Petroleum Federation of India

April 13, 2006

India Oil & Gas Overview & Opportunities

Deepak Mahurkar

Oil & Gas Industry Practice

Page 2PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Agenda

Macroeconomic & Energy Indicators

Overview of India’s Petroleum Sector

Destination India

Opportunities in Upstream Sector

Opportunities in Downstream Sector

Opportunities in Natural Gas Sector

Opportunities in Services Sector

Destination Philippines

PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Page 3

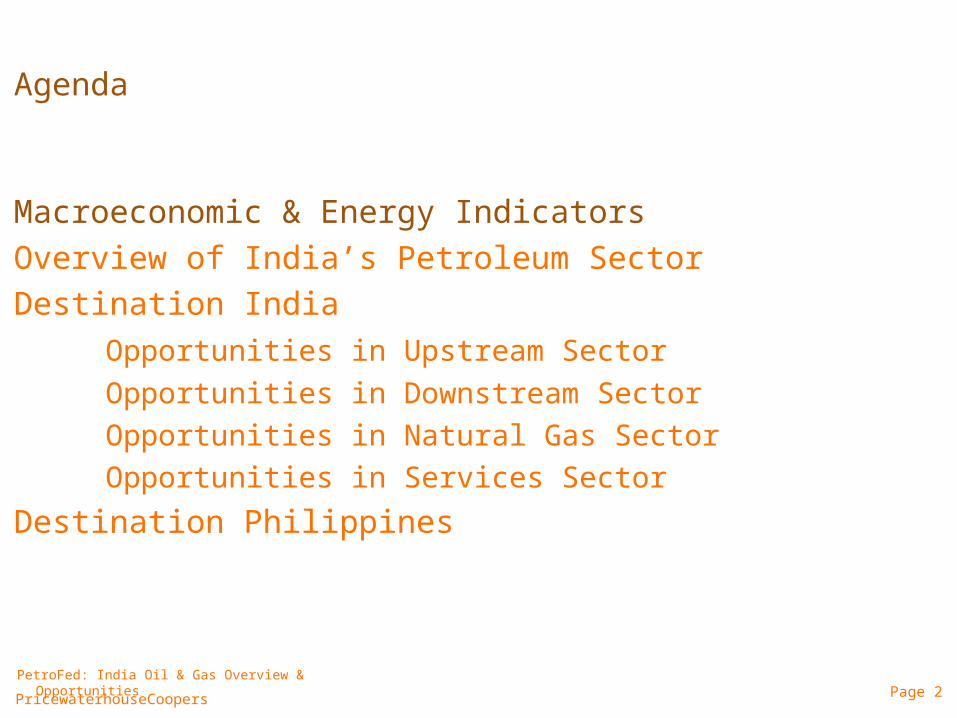

India is a unique economy. Energy challenge is of fundamental importance to India’s economic growth imperatives.

Population : 1.1 bn to 1.47 bn in 2031

Energy consumption : 304 to 1,112 kgoe/capita in 2031

Two Wheelers : 0.6 mn to 41.5 mn over 30 years

Cars : 0.54 mn to 5.71 mn over 30 years ending 2002

CAGR 1.1%

CAGR 5.1%

CAGR 15.3%

CAGR 8.2%

Electricity : absent in 84 mn households in 2000 44.2% of total

Macroeconomic and Energy Indicators

Renewables in use. GHG emissions low. ~ 3% of Globe

Page 4PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

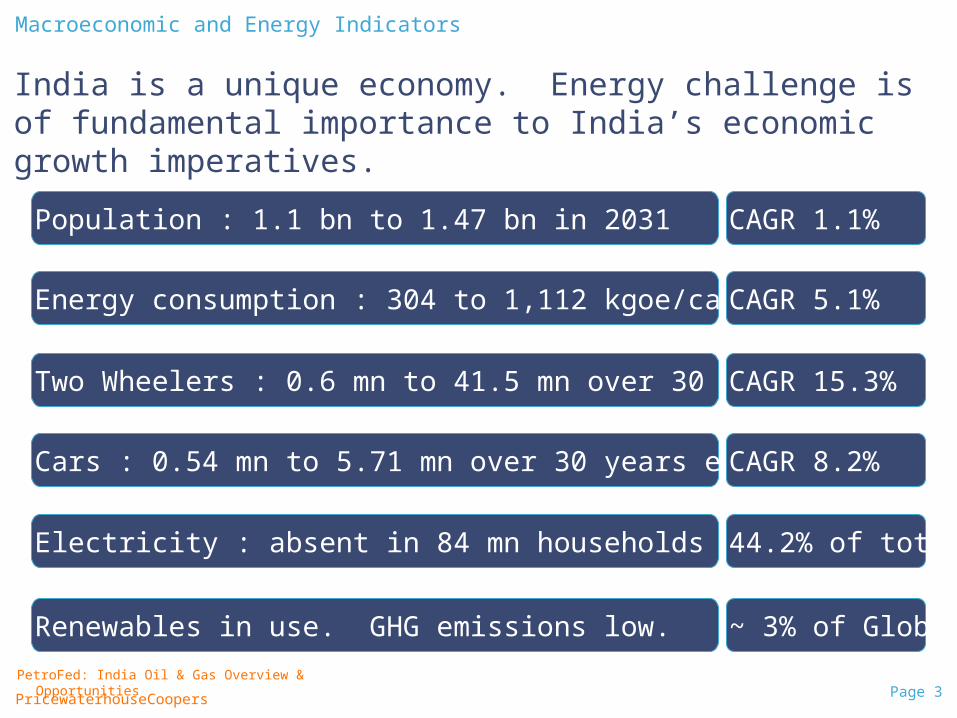

India has an ambition of high Economic Growth Rate.

Macroeconomic and Energy Indicators

Page 5PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

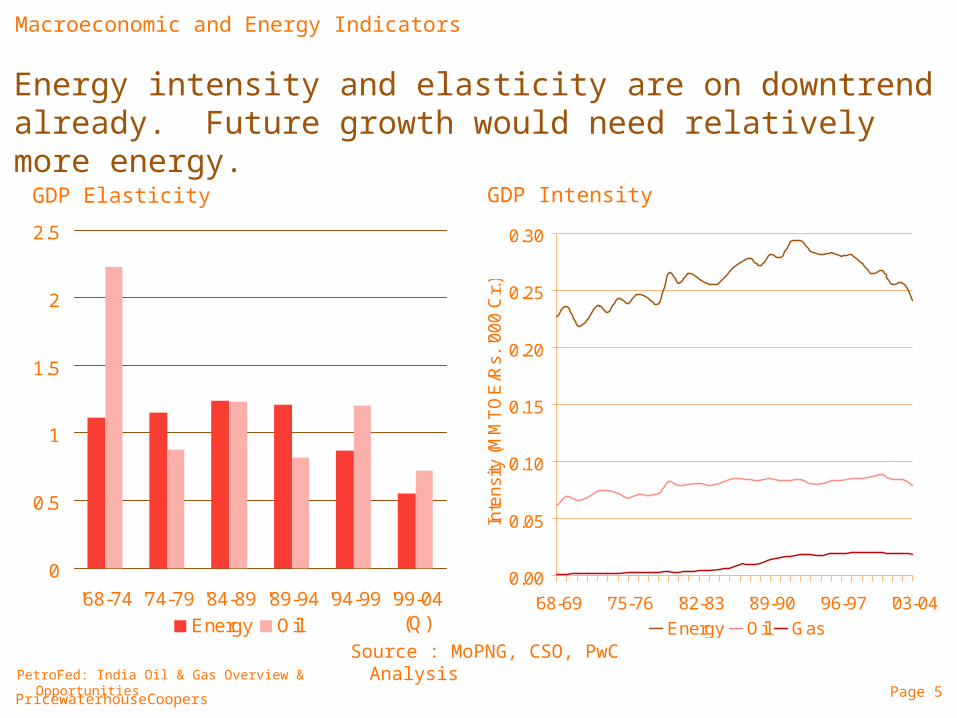

Energy intensity and elasticity are on downtrend already. Future growth would need relatively more energy.

0

0.5

1

1.5

2

2.5

'68-74 '74-79 '84-89 '89-94 '94-99 '99-04(Q)Energy Oil

GDP Intensity

0.00

0.05

0.10

0.15

0.20

0.25

0.30

'68-69 '75-76 '82-83 '89-90 '96-97 '03-04

Inte

nsi

ty (

MM

TO

E/R

s. '0

00

Cr.

)

Energy Oil Gas

GDP Elasticity

Source : MoPNG, CSO, PwC Analysis

Macroeconomic and Energy Indicators

PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Page 6

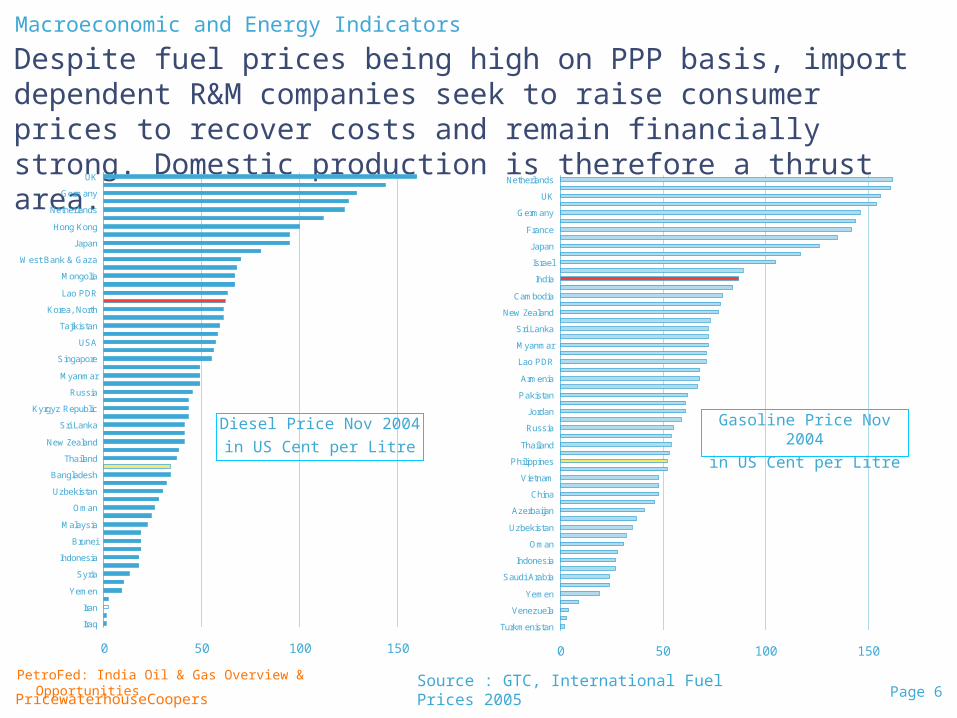

Despite fuel prices being high on PPP basis, import dependent R&M companies seek to raise consumer prices to recover costs and remain financially strong. Domestic production is therefore a thrust area.

0 50 100 150

Iraq

Iran

Yemen

Syria

Indonesia

Brunei

Malaysia

Oman

Uzbekistan

Bangladesh

Thailand

New Zealand

Sri Lanka

Kyrgyz Republic

Russia

Myanmar

Singapore

USA

Tajikistan

Korea, North

Lao PDR

Mongolia

West Bank & Gaza

Japan

Hong Kong

Netherlands

Germany

UK

0 50 100 150

Turkmenistan

Venezuela

Yemen

Saudi Arabia

Indonesia

Oman

Uzbekistan

Azerbaijan

China

Vietnam

Philippines

Thailand

Russia

Jordan

Pakistan

Armenia

Lao PDR

Myanmar

Sri Lanka

New Zealand

Cambodia

India

Israel

Japan

France

Germany

UK

Netherlands

Source : GTC, International Fuel Prices 2005

Diesel Price Nov 2004

in US Cent per Litre

Gasoline Price Nov 2004

in US Cent per Litre

Macroeconomic and Energy Indicators

Page 7PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Agenda

Macroeconomic & Energy Indicators

Overview of India’s Petroleum Sector

Destination India

Opportunities in Upstream Sector

Opportunities in Downstream Sector

Opportunities in Natural Gas Sector

Opportunities in Services Sector

Destination Philippines

Page 8PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

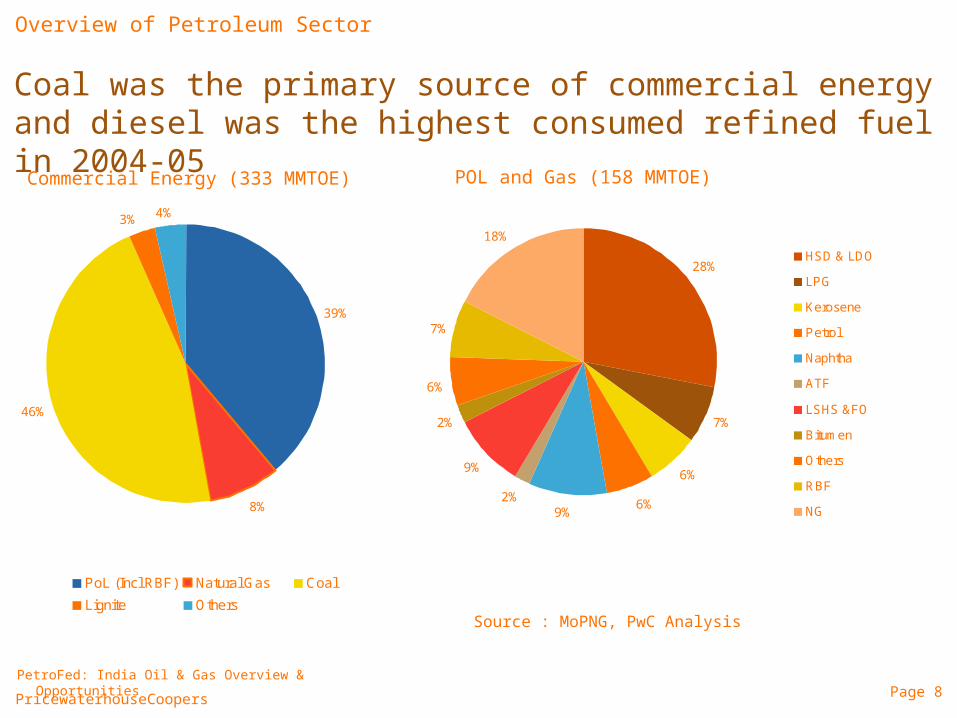

Coal was the primary source of commercial energy and diesel was the highest consumed refined fuel in 2004-05

39%

8%

46%

3% 4%

PoL (Incl RBF) Natural Gas Coal

Lignite Others

Overview of Petroleum Sector

28%

7%

6%

6%9%

2%

9%

2%

6%

7%

18%

HSD & LDO

LPG

Kerosene

Petrol

Naphtha

ATF

LSHS &FO

Bitumen

Others

RBF

NG

Commercial Energy (333 MMTOE) POL and Gas (158 MMTOE)

Source : MoPNG, PwC Analysis

Page 9PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

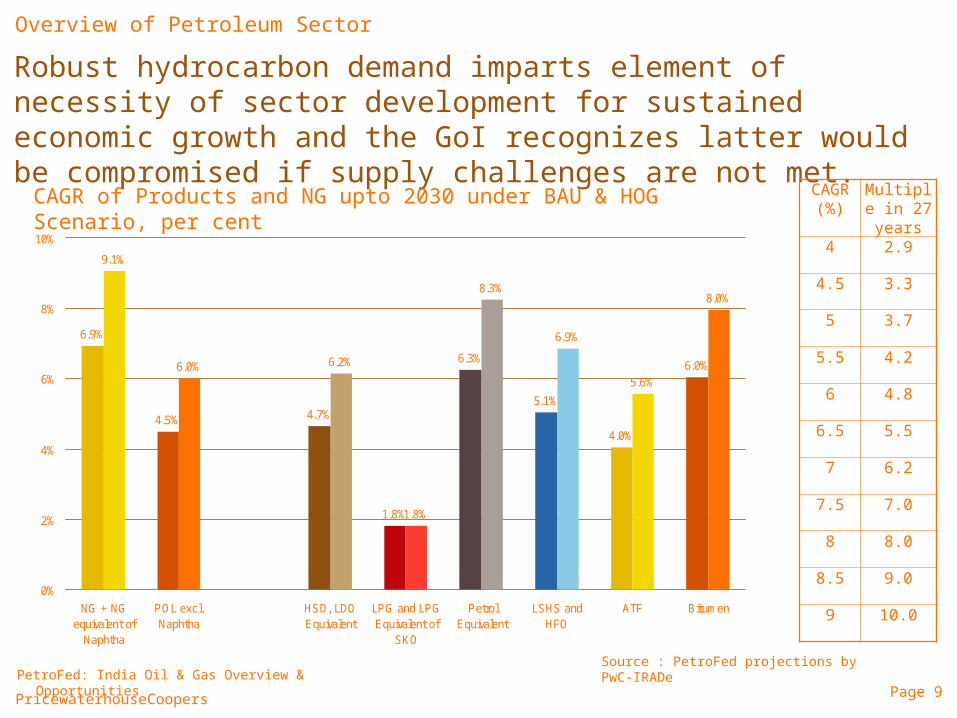

Robust hydrocarbon demand imparts element of necessity of sector development for sustained economic growth and the GoI recognizes latter would be compromised if supply challenges are not met.

Overview of Petroleum Sector

6.9%

4.5% 4.7%

1.8%

6.3%

5.1%

4.0%

6.0%

9.1%

6.0% 6.2%

1.8%

8.3%

6.9%

5.6%

8.0%

0%

2%

4%

6%

8%

10%

NG + NGequivalent of

Naphtha

POL excl.Naphtha

HSD, LDOEquivalent

LPG and LPGEquivalent of

SKO

PetrolEquivalent

LSHS andHFO

ATF Bitumen

CAGR of Products and NG upto 2030 under BAU & HOG Scenario, per cent CAGR(%)

Multiple in 27 years

4 2.9

4.5 3.3

5 3.7

5.5 4.2

6 4.8

6.5 5.5

7 6.2

7.5 7.0

8 8.0

8.5 9.0

9 10.0

Source : PetroFed projections by PwC-IRADe

Page 10PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

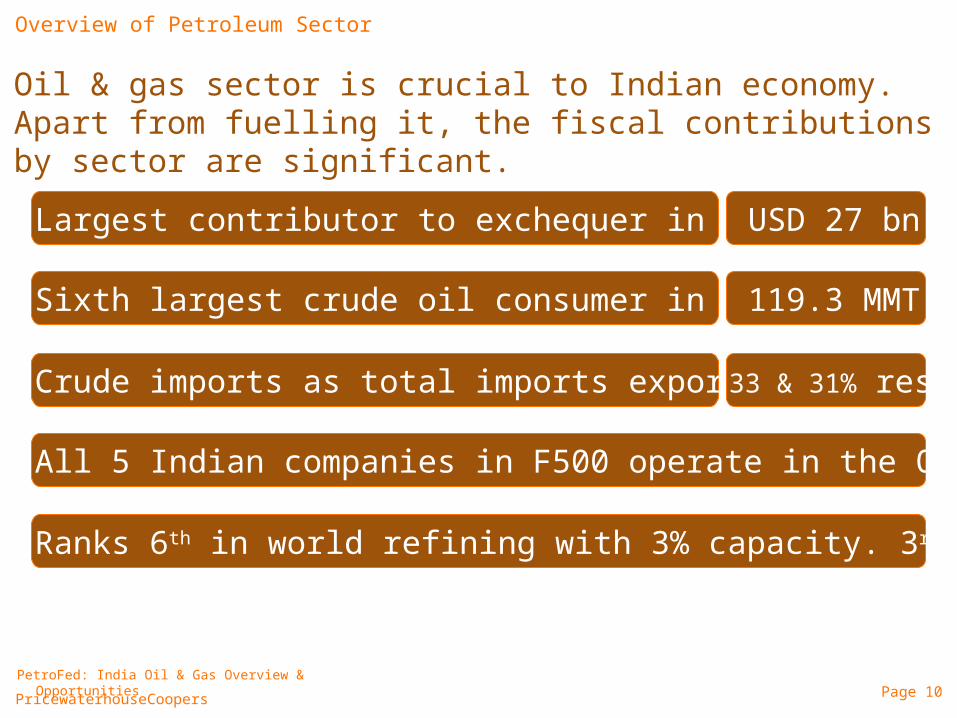

Oil & gas sector is crucial to Indian economy. Apart from fuelling it, the fiscal contributions by sector are significant.

Largest contributor to exchequer in 2004-05

Sixth largest crude oil consumer in the world

Crude imports as total imports exports & imports

All 5 Indian companies in F500 operate in the Oil & Gas sector

USD 27 bn

119.3 MMT

33 & 31% resp.

Ranks 6th in world refining with 3% capacity. 3rd largest refinery.

Overview of Petroleum Sector

Page 11PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

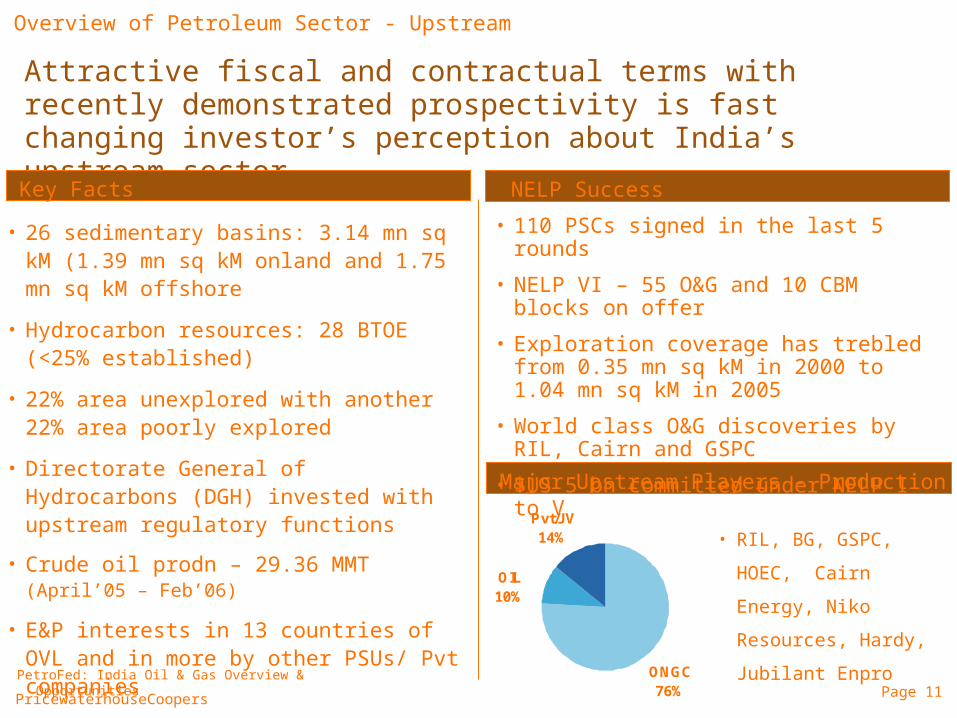

Attractive fiscal and contractual terms with recently demonstrated prospectivity is fast changing investor’s perception about India’s upstream sector

Overview of Petroleum Sector - Upstream

• 26 sedimentary basins: 3.14 mn sq kM (1.39 mn sq kM onland and 1.75 mn sq kM offshore

• Hydrocarbon resources: 28 BTOE (<25% established)

• 22% area unexplored with another 22% area poorly explored

• Directorate General of Hydrocarbons (DGH) invested with upstream regulatory functions

• Crude oil prodn – 29.36 MMT (April’05 – Feb’06)

• E&P interests in 13 countries of OVL and in more by other PSUs/ Pvt companies

Key Facts

Major Upstream Players - Production

Pvt/JV14%

OIL10%

ONGC76%

• RIL, BG, GSPC, HOEC,

Cairn Energy, Niko

Resources, Hardy,

Jubilant Enpro

• 110 PSCs signed in the last 5 rounds

• NELP VI – 55 O&G and 10 CBM blocks on offer

• Exploration coverage has trebled from 0.35 mn sq kM in 2000 to 1.04 mn sq kM in 2005

• World class O&G discoveries by RIL, Cairn and GSPC

• $US 5 bn committed under NELP I to V

NELP Success

Page 12PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

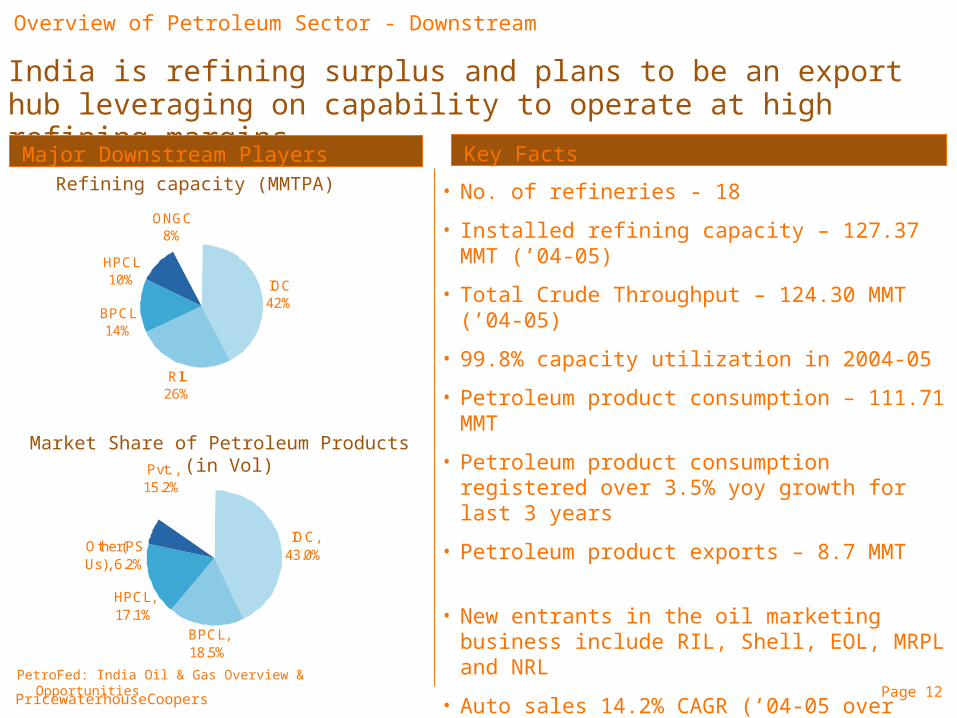

India is refining surplus and plans to be an export hub leveraging on capability to operate at high refining margins

Overview of Petroleum Sector - Downstream

• No. of refineries - 18

• Installed refining capacity – 127.37 MMT (’04-05)

• Total Crude Throughput – 124.30 MMT (’04-05)

• 99.8% capacity utilization in 2004-05

• Petroleum product consumption – 111.71 MMT

• Petroleum product consumption registered over 3.5% yoy growth for last 3 years

• Petroleum product exports – 8.7 MMT

• New entrants in the oil marketing business include RIL, Shell, EOL, MRPL and NRL

• Auto sales 14.2% CAGR (’04-05 over ’00-01)

• Over 31,500 retail outlets including private companies

Major Downstream Players Key Facts

ONGC8%

BPCL14%

RIL26%

IOC42%

HPCL10%

Pvt. , 15.2%

HPCL, 17.1%

BPCL, 18.5%

IOC, 43.0%

Other(PSUs), 6.2%

Refining capacity (MMTPA)

Market Share of Petroleum Products (in Vol)

Page 13PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

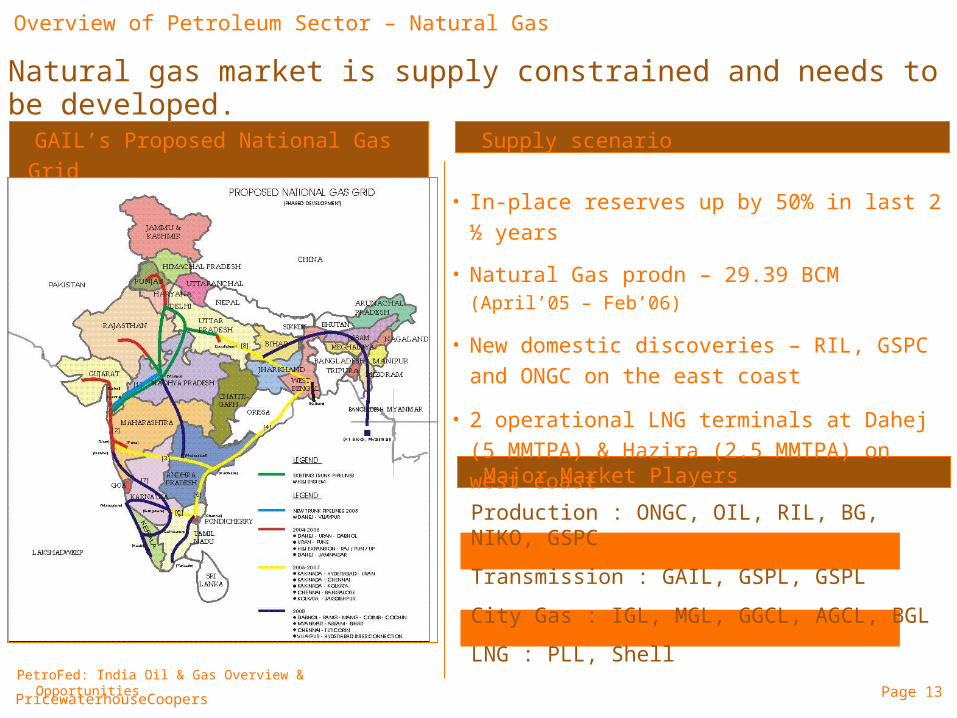

Natural gas market is supply constrained and needs to be developed.

Overview of Petroleum Sector – Natural Gas

Production : ONGC, OIL, RIL, BG, NIKO, GSPC

Transmission : GAIL, GSPL, GSPL

City Gas : IGL, MGL, GGCL, AGCL, BGL

LNG : PLL, Shell

GAIL’s Proposed National Gas Grid

Major Market Players

Supply scenario

• In-place reserves up by 50% in last 2 ½ years

• Natural Gas prodn – 29.39 BCM (April’05 – Feb’06)

• New domestic discoveries – RIL, GSPC and

ONGC on the east coast

• 2 operational LNG terminals at Dahej (5 MMTPA)

& Hazira (2.5 MMTPA) on west coast

Page 14PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Agenda

Macroeconomic & Energy Indicators

Overview of India’s Petroleum Sector

Destination India

Opportunities in Upstream Sector

Opportunities in Downstream Sector

Opportunities in Natural Gas Sector

Opportunities in Services Sector

Destination Philippines

PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Page 15

The

Dem

and

Driv

ers

Gro

win

g ec

onom

y w

ith I

ndus

tria

l, S

ervi

ces

and

Agr

icul

ture

– a

ll th

ree

heav

ily d

epen

dent

on p

etro

leum

sec

tor.

Gro

win

g in

com

e le

vels

and

the

refo

re

disp

osab

le in

com

es

Ris

e in

ene

rgy

inte

nsity

Urb

aniz

atio

n an

d hi

gher

ene

rgy

pene

trat

ion

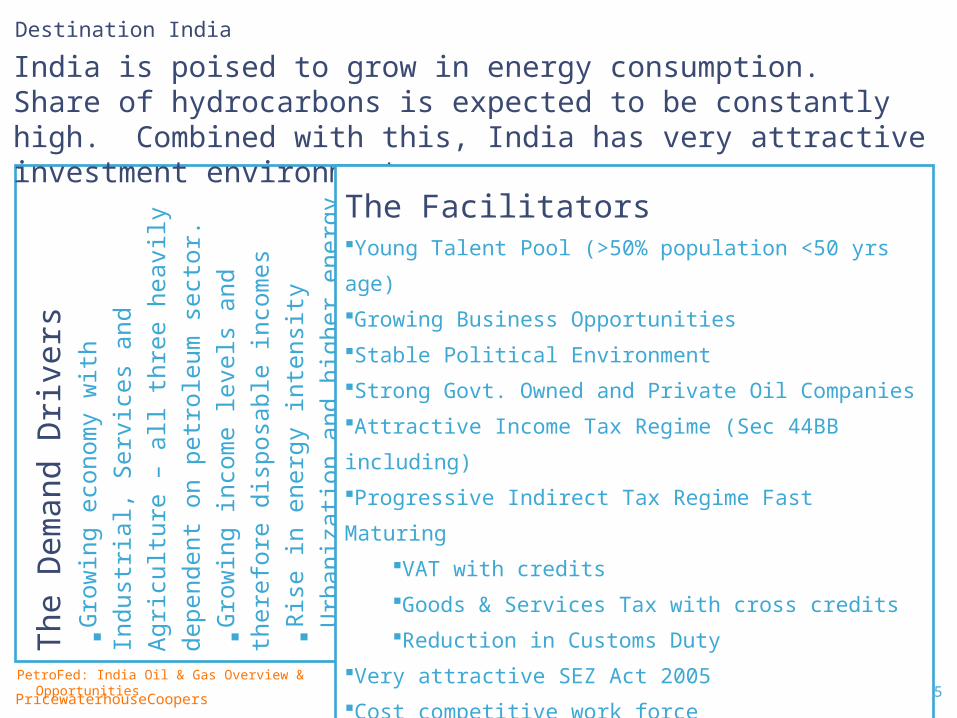

India is poised to grow in energy consumption. Share of hydrocarbons is expected to be constantly high. Combined with this, India has very attractive investment environment.

Destination India

The FacilitatorsYoung Talent Pool (>50% population <50 yrs age)

Growing Business Opportunities

Stable Political Environment

Strong Govt. Owned and Private Oil Companies

Attractive Income Tax Regime (Sec 44BB including)

Progressive Indirect Tax Regime Fast Maturing

VAT with credits

Goods & Services Tax with cross credits

Reduction in Customs Duty

Very attractive SEZ Act 2005

Cost competitive work force

100% FDI allowed* in Petroleum Sector investments

Page 16PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Agenda

Macroeconomic & Energy Indicators

Overview of India’s Petroleum Sector

Destination India

Opportunities in Upstream Sector

Opportunities in Downstream Sector

Opportunities in Natural Gas Sector

Opportunities in Services Sector

Destination Philippines

Page 17PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

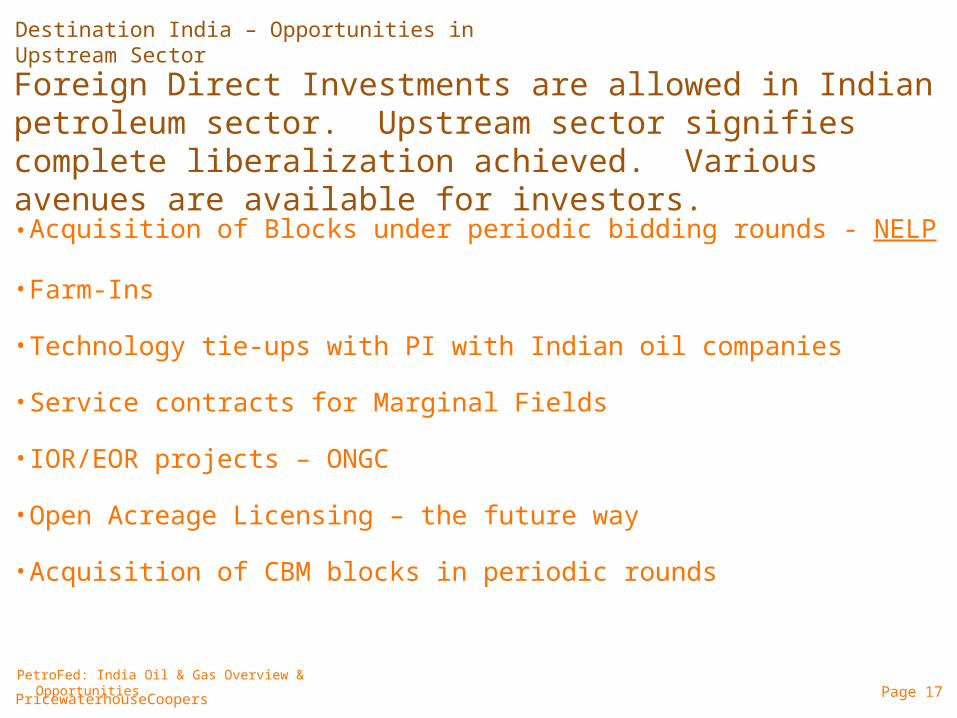

Foreign Direct Investments are allowed in Indian petroleum sector. Upstream sector signifies complete liberalization achieved. Various avenues are available for investors.

• Acquisition of Blocks under periodic bidding rounds - NELP

• Farm-Ins

• Technology tie-ups with PI with Indian oil companies

• Service contracts for Marginal Fields

• IOR/EOR projects – ONGC

• Open Acreage Licensing – the future way

• Acquisition of CBM blocks in periodic rounds

Destination India – Opportunities in Upstream Sector

Page 18PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Agenda

Macroeconomic & Energy Indicators

Overview of India’s Petroleum Sector

Destination India

Opportunities in Upstream Sector

Opportunities in Downstream Sector

Opportunities in Natural Gas Sector

Opportunities in Services Sector

Destination Philippines

Page 19PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Refinery investments are being planned by India for exports and for petrochemical feed-stock purposes. Major oil companies can participate in the activity.

• Refinery expansions and upgradation

• Grass-root refineries

• Integrated complexes – petrochemical & VA products

• Tankages and strategic storage

• Pipelines – crude and products

IOCs interested in retail marketing segment use refining or LNG investment

opportunities to help cross the minimum investment condition for retail market entry

Destination India – Opportunities in Downstream Sector

Page 20PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Agenda

Macroeconomic & Energy Indicators

Overview of India’s Petroleum Sector

Destination India

Opportunities in Upstream Sector

Opportunities in Downstream Sector

Opportunities in Natural Gas Sector

Opportunities in Services Sector

Destination Philippines

Page 21PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

The allied infrastructure needs strengthening. Gas demand and supply imbalance would call for import infrastructure.

• Gas grid connecting producing and consuming locations

• LNG regasification terminals

• Gas Distribution networks

• Fractionators / Extractions

• Petrochemical and VA products

Destination India – Opportunities in Natural Gas Sector

Page 22PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Agenda

Macroeconomic & Energy Indicators

Overview of India’s Petroleum Sector

Destination India

Opportunities in Upstream Sector

Opportunities in Downstream Sector

Opportunities in Natural Gas Sector

Opportunities in Services Sector

Destination Philippines

Page 23PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

More than 800 wells are committed for blocks awarded upto NELP V. The number would go up with ensuing rounds and with discoveries. Service sector is to be in demand.

0

100

200

300

400500

600

700

800

900

2005 & 06 2007 & 08 2009 & 10 2011& 12 Total

ONGC RIL Others Total

Government of India has recognized need for quality, timely and cost optimal services for upstream sector and is ready to offer best investment environment

to companies.

Destination India – Opportunities in Services Sector

Page 24PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Agenda

Macroeconomic & Energy Indicators

Overview of India’s Petroleum Sector

Destination India

Opportunities in Upstream Sector

Opportunities in Downstream Sector

Opportunities in Natural Gas Sector

Opportunities in Services Sector

Destination Philippines

Page 25PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

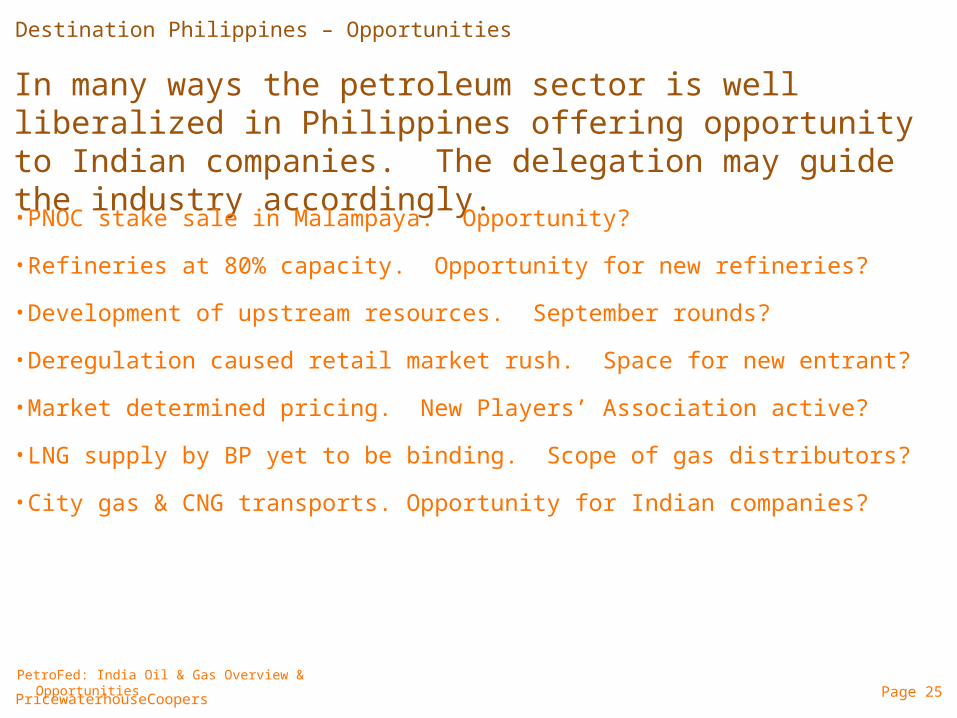

In many ways the petroleum sector is well liberalized in Philippines offering opportunity to Indian companies. The delegation may guide the industry accordingly.

• PNOC stake sale in Malampaya. Opportunity?

• Refineries at 80% capacity. Opportunity for new refineries?

• Development of upstream resources. September rounds?

• Deregulation caused retail market rush. Space for new entrant?

• Market determined pricing. New Players’ Association active?

• LNG supply by BP yet to be binding. Scope of gas distributors?

• City gas & CNG transports. Opportunity for Indian companies?

Destination Philippines – Opportunities

Thank you

© 2006 PricewaterhouseCoopers LLP. All rights reserved. "PricewaterhouseCoopers" refers to PricewaterhouseCoopers LLP (a Delaware limited liability partnership) or, as the context requires, other member firms of PricewaterhouseCoopers International Ltd., each of which is a separate and independent legal entity. *connectedthinking is a trademark of PricewaterhouseCoopers LLP.

India Oil & Gas PracticePricewaterhouseCoopers Pvt. Limited

Sucheta Bhawan11- A, Vishnu Digamber Marg

New Delhi – 110 002Hotline: +91 (11) 23216023Fax: +91(11) 2321 0594/6

Page 27PricewaterhouseCoopers

PetroFed: India Oil & Gas Overview & Opportunities

Upstream sector in India is a relatively unexplored market with reserves estimated in 15 of the 26 sedimentary basins.

Upstream

• Policy approved in Feb 1997

• International competitive bidding

• Single window ECS approval mechanism

• Up to 100% foreign participation

• Fiscal stability provision

• Level playing field – NOCs vs. Pvt companies

• Contract finalization based on MPSC

• Freedom to market O&G in domestic market

• No signature, discovery or production bonus

NELP

Recommended