LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 1

1

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

www.woodmac.com

Delivering commercial insight to the global mining & metals industry

Issues Facing Gold and Silver Miners

Mark Fellows

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 2

3

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Reserves and Resources

Gold Mine Production

Silver Mine Production

Operating and Capital Costs

Macro Factors

• Financing

• Mergers and Acquisitions

• Country Risk

• Other Risk Factors

SWOT Analysis

Agenda

4

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Gold Miners: Depleting, Exploring and Acquiring Resources

-100% -50% 0% 50% 100% 150%

Recent (post 2006) Acquisitions

Yamana Gold, +11.1Moz 5 RNC Gold, Desert Sun, Viceroy, Meridian, Northern Orion

Oz Minerals , +2.2Moz

Buenaventura, +15.1Moz 2 Inversiones Mineras del Sur , Minas Poracota

Polyus, +17.8Moz

Agnico-Eagle, +4.2Moz 3 Riddarhyttan Resources, Pinos Altos project, Cumberland

Randgold, +1.5Moz

AngloGold Ashanti, +6.2Moz 2 São Bento mine, Golden Cycle

Goldcorp, +3.6Moz 4 Wheaton River, some Placer Dome assets, Glamis Gold, Gold Eagle

Eldorado Gold, +0.6Moz 2 Frontier Pacific Mining Corp, Afcan Mining Corp

KazakhGold, +0.5Moz 1 Oxus

Kinross Gold, +1.6Moz 2 Bema, Aurelian

Barrick Gold, +1.5Moz 5 Placer Dome, Cadence, Arizona Star, Cortez , Porgera (20%)

Gold Fields, +0Moz 3 Western Areas/South Deep, Bolivar Gold, Cerro Corona project

Newcrest, +0Moz

Freeport, -0.2Moz 1 Phelps Dodge

Lihir Gold, -0.7Moz 2 Equigold, Ballarat Goldfields

Harmony, -2.3Moz

Newmont, -7.4Moz 1 Miramar Mining

IAMGOLD, -1.7Moz 3 Gallery Gold, Cambior, Euro Resources

Resolute Mining, -0.6Moz

DRD Gold , -2.5Moz

Highland Gold, -7.3Moz

Reserve Change, 2006 to 2007

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 3

5

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

0%

50%

100%

150%

200%

250%

300%

350%

1993 1995 1997 1999 2001 2003 2005 2007

Reser

ve R

ep

lace

men

t %

Gold Mines: Global Reserve Replacement Performance

Bre-X Bust

Exploration Boom

Bear Market

Reserve growth

resumes

Reserve replacement is

the percentage of gold mined in

each year replaced in reserves by exploration.

A reserve replacement figure

of 100% implies that globally, all of

the gold mined in a given year was

replaced by exploration

Analysis removes effect of

acquisitions

…but only marginal (15%) growth in 2007

6

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

The Largest OrebodiesProduction to Date + Reserves + Resources (tonnes contained Au)

0 5000 10000 15000 20000

Production, start-up to 2007

Reserves

Resources

Mine name, start year, production

OFS, 1950, 90t/a

West Rand, 1900, 67t/a

West Wits, 1930, 105t/a

Klerksdorp, 1950, 81t/a

PT Freeport Indonesia, 1973, 90t/a

Evander, 1950, 15t/a

Kalgoorlie, 1890, 24t/a

Newmont Nevada, 1965, 75t/a

Porcupine, 1909, 14t/a

Bingham Canyon, 1900, 17t/a

Ashanti (Obuasi), 1897, 18t/a

Goldstrike, 1977, 65t/a

Yanacocha, 1993, 75t/a

Pueblo Viejo, 1975, 20t/a

El Indio Belt, 1979, 3t/a

Olympic Dam, 1988, 2t/a

Lihir, 1998, 21t/a

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 4

7

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Production Change: Main Gold Producing Regions

Static/falling production since 2000

Some growth from China, Peru, Mexico

-150

-100

-50

0

50

100

150

1986 1990 1994 1998 2002 2006

(to

nn

es)

Rest of World U.S.A. South Africa Canada Australia

Year-on-year change in gold production (tonnes

8

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Gold Mine Production Profile

800

1000

1200

1400

1600

1800

2000

2200

2004 2006 2008 2010 2012 2014 2016 2018 2020

Pro

d (

t)

Operating Base+H Prob Probable Possible Tentative

Shape of curve dictated by reserve depletion

Actual production profile will be dictated by risks:

• Gold price

• Exploration

• Finance

• Construction

• Operating

• Political

In reality, production growth implied by base case + highly probable projects likely to be attenuated

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 5

9

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

2008e Silver Mine Costs, Ranked on C1, Normal Costing (2008$e)

-20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

8

10

0 50 100 150 200 250 300 350 400 450 500 550

Cumulative Production (Paid Moz Ag)

C1

Ca

sh

Co

st (

$/o

z A

g)

© Brook Hunt

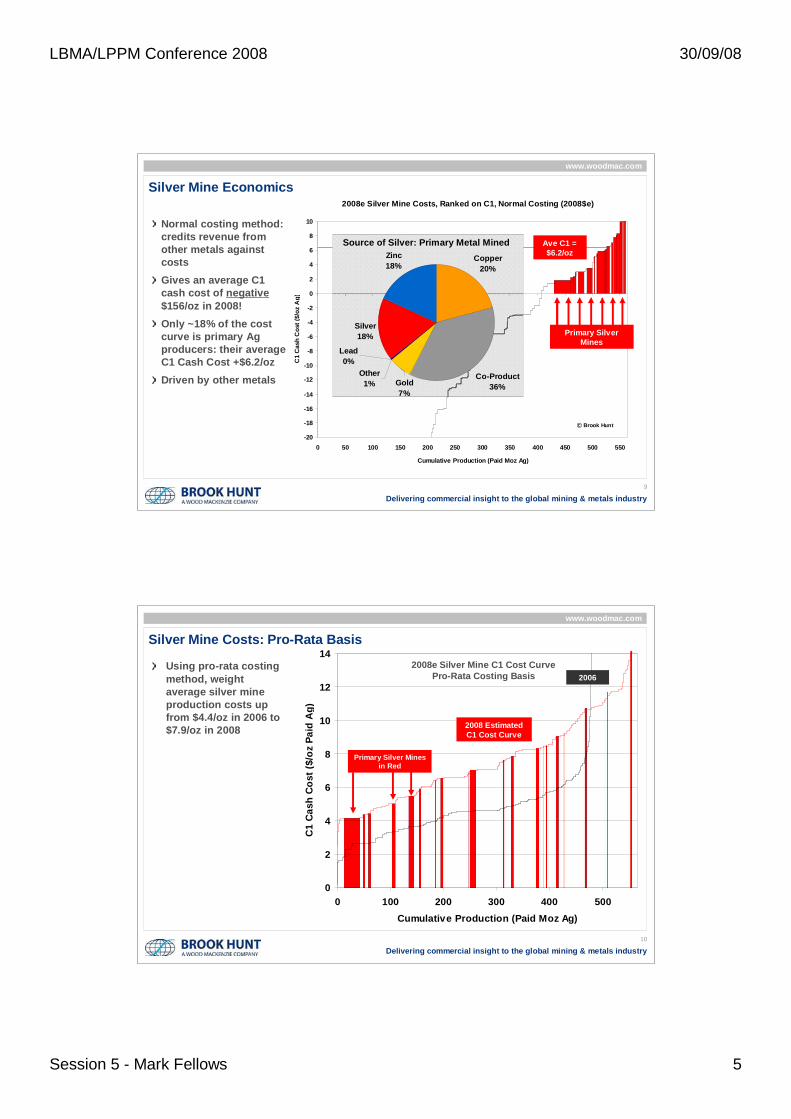

Silver Mine Economics

Primary Silver Mines

Normal costing method: credits revenue from other metals against costs

Gives an average C1 cash cost of negative$156/oz in 2008!

Only ~18% of the cost curve is primary Ag producers: their average C1 Cash Cost +$6.2/oz

Driven by other metals

Copper

20%

Co-Product

36%

Silver

18%

Zinc

18%

Gold

7%

Lead

0%

Other

1%

Source of Silver: Primary Metal Mined Ave C1 = $6.2/oz

10

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Silver Mine Costs: Pro-Rata Basis

Using pro-rata costing method, weight average silver mine production costs up from $4.4/oz in 2006 to $7.9/oz in 2008

0

2

4

6

8

10

12

14

0 100 200 300 400 500

Cumulative Production (Paid Moz Ag)

C1

Ca

sh

Co

st

($/o

z P

aid

Ag

)

Primary Silver Mines in Red

2006

2008 Estimated C1 Cost Curve

2008e Silver Mine C1 Cost Curve Pro-Rata Costing Basis

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 6

11

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Silver Production Costs: Gearing to Other Metal Prices

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

-20% -10% 0 10% 20%

Change in By-product Metal Price (%)

Ch

an

ge

in

Ag

C1 C

ash

Co

st

($/o

z)

Copper

Zinc

Lead

Gold

A 20% fall in the price of the “basket”

of by-/co- product metals = C1 Cash

Costs rise by ~$1/oz

12

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Silver Mine Production Profile

Silver production growth more likely than gold production growth – plenty of project capacity….

…but driven by other metals….

…so closures and delays due to pressure on base metals prices likely

18000

20000

22000

24000

26000

28000

30000

2004 2006 2008 2010 2012 2014 2016 2018 2020

Pro

d (

t)

Operating Base+H Prob Probable Possible

Red line shows production profile implied by market-driven production adjustments expected to affect

copper, zinc, lead and gold mines

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 7

13

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Gold Mine Cost Curve: 2002 versus 2008

Average C1 Cash Costs increased $197/oz (112%) from 2002 to 2008

Chart of C1-C3 trends/yr-o-yr change

2002 Average C1 Cost $175/oz

2008 Average C1 Cost

$372/oz (e)

14

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Operating costs: Key Drivers

Key Cost Drivers

Gold Price

•Catch-up effect

Currencies: US Dollar

Management

Head Grades

Key inputs:

•Energy

•Labour

•Consumables

•Steel

•Spares50

100

150

200

250

1992 1994 1996 1998 2000 2002 2004 2006 2008

C1 Cash Cost

Gold Price

Oil Price

Labour Costs ($/oz)

US dollar

$107/bbl = index value 562

in 2008

Ore Grade

Indexed to 1992 = 100

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 8

15

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Operating costs: Key Inputs

0

50

100

150

200

250

300

350

400

2001 2002 2003 2004 2005 2006 2007 2008 Long

Term

Min

e S

ite

Cas

h C

ost

s (

$/o

z)

Other Costs

Consumables & Spares

Diesel

Electricity

Services

Labour

Mine site costs = mining + ore processing on-site G&A

Change, 2002-2008

+102%

+146%

+131%

+159%

+177%

+87%

16

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

200

300

400

500

600

700

800

900

1999 2001 2003 2005 2007 2009 2011

$/o

z A

u

90th Centile

Upper Quartile

Gold Price

Median

Lower Quartile

Total Operating Costs

C3 Total Costs = C1 + Depreciation, Royalties, Overheads etc

Margin gap must cover:

Exploration

Sustaining capex

Expansion capex

Acquisition costs

Dividends

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 9

17

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

0

25

50

75

100

125

150

175

200

225

1992 1994 1996 1998 2000 2002 2004 2006 2008

Start Year

Ca

pit

al

Co

st,

$/o

z L

OM

Au

Pro

du

cti

on

Project Capital Intensity: Projects Commissioned 1992-2007

Blob size proportional to average

annual production

Blob size Blob size proportional proportional to average to average

annual annual productionproduction

Page 116

LihirLihir

YanacochaYanacocha

KumtorKumtor

ZarafshanZarafshanOlympiadaOlympiada

OmaiOmai

Porcupine Porcupine

BronzewingBronzewing

MinahasaMinahasa

SeponSepon

Ken Ken SnyderSnyder

GeitaGeita

LagunasLagunasNorteNorte

VeladeroVeladero

LouloLoulo

AhafoAhafo

OcampoOcampo

CowalCowal

Moab Moab KhotsongKhotsong

PogoPogo

Los Filos

PioneerPioneer

BulyanhuluBulyanhulu

18

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Cost Escalation – Implications for Mine Value

2007 Dollars

Long Term Assumptions

Gold Mines

Net Present Value Per Ounce of Production (Life-of-Mine)

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 10

19

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

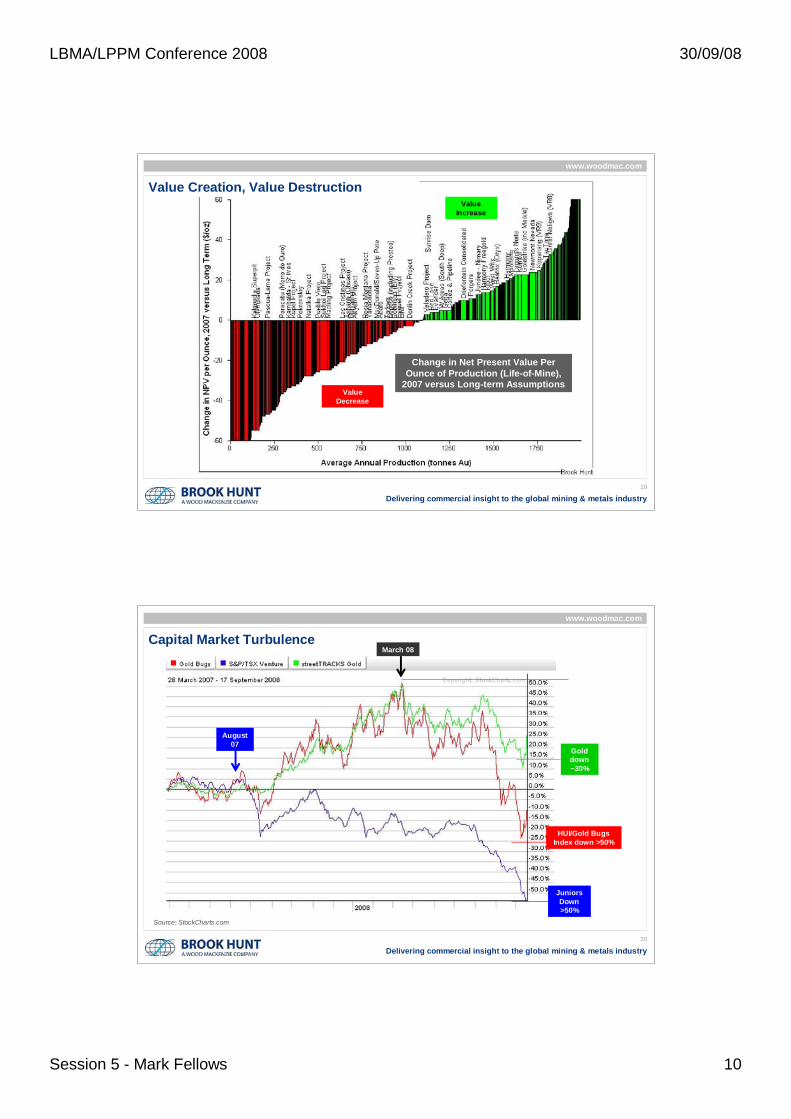

Value Creation, Value Destruction

Value Decrease

Value Increase

Change in Net Present Value Per Ounce of Production (Life-of-Mine),

2007 versus Long-term Assumptions

20

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Capital Market Turbulence

Source: StockCharts.com

HUI/Gold Bugs Index down >50%

March 08

Gold down ~30%

Juniors Down >50%

August 07

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 11

21

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

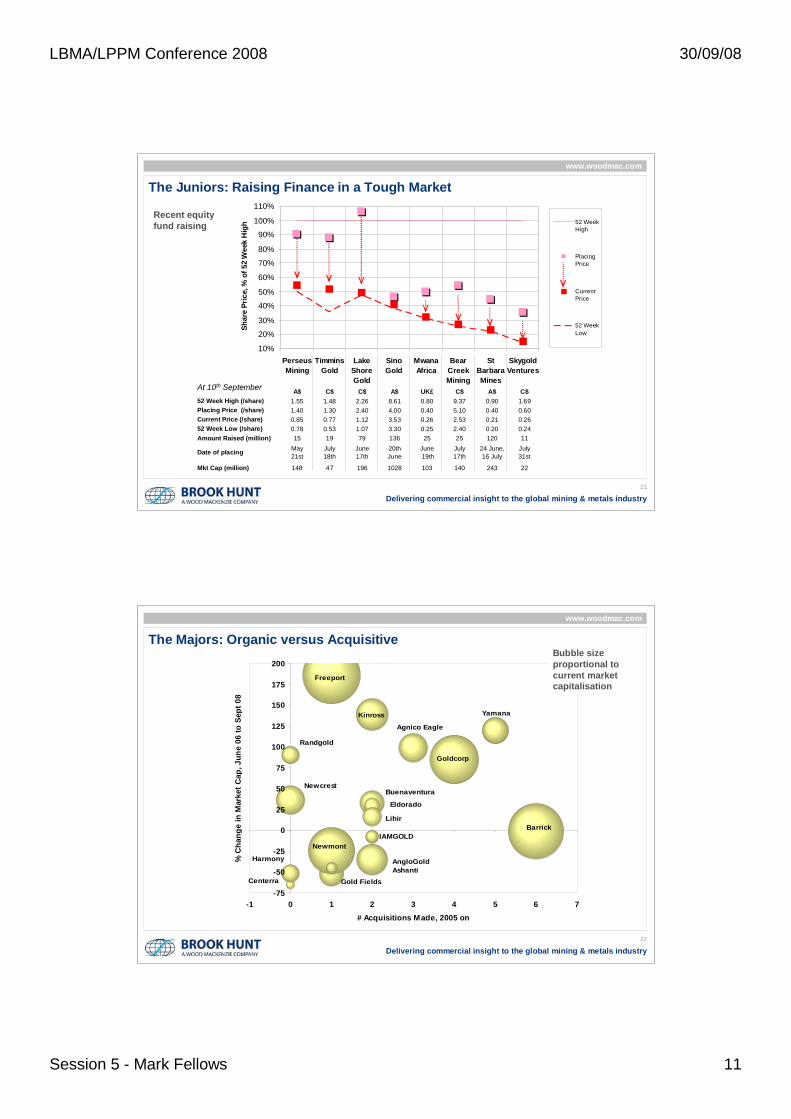

The Juniors: Raising Finance in a Tough Market

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

Perseus

Mining

Timmins

Gold

Lake

Shore

Gold

Sino

Gold

Mwana

Africa

Bear

Creek

Mining

St

Barbara

Mines

Skygold

Ventures

Sh

are

Pri

ce, %

of

52

We

ek H

igh 52 Week

High

PlacingPrice

CurrentPrice

52 Week

Low

A$ C$ C$ A$ UK£ C$ A$ C$

52 Week High (/share) 1.55 1.48 2.26 8.61 0.80 9.37 0.90 1.69

Placing Price (/share) 1.40 1.30 2.40 4.00 0.40 5.10 0.40 0.60

Current Price (/share) 0.85 0.77 1.12 3.53 0.26 2.53 0.21 0.26

52 Week Low (/share) 0.78 0.53 1.07 3.30 0.25 2.40 0.20 0.24

Amount Raised (million) 15 19 79 136 25 25 120 11

Date of placing May21st

July18th

June17th

20th June

June 19th

July17th

24 June, 16 July

July31st

Mkt Cap (million) 148 47 196 1028 103 140 243 22

At 10th September

Recent equity fund raising

22

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

The Majors: Organic versus Acquisitive

-75

-50

-25

0

25

50

75

100

125

150

175

200

-1 0 1 2 3 4 5 6 7

# Acquisitions Made, 2005 on

% C

han

ge i

n M

ark

et

Cap

, J

un

e 0

6 t

o S

ep

t 0

8

Barrick

Randgold

Newmont

Harmony

Newcrest

Centerra Gold Fields

Goldcorp

Agnico Eagle

Kinross Yamana

Freeport

IAMGOLD

Eldorado

Lihir

Buenaventura

AngloGold

Ashanti

Bubble size proportional to current market capitalisation

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 12

23

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Other Issues

Country Risk

• Resource nationalism

Social license

Skills shortages

24

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

+40

+35

+70

+30+126

S Africa +37

Ghana +40

Indonesia +48

Philippines +31

Dominican

Republic +25

+24

Romania +23

Mongolia +21

+14

+20

>+50

Papua New

Guinea +17

Greece +17

+17

Kyrgyzstan +15

Tanzania +17

Eritrea +15

Turkey +11

+15

DRC +30

Burkina Faso +10

Others >+100

Ivory Coast +15

Country Risk versus Potential 10-Year Production Growth Country risk (Policy Potential Index) from Fraser Institute

Survey of Mining Companies 07/08

“Policy Potential Index is a composite index that measures the effects on exploration of government policies including uncertainty concerning the administration, interpretation, and enforcement of existing regulations; environmental regulations; regulatory duplication and inconsistencies; taxation; uncertainty concerning native land claims and protected areas;

infrastructure; socioeconomic agreements; political stability; labor issues; geological database; and security.”

Policy Potential Index

60-100

40-60

0-40

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 13

25

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Global Gold & Silver Miners: SWOT Analysis

Strengths

Weaknesses Threats

Opportunities

Financial muscle (majors)

Acquisitions (majors)

Exploration (juniors)

No financial muscle

(juniors)

Equity/debt markets

Exploration (majors)

Metal prices

Increased cost pressure?

Skills shortage

Country risk

Reduced cost pressure?

26

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Brook Hunt

Woburn House45 High StreetAddlestoneSurrey KT15 1TU

Global Contact Details

Europe +44 (0) 1932 878000 Americas +1 713 470 1600Asia Pacific +65 6518 0800Email [email protected]

Global Offices

Australia - Canada - China - Japan - Malaysia - Russia - Singapore - South Africa - United Arab Emirates - United Kingdom - United States

Wood Mackenzie has been providing its unique range of research products and consulting services to the Energy industry for over 30 years. Wood Mackenzie provides forward-looking commercial insight that enables clients to make better business decisions. For more information visit: www.woodmac.com

LBMA/LPPM Conference 2008 30/09/08

Session 5 - Mark Fellows 14

27

Delivering commercial insight to the global mining & metals industry

www.woodmac.com

Recommended