Applied Mathematics and Computation 170 (2005) 1243–1260

www.elsevier.com/locate/amc

Multiparametric sensitivity analysis ofthe constraint matrix in linear-plus-linear

fractional programming problem

Sanjeet Singh a, Pankaj Gupta b,*, Davinder Bhatia c

a Scientific Analysis Group, DRDO, Ministry of Defence, Metcalfe House, Delhi 110054, Indiab Department of Mathematics, Deen Dayal Upadhyaya College, Shivaji Marg,

Karampura, New Delhi 110015, Indiac Department of Operational Research, University of Delhi, Delhi 110007, India

Abstract

In this paper, we study multiparametric sensitivity analysis for programming prob-

lems with linear-plus-linear fractional objective function using the concept of maximum

volume in the tolerance region. We construct critical regions for simultaneous and inde-

pendent perturbations of one row or one column of the constraint matrix in the given

problem. Necessary and sufficient conditions are given to classify perturbation para-

meters as �focal� and �nonfocal�. Nonfocal parameters can have unlimited variations,because of their low sensitivity in practice, these parameters can be deleted from the

analysis. For focal parameters, a maximum volume tolerance region is characterized.

Theoretical results are illustrated with the help of a numerical example.

� 2005 Elsevier Inc. All rights reserved.

Keywords: Multiparametric sensitivity analysis; Maximum volume region; Generalized fractional

programming; Tolerance approach; Parametric programming

0096-3003/$ - see front matter � 2005 Elsevier Inc. All rights reserved.

doi:10.1016/j.amc.2005.01.016

* Corresponding author.

E-mail addresses: [email protected] (S. Singh), [email protected] (P.

Gupta).

1244 S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260

1. Introduction

A general linear-plus-linear fractional programming problem has the follow-

ing form:

ðLLFPÞ Maximize F ðxÞ ¼ cTxþ pTxqTxþ h

subject to Ax ¼ b;

x P 0;

where A is m · n coefficient matrix with m < n; cT, pT and qT are n-dimensionalrow vectors; x and b are n-dimensional and m-dimensional column vectors

respectively and h is a scalar quantity. It is assumed that the feasible regionof the problem (LLFP) is bounded.

Teterev [14] pointed out that such problems arise when a compromise be-

tween absolute and relative terms is to be maximized. Major applications of

the problem (LLFP) can be found in transportation, problems of optimizingenterprise capital, the production development fund and the social, cultural

and construction fund. Teterev [14] derived an optimality criteria for (LLFP)

using the simplex type algorithm. Several authors studied the problem

(LLFP) and its variants and have discussed their solution properties [2,4,6,

10,11,14].

In practical applications the data collected may not be precise, we would like

to know the effect of data perturbation on the optimal solution. Hence, the

study of sensitivity analysis is of great importance. In general, the main focusof sensitivity analysis is on simultaneous and independent perturbation of the

parameters. Besides this, all the parameters are required to be analyzed at their

independent levels of sensitivity. If one parameter is more sensitive than the

others, the tolerance region characterized by treating all the parameters at

equal levels of sensitivity would be too small for the less sensitive parameters.

If the decision maker has the prior knowledge that some parameters can be

given unlimited variations without affecting the original solution then we con-

sider those parameters as �nonfocal� and these �nonfocal� parameters can be de-leted from the analysis. Wang and Huang [15,16] proposed the concept of

maximum volume in the tolerance region for the multiparametric sensitivity

analysis of a single objective linear programming problem. Their theory allows

the more sensitive parameters called as �focal� to be investigated at their inde-pendent levels of sensitivity, simultaneously and independently. This approach

is a significant improvement over the earlier approaches primarily because be-

sides reducing the number of parameters in the final analysis, it also handles

the perturbation parameters with greater flexibility by allowing them to beinvestigated at their independent levels of sensitivity. Singh et al. [13] extended

the results of Wang and Huang [17] to discuss multiparametric sensitivity

S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260 1245

analysis for changes in the objective function coefficients and the right-hand-

side vector of the problem (LLFP).

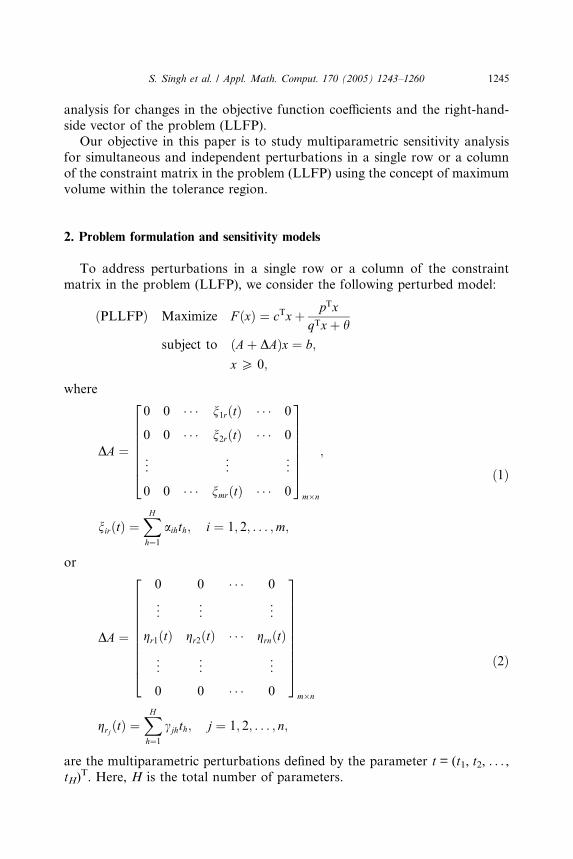

Our objective in this paper is to study multiparametric sensitivity analysis

for simultaneous and independent perturbations in a single row or a column

of the constraint matrix in the problem (LLFP) using the concept of maximum

volume within the tolerance region.

2. Problem formulation and sensitivity models

To address perturbations in a single row or a column of the constraint

matrix in the problem (LLFP), we consider the following perturbed model:

ðPLLFPÞ Maximize F ðxÞ ¼ cTxþ pTxqTxþ h

subject to ðAþ DAÞx ¼ b;

x P 0;

where

DA ¼

0 0 � � � n1rðtÞ � � � 0

0 0 � � � n2rðtÞ � � � 0

..

. ... ..

.

0 0 � � � nmrðtÞ � � � 0

26666664

37777775m�n

;

nirðtÞ ¼XHh¼1

aihth; i ¼ 1; 2; . . . ;m;

ð1Þ

or

DA ¼

0 0 � � � 0

..

. ... ..

.

gr1ðtÞ gr2ðtÞ � � � grnðtÞ

..

. ... ..

.

0 0 � � � 0

26666666664

37777777775m�n

grjðtÞ ¼XHh¼1

cjhth; j ¼ 1; 2; . . . ; n;

ð2Þ

are the multiparametric perturbations defined by the parameter t = (t1, t2, . . . ,tH)

T. Here, H is the total number of parameters.

1246 S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260

Next, we give some notations that are used throughout this study:

B � {1, 2, . . . , n} denotes the index set of basic variables. Without loss ofgenerality, we suppose B = {1, 2, . . . , m}.N = {1, 2, . . . , n}nB denotes the index set of nonbasic variables.AB = The basis matrix with inverse b ¼ A1

B ¼ ½bij�.AN = The submatrix of A corresponding to nonbasic variables.�b ¼ A1

B b P 0; The vector of the values corresponding to xB.

A1B AN ¼ ½yij�.cB = [c1, c2, . . . , cm]

T and cN = [cm+1, cm+2, . . . , cn]T the row vectors of the

objective function coefficients corresponding to basic and nonbasic vari-

ables, respectively.

AÆj = jth column of the matrix A.�Dj = The vector of the reduced cost corresponding to nonbasic variables.

Under the assumptions cTxP 0 and qTx + h > 0 over the feasible region,the optimality criteria for the problem (LLFP) using the simplex type algo-

rithm given by Teterev [14] is stated as follows:

Let AB denotes the optimal basis matrix and let x ¼ xB0

� ¼ ½x1; x2; . . . ;

xm; 0; . . . ; 0�T be the corresponding basic feasible solution to the problem

(LLFP). This solution will be an optimal solution if

Dj ¼ ðzcj cjÞ þZ 00ðzpj pjÞ Z 0ðzqj qjÞ

ðZ 00Þ2P 0 for j ¼ 1; 2; . . . ; n;

where

Z 0 ¼ pTBxB; Z 00 ¼ qTBxB þ h;

zc ¼ cTBA1B AN ; zq ¼ qTBA

1B AN ;

zp ¼ pTBA1B AN :

In general, the sensitivity analysis focuses on characterising sets called as

critical regions over which the entries of the constraint matrix in the problem

(LLFP) may vary simultaneously and independently while still retaining the

same optimal basis index B. Let S be a general notation for a critical region [3].

We now construct the critical regions for changes in the entries of the con-

straint matrix in the problem (LLFP) when perturbations are in the form of (1)or (2).

2.1. Column perturbation

Here, we consider a perturbation in the rth column of A in the form (1) of

the problem (PLLFP).

S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260 1247

Theorem 1. The critical region SNBC of the problem (PLLFP), when perturba-

tions are in the rth column of A and r 2 N is

SNBC ¼ t ¼ ðt1; t2; . . . ; tHÞT �Drm þXHh¼1

Xmi¼1

ciðbi�a�hÞ !

th

�����8>><>>:

þ

PHh¼1

Z 0Pmi¼1qiðbi�a�hÞ Z 00Pm

i¼1piðbi�a�hÞ� �

th

½Z 00�2P 0

9>>=>>;:

Proof. Since any change in the column of a nonbasic variable may violate the

optimality condition in the rth column, therefore we compute D�r , new value of

Dr as follows:

D�r ¼ ðz�cr c�r Þ þ

Z 00ðz�pr p�r Þ Z 0ðz�qr q�r Þ½Z 00�2

: ð3Þ

Now

z�cr c�r ¼ cBA1B A�

�r cr ¼ cBA1B

A1r þ n1rðtÞA2r þ n2rðtÞ

..

.

Amr þ nmrðtÞ

266664

377775 cr

¼ cBA1B A�r þ cBA

1B

XHh¼1

a1hth;XHh¼1

a2hth; . . . ;XHh¼1

amhth

" #T cr

¼ zcr þXHh¼1

Xmi¼1

ciðbi�a�hÞ !

th cr:

Therefore,

z�cr c�r ¼ ðzcr crÞ þXHh¼1

Xmi¼1

ciðbi�a�hÞ !

th:

Similarly,

z�pr p�r ¼ ðzpr prÞ þXHh¼1

Xmi¼1

piðbi�a�hÞ !

th

and

z�qr q�r ¼ ðzqr qrÞ þXHh¼1

Xmi¼1

qiðbi�a�hÞ !

th:

1248 S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260

Using these values in (3), D�r takes the form

D�r ¼ �Drm þ

XHh¼1

Xmi¼1

ciðbi�a�hÞ !

th

þ

PHh¼1

Z 00Pmi¼1piðbi�a�hÞ Z 0Pm

i¼1qiðbi�a�hÞ� �

th

½Z 00�2

Thus the critical region SNBC is given by

SNBC ¼ t ¼ ðt1; t2; . . . ; tHÞT �Drm þXHh¼1

Xmi¼1

ciðbi�a�hÞ !

th

�����8>><>>:

þ

PHh¼1

Z 00Pmi¼1qiðbi�a�hÞ Z 0Pm

i¼1piðbi�a�hÞ� �

th

½Z 00�2P 0

9>>=>>;: �

Definition 1. Parameter th is nonfocal iff

Xmi¼1

ciðbi�a�hÞ þZ 00Pm

i¼1piðbi�a�hÞ Z 0Pmi¼1

qiðbi�a�hÞ

½Z 00�2¼ 0:

Theorem 2. The critical region SBC of the problem (PLLFP), when perturba-

tions are in the rth column of A and r 2 B is

SBC¼ t¼ðt1;t2;...;tH ÞT 1þXHh¼1

ðbr�a�hÞth 6¼0;�����

8>>><>>>:�biþ

XHh¼1

ð�biðbr�a�hÞ�brðbi�a�hÞÞth

" #1þXHh¼1

ðbr�a�hÞth

" #P0;i¼1;2;...;m;

,

�DjþXHh¼1

�Djðbr�a�hÞyrjXmi¼1

ciðbi�a�hÞþZ 00Pm

i¼1piðbi�a�hÞZ 0Pmi¼1qiðbi�a�hÞ

½Z 00�2

! !th

" #

1þXHh¼1

ðbr�a�hÞth

" #P0 for j2N

, 9>>>=>>>;:

S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260 1249

Proof. Since r 2 B, the optimal basis matrix AB will change as a result of per-

turbations and hence XB ¼ A1B b and zcj ¼ cBA

1B A�j, z

pj ¼ pBA

1B A�j, z

qj ¼ qBA

1B A�j

will also change. Therefore a change in AB may disturb both feasibility and

optimality of the current solution.

Let A�B ¼ ½b1; b2; b�r ; . . . ; bm� be the new basis matrix, where

b�r ¼ ½b1r þ n1rðtÞ; b2r þ n2rðtÞ; . . . ; bmr þ nmrðtÞ�T

¼ br þ ½n1rðtÞ; n2rðtÞ; . . . ; nmrðtÞ�T:

Therefore,

A�B ¼ AB þ DAB;

where

DAB ¼

0 � � � n1rðtÞ � � � 0

0 � � � n2rðtÞ � � � 0

..

. ... ..

.

0 � � � nmrðtÞ � � � 0

2666664

3777775:

Let X �B be the new solution corresponding to the basis matrix A�

B. To maintain

the feasibility of the solution, we must have X �B ¼ A�1

B b P 0.

Now,

A�1B ¼ ðAB þ DABÞ1 ¼ ðAB þ FGTÞ1;

where F = [n1r(t), n2r(t), . . . , nmr(t)]T, GT = [0, 0, . . . , 0, 1, 0, . . . , 0].

Applying Bodewig�s formulae [3] to evaluate A�1B , we get

ðAB þ FGTÞ1 ¼ A1B A1

B FGTA1B

1þ GTA1B F

:

Here,

1þ GTA1B F ¼ 1þ

XHh¼1

ðbTr:a:hÞth 6¼ 0:

Therefore,

X �B ¼ A�1

B b ¼ A1B b A1

B FGTA1B b

1þ GTA1B F

¼�bð1þ GTA1

B F Þ A1B FGTA1

B b

1þ GTA1B F

¼ �b

1þ

XHh¼1

ðbr�a�hÞth

!

XHh¼1

�brðb1�a�hÞth; . . . ;XHh¼1

�brðbm�a�hÞth

" # !

1þXHh¼1

ðbr�a�hÞth

" #,:

1250 S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260

Now ith component of X �B is

X �Bi¼

�bi þPH

h¼1ð�biðbr�a�hÞ �brðbi�a�hÞÞth1þ

PHh¼1ðbr�a�hÞth

:

This new solution will be feasible if

�bi þXHh¼1

�biðbi�a�hÞ �brðbi�a�hÞ� �

th

" # "1þ

XHh¼1

ðbi�a�hÞth

#P 0

,;

i ¼ 1; 2; . . . ;m:

For the new solution X �B, to satisfy optimality condition, we compute the new

values D�j of Dj as follows:

D�j ¼ ðz�cj c�j Þ þ

Z 00ðz�pj p�j Þ Z 0ðz�qj q�j ÞðZ 00Þ2

: ð4Þ

Now,

z�cj c�j ¼ cBA�1B A�j cj

¼cBy �j þ

PHh¼1 cBy�jðbr�a�hÞ yrj

Pmi¼1ciðbi�a�hÞ

� �th

� �1þ

PHh¼1ðbr�a�hÞth

cj

¼ðzcj cjÞ þ

PHh¼1ððzcj cjÞðbr�a�hÞ yrj

Pmi¼1ciðbi�a�hÞÞth

1þPH

h¼1ðbr�a�hÞth:

Similarly,

z�pj p�j ¼ðzpj pjÞ þ

PHh¼1 ðzpj pjÞðbr�a�hÞ yrj

Pmi¼1piðbi�a�hÞ

� �th

1þPH

h¼1ðbr�a�hÞth;

z�qj p�j ¼ðzqj qjÞ þ

PHh¼1 ðzqj qjÞðbr�a�hÞ yrj

Pmi¼1qiðbi�a�hÞ

� �th

1þPH

h¼1ðbr�a�hÞth:

Substituting these values in (4), we get

D�j ¼ �Dj þ

XHh¼1

�Djðbr�a�hÞ yrjXmi¼1

ciðbi�a�hÞ "

þ Z 00Pmi¼1piðbi�a:hÞ Z 0Pm

i¼1qiðbi�a�hÞ½Z 00�2

!!th

#1þ

XHh¼1

ðbr�a�hÞth

" #,:

S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260 1251

Therefore critical region SBC is given by

SBC¼ t¼ðt1;t2;...;tH ÞT 1þXHh¼1

ðbr�a�hÞth 6¼0; �biþXHh¼1

�biðbr�a�hÞ�brðbi�a�hÞ� �

th

" #,�����(

1þXHh¼1

ðbr�a�hÞth

" #P0 for i¼1;2;...;m; �Djþ

XHh¼1

�Djðbr�a�hÞyrjXmi¼1

ciðbi�a�hÞ "

þZ 00Pmi¼1piðbi�a�hÞZ 0Pm

i¼1qiðbi�a�hÞ½Z 00�2

!!th

#1þXHh¼1

ðbr�a�hÞth

" #P0; j2N

, ): �

Definition 2. Parameter th is nonfocal if and only if brÆaÆh = 0, �biðbr�a�hÞ�brðbi�a�hÞ ¼ 0 for i = 1, 2, . . ., m and

�Djðbr�a�hÞ yrjXmi¼1

ciðbi�a�hÞ þZ 00Pm

i¼1piðbi�a�hÞ Z 0Pmi¼1qiðbi�a�hÞ

½Z 00�2

!¼ 0

for j 2 N :

To perform sensitivity analysis, we decompose the critical region SBC as

follows:

Let

Sdþ ¼ t ¼ ðt1; t2; . . . ; tH ÞT 1þXHh¼1

ðbr�a�hÞth > 0

�����( )

;

Sd ¼ t ¼ ðt1; t2; . . . ; tH ÞT 1þXHh¼1

ðbr�a�hÞth < 0

�����( )

;

Sbþ ¼ t ¼ ðt1; t2; . . . ; tH ÞT �bi þXHh¼1

½�biðbr�a�hÞ �brðbi�a�hÞ�th P 0;

�����(

i ¼ 1; 2; . . . ;m

);

Sb ¼ t ¼ ðt1; t2; . . . ; tH ÞT �bi þXHh¼1

½�biðbr�a�hÞ �brðbi�a�hÞ�th 6 0;

�����(

i ¼ 1; 2; . . . ;m

);

1252 S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260

SDþ ¼ t ¼ ðt1; t2; . . . ; tH ÞT�����½ �Dj þ

XHh¼1

"�Djðbr�a�hÞ

(

yrjXmi¼1

ciðbi�a�hÞ þZ 00Pm

i¼1piðbi�a�hÞ Z 0Pmi¼1qiðbi�a�hÞ

½Z 00�2

!#th P 0 j 2 N

);

SD ¼(t¼ðt1;t2; . .. ; tH ÞT �Djþ

XHh¼1

�Djðbr�a�hÞ"�����

yrjXmi¼1

ciðbi�a�hÞþZ 00Pm

i¼1piðbi�a�hÞZ 0Pmi¼1qiðbi�a�hÞ

½Z 00�2

!#th60 j2N

):

Then, SBC ¼ ðt ¼ ðt1; t2; . . . ; tHÞT j t 2 fSdþ \ Sbþ \ SDþg or t 2 fSd \ Sb \ SDgÞcan be decomposed into two disjoint regions:

SBCp ¼ fSdþ \ Sbþ \ SDþg and SBCn ¼ fSd \ Sb \ SDg:

2.2. Row perturbation

Consider the perturbations in the rth row of A in the form of (2) of the prob-

lem (PLLFP).

Theorem 3. The critical region SR of the problem (PLLFP), when perturbations

are in the rth row of A in the form (2), is

SR¼ t¼ðt1;t2; .. . ; tH ÞT 1þXHh¼1

ðbT�rc�hÞth 6¼0; �biþXHh¼1

ð�biðbT�rc�hÞ"�����

(

birð�bTc�hÞÞth

#1þXHh¼1

ðbT�rc�hÞth

" #P0; i¼1;2; . .. ;m;

,

and �DjþXHh¼1

�DjðbT�rc�hÞðyT�jc�hcjhÞ cBb�rþZ 00ðpBb�rÞZ 00ðqBb�rÞ

½Z 00�2

! !th

" #

1þXHh¼1

ðbT�rc�hÞth

" #P0 for j2N

, ):

Proof. The proof runs on similar lines as in the proof of Theorem 2 and hence

is omitted here. h

S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260 1253

Definition 3. Parameter th is nonfocal if and only if bT�rc�h ¼ 0, �biðbT�rc�hÞbirð�b

Tc�hÞ ¼ 0 for i = 1, 2, . . ., m and

�DjðbT�rc�hÞ ðy �jc�h cmþj;hÞ cBb�r þZ 00ðpBb�rÞ Z 0ðqBb�rÞ

½Z 00�2

!¼ 0

for j 2 N :

To perform sensitivity analysis, we decompose the critical region SR as

follows:

Let

Sdp ¼ t ¼ ðt1; t2; . . . ; tH ÞT 1þXHh¼1

ðbT�rc�hÞth > 0

�����( )

;

Sdn ¼ t ¼ ðt1; t2; . . . ; tH ÞT 1þXHh¼1

ðbT�rc�hÞth < 0

�����( )

;

Sbp ¼ t ¼ ðt1; t2; . . . ; tH ÞT �bi þXHh¼1

ð�biðbT�rc�hÞ birð�bTc�hÞÞth P 0;

�����(

i ¼ 1; 2; . . . ;m

);

Sbn ¼ t ¼ ðt1; t2; . . . ; tHÞT �bi þXHh¼1

ð�biðbT�rc�hÞ birð�bTc�hÞÞth 6 0;

�����(

i ¼ 1; 2; . . . ;m

);

Scp ¼ t ¼ ðt1; t2; . . . ; tH ÞT �Dj þXHh¼1

�DjðbT�rc�hÞ ðyT�jc�h cjhÞ �����

(

� cBb�r þZ 00ðpBb�rÞ Z 0ðqBb�rÞ

½Z 00�2

!!th P 0 for j 2 N

);

Scn ¼ t ¼ ðt1; t2; . . . ; tHÞT �Dj þXHh¼1

�DjðbT�rc�hÞ ðyT�jc�h cjhÞ �����

(

� cBb�r þZ 00ðpBb�rÞ Z 0ðqBb�rÞ

½Z 00�2

!!th 6 0; for j 2 N

);

1254 S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260

Thus SR can be decomposed into two disjoint regions: SRp = {Sdp \ Sbp \ Scp}and SRn = {Sdn \ Sbn \ Scn}.

Remark 1. For the problem (LLFP), a local optimal solution need not be

global solution [5]. However, if the objective function of the problem (LLFP) is

pseudoconcave over the feasible region then the local optimal is also a globaloptimal solution of the problem (LLFP).

Remark 2. Moreover, if the objective function of (LLFP) is pseudoconvex and

hence pseudolinear, the optimal solution is attained at an extreme point of the

feasible region, which is a compact set [12].

These features of an optimal solution are very valuable from the computa-

tional point of view. The next result provides the conditions which ensure thepseudolinearity of the linear-plus-linear fractional objective function.

Lemma [1]. The function F in the problem (LLFP) is pseudolinearity over the

feasible region of the problem if and only if one of the following conditions holds:

(i) there exists k > 0 such that c = kq and there exists t 2 R such that th > 0

and p = tq;

(ii) there exists k < 0 such that c = kq and there exists t 2 R such that th < 0and p = tq.

However, in this paper, sensitivity analysis has been carried out for the local/

global optimal solution of the problem (LLFP).

Recently, Wang and Huang [15,16] have proposed the concept of maximal

volume region (MVR) within a tolerance region to investigate the focal para-meters at their different levels of sensitivity. The MVR is symmetrically rectan-

gular parallelepiped with the largest volume in a critical region and is

characterized by a maximization problem. This approach is a significant

improvement over the Wendell�s Tolerance approach [8,9,17] primarily becausebesides reducing the number of parameters in the final analysis, it also handles

the perturbation parameters with greater flexibility by allowing them to be ana-

lyzed at their independent levels of sensitivity.

Definition 4 [15]. The Maximum Volume Region (MVR) BS in a critical

region S is given by

BS ¼ ft ¼ ðt1; t2; . . . ; tH ÞT j jtjj 6 k�j ; j ¼ 1; 2; . . . ;Hg;

where k� ¼ ðk�1; k�2; . . . ; k�H Þ is the optimal solution of the following maximiza-tion problem:

S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260 1255

ðP1Þ Maximizek2KðSÞ

V ðkÞ ¼ k1 � k2 � k3 � � � kH ;

where

KðSÞ ¼ fk ¼ ðk1; k2; . . . ; kHÞT j jtjj 6 kj; j ¼ 1; 2; . . . ;H

implies t ¼ ðt1; t2; . . . ; tH ÞT 2 Sg:

The volume of BS is VolðBSÞ ¼ 2H k�1 � k�2 � � � k�H .Since we are interested in characterizing the tolerance region which has the

largest volume, in a given problem, we say that the symmetrically rectangular

parallelepiped Bw ¼ ft ¼ ðt1; t2; . . . ; tH ÞT j jtjj 6 �kj; j ¼ 1; 2; . . . ;Hg of a regionw is the Weak Maximal Volume Region (WMVR) of w if �v ¼ �k1�k2 . . . �kH is theleast upper bound of the set {v = k1k2. . .kH j jtjj 6 kj, j = 1, 2, . . ., H impliest = (t1, t2, . . ., tH)

T 2 w}. Furthermore, if Bw is a subset of w, that is, �v is also themaximum, we say Bw is a Strong Maximal Volume Region (SMVR) of w, anddenote it by B�w.

Remark 3. Let BSBC ¼ ft ¼ ðt1; t2; . . . ; tH ÞT j jtjj 6 �kj; j ¼ 1; 2; . . . ;Hg be a

WMVR of a region SBC. Then BSBC is also a SMVR if and only if

ft ¼ ðt1; t2; . . . ; tH ÞT j jtjj ¼ �kj; j ¼ 1; 2; . . . ;Hg � Sdþ ¼ ft ¼ ðt1; t2; . . . ; tH ÞTj1þPHh¼1ðbr�a�hÞth > 0g.

Remark 4 [16]. The WMVR of SBC is same as the WMVR of SR. Also,

WMVR of SBC is a SMVR of SBC if and only if WMVR of SR is a SMVR of

SR.

Let us suppose that out of H parameters only J parameters are obtained as

focal parameters. Since the critical region is a polyhedral set, there exists

L = [‘ij] 2 RI·J, d = {di} 2 RI, I, J 2 N, where I and J are the number of con-straints and variables of S, respectively, such that S = {t = (t1, t2, . . .,tJ)

T jLt 6 d}. For focal parameters, it is assumed that ‘.j5 0 for j = 1, 2, . . ., J.

Remark 5. It follows from Theorem 1, 2 and 3 that t = 0 belongs to SNBC,

SBC, SR, and thus we have d P 0.

The (MVR) BS of a polyhedral set S = {t = (t1, t2, . . ., tJ)T jLt 6 d} ¼ ft ¼

ðt1; t2; . . . ; tJÞTjPJ

j¼1lijtj 6 di; i ¼ 1; 2; . . . ; Ig, where di P 0 for i = 1, 2, . . . , Iand

PIi¼1jlijj > 0 for j = 1, 2, . . . , J, is BS ¼ ft ¼ ðt1; t2; . . . ; tJ ÞT j jtjj 6

k�j ; j ¼ 1; 2; . . . ; Jg. Here k� ¼ ðk�1; k�2; . . . ; k�J ÞTis uniquely determined with the

following two cases:

1256 S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260

(i) If di > 0 for i = 1, 2, . . . , I, then k* is the unique optimal solution of theproblem (P2), where jLj is obtained by changing the negative elementsof matrix L to be positive

ðP2Þ MaximumY

kj

subject to jLjk 6 d;

k P 0:

(ii) If di = 0 for some i, let I� = {i jdi = 0,i = 1, 2, . . ., I}5 / and

I+ = {i jdi>0,i = 1, 2, . . ., I} then we have:(a) If I+ = / then k* = 0 is the unique optimal solution;

(b) If I+ 5 / then let X ¼S

i2I�fjjlij 6¼ 0; j ¼ 1; 2; . . . ; Jg be the index setof focal parameters that appear in some constraints with right-hand

side di = 0. Then k�j ¼ 0 for all j belonging to X. The others, k�j ,j 62 X, can be uniquely determined as follows: After deleting all vari-ables tj, j 2 X and constraints with right-hand side di = 0 from the sys-

tem of constraints S, let the remaining subsystem be in the form of (5)

with d 0i > 0 for all index i as below:

S0 ¼ ft0 ¼ ½tj�T; j 62 X jL0t0 6 d 0g ð5Þthen k*

0 (i.e., k�j ; j 62 X) can be uniquely determined by solving thefollowing problem (P3):

ðP3Þ MaximumYj 62X

kj

subject to jL0jk0 6 d 0;

k0 P 0:

Multiparametric sensitivity analysis of the problem (PLLFP) can now be per-

formed as follows:

Obtain the critical region as given in Theorems 1–3 by considering perturba-

tions in a single row or a column of the constraint matrix in the problem

(LLFP). Delete all the nonfocal parameters, if any from the analysis. The

MVR of the critical regions is obtained by solving the problem (P2)/(P3).The problem (P2)/(P3) can be solved by existing techniques such as Dynamic

Programming. The detailed algorithm can be found in Wang and Huang

[16]. Software GINO [7] can also be used to solve the nonlinear programming

problem (P2)/(P3).

3. Numerical example

We present the following numerical example to illustrate the theoretical

results developed in this paper.

S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260 1257

ðLLFPÞ Maximize F ðxÞ ¼ ð2x1 þ 6x2 þ 2x3Þ þ3x1 þ 5x2 þ 6x3x1 þ 3x2 þ x3 þ 2

subject to 3x1 x2 þ 2x3 þ x4 ¼ 7;

2x1 þ 4x2 þ x5 ¼ 12;

4x1 þ 3x2 þ 8x3 þ x6 ¼ 10;

xj P 0; j ¼ 1; 2; . . . ; 6:

In view of lemma, it can easily be seen that the objective function F is pseudo-

concave. Hence, local maxima of (LLFP) is also global.

Using simplex type procedure of Teterev [14], the initial and the final

simplex tables are given in Tables 1 and 2.

The optimal solution is

x� ¼ ½x�1; x�2; . . . ; x�6�T ¼ ½4; 5; 0; 0; 0; 11�T ¼ ½4; 5; 11; 0; 0; 0�T

¼ ½Z1; Z2; Z3; . . . ; Z6�T ½say�:

Here B = {1, 2, 3}. The matrix of the optimal basis is

AB ¼3 1 0

2 4 0

4 3 1

264

375 and its inverse b ¼ A1

B ¼

25

110

015

310

0

1 121

264

375:

Table 1

Initial simplex table

Basic variables x1 x2 x3 x4 x5 x6 b

x4 3 1 2 1 0 0 7

x5 2 4 0 0 1 0 12

x6 4 3 8 0 0 1 10

Table 2

Optimal simplex table

qj! 1 3 1 0 0 0

pj! 3 5 6 0 0 0

cj! 2 6 2 0 0 0

qB pB cB Basic x1 x2 x3 x4 x5 x6 b

Variables (z1) (z2) (z3) (z4) (z5) (z6)

1 3 2 x1(z1) 1 0 45

25

110

0 4

3 5 6 x2(z2) 0 1 25

15

310

0 5

0 0 0 x6(z3) 0 0 10 1 12

1 11

ðzcj cjÞ ! 0 0 2 2 2 0

ðzpj pjÞ ! 0 0 1.6 2.2 1.8 0 Z 0 = 37

ðzqj qjÞ ! 0 0 1 1 1 0 Z00 = 21

�Mj ! 0 0 1.84 2.02 2.00 0

1258 S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260

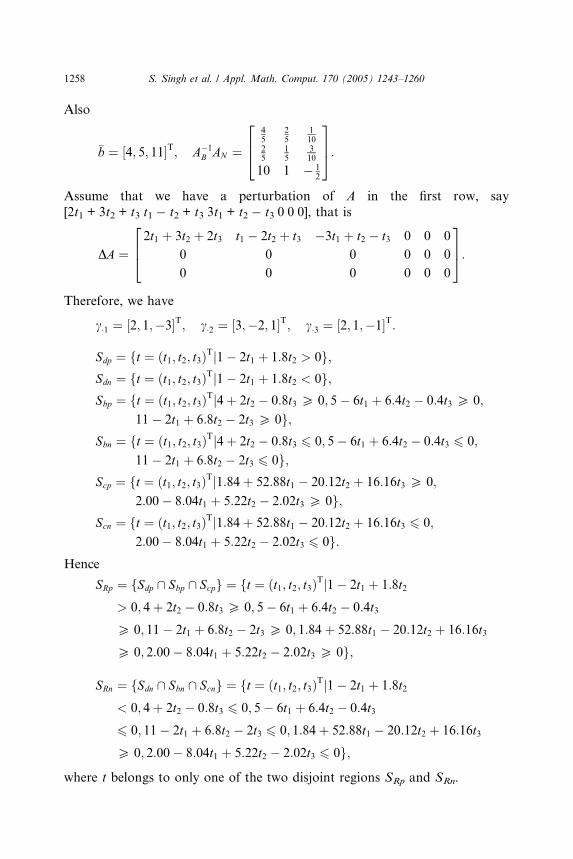

Also

�b ¼ ½4; 5; 11�T; A1B AN ¼

45

25

110

25

15

310

10 1 12

264

375:

Assume that we have a perturbation of A in the first row, say

[2t1 + 3t2 + t3 t1 t2 + t3 3t1 + t2 t3 0 0 0], that is

DA ¼2t1 þ 3t2 þ 2t3 t1 2t2 þ t3 3t1 þ t2 t3 0 0 0

0 0 0 0 0 0

0 0 0 0 0 0

264

375:

Therefore, we have

c�1 ¼ ½2; 1;3�T; c�2 ¼ ½3;2; 1�T; c�3 ¼ ½2; 1;1�T:

Sdp ¼ ft ¼ ðt1; t2; t3ÞTj1 2t1 þ 1:8t2 > 0g;Sdn ¼ ft ¼ ðt1; t2; t3ÞTj1 2t1 þ 1:8t2 < 0g;Sbp ¼ ft ¼ ðt1; t2; t3ÞTj4þ 2t2 0:8t3 P 0; 5 6t1 þ 6:4t2 0:4t3 P 0;

11 2t1 þ 6:8t2 2t3 P 0g;Sbn ¼ ft ¼ ðt1; t2; t3ÞTj4þ 2t2 0:8t3 6 0; 5 6t1 þ 6:4t2 0:4t3 6 0;

11 2t1 þ 6:8t2 2t3 6 0g;Scp ¼ ft ¼ ðt1; t2; t3ÞTj1:84þ 52:88t1 20:12t2 þ 16:16t3 P 0;

2:00 8:04t1 þ 5:22t2 2:02t3 P 0g;Scn ¼ ft ¼ ðt1; t2; t3ÞTj1:84þ 52:88t1 20:12t2 þ 16:16t3 6 0;

2:00 8:04t1 þ 5:22t2 2:02t3 6 0g:Hence

SRp ¼ fSdp \ Sbp \ Scpg ¼ ft ¼ ðt1; t2; t3ÞTj1 2t1 þ 1:8t2

> 0; 4þ 2t2 0:8t3 P 0; 5 6t1 þ 6:4t2 0:4t3

P 0; 11 2t1 þ 6:8t2 2t3 P 0; 1:84þ 52:88t1 20:12t2 þ 16:16t3

P 0; 2:00 8:04t1 þ 5:22t2 2:02t3 P 0g;

SRn ¼ fSdn \ Sbn \ Scng ¼ ft ¼ ðt1; t2; t3ÞTj1 2t1 þ 1:8t2

< 0; 4þ 2t2 0:8t3 6 0; 5 6t1 þ 6:4t2 0:4t3

6 0; 11 2t1 þ 6:8t2 2t3 6 0; 1:84þ 52:88t1 20:12t2 þ 16:16t3

P 0; 2:00 8:04t1 þ 5:22t2 2:02t3 6 0g;

where t belongs to only one of the two disjoint regions SRp and SRn.

S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260 1259

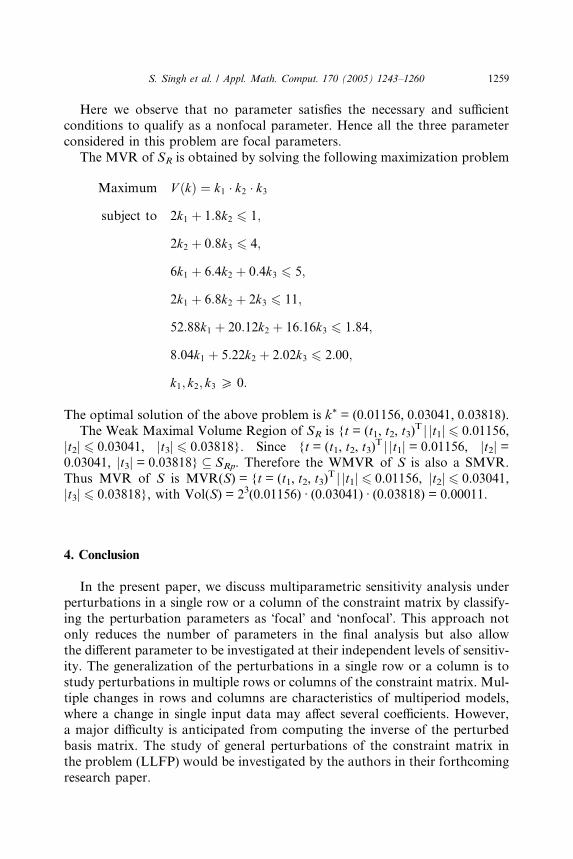

Here we observe that no parameter satisfies the necessary and sufficient

conditions to qualify as a nonfocal parameter. Hence all the three parameter

considered in this problem are focal parameters.

The MVR of SR is obtained by solving the following maximization problem

Maximum V ðkÞ ¼ k1 � k2 � k3

subject to 2k1 þ 1:8k2 6 1;

2k2 þ 0:8k3 6 4;

6k1 þ 6:4k2 þ 0:4k3 6 5;

2k1 þ 6:8k2 þ 2k3 6 11;

52:88k1 þ 20:12k2 þ 16:16k3 6 1:84;

8:04k1 þ 5:22k2 þ 2:02k3 6 2:00;

k1; k2; k3 P 0:

The optimal solution of the above problem is k* = (0.01156, 0.03041, 0.03818).

The Weak Maximal Volume Region of SR is {t = (t1, t2, t3)T j jt1j 6 0.01156,

jt2j 6 0.03041, jt3j 6 0.03818}. Since {t = (t1, t2, t3)T j jt1j = 0.01156, jt2j =

0.03041, jt3j = 0.03818} � SRp. Therefore the WMVR of S is also a SMVR.

Thus MVR of S is MVR(S) = {t = (t1, t2, t3)T j jt1j 6 0.01156, jt2j 6 0.03041,

jt3j 6 0.03818}, with Vol(S) = 23(0.01156) Æ (0.03041) Æ (0.03818) = 0.00011.

4. Conclusion

In the present paper, we discuss multiparametric sensitivity analysis underperturbations in a single row or a column of the constraint matrix by classify-

ing the perturbation parameters as �focal� and �nonfocal�. This approach notonly reduces the number of parameters in the final analysis but also allow

the different parameter to be investigated at their independent levels of sensitiv-

ity. The generalization of the perturbations in a single row or a column is to

study perturbations in multiple rows or columns of the constraint matrix. Mul-

tiple changes in rows and columns are characteristics of multiperiod models,

where a change in single input data may affect several coefficients. However,a major difficulty is anticipated from computing the inverse of the perturbed

basis matrix. The study of general perturbations of the constraint matrix in

the problem (LLFP) would be investigated by the authors in their forthcoming

research paper.

1260 S. Singh et al. / Appl. Math. Comput. 170 (2005) 1243–1260

Acknowledgements

The authors are thankful to the editor and esteemed referees for their eval-

uation of the paper. The authors also wish to express their deep gratitude

Professor R.N. Kaul, Department of Mathematics, University of Delhi, Delhi

and Professor M.C. Puri, Department of Mathematics, I.I.T., Delhi for theirencouragement and inspiration to complete the work.

References

[1] A. Cambini, L. Martein, S. Schaible, On the pseudoconvexity of the sum of two linear

fractional functions, Proceedings of the 7th International Symposium on Generalized

Convexity/Monotonicity, Aug. 27–31, 2002, Hanoi, Vietnam, to appear in Nonconvex

Optimization and its Applications, 77, 2005.

[2] S.S. Chadha, Dual of the sum of a linear and linear fractional program, European Journal of

Operational Research 67 (1993) 136–139.

[3] T. Gal, H.J. Greenberg, Advances in Sensitivity Analysis and Parametric Programming,

Kluwer Academic Press, Boston, MA, 1997.

[4] J. Hirche, On programming problems with a linear-plus-linear fractional objective function,

Cahiers du Centre d�Etudes de Recherche Operationelle 26 (1–2) (1984) 59–64.[5] J. Hirche, A note on programming problems with linear-plus-linear fractional objective

functions, European Journal of Operational Research 89 (1996) 212–214.

[6] H.C. Joksch, Programming with fractional linear objective functions, Naval Research

Logistics Quarterly 11 (1964) 197–204.

[7] J. Liebman, L. Ladson, L. Scharge, A. Waren, Modeling and Optimization with GINO, The

Scientific Press, San Francisco, CA, 1986.

[8] N. Ravi, R.E. Wendell, The tolerance approach to sensitivity analysis of matrix coefficients in

linear programming, Management Science 35 (1989) 1106–1119.

[9] N. Ravi, R.E. Wendell, The tolerance approach to sensitivity analysis of matrix coefficients in

linear programming: general perturbations, Journal of Operational Research Society 36 (10)

(1985) 943–950.

[10] S. Schaible, A note on the sum of a linear and linear fractional functions, Naval Research

Logistics Quarterly 24 (1977) 691–693.

[11] S. Schaible, Fractional programming: Applications and algorithms, European Journal of

Operational Research 7 (1981) 111–120.

[12] S. Schaible, Simultaneous optimization of absolute and relative terms, Z. Angew. Math. Mech.

64 (8) (1984) 363–364.

[13] S. Singh, P. Gupta, D. Bhatia, Multiparametric sensitivity analysis in programming problems

with linear-plus-linear fractional objective function, European Journal of Operational

Research 160 (2005) 232–241.

[14] A.G. Teterev, On a generalization of linear and piecewise linear programming, Matekon 6

(1970) 246–259.

[15] H.F. Wang, C.S. Huang, Multi-parametric analysis of the maximum tolerance in a linear

programming problem, European Journal of Operational Research 67 (1993) 75–87.

[16] H.F. Wang, C.S. Huang, The maximal tolerance analysis on the constraint matrix in linear

programming, Journal of the Chinese Institute of Engineers 15 (5) (1992) 507–517.

[17] R.E. Wendell, The tolerance approach to sensitivity analysis in linear programming,

Management Science 31 (1985) 564–578.

Recommended