1

Public Consultation:

Tourism Policy

Issues Paper and Request for submissions on developing a Tourism Policy Statement

Department of Transport, Tourism and Sport AUGUST 2013

2

Foreword by Mr Leo Varadkar T.D. Minister for Transport, Tourism and Sport and Mr. Michael Ring T.D. Minister of State for Tourism and Sport

The purpose of this document is to frame the debate on our future tourism policy. We are pleased to invite the tourism industry, consumers and other interested parties to contribute to the debate through this review of tourism policy. Tourism is an important driver of economic activity for Ireland. As well as being our longest-standing source of service export earnings, it also directly and indirectly supports employment across the country, both urban and rural. The tourism and hospitality industry employed approximately 185,000 people in 2012 and generated over €5 billion in revenue from home and abroad. Tourism is central to the Government’s economic recovery programme. The competitiveness of the Irish tourism industry has been enhanced through a range of measures we have introduced, not least through the Action Plan for Jobs. These measures, together with tourism industry specific supports for marketing, enterprise development and capital investment have underpinned recovery and growth in the industry, particularly in overseas tourism. Competition in an evolving global tourism industry demands effective prioritisation of industry supports. It is therefore timely to commence a review of tourism policy and the views of stakeholders are invited on the policy position that Government should adopt, the steps the industry should take and the direction that the tourism agencies should follow to support a competitive and sustainable tourism industry in Ireland. Following the review, we plan to issue an overarching tourism policy statement to provide the necessary direction to support a competitive and sustainable tourism industry and give clear direction to the tourism agencies for carrying out their operational programmes. Your input into this process is valuable and through the continued efforts of all stakeholders we are confident that we can develop a policy to ensure a positive outlook for Irish tourism into the future.

______________________ _______________________ Leo Varadkar T.D. Michael Ring T.D. Minister for Transport, Tourism and Sport Minister of State for Tourism and Sport

3

CONTENTS PAGE No.

The Consultation Process ....................................................................... 4 Executive Summary …………………………………………………………………………… 5 Introduction ………………………………………………………………………………………… 7 Tourism Policy Background - Rationale and History …………………………. 9 Tourism Marketing ……………..……………………………………………………....……. 12 Tourism Product Development ……………………………………………….………… 14 Human Resources and Training /Enterprise Support / Innovation and Competitiveness…………………………………………………………………………… 17 Implementing Policy and Service Delivery Mechanisms ……………………… 19 How to submit your views ........................................................................ 22 APPENDIX: FUNCTIONS OF THE TOURISM AGENCIES….……………………………….………. 23

4

The Consultation Process: The purpose of this consultation process is to invite interested parties to submit written views / observations / suggestions to support a competitive and sustainable tourism industry in Ireland. It is envisaged that this public consultation process, along with the relevant stakeholder engagement, will contribute significantly to the delivery of a Tourism Policy Statement which will provide the necessary direction to support a competitive and sustainable tourism industry and give clear direction to the tourism agencies for carrying out their operational programmes. The questions have been categorised under specific headings as follows: 1. Tourism Marketing 2. Tourism Product Development 3. Human Resources and Training / Innovation / Enterprise Support and Competitiveness 4. Implementing Policy and Service Delivery Mechanisms

What will a Tourism Policy Statement do?

A clear statement of tourism policy will set out the Minister’s priorities in terms of:

the contribution tourism is to make to national economic and social goals,

how that contribution will be measured and benchmarked, and

in what manner tourism can best make its contribution

Based on these, the policy will set parameters for allocation and deployment of the resources

available to Tourism through his Department, to achieve those priorities (through the agencies or

otherwise).

Why is a Tourism Policy Statement being prepared now?

There are clear signs of recovery in Irish tourism in terms of overseas arrivals. The scope for State

investment in tourism will remain constrained for the foreseeable future. It is timely therefore to

make a policy statement that prioritises the investment that will maximise the return from tourism

in the long term. If Government and stakeholders are to be persuaded to take on board measures

to support tourism, the Minister and his Department have to make the case based on specific,

benchmarked and measurable policy priorities. Likewise, the capacity of the Department to

influence the impact of wider government policies on the tourism sector will be reinforced if based

on a robust policy foundation.

This approach is an innovation. The value of previous policy documents was in the identification,

with the industry, of a range of actions for the agencies, wider Government and the industry to

pursue to support tourism. This traditional approach will no longer suffice and needs more robust

policy underpinnings.

When finalised by summer 2014, the Minister’s policy statement will form the basis for the

Department to work with its partners in the agencies and the tourism industry, as well as

stakeholders across Government, to develop a detailed strategy and action plan, setting out a range

of specific measures to be pursued.

5

Executive Summary

1. The Minister is seeking the view of interested stakeholders and consumers on the policy priorities for tourism. Following extensive consultations, he will finalise and publish a statement of policy. This will provide the basis for the preparation of a broader tourism strategy and action plan, prepared with the industry and other key stakeholders. Comments should be submitted by Friday 1st November (see page 22).

2. Tourism will remain central to the Government’s economic recovery programme with the focus on growing export earnings and employment through the sector. Tourism is a key driver of social and economic development in Ireland and supports employment across the country for a range of skill levels – in 2011/12 surveys, tourism and hospitality employed approximately 185,000 people and generated €5 billion in domestic and overseas spending. Recent trends in Irish tourism are summarised, noting the return to growth following decline from 2008 to 2010, the longer-term changes in source markets and domestic trends, as well as the recovery in cost competitiveness. Global Tourism trends are also noted and key performance indicators identified.

3. Policy Considerations and issues in relation to Tourism Marketing form the background to the

questions posed, which are summarised as follows:

Q1: What are the respective roles for the private and public sectors in marketing generally, and in terms of target markets or timescale?

Q2: What should be the priority markets/best prospects (geographical/segments) for Ireland?

4. Similarly, the policy issues in relation to Tourism Product Development are outlined, framing questions on, in summary:

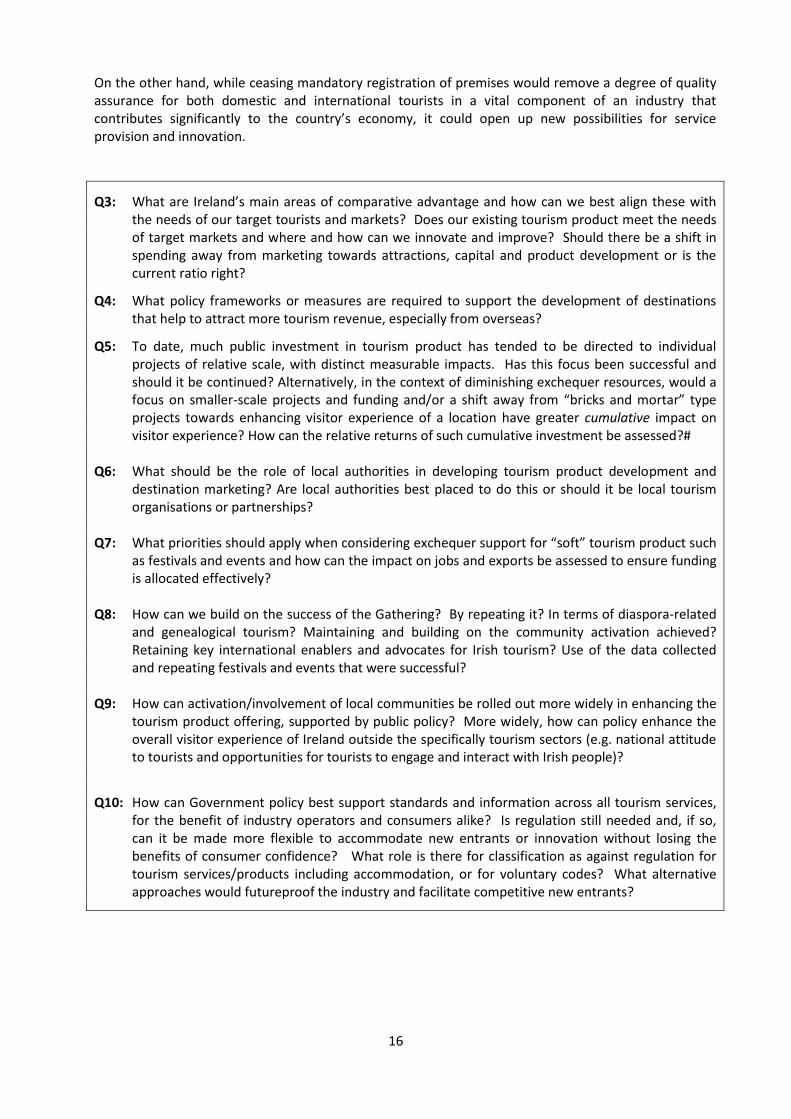

Q3: What are Ireland’s main areas of comparative advantage and how can we best align these with the needs of our target tourists and markets? Is the current ratio between marketing spend and product development right?

Q4: What policy frameworks or measures are required to support the development of destinations that help to attract more tourism revenue, especially from overseas?

Q5: What should be the role of local authorities in developing tourism product development and destination marketing? Are local authorities best placed to do this or should it be local tourism organisations or partnerships?

Q6: Would smaller-scale projects and/or a shift towards enhancing visitor experience of a location have greater cumulative impact than bigger projects?

Q7: What priorities should apply when considering exchequer support for “soft” tourism product such as festivals and events?

Q8: How can we build on the success of the Gathering?

Q9: How can policy support local community involvement in tourism product development?

Q10: How can Government policy best support quality standards and consumer information across all tourism services, for the benefit of industry operators and consumers alike?

6

5. Turning to Human Resources and Training, Enterprise Support, Innovation and Competitiveness, the questions cover:

Q11: How to prioritise the competing demands of training of individuals, labour activation and enterprise supports? What implications would changes in product/market focus have?

Q12: How can the State best support the delivery of appropriate training? Are there other models?

Q13: What is the most appropriate structure so tourism can bring people back into the labour force and help them to remain active? Are there adequate opportunities for career progression?

Q14: What policy frameworks are appropriate for tourism enterprise supports? Where should the State intervene, bearing in mind enterprises’ own responsibilities and the role of other agencies?

Q15: How can public policy, particularly tourism policy, help to ensure that we maintain and if possible enhance cost competitiveness in the longer term?

Q16: Are there wider competitiveness factors? In assessing policy effectiveness, what comparators would be useful?

6. In terms of Implementing Policy and Service Delivery Mechanisms, the questions posed include:

Q17: Is the overall balance of resources right? Are there are gaps in the current tourism policy/programmes or in addressing the impact of Government policy/programmes? Which functions should be discontinued or wound down?

Q18: What should be the priority focus areas for Government and for the tourism agencies? Is the broad distribution of resources between the different activities of the agencies appropriate?

Q19: Are there suggestions that would deliver greater efficiency in the operation of the Department or the tourism agencies or free up resources?

Q20: Is the current agency structure optimal? Are there any suggestions for how the structure could be changed or how co-operation between the three bodies (Fáilte Ireland, Tourism Ireland and the Northern Ireland Tourist Board) be enhanced?

7

Introduction

Background to the Policy Review

Following a request from the industry and others, Minister Varadkar stated his intention to commence a review of tourism policy and included it in his Departmental priorities for 2013. Current policy is set in the Programme for Government with key priorities being to help the industry survive after some of the most challenging years for many decades. With tourism now in recovery mode, the Minister considers it timely to examine how tourism policy should contribute to sustainable growth in the sector in the medium term. Furthermore, within a context of continuing constraints in the resources available to the public sector (both human and financial), it is critical that Government sets its priorities for the deployment of such resources to support tourism. The Consultation Process The Minister is seeking the views of interested stakeholders and consumers on the policy position that the Minister and his Department should adopt, the steps the industry should take and the direction that the tourism agencies should follow. As part of the process, this document is being published and replies to the questions raised are invited. Contact details are set out at the end of the document. Alongside Minister of State, Michael Ring, he also intends to conduct a series of seminars at which stakeholders can highlight key issues in Autumn 2013. For the purposes of consultation, the issues and questions are presented under the following headings. However, it is important to note that the final policy statement will not necessarily follow the same structure. In reality, the different aspects are closely interconnected and overlap.

Tourism Marketing Tourism Product Development Human Resource/Training/Innovation/Enterprise Support/Competitiveness Implementation Frameworks

Views and suggestions are welcome under any or all of these headings, taking account of the policy context and overall goals set out in this introduction and elaborated upon in each specific section. As far as possible, comments should cite the rationale behind them and evidence underpinning them, for example, by reference to product fit, access trends, demand forecasts etc.

Next steps

Following consideration of the submissions received, the Minister will publish a statement of policy priorities for Government intervention in tourism. The Minister intends that this shall provide the basis for development of a broader tourism strategy and action plan, involving key stakeholders. The strategy will set out a range of objectives, actions and measures to develop tourism, addressed not only to Government and the tourism agencies but also to enterprises, industry groups and other relevant bodies. This will be drawn up in consultation with the range of key stakeholders whose actions are critical to the sector. The ultimate objective is a competitive and sustainable tourism industry. Tourism policy will also take into account the medium-term public expenditure framework. Limited resources must be targeted at the highest priorities offering the optimal return – in the short, medium and longer term. The opportunity cost of all ideas and actions must be considered. Like the rest of the public sector, the Department of Transport, Tourism and Sport and the tourism agencies are operating with fewer staff and less funding, meaning that tough choices must be made and priorities identified. Furthermore, any new activities or areas of focus may only be pursued at the expense of other activities.

8

Mindful of the operational independence of the tourism agencies and given that it is a guiding, framework document, the final statement of tourism policy will provide appropriate policy direction and support to the tourism agencies. In particular, it will enable them to focus supports based on changing needs, emerging trends, overall tourism prospects and development opportunities. Underscoring all of this, of course, will be the need to maximise returns on increasingly limited resources and to avoid unnecessary overlaps or duplications.

9

Tourism Policy Background – Rationale and History Value of Tourism Tourism is a key driver of social and economic development at both national and regional levels in Ireland. Its repeated ability to return to growth after periods of even severe recession, has been shown over many decades, and demonstrates its fundamental resilience and competitiveness. It also plays a central role in creating a positive image of Ireland, which is essential to a small country seeking to maximize the benefits of trade, investment and tourism globally. Tourism is an industry largely populated by smaller enterprises and is deeply rooted in the fabric of Irish economic life, urban and rural. As well as being our longest-standing source of service export earnings, it also supports employment across the country for a range of skill levels – often in areas where the scope to develop other industry is constrained. Based on 2011/12 surveys, the tourism and hospitality sector employs approximately 185,000 and generates in the region of €5 billion per year in revenue from home and abroad. Tourism's contribution is not confined to generating employment, economic activity and exports. Tourism has played a vital role in reshaping North/South relationships through the joint marketing and promotion of the island of Ireland in international markets. By intervening in tourism, the Government aims to maximise these wide-ranging economic and social benefits of the sector, by promoting Ireland, supporting enterprises and jobs and providing an attractive, competitive overall offering for tourists. Tourism Policy: Context and Goals

Tourism is central to the Government’s economic recovery programme. The Programme for Government includes a series of specific actions relating to tourism. The Minister is satisfied that significant progress has been and continues to be made on these commitments (see http://www.taoiseach.gov.ie/eng/Publications/Publications_Archive/Publications_2011/PfG_Progress_Report_March_2012.pdf). In particular, the Jobs Initiative in the Government’s first months in office introduced a range of significant measures to enhance the competitiveness of the Irish tourism industry and this has been followed by the ongoing implementation of the Action Plan for Jobs. Having made progress on these measures to assist the industry to survive, there are now signs of recovery, particularly in overseas tourism. It is therefore timely to commence a review of tourism policy. The continuing focus on fiscal responsibility will constrain the quantum of public resources available to support tourism for the foreseeable future. This makes it even more important that everyone involved in Irish tourism has a clear understanding of the Government’s policy priorities. The policy will set out such priorities. This marks a departure from previous policy frameworks which have largely taken the form of high-level or aspirational aims and visions, followed by a set of specific actions to be pursued by tourism agencies and others. They were useful in providing a clear set of objectives for the stakeholders to work towards and actions that could be measured. However, they did not set out the priorities of Government policy. There was no clear statement of how Government should best focus its resources on a defined number of sectors of comparative advantage as opposed to a wide range of sectors. In terms of resources, the tourism services budget has seen significant retrenchment since 2008. There will be further pressures on resources and staffing in the short to medium term and in that context there is a clear need to establish explicit and robust priorities.

The fundamental goal of tourism policy is to ensure tourism contributes to economic and social wellbeing in Ireland. Therefore, the focus shall be on growing export earnings and employment through

10

the sector. With that in mind, it is intended to prioritise indicators that reflect economic activity within such as bednights and revenue, rather than overall volume indicators such as the number of trips.

Review of recent tourism trends in Ireland

Following a period of rapid growth in the 1990s, which was largely sustained into the new century, inbound tourist arrivals and revenue fell from 2008 to 2010 as worldwide economic circumstances affected disposable incomes. However, these broad trends do not tell the full story. The “average” length of trips, particularly holiday/leisure trips, to Ireland, like elsewhere, showed a long-term trend towards getting shorter. This reflects the increasing tendency of consumers to take more short breaks, rather than consumers reducing the duration of all holidays. It was notable that CSO Tourism and Travel data for 2010 showed an increase in average duration, while nearly all other figures (trips, nights, spend) showed declines. There were also significant shifts in terms of market geography and the purpose of trips. Since the 1990s, the biggest driver of growth in trips and revenue has been continental Europe, following the earlier growth from Britain. While work-related migration drove sharp rises in all kinds of trips from Central and Eastern Europe, clearly these produced less revenue. Western Europe also saw growth (particularly from the Mediterranean states) although costs issues had a dampening effect on growth from Germany and other traditional markets. As noted, the growth of short breaks from Britain partially compensated for the long-run decline in more “traditional” British visitors as Irish migrants were assimilated and a wider range of destinations became easily accessible from Britain. There was an associated shift in Ireland’s perception as a destination in Britain - from a culturally distinctive rural product to a more generic urban one. Nonetheless, Britain is our nearest neighbour and is a large outbound market in global, not just European terms, and will remain vitally important for Ireland. Its importance will vary between different destinations on the island and also between different sectors, but it will likely continue to be the source of most overseas trips, if not revenue. North American arrivals have been broadly stable for many years now, fluctuating in line with currency movements, consumer confidence, air access volumes and affordability and shocks to perceptions of safety or security. This is despite newer destinations for US travellers – as well as stagnant real personal incomes over the last 20 years. It remains a vital market, sending us some of our highest-value visitors and in which Ireland, for its size, outperforms most of its European counterparts. Indeed, 2013 could be a record year for Ireland in terms of visitors from North America even though overall American visits to Europe have fallen. There has been a gradual growth in tourism from other long-haul markets, many of which are new and developing. However, methodological issues make it difficult to disaggregate and interpret official data for such small volumes. For example, the impact of migration in either direction on the data. Anecdotal and industry surveys present a picture of gradual development in the face of challenges associated with Ireland’s small size, non-membership of the Schengen area (visas) and our peripheral location.

In Ireland, as elsewhere across Europe, a trend towards substituting overseas travel with domestic travel was apparent in the 2008-2011 period, helping to sustain the industry here in the face of the overseas declines. However, continuing pressure on incomes is dampening domestic demand. Despite the continuing difficulties in economies worldwide, Ireland’s tourism industry achieved a welcome return to growth in overseas visits of 8% in 2011. The industry managed to maintain a similar level of overseas visitors in 2012 but the most important measure, revenue from overseas visitors, was up 4.5%. Overall employment in the tourism sector was estimated at around 185,000 in 2012, up almost 3% on 2011. This recent performance is encouraging but the industry still has many issues that

11

cause concern, including credit supply and accommodation capacity. These must be taken into account in developing future policy. A key contributor to the sharp falls during the downturn, and to the progressive recovery since, has been our performance in terms of value for money and cost competitiveness – both real and perceived. Top line trends from Fáilte Ireland’s annual Visitor Attitudes Survey for 2012 indicate that Ireland is perceived as offering value for money to overseas visitors at rates not seen for over a decade. Ireland has improved significantly and is now receiving net positive ratings across all key markets. 41% of overseas visitors in 2012 rated Ireland as good to very good value for money with another 42% rating us as fair. Only 17% of visitors considered Ireland as poor or very poor value for money – three years previously (2009) this figure was 41%. Ireland’s overall net rating (when negative responses are subtracted from positives) as a value for money destination has improved at a significant rate from -11% in 2009 to +24% in 2012. Maintaining this customer perception by continuing to deliver value for money – right across the range of tourism-related services is critical. The negative impact of rising consumer costs on revenue was demonstrated in the period of the boom, when Irish revenues from inbound tourism stagnated in real terms. It is widely observed that tourists travel with a fixed budget and if costs are higher than expected, they simply reduce consumption to fit the budget. The medium to long-term forecast for international tourism remains positive with continued growth expected in the period to 2020 but at a more moderate pace than in recent decades. New and Developing Markets should see higher levels of growth in outbound tourism (expected to be in the region of 5% growth per annum) but established outbound markets such as Europe and North America are also expected to grow albeit more slowly. Review of Global Tourism Trends The wider trends shaping global and Irish tourism over the past decade include • Growth in tourism trips globally (resumed after a brief downturn) with more short stays and higher

than average growth in the Visiting Friends/Relatives category (associated with migration)

Very slow growth in tourism to mature tourism destinations and a shift to emerging destinations

A linked shift in the sources of tourism growth, as developing countries see both economic growth overall and a rapidly growing middle class, with strong preferences for aspirational consumption of both goods and services often delivering more rapid growth to their neighbours rather than American or European destinations

A “second wave” of new destinations in developing countries attractive to visitors from both developed markets and other developing markets

• Sectoral and skills labour supply shortages even in the face of overall labour surpluses • Growth in business travel, including conferences and incentive travel • Strong price competition on the demand side, along with very late booking, all facilitated by the

internet

Continuing restructuring of tourism packaging, distribution and delivery models driven by technological change, complemented by parallel shifts in marketing and sales

• Pressure to reinvent the product, attract fresh investment and innovate • Restructuring in aviation, following the "low-fares" model, with the emphasis on a market-led

approach in which airlines rapidly shift routes and service levels to ensure routes are profitable • More traditional aviation models on longer-haul routes, but with higher fuel prices and price

competition leading to careful capacity management • Changing consumer demand including an emphasis on visitor "experience" and authenticity and

also new/diversified niche markets (e.g. retired travellers, health and wellness tourism, and cruise tours)

• Safety and security concerns affecting tourism enterprises and consumer preferences and perceptions of travel

12

Tourism Marketing: Background

The respective roles of the agencies are set out in more detail below. Broadly, Fáilte Ireland is responsible for domestic tourism marketing as well as developing attractions and specific niches/products. Tourism Ireland is responsible for the overseas marketing of the island of Ireland as a holiday destination. Policy considerations and areas for consultation

First of all, marketing policy, strategy and operations cannot be considered independently of product characteristics whether in tourism or any other sector. The offer is core to decisions about whom you market to, and how you do so. Factors to be taken into account when deciding on where to focus marketing efforts for maximum returns include: current economic conditions, consumer sentiment, and prospects for growth in the domestic

market and in key overseas tourism markets, product fit to the market or segments of the market, marketing leverage and share of voice (overall or in key segments), access trends and growth prospects for passenger transport and global tourism generally, and particular tourist segments – looking at what types of tourists (particular age-groups, backgrounds,

interests) would be most interested in Ireland’s offering. A balance must be struck between short-term “quick wins” and markets and segments requiring longer-term investment in order to see a return. In that context, there is a need to distinguish between those areas where the State may be substituting for investment that the private sector could make given the short-term return available, and those where the State must invest given the longer term and uncertainties associated with building a brand in a market. Consideration of the revenue generated by different classes of visitor, in terms of origin or segment, is also important – the return from 1,000 visitors from a high-spending market staying 10 days may be greater than that from 20,000 visitors from a low-spending market for one night each. Prospects for growth or good returns may be limited in some traditional markets for Irish tourism, whereas in other markets positive economic developments or new access routes may yield good returns for those who respond appropriately and capitalise quickly on tourism prospects. Some markets may grow slowly and yet provide potentially good returns on investment for priority tourism segments. For long-haul new and developing markets, such as the BRIC countries or others in Asia and South America, our marketing efforts should also recognise the fact that Ireland will rarely be the sole destination for prospective travellers but may be included in a wider trip also taking in Great Britain and/or Europe. These markets are a particular challenge as many are very large and there is a risk of ineffective expenditure without identifying the right marketing levers or points of differentiation. There is also a need to strike the right balance between international and domestic tourism marketing. In the context of ongoing pressure on existing resources, marketing budgets cannot be spread too thin or it will be ineffective. This means difficult decisions must be made as to where to best target spending. If we are to maintain overall marketing activity, additional resources will need to be found. Already, Tourism Ireland generates private sector contributions, in cash or kind, from cooperative marketing initiatives. Given global trends in the sector, the scope for leveraging further private sector resources for marketing campaigns alongside State investment needs to be considered. More generally, the priority of Government is to promote Ireland as a whole to potential visitors from abroad as well as to domestic tourists, rather than any particular region, in a way that recognises those

13

elements of our offering that have the strongest potential to deliver growth. Tourism, like other industries and sectors, is more developed in some parts of the country than others for a complex mix of historical, social and geographical reasons. Inevitably this impacts on both tourism marketing and product development. However, there is also scope to target particular segments using particular products, niches or destinations. There is a balance to be struck in terms of the role of different destinations and experiences in generating overseas tourism to Ireland as well as domestic tourism. The relevant enterprises which gain directly from generating more traffic, acting individually or in concert, must have the central promotional role in those destinations or niches. However, the State may have a complementary role in assisting them to make the most of what they have, as well as through product development in developing their potential.

Q1: With overall Government funding limited, what are the respective roles for the private and public

sectors in marketing generally, and in terms of target markets or timescale? How can tourism policy best support and encourage private sector marketing? What scope is there to leverage private funding with public expenditure on tourism marketing campaigns, and how should strategic and creative control be handled in such cases? How should policy address the complementary roles of the public and private sectors in promoting particular products, niches or destinations?

Q2: What should be the priority markets/best prospects (geographical/segments) for Ireland? Where

should we increase/reduce investment activity? How should the balance be struck between immediate, short-, medium-, and long-term potential markets and what timelines should apply to such investment?

14

Tourism Product Development:

Background

The Irish tourism offering consists of everything a visitor might experience in Ireland between arrival and departure – the physical environment, infrastructure, attractions and services (including accommodation, restaurants and bars, transport, car hire, activities and events). Product development consists of actions taken and investment made to improve this product and its presentation so that it meets consumer demand and expectations. Continued investment in tourism product development is key to maintaining and improving Ireland’s competitive advantage in tourism markets.

Given the importance of the tourism industry as an employer and driver of economic activity throughout the country, investment in tourism capital is a good use of public monies where market cannot do it alone. In fact, the nature of our tourism offering is such that the factors driving and attracting tourism growth are things to see and do, while employment is generally concentrated in services such as transport, accommodation and food that do not in themselves attract visits. Many attractions are non-commercial in nature, often in public or charitable trust ownership, and do not produce a sufficient return to cover re-investment or even operating costs. Much of what is most attractive is in the public realm and free to use e.g. amenities such as walks and cycling routes. This also applies to events and festivals, which also attract visitors. Accordingly, State funding for such public and quasi-public goods is necessary and justified to bridge the investment gap and secure the resulting economic return. For example, the investments for improvements to accessibility, parking facilities and interpretation at the Sliabh Liag cliffs in Donegal or the Mizen Head in Cork would not have provided a commercial return to a private sector investor but will facilitate increased visitors by addressing the blockages in accessibility to these natural attractions, improving the overall experience for the visitor. Accordingly, this investment is akin to other forms of public infrastructure, such as roads, in that it facilitates economic activity that would not otherwise have taken place. Similar arguments apply to supports for festivals and events which attract visitors, especially overseas visitors, and enhance their experience of Ireland. As outlined in Section 2 (with further detail in Appendix), Fáilte Ireland is responsible for the development of quality tourism product in Ireland.

Policy considerations and areas for consultation

Although the final overall statement of tourism policy will not go into operational detail, it will give the overall policy context in support of product development and related priorities across all tourism product: capital assets (accommodation, attractions, amenities, etc.), as well as festivals and events, etc. In this context, how the Irish tourism product appeals to target overseas markets and segments is key to setting investment priorities. The final policy statement will also address issues around public and private funding and ownership of tourism product, as well as acknowledging other sources of funding for tourism-related product outside of the control of the Department and Fáilte Ireland. Fundamental to the development of tourism product of all kinds is the tourist experience. Consequently, product is more than the capital asset – it includes areas like animation, interpretation and participation. The question is then how best does the public sector, particularly the Department, allocate scarce public resources (both current and capital) to make our tourism offering as attractive and competitive as possible – bearing in mind our existing or potential comparative advantages and markets. This is particularly important for a small island like Ireland, in a peripheral location, where product dependent on large populations (either existing holidaymakers or residents) within short distances is not

15

feasible e.g. a large theme park either needs to be in a major summer destination like the Spanish Costas and Florida, or near conurbations like Paris or the West Midlands in the UK. Our tourism product must be feasible for the kinds and numbers of visitors we get and must build on existing advantages over competitors. There may be scope in this context to look at how tourism product can be enhanced across the island of Ireland, given the extent to which it forms a single destination for very many visitors and markets. At the heart of Ireland’s tourism product are particular destinations, complemented by specific niche offerings and activities. It is ultimately the stakeholders in the tourism industry and local community who can develop the potential of any destination or niche product, based on their distinctive characteristics and potential attractiveness for visitors. A range of national and international awards, building on the Tidy Towns Award run by Bord Fáilte for so many years before its transfer to the Department of the Environment, Community and Local Government, has highlighted good practice. Examples include the European Destination of Excellence (EDEN) and the Fáilte Ireland Tourism Town award. In each of these cases, local authorities and/or local community- or industry-based organisations have been critical is securing the support of key stakeholders, delivering enhanced visitor experiences and continuing to develop the destination. Local authorities are key operators of tourist infrastructure, not only dedicated product such as attractions but also the other assets so important to visitors such as beaches, parks, and walks and indeed local infrastructure generally. However, local partnerships and development bodies also play important roles. A specific successful example of this kind of “soft” tourism product, focusing on experiences in and interaction, is The Gathering Ireland 2013, Ireland’s biggest ever tourism initiative. Reaction so far has been positive and has played a role in the tourism performance for the first half of 2013. There has been a 5.4% increase in overseas visits to Ireland for the first half of 2013 compared to January-June 2012, with a particularly strong performance from North America, up 15.4%; if this performance is sustained, the targets for the Gathering will be met. The initiative has not just delivered numbers; one of the key benefits of the Gathering Ireland 2013 has been the way it has energised local communities, right across the country, to look at ways to package and promote their local offering for visitors. While enterprises such as hotels and restaurants are not primary drivers of tourism business (with some limited exceptions), their product is also an important part of the overall tourist experience. Traditionally, regulation and classification backed by legislation has been the means to inform consumers of the nature of individual enterprises’ offering, particularly for hotels. Such regulation is one of Fáilte Ireland’s statutory obligations and sets out standards that a service provider must meet in order to operate as a particular type of accommodation. While this has benefits in terms of consumer information, it can inhibit innovation and the adaptation of tourism product to rapidly evolving consumer preferences. Access to collective information on a range of consumer goods and services has transformed the whole area of consumer information – including in travel and tourism, undermining the original rationale for statutory registration and classification systems. In devising the new tourism policy, it is timely and appropriate to look again at the benefits and drawbacks of such regulation. On the one hand, the regulations ensure that domestic and international tourists alike may readily identify the standard of accommodation they wish to rent. Furthermore, the regulations also ensure that any service providers advertising their properties as having reached a certain standard must comply with this standard thus ensuring fair competition among providers. If such regulation is considered to be of assistance in the accommodation sector, consideration should perhaps be given to extending the regulation of quality and standards to other areas of tourism services.

16

On the other hand, while ceasing mandatory registration of premises would remove a degree of quality assurance for both domestic and international tourists in a vital component of an industry that contributes significantly to the country’s economy, it could open up new possibilities for service provision and innovation.

Q3: What are Ireland’s main areas of comparative advantage and how can we best align these with the needs of our target tourists and markets? Does our existing tourism product meet the needs of target markets and where and how can we innovate and improve? Should there be a shift in spending away from marketing towards attractions, capital and product development or is the current ratio right?

Q4: What policy frameworks or measures are required to support the development of destinations that help to attract more tourism revenue, especially from overseas?

Q5: To date, much public investment in tourism product has tended to be directed to individual projects of relative scale, with distinct measurable impacts. Has this focus been successful and should it be continued? Alternatively, in the context of diminishing exchequer resources, would a focus on smaller-scale projects and funding and/or a shift away from “bricks and mortar” type projects towards enhancing visitor experience of a location have greater cumulative impact on visitor experience? How can the relative returns of such cumulative investment be assessed?#

Q6: What should be the role of local authorities in developing tourism product development and

destination marketing? Are local authorities best placed to do this or should it be local tourism organisations or partnerships?

Q7: What priorities should apply when considering exchequer support for “soft” tourism product such

as festivals and events and how can the impact on jobs and exports be assessed to ensure funding is allocated effectively?

Q8: How can we build on the success of the Gathering? By repeating it? In terms of diaspora-related

and genealogical tourism? Maintaining and building on the community activation achieved? Retaining key international enablers and advocates for Irish tourism? Use of the data collected and repeating festivals and events that were successful?

Q9: How can activation/involvement of local communities be rolled out more widely in enhancing the

tourism product offering, supported by public policy? More widely, how can policy enhance the overall visitor experience of Ireland outside the specifically tourism sectors (e.g. national attitude to tourists and opportunities for tourists to engage and interact with Irish people)?

Q10: How can Government policy best support standards and information across all tourism services, for the benefit of industry operators and consumers alike? Is regulation still needed and, if so, can it be made more flexible to accommodate new entrants or innovation without losing the benefits of consumer confidence? What role is there for classification as against regulation for tourism services/products including accommodation, or for voluntary codes? What alternative approaches would futureproof the industry and facilitate competitive new entrants?

17

Human Resources and Training / Enterprise Support / Innovation and Competitiveness:

Background

As outlined below, Fáilte Ireland is responsible for enterprise support, capability building and human resource development for the tourism industry. At the same time, Solas and the Department of Education and Skills have overall responsibility for ensuring Ireland has the skills required for future competitiveness. Policy considerations and areas for consultation

It is a function of Fáilte Ireland to encourage, promote and support the recruitment, training, education and development of persons for the purposes of employment in connection with the tourism industry in the State, as well as more widely supporting enterprises in developing tourist traffic, services and facilities. Fáilte Ireland provides and funds a suite of training supports for businesses and individuals through supporting education programmes in the Institutes of Technology and direct supports to employees, managers and businesses in the tourism industry. While the peak of the boom was characterised by widespread skills shortages – with further challenges emerging in the visitor experience due to the deployment of non-local staff – the current picture is very different with high unemployment throughout the country. While availability of some individual skills remains challenging we are unlikely to see general skills shortages in the foreseeable future. Unlike many other sectors of industry in Ireland, the Irish tourist industry is made up predominantly of micro-enterprises and Small-to-Medium-sized Enterprises (SMEs). As such, further specific policy and operational responses to support our tourist industry in terms of training and, particularly, enterprise support are required in addition to the more general support provided to broader enterprise. Given the demands of the industry, the need to maximise returns from scarce resources and the decreasing pool of staff available, much of Fáilte Ireland’s training and development work involves providing training, support and advice to existing tourism enterprises and staff members, to enable them enhance in-house knowledge, skills and capacity and so sustain existing jobs in the industry. This was particularly so for many newer enterprises where experience of such adverse conditions was limited after many years of growth. Fáilte Ireland focused on equipping enterprises with core survival skills, especially careful management of costs and resources. As the scope for growth becomes more visible, opportunities to move to a more growth-oriented support framework is emerging. In looking forward to renewed growth in tourism, tourism policy will need to consider how the sector can best generate employment, and particularly how it can play a role in offering opportunities to the unemployed and to others who have limited opportunities for employment. This leads onto consideration of the appropriate balance of entry level and advanced/professional training, where the State needs to play a role or subsidise such training, ensuring that the needs of both workers and enterprises are met in a way that supports long-term growth. The rapidly evolving skills and labour market policy and services environment in Ireland are also factors to be taken into account, with Solas, further education and higher education bodies all playing complementary roles. As noted previously, the enhanced cost competitiveness of the sector as well as the country generally played an important part in stabilising overseas tourism revenues. It is imperative that we maintain appropriate levels of cost competitiveness, while recognising that Ireland is not and does not want to be a “cheap” destination.

18

Competitiveness is about more than cost. As well as the WTTC/WEF World Tourism and Travel Competitiveness Index, the wider elements of competitiveness are being considered in a number of fora, including the OECD. These wider elements will inform the overall policy review and, where elements are outside the tourism policy area, the wider implementation strategy. In using such assessments, however, it is important to be clear about the marketplace that Ireland competes in and who our competitors are. This is also relevant in assessing the impact of policy by using tourism revenues and other data.

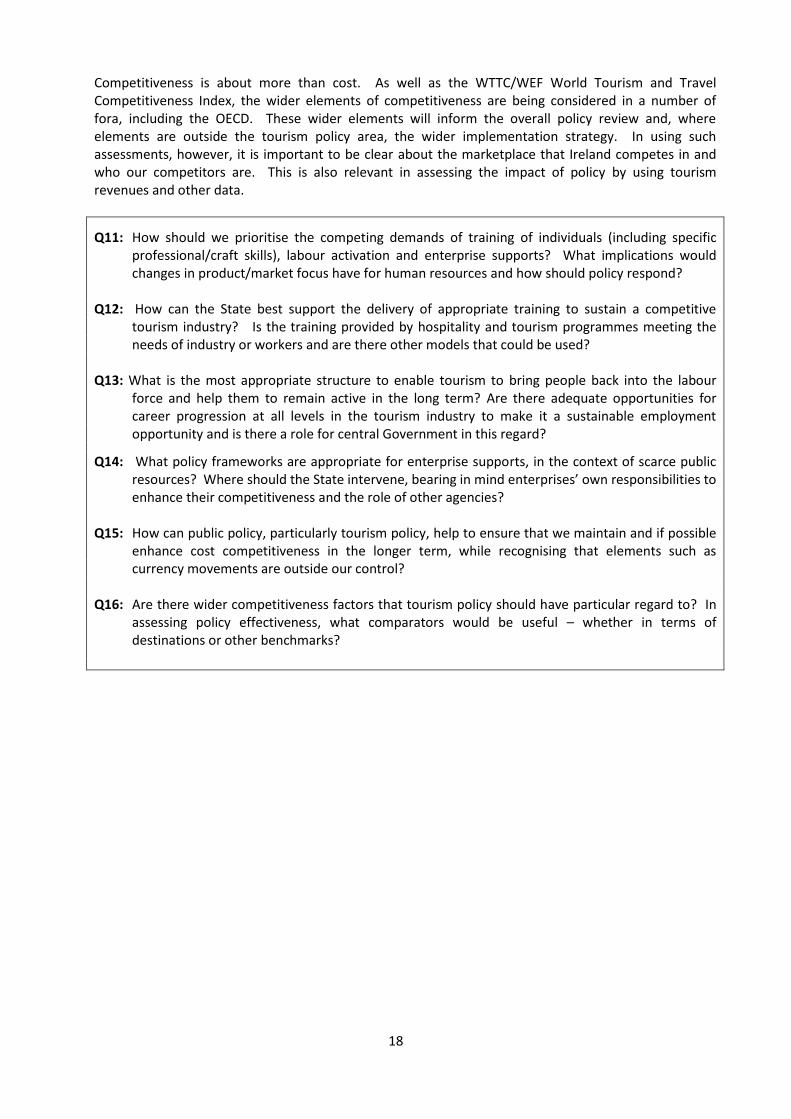

Q11: How should we prioritise the competing demands of training of individuals (including specific professional/craft skills), labour activation and enterprise supports? What implications would changes in product/market focus have for human resources and how should policy respond?

Q12: How can the State best support the delivery of appropriate training to sustain a competitive

tourism industry? Is the training provided by hospitality and tourism programmes meeting the needs of industry or workers and are there other models that could be used?

Q13: What is the most appropriate structure to enable tourism to bring people back into the labour

force and help them to remain active in the long term? Are there adequate opportunities for career progression at all levels in the tourism industry to make it a sustainable employment opportunity and is there a role for central Government in this regard?

Q14: What policy frameworks are appropriate for enterprise supports, in the context of scarce public resources? Where should the State intervene, bearing in mind enterprises’ own responsibilities to enhance their competitiveness and the role of other agencies?

Q15: How can public policy, particularly tourism policy, help to ensure that we maintain and if possible

enhance cost competitiveness in the longer term, while recognising that elements such as currency movements are outside our control?

Q16: Are there wider competitiveness factors that tourism policy should have particular regard to? In

assessing policy effectiveness, what comparators would be useful – whether in terms of destinations or other benchmarks?

19

Implementing Policy and Service Delivery Mechanisms:

Background

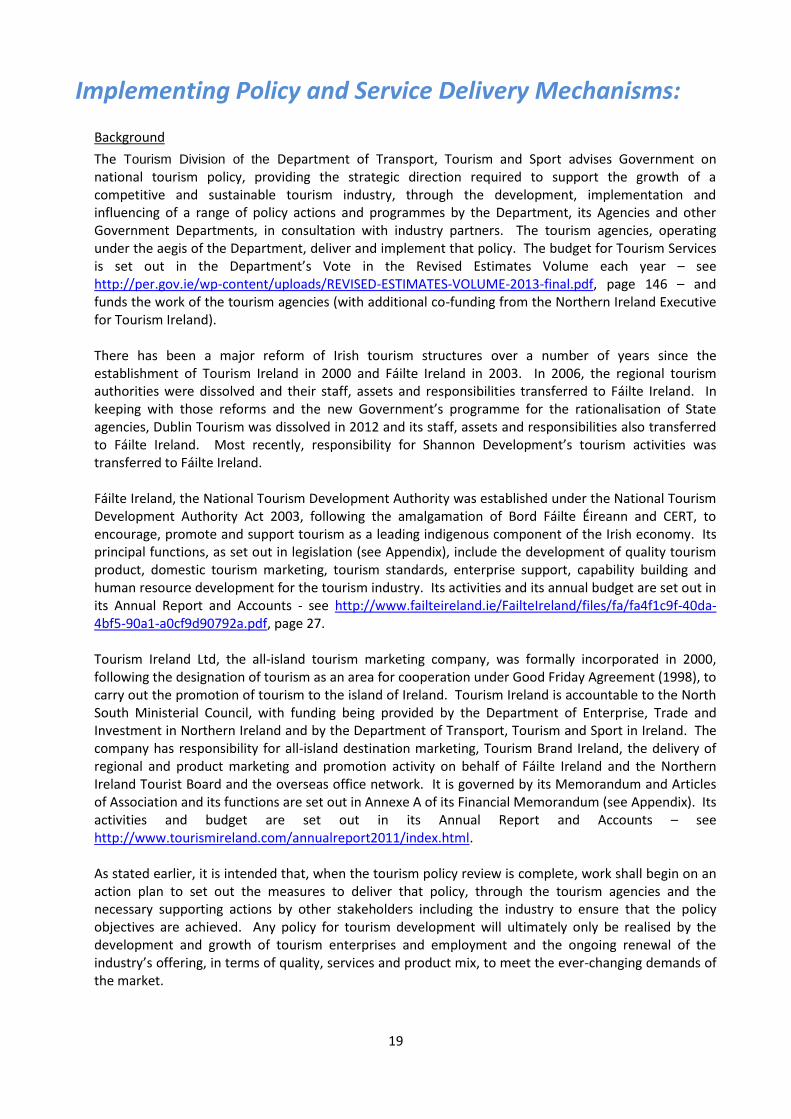

The Tourism Division of the Department of Transport, Tourism and Sport advises Government on national tourism policy, providing the strategic direction required to support the growth of a competitive and sustainable tourism industry, through the development, implementation and influencing of a range of policy actions and programmes by the Department, its Agencies and other Government Departments, in consultation with industry partners. The tourism agencies, operating under the aegis of the Department, deliver and implement that policy. The budget for Tourism Services is set out in the Department’s Vote in the Revised Estimates Volume each year – see http://per.gov.ie/wp-content/uploads/REVISED-ESTIMATES-VOLUME-2013-final.pdf, page 146 – and funds the work of the tourism agencies (with additional co-funding from the Northern Ireland Executive for Tourism Ireland). There has been a major reform of Irish tourism structures over a number of years since the establishment of Tourism Ireland in 2000 and Fáilte Ireland in 2003. In 2006, the regional tourism authorities were dissolved and their staff, assets and responsibilities transferred to Fáilte Ireland. In keeping with those reforms and the new Government’s programme for the rationalisation of State agencies, Dublin Tourism was dissolved in 2012 and its staff, assets and responsibilities also transferred to Fáilte Ireland. Most recently, responsibility for Shannon Development’s tourism activities was transferred to Fáilte Ireland. Fáilte Ireland, the National Tourism Development Authority was established under the National Tourism Development Authority Act 2003, following the amalgamation of Bord Fáilte Éireann and CERT, to encourage, promote and support tourism as a leading indigenous component of the Irish economy. Its principal functions, as set out in legislation (see Appendix), include the development of quality tourism product, domestic tourism marketing, tourism standards, enterprise support, capability building and human resource development for the tourism industry. Its activities and its annual budget are set out in its Annual Report and Accounts - see http://www.failteireland.ie/FailteIreland/files/fa/fa4f1c9f-40da-4bf5-90a1-a0cf9d90792a.pdf, page 27. Tourism Ireland Ltd, the all-island tourism marketing company, was formally incorporated in 2000, following the designation of tourism as an area for cooperation under Good Friday Agreement (1998), to carry out the promotion of tourism to the island of Ireland. Tourism Ireland is accountable to the North South Ministerial Council, with funding being provided by the Department of Enterprise, Trade and Investment in Northern Ireland and by the Department of Transport, Tourism and Sport in Ireland. The company has responsibility for all-island destination marketing, Tourism Brand Ireland, the delivery of regional and product marketing and promotion activity on behalf of Fáilte Ireland and the Northern Ireland Tourist Board and the overseas office network. It is governed by its Memorandum and Articles of Association and its functions are set out in Annexe A of its Financial Memorandum (see Appendix). Its activities and budget are set out in its Annual Report and Accounts – see http://www.tourismireland.com/annualreport2011/index.html. As stated earlier, it is intended that, when the tourism policy review is complete, work shall begin on an action plan to set out the measures to deliver that policy, through the tourism agencies and the necessary supporting actions by other stakeholders including the industry to ensure that the policy objectives are achieved. Any policy for tourism development will ultimately only be realised by the development and growth of tourism enterprises and employment and the ongoing renewal of the industry’s offering, in terms of quality, services and product mix, to meet the ever-changing demands of the market.

20

Similarly, it is internationally recognised that any tourism strategy cannot be delivered solely by the tourism agencies and industry. Tourists experience a wide range of public and private services. An effective strategy will set out how these may best support tourism development, which can be used by the tourism authorities in engaging with such stakeholders. Appropriate mechanisms to facilitate stakeholder engagement should also form part of the strategy. Policy considerations and areas for consultation

As already noted, in tourism, even more than in other sectors, competitiveness is multidimensional. It depends, to varying degrees, on a wide range of factors including all kinds of infrastructure (e.g. air, sea and ground transport, ICT, and tourism-specific), business and taxation rules and regulations, safety and security, cultural and natural resources, environmental sustainability and human resources. Accordingly, no single Government Department controls or directs all related policies and programmes. Local and regional bodies are also critical in contributing to the tourist experience of any destination, not just in providing services specifically for tourists but also in ensuring that the tourist experiences a pleasant and attractive environment. Clearly, the Department of Transport, Tourism and Sport has a key role to play and, where its own policy cannot control all actions affecting tourism, it will continue to champion the tourism sector and engage with other relevant Government Departments in relation to cross-cutting or external policies and programmes that have an impact on tourism. Various parallel strands of funding exist to support the development of certain tourism product at a regional and local level, not all of which come under the aegis of the Department of Transport, Tourism and Sport or the tourism agencies. Although it is not feasible or appropriate to bring all of these funding sources under this Department’s remit, consideration must be given to how expenditure might best be aligned with overarching tourism policy goals.

Substantive changes made to the statutory or North/South frameworks underpinning the two tourism agencies, Fáilte Ireland and Tourism Ireland Ltd, could only progress within a wider political and institutional framework and it is not just a matter of tourism policy. The current structure has delivered very significant efficiencies over the past decade and is the minimum of agencies that can be achieved within the current wider institutional framework. In addition, by matching marketing investment from the Department of Transport, Tourism and Sport with investment from the NI Department of Enterprise, Trade and Investment, Tourism Ireland gains greater purchasing power and voice in the overseas markets. Nonetheless, it is important to keep under review and ensure that all resources, North and South, are best marshalled to support tourism on the island and in the State. The agencies will be bound by overarching Government policy but will exercise discretion and operational independence as provided for in legislation in the execution of their responsibilities. Nonetheless, the new tourism policy will aim to maximise efficiencies, avoid unnecessary duplication of effort and provide the best possible service to industry and to the consumer in line with Government policy priorities. Within the existing high-level architecture, there may be scope to review arrangements to support these objectives particularly given the importance of ensuring that product and experience development is integrated with market focus and marketing campaigns. Within the existing framework, it may also be worth looking at the overall balance of resources – including capital investment, current expenditure on enterprise supports and HR, current expenditure on product and experience promotion and development, information and regulation, and marketing investment.

Q17: Is the overall balance of resources right? Are there are any obvious gaps in the current tourism policy/programmes or in addressing the impact on tourism of other Government policy/programmes? Which functions should be discontinued or wound down?

21

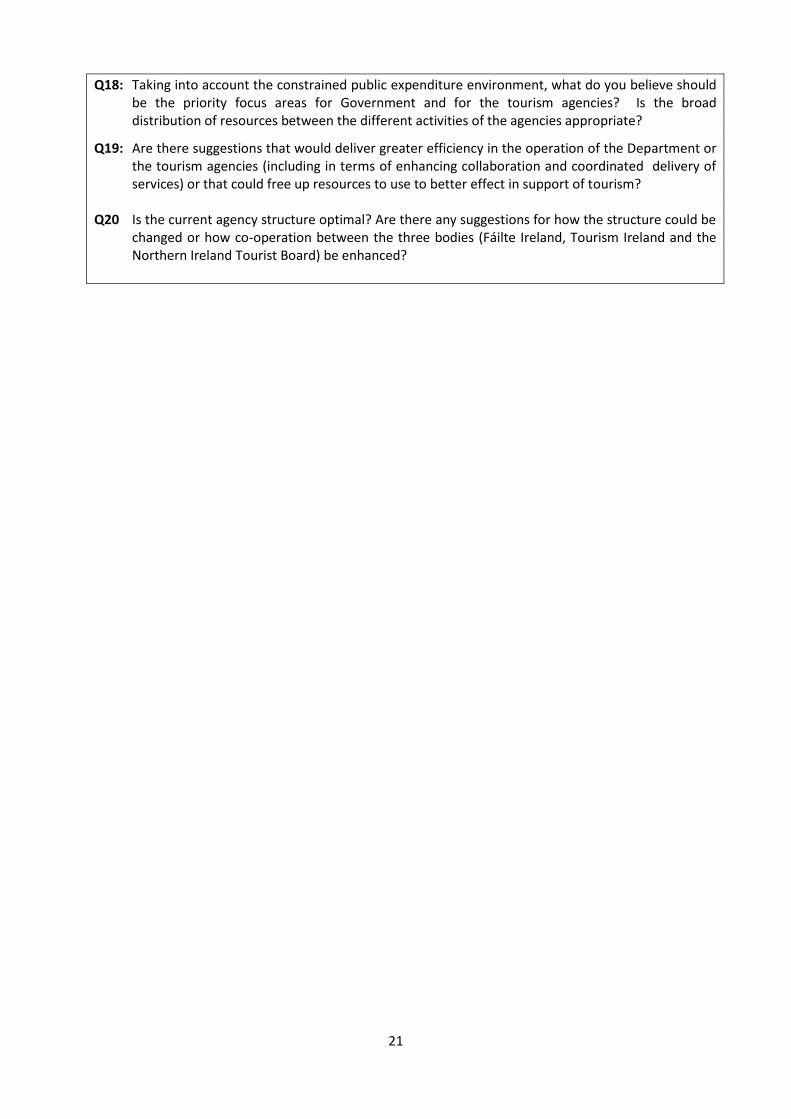

Q18: Taking into account the constrained public expenditure environment, what do you believe should be the priority focus areas for Government and for the tourism agencies? Is the broad distribution of resources between the different activities of the agencies appropriate?

Q19: Are there suggestions that would deliver greater efficiency in the operation of the Department or the tourism agencies (including in terms of enhancing collaboration and coordinated delivery of services) or that could free up resources to use to better effect in support of tourism?

Q20 Is the current agency structure optimal? Are there any suggestions for how the structure could be

changed or how co-operation between the three bodies (Fáilte Ireland, Tourism Ireland and the Northern Ireland Tourist Board) be enhanced?

22

How to submit your views Respondents are requested to make their submissions in writing and, where possible, by email. With regard to the latter, respondents are requested to ensure that electronic submissions are furnished in an unprotected format. Views are requested by Friday 1st November 2013:

1. by email to [email protected] Or 2. by post to: Mr. Anthony Donnelly, Tourism Policy Review, Tourism Marketing and Impact Assessment Unit, Government Buildings, New Road, Killarney, Co. Kerry.

Confidentiality of Submissions Contributors are requested to note that it is the Department’s policy to treat all submissions received as being in the public domain unless confidentiality is specifically requested. Respondents are, therefore, requested to clearly identify material they consider to be confidential and to place same in a separate annex to their response, labelled “confidential”. Where responses are submitted by email, and those emails include automatically generated notices stating that the content of same should be treated as confidential, contributors should clarify in the body of their emails as to whether their comments are to be treated as confidential.

Relevant provisions of Freedom of Information Act 1997 (as amended) Respondents’ attention is drawn to the fact that information provided to the Department may be disclosed in response to a request under the Freedom of Information Act. Therefore, should you consider that any information you provide is commercially sensitive, please identify same, and specify the reason for its sensitivity. The Department will consult with any potentially affected respondent regarding information identified as sensitive before making a decision on any Freedom of Information request.

Queries Any questions regarding this consultation should be emailed to [email protected] or phone Mr. Anthony Donnelly at 064 66 27385.

23

Appendix: Functions of the Tourism Agencies:

Fáilte Ireland (National Tourism Development Authority)

The functions of Fáilte Ireland, the National Tourism Development Authority (referred to below as “the Authority”), are set out in Section 8 of the National Tourism Development Authority Act 2003 (No. 10 of 2003), as follows:

(1) The general functions of the Authority shall be to—

(a) encourage, promote and support (either inside or outside the State)—

(i) the development of tourist traffic within and to the State,

(ii) the development and marketing of tourist facilities and services in the State,

(b) encourage, promote and support the recruitment, training, and education and development, of persons for the purposes of employment in connection with the tourism industry in the State,

(c) establish and maintain registers of hotels, guesthouses, holiday camps, holiday hostels, caravan sites, camping sites, approved holiday cottages, holiday apartments, motor hotels and youth hostels,

(d) promote and engage in research and planning in relation to any matter specified in paragraph (a), (b) or (c), either alone or in cooperation with other persons, and

(e) support, subject to section 25 [paragraph 149], such enterprises and projects relating to—

(i) the development of tourist traffic within or to the State, and

(ii) the development and marketing of tourist facilities and services in the State, as it considers appropriate.

(2) Without prejudice to the generality of subsection (1), the Authority may—

(a) for the purposes of subsection (1)(a)—

(i) engage in advertising and sponsorship or any other form of publicity,

(ii) publish lists of registered and unregistered premises and such other tourist information as it considers appropriate, or

(iii) establish and operate tourist information offices,

(b) in relation to the recruitment, training, and education and development, of persons to whom subsection (1)(b) applies, provide financial aid (including the granting of money in respect of such recruitment, training, or education and development, to persons engaged therein),

(c) in relation to an enterprise or project to which subsection (1)(e) applies provide—

(i) financial aid (including the granting of money in respect of the enterprise or project concerned to persons engaged in the enterprise or project),

(ii) advisory or consultancy services in respect of the enterprise or project, and

(iii) training for persons employed in connection with the enterprise or project, or

(d) provide training to persons in connection with the tourism industry in the State.

(3) The Authority may provide (whether for reward or not)—

(a) advisory services in relation to tourism, or

(b) training to persons in connection with tourism, other than tourism within or to the State.

24

(4) The Authority shall have all such powers as are necessary or expedient for the performance by it of its functions.

(5) The Authority shall, in the performance of its functions, have regard to policies of the Government (including policies of the Government relating to the Irish language and culture) for the time being extant.

(6) The Authority may perform any of its functions through or by any member of the staff of the Authority duly authorised in that behalf by the Authority.

Tourism Ireland Ltd

The functions of Tourism Ireland are set out in Annexe A of the Financial Memorandum, as follows:

OVERALL OBJECTIVE

To promote increased tourism to the island of Ireland MAIN FUNCTIONS OF TOURISM IRELAND LTD

- To plan and deliver international tourism marketing programmes, including programmes in partnership with the industry North and South.

- To publish and disseminate in overseas markets information of a balanced and comprehensive nature on the island of Ireland as a tourist destination which must reflect the diverse traditions, forms of culture expression, and identities within the island.

- To carry out market research, to provide information and other appropriate assistance to help the industry develop international marketing expertise.

- To co-operate with, consult, and assist other bodies or associations in carrying out such activities.

- To carry out surveys and collect relevant statistics and information.

- To subsume the activities [previously] carried out by the Overseas Tourism Marketing Initiative Ltd (OTMI) and to acquire its business assets and undertakings.

- To carry out overseas marketing and promotion activity for Fáilte Ireland and the Northern Ireland Tourist Board.

Recommended

![MINISTRY OF TOURISM AND HOSPITALITY INDUSTRY · ministry of tourism and hospitality industry stakeholder consultation report on alignment of the tourism act [chapter 14:20] with the](https://img.pdfslide.net/doc/110x75/5e7b2aa6e20dcc15ad756736/ministry-of-tourism-and-hospitality-ministry-of-tourism-and-hospitality-industry.jpg)