INSIDE THIS ISSUE:

Money Laundering and Terrorist Financing Through Business Email Compromise

Money or Value Transfer Services in the Context of the

AML/CFT Framework

4

Cyber Fraud Prevention and Security Tips

5

NFIU Activities in Numbers 7

NYSC Anti Corruption Group

Honours NFIU Director,

Modibbo HammanTukur

13

Tukur commends INTERPOL for deploying technology to help secure Nigeria, West

Africa

14

GIABA approves evaluation of Sierra Leone

14

NFIU deploys CRIMS to Crime

Fighting Agencies

15

NFIU NEWSLETTER

J U L Y — D E C E M B E R 2 0 2 0 V O L U M E 1 , I S S U E 2

Money Laundering & Terrorist Financing Through Business Email Compromise (BEC)

In 2020, the NFIU produced various strategic products to advise Law Enforcement Agencies (LEAs), Regulatory/Supervisory Authorities and

other AML/CFT stakeholder agencies to adopt a risk-based approach in mitigating the emerging ML/TF risks. In this article, our focus is on

Business Email Compromise (BEC) which has resulted in record global losses amounting to billions of dollars.

From the Director/CEO’s Desk C

OV

ER

Source: www.csmfo.org

As the world continues to adjust to a new nor-

mal in the age of COVID-19, the Nigeria AML/

CFT regime has successfully adapted to the

changing environment in which we find our-

selves. New threats and risks have emerged,

however new opportunities have also come to

the fore.

Looking back over the past 12 months, I am

proud of the work that the NFIU and indeed all

stakeholders have managed to get done in this

difficult period.

The end of year is always a period for reflection,

to assess our successes and learn from our fail-

ures. In the last year, we have faced lockdowns

and partial closures, restrictions of movement

and travel which are particularly important for

an international facing institution such as the

NFIU and a general slowdown in the economy.

Through this all, reporting institutions have con-

tinued to make disclosures, the NFIU has contin-

ued to generate intelligence, and investigations

and prosecutions have not stopped.

We have also continued to leverage technology

in order to improve the speed and efficiency

with which we support our stakeholders. We

have continued to play an important interna-

tional role as members of GIABA and the Eg-

mont Group.

As we look forward to the end of the pandemic

and a return to a more familiar operating envi-

ronment, we will not lose the lessons we have

learnt through this period. Through this news-

letter and our engagements with stakeholders,

in person and virtual, we will improve our feed-

back and work towards a safer more secure

Nigeria.

Money Laundering & Terrorist Financing Through Business Email

Compromise (BEC)

According to the United States Federal Bureau of In-

vestigations (FBI) (2019), between June 2016 and July

2019, global Business Email Compromise/Email Ac-

count Compromise (BEC/EAC) losses totalled over $26

billion. These losses occurred in 166,349 separate inci-

dents across 177 different countries/jurisdictions1.

BEC/EAC is a classic fraud typology that targets both

businesses and individuals who perform legitimate

transfer-of-funds requests. The scam is frequently car-

ried out when a criminal compromises legitimate busi-

ness or personal email accounts through social engi-

neering or computer intrusion with an intention for

financial advantages.

In this report, a quantitative method of analysis was

employed by analysing statistics related to Business

Email Compromise from international requests for

information received by the NFIU.

Findings

From January 2019 to September 2020, forty-seven

(47) requests containing a total of seventy (70) sub-

jects of interest were received by the NFIU. The USA

sent the most requests with a total of fifty-six (56) sub-

jects involved. Requests were also received from Leb-

anon (4), UK (3), Germany (2), Philippines (2), Austral-

ia (1) and Peru (1).

FBI (2019) reports that the USA has been greatly hit by

BEC scams and identified over $12 billion in potential

losses from over 78,000 reported incidents of BEC

fraud, during a recent five-year period (October 2013

to July 2019), involving victims domestically and inter-

nationally2.

The monetary value in the international requests re-

ceived by the NFIU amounted to Eighty-Five Million, Nine Hun-

dred and Forty-Two Thousand, Seven Hundred and Ninety-Five

Dollars Forty-Three Cents ($85,942,795.43). Through the NFIU’s

efforts a total of Four Million, Six Hundred and Seventy-Five

Thousand, Seven Hundred and Nine Dollars, Twenty-Four Cents

($4,675,709.24) has been recovered, amounting to 5% of the total

value in the requests. However, it is important to note that recov-

ery efforts by the NFIU and other competent authorities are still

ongoing.

Rate of Recovery

Most Vulnerable Sectors Susceptible to BEC Scam based on

International requests received by NFIU

1Available on https://www.tripwire.com/state-of-security/security-data-protection/bec-scams-cost-victims-26b-over-a-three-year-period-finds-fbi/ 2Available on https://www.ic3.gov/Media/Y2019/PSA190910

2

Money Laundering & Terrorist Financing Through Business Email Compromise (BEC)

and artificial intelligence for post-delivery protection to

monitor email network systems for malicious emails.

Implement Security Awareness Training and Phishing

Simulation to staff.

Implement a strong identity management and account

system which can serve as a proactive measure to stop

attackers from gaining access to accounts of individuals.

Possible Solutions to Mitigate BEC Related Crimes in the

Financial and Non-Financial Institutions

During the mandatory rendition of STRs and SARs in ac-

cordance with section 6 of the MLPA, Financial and Non-

Financial Institutions should incorporate all relevant in-

formation available, especially the use of key terms like;

“BEC or EAC fraud” including all pertinent cyber-related

information.

The NFIU encourages all institutions to adopt a multi-

faceted transaction verification process within their risk

management approach, as well as training and aware-

ness-building to identify and avoid spear phishing

schemes.

Financial and Non- Financial institutions should adopt a

rapid information sharing system in providing transaction

details and cyber-related information surrounding BEC

scheme when requesting assistance in recovering funds.

The NFIU continues to encourage financial and Non-

Financial institutions collaboration among AML/CFT units

and other relevant units that can assist financial institu-

tions to identify, prevent and report relevant red flags/

indicators and other information related to cyber fraud.

Funds suspected to be proceeds of BEC or cyber fraud

should be initially blocked upon receipt from high-risk

jurisdictions to stop movement pending further actions

before freezing or clearance.

TRENDS AND PATTERNS OF MONEY LAUNDERING FROM IN-TERNATIONAL REQUESTS ON BEC RELATED CRIME BEC Fraud: When Businesses and Organizations Are the Schemed Victims

An attorney is contracted by a new client to handle an off-

shore lease; the client then issued a counterfeit check to

the attorney with instruction to wire transfer part of the

funds. The cheque eventually bounced leaving the attorney

with an overdrawn account.

An unknown individual contacted a law firm via email, and

stated they needed help with an employee settlement. It

was explained they needed assistance from the law firm to

wire funds. An official cheque was mailed to the law firm,

the law firm then wired the money to a correspondent

bank for beneficiary through a Nigerian bank, the cheque

turned out to be counterfeit.

A company’s corporate email was hacked, where mails

were sent to their clients which directed them to submit

payment to bank accounts controlled by the subjects, who

happen to be Nigerians.

EAC: When Individuals Are the Schemed Victims

A victim received a fraudulent email with altered payment

instructions to an account in the victim’s jurisdiction be-

fore subsequently transferring to Nigeria.

Possible Solutions to Mitigate BEC Related Crimes in Vulnera-

ble Agencies and Organizations

Entities should adopt a multi-faceted approach in securing

email gateways. This acts as a firewall for all email commu-

nications, thereby stopping spam, malware and viruses

from being delivered to users via email.

Agencies should adopt the use of machine learning tools

How BEC works

Source:Trendmicro.com

3

Money or Value Transfer Services in the Context of

the AML/CFT Framework After the events of September 11, 2011 in the

United States of America, countries moved to-

wards the regulation of the Money or Value

Transfer Services (MVTS) industry, because of its

role in facilitating Money Laundering and Terror-

ist Financing (ML/TF). According to the Financial

Action Task Force (FATF), MVTS refers to financial

services that involve the acceptance of cash,

cheques, other monetary instruments or other

stores of value and the payment of a correspond-

ing sum in cash or other form to a beneficiary by

a communication, message, transfer or through a

clearing network to which the MVTS provider

belongs. Transactions performed by such ser-

vices can involve one or more intermediaries and

a final payment to a third party, and may include

any new payment methods.

The main feature of MVTS is that it is cheaper

and faster to transmit money to the beneficiary

unlike domestic and international wire transfer

which has more bank charges and might take

several days to process. It is also dynamic and

flexible as it has no set rules. For example, the

payment method changes depending on the ju-

risdiction; however, it includes cash, cheque,

money order, pay-out cards, mobile wallet, bank

deposit or several combinations of the products.

The FATF (2012) Recommendation 14 provides

that countries should take measures to ensure

that natural or legal persons that provide MVTS

are licensed or registered and subject to effective

systems for monitoring and compliance. Similar-

ly, the Central Bank of Nigeria Guidelines for the

Operation of International Money Transfer Ser-

vices (IMTS) states that no person or institution

shall operate international money transfer ser-

vices unless such person/institution has been

licensed by the CBN and maintain accurate infor-

mation on each transaction.

However, unlicensed or informal money transfer

operators still provide alternative channels through

which monies are sent and received all over the

world including Nigeria. This usually involves the use

of underground banking channels where the transac-

tions are settled by offsetting the equivalent sum at

the receiving location. It begins with a transfer re-

quest by the sender at his or her location (country).

The sender provides the funds to the money service

agent for subsequent remittance to the beneficiary

in another country. The money service agent trans-

fers value to the beneficiary through one or series of

network correspondents. In some cases, the actual

movement of funds are not required for value to be

received by the beneficiary. These services have ties

to particular geographic regions and are described

using a variety of specific terms, including hawala,

hundi and fei-chen.

The informal money remittance system has re-

mained a convenient medium for international ter-

rorism financing. Meanwhile, the formal or licensed

MVTS are also deficient in proper book keeping, Cus-

tomer Due Diligence (CDD) and reporting of suspi-

cious transactions. The Guidance for a Risk-Based

Approach (RBA) on MVTS by FATF (2012) Recom-

mendation 1 provides that countries are expected to

identify, assess and understand the Money Launder-

ing and Terrorist Financing risks they are exposed to

and take measures to mitigate those risks. Thus, Fi-

nancial Institutions must ensure and implement risk-

based AML/CFT policies and procedures that remain

proportionate with the ML/TF risks and relevant to

the size and complexity of the institution, services

offered, and customer types.

Alternative remittance system thrive more in a cash

or commodity-oriented economy, and to further

minimize ML/TF risks in informal money remittance,

Nigeria should intensify efforts in its financial inclu-

sion policy to reduce the number of unbanked citi-

zens.

The Central Bank of

Nigeria Guidelines

for the Operation of

International Mon-

ey Transfer Services

(IMTS) states that

no person or insti-

tution shall operate

international mon-

ey transfer services

unless such person/

institution has been

licensed by the CBN

and maintain accu-

rate information on

each transaction.

The Guidance for a Risk-Based Ap-proach (RBA) on MVTS by FATF (2012) Recommen-dation 1 provides that countries are expected to identi-fy, assess and un-derstand the Mon-ey Laundering and Terrorist Financing risks they are ex-posed to and take measures to miti-gate those risks.

4

one cyber threat faced in Nigeria.

It is now common place in Nigeria, for people to get called by

these cybercriminals who claim to be from your bank but then

request that you tell them sensitive details from your ATM

card, a One Time Password, etc. In addition to impersonating

trusted organizations or individuals, cyber criminals have mas-

tered the art of stirring emotions such as fear, anxiety and

greed, consequently altering the victim’s good sense of judge-

ment.

When you experience any of these emotions or you are being

compelled to take an action urgently in a phone conversation

with a stranger, or in an unsolicited email or text message, re-

sist the urge to act immediately. Stop and think before you click

that link or provide any information to someone over the

phone. Use a service like virustotal.com to verify a link or

attachment is safe. Never share sensitive information with any-

one over the phone, because your bank will never call to ask

you for your BVN, CVV, the full long number across your bank

card, OTP or internet banking password.

INVESTMENT, EMPLOYMENT AND CRYPTO/FOREX MULTI-

LEVEL MARKETING SCAMS

Cyber criminals understand people’s need to survive this pan-

demic. For people who find making quick money appealing,

cybercriminals are now setting up ponzi schemes and tricking

people into making investments with unrealistic Return on In-

vestments. These investments or crypto/forex multi-level mar-

keting scams are usually propagated via social media and are

operated in such a way that the testimonials shared on these

Few weeks ago, I received an unsettling call from my friend

who works for a globally recognized multinational; for the pur-

pose of this article, we’ll call her Miss A. Miss A had tried to

add a new beneficiary to her bank account the previous day

but was unsuccessful, so she put her phone aside and contin-

ued with the activities for the day. Coincidentally, the next day,

she received an email that seemed to be from her bank, advis-

ing her that a new beneficiary had been added to her account,

presenting the name and other details of this beneficiary, as

well as a link to take action if she doesn’t recognize the benefi-

ciary. Miss A panicked when she didn’t recognize the new ben-

eficiary, so she clicked the link without giving it a second

thought. The link led to a website that looked just like her

bank’s website and she entered her banking login details, from

there on things got really ugly; her computing device got in-

fected with a malware, she lost money and more.

What Miss A experienced is one of several ways’ cyber fraud

attacks are happening in Nigeria, so if you are reading this arti-

cle, you are in luck! In this article, I will highlight the top five

cyber fraud threats faced by the average person in Nigeria and

how you can protect yourself.

SOCIAL ENGINEERING (PHISHING, SMISHING AND VISHING)

Why go through the hassle of hacking a computer when you

can hack a human? This is the philosophy of a cybercriminal

that uses social engineering to commit cyberfraud. Social engi-

neering involves a cybercriminal manipulating people, often by

impersonating trusted organizations, so they give up confiden-

tial information such as passwords, bank information, debit

card details, etc. The story I started this article with, is a classic

example of social engineering attack This cyber fraud attack

often perpetuated over text, phone or email, is the number

By Confidence Staveley

OPINION

Source: courtesy Rogatnev/bigstockphoto.com

Source: Cybersafe Foundation

5

Cyber Fraud Prevention and Security Tips

platforms are either fake or the scheme just

works for a very short time to drive word of

mouth growth and referrals. Every now and

again, we have a new fraudulent scheme or or-

ganization that defrauds people online and disap-

pears into thin air as they typically do not have

physical office address. If a self-acclaimed invest-

ment company organization presents an invest-

ment opportunity but are not recognized by The

Securities and Exchange Commission in Nigeria,

please do not invest.

Employment scams are also a thing. Fraudsters

target job seekers like young graduates with bo-

gus job opportunities that they need to pay to

qualify for. No well-meaning organization will ask

applicants to pay money to get a job.

MALWARE

A malware is a harmful piece of code, designed

by cyber attackers to cause damage to a compu-

ting device, data or systems. For example, bank-

ing trojans are used by cybercriminals to steal

money, usually by searching for users’ creden-

tials for e-payment and online banking systems,

hijacking one-time passwords, and then passing

that data to the attackers.

You can protect yourself from this type of attack

by using a good and licensed anti-virus, refraining

from opening attachments or links in unsolicited

emails or downloading applications outside the

official app store for your device.

IDENTITY THEFT

As internet adoption increased across Nigeria,

cyber fraud perpetuated by means of identity

theft has become very common place. For exam-

ple, there has been a spike in the number of,

WhatsApp, Instagram, Facebook accounts that

are being hijacked by cybercriminals and used to

spread investment scams, extort victims, black-

mail or defraud friends and family of the victim.

Protect yourself by, choosing strong passwords

that are unique per online account, contain up-

per- and lower-case alphabets, contain special

characters and are at least 8 characters long. It’s

also very important that you turn on 2 Factor

Authentication for all your online accounts, to

provide extra layer of security. If you receive a

call from anybody, requesting for any code from your

phone (usually a one-time password), do not share it.

COVID-19 RELIEF SCAMS As the government seeks to support the most vulner-

able in our society in these trying times, cybercrimi-

nals are also riding on the wave of this pandemic to

defraud people, using bait like fake COVID-19 relief

funds. These harmful links that have been created to

harvest sensitive information about people have

been spreading on social media. It is important that

you only apply for funding and relief opportunities

through government approved websites; usually

these websites will have a green padlock at the top

left corner of the address bar, signifying the website

will transmit your information securely. A genuine

government website will also have an address that

ends with .gov.ng. Fraudsters often disguise the

harmful COVID-19 relieve scam links using URL short-

eners so people cannot tell if its legitimate. Beat

them to their game by lengthening the shortened

web address using a service like checkshorturl.com;

but do not click the link till you have determined its

legitimacy.

The lack of knowledge of these cyber fraud threats

has remained a top reason why people still become

victims of cyber fraud. This is the reason I established

Cybersafe Foundation, a non-governmental organiza-

tion facilitating pockets of changes to make the inter-

net safer for people resident in Nigeria. We share a

lot of resources to educate the public on online safe-

ty issues on our website https://

cybersafefoundation.org/

Connect with us on social media to learn more about

cyber safety.

Confidence Staveley

(Founder Cybersafe Foundation and Top 50 Women

in Cybersecurity Africa)

https://cybersafefoundation.org/

Protect yourself

by, choosing strong

passwords that are

unique per online

account, contain

upper- and lower-

case alphabets,

contain special

characters and are

at least 8 charac-

ters long. It’s also

very important

that you turn on 2

Factor Authentica-

tion for all your

online accounts, to

provide extra layer

of security.

*The views expressed herein are those of the author

and do not necessarily represent the views of the

NFIU

A malware is a

harmful piece of

code, designed by

cyber attackers to

cause damage to a

computing device,

data or systems…

...protect yourself

from this type of

attack by using a

good and licensed

anti-virus, refrain-

ing from opening

attachments or

links in unsolicited

emails or down-

loading applications

outside the official

app store for your

device.

6

NFIU Activities in Numbers

STATISTICS FOR THE SECOND HALF OF 2020

7

Half Year Currency Transaction Reports (CTRs) Jul – Dec 2020

SN Agency Type Processed Rejected Total % of Rejected

1 Banks 16,894 2,205 19,099 11.55

2 Insurance Companies 3,129 108 3,237 3.34

3 Stock brokers 1,042 89 1,131 7.87

4 Asset Management Companies 1,039 122 1,161 10.51

5 Primary Mortgage Institutions 816 25 841 2.97

6 Insurance Brokers 442 26 468 5.56

7 Merchant Banks 405 126 531 23.73

8 Financial Institutions 280 26 306 8.50

9 Finance Companies 77 3 80 3.75

10 Development Financial Institutions 54 0 54 0.00

11 Microfinance Banks 7 6 13 46.15

12 Issuing Houses 6 9 15 60.00

13 Trustees 6 2 8 25.00

14 Other Financial Institutions 2 0 2 0.00

15 Bureau De Change 1 0 1 0.00

Total 24,200 2,747 26,947

8

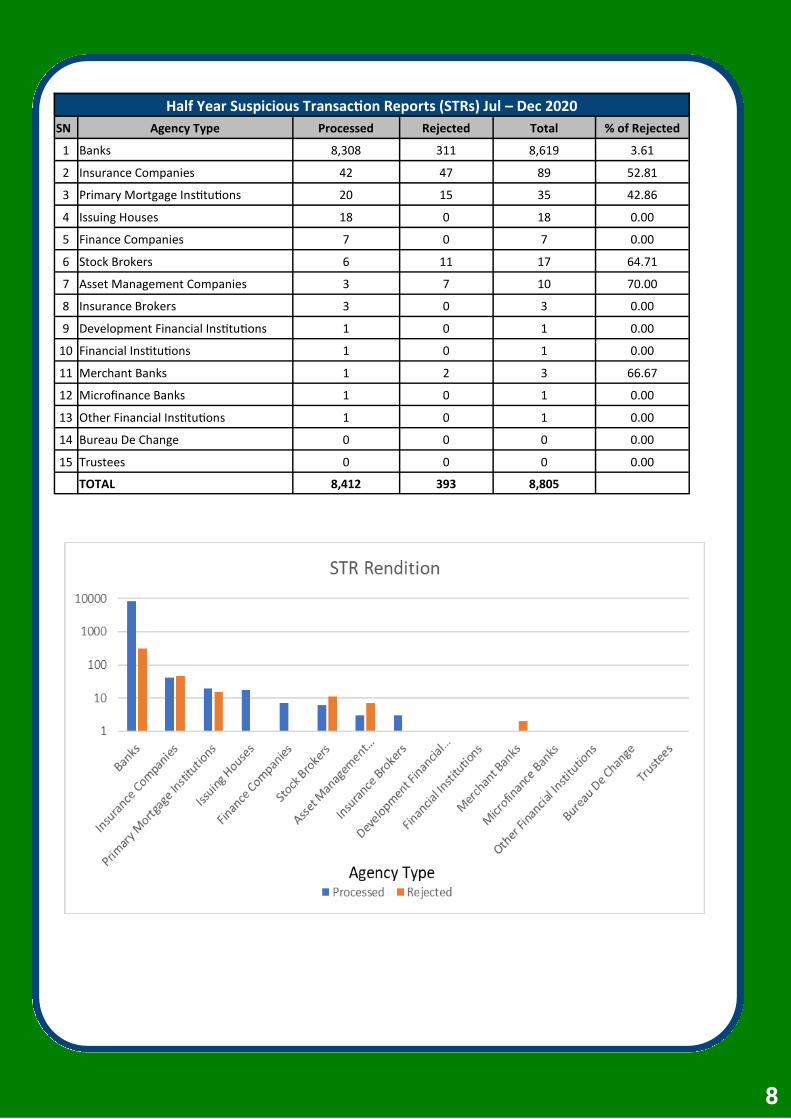

Half Year Suspicious Transaction Reports (STRs) Jul – Dec 2020

SN Agency Type Processed Rejected Total % of Rejected

1 Banks 8,308 311 8,619 3.61

2 Insurance Companies 42 47 89 52.81

3 Primary Mortgage Institutions 20 15 35 42.86

4 Issuing Houses 18 0 18 0.00

5 Finance Companies 7 0 7 0.00

6 Stock Brokers 6 11 17 64.71

7 Asset Management Companies 3 7 10 70.00

8 Insurance Brokers 3 0 3 0.00

9 Development Financial Institutions 1 0 1 0.00

10 Financial Institutions 1 0 1 0.00

11 Merchant Banks 1 2 3 66.67

12 Microfinance Banks 1 0 1 0.00

13 Other Financial Institutions 1 0 1 0.00

14 Bureau De Change 0 0 0 0.00

15 Trustees 0 0 0 0.00

TOTAL 8,412 393 8,805

CTRs Count & Value Jul – Dec 2020

SN Agency Type Trans Count Trans Value (N)

1. Banks 4,953,158 260,689,488,584,144

2. Merchant Banks 38,462 9,603,651,995,257

3. Asset Management Companies 12,182 691,842,881,444

4. Primary Mortgage Institutions 5,668 132,319,019,434

5. Insurance Companies 4,343 158,964,294,355

6. Stock brokers 2,423 104,243,454,303

7. Insurance Brokers 452 27,262,269,423

8. Financial Institutions 280 13,781,539,332

9. Finance Companies 77 4,924,962,668

10. Development Financial Institutions 54 18,311,573,884

11. Trustees 21 849,637,478

12. Microfinance Banks 7 1,892,789,101

13. Issuing Houses 6 100,250,375

14. Other Financial Institutions 2 53,603,123

15. Bureau De Change 1 37,000,000

Total 5,017,136 271,447,723,854,320

STRs Count & Value Jul – Dec 2020

SN Agency Type Trans Count Trans Value (N)

1. Banks 8,401 712,932,654,677

2. Issuing Houses 98 3,931,227,259

3. Insurance Companies 44 1,273,071,666

4. Primary Mortgage Institutions 20 159,409,000

5. Finance Companies 7 837,500,000

6. Stock brokers 6 239,187,465

7. Asset Management Companies 3 199,380,000

8. Insurance Brokers 3 66,014,488

9. Merchant Banks 1 3,810,000

10. Financial Institutions 1 10,000,000

11. Development Financial Institutions 1 17,000,000

12. Microfinance Banks 1 20,000,000

13. Other Financial Institutions 1 25,500,000

14. Trustees 0 0

15. Bureau De Change 0 0

Total 8,587 719,714,754,555

9

10

Submission Statistics (Transaction Count and Value)* CTR STR

Transactions Processed Rejected Processed Rejected

Trans Count 5,017,134 728,940 8,476 739

Trans Value (₦) 271,447,670,251,199 37,956,703,598,927 714,824,512,808 53,612,232,012

Suspicious Activity Reports (SARs) Count Jul - Dec 2019 & 2020

SN Agency Business Trans Count Jul-Dec 2019 Trans Count Jul - Dec 2020 % Change

1 Banks 3,929.00 4,903.00 24.79

2 Insurance Companies 80 69 (13.75)

3 Digital Currency 17 51 200

4 E-Payment Platforms 5 25 400

5 Merchant Banks 3 1 (66.66)

6 Bureau De Change 1 0 (100)

7 Capital Market Operators 1 0 (100)

8 Asset Management Companies 0 1 Nil

Total Number 4,036.00 5,050.00 25.12

Based on the above table, there is an increase in Suspicious Activity Report received across Asset Management Companies, Digital Currency and E-payment platforms in last Half of 2020 compared to last Half of 2019. Decline in suspicious activity reports was observed in Bureau De Change, Insurance Companies, Merchant Banks and Capital

Market Operators in last Half of 2020 compared to last Half of 2019. Overall increase of 25.12% in suspicious Activi-ty reports was observed in the last Half of 2020 compared to last Half of 2019

Half Year Currency Transaction Reports (CTRs) Comparison For 2019 & 2020

SN Agency Business Jul-Dec 2019 Trans Count Jul-Dec 2020 Trans Count % Change

1 Banks 3,546,472 4,953,158 39.66

2 Merchant Banks 15,251 38,462 152.19

3 Asset Management Companies 8,445 12,182 44.25

4 Primary Mortgage Institutions 9,620 5,668 (41.08)

5 Insurance Companies 3,618 4,343 20.04

6 Stock Brokers 1,827 2,423 32.62

7 Insurance Brokers 64 452 (2.59)

Financial Institutions 274 280 2.19

8 Finance Companies 10 77 670.00

9 Development Financial Institutions 86 54 (37.20)

10 Trustee - 21 2,100

11 Micro Finance Banks - 7 700

Issuing Houses 272 6 (97.79)

12 Bureau De Change - 1 100

Other Financial Institutions 1 - (100)

Total Transaction Count 3,586,340 5,017,134 39.90

Total Value(N) 190,389,645,849,134.00 271,447,670,251,199.00 42.57

Based on the table above, it is observed that there is an increase in currency transaction received from Asset Manage-ment companies, Banks, Finance Companies, Financial Institutions, Insurance Companies and Merchant Banks in Sec-ond half of 2020 compared second half of 2019. Micro Finance and Trustee did not file any report in last half of 2019

while they filed 7 and 21 CTR’s in last half of 2020. Overall, there is an increase in CTR received in the last Half of 2020

11

Half Year Suspicious Transaction Reports (STRs) For 2019 & 2020

SN Agency Business Jul-Dec 2019 Trans Count Jul-Dec 2020 Trans Count % Change

1 Banks 5,332 8,401 57.55

2 Insurance Companies 66 44 (33.33)

3 Primary Mortgage Institutions 7 20 185.71

4 Stock Brokers 1 6 500

5 Asset Management Companies 4 3 (25)

6 Merchant Banks 15 1 (93.33)

7 Development Finance Institutions 0 1 Nil

8 Insurance Brokers 2 0 (100)

9 Issuing Houses 1 0 (100)

Total Number 5,428 8,476 56.15

Total Value (N) 137,044,552,719 714,824,512,808 421.60

Based on the table above, a major increase Suspicious Transactions Reports filed to the NFIU was observed across, Banks, Development Financial Institutions, Primary Mortgage Institutions and Stock Brokers in the last Half 0f 2020

compared to last Half of 2019. However, a decline in Suspicious Transactions was observed in the areas of Asset Man-agement Companies, Insurance Brokers, Issuing Houses, Insurance companies and Merchant Banks in the last Half of 2020 compared to last Half of 2019. Overall, there is an increase in suspicious transaction reports in the last half of

2020 compared to last half of 2019 by 56.15%

Half Year Intelligence Reports Disseminated

SN Predicate Offence Jul-Dec 2019 Trans Count Jul-Dec 2020 Trans

Count Difference

1 Fraud 61 139 78

2 Money Laundering 2 58 56

3 Corruption 109 57 -52

4 Tax Evasion 13 41 28

5 Terrorist Financing 26 8 -18

6 Illegal Oil Bunkering 0 7 7

7 Theft/Robbery 1 6 5

8 Illegal Wild Life Trade/Trafficking 0 5 5

9 Fraud (419) 4 2 -2

10 Drug Trafficking 6 1 -5

11 Human Trafficking/Prostitution 3 0 -3

12 Smuggling 2 0 -2

13 Treason 2 0 -2

14 Kidnapping 2 0 -2

15 National Security 1 0 -1

Total Dissemination 232 324 92

Based on the above table,there is a major decline in intelligence desseminated on Corruption, Terrorist Financing, Drug Trafficking, Human Trafficking, Smugling, Treason, Kidnaping and National Security in the last half of 2020 compard to last half of 2019. However, there was a major increase in intelligence desiminated on Fraud,Money Laundry, Tax Evasion, Oil Bunkering, Rubbery and Illegal wildlife trade/Trafficking in the last half of 2020 com-pared to last half of 2019. This could be attributed to the lock down due to COVID-19. Overall, the intelligence

dessiminated in the last half of 2020 has increased by 92 reports compared to the last half of 2019.

12

Half Year Sector Domestic Request for Information Received For 2019 & 2020

SN Agency/Institution No of Request Jul -Dec

2019 No of Request Jul-Dec

2020 Difference

1 Security Agencies 23 7 -16

2 Law Enforcement Agencies 131 149 18

3 Judiciary 2 14 12

4 Legislative Authority 0 1 1

5 Other Competent Authorities 44 42 -2

Total Request for Information Received 200 213 13

Based on the above table, the number of request for information received from Security Agencies and Other competent Authorities have declined in the last Half of 2020 compared to the last Half of 2019. However, the request for infor-

mation received across Law Enforcement, Judiciary and legislative sectors have increased in the last Half 0f 2020 com-pared to last Half of 2019. Overall, there is an increase in request for information received in the last Half of 2020 by 13

compared to the last Half of 2019.

Half Year Outgoing Foreign Requests for Information Jul—Dec 2019 & 2020

SN Countries Number of Request Jul

- Dec 2019 Number of Request Jul - Dec

2020 Difference

1 FIC-S/AFRICA 2 1 -1

2 JFIU-HONGKONG 2 0 -2

3 FIU UK 7 1 -6

4 UAE-FIU 7 0 -7

5 SEPBLAC-SPAIN 1 0 -1

6 SIC-LEBANON 2 0 -2

7 AUSTRAC-AUSTRALIA 3 0 -3

8 FINTRAC-CANADA 2 0 -2

9 FIU GERMANY 2 0 -2

10 FINCEN-USA 16 2 -14

11 FIU-MAURITIUS 1 1 0

12 SEYCHELLES-FIU 1 0 -1

13 CENTIF-NIGER 1 0 -1

14 FIU-CYPRUS 3 0 -3

15 FIU KOREA 1 0 -1

16 SDFM-UKRAINE 1 0 -1

17 MLIU-IRELAND 1 0 -1

18 CENTIF-SENEGAL 0 1 1

19 FIA UGANDA 0 1 1

20 FIU GRENEDA 0 1 1

21 TRACFIN FRANCE 0 1 1

22 FIU INDIA 0 1 1

23 FIU ISLE OF MAN 0 1 1

24 ITALIAN EMBASSEY 0 3 3

25 UIF ITALY 0 1 1

26 JAFIC JAPAN 0 1 1

27 FIU KOREA 0 1 1

28 FCIS LITHUANIYA 0 1 1

TOTAL 53 18 -35

Based on the table above, the NFIU has only forwarded request for information to FIC S/Africa, FIU UK, FINCEN USA and FIU Mauritius in both last two quarters of 2019 and 2020. The NFIU has either forwarded request for information to the other 24 FIUs in the last half of 2019 or last Half of 2020. Overall, the foreign request for information sent by the NFIU in the last

Half of 2020 is less than that of last Half of 2019 by 35 requests.

13

Half Year Incoming Foreign Request For Information Jul - Dec 2019 & 2020

SN Countries Number of Request Jul -

Dec 2019 Number of Request Jul -

Dec 2020 Difference

1 Seychelles 1 0 -1

2 India 1 0 -1

3 Fincen 2 4 2

4 FIA (Uganda) 1 0 -1

5 BVI-FIA 1 0 -1

6 FIU (Portugal) 0 1 1

7 FIU (Korea) 0 1 1

8 FIU (Greneda) 0 1 1

9 FCIS (Lithuania 0 1 1

10 CENTIF(Senegal) 0 1 1

11 CENTIF (Niger) 0 1 1

12 FAU(Czec Republic) 0 1 1

13 NAFI (Cameroon) 0 1 1

Total Request for Information Re-

ceived 6 12 6

Based on the above table, the Number of foreign request for information received by the NFIU in the last half of 2020 is higher than the ones received in the last half of 2019 by 6 requests. Only FINCEN(USA) forwarded

request for information in both last quarters of 2019 and 2020. The other 12 FIUs have either forwarded a re-quest in the last Half of 2019 or the last Half of 2020. Foreign request for information has increased by 6 re-

quests in the last Half of 2020 compared to last Half of 2019.

NFIU Management Team and NYSC Anti Corruption CDS Group

The National Youth Service Corps’ (NYSC), Anti- Corruption

Community Development Service Group, has presented a

Certificate of Endorsement as Anti-Corruption Crusader to the

Director/Chief Executive Officer of the Nigerian Financial

Intelligence Unit, (NFIU), Mr. Modibbo HammanTukur.

The honour was bestowed on Mr HammanTukur in October

at the Headquarters of the NFIU in Abuja.

The CDS group leader, Mohammed Aminu Abbas who

made the presentation remarked that the Director merited

the award after members of the group appraised his

performance in office aince his appointment two years ago.

He made reference to Mr HammanTukur’s devotion to duty

and patriotism.

While expressing gratitude for the award, Mr. Ham-

manTukur declared that the NFIU would partner with the

NYSC Anti-Corruption group in the areas of sensitization

across the nation and to extend the gesture to the group’s

successors.

Community Development Service (CDS), is rated as an

important programme of the NYSC, and have assisted

several host communities positively in various capacities,

since the inception of the scheme in 1973.

NYSC Anti Corruption Group Honours NFIU Director, Modibbo HammanTukur

The Director and Chief Executive Officer of the Nigerian

Financial Intelligence Unit (NFIU), Modibbo HammanTukur,

has commended Interpol Nigeria Office, for its drive towards

the deployment of advanced technology to secure Nigeria

and the West African Sub-Region against the dreadful

activities of men of the underworld.

Mr HammanTukur gave the commendation when he

received a team from the Interpol National Central

Bureau Nigeria on a working visit.

The team was led by the Assistant Inspector General of

Police, Garba Umar Baba.

Mr. HammanTukur, asserted that intelligence remains

paramount to the success of stamping out all-violent

crimes, as the deployment of weaponry, had overtime

proven to be not so effective on its own.

On his part, AIG Baba, reflected on some emerging

trends in criminality and the need for Interpol, as a

national central bureau on crime data, and the NFIU, as

the National AML/CFT data repository with international

links to build on the existing harmonious relationship

between the two organisations.

INTERPOL, created in 1956, is an offshoot of the

International Criminal Police Commission, that was

formed at the 1923 International Police Congress, held in

Vienna. The organization is connected to 194 countries

of the world, usually guided by highly experienced Police

officers and financed by member countries.

14

NFIU Management Team and INTERPOL Nigeria Office Delegation

Member states of the Inter- Governmental Action Group

against Money Laundering in West Africa, (GIABA), has ap-

proved the evaluation of Sierra Leone following the submission

of the 2nd round Mutual Evaluation Report (MER) of

the country after it was presented to the Evaluation and Com-

pliance Group (ECG) during the 34th Hybrid technical commis-

sion/Plenary held from 2nd to 11th December, 2020.

Keys issues on the report were related to Recommendations 1,

5, 6, of the Financial Action Task Force (FATF) and Immediate

Outcome (IO)

The decision, which was taken dur-

ing Plenary also noted “improvements in the country’s legal

and institutional frameworks since its last evaluation in 2007” Source: GiabaEcowas

Director General GIABA, Justice Kimelabalou ABA

Tukur commends INTERPOL for deploying technology to help secure Nigeria, West Africa

GIABA approves evaluation of Sierra Leone

15

adding, however, that “ fundamental gaps necessitated the country being placed on Enhanced Follow-up process and di-

rective issued to present its first Follow-Up Report (FUR) in November 2021.”

Sierra Leone, Liberia and the Gambia are currently being sponsored by Nigeria as they seek to be members of the Egmont

Group of FIUs.

Effectiveness

IO1 IO2 IO3 IO4 IO5 IO6 IO7 IO8 IO9 IO10 IO11

ME LE LE LE LE LE LE LE LE LE LE

Technical Compliance

Recommendation R.1 R.2 R.3 R.4 R.5 R.6 R.7 R.8 R.9 R.10

Rating LC LC LC LC LC PC NC NC C PC

Recommendation R.11 R.12 R.13 R.14 R.15 R.16 R.17 R.18 R.19 R.20

Rating C LC LC PC PC PC PC PC PC C

Recommendation R.21 R.22 R.23 R.24 R.25 R.26 R.27 R.28 R.29 R.30

Rating C PC PC PC PC LC LC PC LC LC

Recommendation R.31 R.32 R.33 R.34 R.35 R.36 R.37 R.38 R.39 R.40

Rating LC PC LC PC LC LC PC PC PC LC

The GIABA Secretariat will publish the MER in 2021, after the quality and consistency review by the Global Network.

NFIU deploys CRIMS to Crime Fighting Agencies

Sequel to the creation and launch of the Crime Records

Information Management System (CRIMS) by the Nigerian

Financial Intelligence Unit (NFIU), in the first quarter of

2020, the Director and Chief Executive Officer of the unit,

Modibbo HammanTukur has set up a committed tasked with

the deployment if the tool to crime fighting agencies across

the nation.

The team, headed by the Special Adviser to the Director/

CEO Dr. Junaid Marshall has already swung into action and

has so far deployed the application to several agencies.

The team’s mandate include practical demonstrations on

how the application works, giving briefs on some extant laws

pertaining to intelligence profiling, offering guidance on the

protocol involved in filling of electronic request forms,

among other vital security issues.

The last quarter of the year 2020, witnessed operational

engagements on CRIMS, at some crime fighting

institutions, which comprised of the Defence Intelligence

Agency (DIA), the Nigerian Air Force Intelligence Corp,

(NAIC) Nigerian Navy Intelligence Corps (NNIC), Nigerian

Army Intelligence Corps (NAIC), Nigeria Immigration

Service, (NIS) The Nigeria Customs Service, (NCS) National

Drug Law Enforcement Agency (NDLEA), National Agency

for the Prohibition of Trafficking in Persons (NAPTIP) and

the Nigerian Security and Civil Defence (NSCDC), Joint Intel-

ligence Board (JIB), Nigeria Police Force (NPF) and Depart-

ment of State Services (DSS).

CRIMS is an application developed by the NFIU to offer fast

solution to the storage and retrieval of information on

crimes and criminals for deployment at designated

locations across the nation.

16

NFIU deploys CRIMS to Crime Fighting Agencies:

Photo News

The Nigerian Financial Intelligence Unit (NFIU) is the central national agency responsible for the receipt of disclosures from reporting organisations, the analysist of these disclosures and the production of intelligence for dissemination to competent authorities. The NFIU is an autonomous unit, domiciled within the Central Bank of Nigeria and the central coordinating body for the country’s Anti-Money Laundering, Counter-Terrorist Financing and Counter-Proliferation Financing (AML/CFT/CPF) framework.

NIGERIAN FINANCIAL INTELLIGENCE UNIT No 12, Ibrahim Taiwo Street Aso Rock Villa, Abuja All feedback should be sent to: [email protected]

Recommended