Regulatory and Supervisory Framework

Susanta Kumar DasFebruary 27, 2017

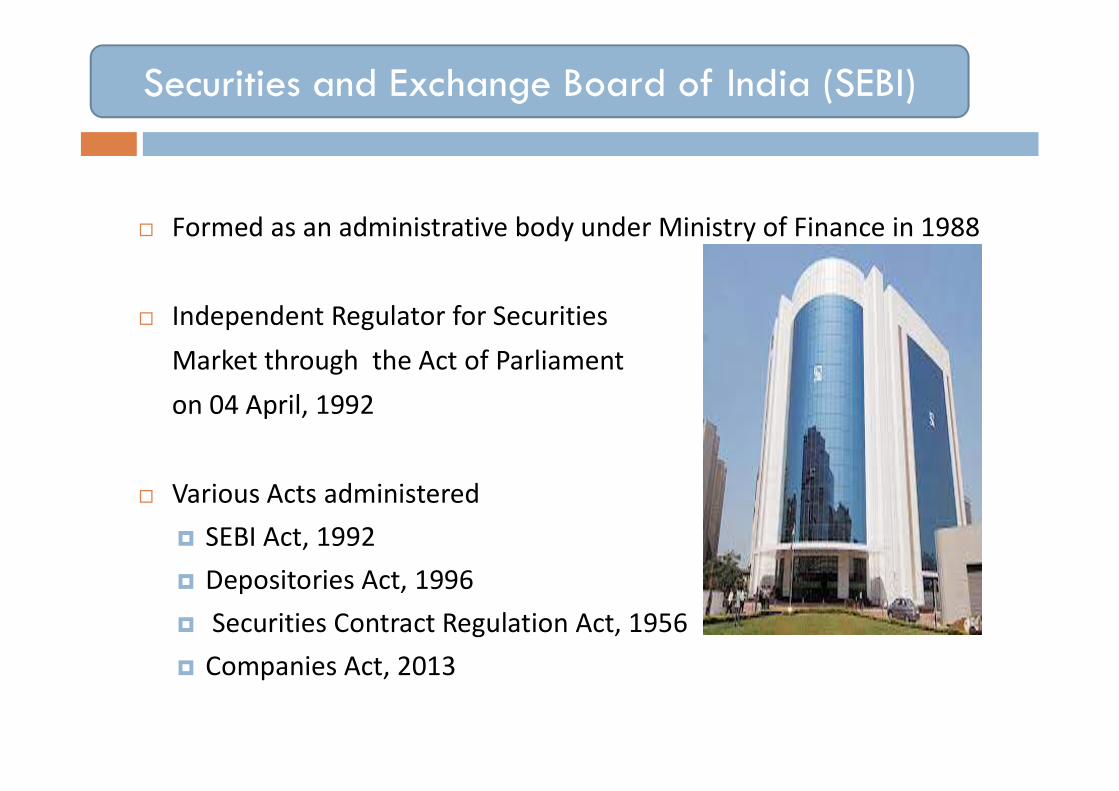

Securities and Exchange Board of India (SEBI)

Formed as an administrative body under Ministry of Finance in 1988

Independent Regulator for SecuritiesMarket through the Act of Parliamenton 04 April, 1992

Various Acts administered SEBI Act, 1992 Depositories Act, 1996 Securities Contract Regulation Act, 1956 Companies Act, 2013

Preamble to SEBI Act, 1992

Investor protection

Regulation of securities market

Development of securities market

Key Market Players

4

Securities Market

Corporates

Regulator

Registrar

Merchant Bankers

Stock Exchanges

Broking & Research

House

Investors Retail &

Institutional

Key Market Players

5

Participants Numbers

Stock Exchanges 3

Registered Brokers 3200

Registered Sub-Brokers 32000

Mutual Funds 51

Depositories 2

Depository Participants 853

Clearing Corporations 3

Key Statistics

6

NSE BSE

No. of Listed Companies 1847 5102

Market Capitalization (USD in billion) (As on 31.01.2017)

1625 1655

Average daily turnover (Cash during January, 2017) (USD in billion)

3.28 0.45

Turnover (F&O during January, 2017) (USD in billion)

58.16 -

No. of Trades (Cash segment- in million) as on February 21, 2017

7.8 1.5

MARKET REGULATION DEPARTMENT

Market Regulation Department

Division of Risk Management and New Products Division of Self Regulatory Organisations (SRO) Administration-

Registration, recognition and administration of depositories and stock exchanges

Division of Market Supervision – Inspection of MIIs Investor Complaints Cell Division of Policy

Slide 8

Corporate Bond Market

Slide 9

Statistics on corporate bond market for primary issuances

Slide 10

0

500

1000

1500

2000

2500

3000

3500

0

10000

20000

30000

40000

50000

60000

70000

80000

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

in U

SD m

illio

n

Year

Statistics on Private Placement

Amount Raised through Private Placement (USDmillion)

No. of Pvt. Placement

0

5

10

15

20

25

30

35

40

0

1000

2000

3000

4000

5000

6000

7000

in U

SD m

illio

n

Year

Statistics on Public Issues

Amount Raised through Public Issue (USDmillion)

No. of Public Issues

Statistics on corporate bond market for primary issuances

Slide 11

17424

25703

3163833564

43661

55654

46829

60860

7233674403

0

10000

20000

30000

40000

50000

60000

70000

80000

2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17

in U

SD m

illio

n

Year

Total Amount Raised through Public Issue and Pvt. Placement (USD million)

Total Amount Raised through Public Issue and Pvt. Placement (USD million)

Corporate Bond Share in Total outstanding Debt

Slide 12

71.8% 69.7% 69.5% 66.8% 65.5%

9.4% 10.7% 11.1%12.1% 12.1%

18.7% 19.6% 19.3% 21.1% 22.4%

0%

20%

40%

60%

80%

100%

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16

Bank Credit External commercial borrowings Corporate bonds and commercial papers

Corporate Bond Share in Incremental lending

Slide 13

64.6%56.9%

68.6%

45.7%52.8%

17.7%

18.1%

14.1%

19.5%12.3%

17.7%25.0%

17.3%

34.8% 34.9%

0%

20%

40%

60%

80%

100%

Mar-12 Mar-13 Mar-14 Mar-15 Mar-16

Bank Credit External commercial borrowings Corporate bonds and commercial papers

Investment in Different Category of Corporate Bond

Slide 14

0%

10%

20%

30%

40%

50%

60%

70%

80%

2011-12 2012-13 2012-13 2013-14 2014-15 2015-16 2016-17 (Sept 16)

Investment in Different Category of Corporate Bond

AAA AA+ AA AA- & Below Not Rated

Features of Corporate Bond Market

Dominated by private placements; Limited investor base; Small outstanding stock of Individual issuances; Structural incentives for borrowers to prefer bank financing

Slide 15

Recent measures to develop bond market

Market making scheme to improve market liquidity; Electronic auction platform for transparent private placements; Integrated trade repository; Introduction of corporate bond index; Credit enhancement for corporate bonds; Enhancing Credit Supply for Large Borrowers through Market

Mechanism Enactment of Bankruptcy Code

Slide 16

Measures which are in the pipeline

Repo in Corporate bonds; Rationalization of investment restrictions; Consolidation and re-issuance of corporate bonds

Slide 17

Securities Lending and Borrowing Mechanism

Slide 18

SLB- Concept

Temporary loan between lender and borrower Securitites are transferred from the borrower to the lender for a

fee. Borrower has to return the securities either on demand or at the

end of agreed term or has an option to early return Lender may recall securities at any time Promotes market efficiency and liquidity Lenders’ motivation- incremental return on an idle portfolio Borrowers’ motivation- to cover a short position- avoid settlement

failures Hedging of futures and option position

19

Participants

Lender Insurance Companies Banks HNIs Mutual Funds Retail Investors

Borrowers Borrowers Short term sellers especially long term shorts Cash and derivative arbitragers Market makers Retail Investors 20

Salient features

Automated screen based trading platform with online matching of trades based on price-time priority

Contracts upto 1 year (12 monthly contracts) Early return and recall Settlement guarantee with clearing corporations acting as Central

Counterparties (CCP).

21

Reasons for low liquidity

Borrower driven- presence of very few lenders; PF Funds are not allowed to participate; Client level position of 1% is too small especially for institutional

investors; Absence of OTC SLB market; Risk of not procuring the security lent, on early recall.

22

Thank You

23

Recommended