Rio Grande City Consolidated Independent School District

BUDGET FOR THE YEAR 2014-2015 September 1, 2014 to August 31, 2015

BOARD OF TRUSTEES

Basilio D. Villarreal Jr., President Roberto Gutierrez, Vice President

Cesar Gonzalez, Secretary Daniel J. Garcia, Member Noe R. Gonzalez, Member

Ruben Klein, Member Leonel Lopez, Member

ADMINISTRATIVE STAFF

Roel A. Gonzalez ~ Superintendent of Schools Vilma Garza ~ Assistant Superintendent for Curriculum & Instruction

Adolfo Peña ~ Assistant Superintendent– West Thelma Ruelas ~ Assistant Superintendent for Finance & Operations

Arcadio Salinas ~ Assistant Superintendent for Human Resources Joel Trigo ~ Assistant Superintendent– East

Office of Business & Operations 1 S Fort Ringgold

Rio Grande City, TX 78582

PAGE INTENTIONALLY LEFT BLANK

RIO GRANDE CITY CISD 2014-2015 BUDGET MANUAL

TABLE OF CONTENTS

ORGANIZATIONAL SECTION Budget and Financial Policies …………………………………………… 1

Budget Process…………………………………………………………… 7

Budget Calendar………………………………………………………….. 10

BUDGET PREPARTION SECTIONS Budget Worksheet……………………………………………………....... 11

Budget Amendment Form………………………………………………... 16

INFORMATIONAL SECTION Overview of Account Codes……………………………………………... 18

Basic System Code Composition………………………………………… 19

Fund Codes………………………………………………………………. 20

Function Codes…………………………………………………………… 21

Object Codes……………………………………………………………... 22

Sub Object Codes………………………………………………………… 23

Organization Codes………………………………………………………. 24

Fiscal Year Codes………………………………………………………... 25

Project Codes…………………………………………………………….. 26

PAGE INTENTIONALLY LEFT BLANK

Business Office Staff & Fund Assignments

Thelma Ruelas, Assistant Superintendent for Finance & Operations….………… 716-6711 Oneida Balderas, Compliance Auditor……………………………………………… 716-6706 Ludivina Cansino, Accounting Supervisor…………………………………………. 716-6727 199- General Fund

211- Title I, Part A ~ Improving Basic Programs

212- Title I, Part C ~ Migrant

224- IDEA Part B Formula

225- IDEA Part B Preschool

255- Title II Part A ~ TPTR

410- Instructional Materials Allotment Lourdes Luna, Accountant………………………..………………………………….. 716-6947 101- Food Service 220- Adult Literacy Education 244- Vocational Education 263- Title III, Part A ~ LEP & Immigrant 265- 21st Century CCLC Cycle 270- Rural and Low Income 274- GEAR UP Juan Ruiz, Data Programmer……………………..………………………………….. 716-6708

Alio System

Business Office Supporting Staff

Nancy Alaniz…………………….…...………………………...……………………… 716-6710 Susie Castillo…………………..………………………….…………………………… 716-6846 Emily Clarke……………………………………………….………………………….. 716-6761 Amparo Treviño………………………………………………………………………. 716-6711

PAGE INTENTIONALLY LEFT BLANK

ORGANIZATIONAL SECTION

PAGE INTENTIONALLY LEFT BLANK

2014-2015 Budget Manual 1

BUDGET & FINANCIAL POLICIES

LEGAL REQUIREMENTS Legal requirements for school district budgets are formulated by the Texas Educa-tion Agency, and the local district. In addition to these requirements, individual school districts also may have their own legal requirements for budget preparation. Additional legal requirements also may be imposed by state and federal grants. STATEMENT OF TEXAS LAW Sections 44.002 through 44.006 of the Texas Education Code establish the legal basis for budget development in school districts. The following six items summarize the legal requirements from the code: • The superintendent is the budget officer for the district and prepares or causes

the budget to be prepared. Note: TEA recommends that an interactive approach between the board of trustees and the superintendent be taken to establish the budget process and define related roles and responsibilities. • The district budget must be prepared by a date set by the state board of educa-

tion, currently August 20 (June 19 if the district uses a July 1 fiscal year start date).

• The president of the board of trustees must call a public meeting of the board of

trustees, giving ten days public notice in a newspaper, for the adoption of the district budget. Any taxpayer in the district may be present and participate in the meeting.

• No funds may be expended in any manner other than as provided for in the

adopted budget. The board does have the authority to amend the budget or adopt a supplementary emergency budget to cover unforeseen expenditures.

• The budget must be prepared in accordance with GAAP (generally accepted

accounting principles) and state guidelines. • The budget must be legally adopted before the adoption of the tax rate. How-

ever, if a school district has a July 1st fiscal year start date, then a school district must not adopt a tax rate until after the district receives the certified appraisal roll for the district required by Section 26.01, Tax Code. Additionally, a school district must publish a revised notice and hold another public meeting be-fore the district may adopt a tax rate that exceeds the following: (1) The rate proposed in the notice prepared using the estimate; or (2) The district’s rollback rate determined under Section 26.08, Tax Code, using the certified appraisal roll.

TEA LEGAL REQUIREMENTS TEA has developed additional requirements for school district budget preparation as follows:

2014-2015 Budget Manual 2

BUDGET & FINANCIAL POLICIES

• The budget must be adopted by the board of trustees, inclusive of amendments, no later than August 31 (June 30 if the district uses a July 1 fiscal year start date).

• Minutes from district board meetings will be used by TEA to record adoption of

and amendments to the budget. • Budgets for the General Fund, the Food Service Fund (whether accounted for in

the General Fund, a Special Revenue Fund or Enterprise Fund) and the Debt Service Fund must be included in the official district budget (legal or fiscal year basis). These budgets must be prepared and approved at least at the fund and function levels to comply with the state’s legal level of control mandates. Funds to be budgeted and reported through PEIMS, both required and optional, are shown in Exhibit 2. Note: Districts may prepare and approve budgets for other funds and/or with even greater detail at their discretion. Such local decisions may affect the need for budget amendments and financial reporting

requirements. • The officially adopted district budget, as amended, must be filed with TEA

through PEIMS (Public Education Information Management System) by the date prescribed in the annual system guidelines. Revenues, other sources, other uses, and fund balances must be reported by fund, object (at the fourth level), fiscal year, and amount. Expenditures must be reported by fund, function, object (at the second level), organization, fiscal year, program intent and amount. These requirements are discussed in further detail in the Data Collection and Reporting module.

• A school district must amend the official budget before exceeding a functional

expenditure category, i.e., instruction, administration, etc., in the total district budget. The annual financial and compliance report should reflect the amended budget amounts on the schedule comparing budgeted and actual amounts. The requirement for filing the amended budget with TEA is satisfied when the school district files its Annual Financial and Compliance Report.

LOCAL DISTRICT REQUIREMENTS In addition to state legal requirements the Rio Grande City CISD Board of Trustees have established their own requirements for annual budget preparation through Board Policy CE (LEGAL AND LOCAL) Annual Operating Budget. ANNUAL OPERATING BUDGET CE (LEGAL) AUTHORIZED EXPENDITURES The District shall not lend its credit or gratuitously grant public money or things of value in aid of any individual, association, or corporation. Tex. Const. Art. III, Sec. 52; Brazoria County v. Perry, 537 S.W.2d 89 (Tex. Civ. App.-Houston [1st Dist.] 1976, no writ) The District shall not grant any extra compensation, fee, or allowance to a public

2014-2015 Budget Manual 3

BUDGET & FINANCIAL POLICIES

officer, agent, servant, or contractor after service has been rendered or a contract entered into and performed in whole or in part. Nor shall the District pay or author-ize the payment of any claim against the District under any agreement or contract made without authority of law. Tex. Const. Art. III, Sec. 53; Harlingen ISD v. C.H. Page and Bro. 48 S.W.2d 983 (Comm. App. 1932) The state and county available funds disbursed to the District shall be used exclu-sively for salaries of professional certified staff and for interest on money borrowed on short time to pay such salaries, when salaries become due before school funds for the current year become available. Loans for paying professional certified staff salaries may not be paid out of funds other than those for the current year. Education Code 45.105(b) Local funds from District taxes, tuition fees, other local sources, and state funds not designated for a specific purpose may be used for salaries of any personnel and for purchasing appliances and supplies; for the payment of insurance premiums; for buying school sites; for buying, building, repairing, and renting school buildings, including acquisition of school buildings and sites by leasing through annual payments with an ultimate option to purchase [see CHG]; and for other purposes necessary in the conduct of the public schools to be determined by the Board. Education Code 45.105(c) No public funds of the District may be spent in any manner other than as provided for in the budget adopted by the Board. Education Code 44.006(a) COMMITMENT OF CURRENT REVENUE A contract for the acquisition, including lease, of real or personal property is a com-mitment of the District's current revenue only, provided the contract contains either or both of the following provisions: Retains to the Board the continuing right to terminate the contract at the expiration of each budget period during the term of the contract. Is conditioned on a best efforts attempt by the Board to obtain and appropriate funds for payment of the contract. FISCAL YEAR The Board may determine if the District's fiscal year begins on July 1 or September 1 of each year. Education Code 44.0011 BUDGET PREPARATION The Superintendent shall prepare, or cause to be prepared, a proposed budget covering all estimated revenue and proposed expenditures of the District for the following fiscal year. Education Code 44.002

2014-2015 Budget Manual 4

BUDGET & FINANCIAL POLICIES

DEADLINES The proposed budget shall be prepared on or before a date set by the State Board of Education, currently August 20 (June 19 if the District uses a July 1 fiscal year start date). Education Code 44.002(a); 19 TAC 109.1(a), 109.41 The adopted budget must be filed with the Texas Education Agency on or before the date established in the Financial Accountability System Resource Guide. Education Code 44.005; 19 TAC 109.1(a) PUBLIC MEETING ON BUDGET AND PROPOSED TAX RATE After the proposed budget has been prepared, the Board President shall call a Board meeting for the purpose of adopting a budget for the succeeding fiscal year. Any taxpayer of the District may be present and participate in the meeting. Education Code 44.004 [See CCG for provisions governing tax rate adoption] The meeting must comply with the notice requirements of the Open Meetings Act. Gov't Code 551.041, 551.043 PUBLISHED NOTICE The Board President shall also provide for publication of notice of the budget and proposed tax rate meeting in a daily, weekly, or biweekly newspaper published in the District. If no daily, weekly, or biweekly newspaper is published in the District, the President shall provide for publication of notice in at least one newspaper of general circulation in the county in which the District's central administrative office is located. The notice shall be published not earlier than the 30th day or later than the tenth day before the date of the hearing. FORM OF NOTICE The published notice of the public meeting to discuss and adopt the budget and the proposed tax rate must meet the size, format, and content requirements dictated by law. The notice is not valid if it does not substantially conform to the language and format prescribed by the comptroller. TAXPAYER INJUCTION If the District has not complied with the published notice requirements in the FORM OF NOTICE described above, and the requirements for DISTRICTS WITH JULY 1 FISCAL YEAR below, if applicable, and the failure to comply was not in good faith, a person who owns taxable property in the District is entitled to an injunction restraining the collection of taxes by the District. An action to enjoin the collection of taxes must be filed before the date the District delivers substantially all of its tax bills. Education Code 44.004

2014-2015 Budget Manual 5

BUDGET & FINANCIAL POLICIES

BUDGET ADOPTION The Board shall adopt a budget to cover all expenditures for the succeeding fiscal year at the meeting called for that purpose and before the adoption of the tax rate for the tax year in which the fiscal year covered by the budget begins. AMENDMENT OF APPROVED BUDGET The Board shall have the authority to amend the approved budget or to adopt a supplementary emergency budget to cover necessary unforeseen expenses. Copies of any amendment or supplementary budget must be prepared and filed in accordance with State Board rules. Education Code 44.006 CERTAIN DONATIONS The District may donate funds or other property or service to the adjutant general's department or to the Texas National Guard. Gov't Code 431.035(b), 431.045(b) ANNUAL OPERATING BUDGET CE (LOCAL) FISCAL YEAR The District shall operate on a fiscal year beginning September 1 and ending August 31. BUDGET PLANNING Budget planning shall be an integral part of overall program planning so that the budget effectively reflects the District's programs and activities and provides the resources to implement them. In the budget planning process, general educational goals, specific program goals, and alternatives for achieving program goals shall be considered, as well as input from the District- and campus-level planning and deci-sion-making committees. Budget planning and evaluation are continuous processes and shall be a part of each month's activities. AVAILABILITY OF PROPOSED BUDGET After it is presented to the Board and prior to adoption, a copy of the proposed budget shall be available upon request from the business office or Superintendent. The Superintendent or designee shall be available to answer questions arising from inspection of the budget. BUDGET MEETING The annual public meeting to discuss the proposed budget and tax rate shall be conducted as follows:

2014-2015 Budget Manual 6

BUDGET & FINANCIAL POLICIES

1. The Board President shall request at the beginning of the meeting that all per-sons who desire to speak on the proposed budget and/or tax rate sign up on the sheet provided.

2. Prior to the beginning of the meeting, the Board may establish time limits for speakers.

3. Speakers shall confine their remarks to the appropriation of funds as contained in the proposed budget and/or the tax rate.

4. No officer or employee of the District shall be required to respond to questions from speakers at the meeting.

AUTHORIZED EXPENDITURES The adopted budget provides authority to expend funds for the purposes indicated and in accordance with state law, Board policy, and the District's approved purchas-ing procedures. The expenditure of funds shall be under the direction of the Super-intendent or designee who shall ensure that funds are expended in accordance with the adopted budget. BUDGET AMENDMENTS The budget shall be amended when a change is made increasing any one of the functional spending categories or increasing revenue object accounts and other resources.

2014-2015 Budget Manual 7

BUDGET PROCESS

OBJECTIVES OF BUDGETING The objectives of budgeting are outlined by the Texas Education Agency in the Financial Accountability System Resource Guide. Performance evaluation allows citizens and taxpayers to hold policy makers and administrators accountable for their actions. Because accountability to citizens often is stated explicitly in state laws and constitutions, it is considered a cornerstone of budgeting and financial reporting. The Governmental Accounting Standards Board (GASB) recognizes its importance with these objectives in its GASB Concepts Statement No. 1 (Section 100.177): • Financial reporting should provide information to determine whether current-

year revenues were sufficient to pay for current-year services.

• Financial reporting should demonstrate whether resources were obtained and used in accordance with the entity’s legally adopted budget. It should also

• demonstrate compliance with other finance-related legal or contractual require-ments.

• Financial reporting should provide information to assist users in assessing the

service efforts, costs and accomplishments of the governmental entity.

Meeting these objectives requires budget preparation to include several concepts recognizing accountability. Often these concepts have been mandated for state and local public sector budgets. They include requirements that budgets should: • Be balanced so that current revenues are sufficient to pay for current services. • Be prepared in accordance with all applicable federal, state, and local legal

mandates and requirements. • Provide a basis for the evaluation of a government’s service efforts, costs and

accomplishments. Note: Although the objective of balanced budgets is generally applicable to all school districts to ensure long-term fiscal health, variations of this objective which are considered appropriate for some school districts over short-term periods are available. For example, the balanced budget objective may be met through the use of fund balance reserves to pay for current services during certain periods. Such uses of fund balance reserves must be in accordance with applicable state and local fund balance policies.

2014-2015 Budget Manual 8

BUDGET PROCESS

BUDGET PROCESS OVERVIEW The budgeting process is comprised of three major phases: planning, preparation and evaluation. The budgetary process begins with sound planning. Planning defines the goals and objectives of campuses and the school district and develops programs to attain those goals and objectives. Once these programs and plans have been estab-lished, budgetary resource allocations are made to support them. Budgetary resource allocations are the preparation phase of budgeting. The allocations cannot be made, however, until plans and programs have been established. Finally, the budget is evaluated for its effectiveness in attaining goals and objectives. Evaluation typically involves an examination of: how funds were expended, what outcomes resulted from the expenditure of funds, and to what degree these outcomes achieved the objectives stated during the planning phase. This evaluation phase is important in determining the following year’s budgetary allocations. In summary, budget preparation is not a one-time exercise to determine how a school district will allocate funds. Rather, school district budget preparation is part of a continuous cycle of planning and evaluation to achieve district goals. BUDGET PLANNING The first phase of the Budget Development Process is planning. Planning involves defining the mission, goals and objectives of campuses, departments, and the district. Importance is placed upon sound budget planning for the following reasons; • In implementing the type, quantity, and quality of school district instruction, the

budget becomes the limiting force. • Providing quality education is very important to the public interest. • The scope and adversity of school district operations make comprehensive plan-

ning necessary for good decision-making. • Planning is a process that is critical to the expression of citizen preferences and

through with consensus is reached among citizens, school board members, and district/campus/department staff on the future direction of a district’s operations.

BUDGET PREPARATION Budget Preparation begins with a training session with principals and program man-agers. At that time the Budget Manual and budget worksheets are distributed. The District uses site-based budgeting to enhance the ability of principals to serve as effective instructional leaders. Site-based budgeting places the principals at the center of the budget preparation process. The Campus Budget reflects the initial campus funding allocations. Pupil allocations are based on peak enrollment for general fund allocation and special populations are based on PEIMS October snap shot date.

2014-2015 Budget Manual 9

BUDGET PROCESS

EVALUATION PHASE Evaluation is the last step of the district’s budget cycle. Information is compiled and analyzed to assess the performance of each individual department and campus, as well as the District as a whole. This information is a fundamental part of the planning phase for the following budget year.

2014-2015 Budget Manual 10

BUDGET CALENDAR

RIO GRANDE CITY CONSOLIDATED SCHOOL DISTRICT TENTATIVE BUDGET DEVELOPMENT CALENDAR

Target Date Activity/Process

February 11, 2014 Budget process approved

February 13, 2014 Projected enrollment developed

February 25, 2014 Budget process outlined to principals

February 27, 2014 Budget process outlined to program directors

March 4, 2014 Budget process outlined to secretaries

March 5,2014 Begin budget preparation for campuses, special programs and support services. Individual campus and department training will be scheduled

March 6, 2014 Review personnel staffing and proposed salary schedule

March 7, 2014 Begin special program and support service budget preparation

April 4, 2014 Completion of campus budgets

April 7, 2014 Initiate review of campus/department budgets and non-

allocated requests

April 11, 2014 Complete prioritization of non-allocated requests

April 14, 2014 Review of building maintenance, renovation and future con-struction schedule

April 21, 2014 Review projected revenue estimates

May 2, 2014 Complete first draft of district budget

May 7, 2014 Initiate superintendent’s review of preliminary district budget

May 12, 2014 Review personnel staffing and proposed salary schedule

May 19, 2014 Complete superintendent’s review of preliminary district

budget, personnel requirements, facility requirements and pro-jected revenue

May 19, 2014 Budget session with Board of Trustees Finance Committee

July 25, 2014 Receive certified values from Appraisal District

July 28, 2014 Complete final budget draft

July 29,2014 Budget session with Board of Trustees

August 6, 2014 Advertise for public hearing in newspaper

August 19, 2014 Official public budget hearing and tax rate public hearing

August 19, 2014 Adoption of 2014-2015 budget and tax rate

BUDGET PREPARATION SECTION

PAGE INTENTIONALLY LEFT BLANK

BUDGET WORKSHEET

2014-2015 Budget Manual 11

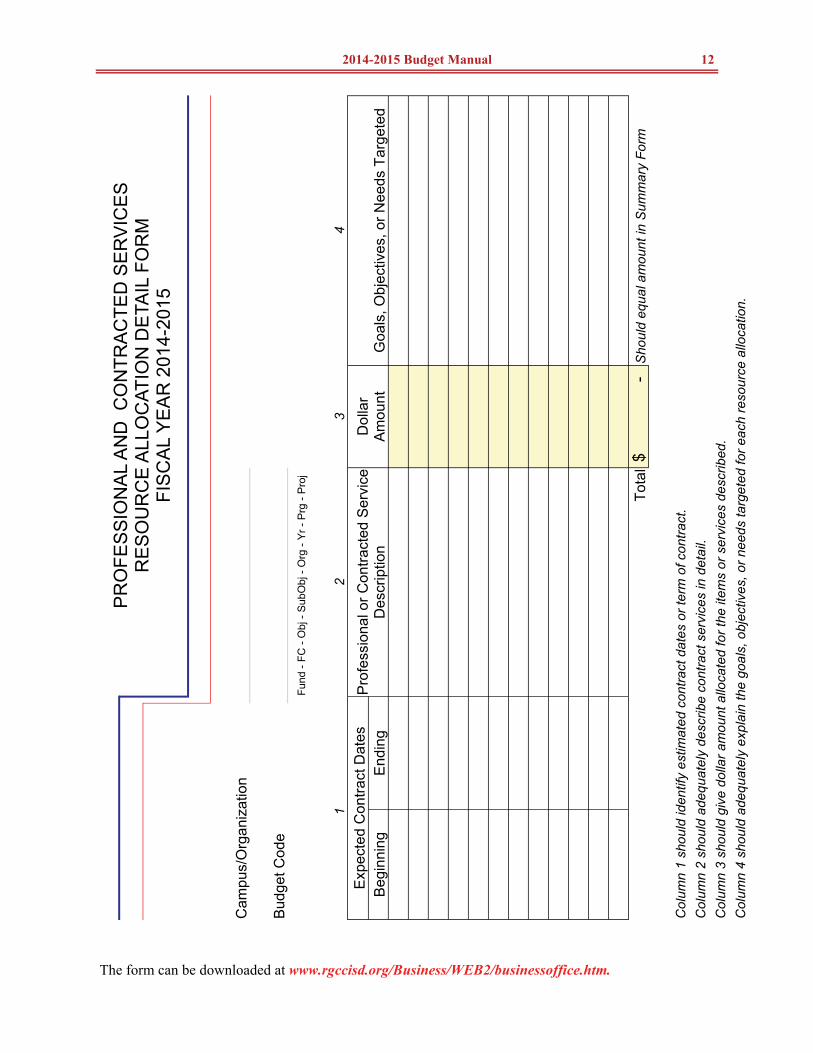

PURPOSE The Budget Worksheet is used for describing major program changes or any new programs. The forms can be downloaded at www.rgccisd.org/Business/WEB2/businessoffice.htm INSTRUCTIONS 1. Complete the Campus/Organization. 2. Complete Budget Code Section. If you have questions concerning account descriptions contact the Business Office. For reference, see the Financial Operating Guidelines at the District Web Page. Go to Business Office or www.rgccisd.org/Business/WEB2/businessoffice.htm 3. Complete the budget description, quantity, and dollar amount. 4. Describe the goals, objectives or needs targeted. Attach any necessary supporting documents.

2014-2015 Budget Manual 12

P

RO

FES

SIO

NA

L A

ND

CO

NTR

AC

TED

SE

RV

ICE

S

R

ES

OU

RC

E A

LLO

CAT

ION

DE

TAIL

FO

RM

FI

SC

AL

YE

AR

201

4-20

15

Cam

pus/

Org

aniz

atio

n

Bud

get C

ode

Fu

nd -

FC -

Obj

- S

ubO

bj -

Org

- Yr

- P

rg -

Pro

j

1

2

3 4

Exp

ecte

d C

ontra

ct D

ates

P

rofe

ssio

nal o

r Con

tract

ed S

ervi

ce

Des

crip

tion

Dol

lar

A

mou

nt

Goa

ls, O

bjec

tives

, or N

eeds

Tar

gete

d B

egin

ning

E

ndin

g

Tota

l $

- S

houl

d eq

ual a

mou

nt in

Sum

mar

y Fo

rm

C

olum

n 1

shou

ld id

entif

y es

timat

ed c

ontra

ct d

ates

or t

erm

of c

ontra

ct.

Col

umn

2 sh

ould

ade

quat

ely

desc

ribe

cont

ract

ser

vice

s in

det

ail.

Col

umn

3 sh

ould

giv

e do

llar a

mou

nt a

lloca

ted

for t

he it

ems

or s

ervi

ces

desc

ribed

.

Col

umn

4 sh

ould

ade

quat

ely

expl

ain

the

goal

s, o

bjec

tives

, or n

eeds

targ

eted

for e

ach

reso

urce

allo

catio

n.

The form can be downloaded at www.rgccisd.org/Business/WEB2/businessoffice.htm.

2014-2015 Budget Manual 13

S

UP

PLI

ES

AN

D M

ATE

RIA

LS

R

ES

OU

RC

E A

LLO

CAT

ION

DE

TAIL

FO

RM

FI

SC

AL

YE

AR

201

4-20

15

Cam

pus/

Org

aniz

atio

n

Bud

get C

ode

Fu

nd -

FC -

Obj

- S

ubO

bj -

Org

- Yr

- P

rg -

Pro

j

1

2

3 4

Exp

ecte

d C

ontra

ct D

ates

P

rofe

ssio

nal o

r Con

tract

ed S

ervi

ce

Des

crip

tion

Dol

lar

A

mou

nt

Goa

ls, O

bjec

tives

, or N

eeds

Tar

gete

d B

egin

ning

E

ndin

g

Tota

l $

- S

houl

d eq

ual a

mou

nt in

Sum

mar

y Fo

rm

C

olum

n 1

shou

ld id

entif

y es

timat

ed c

ontra

ct d

ates

or t

erm

of c

ontra

ct.

Col

umn

2 sh

ould

ade

quat

ely

desc

ribe

cont

ract

ser

vice

s in

det

ail.

Col

umn

3 sh

ould

giv

e do

llar a

mou

nt a

lloca

ted

for t

he it

ems

or s

ervi

ces

desc

ribed

.

Col

umn

4 sh

ould

ade

quat

ely

expl

ain

the

goal

s, o

bjec

tives

, or n

eeds

targ

eted

for e

ach

reso

urce

allo

catio

n.

The form can be downloaded at www.rgccisd.org/Business/WEB2/businessoffice.htm.

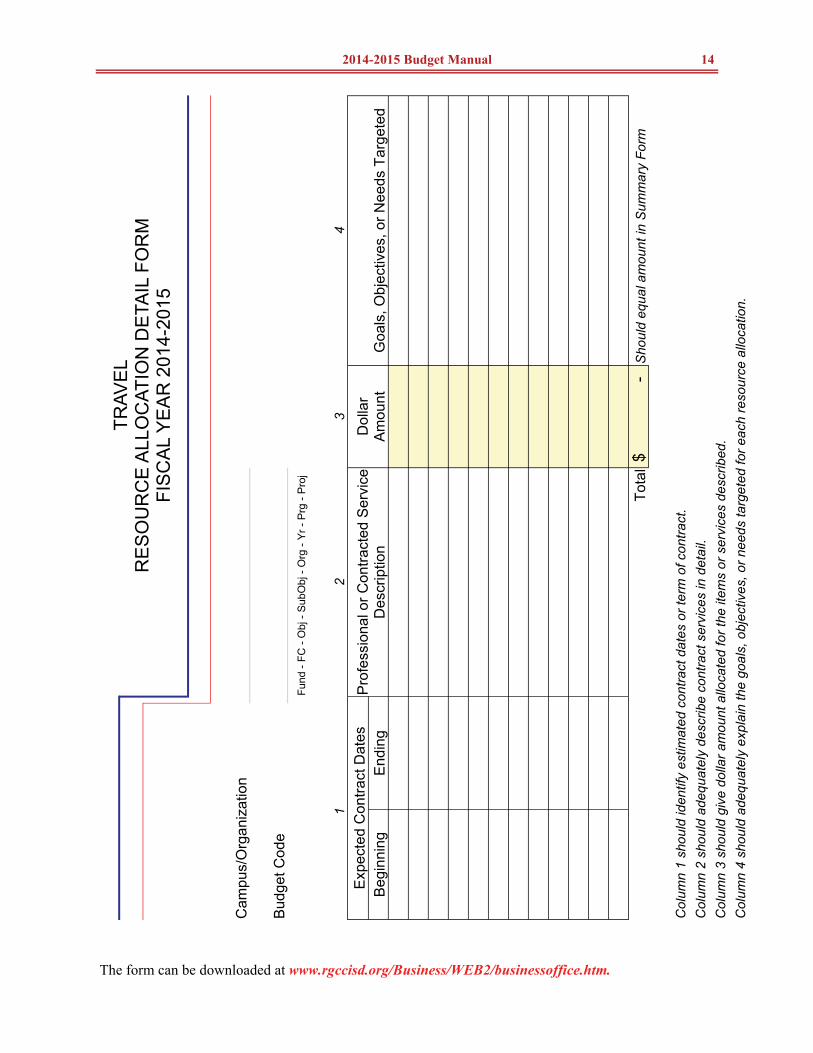

2014-2015 Budget Manual 14

TR

AVE

L

RE

SO

UR

CE

ALL

OC

ATIO

N D

ETA

IL F

OR

M

FIS

CA

L Y

EA

R 2

014-

2015

C

ampu

s/O

rgan

izat

ion

B

udge

t Cod

e

Fund

- FC

- O

bj -

Sub

Obj

- O

rg -

Yr -

Prg

- P

roj

1

2 3

4 E

xpec

ted

Con

tract

Dat

es

Pro

fess

iona

l or C

ontra

cted

Ser

vice

D

escr

iptio

n D

olla

r

Am

ount

G

oals

, Obj

ectiv

es, o

r Nee

ds T

arge

ted

Beg

inni

ng

End

ing

To

tal $

-

Sho

uld

equa

l am

ount

in S

umm

ary

Form

Col

umn

1 sh

ould

iden

tify

estim

ated

con

tract

dat

es o

r ter

m o

f con

tract

.

C

olum

n 2

shou

ld a

dequ

atel

y de

scrib

e co

ntra

ct s

ervi

ces

in d

etai

l.

C

olum

n 3

shou

ld g

ive

dolla

r am

ount

allo

cate

d fo

r the

item

s or

ser

vice

s de

scrib

ed.

C

olum

n 4

shou

ld a

dequ

atel

y ex

plai

n th

e go

als,

obj

ectiv

es, o

r nee

ds ta

rget

ed fo

r eac

h re

sour

ce a

lloca

tion.

The form can be downloaded at www.rgccisd.org/Business/WEB2/businessoffice.htm.

2014-2015 Budget Manual 15

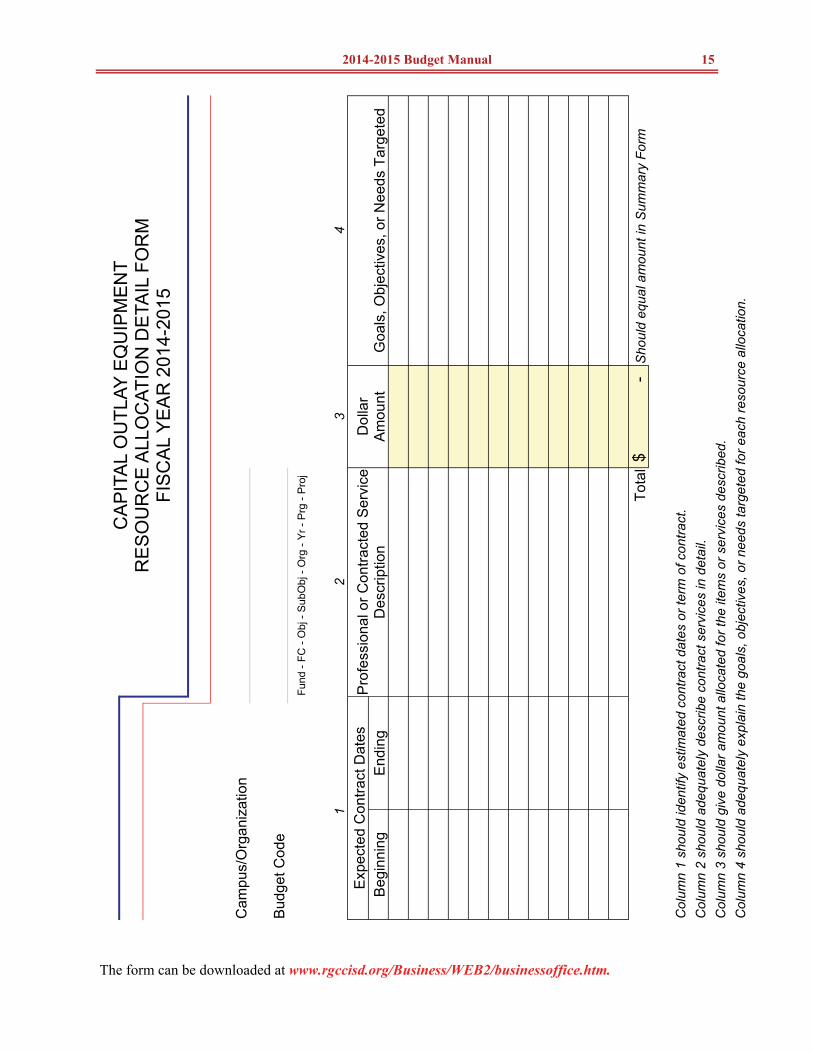

C

AP

ITA

L O

UTL

AY E

QU

IPM

EN

T

RE

SO

UR

CE

ALL

OC

ATIO

N D

ETA

IL F

OR

M

FIS

CA

L Y

EA

R 2

014-

2015

C

ampu

s/O

rgan

izat

ion

B

udge

t Cod

e

Fund

- FC

- O

bj -

Sub

Obj

- O

rg -

Yr -

Prg

- P

roj

1

2 3

4 E

xpec

ted

Con

tract

Dat

es

Pro

fess

iona

l or C

ontra

cted

Ser

vice

D

escr

iptio

n D

olla

r

Am

ount

G

oals

, Obj

ectiv

es, o

r Nee

ds T

arge

ted

Beg

inni

ng

End

ing

To

tal $

-

Sho

uld

equa

l am

ount

in S

umm

ary

Form

Col

umn

1 sh

ould

iden

tify

estim

ated

con

tract

dat

es o

r ter

m o

f con

tract

.

C

olum

n 2

shou

ld a

dequ

atel

y de

scrib

e co

ntra

ct s

ervi

ces

in d

etai

l.

C

olum

n 3

shou

ld g

ive

dolla

r am

ount

allo

cate

d fo

r the

item

s or

ser

vice

s de

scrib

ed.

C

olum

n 4

shou

ld a

dequ

atel

y ex

plai

n th

e go

als,

obj

ectiv

es, o

r nee

ds ta

rget

ed fo

r eac

h re

sour

ce a

lloca

tion.

The form can be downloaded at www.rgccisd.org/Business/WEB2/businessoffice.htm.

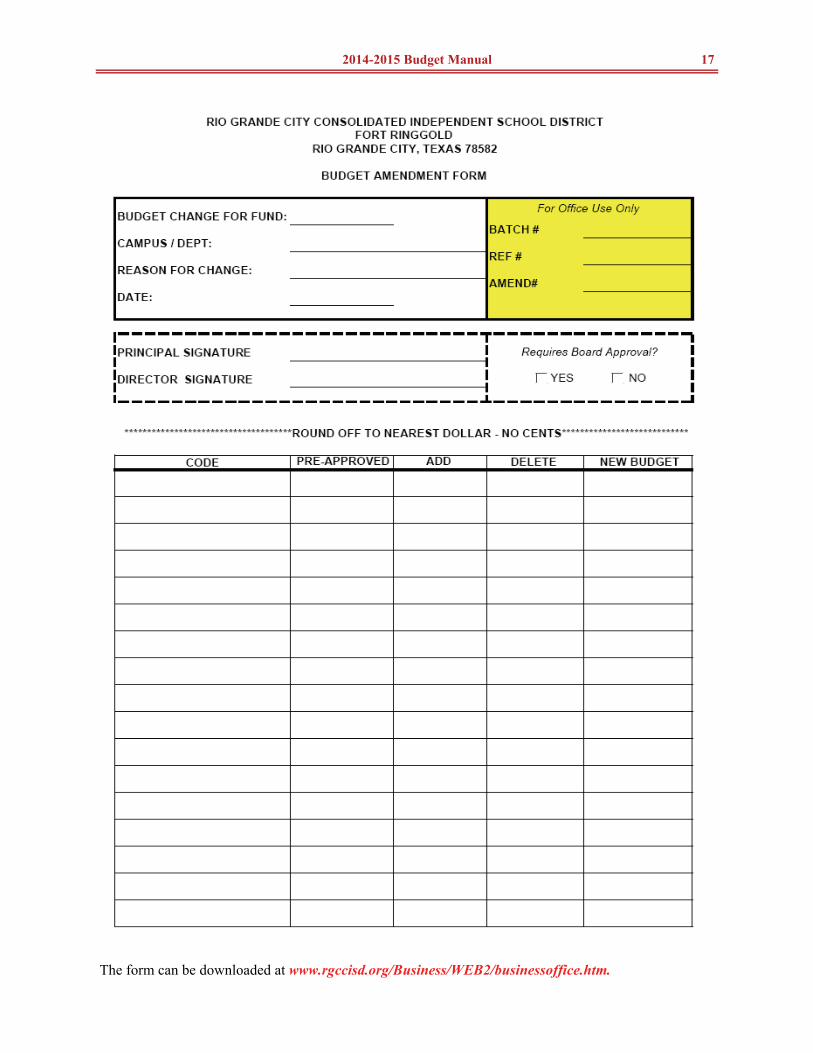

BUDGET TRANSFER FORM

2014-2015 Budget Manual 16

PURPOSE The Board of Trustees adopted district budget projects available resources and how those resources are to be channeled best meet students needs. Unforeseen events or changes in priorities which occur during the year often require redirection of funds. The budget is not intended to hinder these changes. Rather, established procedures allow for necessary amendments to the school district budget. Any amendments that would change budgeted fund or function totals at the district level require formal board approval. As a result, budget amendments at the campus level must be submitted for board approval when they affect fund or function at the district level. Principals and program budget managers have been granted the authority to move budgeted funds from one expenditure object to another within a function. INSTRUCTIONS Use the attached form for both amendments and transfers. Please ensure that re-quired information is included. The form can be downloaded at www.rgccisd.org/Business/WEB2/businessoffice.htm 1. 2. Forward Budget Amendments to the Business Office after it has been approved

by the principal and program director. 3. Budget Amendments that require the approval of the Board of Trustees will be

slowed by the mechanics of the agenda process. 4. Budget Amendments not requiring board approval will be processed as they are

received.

2014-2015 Budget Manual 17

The form can be downloaded at www.rgccisd.org/Business/WEB2/businessoffice.htm.

PAGE INTENTIONALLY LEFT BLANK

BUDGET PREPARATION SECTION

PAGE INTENTIONALLY LEFT BLANK

OVERVIEW OF ACCOUNT CODES

2014-2015 Budget Manual 18

Section 44.007 of the Texas Education Code (Code or TEC) requires that a standard school district fiscal accounting system be adopted by each school district. The system must meet at least the minimum requirements prescribed by the State Board of Education and also be subject to review and comment by the state auditor. Additionally, the accounting system must conform with Generally Accepted Accounting Principles (GAAP). This section further requires that a report be provided at the time that the school district budget is filed, showing financial information sufficient to enable the state board of education to monitor the funding process, and to determine educational system costs by school district, campus and program. The Texas Education Code, Section 44.008, requires each school district to have an annual independent audit conducted that meets the minimum requirements of the state board of education, subject to review and comment by the state auditor. The annual audit must in-clude the performance of certain audit procedures for the purpose of reviewing the accuracy of the fiscal information provided by the district through the Public Education Information Management System (PEIMS). The audit procedures are to be adequate to detect material errors in the school district’s fiscal data to be reported through the PEIMS system for the fiscal period under audit. A major purpose of the following accounting code structure is to establish the standard school district fiscal accounting system required by law. Although certain codes within the overview may be used at local option, the sequence of the codes within the structure, and the funds and chart of accounts, are to be uniformly used by all school districts in accordance with generally accepted accounting principles. The complete Financial Operating Guidelines can be downloaded at www.rgccisd.org/Business/WEB2/businessoffice.htm.

2014-2015 Budget Manual 19

BASIC SYSTEM CODE COMPOSITION

FUND CODE A mandatory 3 digit code is to be used for all financial transactions to identify the fund group and specific fund. The first digit refers to the fund group, and the second and third digit specifies the fund. Example: A Special Revenue Fund could be coded 211. The 2 indicates the Special Revenue Fund, the 11 specifies ESEA, Title I, Part A - Improving Basic Programs. FUNCTION CODE A mandatory 2 digit code applied to expenditures/ expenses that identify the purpose of the transaction. The first digit identifies the major class and the second digit refers to the specific function within the area. Example: The function "Health Service" is coded 33. The first 3 specifies Support Services - Student (Pupil) and the second 3 is Health Services. OBJECT CODE A mandatory 4 digit code identifying the nature and object of an account, a transaction or a source. The first of the four digits identifies the type of account or transaction, the second digit identifies the major area, and the third and fourth digits provide further sub-classifications. Example: Money received for current year taxes is classified in account 5711. The 5 denotes revenue, the 7 shows Local and Intermediate Sources, the 1 denotes local real and personal property taxes revenue and the final 1 specifies current year levy. SUBOBJECT CODE A 2 digit code for optional use to provide special accountability at the local level. ORGANIZATION CODE A mandatory 3 digit code identifying the organization, i.e., High School, Middle School, Elementary School, Superintendent’s office, etc. An organization code does not necessarily correspond with a physical location. The activity, not the location, defines the organization. Campuses are examples of organization codes and are specified for each school district in the Texas School Directory. Example: Expenditures for a high school might be classified as 001. This is a campus organization code that is defined in the Texas School Directory for that high school. FISCAL YEAR CODE A mandatory single digit code that identifies the fiscal year of the transaction or the project year of inception of a grant project. Examples: For the 05-06 fiscal year of the school district, a 6 would denote the fiscal year PROGRAM INTENT CODE A 2 digit code used to designate the intent of a program provided to students. These codes are used to account for the cost of instruction and other services that are directed toward a particular need of a specific set of students. The intent (the student group toward which the instructional or other service is directed) determines the program intent code, not the demographic makeup of the students served. Example: An entire class of physics is taught at the basic level. Program intent code 11 would designate Basic Educational Services. PROJECT CODE A 3 digit code that is used at the local option.

2014-2015 Budget Manual 20

FUND CODES

Fund Codes Description 100 General Fund

101 Food Service 161 Payroll Clearing 164 Accounts Payable Clearing 199 General Fund

200/300/400 Special Revenue Funds 211 ESEA, Title I, Part A, Helping Disadvantaged Children Meet High Standards 212 ESEA, Title I, Part C, Education for Migratory Children 220 Adult Education - English Literacy & Civics Education 224 IDEA-B, Formula 225 IDEA-B, Preschool Grant 244 Vocational Education-Basic Grant 255 Title II, Part A TPTR 263 Title III, Part A, LEP & Immigrant 265 21st Century CCLC Cycle 6 Year 5 270 Rural & Low Income 274 Gear Up 410 Instructional Facilities Allotment

500 Debt Service Funds 516 Debt Service - Series 2000/2002

600 Capital Projects Funds 623 Capital Projects

700-799 Proprietary Fund Types 753 Workers Compensation

800 Trust Funds 816 Scholarship Fund 817 Scholarship Fund 880 Tax Office 884 High School

900 Capital Assets and Long Term Debt 901 Fixed Assets 902 Long Term Debt

2014-2015 Budget Manual 21

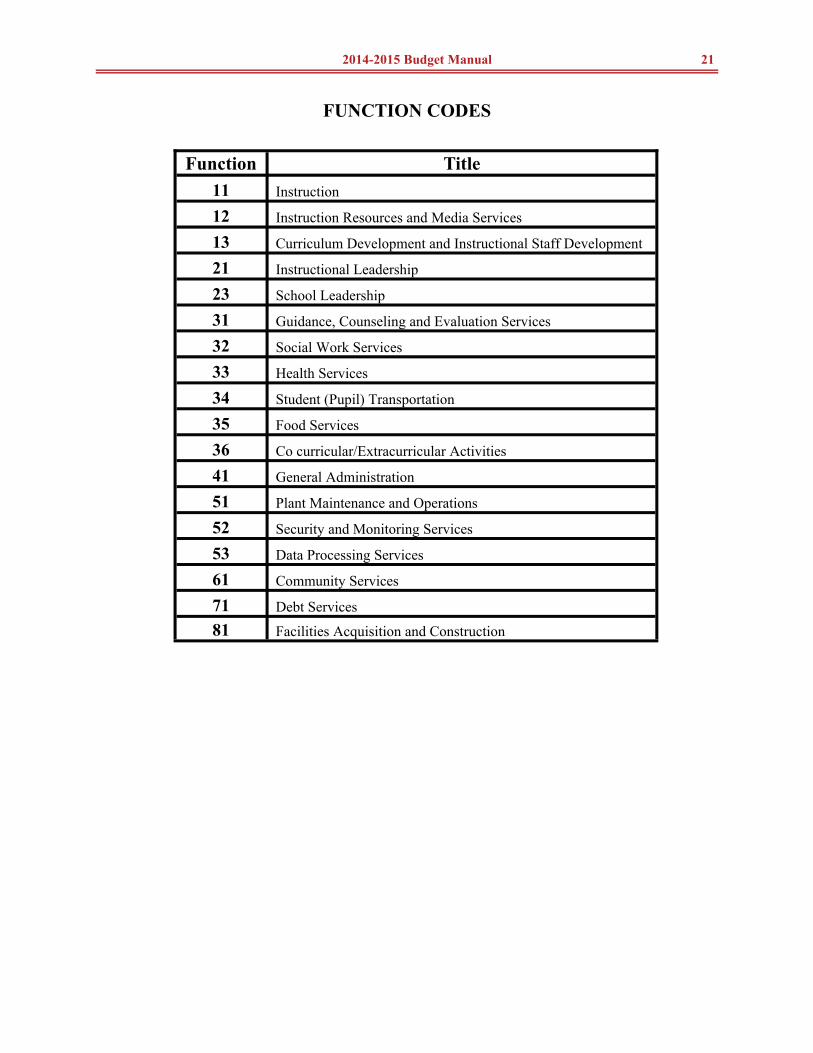

FUNCTION CODES Function Title

11 Instruction

12 Instruction Resources and Media Services

13 Curriculum Development and Instructional Staff Development

21 Instructional Leadership

23 School Leadership

31 Guidance, Counseling and Evaluation Services

32 Social Work Services

33 Health Services

34 Student (Pupil) Transportation

35 Food Services

36 Co curricular/Extracurricular Activities

41 General Administration

51 Plant Maintenance and Operations

52 Security and Monitoring Services

53 Data Processing Services

61 Community Services

71 Debt Services

81 Facilities Acquisition and Construction

2014-2015 Budget Manual 22

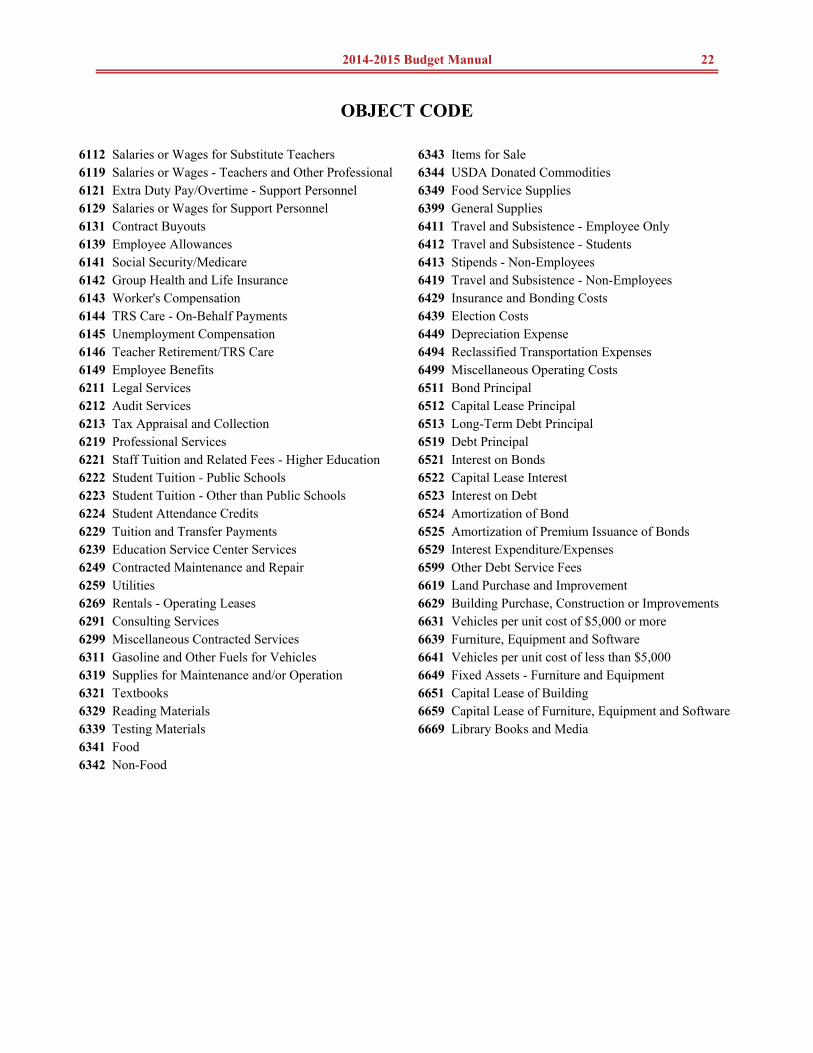

OBJECT CODE

6112 Salaries or Wages for Substitute Teachers 6343 Items for Sale 6119 Salaries or Wages - Teachers and Other Professional 6344 USDA Donated Commodities 6121 Extra Duty Pay/Overtime - Support Personnel 6349 Food Service Supplies 6129 Salaries or Wages for Support Personnel 6399 General Supplies 6131 Contract Buyouts 6411 Travel and Subsistence - Employee Only 6139 Employee Allowances 6412 Travel and Subsistence - Students 6141 Social Security/Medicare 6413 Stipends - Non-Employees 6142 Group Health and Life Insurance 6419 Travel and Subsistence - Non-Employees 6143 Worker's Compensation 6429 Insurance and Bonding Costs 6144 TRS Care - On-Behalf Payments 6439 Election Costs 6145 Unemployment Compensation 6449 Depreciation Expense 6146 Teacher Retirement/TRS Care 6494 Reclassified Transportation Expenses 6149 Employee Benefits 6499 Miscellaneous Operating Costs 6211 Legal Services 6511 Bond Principal 6212 Audit Services 6512 Capital Lease Principal 6213 Tax Appraisal and Collection 6513 Long-Term Debt Principal 6219 Professional Services 6519 Debt Principal 6221 Staff Tuition and Related Fees - Higher Education 6521 Interest on Bonds 6222 Student Tuition - Public Schools 6522 Capital Lease Interest 6223 Student Tuition - Other than Public Schools 6523 Interest on Debt 6224 Student Attendance Credits 6524 Amortization of Bond 6229 Tuition and Transfer Payments 6525 Amortization of Premium Issuance of Bonds 6239 Education Service Center Services 6529 Interest Expenditure/Expenses 6249 Contracted Maintenance and Repair 6599 Other Debt Service Fees 6259 Utilities 6619 Land Purchase and Improvement 6269 Rentals - Operating Leases 6629 Building Purchase, Construction or Improvements

6299 Miscellaneous Contracted Services 6639 Furniture, Equipment and Software 6311 Gasoline and Other Fuels for Vehicles 6641 Vehicles per unit cost of less than $5,000 6319 Supplies for Maintenance and/or Operation 6649 Fixed Assets - Furniture and Equipment 6321 Textbooks 6651 Capital Lease of Building 6329 Reading Materials 6659 Capital Lease of Furniture, Equipment and Software 6339 Testing Materials 6669 Library Books and Media 6341 Food 6342 Non-Food

6291 Consulting Services 6631 Vehicles per unit cost of $5,000 or more

2014-2015 Budget Manual 23

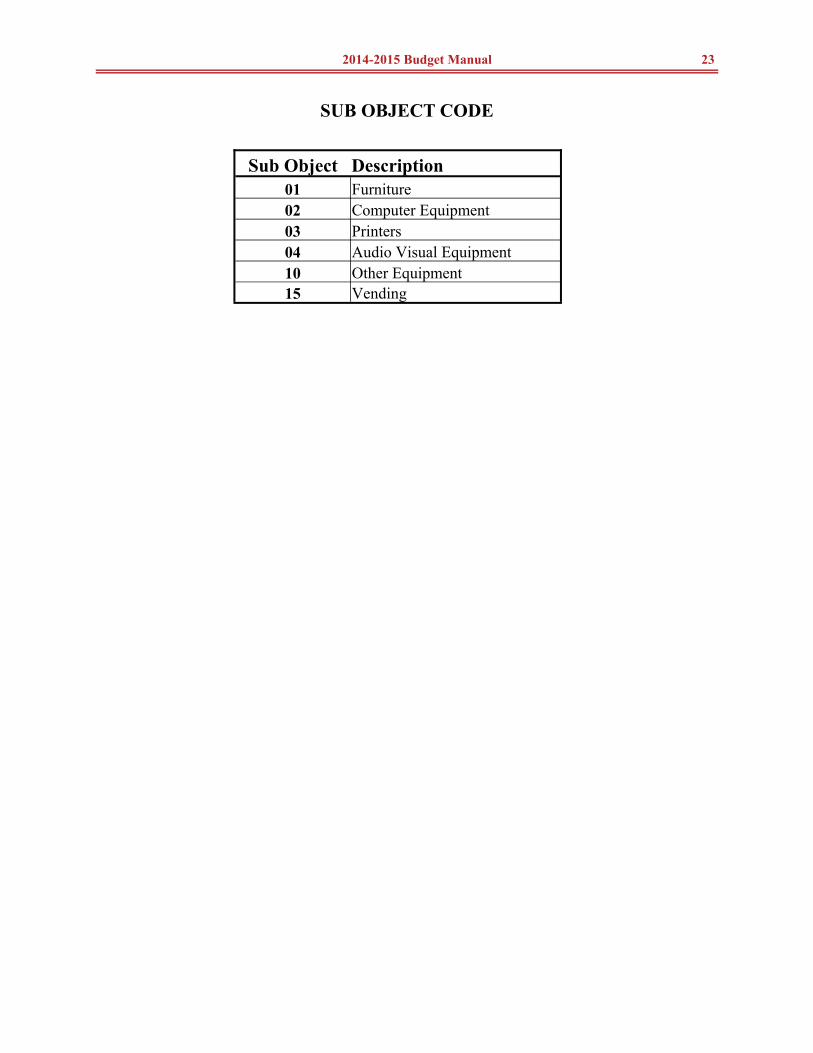

SUB OBJECT CODE

Sub Object Description 01 Furniture 02 Computer Equipment 03 Printers 04 Audio Visual Equipment 10 Other Equipment 15 Vending

2014-2015 Budget Manual 24

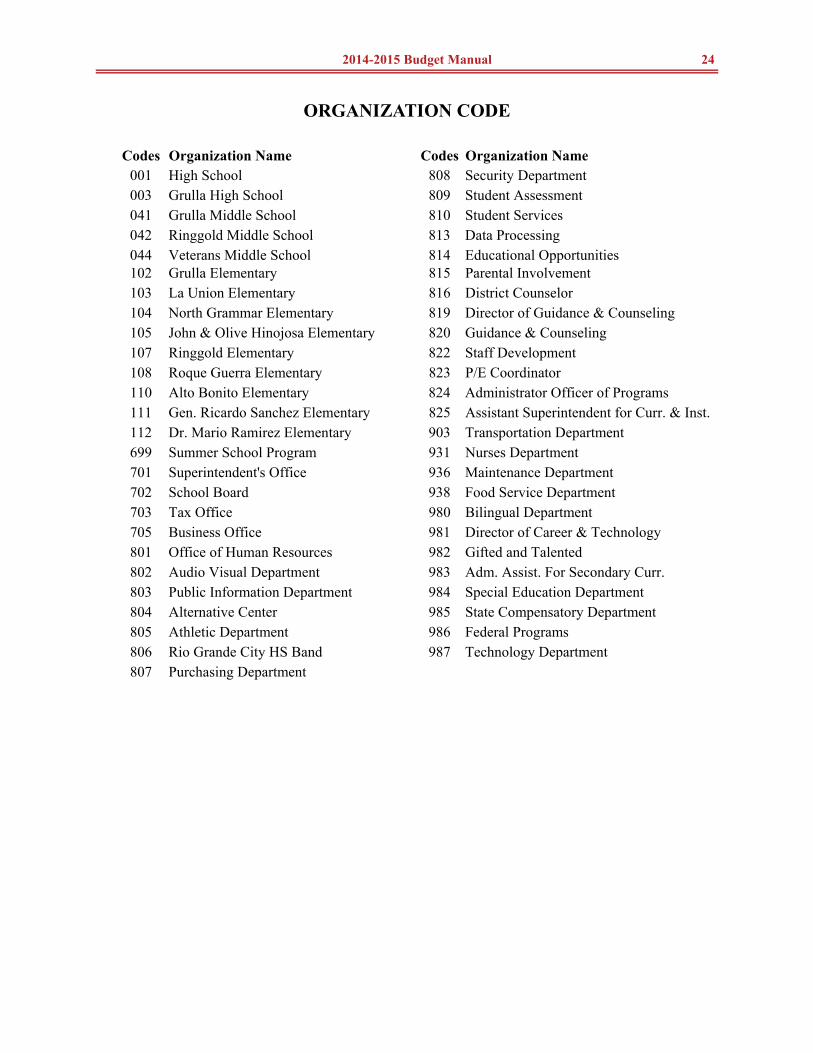

ORGANIZATION CODE

Codes Organization Name Codes Organization Name 001 High School 808 Security Department

041 Grulla Middle School 810 Student Services 042 Ringgold Middle School 813 Data Processing 044 Veterans Middle School 814 Educational Opportunities 102 Grulla Elementary 815 Parental Involvement 103 La Union Elementary 816 District Counselor 104 North Grammar Elementary 819 Director of Guidance & Counseling

107 Ringgold Elementary 822 Staff Development 108 Roque Guerra Elementary 823 P/E Coordinator 110 Alto Bonito Elementary 824 Administrator Officer of Programs 111 Gen. Ricardo Sanchez Elementary 825 Assistant Superintendent for Curr. & Inst. 112 Dr. Mario Ramirez Elementary 903 Transportation Department 699 Summer School Program 931 Nurses Department 701 Superintendent's Office 936 Maintenance Department 702 School Board 938 Food Service Department 703 Tax Office 980 Bilingual Department 705 Business Office 981 Director of Career & Technology 801 Office of Human Resources 982 Gifted and Talented 802 Audio Visual Department 983 Adm. Assist. For Secondary Curr. 803 Public Information Department 984 Special Education Department 804 Alternative Center 985 State Compensatory Department 805 Athletic Department 986 Federal Programs 806 Rio Grande City HS Band 987 Technology Department 807 Purchasing Department

105 John & Olive Hinojosa Elementary 820 Guidance & Counseling

003 Grulla High School 809 Student Assessment

2014-2015 Budget Manual 25

FISCAL YEAR CODE

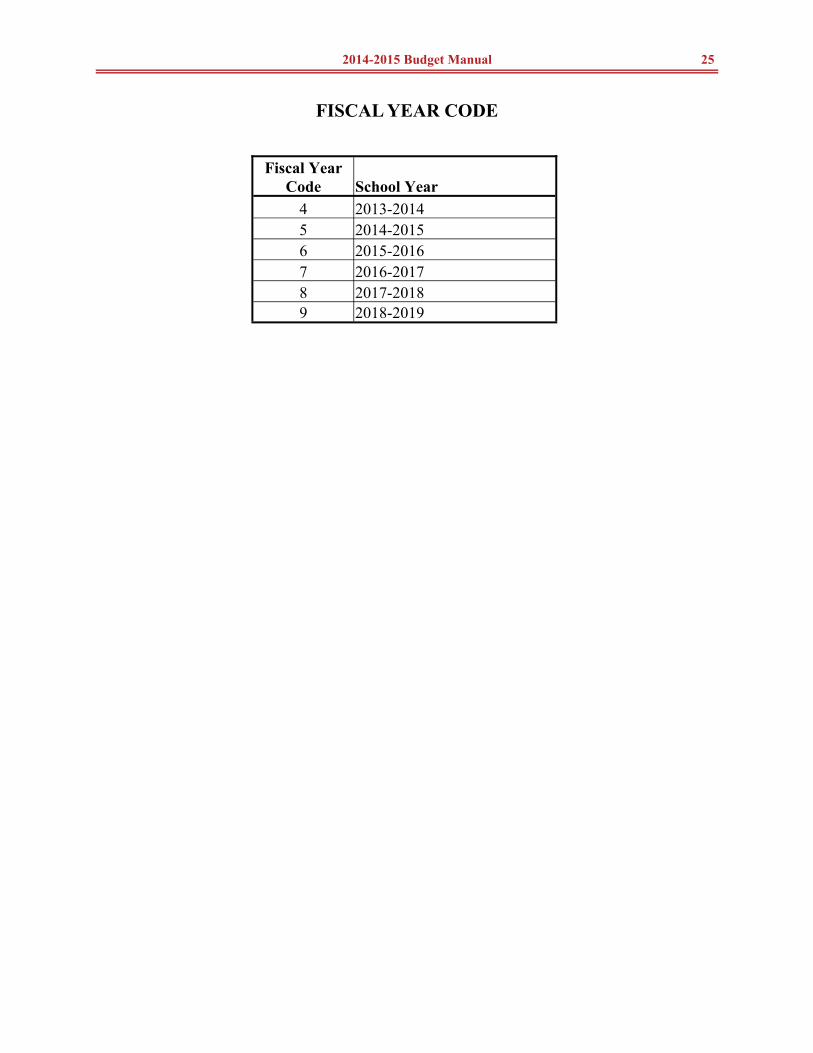

Fiscal Year Code School Year

4 2013-2014 5 2014-2015 6 2015-2016 7 2016-2017 8 2017-2018 9 2018-2019

2014-2015 Budget Manual 26

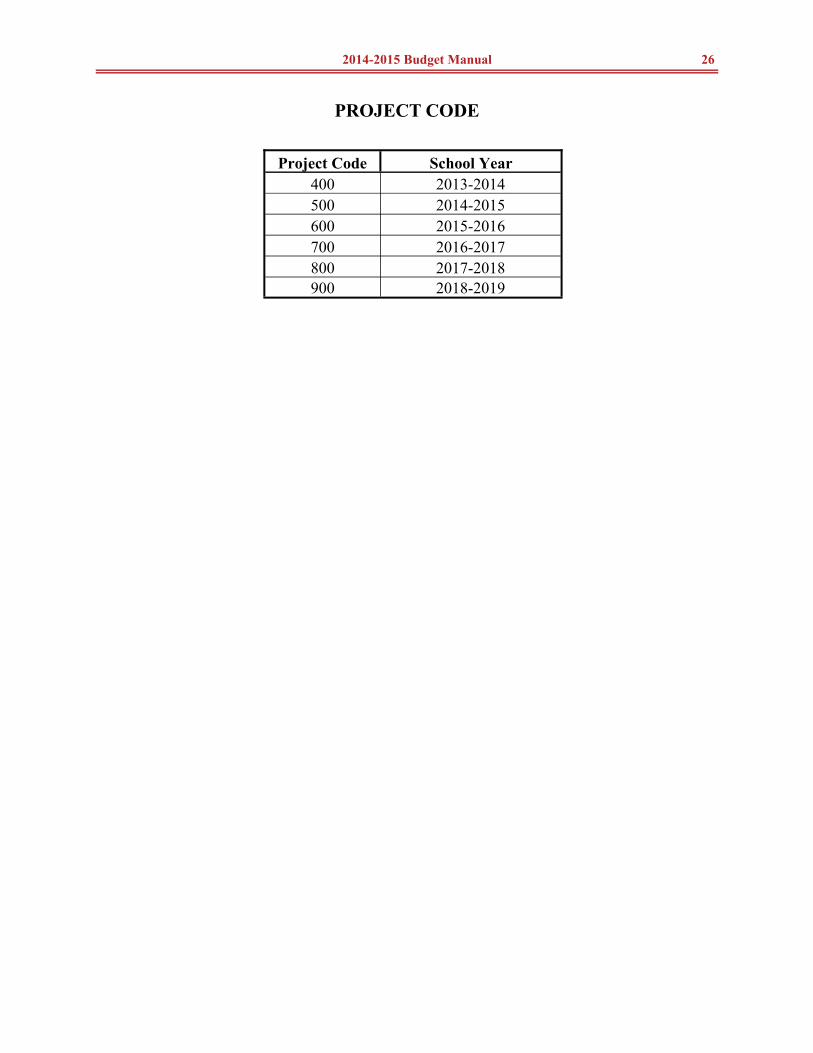

PROJECT CODE

Project Code School Year 400 2013-2014 500 2014-2015 600 2015-2016 700 2016-2017 800 2017-2018 900 2018-2019

Recommended