RESERVE FUND STUDY

METROPOLITAN TORONTO CONDOMINIUM CORPORATION No. XXX LOCATED AT: 123 XXX street, TORONTO, ONTARIO

Your condo picture here

JBCS CANADA INC. PROJECT NUMBER: 8XXXX REPORT DATE: Jan 2013 VERSION: 1.0

1

CONTENTS SECTION 1. EXECUTIVE SUMMARY 2. INTRODUCTION 3. GENERAL INFORMATION 4. RESERVE FUND STUDY PURPOSE 5. ACKNOWLEDGEMENTS AND ASSEMBLY OF THE REPORT 6. DOCUMENTATION 7. THE PHYSICAL ANALYSIS 8. THE FINANCIAL ANALYSIS

APPENDICES A. TABLE 1 - REPLACEMENT COST SUMMARY B. TABLE 2 - ANNUAL OUTLAY (30 YEARS) C. TABLE 3A - CASH FLOW (OPTION 1) D. TABLE 3B - CASH FLOW (OPTION 2) E. TABLE 3C - CASH FLOW (OPTION 3) F. PHOTOGRAPH COMPENDIUM G. Deficiency Schedule H. EXCERPT FROM THE CONDOMINIUM ACT (1998)

2

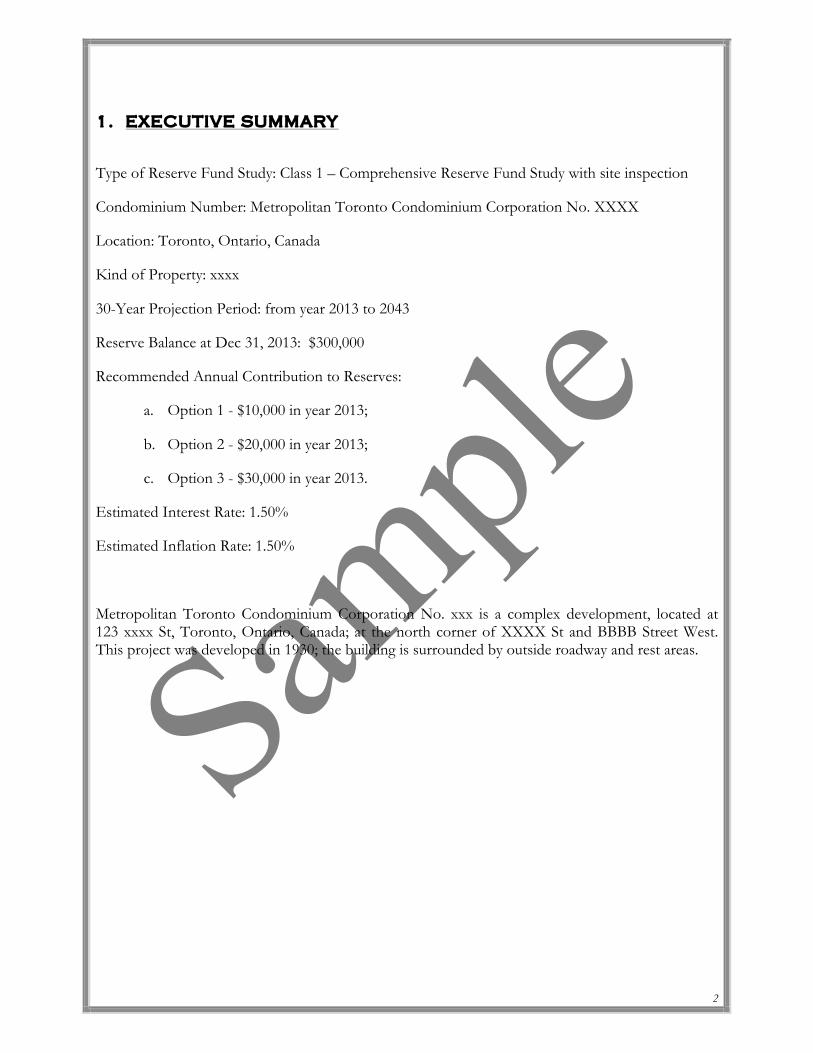

1. EXECUTIVE SUMMARY

Type of Reserve Fund Study: Class 1 – Comprehensive Reserve Fund Study with site inspection

Condominium Number: Metropolitan Toronto Condominium Corporation No. XXXX

Location: Toronto, Ontario, Canada

Kind of Property: xxxx

30-Year Projection Period: from year 2013 to 2043

Reserve Balance at Dec 31, 2013: $300,000

Recommended Annual Contribution to Reserves:

a. Option 1 - $10,000 in year 2013;

b. Option 2 - $20,000 in year 2013;

c. Option 3 - $30,000 in year 2013.

Estimated Interest Rate: 1.50%

Estimated Inflation Rate: 1.50%

Metropolitan Toronto Condominium Corporation No. xxx is a complex development, located at 123 xxxx St, Toronto, Ontario, Canada; at the north corner of XXXX St and BBBB Street West. This project was developed in 1930; the building is surrounded by outside roadway and rest areas.

3

2. INTRODUCTION This document has been provided pursuant to an agreement containing restrictions on its use. No part of this document may be copied or distributed, in any form or by any means, nor disclosed to third parties without the expressed written permission of JBCS Canada Inc. The client shall have the right to reproduce and distribute copies of this report, or the information contained within, as may be required for compliance with all applicable regulations.

JBCS Canada Inc. is an independent consulting firm and it is not under any subsidiary of any company. All of our associates, consultants and employees are not in and related to any of the condominiums board of directors and unit owner.

This reserve analysis study and the parameters under which it has been completed are based upon information provided to us in part by representatives of the condominium, its contractors, assorted vendors, specialist and independent contractors. And various construction pricing and scheduling manuals including, but not limited to: Marshall & Swift Valuation Service, RS Means Facilities Maintenance & Repair Cost Data, RS Means Repair & Remodeling Cost Data, National Construction Estimator, National Repair & Remodel Estimator, Dodge Cost Manual and McGraw-Hill Professional. Additionally, costs are obtained from numerous vendor catalogues, actual quotations or historical costs, and our own experience in the field of property management and reserve study preparation.

It has been assumed, unless otherwise noted in this report, that all assets have been designed and constructed properly and that each estimated useful life will approximate that of the norm per industry standards and/or manufacturer’s specifications. In some cases, estimates may have been used on assets, which have an indeterminable but potential liability to the condominium. The decision for the inclusion of these as well as all assets considered is left to the client.

We recommend that your reserve analysis study be updated on every single year basis (maximum three years) due to fluctuating interest rates, inflationary changes, and the unpredictable nature of the lives of many of the assets under consideration. All of the information collected during our inspection of the condominium and computations made subsequently in preparing this reserve analysis study are retained in our computer files. Therefore, annual updates may be completed quickly and inexpensively each year.

JBCS Canada Inc. would like to thank you for using our services. We invite you to call us at any time, should you have questions, comments or need assistance. In addition, any of the parameters and estimates used in this study may be changed at your request, after which we will provide a revised study.

This reserve analysis study is provided as an aid for planning purposes and not as an accounting tool. Since it deals with events yet to take place, there is no assurance that the results enumerated within it will, in fact, occur as described.

Preparing the annual budget and overseeing the condominium’s finances are perhaps the most

4

important responsibilities of board members. The annual operating and reserve budgets reflect the planning and goals of the condominium and set the level and quality of service for all of the condominium’s activities.

Funding Options

When a major repair or replacement is required in a community, the condominium has essentially four options available to address the expenditure:

The first, and only logical means that the Board of Directors has to ensure its ability to maintain the assets for which it is obligated, is by assessing an adequate level of reserves as part of the regular membership assessment, thereby distributing the cost of the replacements uniformly over the entire membership. The condominium is not only comprised of present members, but also future members. Any decision by the Board of Directors to adopt a calculation method or funding plan which would disproportionately burden future members in order to make up for past reserve deficits, would be a breach of its fiduciary responsibility to those future members. Unlike individuals determining their own course of action, the board is responsible to the “condominium” as a whole.

Whereas, if the condominium was setting aside reserves for this purpose, using the vehicle of the regularly assessed membership dues, it would have had the full term of the life of the roof, for example, to accumulate the necessary moneys. Additionally, those contributions would have been evenly distributed over the entire membership and would have earned interest as part of that contribution.

The second option is for the condominium to acquire a loan from a lending institution in order to affect the required repairs. In many cases, banks will lend to a condominium using “future homeowner assessments” as collateral for the loan. With this method, the current board is pledging the future assets of the condominium. They are also incurring the additional expense of interest fees along with the original principal amount. For example, in the case of a $300,000 roofing replacement, the condominium may be required to pay back the loan over a three to five year period, with interest.

The third option, too often used, is simply to defer the required repair or replacement. This option, which is not recommended, can create an environment of declining property values due to expanding lists of deferred maintenance items and the condominium’s financial inability to keep pace with the normal aging process of the common area components. This, in turn, can have a seriously negative impact on sellers in the condominium by making it difficult, or even impossible, for potential buyers to obtain financing from lenders. Increasingly, lending institutions are requesting copies of the condominium’s most recent reserve study before granting loans, either for the condominium itself, a prospective purchaser, or for an individual within such the condominium.

The fourth option is to pass a “special assessment” to the membership in an amount required to cover the expenditure. When a special assessment is passed, the condominium has the authority and responsibility to collect the assessments, even by means of foreclosure, if necessary. However, the condominium considering a special assessment cannot guarantee that an assessment, when needed, will be passed. Consequently, the condominium cannot guarantee its ability to perform the required repairs or replacements to those major components for which it is obligated when the need arises. Additionally, while relatively new condominium require very little in the way of major “reserve”

5

expenditures, associations reaching fifteen or more years of age and older, find many components reaching the end of their effective useful lives. These required expenditures, all accruing at the same time, could be devastating to a condominium’s overall budget.

Types of Reserve Fund Studies

Most reserve fund studies fit into one of three categories:

Level 1 - Comprehensive Reserve Fund Study;

Level 2 - Update with site inspection; and

Level 3 - Update without site inspection.

In a Comprehensive Reserve Fund Study, the reserve provider conducts a component inventory, a condition assessment (based upon on-site visual observations), and life and valuation estimates to determine both a “fund status” and “funding plan”.

In an Update with site inspection, the reserve provider conducts a component inventory (verification only, not quantification unless new components have been added to the inventory), a condition assessment (based upon on-site visual observations), and life and valuation estimates to determine both the “fund status” and “funding plan.”

In an Update without site inspection, the reserve provider conducts life and valuation estimates to determine the “fund status” and “funding plan.”

6

There are two components of a reserve fund study: a physical analysis and a financial analysis.

Physical Analysis

During the physical analysis, a reserve fund study provider evaluates information regarding the physical status and repair/replacement cost of the association’s major common area components. To do so, the provider conducts a component inventory, a condition assessment, and life and valuation estimates.

Developing a Component List

The budget process begins with full inventory of all the major components for which the condominium is responsible. The determination of whether an expense should be labeled as operational, reserve, or excluded altogether is sometimes subjective. Since this labeling may have a major impact on the financial plans of the condominium, subjective determinations should be minimized. We suggest the following considerations when labeling an expense.

Operational Expenses

Occur at least annually, no matter how large the expense, and can be budgeted for effectively each year. They are characterized as being reasonably predictable, both in terms of frequency and cost. Operational expenses include all minor expenses, which would not otherwise adversely affect an operational budget from one year to the next. Examples of operational expenses include:

Utilities:

Electricity

Gas

Water

Telephone

Cable TV

Administrative:

Supplies

Bank Service Charges

Dues & Publications

Licenses, Permits & Fees

Insurance(s)

Services:

Landscaping

Pool Maintenance

Street Sweeping

Accounting

7

Reserve Expenses

These are major expenses that occur other than annually, and which must be budgeted for in advance in order to ensure the availability of the necessary funds in time for their use. Reserve expenses are reasonably predictable both in terms of frequency and cost. However, they may include significant assets that have an indeterminable but potential liability that may be demonstrated as a likely occurrence. They are expenses that, when incurred, would have a significant effect on the smooth operation of the budgetary process from one year to the next, if they were not reserved for in advance. Examples of reserve expenses include:

SITE WORKS HARD LANDSCAPING Roadways / Driveways Curbs Patios Pedestrian Walks Fencing Site / Street Furnishings Exterior Signage Mail Box System SOFT LANDSCAPING Trees AMENITIES (excludes Recreation Centres) Tennis Courts Playground Structures (play area) Pools Gazebos Utility Sheds

STRUCTURE BUILDINGS Foundations Sub-Structures Superstructures Stairs SITE Stairs Handrails & Guards Retaining Walls Decks SLAB / DECKS Structural Systems Guards / Railings / Dividers Waterproofing Systems PARKING GARAGES Structural Systems Intermediate Slab Waterproofing Systems Roof Slab Waterproofing Systems Ramps

8

BUILDING ENVELOPE WALLS Cladding Other COATINGS Painting DOORS Entrance Doors Service Doors Balcony / Patio Doors Overhead Doors WINDOWS Windows Glazing MEMBRANES & SEALANTS Cladding Joints Caulking to Windows and Doors ROOFING / TERRACES Sloped Roofing Flat Roofing Flashings Hatches Skylights Eaves troughs & Downspouts Soffits & Fascia

MECHANICAL SYSTEMS SITE SYSTEMS Irrigation - Sprinklers Domestic Water Main DRAINAGE SYSTEMS Sanitary Drainage Systems Storm Drainage Systems Pumps DOMESTIC WATER SYSTEMS Boilers Hot Water Storage Tanks Circulating & Booster Pumps Domestic Water System (Hot & Cold) Domestic Hot Water Recirculation System Domestic Hot Water Booster Pump Domestic Hot Water Circulation Pumps Domestic Hot Water Heater Exchanger Water Softeners Plumbing Fixtures Insulation HEATING SYSTEMS Boilers Circulating Pumps Unit Heaters

9

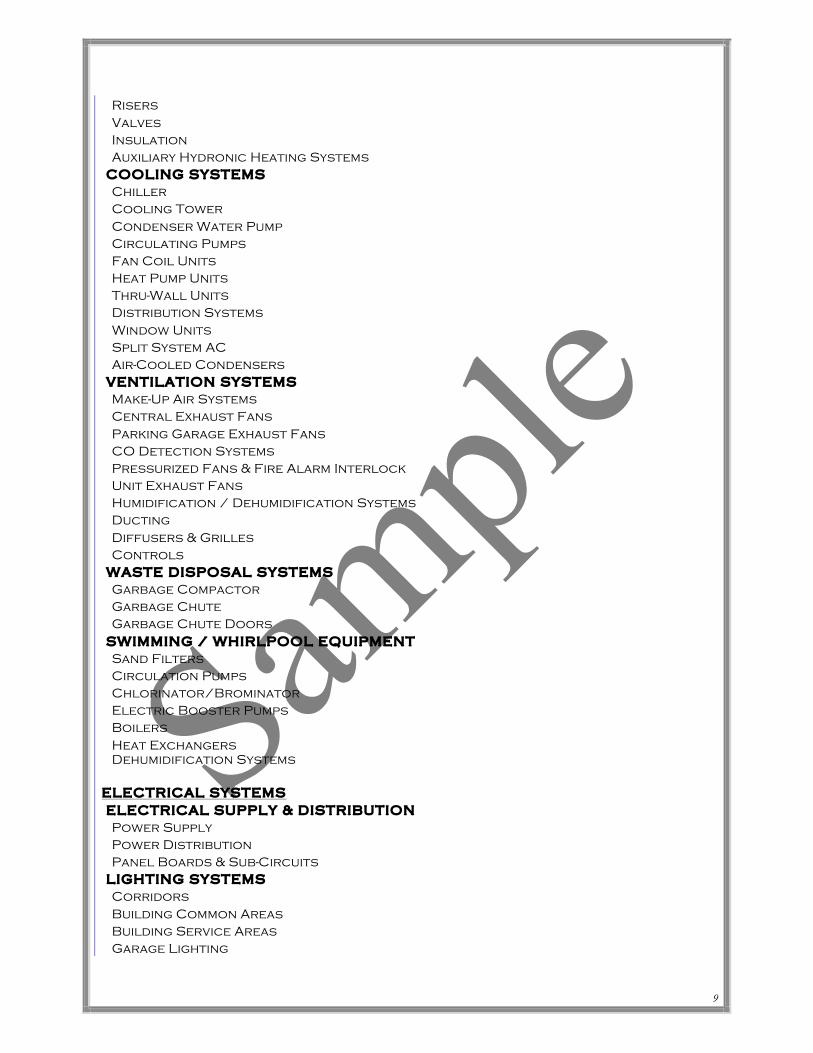

Risers Valves Insulation Auxiliary Hydronic Heating Systems COOLING SYSTEMS Chiller Cooling Tower Condenser Water Pump Circulating Pumps Fan Coil Units Heat Pump Units Thru-Wall Units Distribution Systems Window Units Split System AC Air-Cooled Condensers VENTILATION SYSTEMS Make-Up Air Systems Central Exhaust Fans Parking Garage Exhaust Fans CO Detection Systems Pressurized Fans & Fire Alarm Interlock Unit Exhaust Fans Humidification / Dehumidification Systems Ducting Diffusers & Grilles Controls WASTE DISPOSAL SYSTEMS Garbage Compactor Garbage Chute Garbage Chute Doors SWIMMING / WHIRLPOOL EQUIPMENT Sand Filters Circulation Pumps Chlorinator/Brominator Electric Booster Pumps Boilers Heat Exchangers Dehumidification Systems

ELECTRICAL SYSTEMS ELECTRICAL SUPPLY & DISTRIBUTION Power Supply Power Distribution Panel Boards & Sub-Circuits LIGHTING SYSTEMS Corridors Building Common Areas Building Service Areas Garage Lighting

10

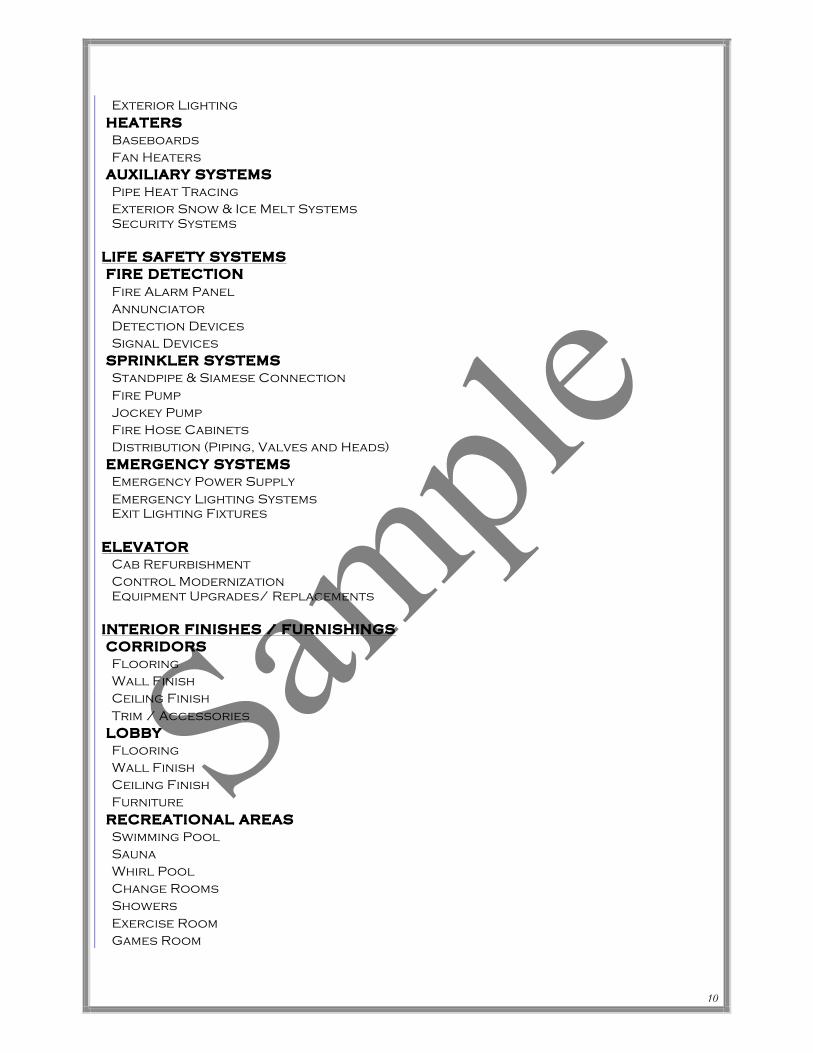

Exterior Lighting HEATERS Baseboards Fan Heaters AUXILIARY SYSTEMS Pipe Heat Tracing Exterior Snow & Ice Melt Systems Security Systems

LIFE SAFETY SYSTEMS FIRE DETECTION Fire Alarm Panel Annunciator Detection Devices Signal Devices SPRINKLER SYSTEMS Standpipe & Siamese Connection Fire Pump Jockey Pump Fire Hose Cabinets Distribution (Piping, Valves and Heads) EMERGENCY SYSTEMS Emergency Power Supply Emergency Lighting Systems Exit Lighting Fixtures

ELEVATOR Cab Refurbishment Control Modernization Equipment Upgrades/ Replacements

INTERIOR FINISHES / FURNISHINGS CORRIDORS Flooring Wall Finish Ceiling Finish Trim / Accessories LOBBY Flooring Wall Finish Ceiling Finish Furniture RECREATIONAL AREAS Swimming Pool Sauna Whirl Pool Change Rooms Showers Exercise Room Games Room

11

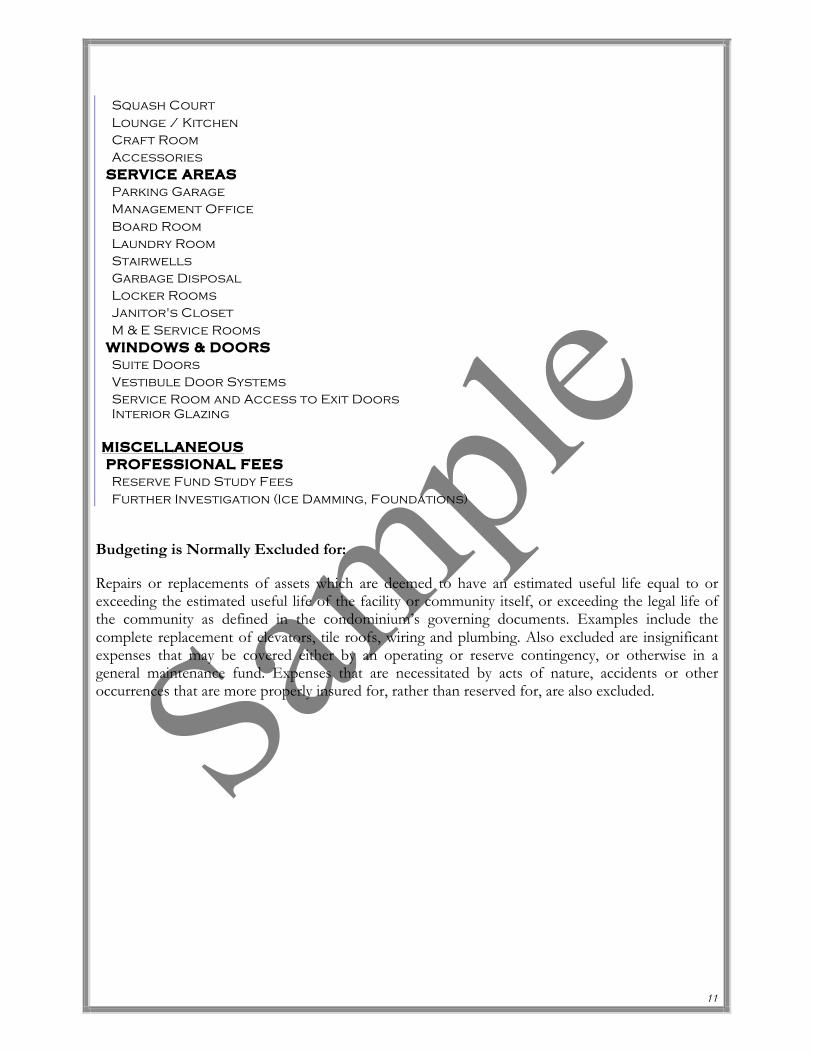

Squash Court Lounge / Kitchen Craft Room Accessories SERVICE AREAS Parking Garage Management Office Board Room Laundry Room Stairwells Garbage Disposal Locker Rooms Janitor's Closet M & E Service Rooms WINDOWS & DOORS Suite Doors Vestibule Door Systems Service Room and Access to Exit Doors Interior Glazing

MISCELLANEOUS PROFESSIONAL FEES Reserve Fund Study Fees Further Investigation (Ice Damming, Foundations)

Budgeting is Normally Excluded for:

Repairs or replacements of assets which are deemed to have an estimated useful life equal to or exceeding the estimated useful life of the facility or community itself, or exceeding the legal life of the community as defined in the condominium’s governing documents. Examples include the complete replacement of elevators, tile roofs, wiring and plumbing. Also excluded are insignificant expenses that may be covered either by an operating or reserve contingency, or otherwise in a general maintenance fund. Expenses that are necessitated by acts of nature, accidents or other occurrences that are more properly insured for, rather than reserved for, are also excluded.

12

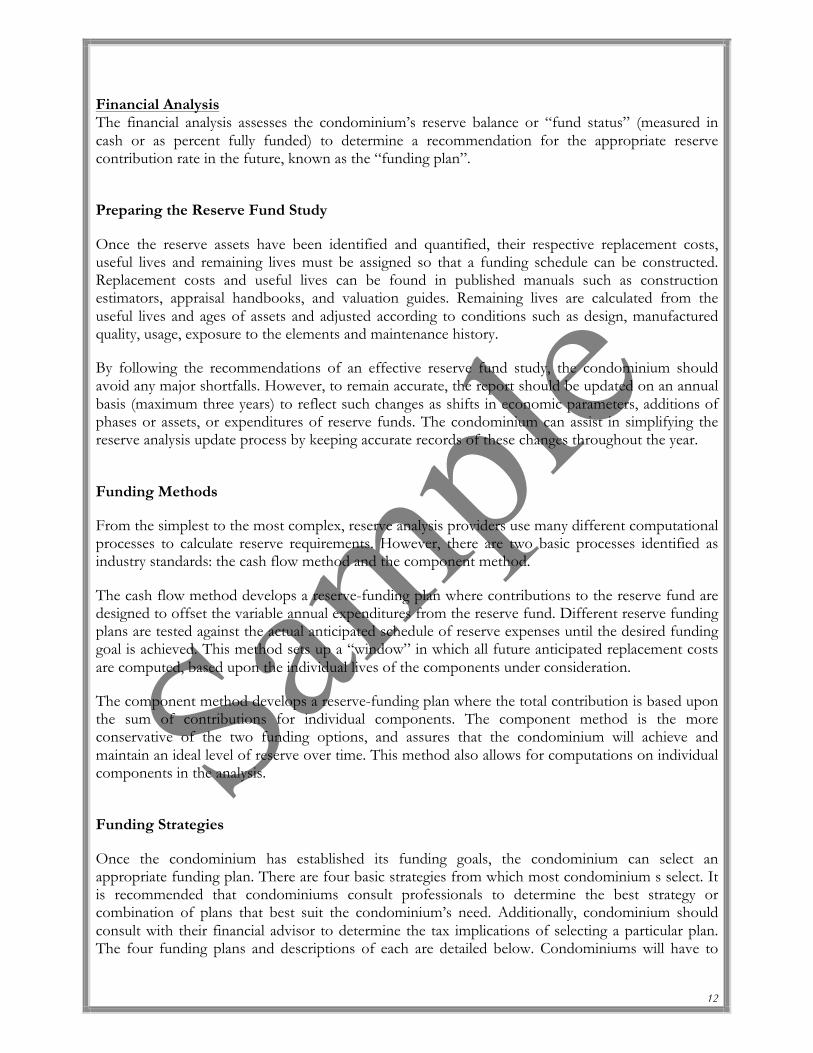

Financial Analysis The financial analysis assesses the condominium’s reserve balance or “fund status” (measured in cash or as percent fully funded) to determine a recommendation for the appropriate reserve contribution rate in the future, known as the “funding plan”.

Preparing the Reserve Fund Study

Once the reserve assets have been identified and quantified, their respective replacement costs, useful lives and remaining lives must be assigned so that a funding schedule can be constructed. Replacement costs and useful lives can be found in published manuals such as construction estimators, appraisal handbooks, and valuation guides. Remaining lives are calculated from the useful lives and ages of assets and adjusted according to conditions such as design, manufactured quality, usage, exposure to the elements and maintenance history.

By following the recommendations of an effective reserve fund study, the condominium should avoid any major shortfalls. However, to remain accurate, the report should be updated on an annual basis (maximum three years) to reflect such changes as shifts in economic parameters, additions of phases or assets, or expenditures of reserve funds. The condominium can assist in simplifying the reserve analysis update process by keeping accurate records of these changes throughout the year.

Funding Methods

From the simplest to the most complex, reserve analysis providers use many different computational processes to calculate reserve requirements. However, there are two basic processes identified as industry standards: the cash flow method and the component method.

The cash flow method develops a reserve-funding plan where contributions to the reserve fund are designed to offset the variable annual expenditures from the reserve fund. Different reserve funding plans are tested against the actual anticipated schedule of reserve expenses until the desired funding goal is achieved. This method sets up a “window” in which all future anticipated replacement costs are computed, based upon the individual lives of the components under consideration.

The component method develops a reserve-funding plan where the total contribution is based upon the sum of contributions for individual components. The component method is the more conservative of the two funding options, and assures that the condominium will achieve and maintain an ideal level of reserve over time. This method also allows for computations on individual components in the analysis.

Funding Strategies

Once the condominium has established its funding goals, the condominium can select an appropriate funding plan. There are four basic strategies from which most condominium s select. It is recommended that condominiums consult professionals to determine the best strategy or combination of plans that best suit the condominium’s need. Additionally, condominium should consult with their financial advisor to determine the tax implications of selecting a particular plan. The four funding plans and descriptions of each are detailed below. Condominiums will have to

13

update their reserve studies more or less frequently depending on the funding strategy they select.

Full Funding

Given that the basis of funding for reserves is to distribute the costs of the replacements over the lives of the components in question, it follows that the ideal level of reserves would be proportionately related to those lives and costs. If the condominium has a component with an expected estimated useful life of ten years, it would set aside approximately one-tenth of the replacement cost each year. At the end of three years, one would expect three-tenths of the replacement cost to have accumulated, and if so, that component would be “fully-funded.” This model is important in that it is a measure of the adequacy of an condominium’s reserves at any one point of time, and is independent of any particular method which may have been used for past funding or may be under consideration for future funding. This formula represents a snapshot in time and is based upon current replacement cost, independent of future inflationary or investment factors:

Fully Funded Reserves = Age divided by Useful Life the results multiplied by Current Replacement Cost

When a condominium’s total accumulated reserves for all components meet this criterion, its reserves are considered “fully-funded.”

Minimum Funding

The goal of this funding method is to keep the reserve cash balance above zero. This means that while each individual component may not be fully funded, the reserve balance overall does not drop below zero during the projected period. The condominium using this funding method must understand that even a minor reduction in a component’s remaining useful life can result in a deficit in the reserve cash balance.

Funding Model

This method is based upon the cash flow funding concept. The minimum reserve cash balance in threshold funding, however, is set at a predetermined dollar amount (other than $0).

Current Assessment Funding Model

This method is also based upon the cash flow funding concept. The initial reserve assessment is set at the condominium’s current fiscal year funding level and a 30-year projection is calculated to illustrate the adequacy of the current funding over time.

Component Funding Model

This is a straight-line funding model. It distributes the cash reserves to individual reserve components and then calculates what the reserve assessment and interest contribution (minus taxes)

14

should be, again by each reserve component. The current annual assessment is then determined by summing all the individual component assessments, hence the name “Component Funding Model”. This is the most conservative funding model. It leads to or maintains the fully funded reserve position. The following details this calculation process.

Component Funding Model Distribution of Accumulated Reserves

The “Distribution of Accumulated Reserves Report” is a “Component Funding Model” calculation. This distribution does not apply to the cash flow funding models.

When calculating reserves based upon the component methodology, a beginning reserve balance must be allocated for each of the individual components considered in the analysis, before the individual calculations can be completed. When this distribution is not available, or of sufficient detail, the following method is suggested for allocating reserves:

The first step the program performs in this process is subtracting, from the total accumulated reserves, any amounts for assets that have predetermined (fixed) reserve balances. The user can “fix” the accumulated reserve balance within the program on the individual asset’s detail page. If, by error, these amounts total more than the amount of funds available, then the remaining assets are adjusted accordingly. A provision for a contingency reserve is then deducted by the determined percentage used, and if there are sufficient remaining funds available.

The second step is to identify the ideal level of reserves for each asset. As indicated in the prior section, this is accomplished by evaluating the component’s age proportionate to its estimated useful life and current replacement cost. Again, the equation used is as follows:

Fully Funded Reserves = (Age/Useful Life) x Current Replacement Cost

Funding Reserves

Three assessment and contribution figures are provided in the report, the “Monthly/Annual Reserve Assessment Required”, the “Average Interest Earned” contribution and the “Total Monthly/Annual Allocation to Reserves.” The condominium should allocate the “Monthly/Annual Reserve Assessment Required” amount to reserves each month when the interest earned on the reserves is left in the reserve accounts as part of the contribution. Any interest earned on reserve deposits, must be left in reserves and only amounts set aside for taxes should be removed.

The second alternative is to allocate the “Total Monthly/Annual Allocation” to reserves (this is the member assessment plus the anticipated interest earned for the fiscal year). This method assumes that all interest earned will be assigned directly as operating income. This allocation takes into consideration the anticipated interest earned on accumulated reserves regardless of whether or not it is actually earned. When taxes are paid, the amount due will be taken directly from the condominium’s operating accounts as the reserve accounts are allocated only those moneys net of taxes.

15

Users’ Guide to your Reserve Fund Study

Adjustment to Useful Life

Once the useful life is determined, it may be adjusted, up or down, by this separate figure for the current cycle of replacement. This will allow for a current period adjustment without affecting the estimated replacement cycles for future replacements.

Annual Assessment Increase

This represents the percentage rate at which the condominium will increase its assessment to reserves at the end of each year. For example, in order to accumulate $10,000 in 10 years, you could set aside $1,000 per year. As an alternative, you could set aside $795 the first year and increase that amount by 5% each year until the year of replacement. In either case you arrive at the same amount. The idea is that you start setting aside a lower amount and increase that number each year in accordance with the planned percentage. Ideally this figure should be equal to the rate of inflation. It can, however, be used to aide those condominiums that have not set aside appropriate reserves in the past, by making the initial year’s allocation less formidable.

Annual Fixed Reserves

An optional figure which, if used, will override the normal process of allocating reserves to each asset.

Budget Year Beginning/Ending

The budgetary year for which the report is prepared. For example, if the condominiums with fiscal years ending December 31st, the monthly contribution figures indicated are for the 12-month period beginning 1/1/20xx and ending 12/31/20xx.

Cash Flow Method

A method of developing a Reserve Funding Plan where contributions to the Reserve fund are designed to offset the variable annual expenditures from the Reserve fund. Different Reserve Funding Plans are tested against the anticipated schedule of Reserve expenses until the desired Funding Goal is achieved.

Component

The individual line items in the Reserve Fund Study developed or updated in the Physical Analysis. These elements form the building blocks for the Reserve Fund Study. Components typically are:

1) Condominium responsibility;

16

2) With limited Useful Life expectancies;

3) Predictable Remaining Useful Life expectancies;

4) Above a minimum threshold cost, and

5) As required by local codes.

Component Inventory

The task of selecting and quantifying Reserve Components. This task can be accomplished through on-site visual observations, review of condominium design and organizational documents, a review of established condominium precedents, and discussion with appropriate condominium representative(s) of the condominium.

Component Method

A method of developing a Reserve Funding Plan where the total contribution is based on the sum of contributions for individual components. See “Cash Flow Method.”

Condition Assessment

The task of evaluating the current condition of the component based on observed or reported characteristics.

Current Replacement Cost

The estimated replacement cost effective at the beginning of the fiscal year for which the report is being prepared

Detail Reports

The Detail Report itemizes each asset and lists all measurements, current and future costs, and calculations for that asset. Provisions for percentage replacements, salvage values, and one-time replacements can also be utilized.

Estimated Useful Life

The estimated useful life of an asset based upon industry standards, manufacturer specifications, visual inspection, location, usage, condominium standards and prior history. All of these factors are taken into consideration when tailoring the estimated useful life to the particular asset. For example, the carpeting in a hallway or elevator (a heavy traffic area) will not have the same life as the identical carpeting in a seldom-used meeting room or office.

17

Estimated Remaining Life

This calculation is completed internally based upon the report’s fiscal year date and the date the asset was placed-in-service.

Effective Age

The difference between Useful Life and Remaining Useful Life. Not always equivalent to chronological age, since some components age irregularly. Used primarily in computations.

Financial Analysis

The portion of a Reserve Study where current status of the Reserves (measured as cash or Percent Funded) and a recommended Reserve contribution rate (Reserve Funding Plan) are derived, and the projected Reserve income and expense over time is presented. The Financial Analysis is one of the two parts of a Reserve Study.

Fixed Assessment

An optional figure which, if used, will override all calculations and set the assessment at this amount. This assessment can be set for monthly, quarterly or annually as necessary.

Fully Funded

100% Funded. When the actual (or projected) Reserve balance is equal to the Fully Funded Balance.

Fully Funded Balance

Total Accrued Depreciation. An indicator against which Actual (or projected) Reserve balance can be compared. The Reserve balance that is in direct proportion to the fraction of life “used up” of the current Repair or Replacement cost. This number is calculated for each component, then summed together for an condominium total. Two formulae can be utilized, depending on the provider’s sensitivity to interest and inflation effects. Note: Both yield identical results when interest and inflation are equivalent.

Fully Status

The status of the reserve fund as compared to an established benchmark such as percent funding.

18

Funding Goals

Independent of methodology utilized, the following represent the basic categories of Funding Plan goals:

Baseline Funding: Establishing a Reserve funding goal of keeping the Reserve cash balance above zero.

Full Funding: Setting a Reserve funding goal of attaining and maintaining Reserves at or near 100% funded.

Statutory Funding: Establishing a Reserve funding goal of setting aside the specific minimum amount of Reserves required by local statues.

Threshold Funding: Establishing a Reserve funding goal of keeping the Reserve balance above a specified dollar or Percent Funded amount. Depending on the threshold, this may be more or less conservative than “Fully Funding.”

Funding Plan

The condominium’s planned to provide income to a Reserve fund to offset anticipated expenditures from that fund.

Funding Principles

Sufficient Funds When Required Stable Contribution Rate over the Years Evenly Distributed Contributions over the Years Fiscally Responsible

Future Replacement Cost

The estimated cost to repair or replace the asset at the end of its estimated useful life based upon the current replacement cost and inflation.

Index Reports

The Distribution of Accumulated Reserves report lists all assets in remaining life order. It also identifies the ideal level of reserves that should have accumulated for the condominium as well as the actual reserves available. This information is valid only for the “Component Funding Model” calculation.

The Component Listing/Summary lists all assets by category (i.e. roofing, painting, lighting, etc.) together with their remaining life, current cost, monthly reserve contribution, and net monthly allocation.

Inflation

This figure is used to approximate the future cost to repair or replace each component in the report.

19

The current cost for each component is compounded on an annual basis by the number of remaining years to replacement, and the total is used in calculating the monthly/annual reserve contribution that will be necessary to accumulate the required funds in time for replacement.

Interest Contribution (After Taxes)

The interest that should be earned on the reserves, net of taxes, based upon their beginning reserve balance and monthly contributions for one year. This figure is averaged for budgeting purposes.

Investment Yield Before Taxes

The average interest rate anticipated by the condominium based upon its current investment practices.

Life and Valuation Estimates

The task of estimating Useful Life, Remaining Useful Life, and Repair or Replacement Costs for the Reserve components.

Number of Units and/or Phases

If applicable, the number of units and/or phases included in this version of the report.

One-Time Replacement

Notation if the asset is to be replaced on a one-time basis.

Percent Fully Funded

The ratio, at the beginning of the fiscal year, of the actual (or projected) reserve balance to the calculated fully funded balance, expressed as a percentage.

Percentage of Replacement or Repairs

In some cases, an asset may not be replaced in its entirety or the cost may be shared with a second party. Examples are budgeting for a percentage of replacement of streets over a period of time, or sharing the expense to replace a common wall with a neighboring party.

Physical Analysis

The portion of the Reserve Study where the Component Inventory, Condition Assessment, and Life and Valuation Estimate tasks are performed. This represents one of the two parts of the Reserve

20

Study.

Phase Increment Detail and/or Age

Comments regarding aging of the components on the basis of construction date or date of acceptance by the condominium.

Placed-In-Service Date

The month and year that the asset was placed-in-service. This may be the construction date, the first escrow closure date in a given phase, or the date of the last servicing or replacement.

Projected Reserve Balance

The anticipated reserve balance on the first day of the fiscal year for which this report has been prepared. This is based upon information provided and not audited.

Projections

Thirty-year projections add to the usefulness of your reserve analysis study. Information provided about reserve projects will be considered reliable. Any onsite inspection should not be considered a project audit or quality inspection.

Remaining Useful Life

Also referred to as “Remaining Life” (RL). The estimated time, in years, that a reserve component can be expected to continue to serve its intended function. Projects anticipated to occur in the initial year have “zero” Remaining Useful Life.

Replacement Costs

The cost of replacing, repairing, or restoring a Reserve Component to its original functional condition. The Current Replacement Cost would be the cost to replace, repair, or restore the component during that particular year.

Report I.D.

Includes the Report Date (example: November 15, 1992), Project Number (example: 82109), and Version (example: 1.0). Please use this information (displayed on the summary page) when referencing your report.

21

Report Summaries

The Report Summary for all funding models lists all of the parameters that were used in calculating the report as well as the summary of your reserve analysis study.

Reserve Balance

Actual or projected funds as of a particular point in time that the condominium has identified for use to defray the future repair or replacement of those major components which the condominium is obligated to maintain. Also known as Reserves, Reserve Accounts, and Cash Reserves. Based upon information provided and not audited.

Reserve Provider

An individual that prepares Reserve Fund Studies.

Reserve Study/ Reserve Fund Study

A budget planning tool which identifies the current status of the Reserve fund and a stable and equitable Funding Plan to offset the anticipated future major common area expenditures. The Reserve Fund Study consists of two parts: the Physical Analysis and the Financial Analysis. “Our budget and finance committee is soliciting proposals to update our Reserve Fund Study for next year’s budget.”

Salvage Value

The salvage value of the asset at the time of replacement, if applicable.

Special Assessment

An assessment levied on the members of the condominium in addition to regular assessments. Special Assessments are often regulated by governing documents or local statutes.

Total Monthly/Annual Allocation

The sum of the monthly/annual assessment and interest contribution figures.

Useful Life

Total Useful Life or Depreciable Life. The estimated time, in years, that a reserve component can be expected to serve its intended function if properly constructed in its present application or installation.

22

3. GENERAL INFORMATION

A Reserve Fund Study is made up of two parts

1) The information about the physical status and repair/ replacement cost of the major common area components the condominium is obligated to maintain (Physical Analysis), and

2) The evaluation and analysis of the condominium’s Reserve balance, income, and expenses (Financial Analysis).

The Physical Analysis is comprised of the Component Inventory, Condition Assessment, and Life and Valuation Estimates. The Component Inventory should be relatively “stable” from year to year, while the Condition Assessment and Life and Valuation Estimates will necessarily change from year to year. The Financial Analysis is made up of a finding of the client’s current Reserve Fund Status (measured in cash or as Percent Funded) and a recommendation for an appropriate Reserve contribution rate (Funding Plan).

Levels of Service The following three categories describe the various types of Reserve Fund Studies, from exhaustive to minimal.

Class 1 - This is the comprehensive reserve fund study with a site visit. It is the first one done and involves a great deal of information gathering to first develop a "component inventory" of those items that have varying and limited "life cycles". Such items as roofs, building cladding, windows, doors, HVAC systems, plumbing and electrical systems, site services, pavement, landscaping, etc. are identified and should be quantified.

While the Condominium Act does not require the reserve fund study to provide this quantification, it would be prudent to engage one who does. It is very useful information for you to have. Each component is inspected in order to initially arrive at a professional opinion on its respective stage in its typical "life cycle".

A great deal of information must be assembled as part of the Class 1 reserve fund study. It includes examining blueprints and drawings, examining repair and replacement histories, ongoing maintenance programs, interviewing people with knowledge of historical problems, and calculating current replacement costs. Their future values are projected at an appropriate and compounded inflation rate with the timing of the major repairs and replacements.

This establishes the "benchmark" for future updates and for the 30 years cash flow projection required as a part of the reserve fund study or update. We use the 'sinking fund' method in developing our benchmark analysis. It is much more realistic and accurate than using the typical and simplistic 'straight line' method favored by professional quantity surveyors; architects and professional engineers.

23

Class 2 - This is the reserve fund study update with a site visit. With this, the component inventory is reviewed and verified, then a condition assessment is conducted of each item (based on visual inspections) and their life cycle costing is updated.

Updated interest and building component inflation rates are applied to the current replacement costs and an updated 30 years cash flow projection is calculated to determine the revised contribution requirements.

While not as extensive as the Class 1 - comprehensive reserve fund study, it nonetheless, does involve a considerable amount of site time. Individual reserve fund inventory components change after 5 to 6 years. They've simply aged and in some cases have been replaced or undergone major repairs. That's why they have to be seen again.

It is done six years or so after the comprehensive reserve fund study and three years after the Class 3 - reserve fund study update without a Site Visit.

When we do Class 2 updates for condominium corporations where previous reserve fund studies have been done by professional quantity surveyors; architects and professional engineers, we've discovered that many of them do not provide adequate component quantification and unit costing. Nor do they even bother to develop a reserve fund history based on analyzing previous reserve fund expenditures. These are critical elements in a proper and diligent Class 2 update and we take the time, if we find it missing, to provide this valuable information. It's simply a part of our due diligence.

Class 3 - This is the reserve fund study update without a site visit. This is an update of the comprehensive reserve fund study and is primarily a financial update of the annual reserve fund contributions and reserve fund expenditures that have been made (if any). We plot the respective life cycles of each component by generally extending them by the number of years since the last reserve fund study or update with a site visit. Again, revised interest rates and building component inflation rates are applied to the calculations to arrive at a revision of the annual reserve contributions required and a revised 30 year cash flow projection is done.

After the initial comprehensive reserve fund study is conducted (Class 1), the prudent client will commission a Class 3 and Class 2 update, alternating between those two types every 3 years.

These reserve fund study updates are important to do because components get closer to their life cycle period ends (in some cases prematurely) and the interest and building component inflation costs change a great deal. These three factors have a great impact on changes to your reserve fund plan; the component costs, the timing of major repairs and replacements, as well as your annual reserve fund conditions.

24

4. RESERVE FUND STUDY PURPOSE

A Reserve Fund Study is the art and science of anticipating, and preparing for, major common area repair and replacement expenses.

A Reserve Study allows the Board and Management to offset the ongoing deterioration of the common areas with Funds to ensure the timely repair, replacement or restoration of those common areas. When properly done, irregular Reserve expenses are offset by ongoing, regular Reserve contributions. Special assessments are then left for true emergencies, not expenses that could have been anticipated.

The purpose of this report is to provide cost estimates for the building components that will be subject to major repairs, replacement or restoration over the life of the property, and to provide an estimate of the funding required for such major repairs and replacement. The study is to be conducted in accordance with the reserve fund standards outlined are regulated by governing documents or local statutes.

A reserve fund study is an analysis of the common property of a Condominium Corporation to determine the financial health of the capital replacement reserve fund.

A study will:

Provide an inventory of all building components which are subject to a physical, functional deterioration

Analyze the present condition of all the components and estimate the effective age and remaining life of each component

Estimate the cost of repair, replacement, or restoration of each component

Determine the amount of funds currently accumulated by the condominium corporation for the purpose of repairing, replacing or restoring the components identified in the study

Make recommendation as to the appropriate amount of funds required to meet the future financial obligation of the condominium corporation. What’s the difference between a Reserve Fund Study and a Reserve Fund Plan? A Reserve Fund Report is a financial document detailing the findings of the study, the qualifications of the analyst and other matters relevant to operation of the condominium corporation as they relate to the reserve fund. The report provides the basis for funding major repairs, replacements, or restorations of the common area building components and provides a practical guide for budgeting and planning maintenance programs. A Reserve Fund Plan is a plan that must be approved by the Board

25

of Directors upon receiving and reviewing the reserve fund study. The plan must establish the Reserve Fund and set out the method of and amount of contribution be made by the unit holders. What are the two main parts in the Reserve Study? Every Reserve Study has two parts: information on the physical condition of the property and the financial analysis performed using that information. It is natural, therefore, to divide the Reserve Study into these two parts.

Many building owners struggle with the concept of a reserve fund for future renewals and funding the reserve through a balance of regular contributions and special assessments. With adequate planning and a reasonable prediction of future costs, Owners can prepare for future costs and avoid the financial hardship that can occur with unexpected large special assessments. The intent of a Reserve Fund Study (RFS) is to assist in the financial planning by:

o Providing financial guidance so that building owners can make prudent and informed decisions regarding the provision of adequate reserve funding.

o Providing a planning tool to help ensure financial continuity and dependability for current and future owners.

In relationship to your personal assets, a Reserve Fund Study for the condominium corporation can be thought of as a list of everything you own (all the common elements of condominium), an assessment of how long your assets will last (remaining service life), an estimate of the cost of replacing your assets in the future (replacement cost) and a roadmap (funding model) demonstrating how to arrive at the end of your assets service life with enough funds to buy a new one.

It can also help to think of a Reserve Fund Study as a sort of retirement plan for the building. In order to estimate the required level of savings for your actual retirement, an accountant first makes an estimate of your living expenses; similar to a reserve analyst estimating the replacement costs of buildings physical assets. In both cases, once future costs are estimated, the accountant or reserve analyst, based on a set saving period, determines the necessary level of yearly retirement savings, or reserve contributions, needed each year to prepare for future costs.

Just as there are many routes available on a road map, and there are also many funding models available to reconcile future costs with potential saving plans. Most funding models involve a combination of regular contributions (monthly strata fees) with discrete funding (special assessments).

The most important aspect of reserve fund modeling is flexibility to satisfy the condominium corporation needs each year in the face of an often unpredictable and changing economic environment. Our company provides dynamic tracking of service life predictions, future cost estimates and reserve fund balances, allowing users to examine multiple funding models.

The Reserve Fund Study is a living document that must be updated periodically (every three years) to reflect changes in the inflation rate, escalation rates, and interest rates. The initial studies establish the baseline for all future updates and it is therefore a significant tool in setting the framework for long-term financial management of the building.

26

A Multi-Purpose Tool

Your Reserve Fund Report is an important part of your condominium’s budgetary process. Following its recommendations should ensure the condominium’s smooth budgetary transitions from one fiscal year to the next, and either decrease or eliminate the need for “special assessments”.

In addition, your Reserve Fund Study Report serves a variety of useful purposes:

� Following the recommendations of a Reserve Fund Study Report performed by a professional quantity surveyors; architects and professional engineers can protect the Board of Directors in a condominium from personal liability concerning reserve components and reserve funding.

� A Reserve Fund Study Report is required by your accountant during the preparation of the condominium’s annual audit.

� The Reserve Fund Study Report is often requested by lending institutions during the process of loan applications, both for the community and, in many cases, the individual owners.

� Your Reserve Fund Study Report is also a detailed inventory of the condominium’s major assets and serves as a management tool for scheduling, coordinating and planning future repairs and replacements.

� Your Reserve Fund Study Report is a tool that can assist the Board in fulfilling its legal and fiduciary obligations for maintaining the condominium in a state of good repair. If a condominium is operating on a special assessment basis, it cannot guarantee that an assessment, when needed, will be passed. Therefore, it cannot guarantee its ability to perform the required repairs or replacements to those major components for which the condominium is obligated.

� Since the Reserve Fund Study Report includes measurements and cost estimates of the client’s assets, the detail reports may be used to evaluate the accuracy and price of contractor bids when assets are due to be repaired or replaced.

� The Reserve Fund Study Report is an annual disclosure to the membership concerning the financial condition of the condominium, and may be used as a “consumers’ guide” by prospective purchasers.

� Your Reserve Fund Study Report provides a record of the time, cost, and quantities of past reserve replacements. At times the condominium’s management company and board of directors are transitory which may result in the loss of these important records.

27

5. ACKNOWLEDGEMENTS AND ASSEMBLY OF THE REPORT

Several personnel have assisted with the Reserve Study Report, under the direction of JBCS Canada Inc., the following individuals comprise the reserve study team:

Note:

• PQS - Member of Canadian Institute of Quantity Surveyors (CIQS);

• PRA - Member of Association of Professional Reserve Analysts (APRA)

• PEng – Member of Professional Engineers Ontario (PEO)

28

6. DOCUMENTATION The following reference materials have been provided by property management, for use in the preparation of this report. (The actual or projected total presented in the Reserve Study is based upon information provided by management and was not audited.)

• Last 5 years record for major repairs or replacement over $500.00;

• Condominium Declaration (only partial of the definition for the common areas);

• Financial Statements;

• Technical Resource Material;

• Partial of Construction drawing;

OTHER REFERENCE SOURCES

Information used in completing this Study was collected from the following sources:

� Condominium Plan

� Condominium Act / By-Laws

� Financial Statements

� Technical Reports on Common Property Components

� Site Investigations

� Property Manager and/or Board Members

� Technical Resource Material

The life cycles of common property components were determined using a combination of the following:

� Recognizable conditions

� Experience factors

� Discussion with manufacturers, suppliers and service contractors

Replacement costs of common property components were determined using a combination of the following:

� RS Means Repair and Re-modeling Cost Data

� RS Means Square Foot Costs

29

� Experience with similar developments

� Discussion with manufacturers, suppliers and service contractors

� Review of financial documentation

30

7. THE PHYSICAL ANALYSIS The physical analysis involves determining the individual components comprising the common elements in order to formulate an inventory of these items. Once the component inventory is determined, a visual condition survey is carried out in order to provide a component assessment and valuation. In this section of the report, we have provided a listing of the inventory or building components that form part of the common elements. A description of the conditions encountered during our site observations of these components has been provided. Comments regarding the estimated remaining life, the extent and phasing of replacement/repairs have also been provided.

1 SITE WORKS

HARD LANDSCAPING

Concrete Curbs

Concrete curbs are installed at XXXX XXXXXXXX XXXXXXXXX XXXXXXXXXXXX XXXX XXX areas and throughout the landscaped areas. Cracking, deterioration and settlement of the concrete curbs were observed to be present at the time during our site visit at isolated locations. Accordingly, the concrete curbs are generally in fair condition.

Major repair of these components will be required over a thirty-five (35) years forecast period. Therefore, we have estimated that replacements will occur in the next xx years. Until then, maintenance and repair of distressed areas is advised.

Pedestrian Walks

The pedestrian walks are located at xxx; they are generally in fair condition. The life expectancy of the fencing is normally thirty-five (35) years. Therefore, we have estimated that replacement will occur in the next xxx years. Until then, maintenance and repair of distressed areas is advised.

Exterior Signage

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

2 STRUCTURE

BUILDING

Structural Systems of the sub-structure and super-structure (Concrete Repairs)

The existing Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

.

31

BASEMENT/UNDERGROUND GARAGE

Waterproofing Systems

The waterproofing systems are generally in fair condition. Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

3 BUILDING ENVELOPE

WALLS

Exterior Wall (Major Repairs)

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

COATINGS

Exterior Painting

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

DOORS

Entrance Doors; Services Doors and Balcony Doors

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

implemented in order to ensure an extended remaining life is achieved.

WINDOWS

Window System

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

MEMBRANES AND SEALANTS

Cladding Joints; Caulking to Windows and Doors

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

ROOFING

Roofing Systems Replacement

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

32

the entire roofing system Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

in order to ensure an extended remaining life is achieved.

4 MECHANICAL & ELECTRICAL EQUIPMENT

SITE SYSTEMS

Water Main

This item includes the underground piping which carries water from the Municipality to the building. Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.in order to ensure an extended remaining life is achieved.

DRAINAGE SYSTEMS

Sanitary Drainage Systems

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

Storm Drainage Systems

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.remaining life is achieved.

WATER SYSTEMS

Water Systems

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

.

HEATING SYSTEMS & COOLING SYSTEMS

Heating Systems & Cooling Systems

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

VENTILATION SYSTEMS

Ventilation Systems

Those systems are expected that a major repair/partial replacement will have to be performed in

33

approximately seven xx years. The life expectancy of this item is thirty (30) years. An annual preventative maintenance program should be implemented in order to ensure an extended remaining life is achieved.

WASTE DISPOSAL SYSTEMS

Waste Disposal Systems

Those systems Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

program should be implemented in order to ensure an extended remaining life is achieved.

5 ELECTRICAL SYSTEMS

ELECTRICAL SUPPLY & DISTRIBUTION

Power Supply, Distribution, Panel Boards and Sub-Circuits

This item refers to those portions of the main electrical service feed and equipment that service the entire building. Elements considered under this item include main switchgears, transformers, and main service disconnects. As it is unreasonable to expect that all items will require replacement in the future and at the Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

.

LIGHTING SYSTEMS

Exterior and Interior Lighting

This item includes fixtures at all the service entrances, soffit lighting, those at building entrances and other common areas. Maintenance budget are assumed to be covered all the isolated replacements. Reserve Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

life is achieved.

AUXILIARY SYSTEMS

Security Systems

Those systems are expected that a major repair/replacement will have to be performed in Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

6 LIFE SAFETY SYSTEMS

34

FIRE DETECTION & SPRINKLER SYSTEMS

Fire Protection System & Sprinkler Systems

This item refers to the buildings' smoke and heat detectors, horns, sirens, bells, pull stations and other standard detection or signal devices used in the Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

7 ELEVATORS

ELEVATOR UPGRADES/REPLACEMENTS

Equipment Upgrades/Partial Replacements

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

.

8 INTERIOR FINISHES / FURNISHINGS

CORRIDORS

Flooring - material

The flooring system listed here is located inside the corridors and are still in a fair condition. The remaining life span of this material has been estimated Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

Flooring -

This item is located inside the Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

35

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

Wall Finishes

The corridors are generally finished with painted gypsum board. The wall finishes are scheduled to be refreshed every fifteen (15) years respectively to maintain the as-new appearance of the common corridors.

Ceiling Finishes

The corridors are generally finished with acoustical ceiling tile, depending on the location. The ceiling finishes are scheduled to be refreshed every thirty (30) years to maintain the as-new appearance of the common corridors.

LOBBY/VESTIBULE

Flooring

The flooring system listed here is located at the entrances of the mall and is in a fair condition. The remaining life span of this material has been estimated xxxx) years, and a life expectancy of forty (40) years.

Flooring

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

Wall Finishes

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

Ceiling Finishes

Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

SERVICES AREAS

Stairwells

This item includes all the Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

Garbage Room

This item Xxx bbbb bbbbbb bbbb bbbbbbb bbbbb bbbb bbbbbbb bbb bbbb bb bbbbbb bbbbbbbbbbbb bbbb bbbbb bbb bbbbbbb b bbtypic al conditions.

36

.

9 MISCELLANEOUS

PROFESSIONAL FEES

Reserve Fund Study Fees

This item includes updates to the Reserve Fund Study at every three (3) years intervals.

General Note:

Life expectancies have been extended, where possible, in order to ensure a positive cash flow over a 30 year period. Items with extended life expectancies should be reviewed on a periodic basis and the extended life expectancy for every item should be adjusted, as required. An ongoing preventative maintenance program should be implemented in order to ensure an extended remaining life expectancy is achieved.

37

8. THE FINANCIAL ANALYSIS

The financial analysis portion of the Reserve Fund Study is made up of determining the present financial strength or status of the Reserve Fund and to provide a recommendation for an appropriate annual Reserve Fund contribution which would be required to offset anticipated future major repairs and/or replacement expenditures.

1. Financial Assumptions

1.1. Cost Estimates

Estimated repair and/or replacement estimates are based on present day dollars and on the assumption regarding the required scope of repair work. Replacement costs are generally different than new construction costs as a result of difficulties with access and the requirements to remove and replace existing building components and interior finishes.

The replacement costs of the various components forming the common elements detailed in this report are based on the unit rates detailed in the Building Construction Cost Data published by RS Means, combined with experience gained by JBCS Canada Inc. in the repair and renovation of residential and commercial buildings.

The assumptions regarding the life expectancy of each of the various components forming the common elements of this development as detailed in this report are based on the technical literature of manufacturers and our experience with the materials forming the common elements. The remaining life expectancy periods of the common elements are based on the observations made during visual examinations of the property and on information supplied to us by Building Management.

The number of years allocated to the life expectancy of the inventory of items is also based on the assumption that all Reserve Fund items will receive regular and ongoing maintenance and proper care throughout their operational life.

1.2. Operating Budget Costs

In order to properly assess the inventory of items that comprise the Reserve Fund, it was assumed that minor repairs under $500.00 would be carried out as part of the ongoing program of maintenance. Therefore, for the purposes of this report, these items are not generally included in the Reserve Fund.

38

1.3. Inflation Rate

An assumed inflation rate for this report (This Inflation Rate and the parameters under which it has been completed are based upon information provided to us in part by representatives of the condominium, its contractors, assorted vendors, specialist and independent contractors. And various construction pricing and scheduling manuals. Additionally, the rate is obtained from numerous vendor catalogues, actual quotations or historical costs, and our own experience in the field of property management and reserve study preparation) has been used in our financial analysis for 30 years forecast period.

1.4. Interest Rate

It is assumed that the Board of Directors will reinvest all Reserve Fund interest income back into the Reserve Fund. We believe this approach will lessen the net effect of inflationary increases. An assumed interest rate for this report (This Interest Rate are based upon information provided to us in part by representatives of the condominium, and also, refer to the current banking information.) has been used over a 30 years forecast period.

2. Financial Calculations and Cost Analysis

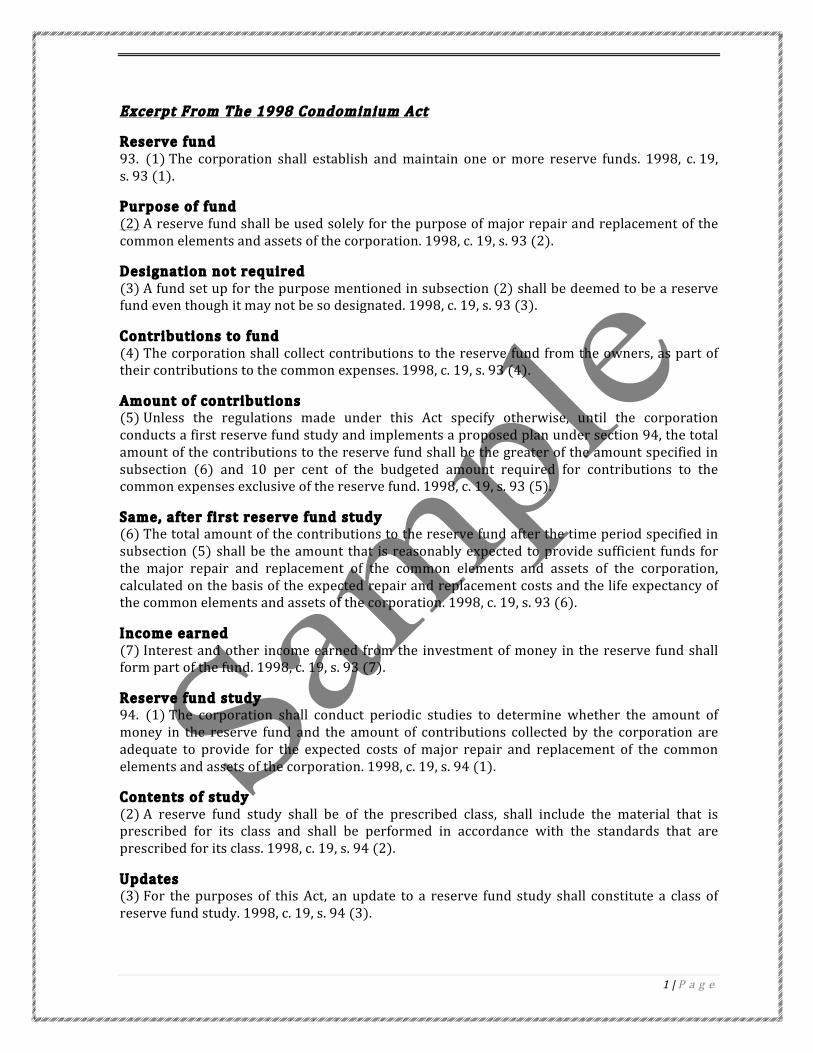

The Condominium Act defines a Reserve Fund, as a Fund set up by the Corporation in a special account for major repairs and replacement of common elements and assets of the Corporation. The Condominium Act also requires that the amounts in the Reserve Fund be calculated on the basis of expected repair and replacement costs and life expectancy.

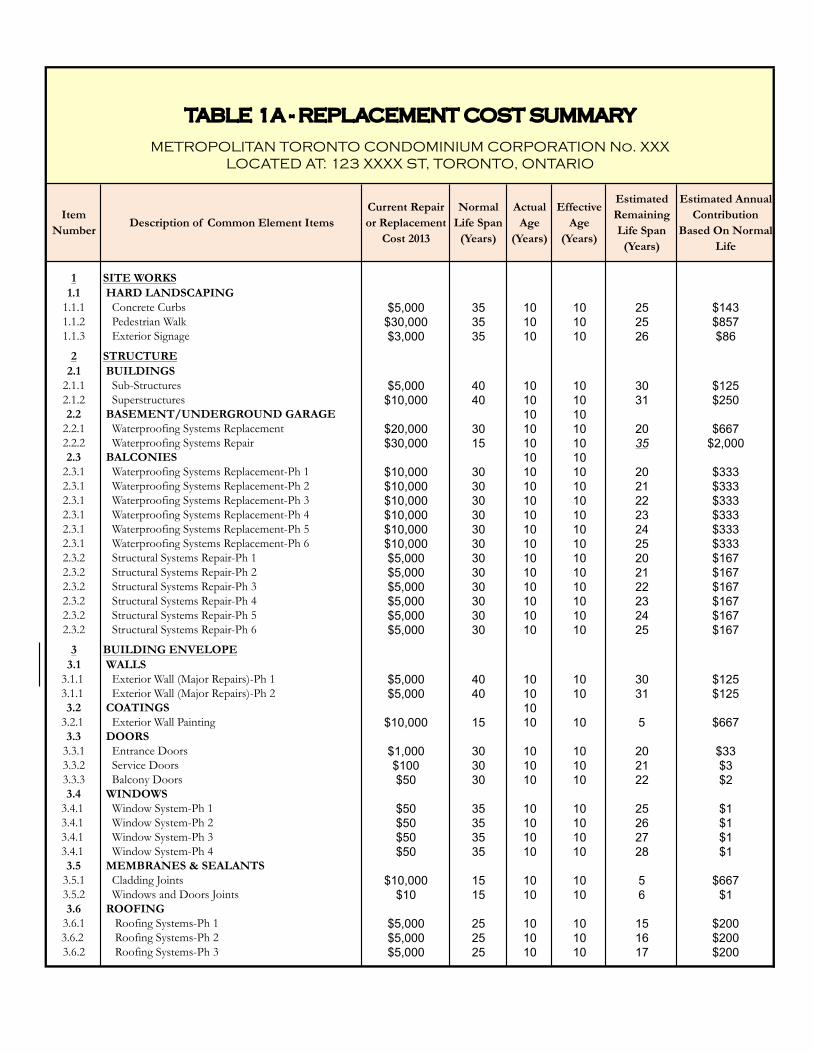

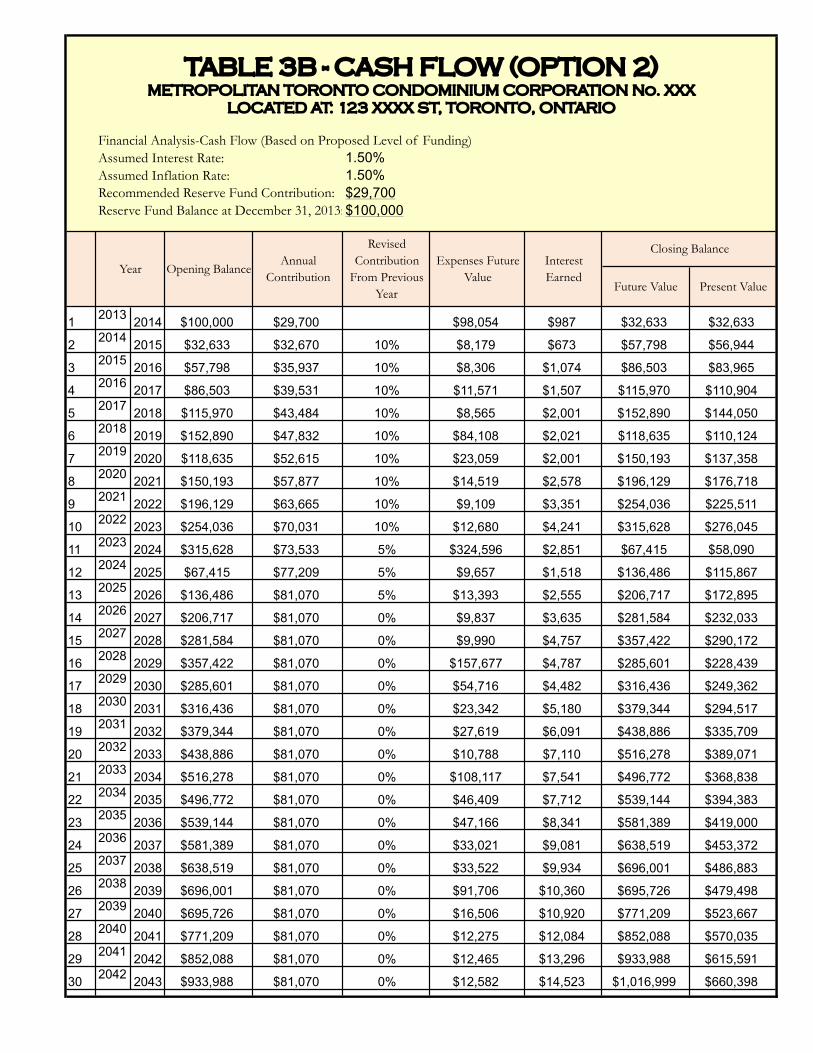

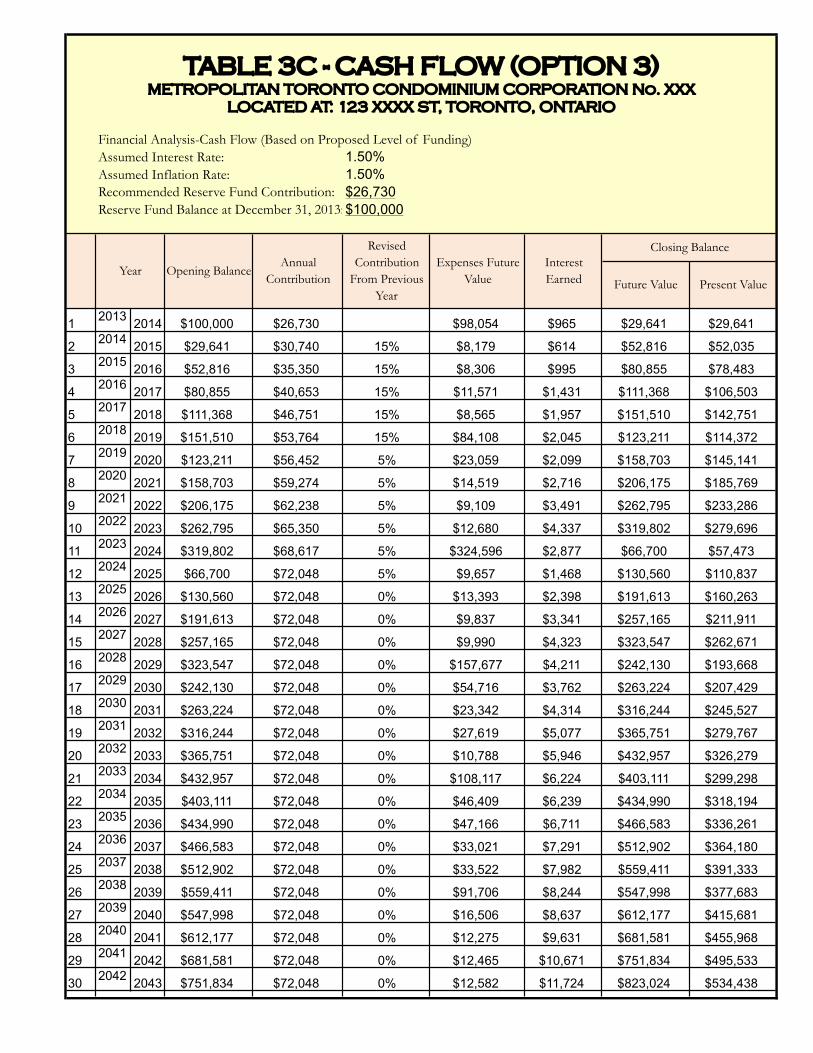

The reserve fund calculations are outlined in Tables 1 to 3.

Table 1 entitled “Replacement Cost Summary”, details information in regards to the items that comprise the common elements including their estimated repair/replacement costs, the normal life, present age, estimated remaining life and the estimated annual contribution based on the normal life of a component. The last column is included for information purposes and it establishes at a glance, prior to carrying out cash flow scenarios, the adequacy for present funding.

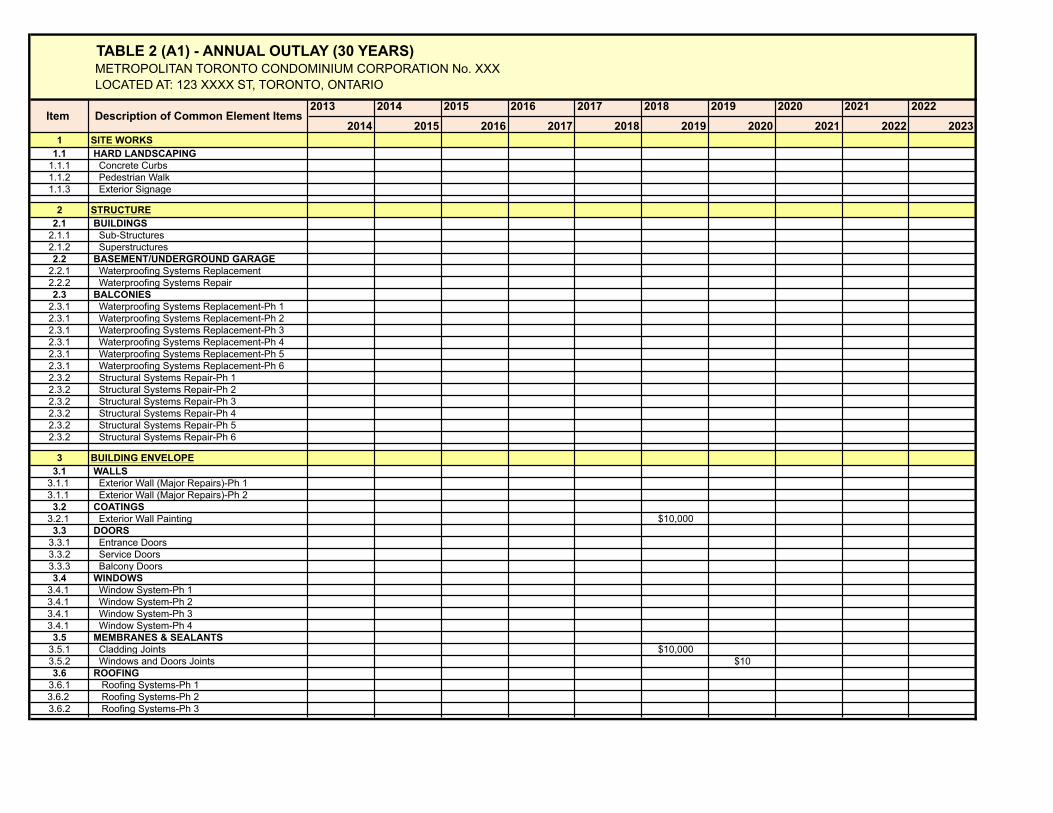

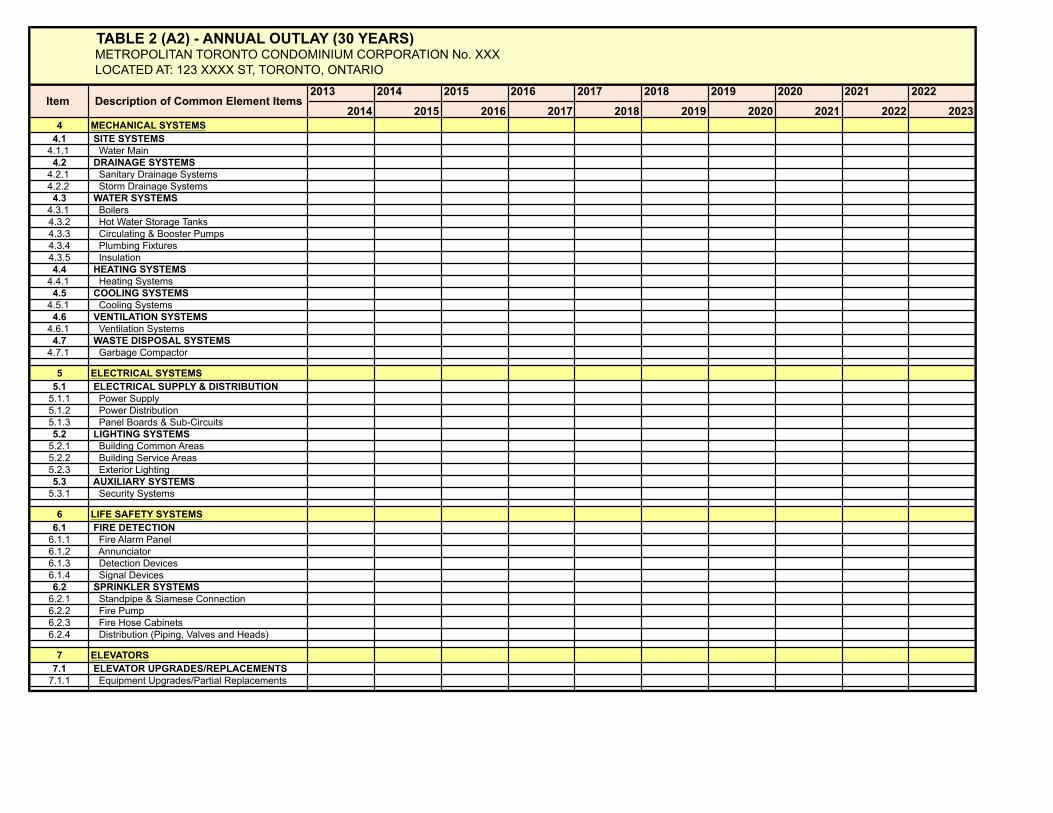

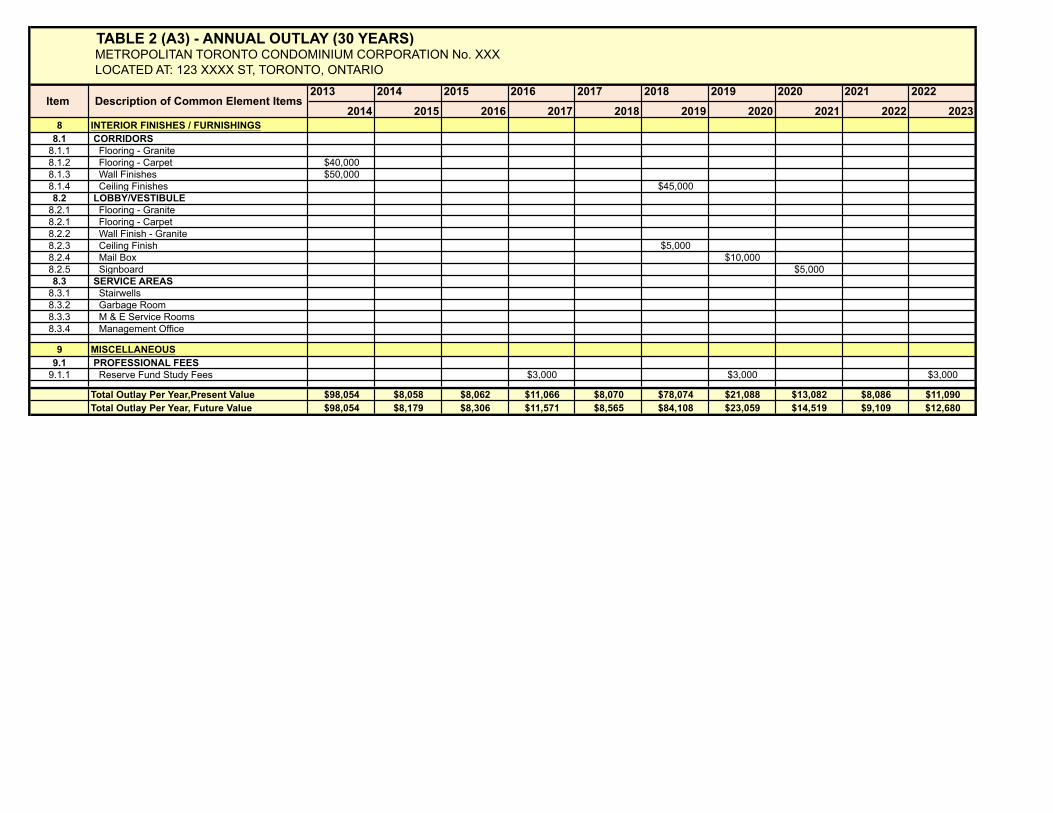

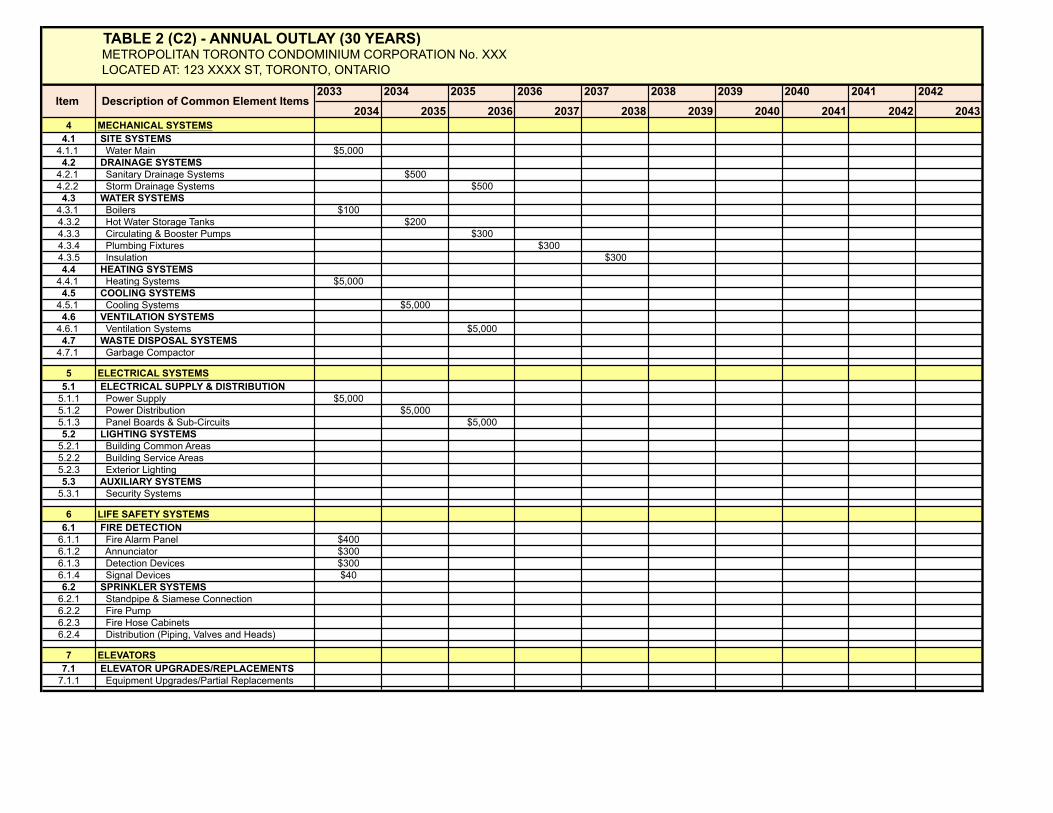

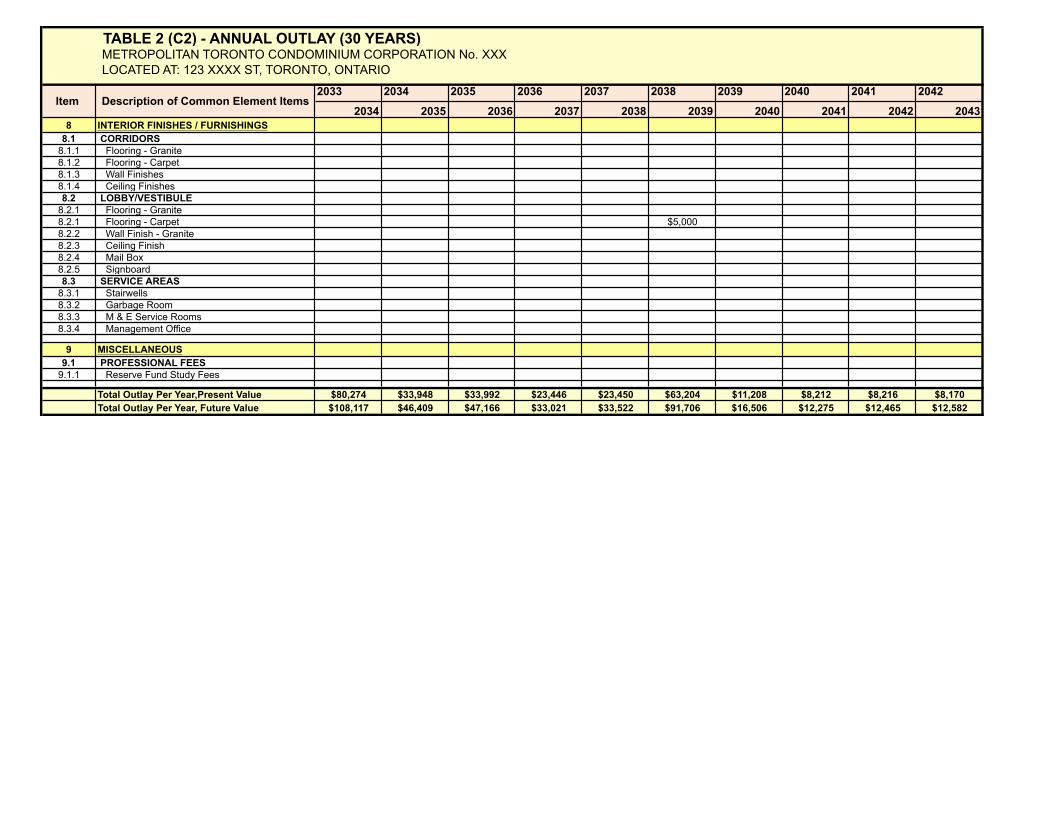

Table 2 is entitled “Annual Outlay”, this table provides the anticipated expenditures over a 30-year forecast period. This table summarizes the annual outlay of expenses for each year and the costing in this table is in present and future dollars.

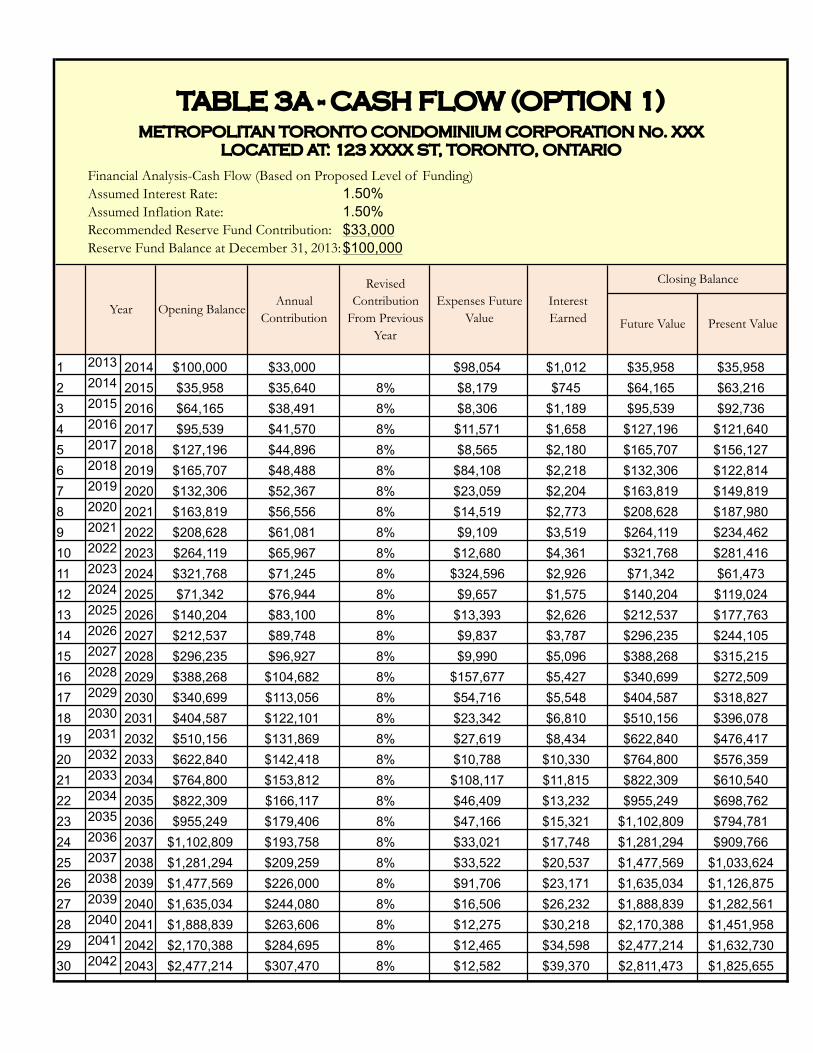

Table 3 is entitled “Cash Flow”, the primary purpose of this table is to provide a recommendation for an appropriate annual Reserve Fund contribution, which would be required to offset, anticipated future major repairs and/or replacement expenditures. In order to calculate the minimum recommended annual contribution, the contribution is adjusted until the closing balance approaches

39

zero funding for a critical year. Since the critical year is a year where a number of items require replacement/repair, the fund usually increases thereafter.

Detailed below is a brief description of the columns in Tables 1 and 3.

Description of Common Element Items A list of the common element items. Once the component was determined a detailed visual condition survey was carried out in order to provide a component assessment and valuation.

Estimated Repair/Replacement Cost The estimated cost for repair and/or replace building components in present day dollars.

Normal Life The normal life expectancy, in years, of the list of items.

Actual Age The actual age, in years, of the list of items.

Effective Age The existing condition, in years, of the list of items.

Estimated Remaining Life The estimated years before major repair and/or replacement of an item is required.

Estimated Annual Contribution Based On Normal Life The estimated annual contribution based on the normal life expectancy of an item is used for illustration purposes and serves as a guide to the required level of contribution without factors such as interest and inflation rates.

Opening Balance The amount of money in the Reserve Fund at the beginning of fiscal the year.

Annual Contribution The annual contribution allocated to the Reserve Fund.

Revised Contribution From Previous Year The variation for the annual contribution.

Expenses, Future Value Future value of anticipated annual expenditures derived from Table 2.

40

Interest Earned Assumed yearly interest earned by the moneys in the Reserve Fund. A simplified calculation has been used whereby interest that is earned on investments and one-half of the annual contributions are paid at every year-end. The interest earned is assumed to be reinvested back into the reserve fund.

Closing Balance, Future Value and Present Value The closing balance is calculated by adding the opening balance plus interest earned, less the annual expenses incurred. Both the future and present values are calculated for illustration purposes.

Present Value The equivalent value of money at the present, based on the time value of money.

Future Value The equivalent value of money at a designated future date based on the time value of money.

3. Discussion and Recommendations

The cash flow projections in Table 3 illustrate recommended minimum annual contributions necessary to avoid any future short fall in the Reserve Fund. In order to calculate the minimum recommended annual contribution, the contribution is adjusted until the closing balance approaches zero funding for a critical year.

In order to keep the financial analysis in Table 3 to be accurate and up-to-date, this Reserve Fund Study should be reviewed and updated every three years. The importance of the review is to ensure the reserve fund study is a useful and relevant document to sustain with the ongoing fiscal policy of the Condominium Corporation.

Prepared by: __________________________________________

APPENDICES

APPENDIX A TABLE 1 - REPLACEMENT COST

SUMMARY

1 SITE WORKS1.1 HARD LANDSCAPING

1.1.1 Concrete Curbs $5,000 35 10 10 25 $1431.1.2 Pedestrian Walk $30,000 35 10 10 25 $8571.1.3 Exterior Signage $3,000 35 10 10 26 $86

2 STRUCTURE2.1 BUILDINGS

2.1.1 Sub-Structures $5,000 40 10 10 30 $1252.1.2 Superstructures $10,000 40 10 10 31 $2502.2 BASEMENT/UNDERGROUND GARAGE 10 10

2.2.1 Waterproofing Systems Replacement $20,000 30 10 10 20 $6672.2.2 Waterproofing Systems Repair $30,000 15 10 10 35 $2,0002.3 BALCONIES 10 10

2.3.1 Waterproofing Systems Replacement-Ph 1 $10,000 30 10 10 20 $3332.3.1 Waterproofing Systems Replacement-Ph 2 $10,000 30 10 10 21 $3332.3.1 Waterproofing Systems Replacement-Ph 3 $10,000 30 10 10 22 $3332.3.1 Waterproofing Systems Replacement-Ph 4 $10,000 30 10 10 23 $3332.3.1 Waterproofing Systems Replacement-Ph 5 $10,000 30 10 10 24 $3332.3.1 Waterproofing Systems Replacement-Ph 6 $10,000 30 10 10 25 $3332.3.2 Structural Systems Repair-Ph 1 $5,000 30 10 10 20 $1672.3.2 Structural Systems Repair-Ph 2 $5,000 30 10 10 21 $1672.3.2 Structural Systems Repair-Ph 3 $5,000 30 10 10 22 $1672.3.2 Structural Systems Repair-Ph 4 $5,000 30 10 10 23 $1672.3.2 Structural Systems Repair-Ph 5 $5,000 30 10 10 24 $1672.3.2 Structural Systems Repair-Ph 6 $5,000 30 10 10 25 $167

3 BUILDING ENVELOPE3.1 WALLS

3.1.1 Exterior Wall (Major Repairs)-Ph 1 $5,000 40 10 10 30 $1253.1.1 Exterior Wall (Major Repairs)-Ph 2 $5,000 40 10 10 31 $1253.2 COATINGS 10

3.2.1 Exterior Wall Painting $10,000 15 10 10 5 $6673.3 DOORS

3.3.1 Entrance Doors $1,000 30 10 10 20 $333.3.2 Service Doors $100 30 10 10 21 $33.3.3 Balcony Doors $50 30 10 10 22 $23.4 WINDOWS

3.4.1 Window System-Ph 1 $50 35 10 10 25 $13.4.1 Window System-Ph 2 $50 35 10 10 26 $13.4.1 Window System-Ph 3 $50 35 10 10 27 $13.4.1 Window System-Ph 4 $50 35 10 10 28 $13.5 MEMBRANES & SEALANTS

3.5.1 Cladding Joints $10,000 15 10 10 5 $6673.5.2 Windows and Doors Joints $10 15 10 10 6 $13.6 ROOFING

3.6.1 Roofing Systems-Ph 1 $5,000 25 10 10 15 $2003.6.2 Roofing Systems-Ph 2 $5,000 25 10 10 16 $2003.6.2 Roofing Systems-Ph 3 $5,000 25 10 10 17 $200

TABLE 1A - REPLACEMENT COST SUMMARY

METROPOLITAN TORONTO CONDOMINIUM CORPORATION No. XXXLOCATED AT: 123 XXXX ST, TORONTO, ONTARIO

Estimated Annual Contribution

Based On Normal Life

Item Number

Description of Common Element ItemsCurrent Repair or Replacement

Cost 2013

Normal Life Span

(Years)

Actual Age

(Years)

Effective Age

(Years)

Estimated Remaining Life Span

(Years)

4 MECHANICAL SYSTEMS4.1 SITE SYSTEMS

4.1.1 Water Main $5,000 30 10 10 20 $1674.2 DRAINAGE SYSTEMS

4.2.1 Sanitary Drainage Systems $500 30 10 10 21 $174.2.2 Storm Drainage Systems $500 30 10 10 22 $174.3 WATER SYSTEMS

4.3.1 Boilers $100 30 10 10 20 $34.3.2 Hot Water Storage Tanks $200 30 10 10 21 $74.3.3 Circulating & Booster Pumps $300 30 10 10 22 $104.3.4 Plumbing Fixtures $300 30 10 10 23 $104.3.5 Insulation $300 30 10 10 24 $104.4 HEATING SYSTEMS

4.4.1 Heating Systems $5,000 30 10 10 20 $1674.5 COOLING SYSTEMS

4.5.1 Cooling Systems $5,000 30 10 10 21 $1674.6 VENTILATION SYSTEMS 10 10

4.6.1 Ventilation Systems $5,000 30 22 $1674.7 WASTE DISPOSAL SYSTEMS 10 10

4.7.1 Garbage Compactor $6,000 20 10 10 10 $3005 ELECTRICAL SYSTEMS

5.1 ELECTRICAL SUPPLY & DISTRIBUTION5.1.1 Power Supply $5,000 30 10 10 20 $1675.1.2 Power Distribution $5,000 30 10 10 21 $1675.1.3 Panel Boards & Sub-Circuits $5,000 30 10 10 22 $1675.2 LIGHTING SYSTEMS

5.2.1 Building Common Areas $100 20 10 10 10 $55.2.2 Building Service Areas $100 20 10 10 11 $55.2.3 Exterior Lighting $100 20 10 10 12 $55.3 AUXILIARY SYSTEMS

5.3.1 Security Systems $500 20 10 10 10 $256 LIFE SAFETY SYSTEMS

6.1 FIRE DETECTION6.1.1 Fire Alarm Panel $400 20 0 0 20 $206.1.2 Annunciator $300 20 0 0 20 $156.1.3 Detection Devices $300 20 0 0 20 $156.1.4 Signal Devices $40 20 0 0 20 $26.2 SPRINKLER SYSTEMS

6.2.1 Standpipe & Siamese Connection $1 20 5 5 15 $06.2.2 Fire Pump $1 20 5 5 15 $06.2.3 Fire Hose Cabinets $1 20 5 5 15 $06.2.4 Distribution (Piping, Valves and Heads) $1 20 5 5 15 $0

7 ELEVATORS7.1 ELEVATOR UPGRADES/REPLACEMENTS

7.1.1 Equipment Upgrades/Partial Replacements $260,000 20 10 10 10 $13,000

Effective Age

(Years)

Estimated Remaining Life Span

(Years)

Estimated Annual Contribution

Based On Normal Life

Item Number

Description of Common Element ItemsCurrent Repair or Replacement

Cost 2013

Normal Life Span

(Years)

Actual Age

(Years)

TABLE 1B - REPLACEMENT COST SUMMARY (CONT.)

METROPOLITAN TORONTO CONDOMINIUM CORPORATION No. XXXLOCATED AT: 123 XXXX ST, TORONTO, ONTARIO

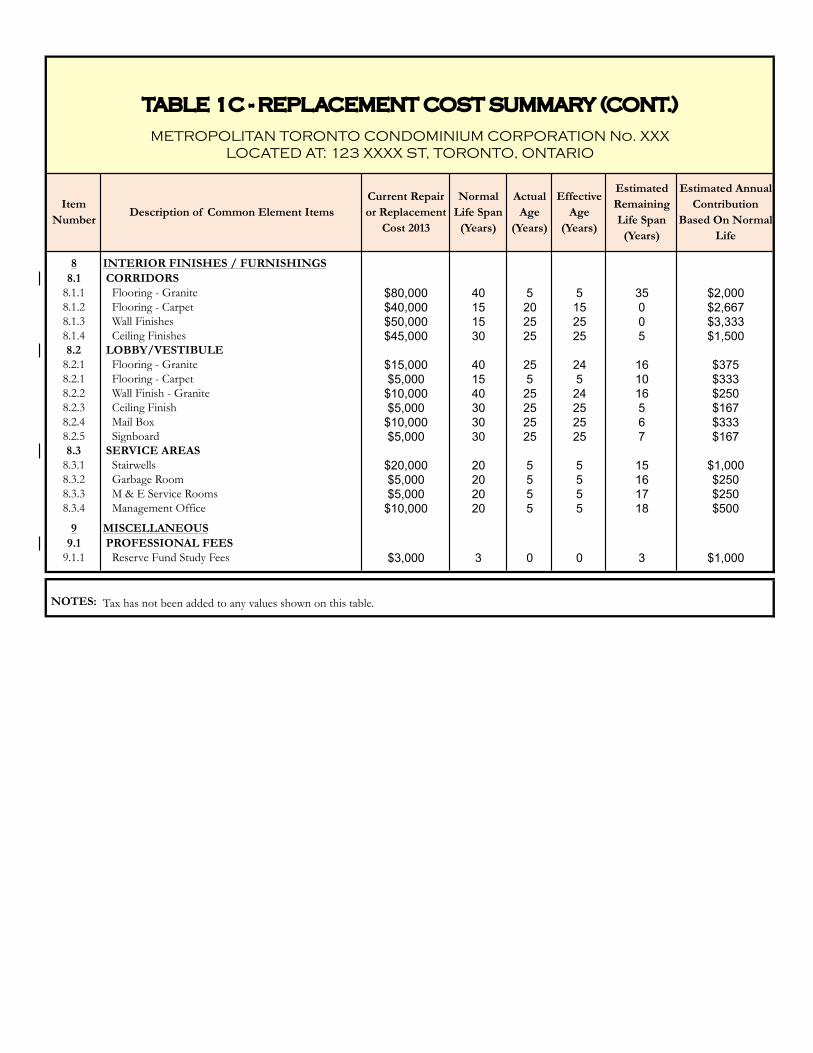

8 INTERIOR FINISHES / FURNISHINGS8.1 CORRIDORS

8.1.1 Flooring - Granite $80,000 40 5 5 35 $2,0008.1.2 Flooring - Carpet $40,000 15 20 15 0 $2,6678.1.3 Wall Finishes $50,000 15 25 25 0 $3,3338.1.4 Ceiling Finishes $45,000 30 25 25 5 $1,5008.2 LOBBY/VESTIBULE

8.2.1 Flooring - Granite $15,000 40 25 24 16 $3758.2.1 Flooring - Carpet $5,000 15 5 5 10 $3338.2.2 Wall Finish - Granite $10,000 40 25 24 16 $2508.2.3 Ceiling Finish $5,000 30 25 25 5 $1678.2.4 Mail Box $10,000 30 25 25 6 $3338.2.5 Signboard $5,000 30 25 25 7 $1678.3 SERVICE AREAS

8.3.1 Stairwells $20,000 20 5 5 15 $1,0008.3.2 Garbage Room $5,000 20 5 5 16 $2508.3.3 M & E Service Rooms $5,000 20 5 5 17 $2508.3.4 Management Office $10,000 20 5 5 18 $500

9 MISCELLANEOUS9.1 PROFESSIONAL FEES

9.1.1 Reserve Fund Study Fees $3,000 3 0 0 3 $1,000

NOTES: Tax has not been added to any values shown on this table.

TABLE 1C - REPLACEMENT COST SUMMARY (CONT.)

METROPOLITAN TORONTO CONDOMINIUM CORPORATION No. XXXLOCATED AT: 123 XXXX ST, TORONTO, ONTARIO

Item Number

Description of Common Element ItemsCurrent Repair or Replacement

Cost 2013

Normal Life Span

(Years)

Actual Age

(Years)

Effective Age

(Years)

Estimated Remaining Life Span

(Years)

Estimated Annual Contribution

Based On Normal Life

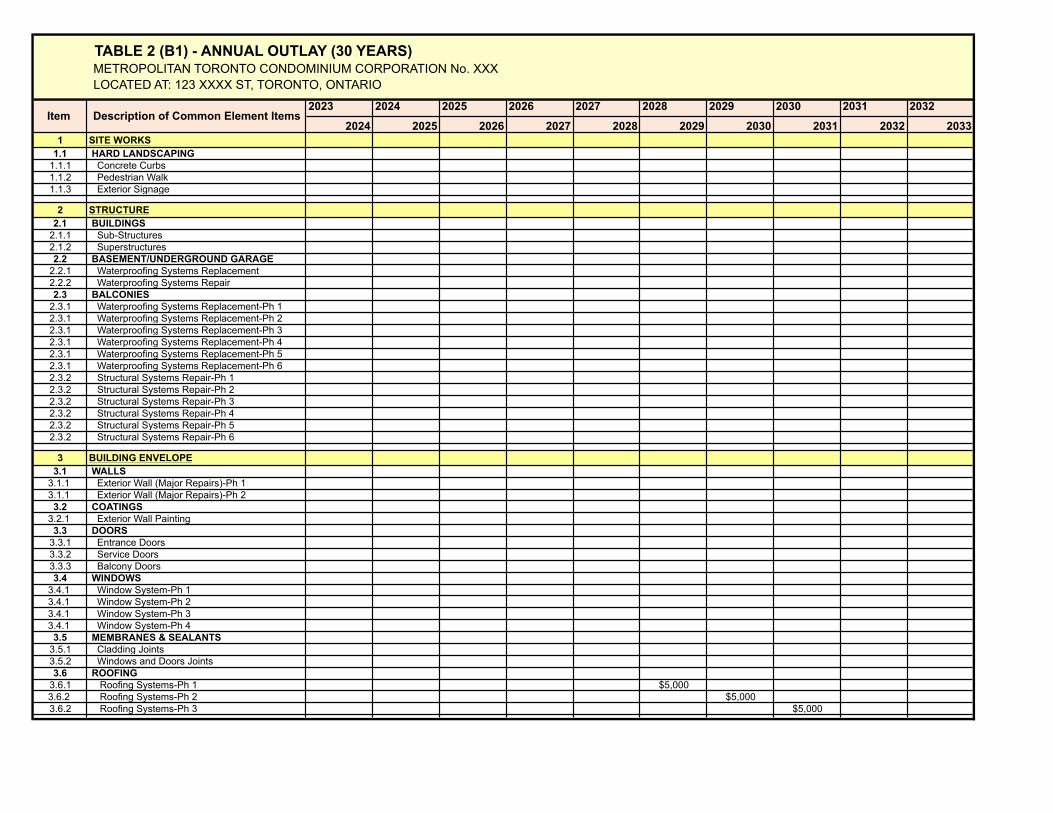

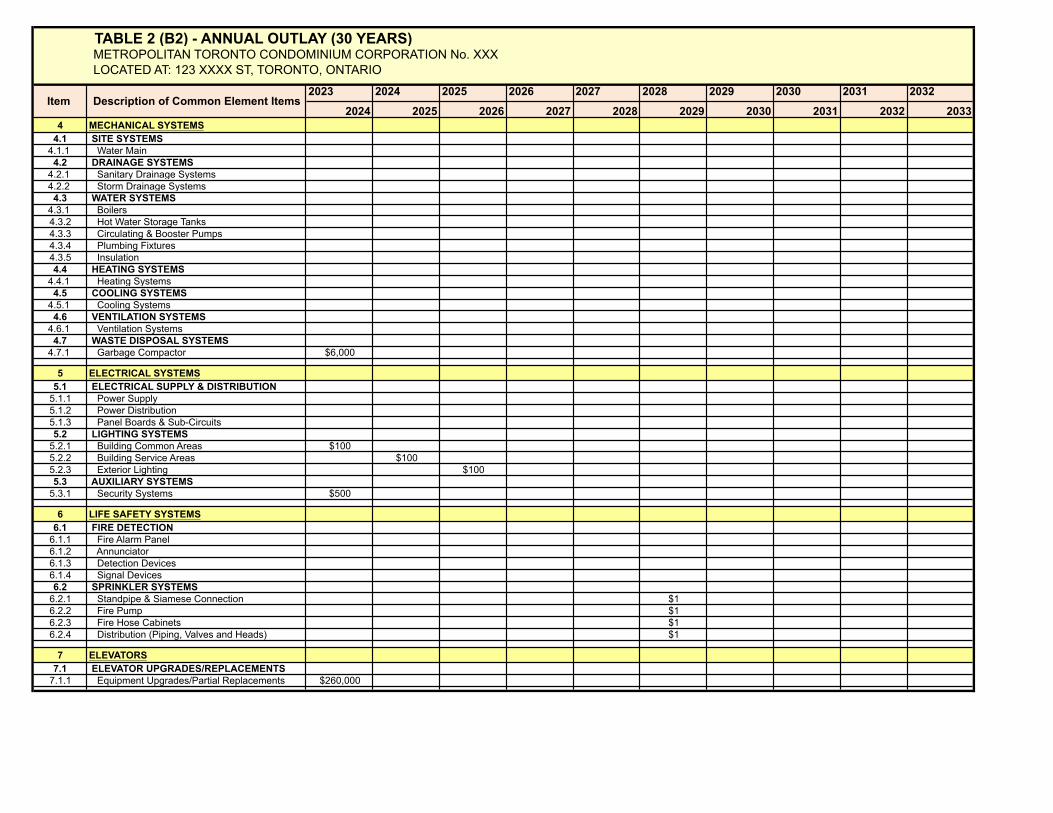

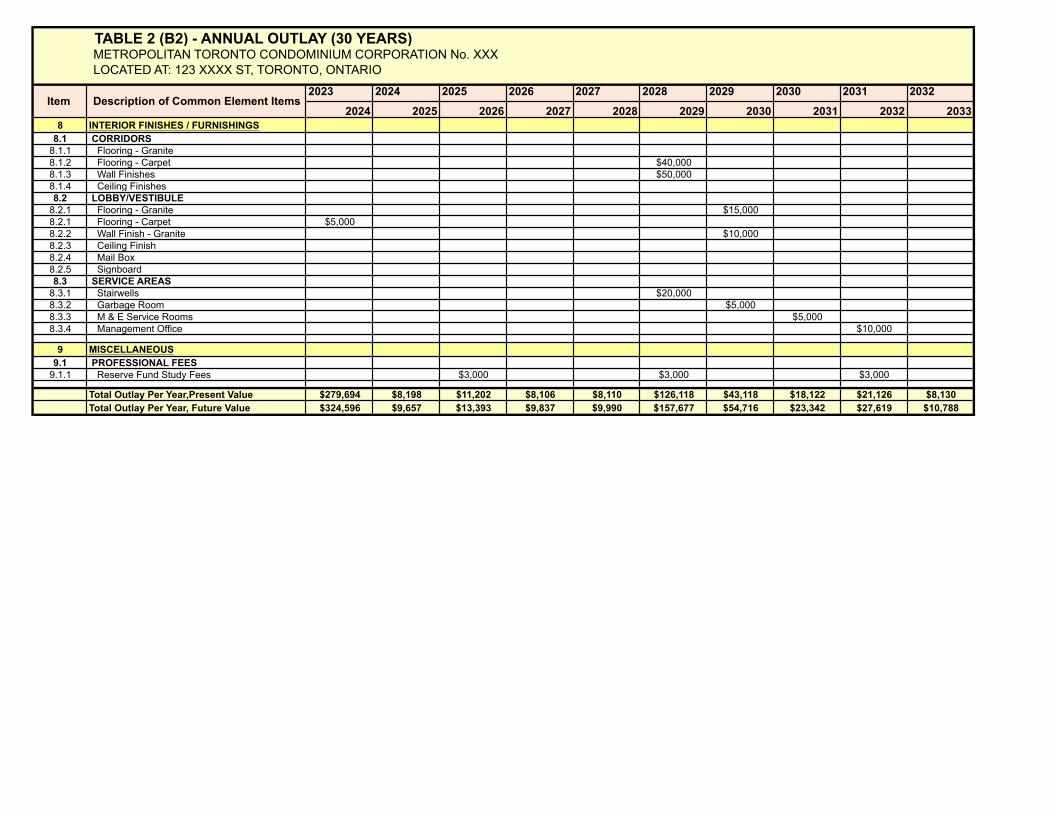

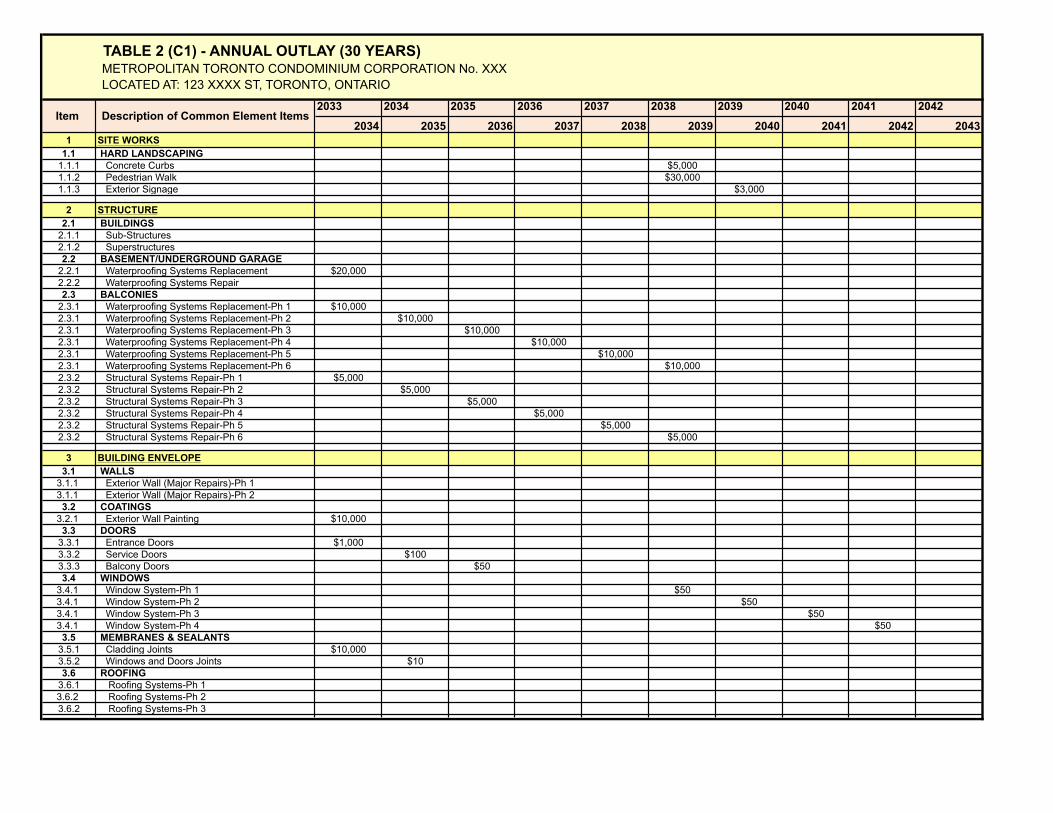

APPENDIX B TABLE 2 - ANNUAL OUTLAY

(30 YEARS)

TABLE 2 (A1) - ANNUAL OUTLAY (30 YEARS)METROPOLITAN TORONTO CONDOMINIUM CORPORATION No. XXXLOCATED AT: 123 XXXX ST, TORONTO, ONTARIO

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

2014 2015 2016 2017 2018 2019 2020 2021 2022 20231 SITE WORKS

1.1 HARD LANDSCAPING1.1.1 Concrete Curbs1.1.2 Pedestrian Walk1.1.3 Exterior Signage

2 STRUCTURE2.1 BUILDINGS

2.1.1 Sub-Structures2.1.2 Superstructures2.2 BASEMENT/UNDERGROUND GARAGE

2.2.1 Waterproofing Systems Replacement2.2.2 Waterproofing Systems Repair2.3 BALCONIES