Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 1

Professor Habib Ahmed Durham University

Presented at the Durham Islamic Finance Autumn School 2011 jointly organised by Durham Centre for Islamic Economics and Finance and ISAR-‐Istanbul Foundation for Research and Education Istanbul Commerce University, Istanbul 19th-‐22nd September 2011

Outline � Introduction

� Product Development System � Product Development Cycle

� Empirical Results

� Issues in PD?

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 2

Introduc.on � A business organization is the sum of its products/services

� Product Development (PD) is an issue related to a bigger problem � How organizations adjust to changing world?

� Future success depends on new products that satisfy the changing markets and needs

� Innovation in Islamic banks is important � Catch up to provide variety of existing services � Provide new innovative products

Clients/Product Types in Banking

• Retail—products cannot be customized to satisfy preferences of each customer – Usually uses standardised products for all clients

• Corporate/Business—uses standardised products with the flexibility to change features – Meet the needs of specific clients.

• Project financing and treasury operations—each transaction can be unique – Need to structure products without delay for quick

implementation • The focus of this session is on standardized

products

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 3

Financing Product: An Example Front End (Experienced by Client) Back End (Not seen by Client)

1. Client fills forms at branch 6. Client signs letter of offer. 7. Client asked to sign documents with

relevant people (lawyer, surveyor, developer, etc.).

8. Upon completion of all formalities, an account created for disbursement.

2. Relevant department (operations) checks status of client/creates a file.

3. File sent to processing centre to cross-check identity and documents.

4. Approving committee makes a decision (depending on the amount may need different levels of approval)

5. Approval and letter of offer sent to the branch.

7a. Lawyers of the banks sign the documents

9. Relevant department handles the

disbursement, documentation and collection.

IT System maintains the records of the transactions during the transaction period

Important Organizational Functions Depts. Functions/Responsibilities Finance Bookkeeping and financial health

Treasury Asset-liability management

RM Identify and control risks

Compliance Ensure compliance with internal and external rules/regulations

Legal Examine legal issues related to transactions

IT Implement/maintain IT systems

Operations Ensure flawless process flow implementation

Marketing Market survey and sale of products

Shari’ah Ensure Shari’ah compliance

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 4

Product Development System • PD a part of the PD System • PD System has three main components

– Strategy and Plans • Mission/Vision and Innovation • Strategy—target market and products

– Structure and Resources • Innovation requires a certain organizational

structure and culture • Innovation is expensive—requires resources

– PD Process • PD is complex involving many departments—need

for structured flow of activities and information

PD Process � A sequence of activities undertaken by different depts. � Distribution of responsibilities

� Product owner—drives the PD process � Usually PD Manager

� Product development cycle � Idea Generation and Acceptance � Converting Concept into Product � Commercialization

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 5

Idea Genera.on and Acceptance 1. Idea Generation 2. Idea Screening 3. Preparation of Concept Paper 4. Shari’ah approval (Concept) 5. Business Case 6. Authorization

Conver.ng Concept into Product 1. Product Design & Process Flow 2. Sign-‐off from Relevant Departments 3. Documentation 4. Shari’ah Approval (Documents & Process flow) 5. Develop IT Systems 6. In-‐house Testing

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 6

Commercializa.on 1. Personnel Training 2. Pilot-‐run 3. Marketing Program 4. Full Scale Launch 5. Post-‐Launch Review 6. Shari’ah Audit

Outline • Introduction

• Product Development System – Product Development Cycle

• Empirical Results

• Issues in PD?

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 7

Survey on PD in IBs � Survey of a total of 20 independent Islamic banks from 12 countries � 17 commercial banks � 2 investment banks � 1 cooperative bank.

Status of Idea Genera.on and Acceptance

STEPS Always Undertaken (No. of Banks)

Percentage of Total

A.1. Structured idea genera.on process 8 40%

A.2. Formal Idea screening process 8 40%

A.3. Development of Concept paper for new product

12 60%

A.4. Approval of Concept by Shari’ah Board 16 80%

A.5. Detailed Business case 11 55%

A.6. Authoriza.on to develop product by senior management

18 90%

Average 12.2 60.8%

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 8

Status of Conver.ng Concept into Product STEPS Always

Undertaken (No. of Banks)

Percentage of Total

B.1. Product Design and Process Flow 15 75%

B.2. Sign-‐off from various Relevant Departments

15 75%

B.3. Prepara.on of documenta.ons 18 90%

B.4.Shari’ah Approval (documents and process flow)

18 90%

B.5. Development of IT system 17 85%

B.6. In-‐house tes.ng 18 90%

Average 16.8 84.2%

Status of Commercialisa.on STEPS Always

Undertaken (No. of Banks)

Percentage of Total

C.1. Training of personnel 16 80%

C.2. Pilot-‐run of the product 15 75%

C.3. Marke.ng Programme 15 75%

C.4. Full-‐scale launch 11 55%

C.5. Post launch review 12 60%

C.6 Shari’ah Audit of the product 12 60%

Average 13.5 67.5%

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 9

Averages for PD Phases Product Development Phase Number of

Banks Percentage of Total

Idea Genera.on and Acceptance 12.2 60.8%

Conver.ng Concept into Product 16.8 84.2%

Commercializa.on 13.5 67.5%

Factors Ranks Weighted Total Score

1st 2nd 3rd 4th 5th Financial considera.ons 3 6 3 5 1 59

Market considera.ons 4 3 2 5 5 53

Fit with corporate strategy and plan

2 3 5 2 2 43

Resource availability 0 0 2 2 4 14

Shari’ah compliance 10 2 3 1 2 71

Islamic values (equity, risk-‐sharing, etc.)

0 4 3 3 4 35

Criteria used to Indentify Development of New Products

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 10

Outline • Introduction

• Product Development System – Product Development Cycle

• Empirical Results

• Issues in PD?

Issues in PD in Islamic Finance � Islamic worldview and Islamic finance

� A moral economy: if there is a conflict between the material gains and ethical principles, the latter should prevail

� Products should fulfil the form and spirit of Islamic law (maqasid al-‐Shari’ah) � Legal requirements � Social requirements

� How can the maqasid be reflected at the product level?

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 11

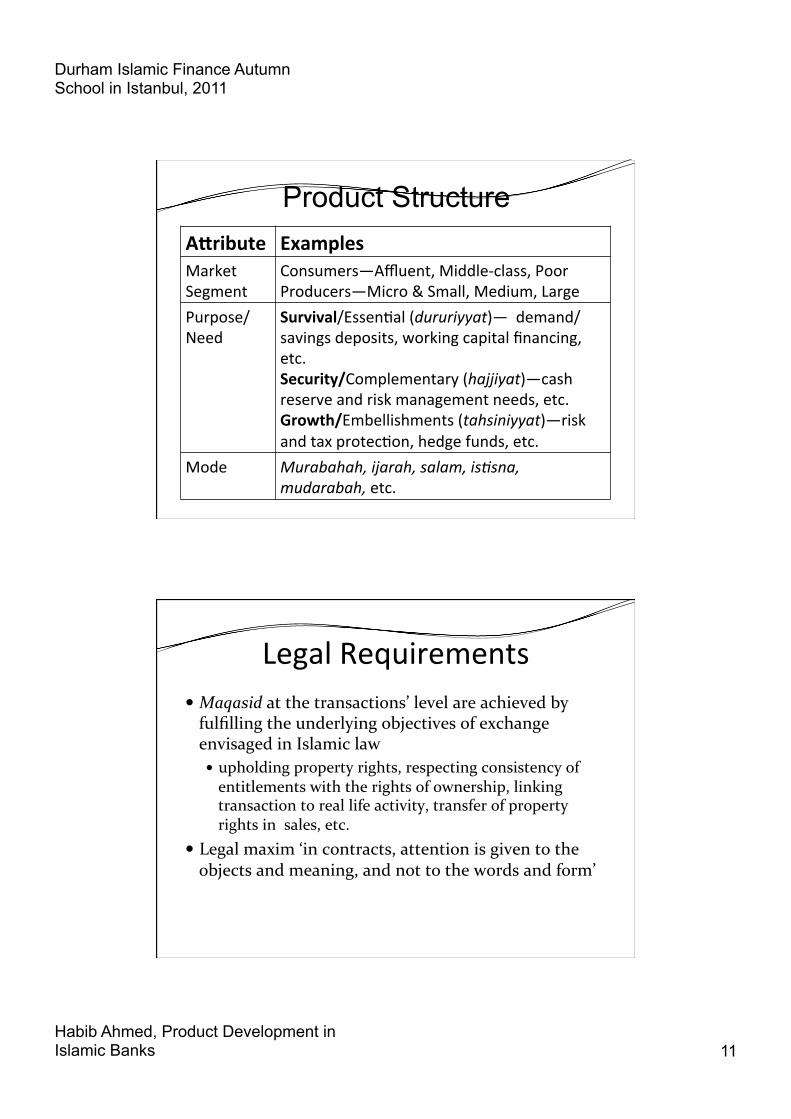

AIribute Examples Market Segment

Consumers—Affluent, Middle-‐class, Poor Producers—Micro & Small, Medium, Large

Purpose/ Need

Survival/Essen.al (dururiyyat)— demand/savings deposits, working capital financing, etc. Security/Complementary (hajjiyat)—cash reserve and risk management needs, etc. Growth/Embellishments (tahsiniyyat)—risk and tax protec.on, hedge funds, etc.

Mode Murabahah, ijarah, salam, is3sna, mudarabah, etc.

Product Structure

Legal Requirements � Maqasid at the transactions’ level are achieved by fulfilling the underlying objectives of exchange envisaged in Islamic law � upholding property rights, respecting consistency of entitlements with the rights of ownership, linking transaction to real life activity, transfer of property rights in sales, etc.

� Legal maxim ‘in contracts, attention is given to the objects and meaning, and not to the words and form’

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 12

Social Requirements Needs/Segments Matrix

Segments Needs

Poor/ Micro & Small

Middle Class/ Medium

Affluent / Large

Survival (necessities)

A1 B1 C1

Security (complementary)

A2 B2 C2

Growth (luxuries)

A3 B3 C3

� Not fulfilling Social Requirements—products satisfying A3, B2, B3, C1, C2, C3

� Fulfilling Social Requirements—products satisfying A1, A2, B1, B2

Product Types Legal Social

Form Substance Market segment

Needs

Pseudo Shari’ah Compliant

√ ? ? ?

Shari’ah compliant

√ √ ? ?

Shari’ah based √ √ √ √

Classifica.on of Products

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 13

Islamic Products—Who Decides? • Board of Directors (BOD)/Management—

strategic positioning – Profit versus ethical principles/social goals

• Shari’ah Supervisory Board (SSB)—SSB gatekeepers of Islamic finance – All products coming to the market are

approved by SSB – Should SSB only oversee legal issues or

should it also ensure ethical principles/social goals?

Islamic Products—Who Decides? • Sign-off from relevant departments

– Risk Management

– Finance/Treasury

– Legal

– Compliance

– IT

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 14

Islamic Products—Who Decides? An Example

• Working Capital Requirements – Temporary musharakah

• The bank and client enters into a temporary partnership for a limited period of time

• At the end of contract period profit-share and capital of the bank is paid back (any loss shared by bank and client)

– Murabahah—bank buys the input and sells to the client. Client pays back the price over the contract period

– Tawarruq—purchases and sales result in cash given to client. Debt created that is paid back over the contract period

Organized Tawarruq

The client wants a personal loan and approaches the bank 1. Bank buys commodity from a broker paying spot (for £100) 2. Bank sells the commodity to client payable at a future date (for

£110) 3. The client sells commodity to broker spot (for £100)

[The client appoints the bank as agent to sell the commodity. The bank sells the commodity spot to the broker for £100 on behalf of the client and deposits the money in his account.]

At the end of the transaction, the client walks away with £100 and owes the bank £110 payable in the future

[Bai al’Inah: No third party involved—bank and client do the selling and buy-‐back]

1

2

3Bank Client

Broker

Durham Islamic Finance Autumn School in Istanbul, 2011

Habib Ahmed, Product Development in Islamic Banks 15

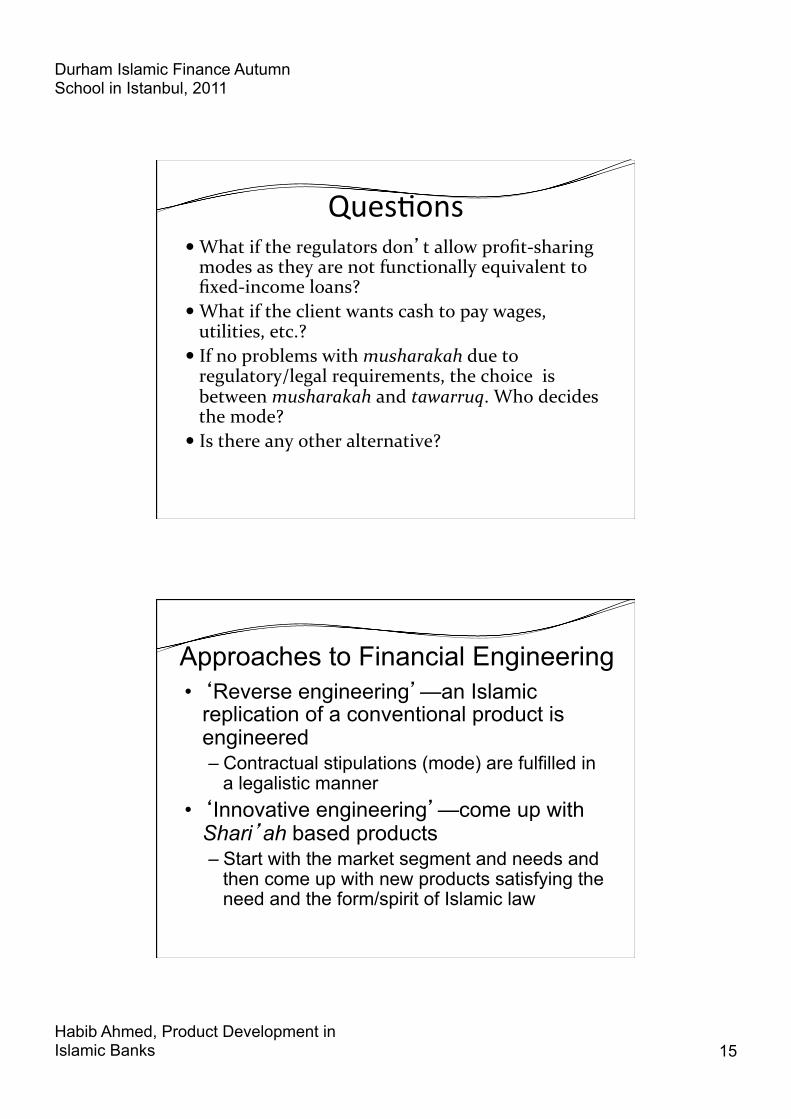

Ques.ons � What if the regulators don’t allow profit-‐sharing modes as they are not functionally equivalent to fixed-‐income loans?

� What if the client wants cash to pay wages, utilities, etc.?

� If no problems with musharakah due to regulatory/legal requirements, the choice is between musharakah and tawarruq. Who decides the mode?

� Is there any other alternative?

Approaches to Financial Engineering • ‘Reverse engineering’—an Islamic

replication of a conventional product is engineered – Contractual stipulations (mode) are fulfilled in

a legalistic manner • ‘Innovative engineering’—come up with

Shari’ah based products – Start with the market segment and needs and

then come up with new products satisfying the need and the form/spirit of Islamic law

Recommended