1

ANRE

Romanian Electricity Sector Facts and Perspectives

2

ANRE

Where we are?

3

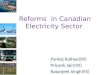

ANRE Present structure of the electricity sector

Transmission and system operatorMarket operator

8 Distribution and supply companies

16 Industrial platform distributors

120 Suppliers

14 municipal CoGenproducers and other IPP and self-producers

Hydro producer

Nuclear producer

7 Major thermal producers

RENEL

S120S1 S10 S11

Transelectrica TSO

OPCOM – Market operator

Nuclearelectrica

Hidroelectrica

Ro Cr De ElB TeTu Ga

D_1 D_2 D_16

TrNBa OlMuS TrSMoDo MuN

ENEL SpaApril 28 2005

June 2006

E.ONApril 04, 2005

CEZApril 05, 2005

4

ANRE

5

ANRE

17

2836

4943

52 51

7061

112

68

128

0

20

40

60

80

100

120

140

2001 2002 2003 2004 2005 Aug-06

Producers, license holders Suppliers, license holders

Rules for granting licenses and authorizations in the electricity sector approved by GD 540/2004, published in Romanian Official Gazette 399/2004

Authorizations and licenses

6

ANRE The wholesale electricity market

Bilateral Contracts Centralised Market

7

ANRE

Bilateral Contracts Market

regulated contracts between producers and 8 DISCOs

(suppliers of captive consumers)

negotiated contracts between market participants

Bilateral Contracts Centralized Market -starting with December 2005

Trading platforms on the wholesale electricity market (1)

GENERATORS PARTICIPATION TO ELECTRICITY GENERATION

Jan - Jun 2006

8

ANRE

Centralized Markets:– DAM (voluntary)– Balancing (mandatory)– Ancillary System Services (mandatory) – Cross Border Capacities (explicit auctions)

Priority productions• Renewable energy: supply quota & green certificates market• Cogeneration: capacity payments

Trading platforms on the wholesale electricity market (2)

Introduction of a financial market is envisaged

9

ANRE

Volume tranzactionate pe PZU si PE

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

iul 2005 aug sep oct nov dec ian 2006 feb mart apr mai iun

% din consumul intern

Volum tranzactionat pe PZU Volum tranzactionat pe PE

Electricity traded volumes on DAM and BM

% from final consumption

Electricity traded on DAMElectricity traded on BM

10

ANRE PRETURI SPOT MEDII ZILNICE- stabilite de S.C. OPCOM S.A. -

Ianuarie - Iunie 2006

0

10

20

30

40

50

60

70

80

90

100

1-Jan

8-Jan

15-Ja

n22

-Jan

29-Ja

n5-F

eb12

-Feb

19-F

eb26

-Feb

5-Mar

12-M

ar19

-Mar

26-M

ar2-A

pr9-A

pr16

-Apr

23-A

pr30

-Apr

7-May

14-M

ay21

-May

28-M

ay4-J

un11

-Jun

18-Ju

n25

-Jun

Euro/MWh

Daily average DAM prices

Last months results:

July 41.33 Euro/MWh

August 41.03 Euro/MWh

A yearly average of 36.4 Euro/MWh

11

ANRE Evolution of the electricity market opening degreeEvolutia gradului de deschidere a pietei de energie electrica

in perioada ianuarie 2004 - iunie 2006

12% 14% 15%21% 21% 22% 23% 23% 24% 24% 23% 24%

28% 27% 28%31% 33% 33% 35%

38% 38% 39% 40%38%

40% 40% 41%46%

48% 49%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

ian 20

04 feb mar apr

mai iun iulau

g

sep oct nov

decian

2005 feb mar ap

r

mai iuniul 2

005

aug

sep oct nov

decian

2006 feb mar ap

r

mai iun

Ponderea consumului consumatorilor care si-au schimbat furnizorul sau au renegociat contractul, din total consum

HG 1563/2003: 40%

HG 1823/2004: 55%

HG 644/2005: 83,5%

Grad de deschidere piaţa permis prin Hotărâre de Guvern

legal market opening degree real market opening degree

12

ANRE

Cote de piata ale furnizorilor de energie electrica pentru consumatorii finali - Iunie 2006 -

F1, 5.38%F2, 3.71%F3, 5.78%

F4, 7.01%

F5, 9.28%

F6, 6.78%

F7, 5.68%

F8, 7.22%

E1, 9.73% E2, 9.67%

E3, 2.66%

E4, 2.82%

E5, 2.39%

E6, 2.08%

E7, 1.17%E8, 1.11%E9, 1.25%E10, 1.55%E11, 1.41%

E12, 1.59%

E14, 1.39%

Altii, 9.29%

E13, 1.07%

Indicatori concentrare piata:HHI - 575 C4 - 36%

F1 … F8 furnizori pentru consumatorii captiviE1 … E14 furnizori pentru consumatorii eligibiliCategoria "Altii" include 31 de furnizori ale caror cote de piata individuale sunt sub 1%

Electricity suppliers market shares

June 2006

13

ANRE Support schemes for priority production (1)

Green certificates trading: bilateral or on a centralized market organized by the Market Operator (operational from November 2005)

Max and min limitation for green certificates values set up by ANRE (minimum value 24 Euro / MWh, maximum value 42 Euro / MWh)

Renewable sourcesMandatory supply quota for suppliers Generators received green certificates

November – August 2006

7839 green certificates traded on centralized market

14

ANRE

Cogeneration units

• Capacity payments for efficient qualified units

• Contracts between TSO and generators with efficient qualified units

• Contract prices: ancillary services tariffs

Support schemes for priority production (2)

15

ANRE

Transmission and Distribution – regulated activities Applied regulation - incentive regulation

Transmission:

revenue cap;

zonal Gs & Ls based on marginal costs

Distribution:

price cap (tariff basket)

Network tariffs

16

ANRE

• NUT ensured by ANRE until full liberalization of the market

• Full pass through upstream costs

• Regulated margin of 2.5% of the acquisition costs

• Six month ex-post adjustments

Captive end-user tariffs

End-users average electricity price (without taxes) 74 Euro/MWh

17

ANRE

Perspectives

18

ANRE Main Projects for Electricity Sector

• Distribution of the necessary investments 2006-2008• Total - 3,6 billion euros

Grid10%

Nuclear power plant10%

Thermal power plants35%

Hydro power plants 35%

Distribution networks

10%

Source: Romanian Energy Policy 2006-2008 - draft

District Heating program “Termoficare 2006-2009”

19

ANRE Undergoing privatisations

• Remaining three distribution/supply companies – 2006 - 2007;

• Complexul Energetic Turceni - S.A. – integrated electricity&mining;• Complexul Energetic Rovinari - S.A. – integrated electricity&mining;• Complexul Energetic Craiova - S.A. – integrated electricity&mining

SC "Hidroelectrica" - S.A. Bucuresti• Private capital increase for finalizing some hydro objectives under construction (public

private partnership). • Hidroserv branches• For small hydro power plants

– new companies with mix capital (private and public);– other forms of partnership;– sell of assets.

"Transelectrica" - S.A. Bucuresti• Sell of shares for branches/services• 10% of shares offered on the stock exchange

20

ANRE Investments projects to enforce regional cooperation and trade:

Pump-storage Power Plant Tarnita-Lapustesti• Units 2, 3 and 4 of Cernavoda Nuclear Power Plant

• 400 kV Interconnection Lines with Hungary and Serbia & Montenegro•400 kV Interconnection Lines with Moldova (Gadalin-Suceava-Balti)

• Black Sea DC link cable (Romania –Turkey) Regional cooperation:

•Increase communication, exchange of information,

rules harmonization

•Promote opportunities for investment developments

•Generation cost savings

• Macroeconomic benefits

21

ANRE Conclusions

• Consistent legal and regulatory framework• Potential for investments • Undergoing privatization process for generation and

distribution

Romania has:

22

ANRE

Thank you for your attention!

Romanian Electricity and Heat Regulatory Authority Phone: (+ 40 21) 311 22 44Fax : (+ 40 21) 312 43 65

www.anre.ro

Recommended