Cost Benefit Analysis (CBA) and portfolio development for adaptation options

Dr. Tran Dai NghiaIPSARD

1. Costs of climate change

2. Cost-benefit analysis

3. Valuing the Environment bebefits and costs

4. Problems of measurement of environmental

costs/benefits

5. CBA for Evaluating Proposed CAMs

6. Some example

Contents

3

- Cost benefit analysis is an economic analysis is used to evaluate the desirability of a given intervention/CC adaption measure- The method compares all costs and benefits that can be expressed in monetary terms.- Cost benefit analysis is used to evaluate practices e.g.,improved yields can be realized or/and adapted or/and mitigated climate change. - This also allows farmers to choose the possible efficient strategy/CAM- The CBA focuses on the quantitative evaluation of climate change impacts and allows for estimation of the net benefits of response options/measures

Cost-benefit analysis

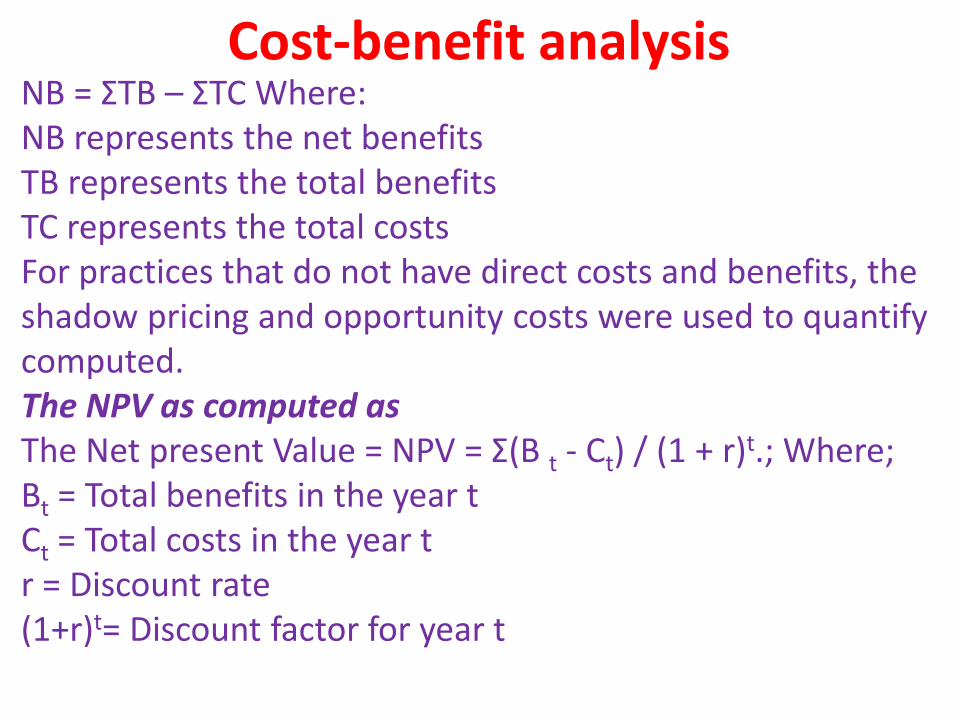

NB = ƩTB – ƩTC Where:NB represents the net benefits TB represents the total benefits TC represents the total costs For practices that do not have direct costs and benefits, the shadow pricing and opportunity costs were used to quantify computed.The NPV as computed asThe Net present Value = NPV = Ʃ(B t - Ct) / (1 + r)t.; Where;Bt = Total benefits in the year tCt = Total costs in the year tr = Discount rate(1+r)t= Discount factor for year t

Cost-benefit analysis

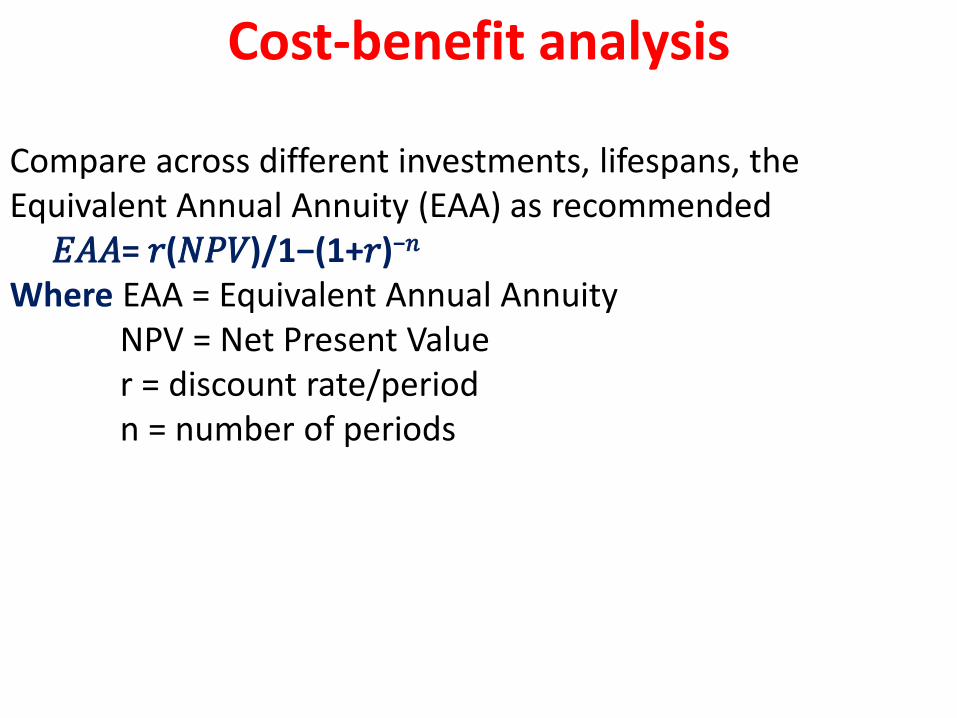

Compare across different investments, lifespans, the Equivalent Annual Annuity (EAA) as recommended𝐸𝐴𝐴= 𝑟(𝑁𝑃𝑉)/1−(1+𝑟)−𝑛

Where EAA = Equivalent Annual AnnuityNPV = Net Present Valuer = discount rate/periodn = number of periods

Cost-benefit analysis

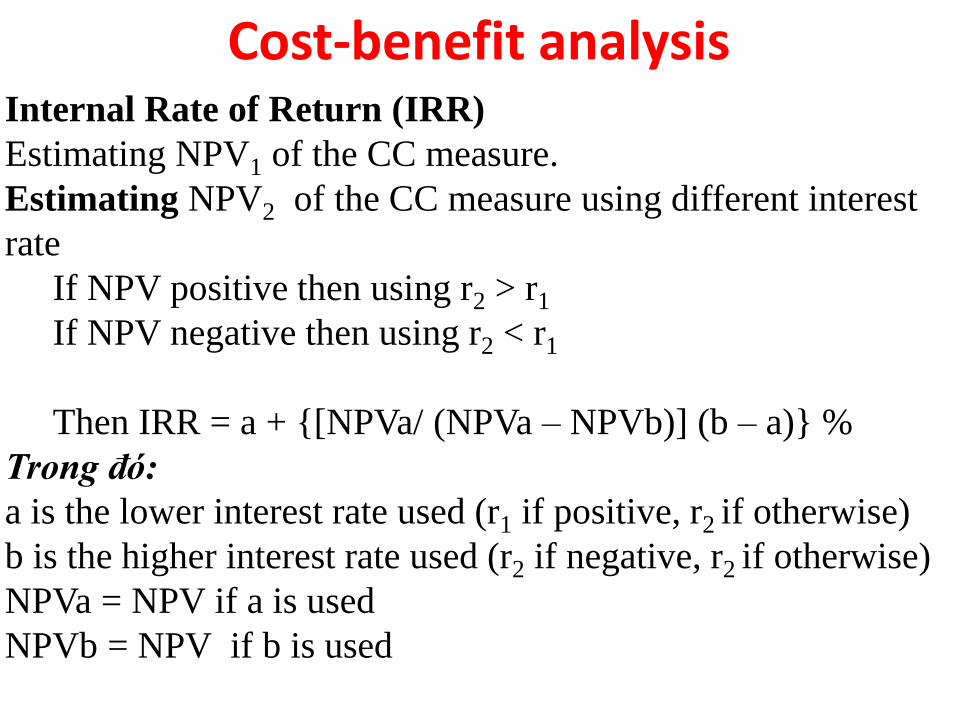

Internal Rate of Return (IRR)

Estimating NPV1 of the CC measure.

Estimating NPV2 of the CC measure using different interest

rate

If NPV positive then using r2 > r1

If NPV negative then using r2 < r1

Then IRR = a + {[NPVa/ (NPVa – NPVb)] (b – a)} %

Trong đó:

a is the lower interest rate used (r1 if positive, r2 if otherwise)

b is the higher interest rate used (r2 if negative, r2 if otherwise)

NPVa = NPV if a is used

NPVb = NPV if b is used

Cost-benefit analysis

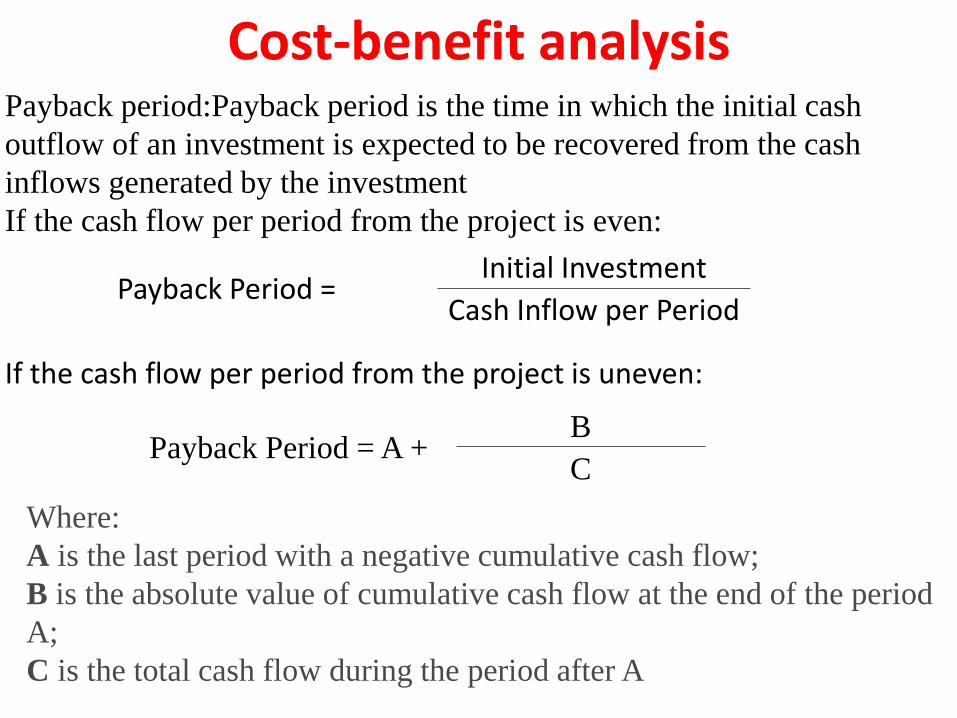

Payback period:Payback period is the time in which the initial cash

outflow of an investment is expected to be recovered from the cash

inflows generated by the investment

If the cash flow per period from the project is even:

If the cash flow per period from the project is uneven:

Cost-benefit analysis

Payback Period =Initial Investment

Cash Inflow per Period

Payback Period = A +B

C

Where:

A is the last period with a negative cumulative cash flow;

B is the absolute value of cumulative cash flow at the end of the period

A;

C is the total cash flow during the period after A

9

Valuing the Environment bebefits and costs:

• A measure used in survey-based valuation techniques,

known as contingent valuation method (CVM), indicates an

individual’s willingness to pay money to obtain some

derived level of a good or service for an improved

environment categorized as either instrumental or intrinsic.

• Instrumental or use value, can be defined as “accruing from

those benefits which are attributed to present consumption

of the goods/resources

• Direct use value may emerge from exchange or outside of

exchange through self-consumption of resources to which

individuals have access.

• Indirect use value is the main consequence of the

ecological functions that the natural resources perform.

10

• Option value refers to willingness of the people to keep the

option of postponing the decision on the use of the

resources.

• Existence value represents the value which an individual is

willing to pay for the environmental amenity, even though

that person receives no direct value. The existence value is

often termed as non-use value.

• Total economic value (TEV) consists of its use value (UV)

and non-use value (NUV)

• TEV = UV + NUV

• Use value may be divided into direct use value (DUV), the

indirect use value (IUV) and the option value (OV).

Therefore, equation (1) can be rewritten as

• TEV = [DUV + TUV + OV] + [NUV]

11

Problems of measurement of environmental

costs/benefitsMarket Prices:

• When there are adverse health effects and loss in productivity

due to environmental damage, market prices are to evaluate

them.

• The procedure is to evaluate damages due to soil erosion,

deforestation, and air and water pollution, GHG. For this

purpose, the ecological relationship between environmental

damages and its effects on production or health are estimated

on the basis of prices to derive monetary values.

• Welfare losses relating to health risks due to polluted

environment are measured by income foregone because of

illness or premature death. Such estimates are difficult to

compute because they rely on loss in income.

12

Costs of Replacement:

People and firms invest in installing alternate devices to avert

environmental damage of air, water and land. Such

investments can provide an estimate of environmental

damage. But the effects of damages cannot be evaluated.

Surrogate Markets:

• The effects of environmental damages on other markets

like property values and wages of workers are also

evaluated.

• Valuation in the case of property is based on risks

involved in evaluating the value of property due to

environmental damage.

• Jobs with high environmental risks will have high wages

which will include larger risk premiums. But this technique

is impracticable because property owners and workers

are ignorant of the effects of environmental damages.

13

Social Discount Rate

Environmental degradation leads to costs and environmental

improvements confer benefits on CAMs.

• The problem of measuring environmental damage is to

evaluate it and compare it with the cost of preventing it.

• The main problem is how to measure costs and benefits of

environmental effects on the present and future

generations. For this, a rate of discount is needed for

discounting all costs and benefits, but there is lot of

confusion.

14

• Discount rates are high, the level of investment falls which discourages development projects and slows down the pace of development, shifts the burden of high costs to future generations.

• The main problem is how to choose a social discount rate. This cannot be the market rate of interest because of uncertainties and imperfections of capital markets.

• Majority of economists measure the social rate of discount at government’s borrowing rates on long-term securities because they are riskless. But there are numerous borrowing rates on government securities relating to different time periods. The problem is which rate to choose as the social discount rate.

• Many economists favour social rate of time preference and opportunity cost of capital in measuring the cost and benefit of environmental degradation.

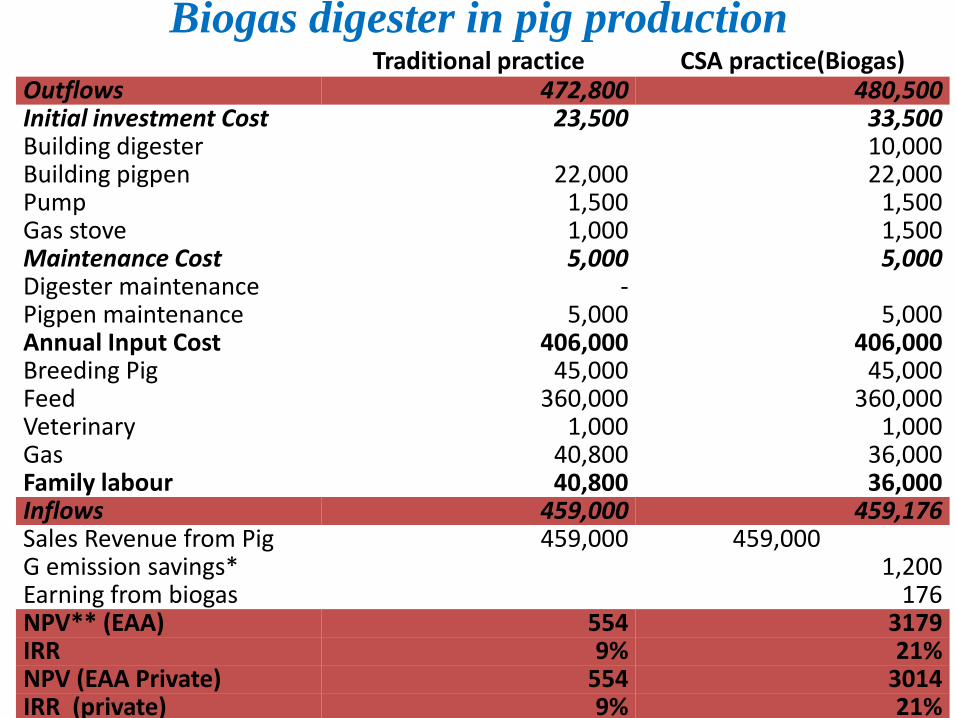

Biogas digester in pig production Traditional practice CSA practice(Biogas)

Outflows 472,800 480,500 Initial investment Cost 23,500 33,500 Building digester 10,000 Building pigpen 22,000 22,000 Pump 1,500 1,500 Gas stove 1,000 1,500 Maintenance Cost 5,000 5,000 Digester maintenance -Pigpen maintenance 5,000 5,000 Annual Input Cost 406,000 406,000 Breeding Pig 45,000 45,000 Feed 360,000 360,000 Veterinary 1,000 1,000 Gas 40,800 36,000 Family labour 40,800 36,000 Inflows 459,000 459,176 Sales Revenue from Pig 459,000 459,000 G emission savings* 1,200 Earning from biogas 176NPV** (EAA) 554 3179IRR 9% 21%NPV (EAA Private) 554 3014IRR (private) 9% 21%

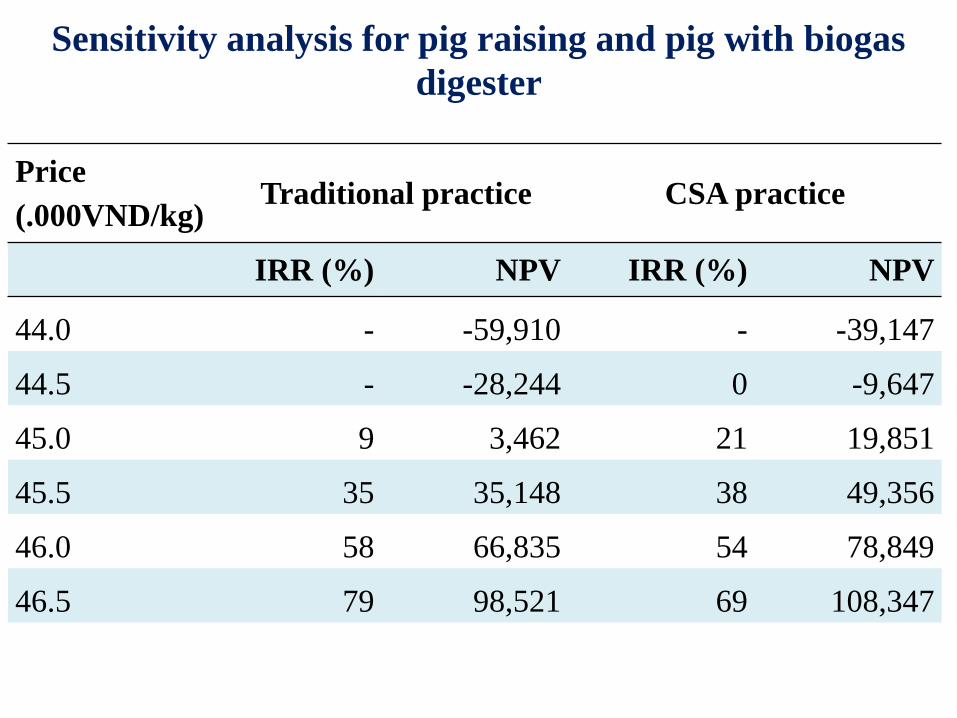

Sensitivity analysis for pig raising and pig with biogas

digester

Price

(.000VND/kg)Traditional practice CSA practice

IRR (%) NPV IRR (%) NPV

44.0 - -59,910 - -39,147

44.5 - -28,244 0 -9,647

45.0 9 3,462 21 19,851

45.5 35 35,148 38 49,356

46.0 58 66,835 54 78,849

46.5 79 98,521 69 108,347

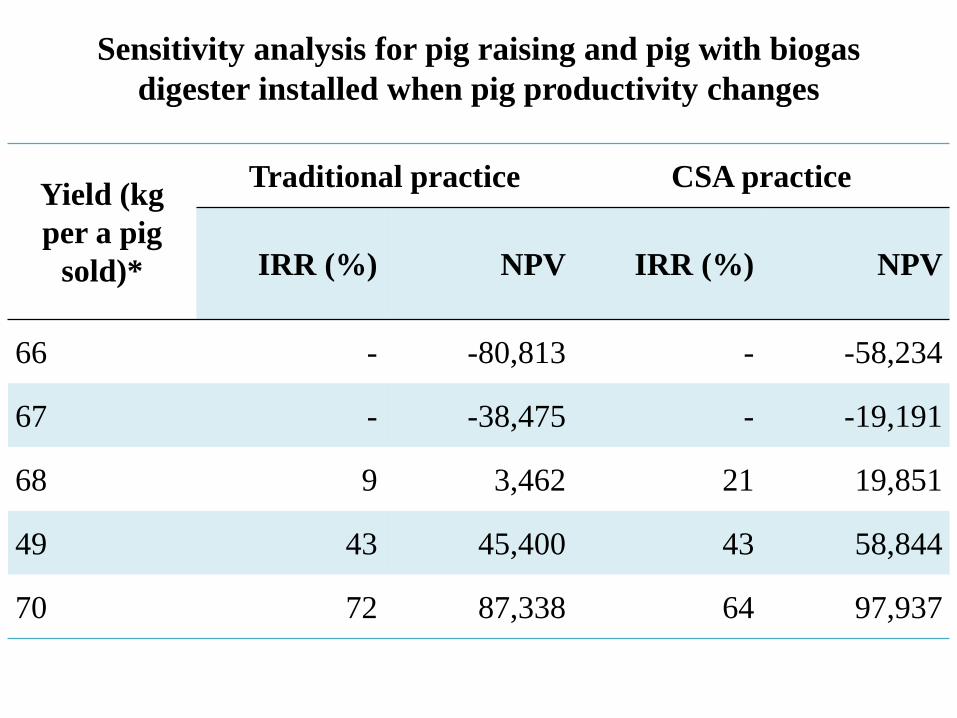

Sensitivity analysis for pig raising and pig with biogas

digester installed when pig productivity changes

Yield (kg

per a pig

sold)*

Traditional practice CSA practice

IRR (%) NPV IRR (%) NPV

66 - -80,813 - -58,234

67 - -38,475 - -19,191

68 9 3,462 21 19,851

49 43 45,400 43 58,844

70 72 87,338 64 97,937

2 rice seasons and rice- shrimp

Traditional practice (rice-rice) CSA practice (rice-shrimp)

Outflows 66876 104641

Rice 66876 39113

Variety 2156 1078

Tillage 6160 3080

Fertilizer 12560 6280

Pesticides 3080 1540

Irrigation 3850 1925

Harvesting 3080 1540

Land rent 11,350 11,350

Family labor 24640 12320

Shrimp

65528

Field digging

3000

Field cleaning

1000

Lime

3850

Variety

1078

Feed

30000

Veterinary

1500

Harvesting

23100

Family labor

2000

Inflows 66200 192764.5

Sales revenue from Rice* 64200 21000

Sales revenue from Straw 2000 1000

Sales revenue from shrimp* 170,000

HG emission savings 765

NPV** -2334 84021

IRR 0% 22%

NPV(family labors excluded) 20818 94359

IRR (family labors excluded) 9.3% 24.1%

NPV(no labor private) 20818 93652

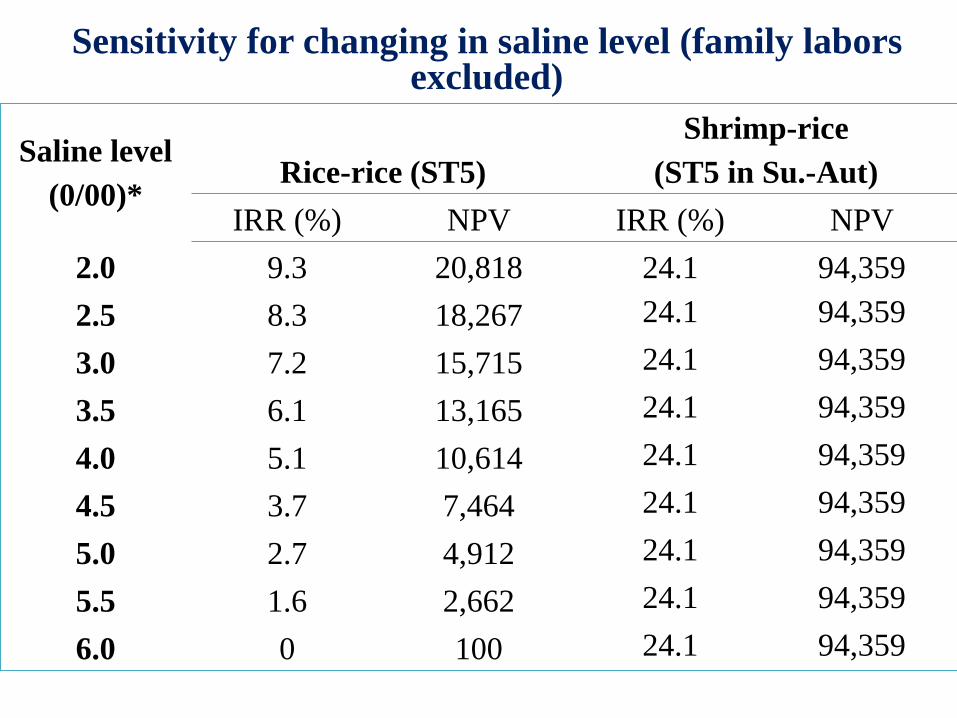

Sensitivity for changing in saline level (family labors excluded)

Saline level

(0/00)*Rice-rice (ST5)

Shrimp-rice

(ST5 in Su.-Aut)

IRR (%) NPV IRR (%) NPV

2.0 9.3 20,818 24.1 94,359

2.5 8.3 18,267 24.1 94,359

3.0 7.2 15,715 24.1 94,359

3.5 6.1 13,165 24.1 94,359

4.0 5.1 10,614 24.1 94,359

4.5 3.7 7,464 24.1 94,359

5.0 2.7 4,912 24.1 94,359

5.5 1.6 2,662 24.1 94,359

6.0 0 100 24.1 94,359

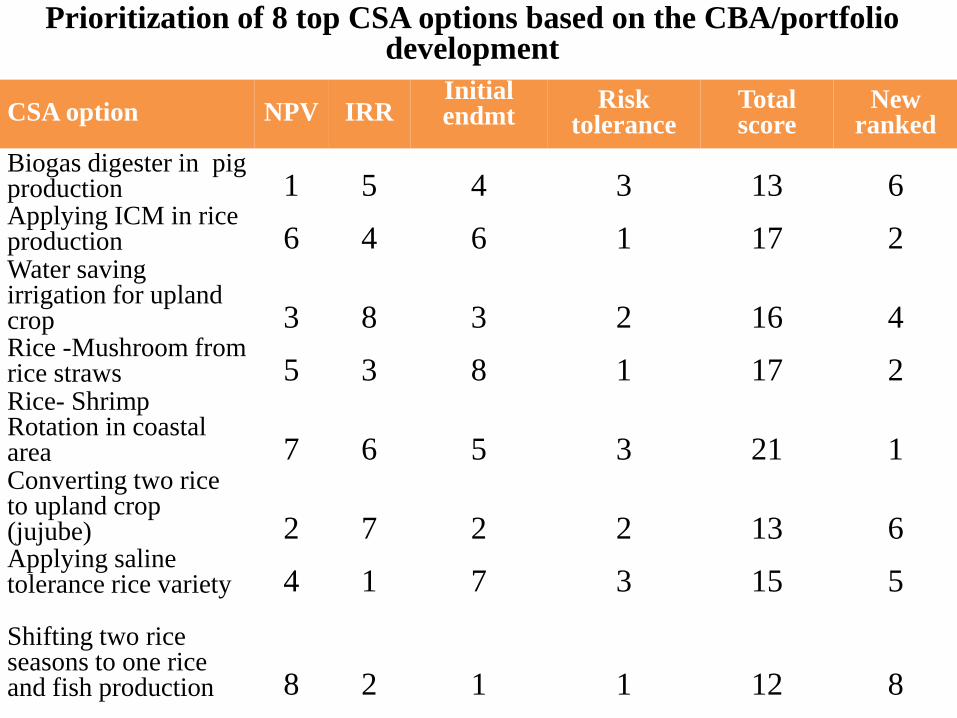

CSA option NPV IRRInitial endmt

Risk tolerance

Total score

New ranked

Biogas digester in pig production 1 5 4 3 13 6Applying ICM in rice production 6 4 6 1 17 2Water saving irrigation for upland crop 3 8 3 2 16 4Rice -Mushroom from rice straws 5 3 8 1 17 2Rice- Shrimp Rotation in coastal area 7 6 5 3 21 1Converting two rice to upland crop (jujube) 2 7 2 2 13 6Applying saline tolerance rice variety 4 1 7 3 15 5

Shifting two rice seasons to one rice and fish production 8 2 1 1 12 8

Prioritization of 8 top CSA options based on the CBA/portfolio development

21

CBA for Evaluating Proposed CAMs

A public cost- benefit framework is appropriate to

assess the desirability of government initiative, such as

green house gas reduction program and application of

different climate change adaptation measures. These

usually involve various social and environmental

impacts of these /measures which the policy makers

want to assess.

- NPV/EAA

- IRR

- Payback period

- Risk tolerance

- Upfront cost

22

THANK YOU!

Recommended