1

Outlook for European Political EconomyDivision, Dithering, Deflation, and Decline

(but not ‘Crisis’)

Adam S. PosenInstitute for International Economics

Global Insight’s World Economic Conference09 May 2006

2

Echoes of 1930 without the violence:• Economic dislocation of the politically influential middle classes

– Credible threat of unemployment for some bourgeoisie– Competitive pressure from identifiable trading partners

• Fear of social erosion by demography and ethnicity• Failure of grand projects and international organizations• Extended growth slowdown and near-deflationary policies• Declining support for mainstream parties and liberalism

Result: Protectionism, Economic Nationalism, and Fiscal Expenditure on Symbolic Projects

Outlook for European Political EconomyDivision, Dithering, Deflation, and Decline

3

• The entire postwar system was about buying off their dissatisfaction and buying their support

• Unemployment fell largely on ‘outsiders’ by various criteria, or there were glide paths to retirement

• Even limited fiscal pressures are now hitting pensions• Restructuring is beginning to threaten established

high wage sectors and professions• The potential 1-2-3 punch of EU enlargement,

Services Directive, and Asian competition breeds fear– And outright opposition to these constructive measures

Economic dislocation of the middle classes

4

Resistance to globalization through denial at home and recalcitrance abroad

• Outsourcing remains low compared to other countries• FDI is concentrated in CEE, but with mixed feelings• Service sector liberalization will be fought all the way

– National champions yes, but even more local protections– The ‘qualifications’ barriers are very high and unaddressed– Various precautionary and privacy principles spill over

• The moment to move on agriculture was missed• Aggressive state promotion of commercial deals is

beginning to go well beyond Airbus– Discussions of EU military capabilities abet this trend

5

Restructuring is just real enough to be scary% of sectoral workforce losing jobs due to restructuring (2002-present)

0

1

2

3

4

5

6

7

8

9

Constructi

on

Commerce

Extrac

tive I

ndustries

Financia

l Serv

.Meta

l and M

achinery

MotorPost

& Teleco

mm.Eco

nomy's to

tal

% s

ecto

r's w

orkf

orce

GermanyEUbig18 less Germany

Source: Author's calculations, EMCC, OECD STAN Database

"EUbig18" consists of EU15 less Luxembourg and the four largest new members (Czech, Hungary, Poland, and Slovakia)

6

• Guest workers and immigration were always more important than publicly acknowledged– But the myth that people could be sent ‘home’ comforted

• Greater cohesion of ethnic communities threatens• Declining fertility brings echoes of post-WWI fears• As with 1920s Popular Front-type governments, there

is a feeling that cosmopolitan values went too far– Difficult to maintain citizenship definition without nationalism

• Cultural exports by US and by Islamic world seen as dangerous and divisive

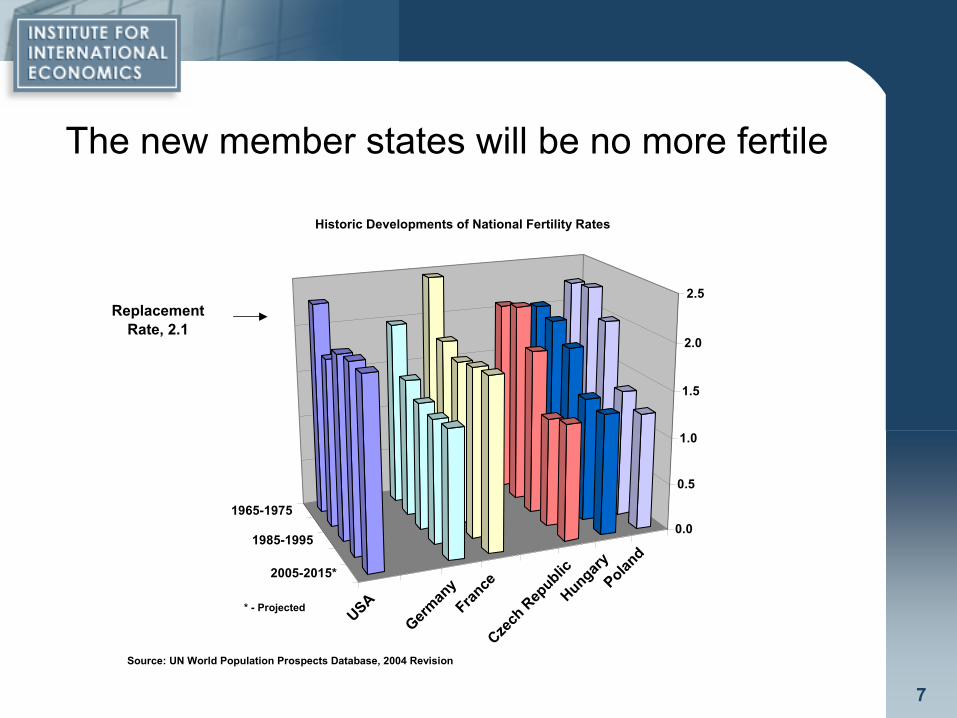

Fear of social erosion by demography and ethnicity

7

The new member states will be no more fertile

1965-1975

1985-1995

2005-2015*

USA

German

yFran

ceCze

ch R

epublic

HungaryPolan

d

0.0

0.5

1.0

1.5

2.0

2.5

Historic Developments of National Fertility Rates

Source: UN World Population Prospects Database, 2004 Revision

ReplacementRate, 2.1

* - Projected

8

• Constitutional ‘No’, grudging enlargement, and underperforming euro/SGP all build-up resentment– Functionalists: EU always comes back with new initiatives

– Rationalists: The EU just went too far in adjustable specifics

• But there is no plan “B” and the means of adjustment were rejected in the constitutional vote

• Recently ignored concepts of ‘subsidiarity’ and ‘democratic deficit’ are re-emerging

Perceived failure of European Union’s grand projects and of international organizations

9

• There was a battle taking place between statism and liberalism in Brussels– Brussels has been weakened politically, which means the

force for liberalism has been taken away– Franco-German logrolling has replaced Anglo-German use

of Brussels for liberalization

• Anglo-American fantasies about ‘break-up’ are mistaken, but there is still an economic effect

• Fantasies about the positive impact of eastern enlargement are equally unfounded and mislead

Perceived failure of European Union’s grand projects and of international organizations

10

No fiscal brick wall will be hit on health care or elsewhere in the welfare state for many years• General point – unless debt dynamics are bad or

most debt is foreign-held, there is no fiscal risk– Ex Bel and Italy, there is ample national savings, low foreign

debt, and too high investment ratios for crowding out

• Health care outcomes demonstrates the Tolstoy view of medical systems (“Every happy family…)– Cost containment efforts are underway but largely on the

demand side and via the state’s bargaining power

– Ideologically, EU is getting to be like Canada defining moral superiority if not identity vs. US by health care

– There are unlikely to be supply-driven opportunities

11

No Rubinomics for the Euro ZoneItalian Interest Rates and Private Sector Fixed Investment Growth

-7

-2

3

8

13

1994

M1

1994

M5

1994

M9

1995

M1

1995

M5

1995

M9

1996

M1

1996

M5

1996

M9

1997

M1

1997

M5

1997

M9

1998

M1

1998

M5

1998

M9

1999

M1

1999

M5

1999

M9

2000

M1

2000

M5

2000

M9

2001

M1

2001

M5

2001

M9

2002

M1

2002

M5

2002

M9

2003

M1

2003

M5

2003

M9

2004

M1

2004

M5

2004

M9

Long Term Government Bond Yield Real Investment Growth

Source: IFS, January 2005 and Eurostat

1994-1998 inv.growth avrg

2.5%

1999-2004 invgrowth avrg

1.8%

Y-on-Y investment Growth,Interest Rates(%)

12

No obvious benefits from euro, either

Economic Performance before and after Maastricht Treaty for four eurozone members, 1994-2004 compared with 1984-1993

-4

-2

0

2

4

6

8

Italy Germany France Ireland Sweden UnitedKingdom

Denmark

Perc

enta

ge p

oint

diff

eren

ce b

etw

een

84/9

3 - 9

4/03

per

iod

aver

ages

Productivity Growth Unemployment Rate Real GDP GrowthSource: OECD Economic Outlook #74

NOTE: the sign on the unemployment difference has been reversed in order to facilitate visual comparison. A positive value signifies a fall in unemployment.

13

Divergence or Just Disappointment?Euro-area Real GDP growth

-3

-2

-1

1

2

3

4

5

1991

Q119

91Q3

1992

Q119

92Q3

1993

Q119

93Q3

1994

Q119

94Q3

1995

Q119

95Q3

1996

Q119

96Q3

1997

Q119

97Q3

1998

Q119

98Q3

1999

Q119

99Q3

2000

Q120

00Q3

2001

Q120

01Q3

2002

Q120

02Q3

2003

Q120

03Q3

2004

Q120

04Q3

Unweighted Average+ 1std dev-1 std. dev

Sample includes all euro-members apart from Portugal, data for Ireland are only available from 1997.Data from OECD, Quarterly National Accounts

%, Y/Y

14

Germany’s Own “ERM-Crisis”

Source: Posen and Popov Gould, “ECB Monetary Policy and Eurozone Stress”, Sept 2005- Indicators are the difference between national (1990-98) and European (1999-2004) actual rates and rates implied by the Bundesbank/ECB reaction functions using national data on output gaps and inflation. A positive value implies an excessively high de facto interest rate. Indicators extend to 2004m6 only due to forward-looking reaction function models used in estimations.

-5

-3

-1

1

3

5

7

9

11

1990

M119

90M7

1991

M119

91M7

1992

M119

92M7

1993

M119

93M7

1994

M119

94M7

1995

M119

95M7

1996

M119

96M7

1997

M119

97M7

1998

M119

98M7

1999

M119

99M7

2000

M120

00M7

2001

M120

01M7

2002

M120

02M7

2003

M120

03M7

2004

M1

Germany Italy France

percentage points

15

Expect a cut-off recovery in 2006 and ongoing drag from monetary and fiscal policies• No one should believe the euro break-up stories

• The ECB will raise rates prematurely due to the monetary pillar, which will kill off the current upswing

• Germany’s relative wage deflation will not make up for the real interest rate and wage effects

• SGP violators will stay in the worst of both worlds, tightening fiscal policy with no interest rate payoff

• All this, abetted by an eventual dollar decline and rising interest rates globally will limit growth

16

The Euro’s global role is precluded by poor relative performance and capital integration• Obstacles to financial integration in Europe

– Money and bond market progress is undeniable

– Equity and ownership market integration are slow

• Fragmented financial supervision and crisis response capabilities in the eurozone

• Unconsolidated eurozone representation in the IMF and other international fora, and

• Deficient macroeconomic stability and growth

…all remain (eurozone entrants beware!)

17

- If the euro moves but Asian currencies do not 84% - If the euro moves and Asian currencies appreciate 20% 42% - If the euro moves and Asian currencies appreciate 41% 20%

* - Estimation assumes an average 25% appreciation by all otherindustrial countries including Japan

Source: Truman, Edwin (2005) "Postponing Global Adjustment: AnAnalysis of the Pending Adjustment of Global Imbalances"(IIE Working Paper #05-6)

Appreciation of the Euro in response to a 20% US$ depreciation*

The euro is more vulnerable than the yen to dollar adjustment

18

Extended growth slowdown and deflationary policies• It is possible to paint a somewhat rosy picture for EU

performance in comparison to the past or to the US– Productivity levels, choice of leisure, some positive outliers– Labor market reforms are working in some places

• Ultimately, though, the EU has to grow faster than the US to meet the demands of demography, enlargement, and social solidarity and it is not – Real returns on capital (NIPA) have been consistently lower

and consumer prices have been higher– The slowing performance of late in the Netherlands and

Sweden, even if only cyclical, tends to undercut the claims that reforms are beneficial

• In fact, there is little sign of a growth or innovation acceleration even where R&D/Human cap are high

19

Outlook: Division, Dithering, Deflation, and Decline(but not ‘Crisis’)

• If one does not want to identify with the EU or with Atlanticism, what is left but nationalism?

• If one does not want to be Anglo-capitalist, but communism is out, what is left but protectionism?

• If government officials cannot take credit for improving economic performance, and cannot significantly redistribute wealth, what can they do but try to generate symbols of solidarity and accomplishment?

•Think the 1930s redux with nationalism minus militarism, racism minus (state sponsored) violence, and public works projects minus the fascist imagery

•But in a global economy where there is real competition

20

Result: Robust stagnation in EU3-plus

• There will be mounting reform fatigue with little to show for it, which will further weaken party support

• With a likely structural budget deficits of 1.5-2.0% p.a., gross debt will not rise enough to cause change

• The outflow of young people, capital, and ideas will be a steady trickle, not a stream, but very clear

• A dual economy (not unlike Japan) will see the best companies do the most restructuring, and vice versa

• Growth will be insufficient to lower unemployment• An anti-globalization Germany and Italy will weaken

the EU and the international economy

The Premier Forum on the Direction of the Global Economy

Recommended