The Role of Trust in the Informal Investor’s Investment Decision:

An Exploratory Analysis

Group 3 Ankita S Bhavika V Mohit S Neethesh G Sahil S Saurav D

Richard T. Harrison, Mark R. Dibben & Colin M. Mason

Overview

Introduction

Informal Investment Decision Making

Swift Trust

Research Methodology

Verbal Protocol Analysis

Findings

Conclusion

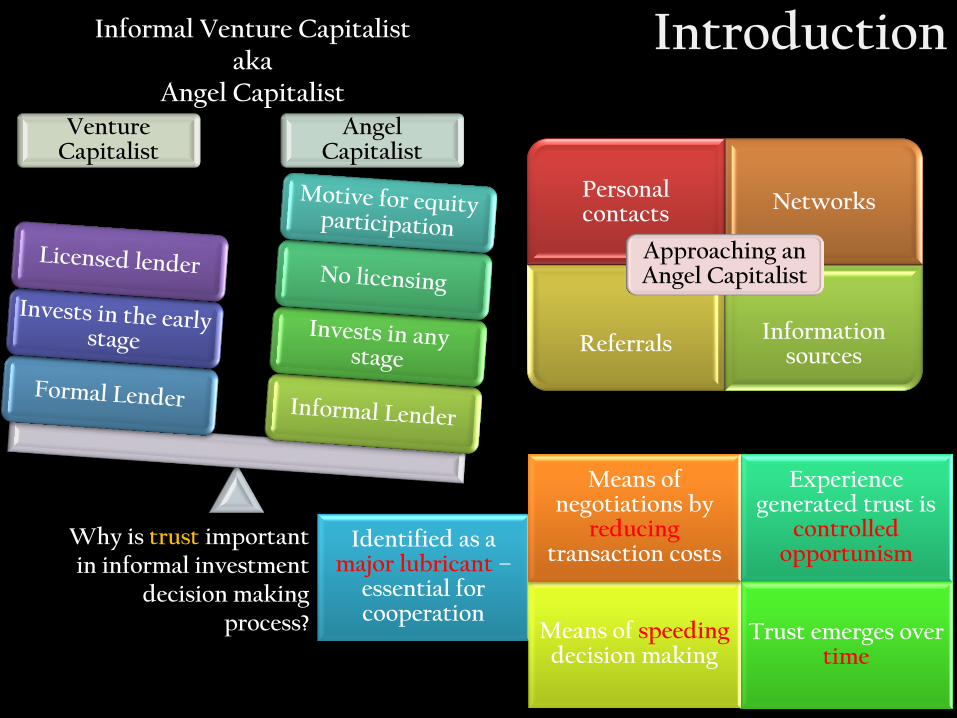

Introduction

Venture Capitalist

Angel Capitalist

Informal Venture Capitalist aka

Angel Capitalist

Personal contacts

Networks

Referrals

Information sources

Approaching an Angel Capitalist

Why is trust important in informal investment

decision making process?

Identified as a major lubricant –

essential for cooperation

Experience generated trust is

controlled opportunism

Trust emerges over time

Means of speeding decision making

Means of negotiations by

reducing transaction costs

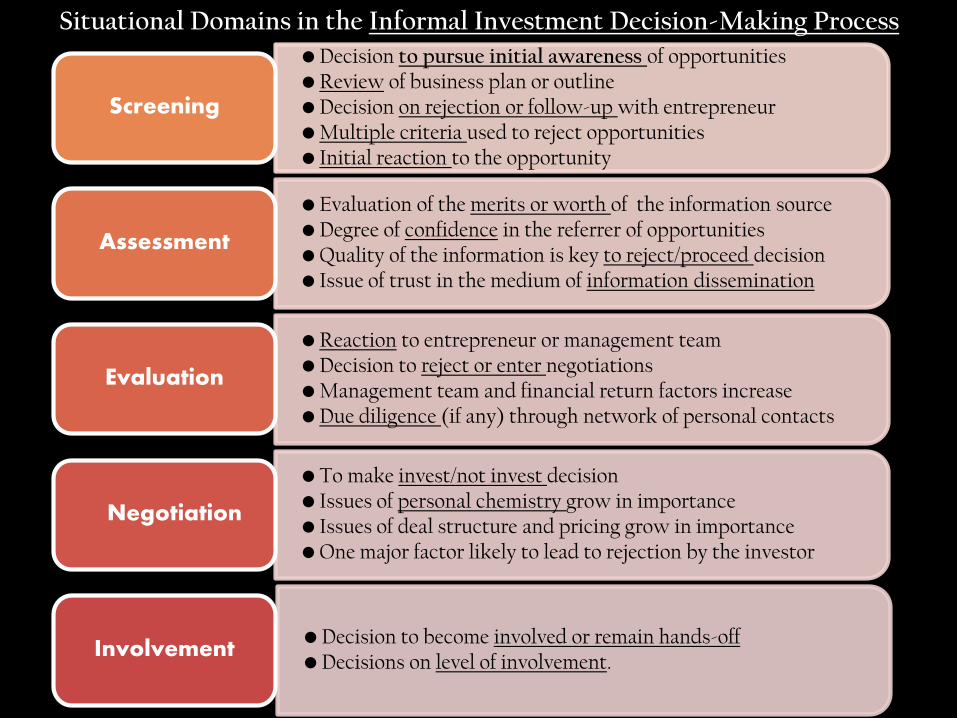

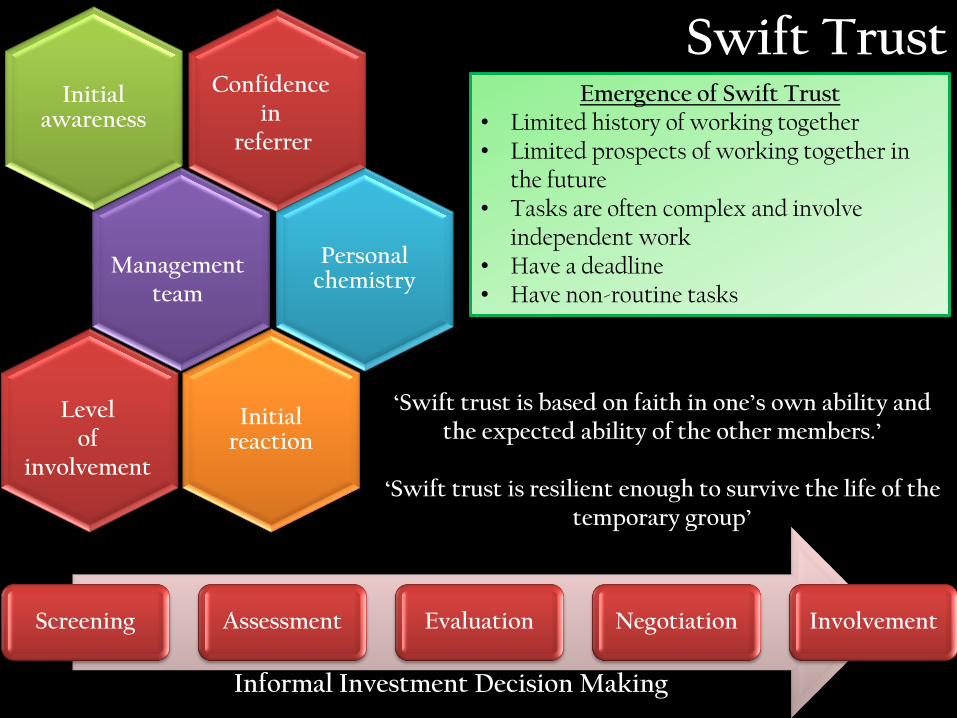

• Decision to pursue initial awareness of opportunities • Review of business plan or outline • Decision on rejection or follow-up with entrepreneur • Multiple criteria used to reject opportunities • Initial reaction to the opportunity

Screening

• Evaluation of the merits or worth of the information source • Degree of confidence in the referrer of opportunities • Quality of the information is key to reject/proceed decision • Issue of trust in the medium of information dissemination

Assessment

• Reaction to entrepreneur or management team • Decision to reject or enter negotiations • Management team and financial return factors increase • Due diligence (if any) through network of personal contacts

Evaluation

• To make invest/not invest decision • Issues of personal chemistry grow in importance • Issues of deal structure and pricing grow in importance • One major factor likely to lead to rejection by the investor

Negotiation

• Decision to become involved or remain hands-off • Decisions on level of involvement.

Involvement

Situational Domains in the Informal Investment Decision-Making Process

Informal Investment Decision Making

Screening Assessment Evaluation Negotiation Involvement

Initial awareness

Personal chemistry

Initial reaction

Management team

Confidence in

referrer

Level of

involvement

Swift Trust Emergence of Swift Trust

• Limited history of working together • Limited prospects of working together in

the future • Tasks are often complex and involve

independent work • Have a deadline • Have non-routine tasks

‘Swift trust is based on faith in one’s own ability and the expected ability of the other members.’

‘Swift trust is resilient enough to survive the life of the

temporary group’

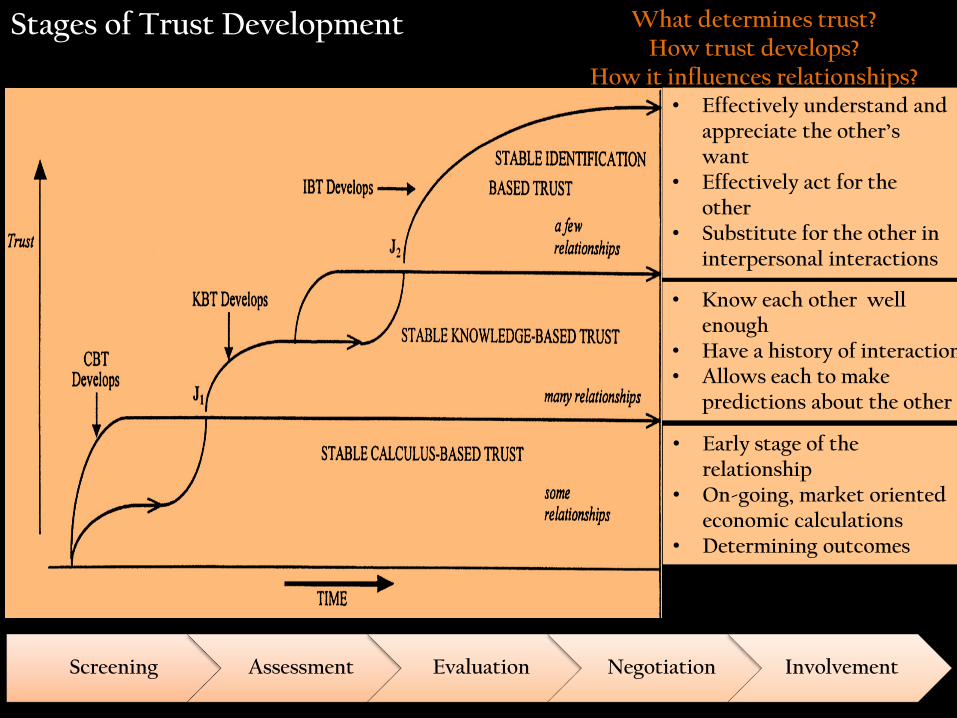

What determines trust? How trust develops?

How it influences relationships?

Stages of Trust Development

• Effectively understand and appreciate the other’s want

• Effectively act for the other

• Substitute for the other in interpersonal interactions

• Know each other well enough

• Have a history of interaction • Allows each to make

predictions about the other

• Early stage of the relationship

• On-going, market oriented economic calculations

• Determining outcomes

Screening Assessment Evaluation Negotiation Involvement

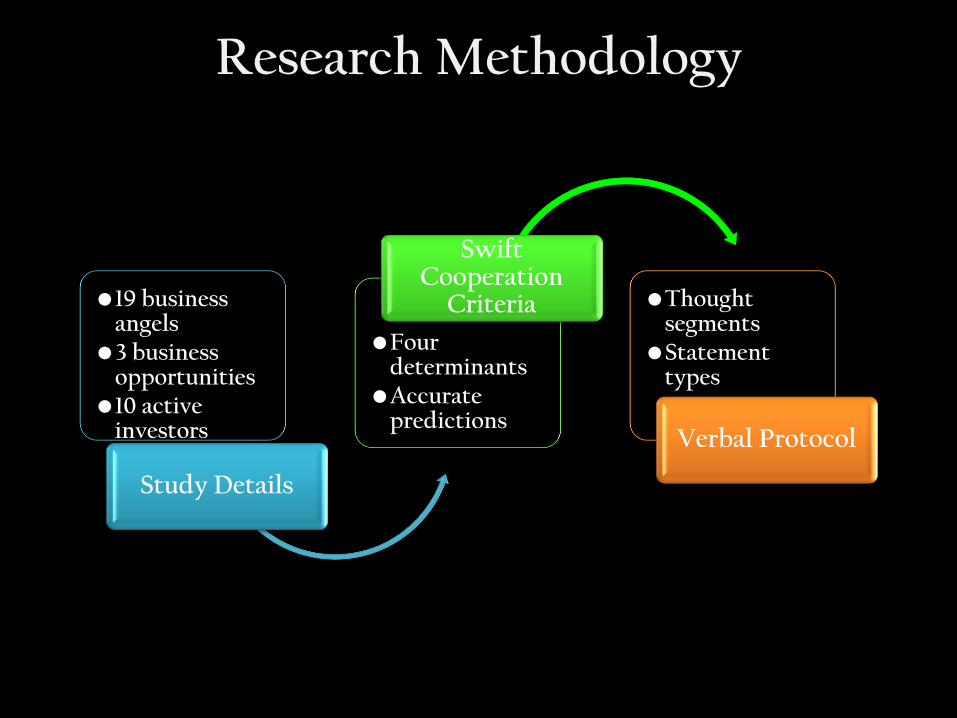

Research Methodology

•19 business angels

•3 business opportunities

•10 active investors

Study Details

•Four determinants

•Accurate predictions

Swift Cooperation

Criteria •Thought segments

•Statement types

Verbal Protocol

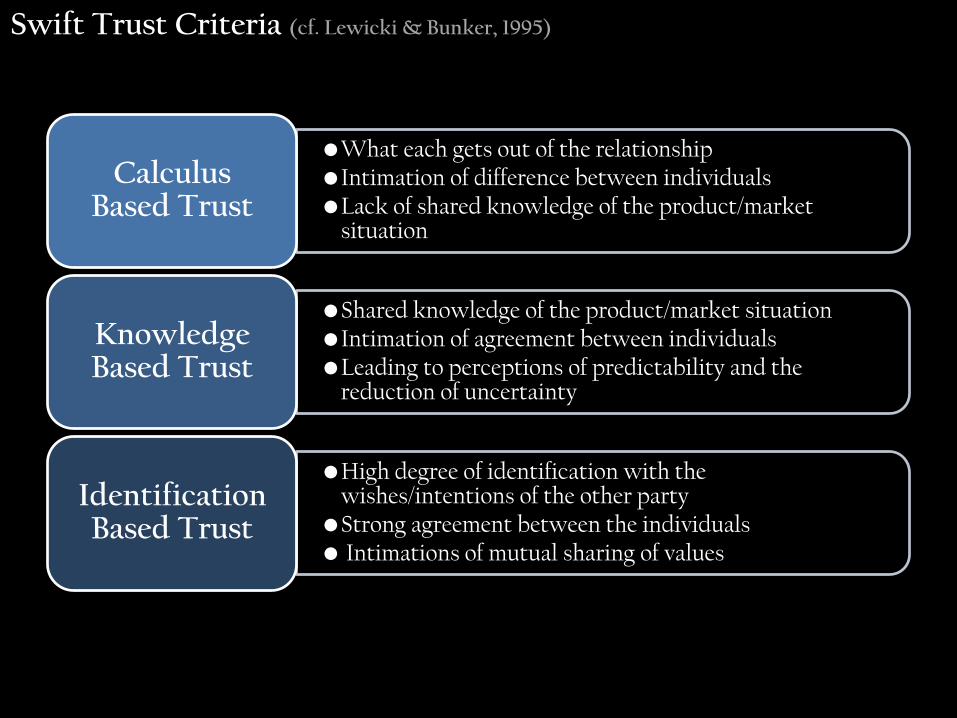

•What each gets out of the relationship •Intimation of difference between individuals •Lack of shared knowledge of the product/market

situation

Calculus Based Trust

•Shared knowledge of the product/market situation •Intimation of agreement between individuals •Leading to perceptions of predictability and the

reduction of uncertainty

Knowledge Based Trust

•High degree of identification with the wishes/intentions of the other party

•Strong agreement between the individuals • Intimations of mutual sharing of values

Identification Based Trust

Swift Trust Criteria (cf. Lewicki & Bunker, 1995)

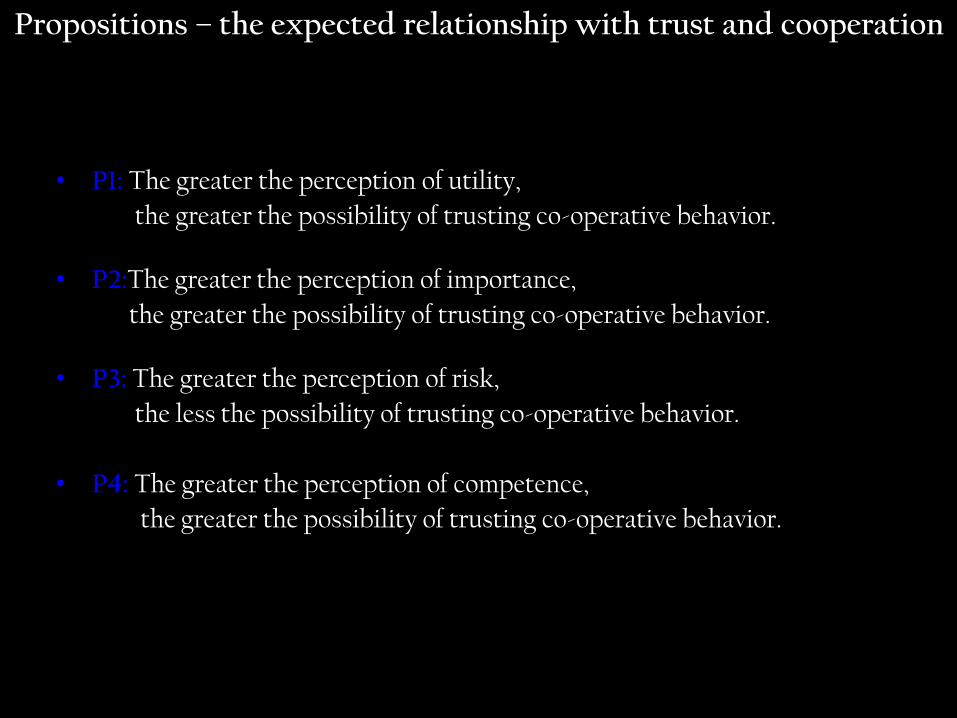

• P1: The greater the perception of utility,

the greater the possibility of trusting co-operative behavior.

• P2:The greater the perception of importance,

the greater the possibility of trusting co-operative behavior.

• P3: The greater the perception of risk,

the less the possibility of trusting co-operative behavior.

• P4: The greater the perception of competence,

the greater the possibility of trusting co-operative behavior.

Propositions – the expected relationship with trust and cooperation

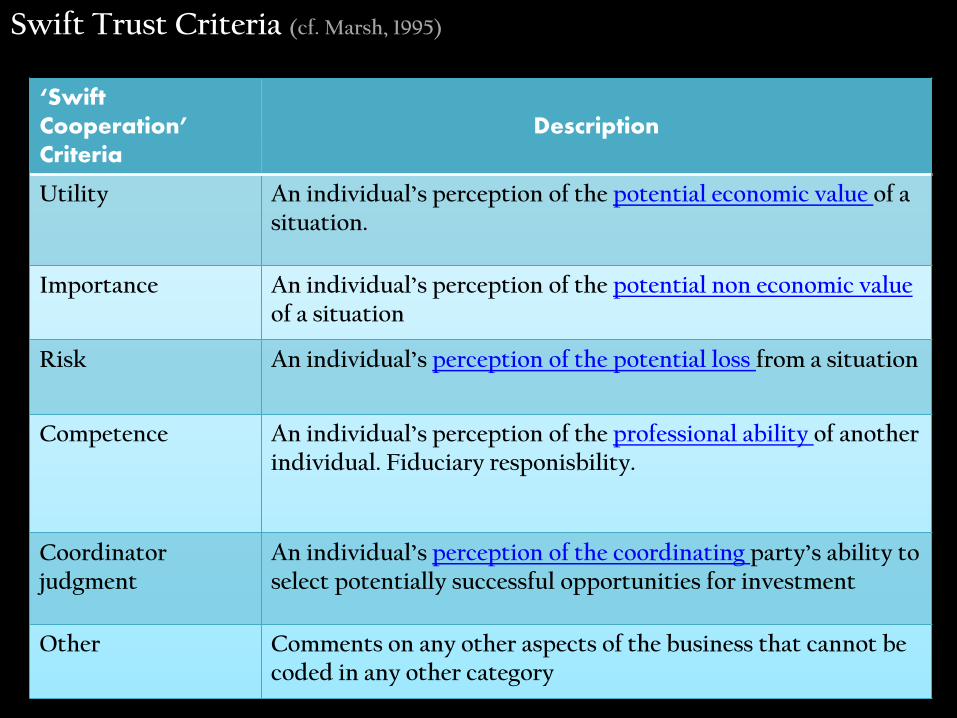

‘Swift Cooperation’ Criteria

Description

Utility An individual’s perception of the potential economic value of a situation.

Importance An individual’s perception of the potential non economic value of a situation

Risk An individual’s perception of the potential loss from a situation

Competence An individual’s perception of the professional ability of another individual. Fiduciary responisbility.

Coordinator judgment

An individual’s perception of the coordinating party’s ability to select potentially successful opportunities for investment

Other Comments on any other aspects of the business that cannot be coded in any other category

Swift Trust Criteria (cf. Marsh, 1995)

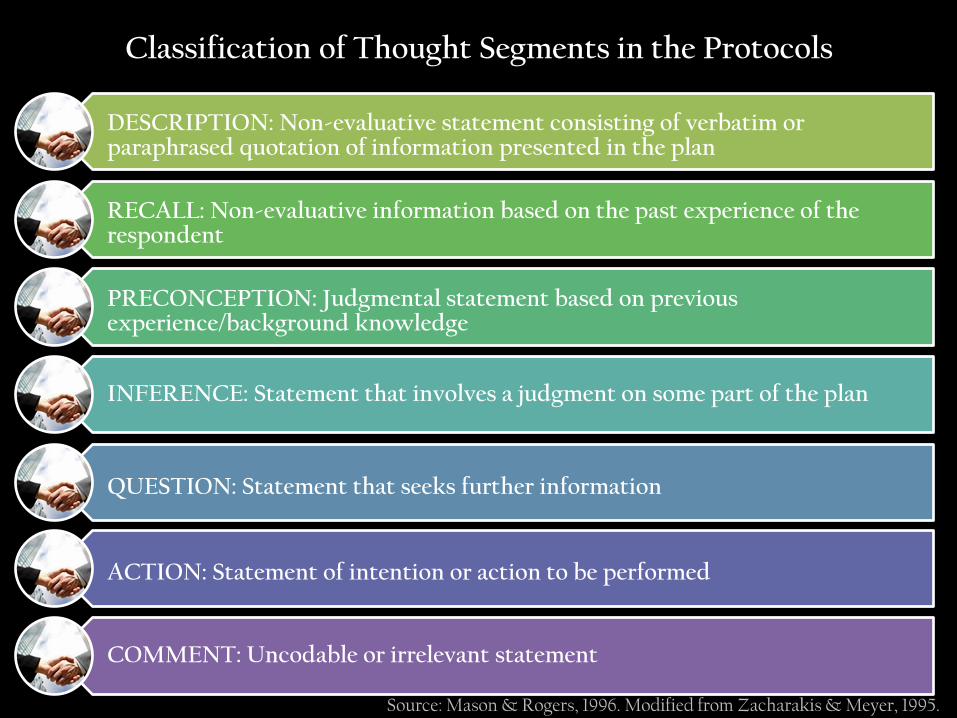

DESCRIPTION: Non-evaluative statement consisting of verbatim or paraphrased quotation of information presented in the plan

RECALL: Non-evaluative information based on the past experience of the respondent

PRECONCEPTION: Judgmental statement based on previous experience/background knowledge

INFERENCE: Statement that involves a judgment on some part of the plan

QUESTION: Statement that seeks further information

ACTION: Statement of intention or action to be performed

COMMENT: Uncodable or irrelevant statement

Classification of Thought Segments in the Protocols

Source: Mason & Rogers, 1996. Modified from Zacharakis & Meyer, 1995.

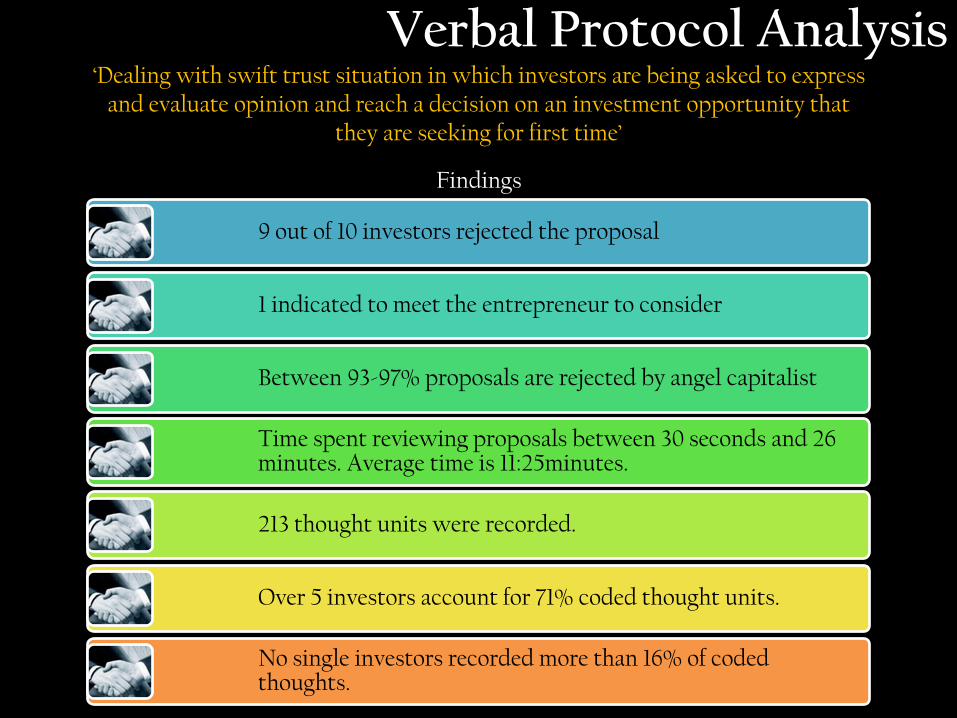

‘Dealing with swift trust situation in which investors are being asked to express and evaluate opinion and reach a decision on an investment opportunity that

they are seeking for first time’

Verbal Protocol Analysis

Findings

9 out of 10 investors rejected the proposal

1 indicated to meet the entrepreneur to consider

Between 93-97% proposals are rejected by angel capitalist

Time spent reviewing proposals between 30 seconds and 26 minutes. Average time is 11:25minutes.

213 thought units were recorded.

Over 5 investors account for 71% coded thought units.

No single investors recorded more than 16% of coded thoughts.

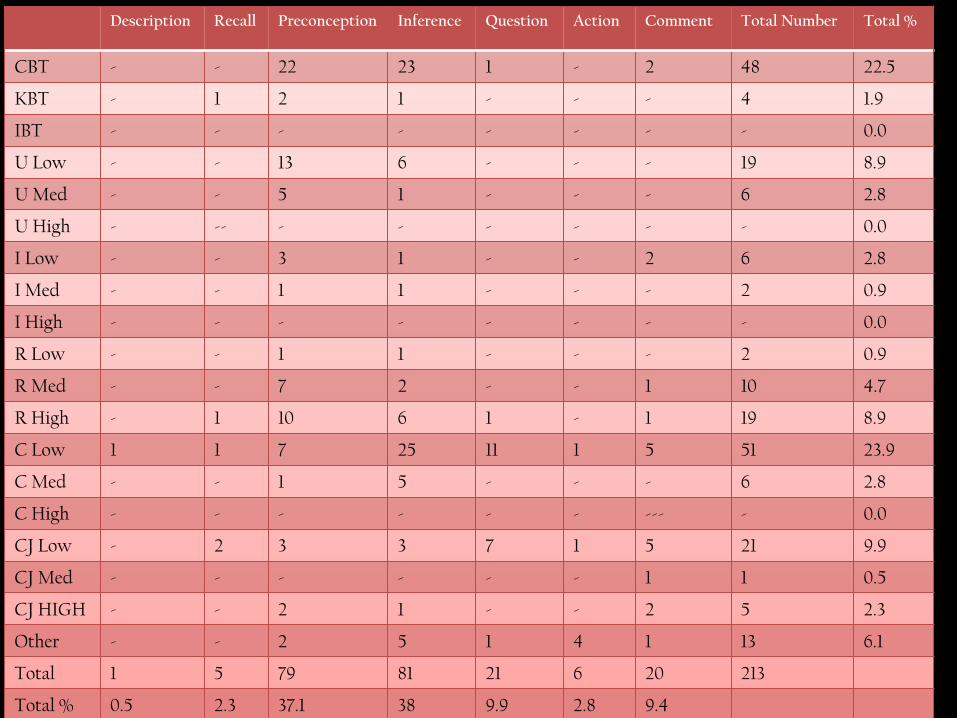

Description Recall Preconception Inference Question Action Comment Total Number Total %

CBT - - 22 23 1 - 2 48 22.5

KBT - 1 2 1 - - - 4 1.9

IBT - - - - - - - - 0.0

U Low - - 13 6 - - - 19 8.9

U Med - - 5 1 - - - 6 2.8

U High - -- - - - - - - 0.0

I Low - - 3 1 - - 2 6 2.8

I Med - - 1 1 - - - 2 0.9

I High - - - - - - - - 0.0

R Low - - 1 1 - - - 2 0.9

R Med - - 7 2 - - 1 10 4.7

R High - 1 10 6 1 - 1 19 8.9

C Low 1 1 7 25 11 1 5 51 23.9

C Med - - 1 5 - - - 6 2.8

C High - - - - - - --- - 0.0

CJ Low - 2 3 3 7 1 5 21 9.9

CJ Med - - - - - - 1 1 0.5

CJ HIGH - - 2 1 - - 2 5 2.3

Other - - 2 5 1 4 1 13 6.1

Total 1 5 79 81 21 6 20 213

Total % 0.5 2.3 37.1 38 9.9 2.8 9.4

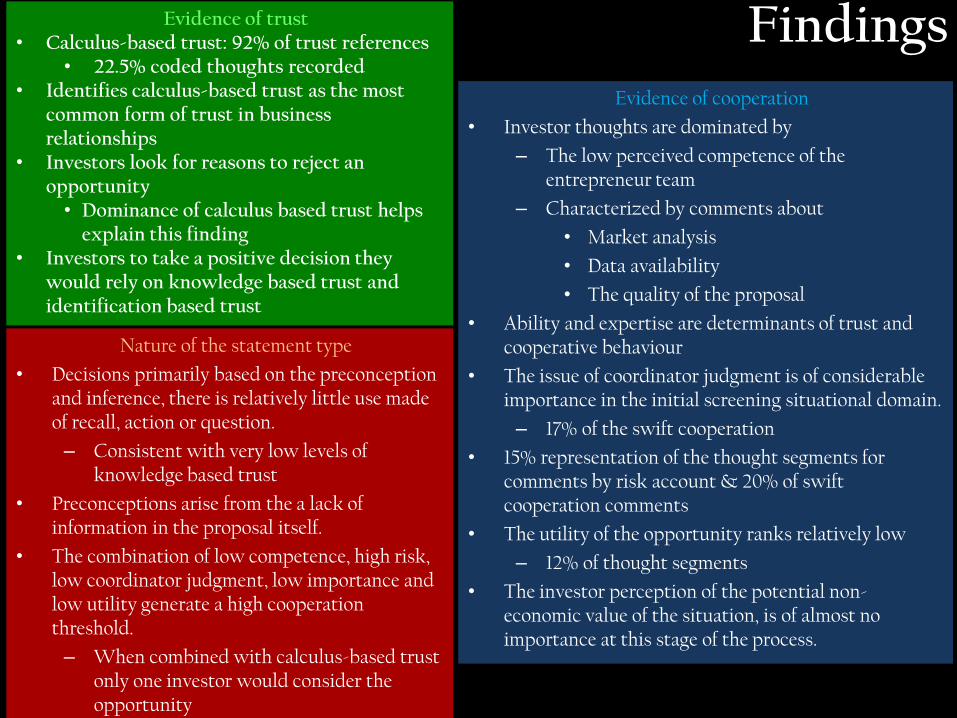

Evidence of trust • Calculus-based trust: 92% of trust references

• 22.5% coded thoughts recorded • Identifies calculus-based trust as the most

common form of trust in business relationships

• Investors look for reasons to reject an opportunity • Dominance of calculus based trust helps

explain this finding • Investors to take a positive decision they

would rely on knowledge based trust and identification based trust

Findings Evidence of cooperation

• Investor thoughts are dominated by

– The low perceived competence of the entrepreneur team

– Characterized by comments about

• Market analysis

• Data availability

• The quality of the proposal

• Ability and expertise are determinants of trust and cooperative behaviour

• The issue of coordinator judgment is of considerable importance in the initial screening situational domain.

– 17% of the swift cooperation

• 15% representation of the thought segments for comments by risk account & 20% of swift cooperation comments

• The utility of the opportunity ranks relatively low

– 12% of thought segments

• The investor perception of the potential non-economic value of the situation, is of almost no importance at this stage of the process.

Nature of the statement type

• Decisions primarily based on the preconception and inference, there is relatively little use made of recall, action or question.

– Consistent with very low levels of knowledge based trust

• Preconceptions arise from the a lack of information in the proposal itself.

• The combination of low competence, high risk, low coordinator judgment, low importance and low utility generate a high cooperation threshold.

– When combined with calculus-based trust only one investor would consider the opportunity

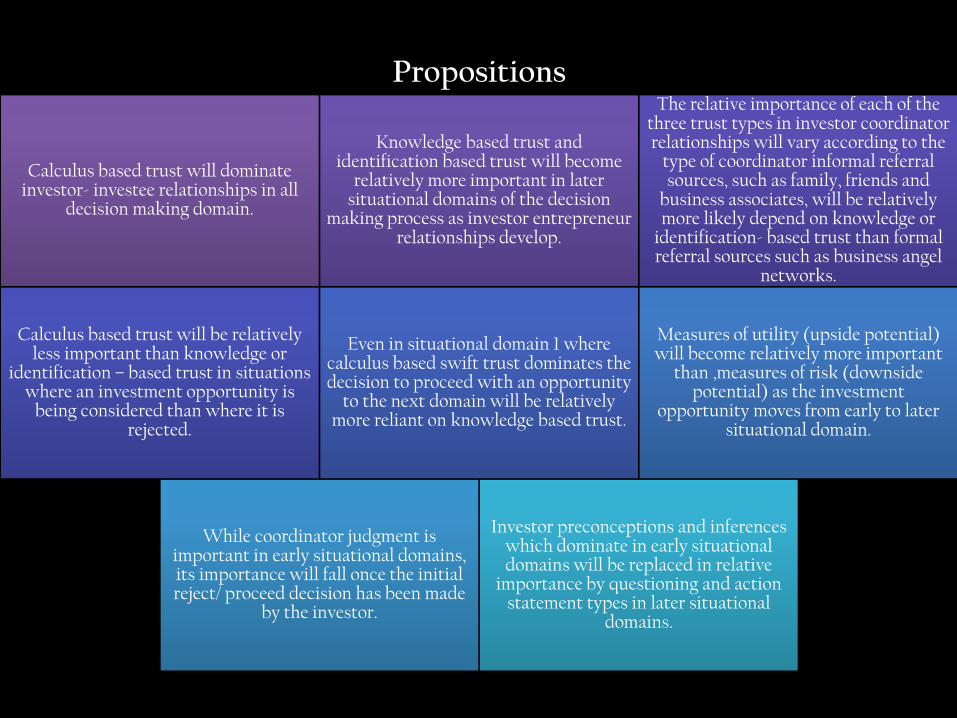

Calculus based trust will dominate investor- investee relationships in all

decision making domain.

Knowledge based trust and identification based trust will become

relatively more important in later situational domains of the decision

making process as investor entrepreneur relationships develop.

The relative importance of each of the three trust types in investor coordinator relationships will vary according to the

type of coordinator informal referral sources, such as family, friends and

business associates, will be relatively more likely depend on knowledge or

identification- based trust than formal referral sources such as business angel

networks.

Calculus based trust will be relatively less important than knowledge or

identification – based trust in situations where an investment opportunity is

being considered than where it is rejected.

Even in situational domain 1 where calculus based swift trust dominates the decision to proceed with an opportunity

to the next domain will be relatively more reliant on knowledge based trust.

Measures of utility (upside potential) will become relatively more important

than ,measures of risk (downside potential) as the investment

opportunity moves from early to later situational domain.

While coordinator judgment is important in early situational domains, its importance will fall once the initial reject/ proceed decision has been made

by the investor.

Investor preconceptions and inferences which dominate in early situational domains will be replaced in relative

importance by questioning and action statement types in later situational

domains.

Propositions

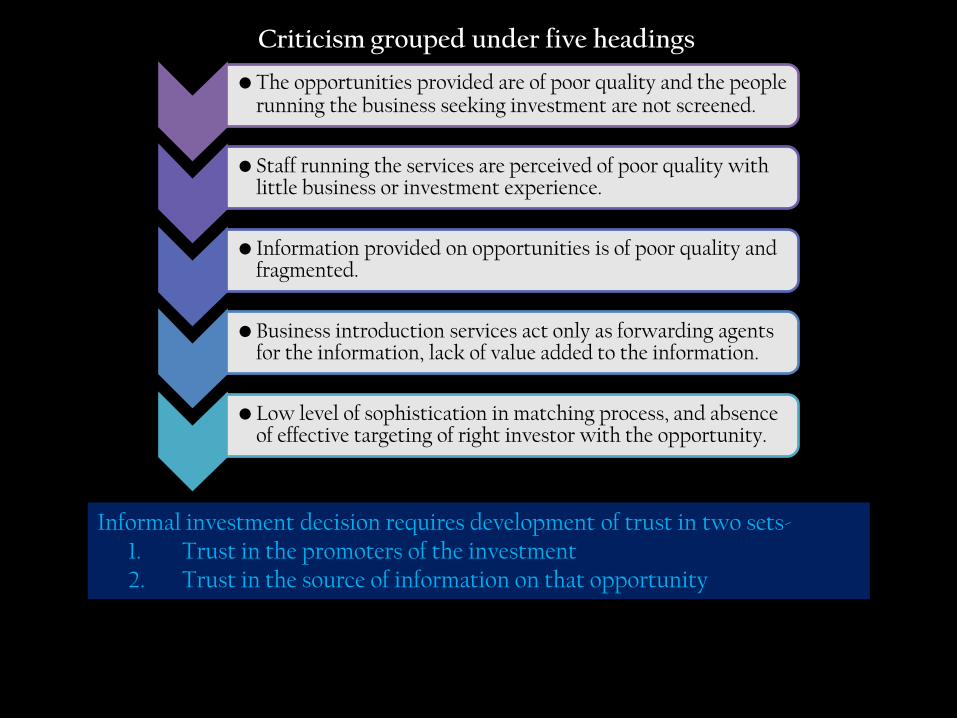

Informal investment decision requires development of trust in two sets- 1. Trust in the promoters of the investment 2. Trust in the source of information on that opportunity

• The opportunities provided are of poor quality and the people running the business seeking investment are not screened.

• Staff running the services are perceived of poor quality with little business or investment experience.

• Information provided on opportunities is of poor quality and fragmented.

• Business introduction services act only as forwarding agents for the information, lack of value added to the information.

• Low level of sophistication in matching process, and absence of effective targeting of right investor with the opportunity.

Criticism grouped under five headings

Conclusion

Swift trust framework

• Allows accurate identification of different trust types

• Forms the basis for uncovering interplay between trust and cooperation in the

informal investment decision- making process.

Limitations faced by business angel’s informal investment decision making process-

1. Primary focus is on one situational domain

2. Present study restricted to analysis of trust and cooperation of investment

opportunity

This study only provides for trust based factors that lead an investor to reject an

opportunity, and not on those that lead him/ her to accept and pursue an interest in

the opportunity.

Thank You

Recommended