Recent amendments in GST withcomprehensive coverage of QRMP scheme,ITC utilization restriction and E- Invoicing

CA AANCHAL ROHIT KAPOORCA NEETU SHARMA

M. No. 9988692699, 9888069269,[email protected]

07-01-2021 CA AANCHAL KAPOOR 1

Sr. No. Notification Remarks

1 Notification No. 82/2020 – Central Tax, dated 10.11.2020.

Makes the Thirteenth amendment (2020) to the CGST Rules 2017.

2 Notification No. 84/2020 – Central Tax, dated 10.11.2020.

Notifies class of persons under proviso to section 39(1) of the CGST Act.

3 Notification No. 85/2020 – Central Tax dated 10.11.2020.

Notifies special procedure for making payment of tax liability in the first two months of a quarter

QRMP Applicable

from 01.01.2021

Registered person having aggregate turnoverIN preceding FY up to Five (5) crore rupees

07-01-2021 CA AANCHAL KAPOOR 2

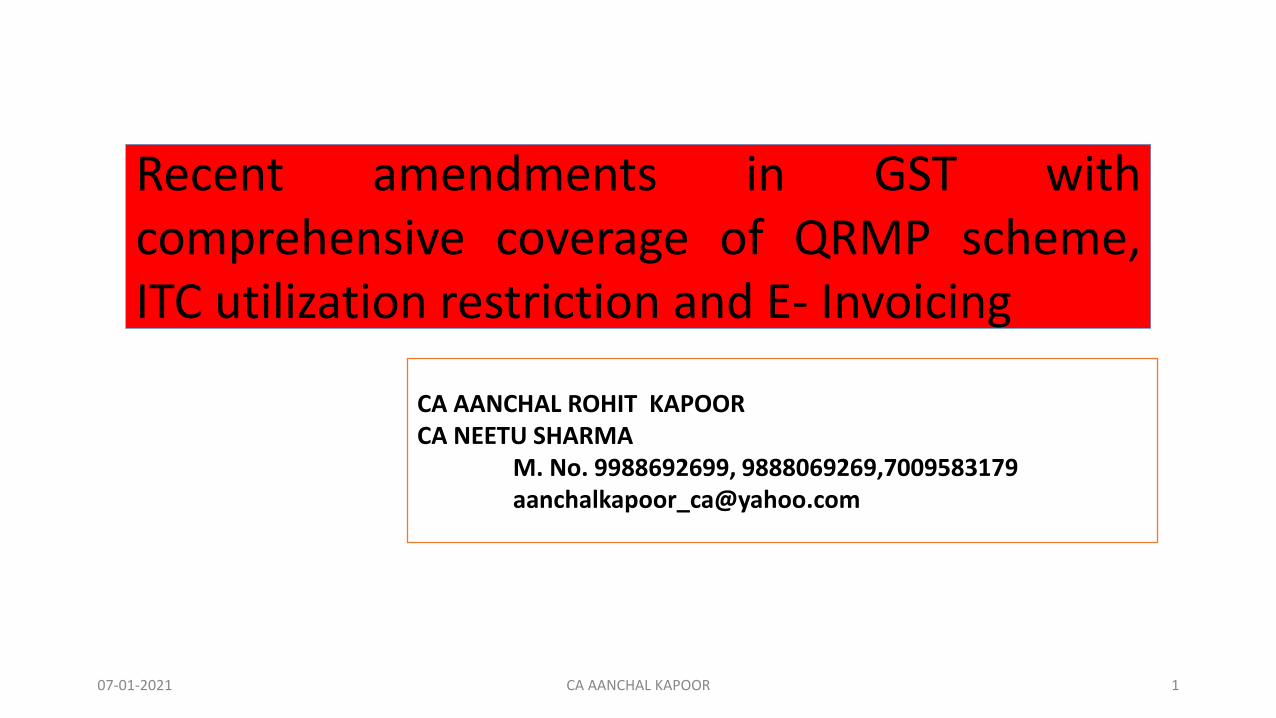

Section Rules Particulars

37 59 Furnishing details of outward supplies

38 59 and 60 Furnishing details of Inward supplies

39 61 to 67 Furnishing details of returns

Sections & Rules to be considered

07-01-2021 CA AANCHAL KAPOOR 3

Whether tax required to be paid if there is Nil liability in preceding

quarter

Switching from fixed methodto self assessment method

Eligibility for QRMP Scheme

Interest liability if amount deposited in first two

months is less than actual liability

Refund if tax paid in first two months is

more than actual tax liability

Late Fee on Delayed Payment of PMT-06

GSTR-1 monthly or quarterly

Conditions of scheme

07-01-2021 CA AANCHAL KAPOOR 4

Overview of QRMP(Quarterly Return Monthly Payment)

07-01-2021 CA AANCHAL KAPOOR 5

RULE 61Form & Manner of Furnishing Return

3B made quarterly for • Agg Turnover upto

Rs. 5 cr. As per 84/2020

Monthly Filling

Quarterly Filling

Pay Tax for each of firsttwo months of the qtr =Form GST PMT-06 by25th day of succeedingmonth

❑ The amount deposited through PMT-06 for 1st and 2nd month will remain inthe cash ledger and will be adjusted on filing 3B at the end of Quarter.

❑ Any claim of refund of such amount lying in balance in the electronic cashledger, if any, out of the amount so deposited shall be permitted only afterthe return in FORM GSTR-3B for the said quarter has been filed.

20th of Succeeding

MonthAs per States

22nd or 24th day of month of

Succeeding quarter

Pay Tax through GSTR-3B

Effective from 01.01.2021

07-01-2021 CA AANCHAL KAPOOR 6

SCREEN SHOT AGGREGATE TURNOVER

07-01-2021 CA AANCHAL KAPOOR 7

Aggregate annual turnover for the preceding financial year shall be calculated in the common portal taking into account

the details furnished in the returns by the taxpayer for the tax periods in the preceding financial year

Registered Person

Intending to file

U/s 39(1) i.e. 3B

Quarterly Indicate his preference for furnishing of return on aquarterly basis, electronically, on the common portal,from the 1st day of the second month of thepreceding quarter till the last day of the first monthof the quarter for which the option is beingexercised:

Example:- Option for filing return for Jan- March, 2022 is to be selected❑ Option to be selected on the portal from 1st Nov,2021 to 31st Jan,

2022.(subject to conditions)

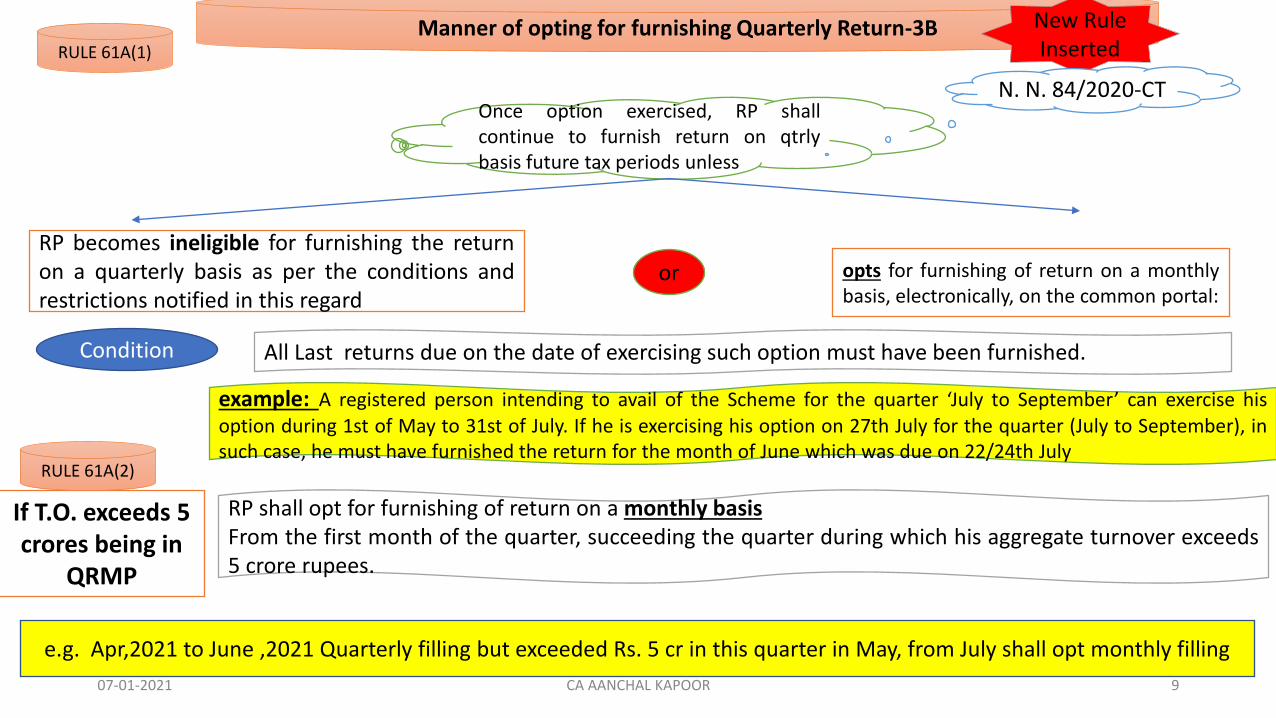

Manner of opting for furnishing Quarterly Return-3B

07-01-2021 CA AANCHAL KAPOOR 8

Fixed Quarters in GST

RULE 61A

RULE 61A(1)Manner of opting for furnishing Quarterly Return-3B New Rule

Inserted

Once option exercised, RP shallcontinue to furnish return on qtrlybasis future tax periods unless

RP becomes ineligible for furnishing the returnon a quarterly basis as per the conditions andrestrictions notified in this regard

or opts for furnishing of return on a monthlybasis, electronically, on the common portal:

If T.O. exceeds 5 crores being in

QRMP

RP shall opt for furnishing of return on a monthly basisFrom the first month of the quarter, succeeding the quarter during which his aggregate turnover exceeds5 crore rupees.

N. N. 84/2020-CT

e.g. Apr,2021 to June ,2021 Quarterly filling but exceeded Rs. 5 cr in this quarter in May, from July shall opt monthly filling

07-01-2021 CA AANCHAL KAPOOR 9

RULE 61A(2)

example: A registered person intending to avail of the Scheme for the quarter ‘July to September’ can exercise hisoption during 1st of May to 31st of July. If he is exercising his option on 27th July for the quarter (July to September), insuch case, he must have furnished the return for the month of June which was due on 22/24th July

All Last returns due on the date of exercising such option must have been furnished.Condition

Quarterly Return Monthly Payment Scheme

Circular No. 143/13/2020- GST

Registered persons are not required to exercise the option every quarter. Where such option has been exercised once, they shall

continue to furnish the return as per the selected option for future tax periods, unless they revise the said option

Opting out ofscheme

Opting out of the Scheme for a quarter will be available from first day of second month of preceding quarter to the lastday of the first month of the quarter

QRMP Scheme is GSTIN wise and therefore, distinct persons as defined in Section 25 of the CGST Act(different GSTINs on same PAN) have the option to avail the QRMP Scheme for one or more GSTINs. In otherwords, some GSTINs for that PAN can opt for the QRMP Scheme and remaining GSTINs may not opt for theScheme

07-01-2021 CA AANCHAL KAPOOR 10

Timeline for opting IN/OUT from QRMP Scheme

• 1st August to 31st Oct

• 1st Nov. to 31st Jan

• 1st May to 31st July

• 1st Feb to 30th April

April-June

July-Sept

Oct-Dec

Jan-March

07-01-2021 CA AANCHAL KAPOOR 11

Notification 84/2020-CT

Deemed Option forGSTR-3B based GSTR-1

RP furnished the return 3B for the tax period October, 2020 on or before 30th November, 2020

Sl. No. Class of registered persons Deemed option—3B

1 Aggregate turnover of up to 1.5 crore rupees, Form GSTR-1 ---Quarterly in C/Y Quarterly return

2 Aggregate turnover of up to 1.5 crore rupees, Form GSTR-1 --- Monthly in C/Y Monthly return

3 Aggregate turnover >1.5 crore rupees =< 5 crore rupees in P/Y Quarterly return

RP may change default option electronically on the common portal, during the period from the 5th day of December,2020 to the 31st day of January, 2021.

07-01-2021 CA AANCHAL KAPOOR 12

SCREEN SHOTS

07-01-2021 CA AANCHAL KAPOOR 13

How to opt the QRMP Scheme?

07-01-2021 CA AANCHAL KAPOOR 14

How to opt the QRMP Scheme?

07-01-2021 CA AANCHAL KAPOOR 15

How to opt the QRMP Scheme?

07-01-2021 CA AANCHAL KAPOOR 16

PRACTICAL CASE STUDIES

07-01-2021 CA AANCHAL KAPOOR 17

Eligibility

F.Y. 2019-20

Aggregate T.O.

4 Cr

F.Y. 2020-21Up to Nov.

3.5 Cr

Eligible

1

F.Y. 2019-20

F.Y. 2020-21Up to Nov.

2

4 Cr

6.5 Cr

07-01-2021 CA AANCHAL KAPOOR 18

Deemed Quarterly

Eligibility

F.Y. 2019-20

Aggregate T.O.

6 Cr

F.Y. 2020-21Up to Nov.

2 Cr

Eligible

3

F.Y. 2019-20

F.Y. 2020-214

4 Cr

4.5 Cr

F.Y. 2021-22 Upto May 7 CrUpto 1st Qtr of 2021-22,thereafter not eligible07-01-2021 CA AANCHAL KAPOOR 19

F.Y. 2019-20

F.Y. 2020-21Up to Nov.

QRMP not eligible

07-01-2021 CA AANCHAL KAPOOR 20

Not eligible for QRMP

Composition Taxpayer

Input Service Distributor

Non Resident Taxable Person

Department orestablishment ofState/ CentralGovt.

If one crossesturnover of Rs. 5Crore, during thequarter

07-01-2021 CA AANCHAL KAPOOR 21

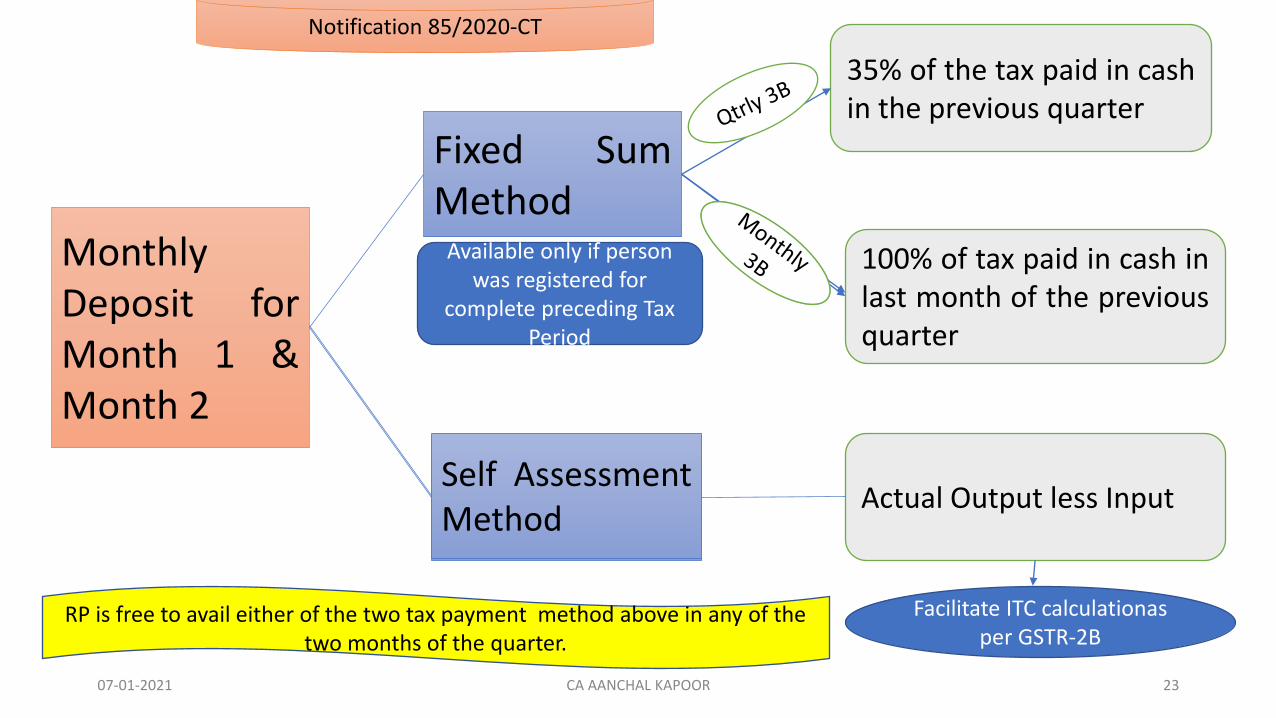

Method of payment

07-01-2021 CA AANCHAL KAPOOR 22

MonthlyDeposit forMonth 1 &Month 2

Fixed SumMethod

Self AssessmentMethod

35% of the tax paid in cashin the previous quarter

100% of tax paid in cash inlast month of the previousquarter

Actual Output less Input

07-01-2021 CA AANCHAL KAPOOR 23

Available only if person was registered for

complete preceding Tax Period

Notification 85/2020-CT

Facilitate ITC calculationasper GSTR-2B

RP is free to avail either of the two tax payment method above in any of the two months of the quarter.

Self AssessmentMethod

A complete tax period means a tax period in which the person is registered from the first day of the tax period till the last day of the tax period.

07-01-2021 CA AANCHAL KAPOOR 24

Complete Tax Period for Fixed Sum Method

Consequences in case of cancellation of registration

• In case of cancellation of registration,

• such person during any of the first two months of the quarter ,

• he is still required to furnish return in Form GSTR-3B for the relevant tax period.

Example :- If one is opting for the scheme on 25th January for Jan-Mar, 2021 quarter, then if got registration on 10th

December, then he cannot opt for Fixed Payment Method, as he was not registered on first day of Tax Period.

Offsetting in 3B

07-01-2021 CA AANCHAL KAPOOR 25

07-01-2021 CA AANCHAL KAPOOR 26

✓ The Amount Deposited in First Two Months will be OFFSET ON FILLING OF GSTR-3B.

✓ Any claim of refund in respect of the amount deposited for the first two months of a quarter for payment of tax shall

be permitted only after the return in FORM GSTR-3B for the said quarter has been furnished.

✓ Further, this deposit cannot be used by the taxpayer for any other purpose till the filing of return for the quarter

Notification 85/2020-CT

Special procedure for payment of tax under proviso to sec. 39(1)

Deposit of an amount in the electronic cash ledger equivalent to, -

i. 35%. of the tax liability paid by debiting the electronic cash ledger in the return for the preceding quarter where the return is

furnished quarterly; or

ii. the tax liability paid by debiting the electronic cash ledger in the return for the last month of the immediately preceding

quarter where the return is furnished monthly:

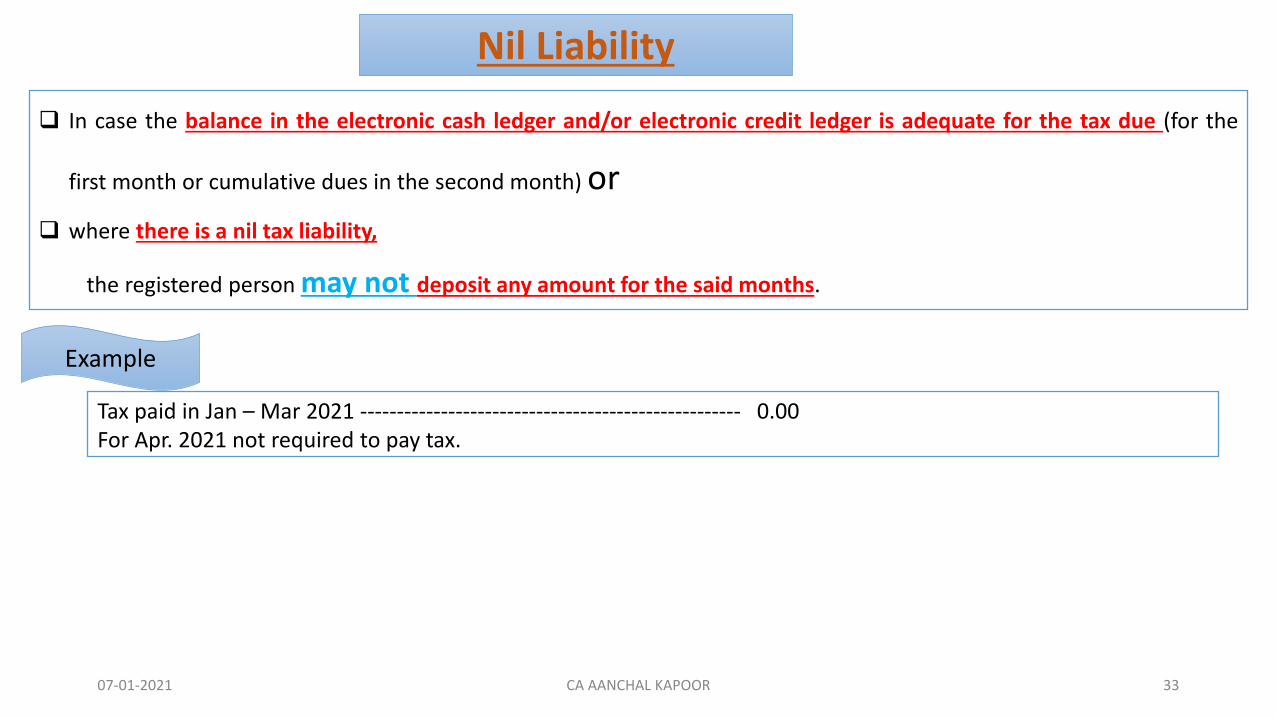

Provided that no such amount may be required to be deposited-

a) for the first month of the quarter, where the balance in the electronic cash ledger or electronic credit ledger is adequate for the tax

liability for the said month or where there is nil tax liability ;

b) for the second month of the quarter, where the balance in the electronic cash ledger or electronic credit ledger is adequate for the

cumulative tax liability for the first and the second month of the quarter or where there is nil tax liability:

Provided further that registered person shall not be eligible for the said special procedure unless he has furnished the return for a

complete tax period preceding such month.

Explanation- For the purpose of this notification, the expression ―a complete tax period means a tax period in which the

person is registered from the first day of the tax period till the last day of the tax period.

Effective from 01.01.2021

07-01-2021 CA AANCHAL KAPOOR 27

Notification No. 85/2020-CTPayment system

Pay tax every month by way of making a deposit of an amount in the electronic cash ledger equivalent to,

i. thirty five per cent. of the tax liability paid by debiting the electronic cash ledger in the

return for the preceding quarter where the return is furnished quarterly; or

ii. the tax liability paid by debiting the electronic cash ledger in the return for the last month of the

immediately preceding quarter where the return is furnished monthly:

no such amount may be required to be deposited-(a) for the first month of the quarter, where the balance in the electronic cash ledger

Orelectronic credit ledger is adequate for the tax liability for the said month

Orwhere there is nil tax liability ;

(b) for the second month of the quarter, where the balance in the electronic cash ledger or electronic creditledger is adequate for the cumulative tax liability for the first and the second month of the quarter or wherethere is nil tax liability:

Proviso

Effective from 01.01.2021

07-01-2021 CA AANCHAL KAPOOR 28

Monthly Payment of Tax

The registered person under the QRMP Scheme would be required to pay the tax due in each of the first two months of the quarterby depositing the due amount in FORM GST PMT-06, by the twenty fifth day of the month succeeding such month.

While generating the challan, taxpayers should select “Monthly payment for quarterly taxpayer” as reason for generating the challan

Methods for monthly payment of tax

Fixed Sum Method

Self assessment Method

A facility is being made available on the portal for generating a pre-filled challan inFORM GST PMT-06 for an amount equal to• 35% of the tax paid in cash in the preceding quarter where the return was

furnished quarterly; or• equal to the tax paid in cash in the last month of the immediately preceding

quarter where the return was furnished monthly.

In case the last return filed was on quarterly basis for Quarter Ending March, 2021:

Tax paid in Cash in Quarter (January -March, 2021)

Tax required to be paid in each of the months – April and May, 2021

CGST 100 CGST 35

SGST 100 SGST 35

IGST 500 IGST 175

Cess 50 Cess 17.5

In case the last return filed was monthly for tax period March, 2021:

Tax paid in Cash in March, 2021

Tax required to be paid in each of the months – April and May, 2021

CGST 50 CGST 50

SGST 50 SGST 50

IGST 80 IGST 80

Cess - Cess -

The said persons, in any case, can pay the tax due by consideringthe tax liability on inward and outward supplies and the inputtax credit available, in FORM GST PMT-06.In order to facilitate ascertainment of the ITC available for themonth, an auto-drafted input tax credit statement has beenmade available in FORM GSTR2B, for every month.

Monthly tax payment through this methodwould not be available to those registeredpersons who have not furnished the return fora complete tax period preceding such month. Acomplete tax period means a tax period inwhich the person is registered from the first dayof the tax period till the last day of the taxperiod

07-01-2021 CA AANCHAL KAPOOR 29

Return Filing Structure

07-01-2021 CA AANCHAL KAPOOR 30

Return Filing Structure

Existing till 31.12.2020

Aggregate Turnover in previousFinancial Year

More than 1.5 cr. Up to 1.5 Cr.

GSTR-1--- MonthlyGSTR-3B--Monthly

GSTR-1--- MonthlyGSTR-3B--Monthly

GSTR-1--- QuarterlyGSTR-3B--Monthly

From 01.01.2021

Aggregate Turnover in previousFinancial Year

More than 5 cr. Up to 5 Cr.

GSTR-1--- MonthlyGSTR-3B--Monthly

GSTR-1--- MonthlyGSTR-3B--Monthly

GSTR-1--- QuarterlyGSTR-3B--Quarterly

07-01-2021 CA AANCHAL KAPOOR 31

Head wise Payment issue

07-01-2021 CA AANCHAL KAPOOR 32

Preceding Month Only Cash Paid in CGST/SGST

QRMP First month Payment is required in IGST

What would be auto-generation of Challan by the portal if it generated for IGST or vice-versa and supply is otherwise?

✓ It will be CGST/SGST

✓ It is pertinent to note that FOR Cash payment to be utilized in other head, one can use PMT-09.

Nil Liability

07-01-2021 CA AANCHAL KAPOOR 33

❑ In case the balance in the electronic cash ledger and/or electronic credit ledger is adequate for the tax due (for the

first month or cumulative dues in the second month) or

❑ where there is a nil tax liability,

the registered person may not deposit any amount for the said months.

Example

Tax paid in Jan – Mar 2021 ---------------------------------------------------- 0.00For Apr. 2021 not required to pay tax.

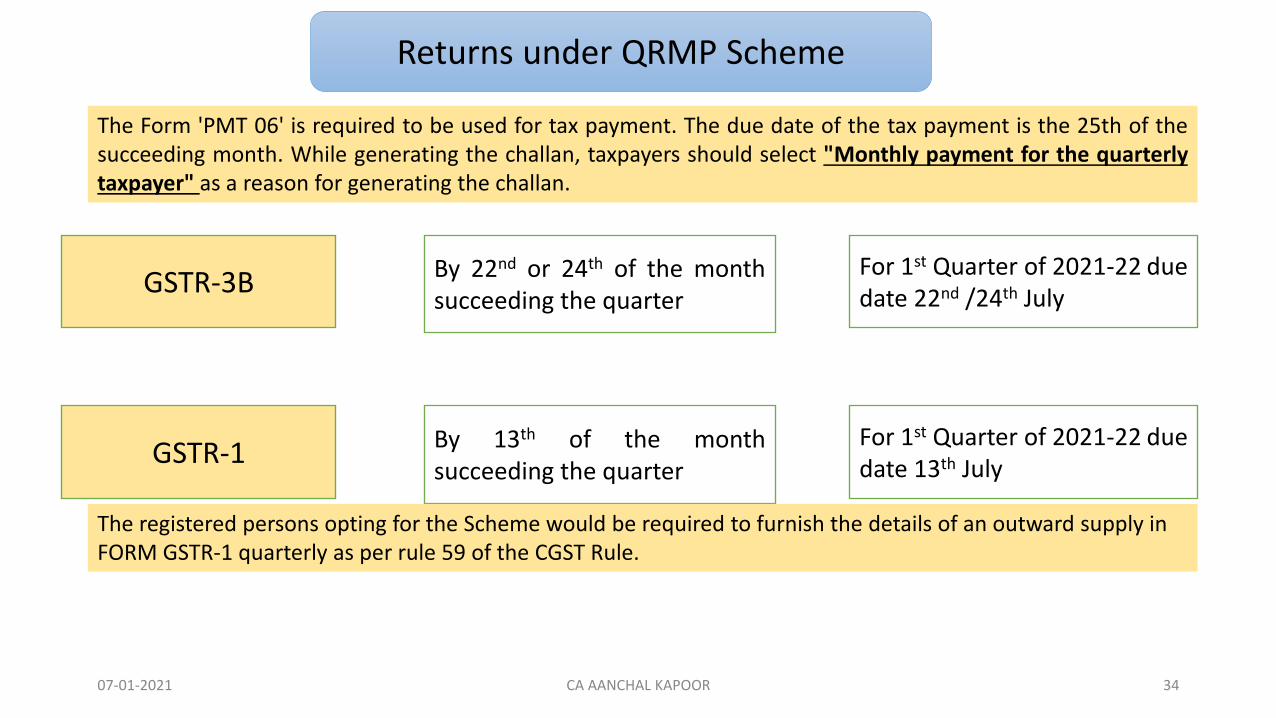

Returns under QRMP Scheme

GSTR-3B By 22nd or 24th of the monthsucceeding the quarter

For 1st Quarter of 2021-22 duedate 22nd /24th July

GSTR-1 By 13th of the monthsucceeding the quarter

For 1st Quarter of 2021-22 duedate 13th July

07-01-2021 CA AANCHAL KAPOOR 34

The registered persons opting for the Scheme would be required to furnish the details of an outward supply in FORM GSTR-1 quarterly as per rule 59 of the CGST Rule.

The Form 'PMT 06' is required to be used for tax payment. The due date of the tax payment is the 25th of thesucceeding month. While generating the challan, taxpayers should select "Monthly payment for the quarterlytaxpayer" as a reason for generating the challan.

INTEREST APPLICABILITY

07-01-2021 CA AANCHAL KAPOOR 35

Interest Applicability

No interest would be payable in case the tax due is paid in the first two months of the quarter by way of depositingauto-calculated fixed sum amount as detailed in para 6.1(a) above by the due date.In other words, if while furnishing return in FORM GSTR-3B, it is found that in any or both of the first two months ofthe quarter, the tax liability net of available credit on the supplies made /received was higher than the amount paidin challan, then, no interest would be charged provided they deposit system calculated amount for each of the firsttwo months and discharge their entire liability for the quarter in the FORM GSTR-3B of the quarter by the due date.

In case such payment of tax by depositing the system calculated amount in FORM GST PMT-06 is not done by duedate, interest would be payable at the applicable rate, from the due date of furnishing FORM GST PMT-06 till the dateof making such payment.

Further, in case FORM GSTR-3B for the quarter is furnished beyond the due date, interest would be payable as perthe provisions of Section 50 of the CGST Act for the tax liability net of ITC.

Fixed Sum Method

07-01-2021 CA AANCHAL KAPOOR 36

A registered person, who has opted for the Scheme, had paid a total amount of Rs. 100/- in cash as tax liability in the previous quarter

of October to December. He opts to pay tax under fixed sum method.

He therefore pays Rs. 35/- each on 25th February and 25th March for discharging tax liability for the first two months of quarter viz.

January and February. In his return for the quarter, it is found that total liability for the quarter net of available credit was Rs. 125 but

he files the return on 30th April.

Interest would be payable at applicable rate on Rs. 55 [Rs. 125 – Rs. 70 (deposit made in cash ledger in M1 and M2)] for the period

between due date of quarterly GSTR 3B and 30th April

A registered person, who has opted for the Scheme, had paid a total amount of Rs. 100/- in cash as tax liability in the previous

quarter of October to December.

He opts to pay tax under fixed sum method. He therefore pays Rs. 35/- each on 25th February and 25th March for discharging tax

liability for the first two months of quarter viz. January and February.

In his return for the quarter, it is found that liability, based on the outward and inward supplies, for January was Rs. 40/- and for

February it was Rs. 42/-.

No interest would be payable for the lesser amount of tax (i.e. Rs. 5 and Rs. 7 respectively) discharged in these two months

provided that he discharges his entire liability for the quarter in the FORM GSTR-3B of the quarter by the due date.

EXAMPLES

07-01-2021 CA AANCHAL KAPOOR 37

Tax due in 1st

month

PMT-06 filed on 25th

Tax due for 2nd

month

PMT-06 filed on 25th

Total Liability in the quarter(Net ITC)

Difference GSTR 3B filed on due date

Interest Payable?

Remarks

35 Yes 35 Yes 150 80 Yes No -

35 No 35 Yes 150 80 Yes Yes Interest payable on 35 for no. of delay in filing 1st month PMT-06

35 Yes 35 No 150 80 Yes Yes Interest payable on 35 for no. of delay in filing 2nd month PMT-06

35 Yes 35 Yes 150 80 No Yes Interest payable on 80 for no. of days delay in filing 3B

35 No 35 No 150 80 No Yes Interest to be calculated separately for No. of days delay in 1st month PMT-06, 2nd month PMT-06 and GSTR 3B

Interest under Fixed Sum Method

07-01-2021 CA AANCHAL KAPOOR 38

Interest Applicability Self Assessment method

Interest amount would be payable as per the provision of Section 50 of the CGST Act for tax or any part thereof (net ofITC) which remains unpaid / paid beyond the due date for the first two months of the quarter.

Interest calculation for self assessment

Total liability for month1=100

ITC Available forMonth 1=50

Interest will becalculated on• Net of cash

liability ifnotdepositedby due date

OR• If any

amount isunpaid forany month

Net of cash =50

Total liability for month2=150

ITC Available forMonth 2=100

Net of cash =50

Total liability for month3=200

ITC Available forMonth 3=100

Net of cash =5007-01-2021 CA AANCHAL KAPOOR 39

LATE FEE

07-01-2021 CA AANCHAL KAPOOR 40

Late Fee Under QRMP Scheme

Late Fee is applicable only for the delay in furnishing the GSTR 3B and GSTR 1

For Quarterly GSTR 3B filers, the late fee will apply only on the delay in furnishing theGSTR 3B for the quarter.

No late fee if the PMT-06 is filed beyond the due date during M1 and M2

07-01-2021 CA AANCHAL KAPOOR 41

Is scheme applicable GSTIN wise or PAN wise ?

➢ It is clarified that for calculating aggregate annual turnover, the turnover of PAN shall be considered. And while

opting for the scheme, taxpayer can opt in as per GSTIN wise.

Example:- If ABC Ltd, is having PAN based turnover of Rs. 3.67 Crore, then it can opt for the scheme. Now, it’s

having 3 GSTIN A, B, C, then GSTIN A can opt for the scheme. It is not compulsory that all GSTIN should opt for

the scheme.

Due Date for filling quarterly returns and payment of tax ?

Due date for filling GSTR 3B would be 22nd or 24th day of month succeeding such quarter. The due date for filling

GSTR 1 would be 13th day of month succeeding such quarter. Also, the tax shall be paid by 25th day of the

succeeding month due in each of the first two months.

07-01-2021 CA AANCHAL KAPOOR 42

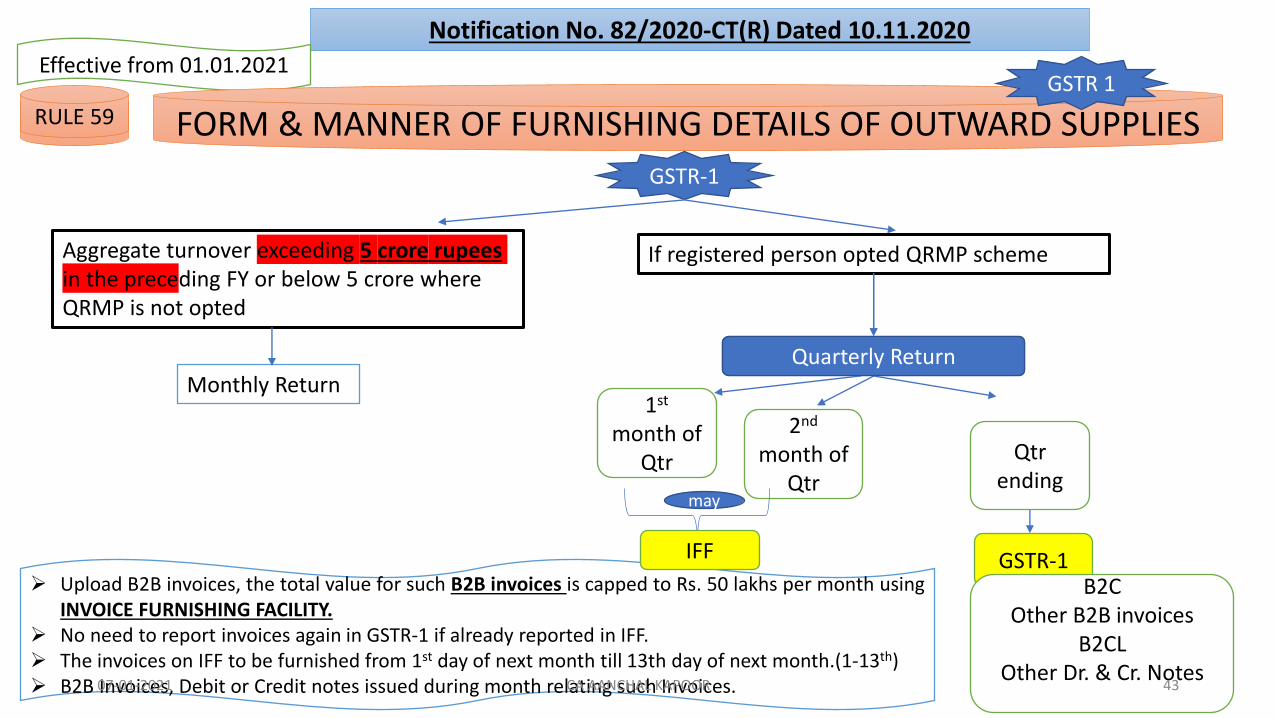

Notification No. 82/2020-CT(R) Dated 10.11.2020

Effective from 01.01.2021

RULE 59

➢ Upload B2B invoices, the total value for such B2B invoices is capped to Rs. 50 lakhs per month usingINVOICE FURNISHING FACILITY.

➢ No need to report invoices again in GSTR-1 if already reported in IFF.➢ The invoices on IFF to be furnished from 1st day of next month till 13th day of next month.(1-13th)➢ B2B Invoices, Debit or Credit notes issued during month relating such Invoices.

FORM & MANNER OF FURNISHING DETAILS OF OUTWARD SUPPLIESGSTR 1

GSTR-1

Monthly Return

Aggregate turnover exceeding 5 crore rupees in the preceding FY or below 5 crore where QRMP is not opted

If registered person opted QRMP scheme

Quarterly Return

1st

month of Qtr

2nd

month of Qtr

Qtrending

may

GSTR-1B2C

Other B2B invoicesB2CL

Other Dr. & Cr. Notes

IFF

RULE 59

07-01-2021 CA AANCHAL KAPOOR 43

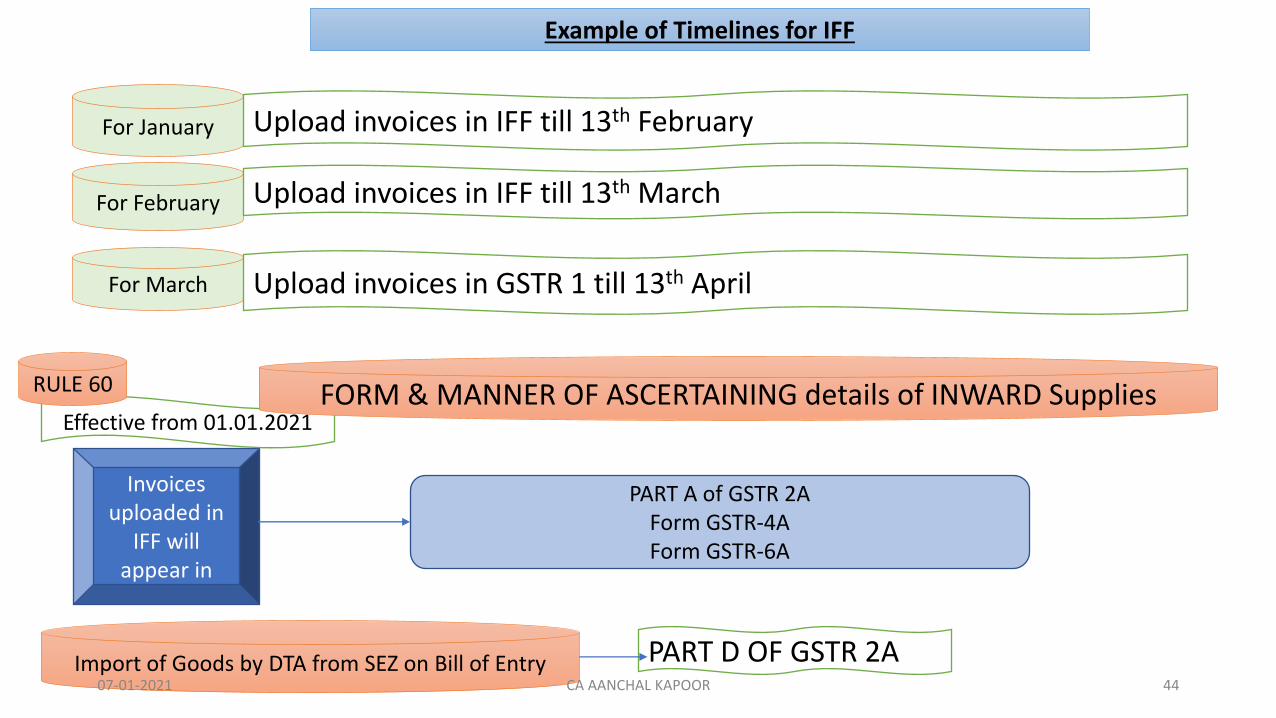

Quarterly Return

For January Upload invoices in IFF till 13th February

For February Upload invoices in IFF till 13th March

For March Upload invoices in GSTR 1 till 13th April

Example of Timelines for IFF

Invoices uploaded in

IFF will appear in

PART A of GSTR 2AForm GSTR-4AForm GSTR-6A

Effective from 01.01.2021

RULE 60 FORM & MANNER OF ASCERTAINING details of INWARD Supplies

Import of Goods by DTA from SEZ on Bill of Entry PART D OF GSTR 2A07-01-2021 CA AANCHAL KAPOOR 44

Effective from 01.01.2021

RULE 60FORM & MANNER OF ASCERTAINING details of INWARD Supplies

Form GSTR-2B notified Made available to RP EVERY MONTH

Day Immediately after Due Date of furnishing of IFF or

FORM GSTR 1 for the month whichever is later

1st& 2nd

month of Qtr

Qtrending

i.e 14th of Next Month

Day Immediately after Due Date of furnishing of FORM

GSTR 1 for the quarter

i.e 14th of Next Month after Qtrending

Details in Form GSTR-2B

For his Supplier with Monthly

Filling of GSTR1

Details uploaded from Day Immediately after Due Date of

furnishing last GSTR 1 till due date of furnishing GSTR1 for the month

e.g For January 2021 12th Jan ––––11th Feb

00:00 hours 23:59 hours

GSTR-5 NRTPGSTR-6 ISD

Details uploaded from Day Immediately after Due Date of

furnishing last GSTR 1 of quarter till due date of furnishing IFF

1stmonth of Qtr

2ndmonth of Qtr

3rd month of Qtr

e.g For January 2021 14th Jan ––––13th Feb

00:00 hours 23:59 hrs

Details uploaded from Day Immediately after Due Date of

furnishing last IFF till due date of furnishing IFF for the month

e.g For Feb, 2021 14th Feb ––––13th Mar

00:00 hours 23:59 hrs

Details uploaded from Day Immediately after Due Date of

furnishing last IFF till due date of furnishing GSTR 1 for the quarter

e.g For Mar, 2021 14th Mar ––––13th April

00:00 hours 23:59 hrs

For his Supplier with Quarterly Filling of

GSTR1

Import of Goods by DTA from SEZ on Bill of Entry07-01-2021 CA AANCHAL KAPOOR 45

Category oftaxpayers

GSTR-1 Invoice filingfacility

PMT-06 forMonth 1

PMT-06 for month2

GSTR 3B

Taxpayer who arerequired to filemonthly return:Taxpayers whoseaggregateturnover is overRs. 5 crore

11th of thefollowing month

NA NA NA 20th of thefollowing month

Taxpayer whohave opted forQRMP scheme

13th day of themonth followingthe quarter

1st to 13th day inMonth 1 & Month2

25th day of themonth followingmonth 1

25th day of themonth followingMonth 2

22nd or 24th day ofthe monthfollowing thequarter.

Return filing due dates w.e.f. 1st Jan 2021

07-01-2021 CA AANCHAL KAPOOR 46

Benefits of QRMP

07-01-2021 CA AANCHAL KAPOOR 47

Benefits of QRMP

Compliance burden of the taxpayer will be reduced significantly

Taxpayer needs to file only 4 GSTR-3B returns instead of 12 GSTR 3B returns in a year.

Taxpayer would be required to file only 4 GSTR -1 returns since invoice filing facility is providedunder the scheme

Pay the tax on monthly basis either by fixed sum method or self assessment method by generatingpre filled challan selecting “Monthly payment for quarterly taxpayers”

Furnish invoice details in IFF depending upon the requirement of their recipient, for first two monthsof the quarter. The remaining invoice details can be furnished in the quarterly GSTR-1

07-01-2021 CA AANCHAL KAPOOR 48

Dec 2020 (Advisory Issued)

No Tab GSTR-3B In Jan 2021

Important points regarding GSRT 1 ( Notified vide NN 94/2020 CT dt 22-12-2020

▪A registered person shall not be allowed to file GSTR-1 if he has not furnished the GSTR 3B for the

preceding 2 months.

▪ A registered person who opted for the QRMP scheme shall not be allowed to furnish the GSTR-1 or

use the IFF , if he has not furnished the GSTR 3B for the preceding tax period.

▪ A Registered person who is restricted from using the amount in the credit ledger in terms of Rule 86B

shall not be allowed to be allowed to file the GSTR-1 or use the IFF if he has not furnished the GSTR 3B

for the preceding tax period.

▪With effect from Jan 2021 , where the value of taxable supply in a month exceeds Rs. 50 Lakhs

(excluding exempt supply and zero-rated supply), the registered person shall be allowed to use the

credit ledger only for discharge of 99% of the tax liability – (New Rule 86B inserted)(subject to

Exceptions)07-01-2021 CA AANCHAL KAPOOR 52

OTHER AMENDMENTS

07-01-2021 CA AANCHAL KAPOOR 53

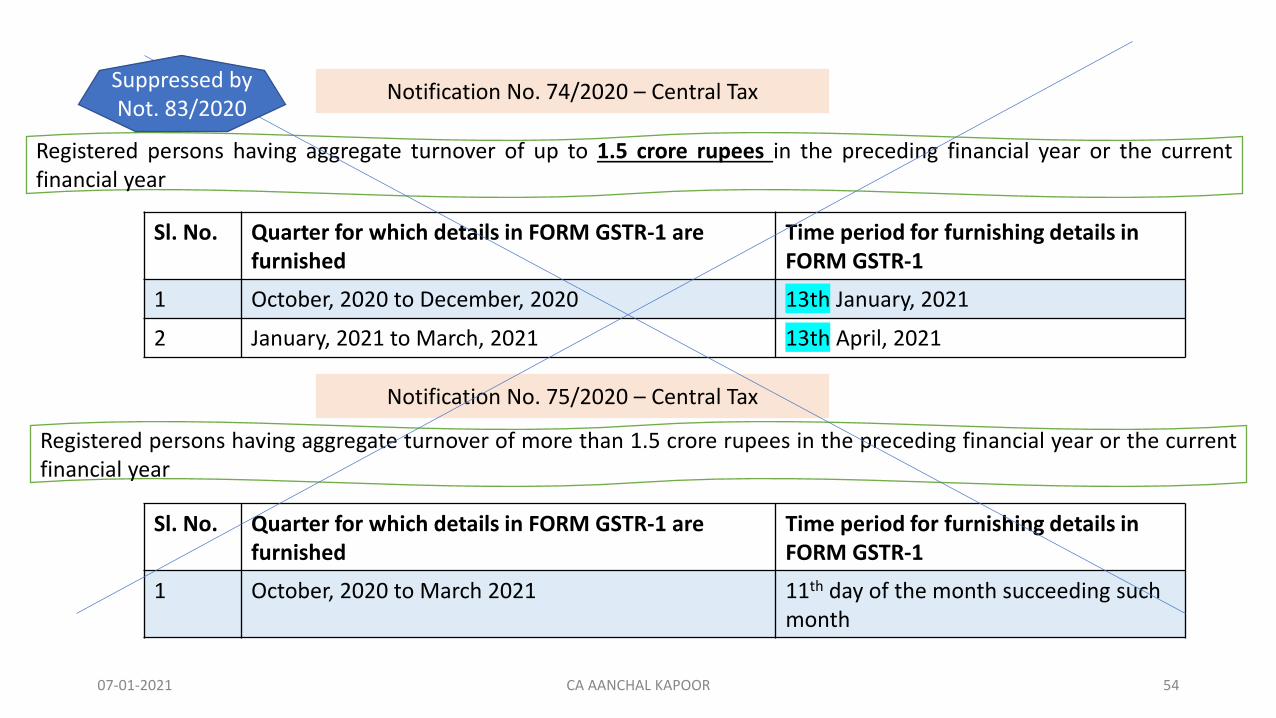

Notification No. 74/2020 – Central Tax

Registered persons having aggregate turnover of up to 1.5 crore rupees in the preceding financial year or the currentfinancial year

Sl. No. Quarter for which details in FORM GSTR-1 are furnished

Time period for furnishing details in FORM GSTR-1

1 October, 2020 to December, 2020 13th January, 2021

2 January, 2021 to March, 2021 13th April, 2021

Registered persons having aggregate turnover of more than 1.5 crore rupees in the preceding financial year or the currentfinancial year

Notification No. 75/2020 – Central Tax

Sl. No. Quarter for which details in FORM GSTR-1 are furnished

Time period for furnishing details in FORM GSTR-1

1 October, 2020 to March 2021 11th day of the month succeeding such month

Suppressed by Not. 83/2020

07-01-2021 CA AANCHAL KAPOOR 54

In suppression of Not. 74/2020 and 75/2020. Time Limit for furnishing GSTR-1

Notification No. 83/2020 – Central Tax

Sl. No. Time period for furnishing details in FORM GSTR-1

1 Monthly 11th day of the month succeeding such month

2 Quarterly 13th day of the month succeeding such quarter

Effective from 01.01.2021N.N. 83/2020

07-01-2021 CA AANCHAL KAPOOR 55

N.N. 87/2020

Extension of time limit for furnishing the declaration in FORM GST ITC-04, in respect of goods dispatched to a job worker or received from a job worker, during the period from July, 2020 to September, 2020 till the 30th day of November, 2020. (Effective 25th October,2020)

N.N. 86/2020

Not. 76/2020 rescinded.(GSTR 3B dates for Oct,20-March,21)

N.N. 88/2020

E-invoicing is mandatory from 01.01.2021 for every taxpayer (other than SEZ unit) whose aggregate TO in any of the FY from 17-18 exceeds 100 Crores

N.N. 92/2020

The Central Government hereby appoints the 1st day of January, 2021, as the date on which the provisions of sections119, 120, 121, 122, 123, 124, 126, 127 and 131 of the said Act shall come into force.

N.N. 93/2020

Late fee payable for delay in furnishing of FORM GSTR-4 for the Financial Year 2019-20 under section 47 of the said Act,from the 1st day of November, 2020 till the 31st day of December, 2020 shall stand waived for the registered personwhose principal place of business is in the Union Territory of Ladakh.”.

N.N. 89/2020

Waiver of penalty payable by registered person u/s 125 for non compliance of N.N. 14/2020 till01.04.2021

N.N. 90/2020

8 digits HSN codes in tax invoice mandatory for some items

N.N. 91/2020

Anti- Profiteering Action by department time extended till March 2021

07-01-2021 CA AANCHAL KAPOOR 56

07-01-2021 CA AANCHAL KAPOOR 57

REGISTRATION PROCEDURES

New Registration

07-01-2021 CA AANCHAL KAPOOR 58

07-01-2021 CA AANCHAL KAPOOR 59

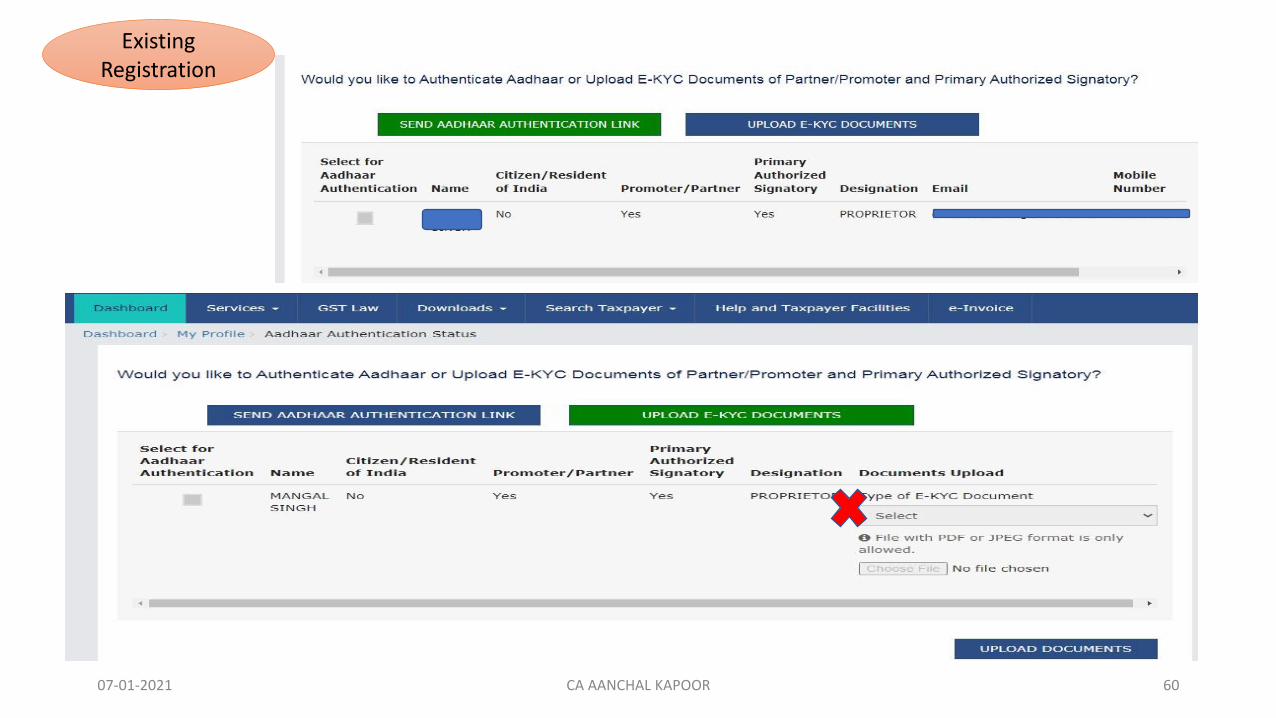

Existing Registration

07-01-2021 CA AANCHAL KAPOOR 60

Existing Registration

Notification No. 17/2020 dated 23.03.2020

The class of persons who shall be exempted from Aadhaar authentication has been notifiedAny person who is not a citizen of India or belong to a class of persons, except the persons mentioned below, are not required to get an aadhaar authentication done, from 1st April 2020:1. Individual2. Authorised signatory of all types3. Managing and Authorised partner, and4. Karta of an Hindu undivided family.

Notification No. 18/2020 dated 23.03.2020

The effective date for Aadhaar authentication before obtaining GST registration is notified.The effective date for Aadhaar authentication before obtaining GST registration is notified------------- 01-04-2020.

Notification No. 19/2020 dated 23.03.2020

The class of persons, other than individuals who shall undergo authentication of Aadhaar number to be eligible forregistration, has been notified.The following persons shall undergo the aadhaar authentication from 1st April 2020:1. Authorised signatory of all types,2. Managing and Authorised partners of a partnership firm, and3. Karta of an Hindu undivided family

07-01-2021 CA AANCHAL KAPOOR 61

Amendment in Rule 8(4A)

Every application made under rule (4) shall be followed by—

(a) biometric-based Aadhaar authentication and taking photograph, unless exempted under sub-section (6D) of section25, if he has opted for authentication of Aadhaar number; or

(a) taking biometric information, photograph and verification of such other KYC documents, as notified, unless theapplicant is exempted under sub-section (6D) of section 25, if he has opted not to get Aadhaar authentication done,

of the applicant where the applicant is an individual or of such individuals in relation to the applicant as notified undersub-section (6C) of section 25 where the applicant is not an individual, along with the verification of the original copy ofthe documents uploaded with the application in FORM GST REG-01 at one of the Facilitation Centres notified by theCommissioner for the purpose of this sub-rule and the application shall be deemed to be complete only after completionof the process laid down under this sub-rule.”.

N.N. 94/2020-CT Dated 22-12-2020

Date to be notified

07-01-2021 CA AANCHAL KAPOOR 62

Aadhar Authentication N.N. 62/2020

Rule 9:- (Verification of the application and approval)Cases of Deemed Registration:-Rule9(5) Proper officer fails to take any action within a period of :-

person successfully undergoesauthentication of Aadhaar number

three working days from the date of submission of the application

fails to undergo authentication of Aadhaarnumber as specified in sub-rule (4A) of rule 8 twenty one days from the date of submission of the application

person does not opt forauthentication of Aadhaar number twenty one days from the date of submission of the application

within a period of seven working days from the date of the receipt of the clarification, information or documents furnished by theapplicant under sub-rule (2),

Rule 25 substituted with following:-“Physical verification of business premises in certain cases.-Where the proper officer is satisfied that the physicalverification of the place of business of a person is required due to failure of Aadhaar authentication or due to not optingfor Aadhaar authentication before the grant of registration, or due to any other reason after the grant of registration, hemay get such verification of the place of business, in the presence of the said person, done and the verification reportalong with the other documents, including photographs, shall be uploaded in FORM GST REG-30 on the common portalwithin a period of fifteen working days following the date of such verification.”.

UPTO 22.12.2020

07-01-2021 CA AANCHAL KAPOOR 63

person successfully undergoesauthentication of Aadhaar number

three working days from the date of submission of the application

fails to undergo authentication of Aadhaarnumber as specified in sub-rule (4A) of rule 8 twenty one days from the date of submission of the application

person does not opt forauthentication of Aadhaar number

Amendment in Rule 9

Verification of the application and approval

07-01-2021 CA AANCHAL KAPOOR 64

w.e.f 22-12-2020

N.N. 94/2020-CT Dated 22-12-2020

Rule 9:- (Verification of the application and approval)Cases of Deemed Registration:-Rule9(5) Proper officer fails to take any action within a period of :-

Thirty days from the date of submission of the application*

person successfully undergoesauthentication of Aadhaar number

Seven working days from the date of submission of the application

fails to undergo authentication of Aadhaarnumber as specified in sub-rule (4A) of rule 8 Thirty days from the date of submission of the application*

person does not opt forauthentication of Aadhaar number

within a period of seven working days from the date of the receipt of the clarification, information or documents furnished by theapplicant under sub-rule (2),

*PO not below rank of AC authorized by Commissioner may carry the Physical Verification of Place of Business, inpresence of said person.

*Notice in Form GST REG-03 may be issued upto 30 days from date of submission of application.

N.N. 94/2020-CT Dated 22-12-2020

The registration granted to a person is liable to be cancelled, if the said person:-

a) does not conduct any business from the declared place of business; or

b) issues invoice or bill without supply of goods or services 2[or both] in violation of the provisions of the Act, or the

rules made thereunder; or

c) violates the provisions of section 171 of the Act or the rules made thereunder.

d) violates the provision of rule 10A

e) avails input tax credit in violation of the provisions of section 16 of the Act or the rules made thereunder; or

f) furnishes the details of outward supplies in FORM GSTR-1 under section 37 for one or more tax periods which is in

excess of the outward supplies declared by him in his valid return under section 39 for the said tax periods; or

g) violates the provision of rule 86B.

Amendment in Rule 21

Cancellation of registration

07-01-2021 CA AANCHAL KAPOOR 65

GSTR1 > GSTR 3B

Anti Prof.

Bank a/c details in 45 days

Amendment in Rule 21A

1. Where a registered person has applied for cancellation of registration under rule 20, the registration shall be deemed tobe suspended from the date of submission of the application or the date from which the cancellation is sought,whichever is later, pending the completion of proceedings for cancellation of registration under rule 22.

2. Where the proper officer has reasons to believe that the registration of a person is liable to be cancelled under section29 or under rule 21, he may 2[***], suspend the registration of such person with effect from a date to be determined byhim, pending the completion of the proceedings for cancellation of registration under rule 22.

(2A) Where, a comparison of the returns furnished by a registered person under section 39 with

a) the details of outward supplies furnished in FORM GSTR-1 ; or

b) the details of inward supplies derived based on the details of outward supplies furnished by his suppliers in their FORM

GSTR-1,

or such other analysis, as may be carried out on the recommendations of the Council, show that there are significant

differences or anomalies indicating contravention of the provisions of the Act or the rules made thereunder, leading to

cancellation of registration of the said person, his registration shall be suspended and the said person shall be intimated

in FORM GST REG-31 , electronically, on the common portal, or by sending a communication to his e-mail address

provided at the time of registration or as amended from time to time, highlighting the said differences and anomalies and

asking him to explain, within a period of thirty days, as to why his registration shall not be cancelled.]

(3) A registered person, whose registration has been suspended under sub-rule (1) or sub-rule (2), 3[or sub-rule (2A)] shall notmake any taxable supply during the period of suspension and shall not be required to furnish any return under section 39.

Suspension of registration.

07-01-2021 CA AANCHAL KAPOOR 66

OBH removed

GSTR 2A/2B

GSTR 3B

Rule 36(4):- Input tax credit to be availed by a registered person in respect of invoices or debit notes, the details of

which have not been furnished by the suppliers under sub-section (1) of section 37, in FORM GSTR-1 or using the

invoice furnishing facility shall not exceed 5 per cent of the eligible credit available in respect of invoices or

debit notes the details of which have been furnished by the suppliers under sub-section (1) of section 37 in FORM GSTR-

1 or using the invoice furnishing facility

Rule 36(4) amended (effective from January 1, 2021)

Reduction in ITC entitlement for invoices not furnished by supplier from 10% to 5%

07-01-2021 CA AANCHAL KAPOOR 67

Explanation.-For the purposes of this sub-rule, the expression "shall not make any taxable supply" shall mean that the registered personshall not issue a tax invoice and, accordingly, not charge tax on supplies made by him during the period of suspension4) The suspension of registration under sub-rule (1) or sub-rule (2) 3[or sub-rule (2A)] shall be deemed to be revoked upon completion of theproceedings by the proper officer under rule 22 and such revocation shall be effective from the date on which the suspension had come intoeffect:]Provided that the suspension of registration under this rule may be revoked by the proper officer, anytime during the pendency of theproceedings for cancellation, if he deems fit.]5) Where any order having the effect of revocation of suspension of registration has been passed, the provisions of clause (a) of sub-section(3) of section 31 and section 40 in respect of the supplies made during the period of suspension and the procedure specified therein shallapply.]

Circular No. 145/01/2021-GST

SOP for implementation of the provision of suspension of registrations under sub-rule (2A) of rule 21A of CGST Rules, 2017

Return furnishedu/s 39 Compared with

the details of outward supplies furnishedin FORM GSTR-1

the details of inward supplies derivedbased on the details of outward suppliesfurnished by his suppliers in their FORMGSTR-1

or

Significant differencesor anomaliesindicatingcontravention of theprovisions of the Actor the rules

leading to cancellation ofregistration of the said person

Registration shall besuspended and the saidperson shall be

Intimation inFORM GST REG-31

electronically, onthe common portal

by sending acommunication tohis e-mail address

highlighting the said differences and anomaliesand asking him to explain, within a period ofthirty days, as to why his registration shall notbe cancelled.”

Post issuance of FORM GST REG-31 via email, the list

of such taxpayers would be sent to the concerned

Nodal officers of the CBIC/ States. Upon receipt of

reply from the said person or on expiry of thirty days

(reply period), a task would be created in the

dashboard of the concerned proper officer under

“Suo moto cancellation proceeding”.

Till the time functionality for FORM REG-31 is made available on portal, such notice/intimation shall be made availableto the taxpayer on their dashboard on common portal in FORM GST REG-17

The taxpayers will be able to view the notice in the “View/Notice and Order” tab post login.

Taxpayer whoseregistrationsuspended

furnish reply to the jurisdictionaltax officer within thirty daysfrom the receipt of such notice /intimation, explaining thediscrepancies/anomalies

reply to the jurisdictional officer against the noticefor cancellation of registration sent to them, inFORM GST REG-18 online through Common Portalwithing the time limit of thirty days from thereceipt of notice/ intimation.

In case the intimation for suspension and notice for cancellationof registration is issued on ground of non -filing of returns, thesaid person may file all the due returns and submit the response.Similarly, in other scenarios as specified under FORM GST REG-31,they may meet the requirements and submit the reply.

post examination of the response received from the said person, may pass an order either for dropping the proceedings forsuspension/ cancellation of registration in FORM GST REG-20 or for cancellation of registration in FORM GST REG-19. Basedon the action taken by the proper officer, the GSTIN status would be changed to “Active” or “Cancelled Suo-moto” as the casemaybe.

N.N. 94/2020-CT Dated 22-12-2020

GSTR-1 to be blocked in case of non filing of GSTR 3B

✓ Where a taxpayer fails to file GSTR 3B for two preceeding months, his GSTR 1 shall now be blocked.

✓ Similarly, for quarterly return filers, the taxpayer failing to file GSTR 3B for the preceding quarter shall not be permitted to file GSTR

1 of subsequent quarter or IFF.

✓ Persons covered by provisions of Rule 86B, fails to file GSTR 3B for preceeding Tax Period(M/Q), his GSTR 1 shall now be blocked

(Earlier non filing of GSTR 3B used to result in blocking of E-way Bill facility but from now on it shall also result in blocking of GSTR 1 of the taxpayer.)

Rule 59

07-01-2021 CA AANCHAL KAPOOR 70

Not. 94/2020 wrongly mentioned sub rule (5) of 59

Anomaly removed by not. 01/2021 by making it Rule

59(6)

Rule 86B

Notwithstanding anything contained in these rules, the registered person shall not use the amount available in electronic creditledger to discharge his liability towards output tax in excess of ninety-nine per cent. of such tax liability, in cases where thevalue of taxable supply other than exempt supply and zero-rated supply, in a month exceeds fifty lakh rupees:

Provided that the said restriction shall not apply where –a) the said person or the proprietor or karta or the managing director or any of its two partners, whole-time Directors, Members

of Managing Committee of Associations or Board of Trustees, as the case may be, have paid more than one lakh rupees asincome tax under the Income-tax Act, 1961(43 of 1961) in each of the last two financial years for which the time limit to filereturn of income under subsection (1) of section 139 of the said Act has expired; or

b) the registered person has received a refund amount of more than one lakh rupees in the preceding financial year onaccount of unutilised input tax credit under clause (i) of first proviso of sub-section (3) of section 54; or

c) the registered person has received a refund amount of more than one lakh rupees in the preceding financial year on accountof unutilised input tax credit under clause (ii) of first proviso of sub-section (3) of section 54; or

d) the registered person has discharged his liability towards output tax through the electronic cash ledger for an amountwhich is in excess of 1% of the total output tax liability, applied cumulatively, upto the said month in the current financialyear; or

e) the registered person is –(i) Government Department; or(ii) a Public Sector Undertaking; or(iii) a local authority;or ((iv) .statutory body:

Provided further that the Commissioner or an officer authorised by him in this behalf may remove the said restriction after suchverifications and such safeguards as he may deem fit.”.

Restrictions on use of amount available in electronic credit ledger

07-01-2021 CA AANCHAL KAPOOR 71

01.01.2021

07-01-2021

CA AANCHAL KAPOOR 72

Registered Person

Value of taxablesupply in a monthexceeds 50 Lacs

Exempt Supply

Zero Rated Supply This provision is N.A

(can use 100% credit)

Person

proprietorKarta

Any of its twopartnerswhole-timeDirectors, Membersof ManagingCommittee ofAssociations orBoard of Trustees

Paid more than 1lakh as income taxin each of last twoF.Y.

Claimed Refund>100000 inpreceding F.Y. onaccount of unutilized ITC ofexports

Claimed Refund>100000 inpreceding F.Y. onaccount of unutilized ITC ofinverted dutystructure

Output tax paidthrough cashledger > 1% of totaloutput, appliedcumulatively, uptothe said month incurrent F.Y.

Registered person isI. Government

Department; orII. a Public Sector

Undertaking; orIII. a local authority;orIV. a statutory body:MAT and TDS also

considered as IncomeTax (not necessarilyCash Payment)

Provided further that the Commissioner or an officer authorised by him in this behalf may remove the said restriction aftersuch verifications and such safeguards as he may deem fit.”.

99% of such tax liability

Shall not use the

amount available inelectronic credit ledger

i.e Max 99% of Input can be used

to discharge output liability

LEGAL PROVISION

Registered Person Exempt Turnover Export turnover Taxable turnover Rule 86B applicable

February,2021 1 crore 2 crore 45 lakhs No (Rs. 45 lakhs)

March,2021 40 lakhs 15 lakhs 1 crore Yes (Rs. 1 crore)

March 2021

Taxable Sale = 1 Crore Monthly turnover > 50 lakhs Tax @ 5% = 500000 ITC = 800000

Old New

Output 500000 Output 500000

ITC utilized 500000 ITC Utilized (99 % of 500000) 495000

Tax payable 0.00 Tax payable (1%) 5000

Exceptions:- 100 % ITC (Old Rule)

F.Y. 19-20, F.Y. 18-19- 139(1) time expired, Income Tax paid> 1000001

April, 2020- FEb, 2021

Output ITC Cash Ledger

10 Cr 99 Lacs 100000

10Cr 98.5 Lacs 150000

New Rule

Old Rule

3

2

Refund > 1 lakh in F.Y 2019-20

Exports Inverted Duty structure

What if Export with Payment of Taxes ?

or

CASE STUDY

Illustration 1

Particulars CGST SGST IGST Total

Output Turnover 5000000 5000000 3000000 1,30,00,000

Output Tax @18% 900000 900000 540000 23,40,000

Input Tax 960000 960000 500000 24,20,000

Minimum Tax payable as per Rule 86B 9000 9000 5400 23,400

Particulars CGST SGST IGST Total

Output Tax 900000 900000 540000 23,40,000

Input Tax 820000 1000000 540000 2360000

Minimum Tax payable as per Rule 86B 9000 9000 5400 23400

Payment if 86B not there 80000 0 0 80000

Tax payable as per 86B 80000-5400= 74600 9000 (not adjustable with CGST)

5400 paid in IGST adjusted with CGST.

89000

Illustration 2

Particulars CGST SGST IGST Total

Output Turnover 5000000 5000000 3000000 1,30,00,000

Output Tax @18% 900000 900000 540000 23,40,000

Input Tax 820000 820000 540000 21,80,000

Minimum Tax payable as per Rule 86B 9000 9000 5400 23,400

Minimum tax otherwise payable through cash ledger without 86B 80000 80000 - 1,60,000

By paying Rs. 5400 in cash, IGST ITC of 5400 adjusted with C & S, so now Net Payable 77300 77300 5400 1,60,000

Illustration 3

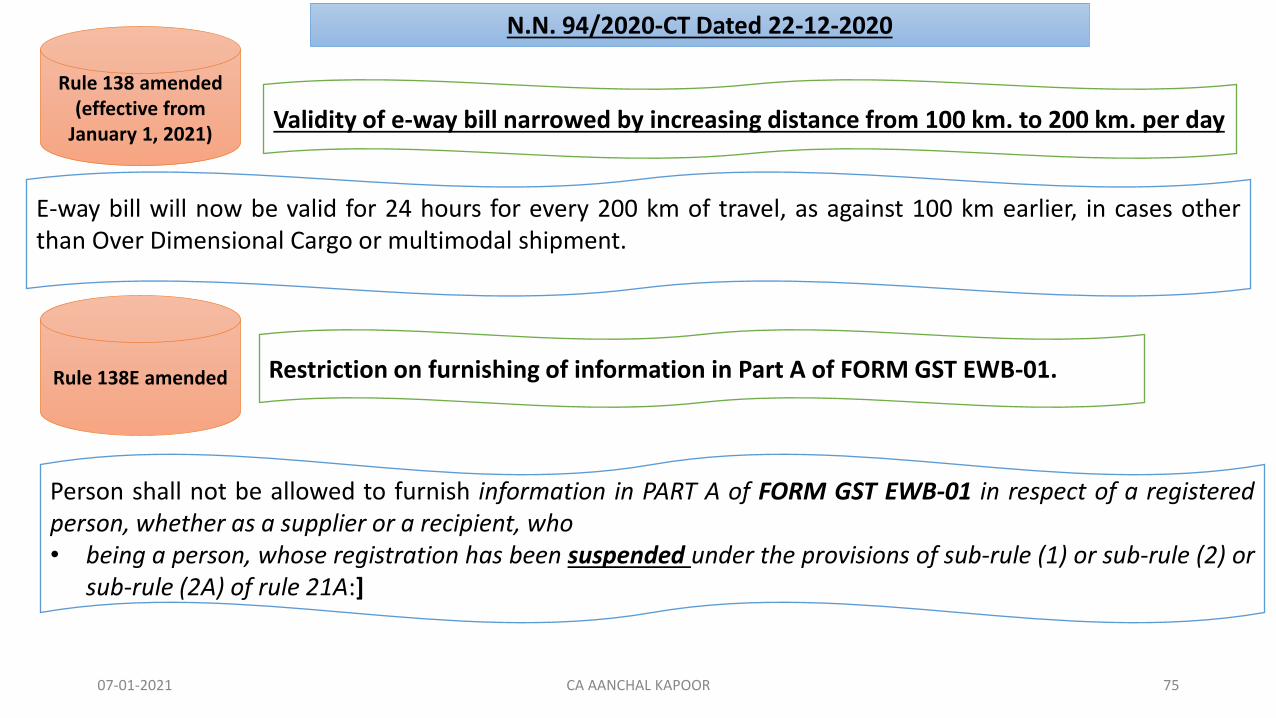

Rule 138 amended (effective from

January 1, 2021)Validity of e-way bill narrowed by increasing distance from 100 km. to 200 km. per day

E-way bill will now be valid for 24 hours for every 200 km of travel, as against 100 km earlier, in cases otherthan Over Dimensional Cargo or multimodal shipment.

N.N. 94/2020-CT Dated 22-12-2020

07-01-2021 CA AANCHAL KAPOOR 75

Person shall not be allowed to furnish information in PART A of FORM GST EWB-01 in respect of a registeredperson, whether as a supplier or a recipient, who• being a person, whose registration has been suspended under the provisions of sub-rule (1) or sub-rule (2) or

sub-rule (2A) of rule 21A:]

Rule 138E amended Restriction on furnishing of information in Part A of FORM GST EWB-01.

Delinking of Debit Notes

Document

Type

Document date Due date for availing credit

Before Amendment

Debit note 15-08-2021

(Linked to Invoice dated 01-

03-2021)

Return for the month of sept. 2021

Debit note 15-11-2021

(Linked to Invoice dated 01-

03-2021)

Return for the month of sept. 2021.

The credit was not getting availed for Debit notes issued after 6 months from end of

Financial Year to which Invoice pertains to.

After amendment

Debit note 15-08-2021

(Linked to Invoice dated 01-

03-2021)

Invoice Linkage became

irrelevant

Return for the month of sept. 2022

Debit note 15-11-2021

(Linked to Invoice dated 01-

03-2021)

Invoice Linkage became

irrelevant

Return for the month of sept. 2022.

The credit which was earlier not getting availed for Debit notes issued after 6 months

from end of Financial Year to which Invoice pertains to will now be available.

FA,2020

FAQ’s on QRMP

What is QRMP scheme? What are its benefit?

➢ Quarterly Return, Monthly Payment of Taxes (QRMP) Scheme is a scheme to simplify compliance for small taxpayers.➢ Under this scheme, taxpayers having an aggregate turnover at PAN level up to Rs. 5 Crore can opt for quarterly GSTR-1 and

GSTR-3B filing. Payment can be made in the first two months by a simple challan in FORM GST PMT-06. For the ease oftaxpayers, system has assigned quarterly frequency to small taxpayers automatically.

Why have I been assigned quarterly filing without opting for the same?

➢ Taxpayers eligible for the simplified compliance scheme were assigned quarterly frequency by the GST system. Alltaxpayers were informed regarding the frequency assigned to them by e-mail and SMS.

Why have I been assigned quarterly frequency by system even when my aggregate turnover on PAN is greater thanRs. 5 crore?

➢ For the purpose of determining the eligibility for QRMP, the turnover was determined on the basis of the valuesdeclared by taxpayers in Table-3.1 of GSTR-3B (except inward supplies attracting reverse charge) for the FinancialYear 2019-20. If a component of the turnover, like exempted or non-GST turnover, was not declared by a taxpayer inGSTR-3B or was declared in next financial year, then the turnover computed by the system for such taxpayers couldbe less than Rs. 5 crore. Such taxpayers may have been assigned to QRMP on the basis of values declared by them inGSTR-3B. Such taxpayers are advised to opt-out of scheme for quarter Apr-Jun’21 by 30 th April 2021.

Why have I been assigned monthly frequency by system even when my aggregate turnover on PAN is upto Rs. 5crore?

At the time of assigning the frequency by the system, system considered the aggregate turnover of the taxpayer and thefiling status of FORM GSTR-3B for the month of October 2020. If the said GSTR3B was not filed till 30th November 2020,the taxpayer were assigned to monthly frequency. The system allows the taxpayer to opt for QRMP scheme only if the lastapplicable return in FORM GSTR-3B, whose due date is over, is filed.

Illustration : If the taxpayer is trying to opt for QRMP Scheme on 25th Feb’21, from Quarter Apr-Jun’21 onwards then itwill be allowed only if the return in form GSTR-3B is filed for the month Jan’21. If the taxpayer is trying to opt for QRMPScheme on 19th Feb’21, from Quarter Apr-Jun’21 onwards then it will be allowed only if the return in form GSTR-3B isfiled for the month Dec’20.

I want to opt-out of QRMP scheme and become monthly filer. Why the portal is not allowing me to do same for thequarter Jan-Mar, 2021?

The last date to choose or change the filing frequency for the quarter of January to March 2021 was 31st January, 2021.After 31st January 2021, the filing frequency cannot be changed for the quarter January to March 2021.

However, for the quarter of April to June 2021, taxpayers may change their filing frequency from quarterly to monthlyfrom 1st February, 2021 to 30 th April, 2021. It may be noted that profile selection is not a recurring requirement everyquarter. Once a frequency has been opted for, it is applicable for all future periods unless changed further.

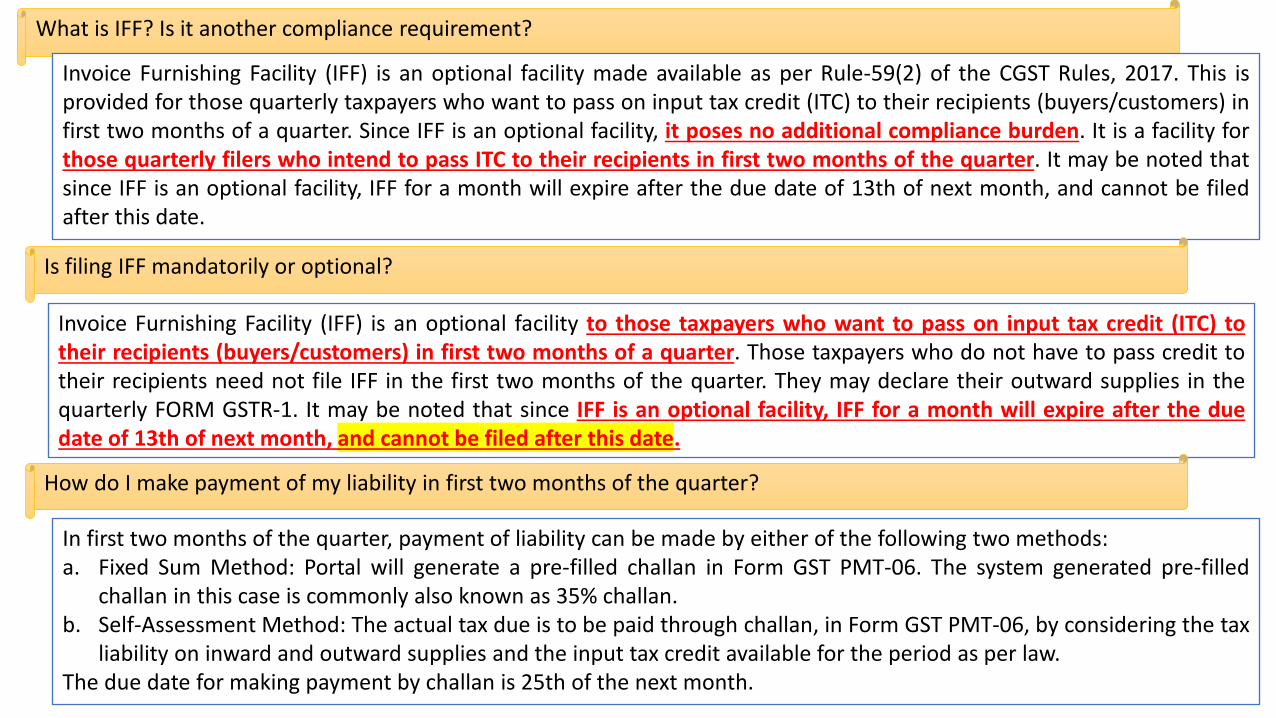

What is IFF? Is it another compliance requirement?

Invoice Furnishing Facility (IFF) is an optional facility made available as per Rule-59(2) of the CGST Rules, 2017. This isprovided for those quarterly taxpayers who want to pass on input tax credit (ITC) to their recipients (buyers/customers) infirst two months of a quarter. Since IFF is an optional facility, it poses no additional compliance burden. It is a facility forthose quarterly filers who intend to pass ITC to their recipients in first two months of the quarter. It may be noted thatsince IFF is an optional facility, IFF for a month will expire after the due date of 13th of next month, and cannot be filedafter this date.

Is filing IFF mandatorily or optional?

Invoice Furnishing Facility (IFF) is an optional facility to those taxpayers who want to pass on input tax credit (ITC) totheir recipients (buyers/customers) in first two months of a quarter. Those taxpayers who do not have to pass credit totheir recipients need not file IFF in the first two months of the quarter. They may declare their outward supplies in thequarterly FORM GSTR-1. It may be noted that since IFF is an optional facility, IFF for a month will expire after the duedate of 13th of next month, and cannot be filed after this date.

How do I make payment of my liability in first two months of the quarter?

In first two months of the quarter, payment of liability can be made by either of the following two methods:a. Fixed Sum Method: Portal will generate a pre-filled challan in Form GST PMT-06. The system generated pre-filled

challan in this case is commonly also known as 35% challan.b. Self-Assessment Method: The actual tax due is to be paid through challan, in Form GST PMT-06, by considering the tax

liability on inward and outward supplies and the input tax credit available for the period as per law.The due date for making payment by challan is 25th of the next month.

What is fixed sum method of payment?

In fixed sum method, the taxpayer is required to pay a system generated challan in the first two months of a quarter. Thesystem generated pre-filled challan in this case is commonly also known as 35% challan. If fixed sum method is opted forby the taxpayer & there is no ITC to be passed in that month, then except for paying system generated challan, no othercompliance requirement is there in the first two months of the quarter.

How is the 35% challan computed under the fixed sum method?

Under the fixed sum method, depending on the filing frequency in the previous quarter, the 35% challan is calculated by

either of the following methods:

Method (a) : An amount which is equivalent to the amount paid as tax from electronic cash ledger in their GSTR-3B return

for the last month of the immediately preceding quarter, where the GSTR-3B return was furnished on monthly basis.

OR

Method (b) : 35% of amount paid as tax from electronic cash ledger in their return for the preceding quarter, where the

GSTR-3B return was furnished on quarterly basis; or

It may be noted that since QRMP scheme is introduced in January 2021, all taxpayers were monthly filers in December

2020. Hence, the 35% challan will be populated as per method (a) for the quarter of January to March 2021 for quarterly

filers.

How do I declare B2C supplies in IFF for first two month of quarter if I have opted for QRMP?

Illustration:

Method (a) : Taxpayer paid liability by cash amounting to Rs. 5500/- [IGST: Rs. 2,000/-, CGST: Rs. 1,000/-, SGST: Rs. 2,500/-

] in monthly GSTR-3B for December 2020. The 35% challan generated as per the fixed sum method for January to March

2021 quarter will be of Rs. 5,500/- with the same head-wise break-up.

Method (b) : Taxpayer paid liability by cash amounting to Rs. 7000/- [IGST: Rs. 1,000/-, CGST: Rs. 2,000/-, SGST: Rs. 4,000/-

] in quarterly GSTR-3B for January to March 2021. The 35% challan generated as per the fixed sum method for April to

June 2021 quarter will be of Rs. 2,450/- [IGST: Rs. 350/-, CGST: Rs. 700/-, SGST: Rs. 1,400/-].

Supplies made to unregistered persons (also called B2C supplies) are not required to be declared in IFF. These may bedeclared in FORM GSTR-1 for the quarter

Taxpayers will be provided with a draft GSTR-3B, which will contain the details of the liability to be paid by taxpayers in

the quarterly GSTR-3B. This will be prepared on the basis of the supplies declared in FORM GSTR-1 for the quarter. It will

also contain data from the optional IFF, if any is filed in either of the first two months of the quarter. The said system

computed values will also be autopopulated in quarterly GSTR-3B.

How will I reconcile the values declared in IFF & GSTR-1 with quarterly GSTR-3B?

How do I claim ITC for the first two months of the quarter?

In first two months of the quarter, no declaration pertaining to ITC is required to be made. The available ITC for the entire

quarter will be made available by the system in quarterly FORM GSTR-2B. This quarterly facility will be in addition to the

FORM GSTR-2B being made available on monthly basis, which can still be used for doing self-assessment.

How do I again become a Monthly filer?

Filing frequency either monthly or quarterly can be selected as per timelines mentioned in below table.Kindly navigate : Services > Returns > Opt-in for Quarterly Return

Effective Quarter (1)

Period during which filing frequency can be selected (2)

Last date for selecting the filing frequency (3)

January–February– March# 1st November to 31st January 31st January

April – May – June 1st February to 30th April 30th April

July – August – September 1st May to 31st July 31st July

October – November – December 1st August to 31st October 31st October

# For the quarter of January to March 2021, this option was available from 5th December 2020 to 31st January2021.

How do I again become a Monthly filer?

Filing frequency either monthly or quarterly can be selected as per timelines mentioned in below table.Kindly navigate : Services > Returns > Opt-in for Quarterly Return

Effective Quarter (1)

Period during which filing frequency can be selected (2)

Last date for selecting the filing frequency (3)

January–February– March# 1st November to 31st January 31st January

April – May – June 1st February to 30th April 30th April

July – August – September 1st May to 31st July 31st July

October – November – December 1st August to 31st October 31st October

# For the quarter of January to March 2021, this option was available from 5th December 2020 to 31st January2021.

E- Invoicing

E- InvoicingNotification No. Particulars

N. N. 68/2019-CT Rule 48(4) :- E- Invoice introduced

N.N. 69/2019-CT Seeks to notify the common portal for the purpose of e-invoice.

N. N. 70/2019-CT Notify the class of registered person required to issue e-invoice.

N.N. 72/2019-CT Seeks to notify the class of registered person required to issue invoice having QR Code.

N.N. 02/2020-CT Form INV-01 substituted

N.N. 13/2020-CT Seeks to exempt certain class of registered persons from issuing e-invoices and the date for implementation of e-invoicing extended to 01.10.2020

N.N. 14/2020-CT Seeks to exempt certain class of registered persons capturing dynamic QR code and the date for implementation of QR Code to be extended to 01.10.2020.

N. N. 61/2020-CT Seeks to amend Notification no. 13/2020-Central Tax in order to amend the class of registered persons for the purpose of e-invoice.

N.N. 70/2020-CT Seeks to amend notification no. 13/2020-Central Tax dt. 21.03.2020.

N.N. 71/2020-CT Seeks to amend notification 14/2020- Central Tax to extend the date of implementation of the Dynamic QR Code for B2C invoices till 01.12.2020.

N.N. 73/2020-CT Seeks to notify a special procedure for taxpayers for issuance of e-Invoices in the period 01.10.2020 - 31.10.2020.

N.N. 88/2020-CT Seeks to implement e-invoicing for the taxpayers having aggregate turnover exceeding Rs. 100 Cr from 01st January 2021.

N.N. 89/2020-CT Seeks to waive penalty payable for noncompliance of the provisions of notification No.14/2020 – Central Tax, dated the 21st March, 2020.

E-invoicing under GST

Legal Provisions

N. N. 68/2019-CT Rule 48(4)

The invoice shall be prepared by such class of registered persons as may be notified bythe Government, on the recommendations of the Council, by including such particularscontained in FORM GST INV-01 after obtaining an Invoice Reference Number byuploading information contained therein on the Common Goods and Services TaxElectronic Portal in such manner and subject to such conditions and restrictions as maybe specified in the notification.

(5) Every invoice issued by a person to whom sub-rule (4) applies in any manner otherthan the manner specified in the said sub-rule shall not be treated as an invoice.

N. N. 61/2020-CT Registered person, whose aggregate turnover in a financial year exceeds 500 Crore w.e.f

01.10.2020

N. N. 70/2020-CTAny preceding financial year from2017-18 onwards.

N. N. 88/2020-CT Registered person, whose aggregate turnover in a financial year exceeds 100 Crore w.e.f

01.01.2021

N.N. 69/2019-CT:- Common portal for the purpose of e-invoice

(i) www.einvoice1.gst.gov.in;

(ii) www.einvoice2.gst.gov.in;

(iii) www.einvoice3.gst.gov.in;

(iv) www.einvoice4.gst.gov.in;

(v) www.einvoice5.gst.gov.in;

(vi) www.einvoice6.gst.gov.in;

(vii) www.einvoice7.gst.gov.in;

(viii)www.einvoice8.gst.gov.in;

(ix) www.einvoice9.gst.gov.in;

(x) www.einvoice10.gst.gov.in

Effective from 01.01.2020

• E Invoicing aggregate Turnover > 500 crores ----------------------------------------------------------------------------------------------01.10.2020

• Invoice Reference Number (IRN) for such invoice by uploading specified particulars

in FORM GST INV-01 within 30 days from the date of such invoice--------------------------------------------------------01.10.2020 to 31.10.2020

(N.N. 73/2020-CT)

• E Invoicing Aggregate Turnover > 100 crores ------------------------------------01.01.2021

N.N. 73/2020-CT:- Seeks to notify a special procedure for taxpayers for issuance of e-Invoices in the period 01.10.2020 - 31.10.2020.

E- Invoice Process

Taxpayer

Upload

Invoice Details

Government Invoice RegistrationPortal (IRP) managed by GSTNlaunched by the NationalInformatics Centreat einvoice1.gst.gov.in.

GSTR-1 No Manual filing

E-way Bill

Real Time Basis

❑ Post successful authentication, a unique Invoice ReferenceNumber (IRN) is generated for each invoice.

❑ Each invoice is digitally signed and added with QR code.

Exemption from E- Invoicing

An Insurer, BankingCompany, orFinancial Institutionincluding NBFC.

Goods

Transport

Agency (GTA).

Passenger

Transport Service.

Admission to the

exhibition of

Cinematograph

Films in Multiplex

Screens ie. PVR.

SEZ UNIT (SEZ

DEVELOPER is not

exempted)

N.N. 13/2020-CT

N.N. 61/2020-CT

E- Invoice Process

Documents Covered by E- Invoice System

Invoice Credit Note Debit Note

‘e-invoicing’ is not generation of invoice by a Government portal. Taxpayers will continue to create their GST invoices on their own

Accounting/Billing/ERP Systems.

These invoices will now be reported to ‘Invoice Registration Portal (IRP)’.

On reporting, IRP will generate a unique ‘Invoice Reference Number (IRN)’, digitally sign it and return the e-invoice. A GST

invoice will be valid only with a valid IRN.

IRP will also generate a QR code containing the unique IRN along with certain other key particulars. The QR code (which can

be printed on invoice) enables offline verification of the fact whether the e-invoice has been reported on the IRP or not (using

Mobile App etc.)

E- Invoicing Process

Supplier with PAN basedaggregate turnover inpreceding F.Y. > 100 Crore

Buyer

Issues Invoice with QR Code

IRPInvoice registration portal

• Performs prescribed validations• No storage/ archival

IRP 2 will be added soon

E-way bill System(Auto population of E-wayBill (Where required)

IRN Lookup System(To Check and rule outexistence of some IRN)

Auto population of invoicedetails into GSTR-1/2A

Search IRN facility on GSTPortal (To verifyauthenticity of IRN)

Modes of generation of E- Invoice

API Based (Integrationwith tax payer systemdirectly)(e.g Tally)

API Based (Integration with tax payer system throughGSP/ASP) (e.g an offline utility like spreadsheetwhere taxpayers could fill out their invoices and thenupload on GST portal.) (Approved GSP examples- TCSltd., Tally solutions Pvt. Ltd., Taxmann PubliactionsPvt. Ltd. Etc)

‘Free Offline Utility (Bulkgeneration Tool’,downloadable from IRP)

Web Based/ mobile based modes will also be provided in future.

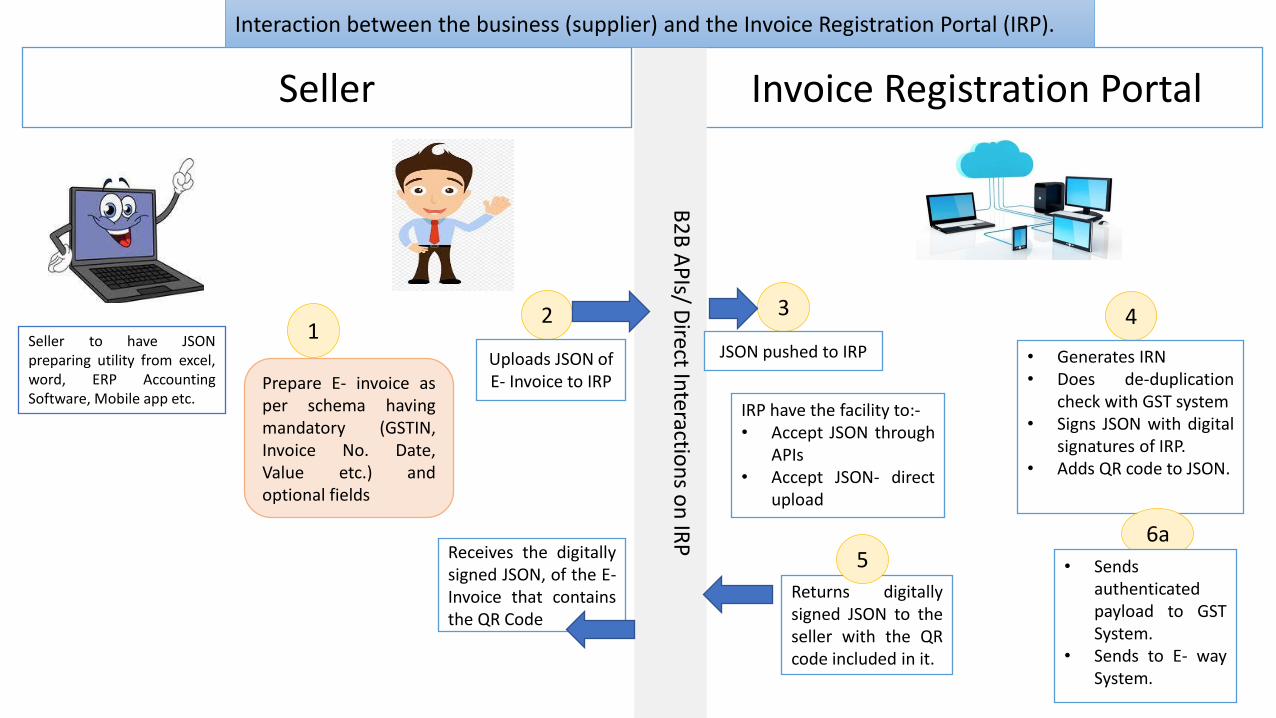

E-invoice – Detailed Work flow

Seller

• Uploads E- invoice

(Containing GSTIN,

Invoice Number, Date,

Value etc.

• Receives digitally signed

JSON of E- Invoice that

contains the QR Code.

• Sellers GSTR-1 gets

updated with liability

entered in invoice.

Invoice Registration Portal

• Signs the invoice.

• Adds a QR to the JSON.

• Sends back signed JSON

to buyer.

• Sends the invoice to

GST System.

GST System

• Updates outward and

inward supplies for

buyer and seller.

• Now has unique invoice

with unique number.

Buyer

• Buyer can view the

ITC related to the

invoice in GSTR-2A.

B2B APIs

APIs

Seller

Seller to have JSONpreparing utility from excel,word, ERP AccountingSoftware, Mobile app etc.

1

Prepare E- invoice asper schema havingmandatory (GSTIN,Invoice No. Date,Value etc.) andoptional fields

2

Uploads JSON of E- Invoice to IRP

Receives the digitallysigned JSON, of the E-Invoice that containsthe QR Code

Invoice Registration Portal

3

B2

B A

PIs/ D

irect Interactio

ns o

n IR

P

JSON pushed to IRP

IRP have the facility to:-• Accept JSON through

APIs• Accept JSON- direct

upload

Returns digitallysigned JSON to theseller with the QRcode included in it.

4

5

• Generates IRN• Does de-duplication

check with GST system• Signs JSON with digital

signatures of IRP.• Adds QR code to JSON.

6a

• Sendsauthenticatedpayload to GSTSystem.

• Sends to E- waySystem.

Interaction between the business (supplier) and the Invoice Registration Portal (IRP).

Invoice Registration Portal

3

JSON pushed to IRP

IRP have the facility to:-• Accept JSON through

APIs• Accept JSON- direct

upload

Returns digitallysigned JSON to theseller with the QRcode included in it.

4

5

• Generates IRN• Does de-duplication

check with GST system• Signs JSON with digital

signatures of IRP.• Adds QR code to JSON.

6a

• Sendsauthenticatedpayload to GSTSystem.

• Sends to E- waySystem.

Interaction between the IRP and the GST/E-Way Bill Systems and the Buyer.

GST System

B2

B A

PIs/ D

irect Interactio

ns o

n IR

P

• Invoice informationstored in GST invoiceregistry.

• De- duplicationchecked.

4a

6b

• GST system now hasunique invoice withunique number.

• GSTR-1 of sellerupdated.

• GSTR-2A of buyerupdated.

Buyer

• Buyer can use the QRcode to verify theinvoice.

• Buyer can view the ITCrelated to the invoicein his GSTR-2A

• E-way bill system willcreate the E-way Bill.

6c

Cancellation/Amendment of Reported Invoice:

The seller can initiate cancellation of IRN of the e-invoice already reported, if that invoice is required to be cancelled by him/her. The

cancellation of an invoice will be done as per procedure given under accounting standards. The cancellation will be allowed within

specified time after generation of IRN.

The cancellation of e-invoice will be done by using the ‘Cancel IRN’ API (published on the e-invoice sandbox portal). The API will be a

POST API and will require the IRN that is to be cancelled as the key parameter of the payload.

The invoice number of cancelled invoice can’t be used again.

Amendment of e-invoice already uploaded on IRP will be done only on GST portal.

Any amended e-invoice, if reported to IRP, will get rejected as its IRN (unique hash) will already be existing in the IRP system. Hence,

amendment of invoices will not be possible through the IRP.

Advantages of E- Invoice

Advantages

Elimination of Fake invoices

One Time reporting

Helpful in GSTReturn preparation

Helpful in E- WayBill preparation

Trigger Point of Entire Automated Process

FAQ’s

For which businesses, e-invoicing is mandatory ?

For Registered persons whose aggregate turnover (based on PAN) in any preceding financial year from 2017-18 onwards, is more than

prescribed limit (as per relevant notification), e-invoicing is mandatory.

What supplies are presently covered under e-invoice?

• Supplies to registered persons (B2B),

• Supplies to SEZs (with/without payment),

• Exports (with/without payment),

• Deemed Exports,

by notified class of taxpayers are currently covered under e-invoicing.

B2C (Business to Consumer) supplies can also be reported by notified persons?

No. Reporting B2C invoices by notified persons is not applicable/allowed currently. However, they will be brought under e-invoice in the next

phase.

Is e-invoicing applicable for NIL-rated or wholly-exempt supplies?

No. In those cases, a bill of supply is issued and not a tax invoice.

Whether the financial/commercial credit notes also need to be reported to IRP?

No, only the credit and debit notes issued under Section 34 of CGST/SGST Act have to be reported.

Whether e-invoicing is applicable for invoices between two different GSTINs under same PAN?

Yes. e-invoicing by notified persons is mandated for supply of goods or services or both to a registered person.

As per Section 25(4) of CGST/SGST Act, “A person who has obtained or is required to obtain more than one registration, whether in one State

or Union territory or more than one State or Union territory shall, in respect of each such registration, be treated as distinct persons for the

purposes of this Act.”

Do SEZ Developers need to issue e-invoices?

Yes, if they have the specified turnover and fulfilling other conditions of the notification.

In terms of Notification (Central Tax) 61/2020 dt. 30-7-2020, only SEZ Units are exempted from issuing e-invoices.

Are Free Trade & Warehousing Zones (FTWZ) exempt from e-invoicing?

Yes. As per Foreign Trade Policy, Free Trade & Warehousing Zones (FTWZ) are only a special category of Special Economic Zones, with a focus

on trading and warehousing.

Is e-invoicing applicable for supplies by notified persons to SEZs?

Yes, e-invoicing is applicable for supplies by notified persons to SEZs.

In terms of Notification (Central Tax) 61/2020 dt. 30-7-2020, only SEZ Units are exempt from issuing e-invoices.

• There is an SEZ unit and a regular DTA unit under same legal entity (i.e. having same PAN).

• The aggregate total turnover of the legal entity is more than Rs. 100 Crores (considering both the GSTINs). However, the turnover of

DTA unit is below Rs. 100 crores for FY 19-20.

• In this scenario, as SEZ unit is exempt from e-invoicing, whether e-invoicing will be applicable to DTA Unit?

Yes, because the aggregate turnover of the legal entity in this case is > Rs. 100 Crores. The eligibility is based on aggregate annual

turnover on the common PAN.

Is e-invoicing applicable to invoices issued by Input Service Distributor (ISD)? No

Whether e-invoicing is applicable for supplies involving Reverse Charge?

If the invoice issued by notified person is in respect of supplies made by him but attracting reverse charge under Section 9(3), e-invoicing is

applicable.

For example, a taxpayer (say, a Firm of Advocates having aggregate turnover in a FY is more than Rs. 100 Cr.) is supplying services to a

company (who will be discharging tax liability as recipient under RCM), such invoices have to be reported by the notified person to IRP.

On the other hand, where supplies are received by notified person from (i) an unregistered person (attracting reverse charge under Section

9(4)) or (ii) through import of services, e-invoicing doesn’t arise / not applicable.

How to know a particular supplier is supposed to issue e-invoice (i.e. invoice along with IRN/QR Code)?

On fulfilment of prescribed conditions, the obligation to issue e-invoice in terms of Rule 48(4) (i.e. reporting invoice details to IRP,

obtaining IRN and issuing invoice with QR Code) lies with concerned taxpayer.

However, as a facilitation measure, all the taxpayers who had crossed the prescribed turnover in a financial year from 2017-18 onwards

have been enabled to report invoices to IRP.

One can search the status of enablement of a GSTIN on e-invoice portal: https://einvoice1.gst.gov.in/ > Search > e-invoice status of

taxpayer

This listing of GSTINs is solely based on the turnover of GSTR-3B as reported to GST System. It may contain exempt entities or those

for whom e-invoicing is not applicable for some other reason. So, it may be noted that enablement status on e-invoice portal

doesn’t mean that the taxpayer is supposed to do e-invoicing. If e-invoicing is not applicable to a taxpayer, they need not be

concerned about the enablement status and may ignore it.

Further, the turnover slab of taxpayer can also be ascertained through “Search Taxpayer” / “Know Your Supplier” Sections on GST

portal also.

In case any registered person, is required to prepare invoice in terms of Rule 48(4) but not enabled on the portal, he/she may request

for enablement on portal: ‘Registration -> e-Invoice Enablement’.

In the current schema, there is no provision to report details of supplies not covered under GST, e.g. a hotel wants to give single invoice for a B2B supply where the supply includes food and beverages (leviable to GST) and Alcoholic beverages (outside GST).

For items outside GST levy, separate invoice may be given by such businesses.

In case of Credit Note and Debit Note, is there any validation w.r.t referred invoice number?

No linkage with invoice is built, in view of the amended provisions of GST.