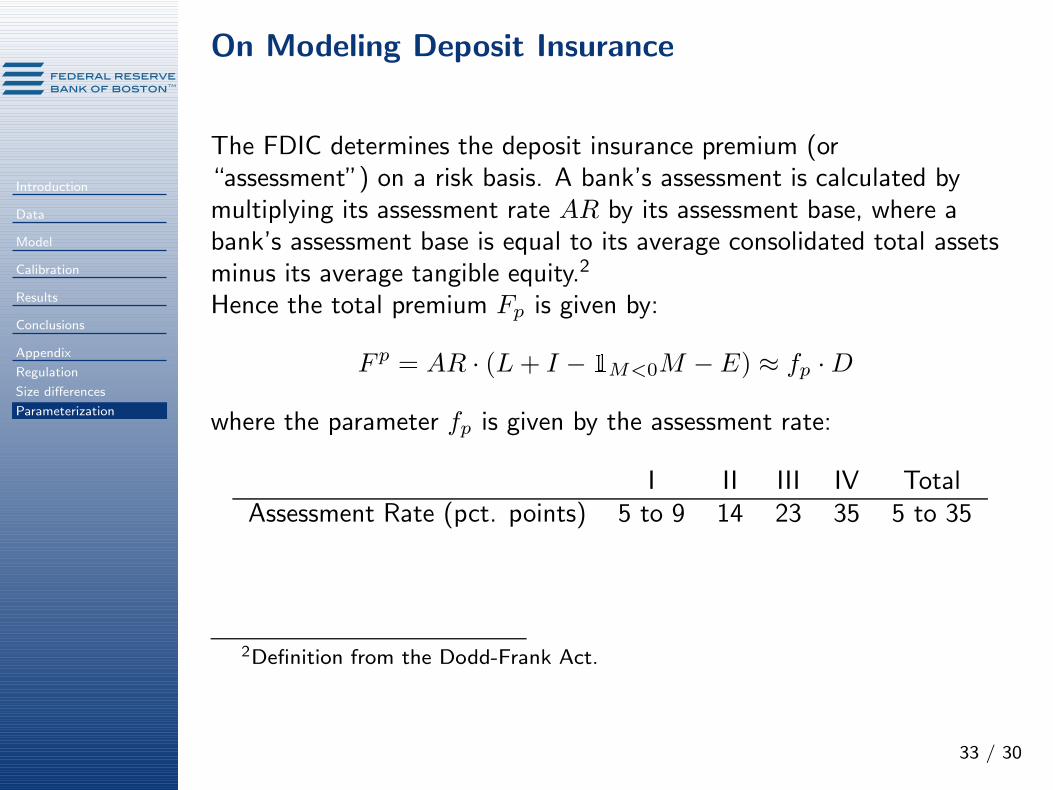

The FDIC determines the deposit insurance premium (or“assessment”) on a risk basis. A bank’s assessment is calculated bymultiplying its assessment rate AR by its assessment base, where abank’s assessment base is equal to its average consolidated total assetsminus its average tangible equity.2

Hence the total premium Fp is given by:

F p = AR · (L+ I − 1M<0M − E) ≈ fp ·D

where the parameter fp is given by the assessment rate:

I II III IV TotalAssessment Rate (pct. points) 5 to 9 14 23 35 5 to 35

2Definition from the Dodd-Frank Act.

On the Loan Size Distribution

Introduction

Data

Model

Calibration

Results

Conclusions

Appendix

Regulation

Size differences

Parameterization

34 / 30

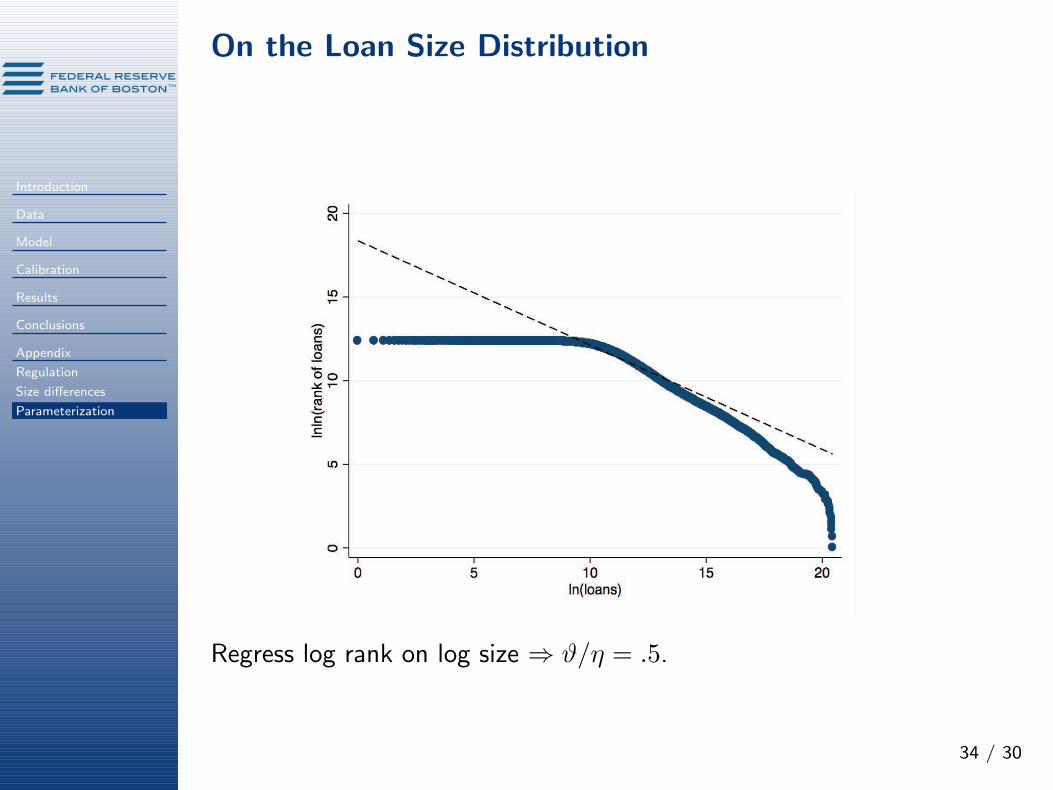

Regress log rank on log size ⇒ ϑ/η = .5.

Recommended