Contents

Preface................................................................................................................31. Introduction....................................................................................................52. Smart Card Basic..........................................................................................9

2.1 What is smart card........................................................................................92.2 History of smart card development...........................................................102.3 Different types of smart cards...................................................................11

2.3.1 Memory Cards.....................................................................................112.3.2 Contact CPU Cards.............................................................................112.3.3 Contactless Cards...............................................................................122.3.4 CombiCard.........................................................................................13

2.4 Different standards of smart cards............................................................133. Current Smart Card Applications.................................................................16

3.1 Electronic payment Applications...............................................................163.1.1 Electronic Purse...................................................................................163.1.2 Stored Value Cards.............................................................................17

3.2 Security and Authentication Applications................................................173.2.1 Cryptographic uses..............................................................................183.2.2 Identity card.........................................................................................193.2.3 Access control card.............................................................................193.2.4 Digital certificate..................................................................................203.2.5 Computer login....................................................................................20

3.3 Transportation uses....................................................................................213.4 Telecommunication Applications..............................................................223.5 HealthCare Applications.............................................................................223.6 Loyalty Applications...................................................................................23

4. Technology Aspects of Smart Card.............................................................254.1 Overview of ISO 7816 Standards .............................................................254.2 Communication Protocol between Terminal and Smart Cards...............264.3 Overview of File Systems ..........................................................................314.4 Overview of Naming Scheme.....................................................................324.5 Overview of the Security Architecture......................................................324.6 An Example of Smart Card Application : SmartFlow Internet Payment System...............................................................................................................33

5. Java Card Programming..............................................................................386. Building your own smart card application....................................................43

6.1 Plan the smart card solution......................................................................436.2 Understand the need of smart card...........................................................46

Guide to Smart Card Technology Page 1

6.3 Managing data storage on the card...........................................................476.4 Determine the required back end support................................................546.5 Choosing cardside and hostside environment......................................566.6 Miscellaneous Tools...................................................................................58

7. Future trend of smart card...........................................................................637.1 Unification of smart card hostside standards on PC..............................64

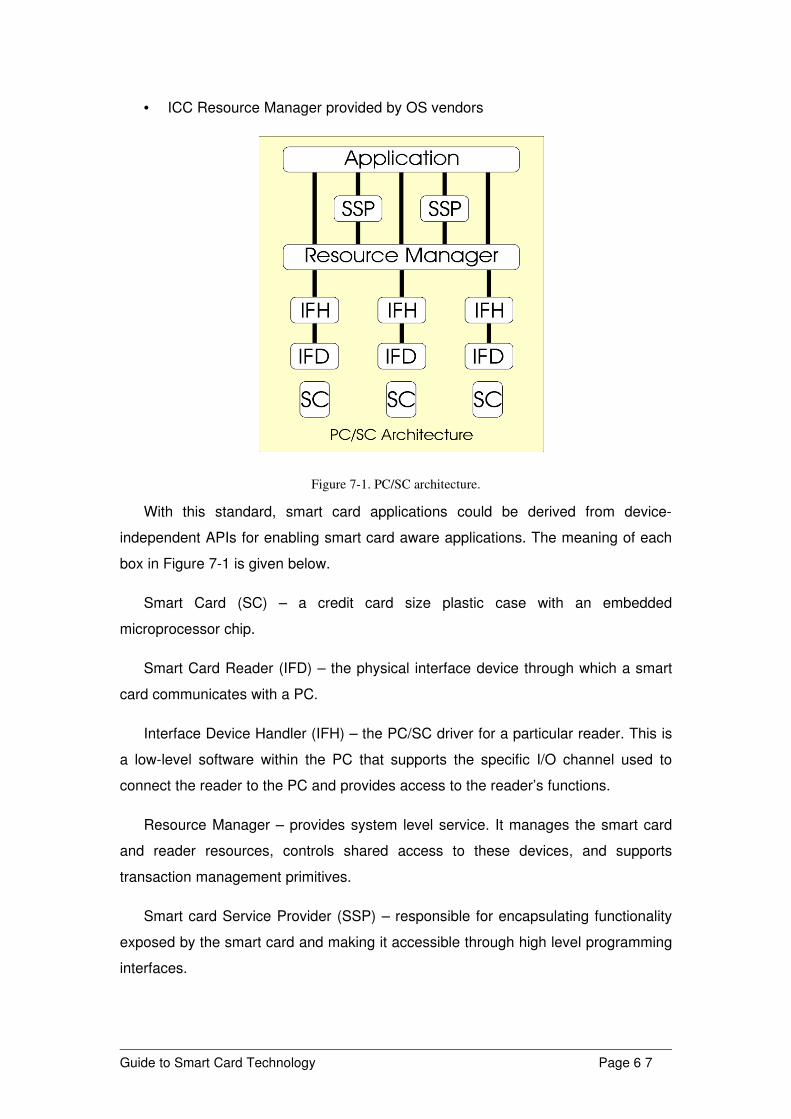

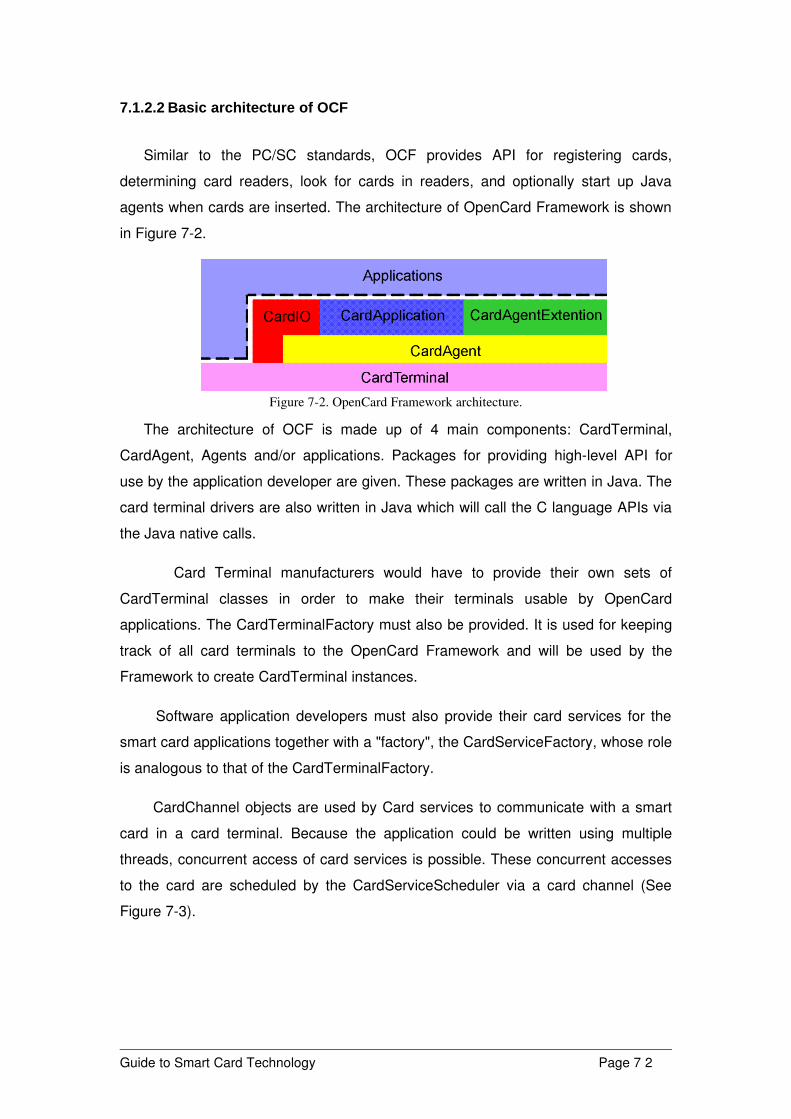

7.1.1 Personal Computer/Smart Card standard (PC/SC)..............................647.1.2 Alternative standard of smart card in PC and Minicomputer (OpenCard Framework) .................................................................................................71

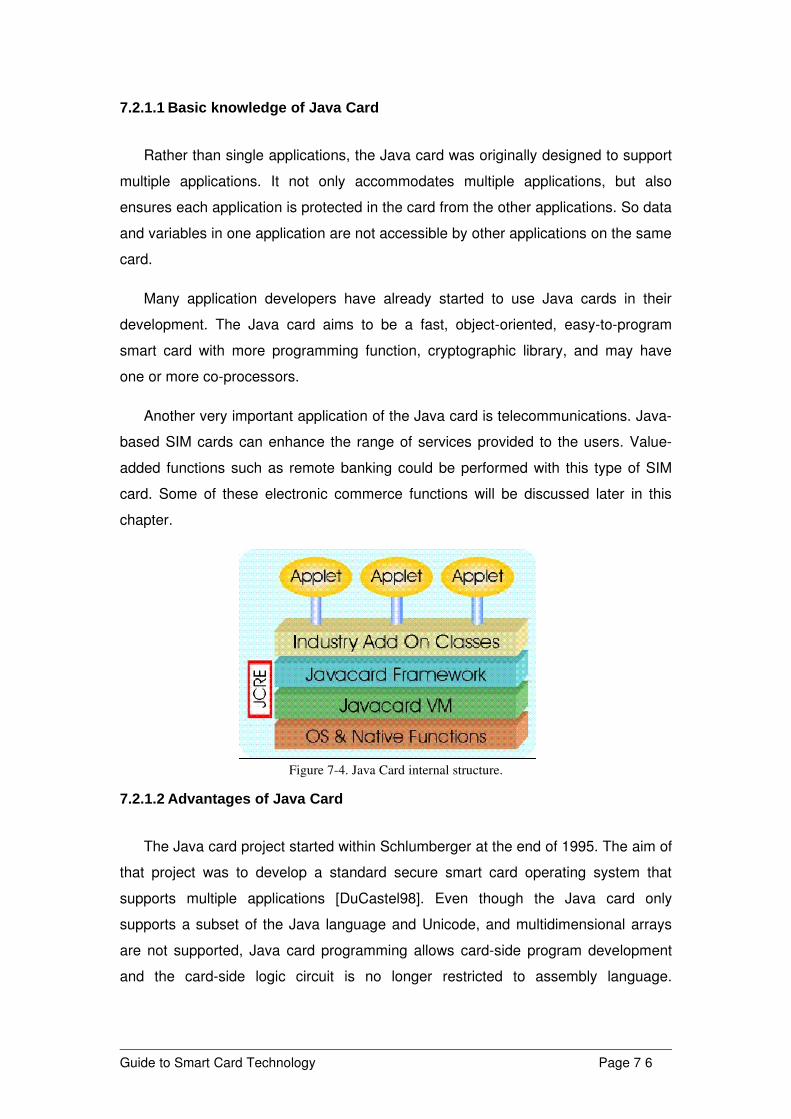

7.2 Trends in smart card cardside standards................................................747.2.1 Java inside...........................................................................................757.2.2 Mondex MULTOS OS..........................................................................777.2.3 Microsoft Windows in Smart card.........................................................797.2.4 Card OS future.....................................................................................81

7.3 Smart card in electronic commerce..........................................................827.3.1 Smart Card Payment Protocol.............................................................837.3.2 Smart card as prepaid and loyalty card................................................847.3.3 Smart card as electronic wallet............................................................857.3.4 Electronic Payment over Mobile Telecommunications.........................85

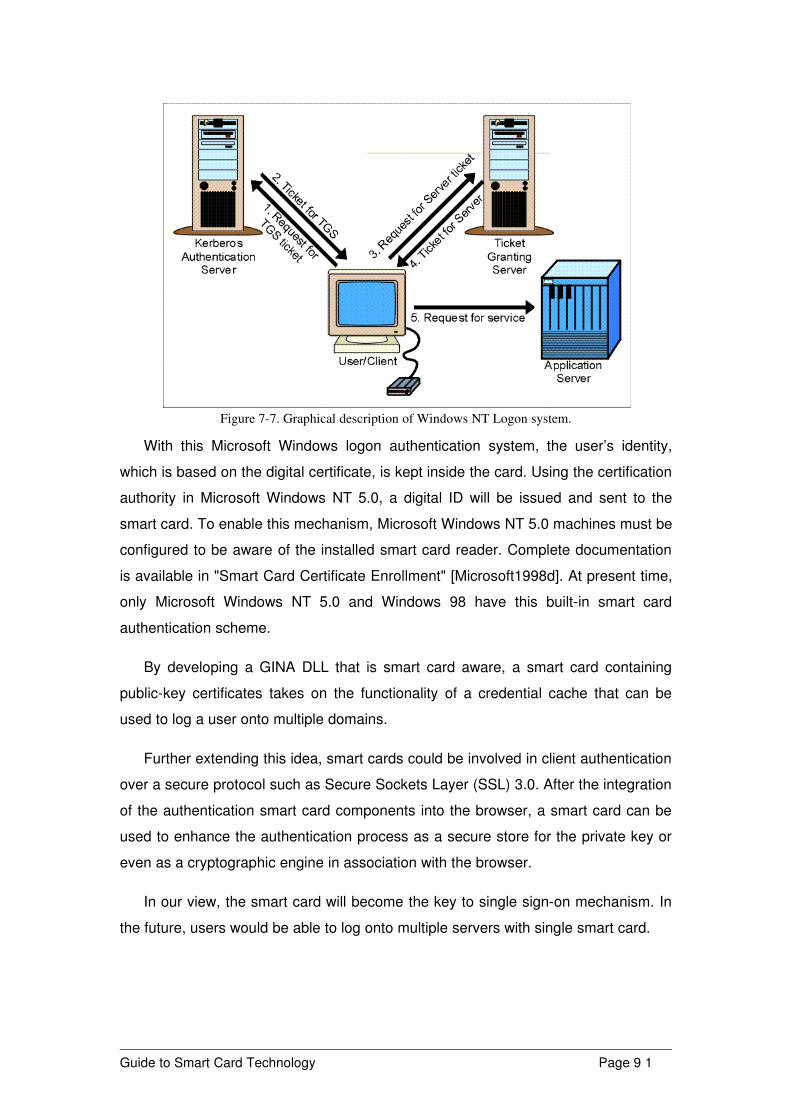

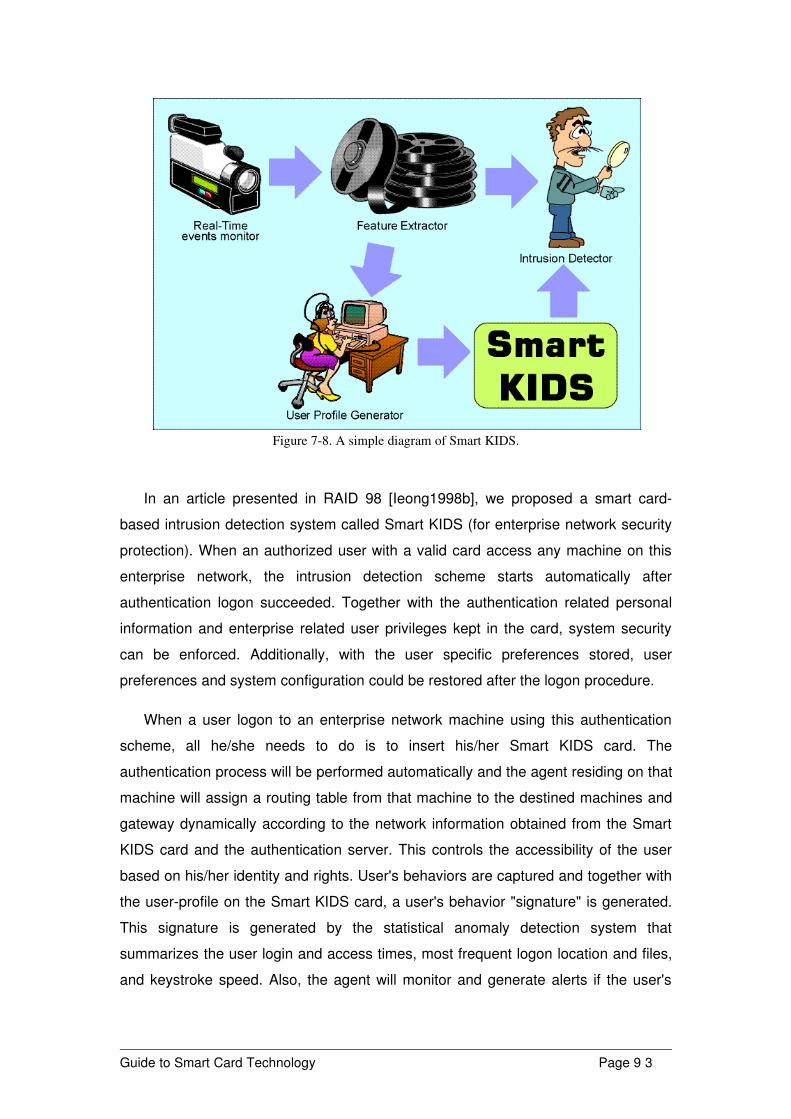

7.4 Smart card in Internet security..................................................................867.4.1 Smart card as Digital ID.......................................................................877.4.2 Smart card as Computer access logon key.........................................897.4.3 Smart card in Intrusion detection System as userprofile holder..........927.4.4 Biometric authentication.......................................................................94

8. Summaries and Conclusions.......................................................................95 Glossary........................................................................................................100 References....................................................................................................111 Appendix.......................................................................................................119

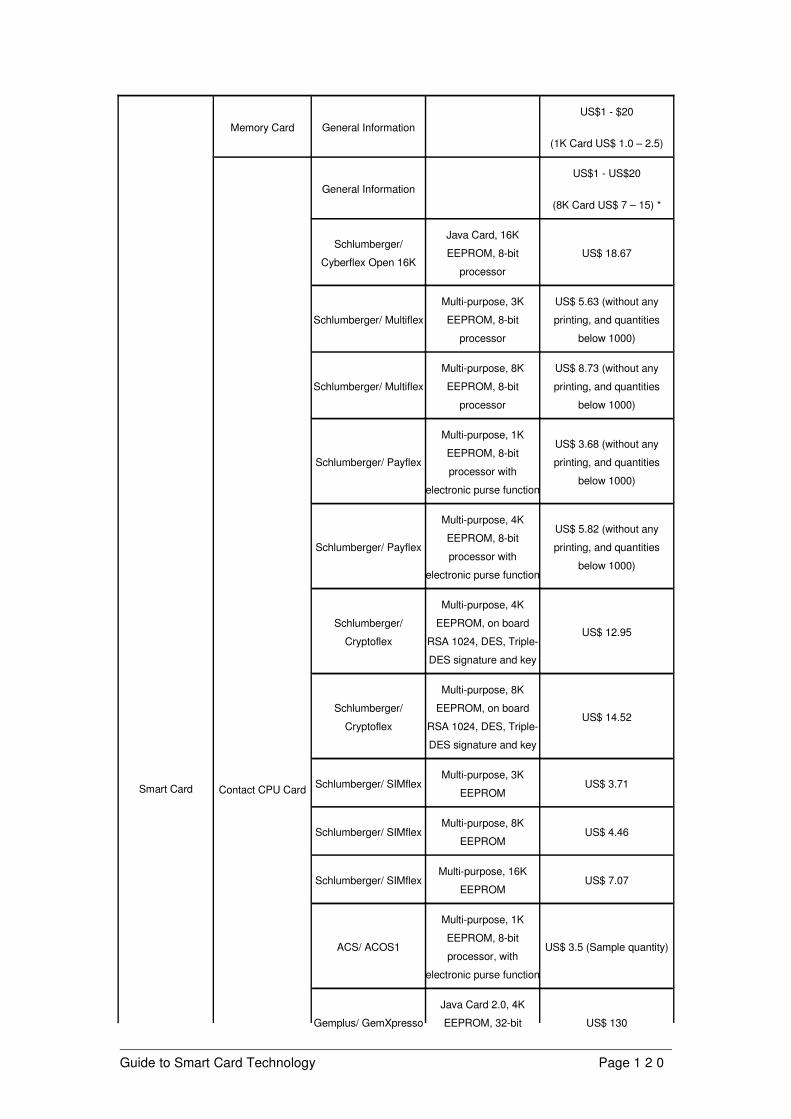

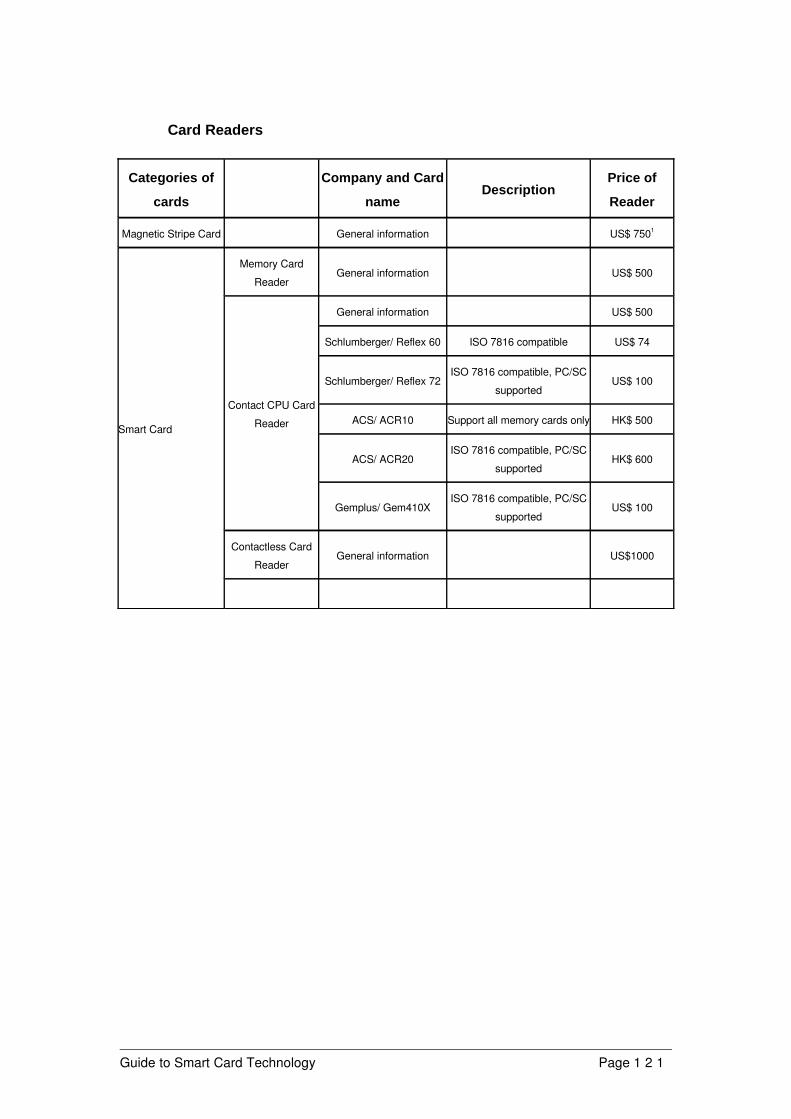

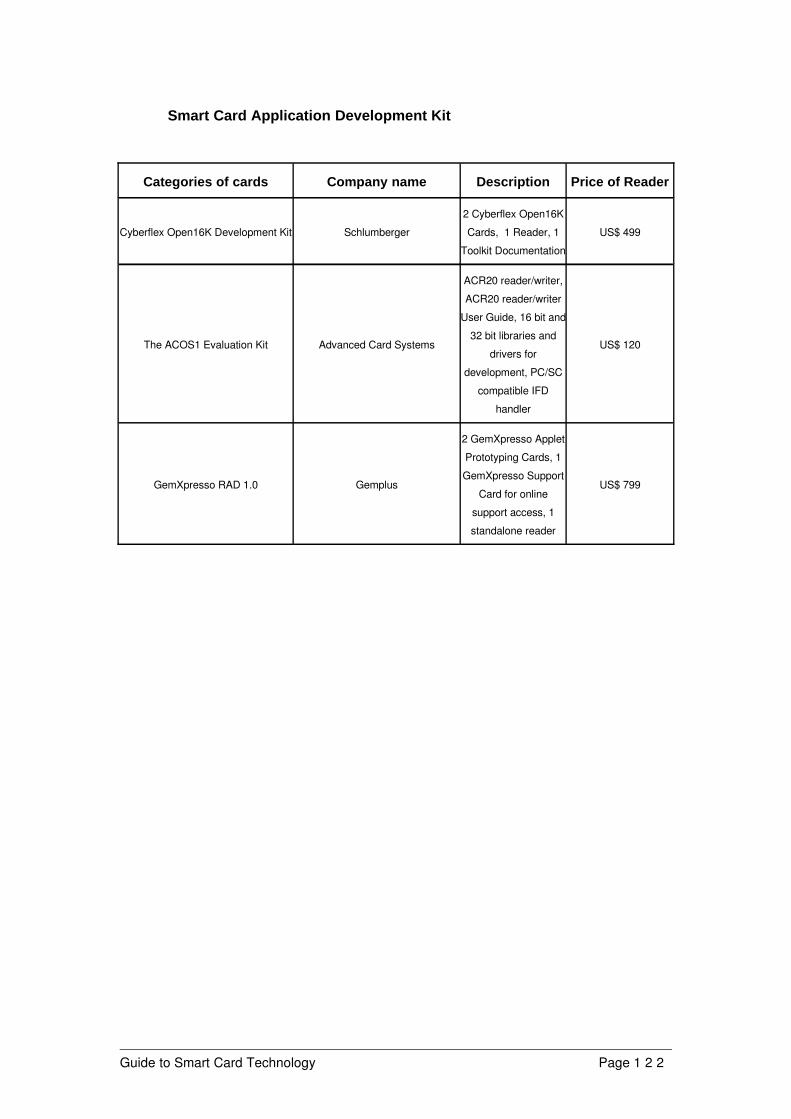

A. Price Comparison of different cards and readers...................................119 B. Resources.................................................................................................123

Collections of Smart Card Books...............................................................123 Collections of General Smart Card Internet Resources.............................123 Collections of Java Card Technology on Internet......................................124 Collections of Smart Card Security Technology on Internet.......................125 Collections of Smart Card Payment Technology on Internet.....................125 Collections of Smart Card Vendors............................................................126

Guide to Smart Card Technology Page 2

PrefaceThis handbook aims to provide a comprehensive overview of the current state of

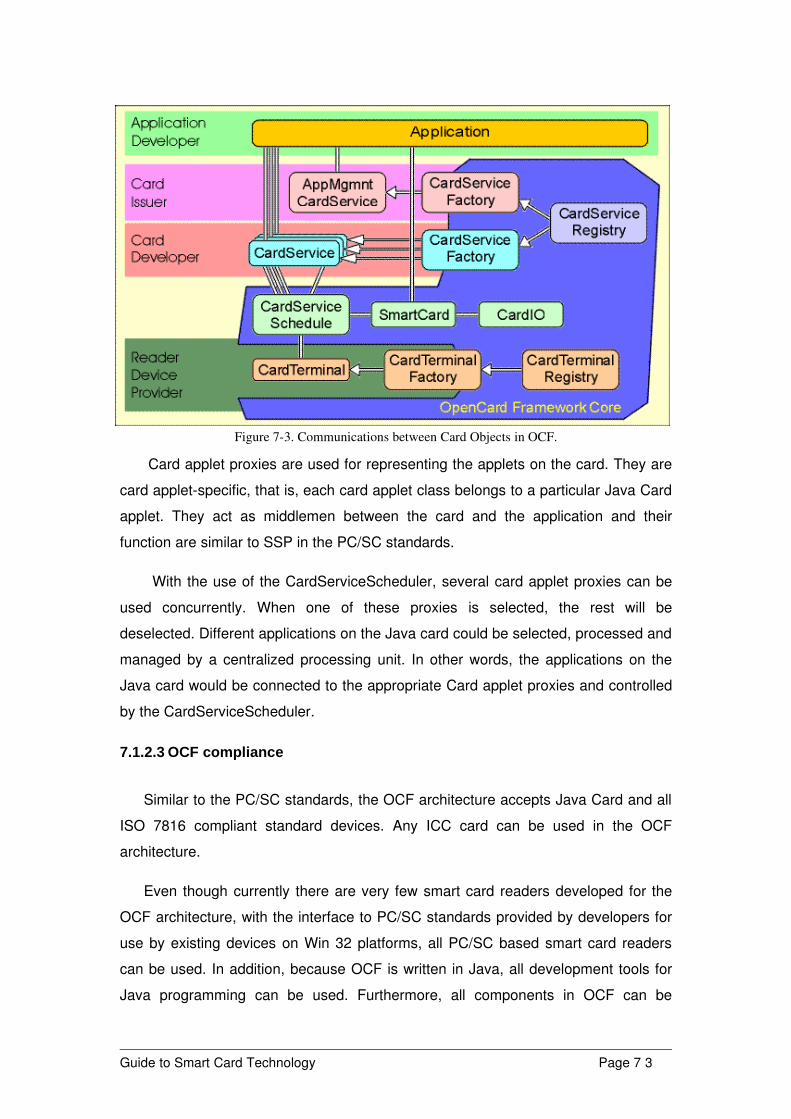

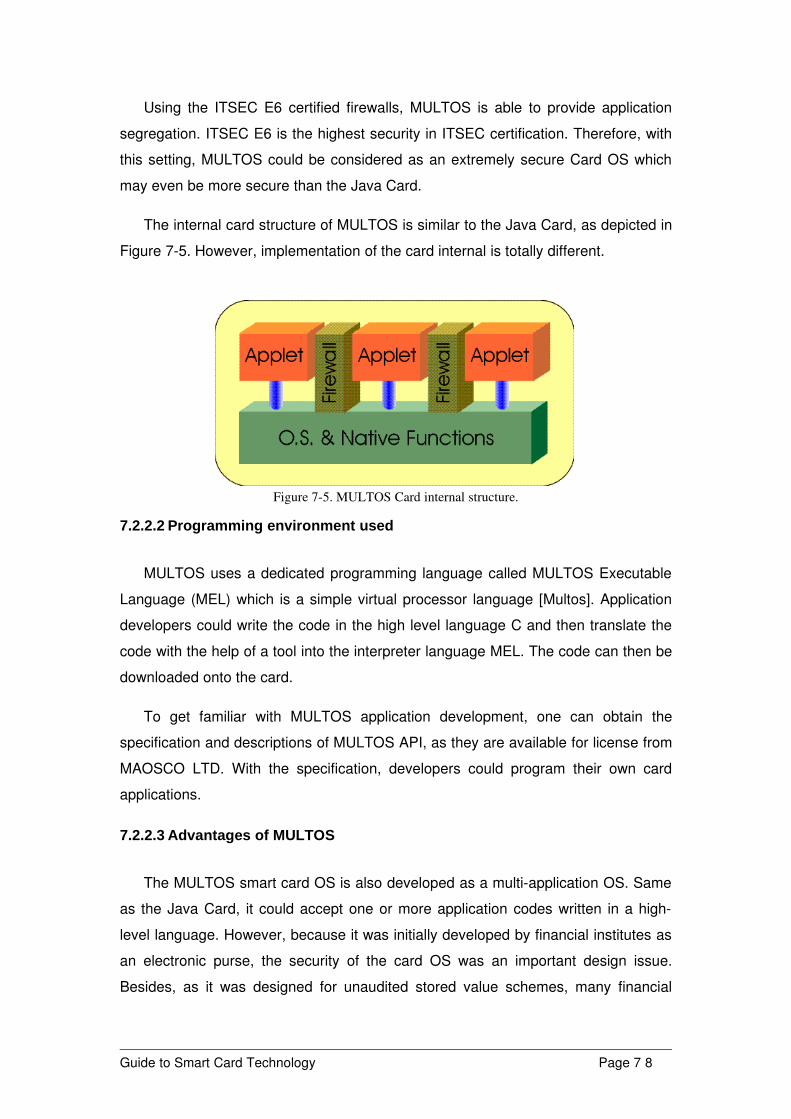

the art in smart card software technology development, applications, and future trends. The information would be useful to IT managers and executives wishing to explore the possibility of developing smart card applications.

The handbook consists of three sections. The basic concepts of smart cards and current applications are presented in the first section in layman's language. The second section gets into some of the technical aspects of smart card internals, and offers suggestions on smart card development procedures as well as general ideas in programming smart cards, including the new Java Card. This section is for programmers and IT managers who would like to go beyond the basic concepts and get an idea on what it takes to develop smart card applications. Finally, the third section presents our views on future trends in smart card development framework, standards and possible applications. A list of useful reference materials is also included.

The growth of smart card adoption in Asia is increasing rapidly and we believe this technology will be an important one in the near future. The Cyberspace Center is working to develop the security, biometric identification, micropayment and other aspects of smart card technology for use over the Internet. The handbook summarizes some of our experience in this work.

Many people have contributed to the handbook, especially Ricci Ieong, Andy Fung, Ivan Leung, Patrick Hung, James Pang and Ronald Chan. Ricci, Ivan, Andy and Patrick in particular, wrote parts of the handbook.

This document can be accessed online from the Cyberspace Center's home page http://www.cyber.ust.hk. Some chapters are actually better viewed online since they provide URLs directly to sources of additional information.

Finally, I would like to acknowledge the Industry Department of the Hong Kong SAR for funding the Cyberspace Center. Our objective is to help Hong Kong industries make more effective use of the Internet to enhance their competitiveness

Guide to Smart Card Technology Page 3

in the world markets. This and our other handbooks are part of the effort in attaining this goal. Please visit our web site to learn about some of our other activities.

Samuel ChansonDirectorCyberspace Center

Guide to Smart Card Technology Page 4

1. INTRODUCTION

Smart card technology has been around for more than 20 years. Since its first introduction into the market, its main application is for the payphone system. As card manufacturing cost decreases, smart card usage has expanded. Its use in Asia is expected to be growing at a much faster pace than in Europe. According to a survey performed by Ovum Ltd. [Microsoft1998a], the number of smart card units will reach 2.7 billion by 2003. The largest markets will be in prepayment applications, followed by access control, and electronic cash applications. According to a recent study by Dataquest [Microsoft1998c], the overall market for memory and microprocessorbased cards will grow from 544 million units in 1995 to 3.4 billion units by 2001. Of that figure, microprocessorbased smart cards, which accounted for only 84 million units in 1995 will grow to 1.2 billion units in 2001.

Based on the report from Hong Kong SAR Government Industry Department on the Development and Manufacturing Technology of Smart Card [HKSAR1997], Hong Kong industries have the capability and should participate in development and manufacturing of smart card IC chips, readers and card operating systems. To promote this, Hong Kong SAR government has decided to form a Hong Kong Smart Card Forum. Under this active participation and encouragement from the Hong Kong SAR Government, smart card development and support will expand in Hong Kong.

Although the Octopus card is relatively new to Hong Kong, smart cards have already been introduced in Hong Kong for at least two years. These include Mondex by Hong Kong bank and GSM cards in the mobile phone market. However, using this powerful and highly secure card on Personal computer (PC) as well as the Internet is still not common. Many international companies have identified the smart card as one of the new directions in electronic money and personal identification and authentication tools.

In May 1996, several companies including Microsoft, HewlettPacket and Schlumberger formed a PC/SC workgroup which aimed at integrating the smart card with personal computer (PC). This workgroup mainly concentrates on producing a

Guide to Smart Card Technology Page 5

common smart card and PC interface standards for the smart card and PC software producers. Many of the interface standards and hierarchy have already been established. Some of these prototype products are now available on the market.

Moreover, Netscape and Microsoft have also announced that the smart card will be their new direction in computer security and electronic commerce area. Microsoft has even published some documents on its role in the smart card market. Although it will not be a smart card manufacturing company, it has indicated that the smart card will be a key component in Microsoft Windows 98 and Windows NT 5.0. Together with the latest smart card operating system announcement [Microsoft1998a], Microsoft will be actively involved in the smart card market. Furthermore, programming modules for smart cards using Visual C++, Visual J++ and Visual Basic have also been developed.

The Cyberspace Center believes smart card technology will play a major role in Internet applications in the future. Therefore, we decided to start evaluating the available Smart card development tools and study the use of Smart card in Internet security and electronic commerce. With firsthand information and experience, we will be able to provide advice and assistance to the Hong Kong Industry.

The smart card is expected to be used in many applications and especially in personal security related applications such as access control, computer logon, secure email sending and retrieving services.

The reason for this growth lies in the smart card’s portability and security characteristics. In addition, as the recent growth of palmtop computers shows, people are looking for smaller and smaller devices for carrying their data with them. Smart card provides a good solution for many applications.

Applications are the driving force behind the new smart card market. Many of these applications have already been implemented, such as prepayment for services, credit and debit card, loyalty card, and access control card. The most commonly known example is the prepayment services cards, namely, prepaid phone cards, transportation cards and parking cards. Based on the epurse card, people could perform bank transaction from ATM machines at home or in the bank. With the use of loyalty cards, companies could store discount information and shopping preferences of their customers. Using these shopping preferences, companies could

Guide to Smart Card Technology Page 6

design new strategies for the users. Access control systems to buildings, computers or other secure areas will soon be handled by a single smart card.

In this handbook, we shall briefly describe what smart card is and how it can be used in different applications. The aim of this handbook is to provide a business and executive overview to companies that wish to join the smart card era. This handbook is divided into 8 chapters classified into 3 sections – Smart card Overview, Smart card in Details, and Smart card in the Future.

In the first section, basic concepts of smart cards will be described. In chapter 2, we review the history of smart cards. Then we outline the different types of smart cards and their standards. Current applications and uses of smart cards are mentioned in chapter 3.

In the second section, technical aspects of smart card internals as well as programming tips are briefly described in chapter 4. Because programming and design methodology for the Java card is different from traditional card programming, in chapter 5, we describe the basics in Java Card programming. In chapter 6, procedures of smart card development are given.

In the last section of this handbook, the future of smart card development is presented. Different ideas on future smart card applications are used in formulating a forecast in chapter 7.

Lastly, we conclude the handbook with a summary of different research, survey and reports on smart cards. References and glossaries are provided at the end of this handbook.

We hope that based on our handbook, company executives, technical managers and software developers would gain knowledge and insight into the emerging smart card technology and applications.

Guide to Smart Card Technology Page 7

Part I. Smart card Overview

Guide to Smart Card Technology Page 8

2. SMART CARD BASICA smart card is a plastic card with a microprocessor chip embedded in it. The

card looks like a normal credit card except for its metal contact (in contact card only), but applications performed could be totally different. Other than normal credit card and bankcard functions, a smart card could act as an electronic wallet where electronic cash is kept. With the appropriate software, it could also be used as a secure access control token ranging from door access control to computer authentication.

The term “smart card” has different meanings in different books [Guthery1998, Rankl1997] because smart cards have been used in different applications. In this chapter, we provide our definition of “smart card” to put the subsequent chapters in context. We also describe the development history of smart cards and depict the types of card available on market. Finally, descriptions on different smart card standards, such as ISO and EMV are given at the end of this chapter.

2.1 What is smart cardIn the article “Smart cards: A primer” [DiGiorgio1997a], the smart card is defined

as a “credit card” with a “brain” on it, the brain being a small embedded computer chip. Because of this “embedded brain”, smart card is also known as chip or integrated circuit (IC) card. Some types of smart card may have a microprocessor embedded, while others may only have a nonvolatile memory content included. In general, a plastic card with a chip embedded inside can be considered as a smart card.

In either type of smart card, the storage capacity of its memory content is much larger than that in magnetic stripe cards. The total storage capacity of a magnetic stripe card is 125 bytes while the typical storage capacity of a smart card ranges from 1K bytes to 64K bytes. In other words, the memory content of a large capacity smart card can hold the data content of more than 500 magnetic stripe cards.

Obviously, large storage capacity is one of the advantages in using smart card, but the singlemost important feature of smart card consists of the fact that their

Guide to Smart Card Technology Page 9

stored data can be protected against unauthorized access and tampering. Inside a smart card, access to the memory content is controlled by a secure logic circuit within the chip. As access to data can only be performed via a serial interface supervised by the operating system and the secure logic system, confidential data written onto the card is prevented from unauthorized external access. This secret data can only be processed internally by the microprocessor.

Due to the high security level of smart cards and its offline nature, it is extremely difficult to "hack" the value off a card, or otherwise put unauthorized information on the card. Because it is hard to get the data without authorization, and because it fits in one’s pocket, a smart card is uniquely appropriate for secure and convenient data storage. Without permission of the card holder, data could not be captured or modified. Therefore, smart card could further enhance the data privacy of user.

Therefore, smart card is not only a data store, but also a programmable, portable, tamperresistant memory storage. Microsoft considers smart card as an extension of a personal computer and the key component of the publickey infrastructure in Microsoft Windows 98 and 2000 (previous known as Windows NT 5.0) [Microsoft1997a].

2.2 History of smart card developmentA card embedded with a microprocessor was first invented by 2 German

engineers in 1967. It was not publicized until Roland Moreno, a French journalist, announced the Smart Card patent in France in 1974 [Rankl1997]. With the advances in microprocessor manufacturing technology, the development cost of the smart card has been greatly reduced. In 1984, a breakthrough was achieved when French Postal and Telecommunications services (PTT) successfully carried out a field trial with telephone cards. Since then, smart cards are no longer tied to the traditional bankcard market even though the phone card market is still the largest market of smart cards in 1997.

Due to the establishment of the ISO7816 specification in 1987 (a worldwide smart card interface standard), the smart card format is now standardized. Nowadays, smart cards from different vendors could communicate with the host machine using a common set of language.

Guide to Smart Card Technology Page 1 0

2.3 Different types of smart cardsAccording to the definitions of “smart card” in the Smart card technology

frequently asked questions list [Priisalu1995], the word smart card has three different meanings:

• IC card with ISO 7816 interface• Processor IC card• Personal identity token containing ICs

Basically, based on their physical characteristics, IC cards can be categorized into 4 main types, memory card, contact CPU card, contactless card and combi card.

2.3.1 Memory Cards

A memory card is a card with only memory and access logic onboard. Similar to the magnetic stripe card, a memory card can only be used for data storage. No data processing capability should be expected. Without the onboard CPU, memory cards use a synchronous communication mechanism between the reader and the card where the communication channel is always under the direct control of the card reader. Data stored on the card can be retrieved with an appropriate command to the card.

In traditional memory cards, no security control logic is included. Therefore, unauthorized access to the memory content on the card could not be prevented. While in current memory cards, with the security control logic programmed on the card, access to the protection zone is restricted to users with the proper password only.

2.3.2 Contact CPU Cards

A more sophisticated version of smart card is the contact CPU card. A microprocessor is embedded in the card. With this real “brain”, program stored inside the chip can be executed. Inside the same chip, there are four other functional blocks: the maskROM, Nonvolatile memory, RAM and I/O port [HKSAR1997, Rankl1997].

Except for the microprocessor unit, a memory card contains almost all components that are included in a contact CPU card. Both of them consist of Non

Guide to Smart Card Technology Page 1 1

volatile memory, RAM, ROM and I/O unit. Based on ISO 7816 specifications, the external appearance of these contact smart cards is exactly the same. The only difference is the existence of the CPU and the use of ROM. In the CPU card, ROM is masked with the chip’s operating system which executes the commands issued by the terminal, and returns the corresponding results. Data and application program codes are stored in the nonvolatile memory, usually EEPROM, which could be modified after the card manufacturing stage.

One of the main features of a CPU card is security. In fact, contact CPU card has been mainly adopted for secure data transaction. If a user could not successfully authenticate him/herself to the CPU, data kept on the card could not be retrieved. Therefore, even when a smart card is lost, the data stored inside the card will not be exposed if the data is properly stored [Rankl1997]. Also, as a secure portable computer, a CPU card can process any internal data securely and outputs the calculated result to the terminal.

2.3.3 Contactless Cards

Even though contact CPU smart card is more secure than memory card, it may not be suitable for all kinds of applications, especially where massive transactions are involved, such as transportation uses. Because in public transport uses, personal data must be captured by the reader within a short period of time, contact smart card which requires the user to insert the card to the reader before the data can be captured from the card would not be a suitable choice. With the use of radio frequency, the contactless smart card can transmit user data from a fairly long distance within a short activation period. The card holder would not have to insert the card into the reader. The whole transaction process could be performed without removing the card from the user’s wallet.

Contactless smart cards use a technology that enables card readers to provide power for transactions and communications without making physical contact with the cards. Usually electromagnetic signal is used for communication between the card and the reader. The power necessary to run the chip on the card could either be supplied by the battery embedded in the card or transmitted at microwave frequencies from the reader onto the card.

Guide to Smart Card Technology Page 1 2

Contactless card is highly suitable for large quantity of card access and data transaction. However, contactless smart card has not been standardized. There are about 16 different contactless card technologies and card types in the market [ADE]. Each of these cards has its specific advantages, but they may not be compatible with each other. Nevertheless, because of its high production cost and the technology is relatively new, this type of cards has not been widely adopted.

2.3.4 CombiCard

At the current stage, contact and contactless smart cards are using two different communication protocols and development processes. Both cards have their advantages and disadvantages. Contact smart cards have higher level of security and readilyavailable infrastructure, while contactless smart cards provide a more efficient and convenient transaction environment. In order to provide customers with the advantages of these two cards, two methods could be employed. The first method is to build a hybrid card reader, which could understand the protocols of both types of cards. The second method is to create a card that combines the contact functions with the contactless functions. Because the manufacturing cost of the hybrid reader is very expensive, the later solution is usually chosen.

Sometimes, the term “combi card” is being misused by manufacturers. In general, there are two types of combine contactcontactless smart cards, namely the hybrid card and the combi card. Both cards have contact and contactless parts embedded together in the plastic card. However, in the hybrid card, the contact IC chip and contactless chip are separate modules. No electrical connections have been included for communications between the two chips. These two modules can be considered as separate but coexisting chips on the same card. While in the combi card, the contact and contactless chips could communicate between themselves, thus giving the combi card the capability to talk with external environment via either the contact or contactless method.

As the combi card possess the advantages of both contact and contactless cards, the only reason that is hindering its acceptance is cost. When the cost and technical obstacles are overcome, combi cards will become a popular smart card solution.

2.4 Different standards of smart cards

Guide to Smart Card Technology Page 1 3

Throughout the history of smart card development, various standards have been established for resolving the interoperability problem. The very first standard is the ISO 7816 smart card standard published by the International Organization for Standardization (ISO) in 1987. Before this, card vendors and manufacturers developed their own proprietary cards and readers which could not interoperate. With the ISO standard, smart cards could communicate using the same protocol. The physical appearance and dimensions of a card is also fixed. The meaning and location of the contacts, the protocols and contents of the high and low level messages exchanged with the IC card are all standardized. This ensures that card manufactured and issued by one company can be accepted by a device from other companies. Because this specification is important to card programming development, details of this standard is given in Chapter 4, “Technical Aspects of smart card”, of this handbook.

Two other important standards in this area are EMV (Europay, Mastercard and Visa) and GSM (Global Standard for Mobile Communications). EMV standard is for debit/credit cards where major international financial institutions Visa, Mastercard and Europay are involved. It started in 1993 and was finalized in 1996 [HKSAR1997]. This standard covers the electromechanical, protocol, data elements and instruction parts together with the transactions involving bank microprocessor smart cards. The goal of the EMV specification is for payment systems to share a common Point of Sales (POS) Terminal, as they do for magnetic stripe applications. Because the magnetic stripebased banking card would soon be replaced by the smart card, this standard has to be established to ensure that the new smart card based banking card would be compatible with the bank transaction system. Based on this specification, all bankrelated smart card solutions would be compatible with one another as well as the previous magnetic stripe card solution. Terminal manufacturers could develop and modify their own sets of API in EMV standard for their terminals, so these terminals could be used in different payment systems. Credit, debit, electronic purse and loyalty functions could be processed on these EMVcompliant terminals. With the flexibility provided by the EMV standard, banks are allowed to add their own options and special requirements in the smart card payment system.

The GSM standard is one of the most important smart card and digital mobile telecommunication standards. GSM specification started in 1982 under CEPT

Guide to Smart Card Technology Page 1 4

(Conference Europeenne des Postes et Telecommunications) and was later continued by ETSI (European Telecommunications Standards Institute). Originally, this specification is designated for the mobile phone network. However, when the smart card is used in the mobile phone system as the Subscriber Identification Module (SIM), parts of the GSM specification becomes a smart card standard. This part of the GSM specification started in January 1988 by the Subscriber Identification Module Expert Group (SIMEG).

Within a GSM network, all GSM subscribers would be issued a SIM card which can be viewed as the subscriber’s key into the network. The size of a SIM card is fixed to be either the normal credit card or mini card size. Because this card is used for handling the GSM network functions, a rather high performance microcontroller (a 16bit microprocessor) is used and the EEPROM memory is dedicated for storing the application data, including the network parameters and subscriber data.

The GSM specification is divided into two sections. The first section describes the general functional characteristics, while the second section deals with the interface description and logical structures of a SIM card. Details of this specification are given in [Scourias].

Before the smart card could be widely adopted by the market, one or more standardized card development environment is needed. Currently, four significant smart card standards have been recently established in the smart card industry, they are PC/SC, OpenCard Framework, JavaCard and MULTOS and all of them are compatible to the ISO smart card standard. Details of these specifications are briefly mentioned in chapters 5 and 7 of this handbook while other specifications could be found in [CityU1997].

Guide to Smart Card Technology Page 1 5

3.CURRENT SMART CARD APPLICATIONS

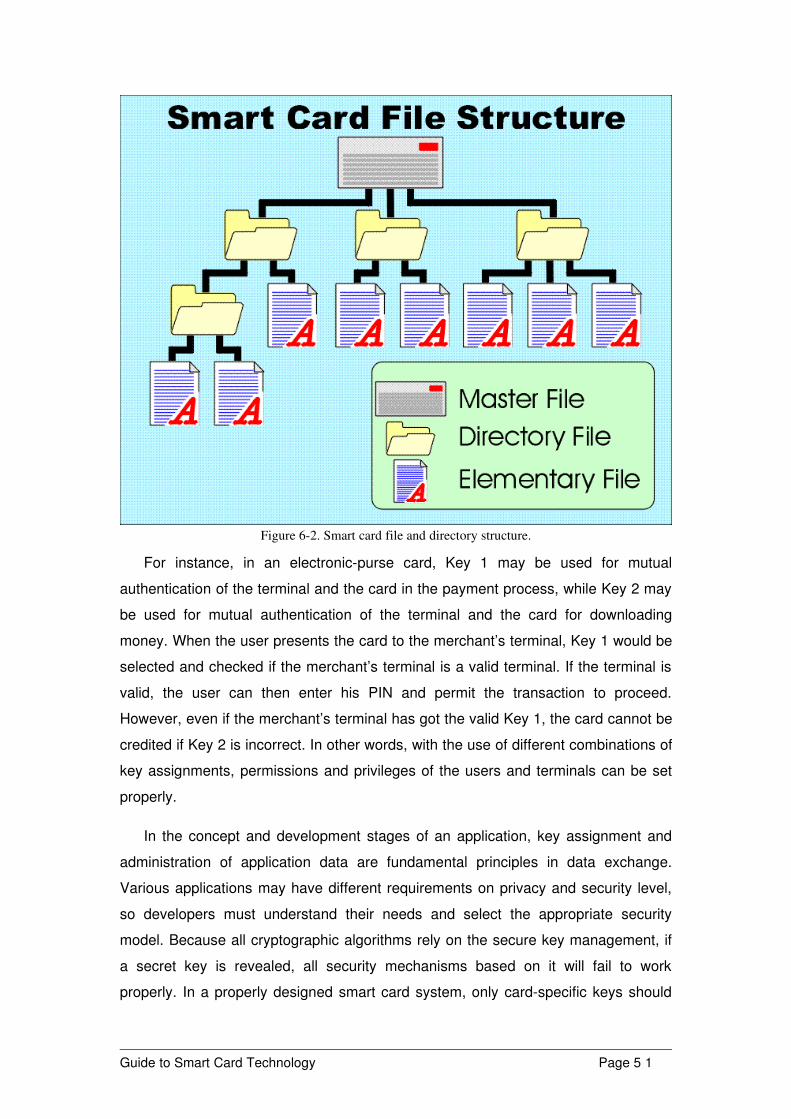

With the rapid expansion of Internet technology and electronic commerce, smart cards are now more widely accepted in the commercial market as storedvalue and secure storage cards. Moreover, it has also been widely used as an identity card. For instance, in City University of Hong Kong, the old student/staff cards have been replaced by the hybridcard based identity cards. This identity card can be used for normal access control as well as electronic payment.

The smart card has also been used in transportation such as the Octopus card which has been adopted by the MTRC and KCRC to replace of the old Magnetic stripe card. Medical record can also be stored in the smart card. This enables critical information of the patient to be retrieved whenever it is required. With the help of smart card technology, many secure data such as the computer login name and password can also be kept, so user need not remember a large number of passwords.

In this chapter, we shall briefly describe some current applications of smart cards. These applications can be classified into 6 main categories: Electronic Payment, Security and Authentication, Transportation, Telecommunications, Loyalty Program and Health Care Applications.

3.1 Electronic payment Applications

3.1.1 Electronic Purse

The Electronic Purse is also known as electronic cash. Funds can be loaded onto a card for use as cash. The electronic cash can be used for small purchases without necessarily requiring the authorization of a PIN. The card is credited from the cardholder’s bank account or some other ways. When it is used to purchase goods or services, electronic value is deducted from the card and transferred to the

Guide to Smart Card Technology Page 1 6

retailer’s account. Similar to a real wallet, the cardholder could credit his/her card at the bank any time when required.

Electronic cash transactions do not usually require the use of a PIN. This speeds up the transactions but the electronic cash on the card is then vulnerable like conventional cash. The amounts involved, fortunately, are usually small, so loses will not be significant. Widespread adoption of electronic cash will reduce the costs to banks and retailers in handling large quantities of cash.

Since 1994, there has been significant development of Intersector electronic purse applications in Europe which has been extended to outside of Europe. Several global card projects have been developed for this purpose, such as Proton card by Banksys, VisaCash by Visa International and Mondex card by Mastercard [Bull1998]. These have all been adopted by shops from all over the world.

3.1.2 Stored Value Cards

Another use of smart cards in electronic commerce is Electronic token. It is an example of the storedvalue card. The principle is that some memory in the smart card is set aside to store electronic tokens or electronic tickets. A smart card can store tokens for different services and each of the tokens can be refilled, depending on the types of the memory card. This allows the cost to be distributed over a number of services and over a much longer life span.

For example, the card could be used to pay for gas and instead of putting coins in a parking meter. Consumers load up the card from a vending machine. The card can then be used to operate the meters. One advantage of this system is that collections of coins would no longer be necessary. This would reduce the operation overhead and eliminate theft. This would also benefit the consumer as tokens could be bought and stored in the card in advance so it is not necessary to carry many heavy coins around. It is also possible that the card could monitor patterns of use and return the information to the merchant as well as the consumer, so better shopping model could be derived [McCrindle1990].

3.2 Security and Authentication Applications

Guide to Smart Card Technology Page 1 7

3.2.1 Cryptographic uses

From the pointofview of the supplier and system operator, the main requirement of almost all machinereadable card systems is to ensure that the card presented is valid and the cardholder is indeed the person entitled to use that particular card. To verify the cardholder’s identity, users are required to enter their PIN code (personal identification number). This PIN code is kept in the card rather than on the terminals or host machines.

Identification and authentication procedures take place at the card terminal. One of the problems is to ensure that the card furnishes some sort of machinereadable authenticity criterion. This can be solved by the use of encrypted communications between the card and terminal. It is well known that encryption can be used to ensure secrecy of messages sent and also to authenticate messages.

In order to perform the encryption procedure, the cryptographic smart cards must have the following properties:

• The cards must have sufficient computational power to run the cryptographic algorithms.

• The cryptographic algorithms must be theoretically secure. This means that it is not possible to derive the secret key from the corresponding texts.

• The smart cards must be physically secure. It should not be possible to extract the secret key from the card’s memory.

Provided these conditions are met, and with advances in card microcontroller technology, the microprocessorbased smart card can be made to meet the required security level [Chaum1989].

For instance, Verisign and Schlumberger have developed the use of Cryptoflex smart card for carrying a Verisign Class 1 Digital ID [Verisign9701]. Cryptoflex card is the first cryptographic smart card in the industry, which is designed based on the PC/SC specifications. This enables the use of smart card for portable Internet access with Microsoft Internet Explorer 3.0 at all sites accepting Verisign Digital IDs.

In Michigan University, the Cyberflex card has been used for storing Kerberos keys in a secure login project [Michgan9701].

Guide to Smart Card Technology Page 1 8

3.2.2 Identity card

The identification of an individual is one of the most complex processes in the field of Information Technology. It requires both the individual to identify himself and for the system to recognize the incoming connection is generated by a legal user. The system then accepts responsibility for allowing all subsequent actions, sage in the knowledge that the user has authorization to do whatever he is asking of the system.

If a smart card is used, the information stored on the card can be verified locally against a ‘password’ or PIN before connection is made to the host. This prevents the password from being eavesdropped by perpetrators on the Internet.

Some of the smart cards will have personal data stored on the card. For example, the cardholder’s name, ID number, and date of birth [Devargas1992].

3.2.3 Access control card

The most common devices used to control access to private areas where sensitive work is being carried out or where data is held, are keys, badges and magnetic cards. These all have the same basic disadvantages: they can easily be duplicated and when stolen or passed on, they can allow entry by an unauthorized person. The smart card overcomes these weaknesses by being very difficult to be reproduced and capable of storing digitized personal characteristics. With suitable verification equipment, this data can be used at the point of entry to identify whether the user is the authorized cardholder. The card can also be individually personalized to allow access to limited facilities, depending on the holder’s security clearance. A log of the holder’s movements, through a security system, can be stored on the card as a security audit trail [McCrindle1990].

The card could contain information on the user’s privileges (i.e. access to secure areas of the building, automatic vehicle identification at entrances to company car parks, etc.) and time restrictions. All information are checked on the card itself. Access to different areas of the building can be distinguished by different PINs. Furthermore it can also track the user’s movement around the building [Devargas1992].

Guide to Smart Card Technology Page 1 9

3.2.4 Digital certificate

The most important security measures we encounter in our daily business have nothing to do with locks and guards. A combination of a signed message and the use of public key cryptosystem, so called digital signature, are typically used.

A digitally signed message containing a public key is called a certificate. In addition to a public key, a certificate typically contains a name, address, and other information describing the holder of the corresponding secret key. All of these carry the digital signature of a registry service that records public keys for all members of the community. To become a member of this community, a subscriber must do two things:

• Provide the directory service with a public key and the associated identification information so that other people will be able to verify his/her signature.

• Obtain the public key of the directory service so that he/she can verify other people’s signatures.

Because certificates are extremely tamper resistant, the authenticity of a certificate is a property of the certificate itself, rather than of the authenticity of the channel over which it was received. This important property allows certificates to be employed in very much the same way as a passport. The border police expect to see your passport and in most cases count on the passport’s tamper resistance to guarantee its authenticity. Because of the fragility of paper credentials, however, there are circumstances in which this is not considered adequate. In making a classified visit to a military installation, for example, no badge or letter of introduction by itself is sufficient. Prior arrangements must have been made using channels maintained for the purpose. Because public key certificates are more secure than any paper document, they can be safely authenticated by direct signature checking and no trusted directory is needed.

3.2.5 Computer login

Access to the Computer room and its services can be controlled by the smart card. In terms of network access, smart card can authenticate the user to the host.

Guide to Smart Card Technology Page 2 0

Furthermore, depending on the environment being protected the network access card can also perform the following functions:

• Manipulation of different authentication codes for different levels of security.• Use of biometric techniques as an added security measure.• Maintaining an audit trail of failures and attempted violations.

Meanwhile, in terms of access to the computer room itself, PIN checking can be done on the card without the need for hard wiring the access points to a central computer.

The identification of a user is usually done by means of a (Personal Identification Number) PIN. The PIN is verified by the microcomputer of the card with the PIN stored in its RAM. If the comparison is negative, the CPU will refuse to work. The chip also keeps tack of the number of consecutive wrong PIN entries. If this number reaches a preset threshold, the card blocks itself against any further use.

3.3 Transportation usesThe smart card can act as electronic money for car drivers who would need to

pay a fee before being able to use a road or tunnel. It would then contain a balance that can be increased at payment stations or in the prepaid process, and is decreased for each use.

If privacy is not an issue (i.e. the driver does not care if he is identified as using a particular stretch of motorway at a particular point in time), then the card could be linked to a bank debiting system as a debit card. Besides, the card could also act as a credit card.

Another example is the Octopus card. This service aims at reducing the amount of cash handled by the service provider and also increasing management information. This information would be invaluable in giving the customer the right service at the right time.

Each individual would possess a reloadable card that could either be paid directly (immediately) or as a credit payment based system where monthly settlement would be required. If the card has a positive balance, the card holder could use the card in any of the transport services by simply inserting the card into the cardreader which would be either on the bus or at the entrance to the MTR station.

Guide to Smart Card Technology Page 2 1

If the travel charge is different for different zones, then the card would need to be used at the entrance of the bus or station and also at the exit. This process would then calculate the amount owed for a certain journey [Devargas1992].

3.4 Telecommunication ApplicationsTelecommunication is one of the largest markets for smart card applications. In

1997, payphone cards occupy the largest share of the smart card market. Over 70% of the smart cards are issued as payphone cards [CardTech1997] and this will continue be the largest market in at least the next 3 years.

Since 1988, smart card has become an essential component in cellular phone systems. Network data, subscriber’s information and all mobile network critical data are kept inside the card. With this card, subscribers could make calls from any portable telephone. Moreover, through the IC card, any calls through the mobile phone could be encrypted, and thus ensure privacy. In the future, more and more valueadded services, such as electronic banking, could be supported by using this microprocessor card. Examples can be found in chapter 7.

3.5 HealthCare ApplicationsDue to the level of security provided for data storage, IC cards offer a new

perspective for healthcare applications. Medical applications of smart cards can be used for storing information including personal data, insurance policy, emergency medical information, hospital admission data and recent medical records. Numerous national hospitals in France, Germany and even Hong Kong have already started to implement this kind of healthcare card.

With the microcontroller onboard, smart cards could be used for managing the levels of information authorized for different users similar to a workflow control system. Doctors would be able to access the medical record from the patient’s card, while chemists could make use of the prescription information stored on the card for preparing the medical treatment. Emergency data kept on the patient’s card, which includes the cardholder’s identity, persons to contact in case of accident and special illness details, can be used for saving the patient’s life. In some countries, medical insurance is required for hospital payment. With the insurance records stored in the patient’s card, the administrative procedures are simplified.

Guide to Smart Card Technology Page 2 2

3.6 Loyalty ApplicationsLoyalty program is another important application of smart cards in the shopping

model. The preferred customer status together with detailed information on shopping habits is stored and processed on the smart card. With this information, merchants could derive better shopping model or tailormake personalized customer shopping profiles. In addition, this shopping habit profile is kept in the customer’s card; therefore, his/her shopping record could be kept confidential from unauthorized access.

As an extension to the loyalty application, stored value functions could be added. In current pay television systems, users’ preferences are kept together with the electronic payment scheme. Users would not have to set their preferences each time they use the television system. As this card will also be used as the key to the television, users would not be permitted to use the television box unless they have paid their television fee. So sufficient security and convenient television usage could be guaranteed.

Guide to Smart Card Technology Page 2 3

Part II. Smart card in details

Guide to Smart Card Technology Page 2 4

4.TECHNOLOGY ASPECTS OF SMART CARD

From the technical point of view, smart cards can be classified into two main types: programmable and nonprogrammable. A smart card application programmer can either put the application logic on the terminal, the card (if it is a programmable card) or both. We can view the nonprogrammable smart cards as external storage, just like a floppy disk, with security features. Therefore, we can design to store certain portable information on the smart card and the application logic is allocated on the terminal side. On the other hand, the programmable smart card, such as the Java card, allows the application logic (intelligence) to be partially built on the smart card. In this chapter, we are going to describe the overview concepts of smart card programming.

4.1 Overview of ISO 7816 Standards ISO 7816 is the interface standard for smart card. The following subparts are of

interest to the smart card application programmer:

ISO 78161: Physical characteristics of cardsDefines the dimensions of cards and the physical constraints.

ISO 78162: Dimensions and locations of the contactsDefines the dimensions, location and role of the electrical contacts (the power VCC, the ground GND, the clock CLK, the reset RST, the I/O port I/O, the programming power VPP and two additional reserved contacts for future use) on the microchip.

ISO 78163: Electronic signals and transmission protocolsDefines the characteristics of the electronic signals exchanged between the card and terminal and two communication protocols: T=0 (Asynchronous half duplex character transmission protocol) and T=1 (Asynchronous half duplex block transmission protocol)

ISO 78164: Interindustry commands for interchangeDefines a set of standard commands and a hierarchical file system structure.

Guide to Smart Card Technology Page 2 5

ISO 78165: Numbering system and registration procedure for application identifiersDefines a unique card application name.

ISO 78167: Interindustry commands for Structured Card Query Language (SCQL)Defines a set of commands to access smart card content and relational database structure.

Other parts are not covered here since smart card application programmers do not need to know them and also some of them are still under preparation. We shall discuss ISO 78163, ISO 78164 and ISO 78165 below.

4.2 Communication Protocol between Terminal and Smart Cards

The communication protocols between the terminal and the smart card are described in ISO 78163 (Transport Protocol) and ISO 78164 (Application Protocol). These two protocols are briefly described in this section.

The terminal initializes a smart card by transmitting a signal to the reset (RST) contact of the card. The card will response by transmitting a string of bytes to the terminal called the ATR (AnswerToReset). This string of bytes consists of two parts: the protocol bytes provide information about the communication protocols supported by the card and the historical bytes provide information about the type of card. An example is given for the ATR of ACS ACOS1 smart card (which is a type of memory card of Advanced Card System company):

Protocol Bytes Historical Bytes

3B BE 11 00 00 41 01 10 04 00 12 00 00 00 00 00 02 90 00 (in hexidecimal)

The details of ATR are described in the ISO 78163 standard. We briefly describe the first three bytes in the protocol bytes here. The bytes “3B” stand for the method of bit transfer. “BE” means that there is additional information (14 historical bytes). The bytes “11” describe the information of clock speed and bit transfer rate.

Guide to Smart Card Technology Page 2 6

The historical bytes give information about the references and versions of the card’s chip and operating system.

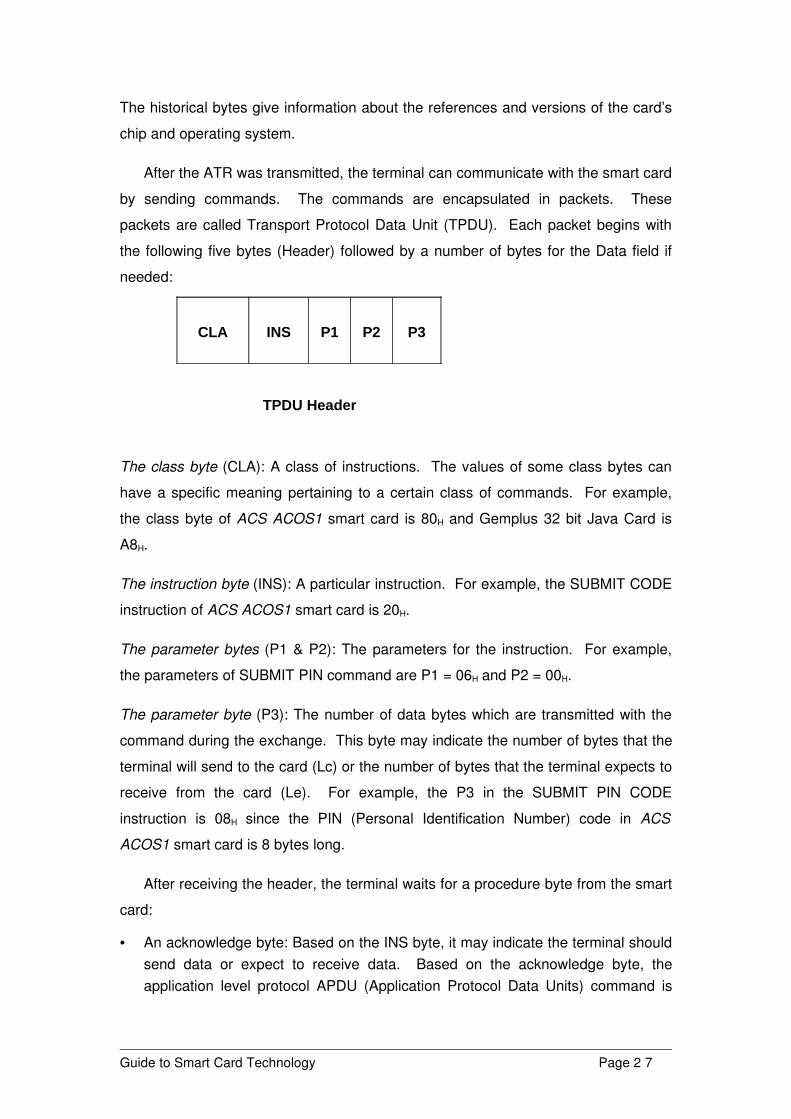

After the ATR was transmitted, the terminal can communicate with the smart card by sending commands. The commands are encapsulated in packets. These packets are called Transport Protocol Data Unit (TPDU). Each packet begins with the following five bytes (Header) followed by a number of bytes for the Data field if needed:

CLA INS P1 P2 P3

TPDU Header

The class byte (CLA): A class of instructions. The values of some class bytes can have a specific meaning pertaining to a certain class of commands. For example, the class byte of ACS ACOS1 smart card is 80H and Gemplus 32 bit Java Card is A8H.

The instruction byte (INS): A particular instruction. For example, the SUBMIT CODE instruction of ACS ACOS1 smart card is 20H.

The parameter bytes (P1 & P2): The parameters for the instruction. For example, the parameters of SUBMIT PIN command are P1 = 06H and P2 = 00H.

The parameter byte (P3): The number of data bytes which are transmitted with the command during the exchange. This byte may indicate the number of bytes that the terminal will send to the card (Lc) or the number of bytes that the terminal expects to receive from the card (Le). For example, the P3 in the SUBMIT PIN CODE instruction is 08H since the PIN (Personal Identification Number) code in ACS ACOS1 smart card is 8 bytes long.

After receiving the header, the terminal waits for a procedure byte from the smart card:

• An acknowledge byte: Based on the INS byte, it may indicate the terminal should send data or expect to receive data. Based on the acknowledge byte, the application level protocol APDU (Application Protocol Data Units) command is

Guide to Smart Card Technology Page 2 7

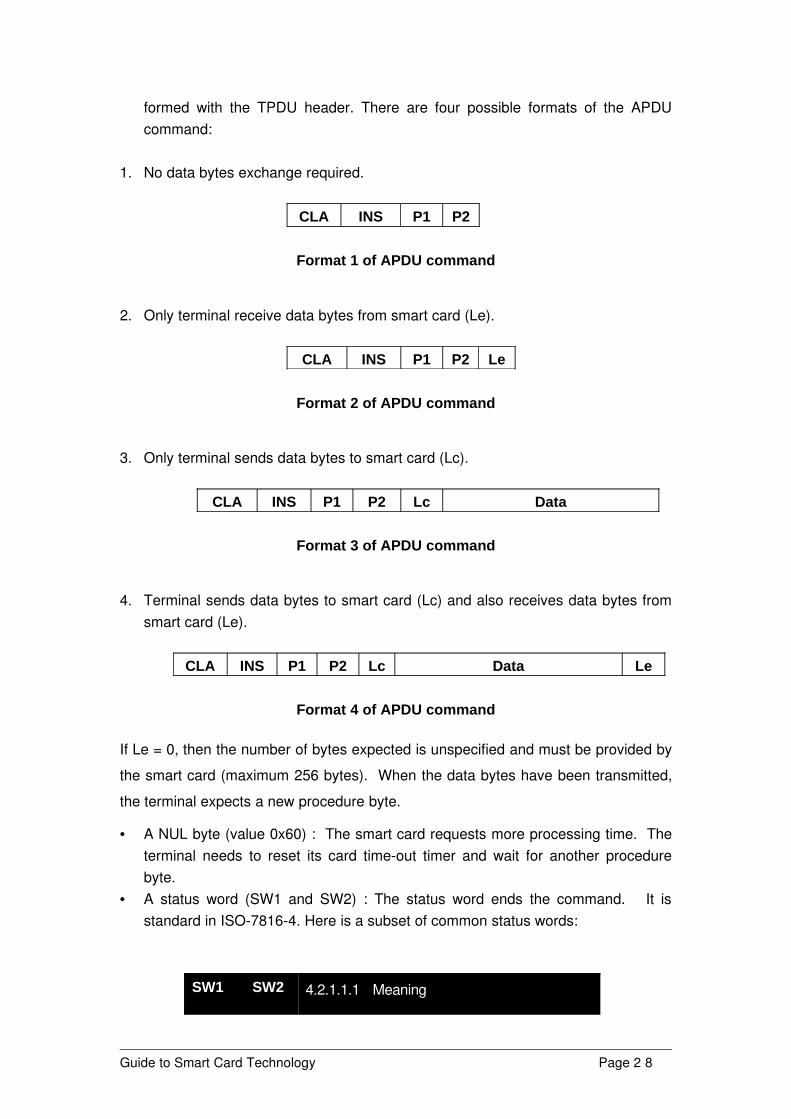

formed with the TPDU header. There are four possible formats of the APDU command:

1. No data bytes exchange required.

CLA INS P1 P2

Format 1 of APDU command

2. Only terminal receive data bytes from smart card (Le).

CLA INS P1 P2 Le

Format 2 of APDU command

3. Only terminal sends data bytes to smart card (Lc).

CLA INS P1 P2 Lc Data

Format 3 of APDU command

4. Terminal sends data bytes to smart card (Lc) and also receives data bytes from smart card (Le).

CLA INS P1 P2 Lc Data Le

Format 4 of APDU command

If Le = 0, then the number of bytes expected is unspecified and must be provided by the smart card (maximum 256 bytes). When the data bytes have been transmitted, the terminal expects a new procedure byte.

• A NUL byte (value 0x60) : The smart card requests more processing time. The terminal needs to reset its card timeout timer and wait for another procedure byte.

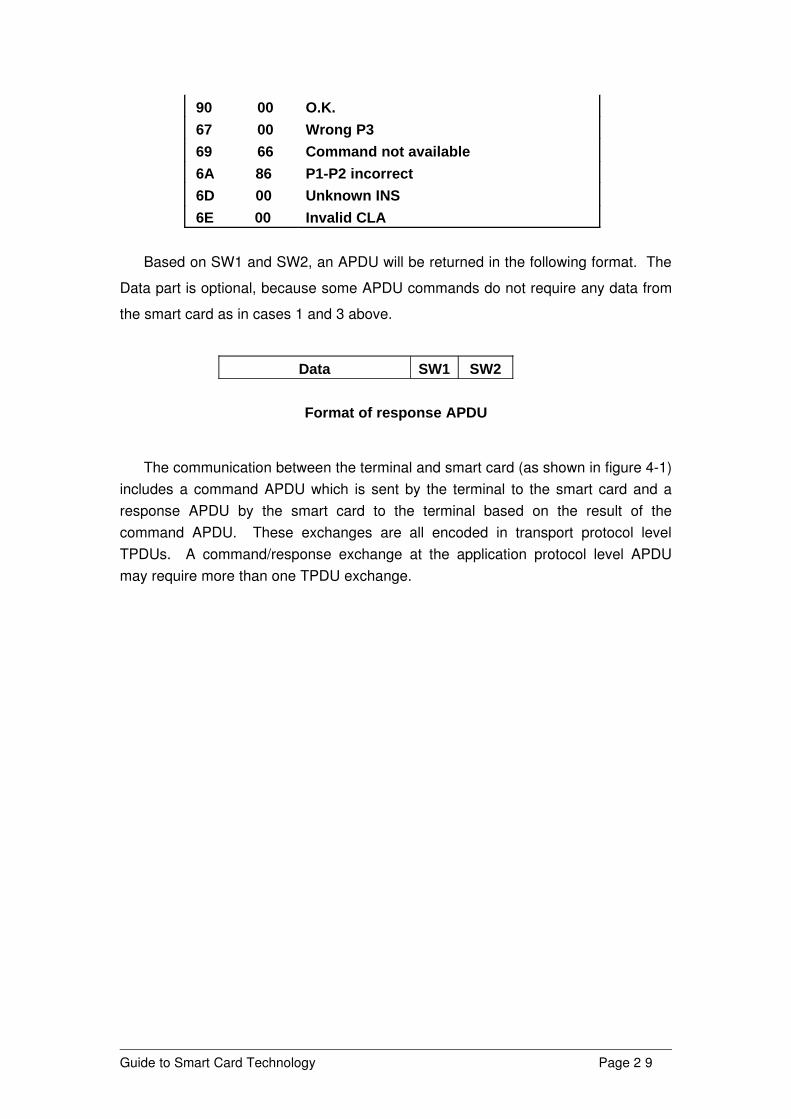

• A status word (SW1 and SW2) : The status word ends the command. It is standard in ISO78164. Here is a subset of common status words:

SW1 SW2 4.2.1.1.1 Meaning

Guide to Smart Card Technology Page 2 8

90 00 O.K. 67 00 Wrong P3 69 66 Command not available 6A 86 P1P2 incorrect 6D 00 Unknown INS 6E 00 Invalid CLA

Based on SW1 and SW2, an APDU will be returned in the following format. The Data part is optional, because some APDU commands do not require any data from the smart card as in cases 1 and 3 above.

Data SW1 SW2

Format of response APDU

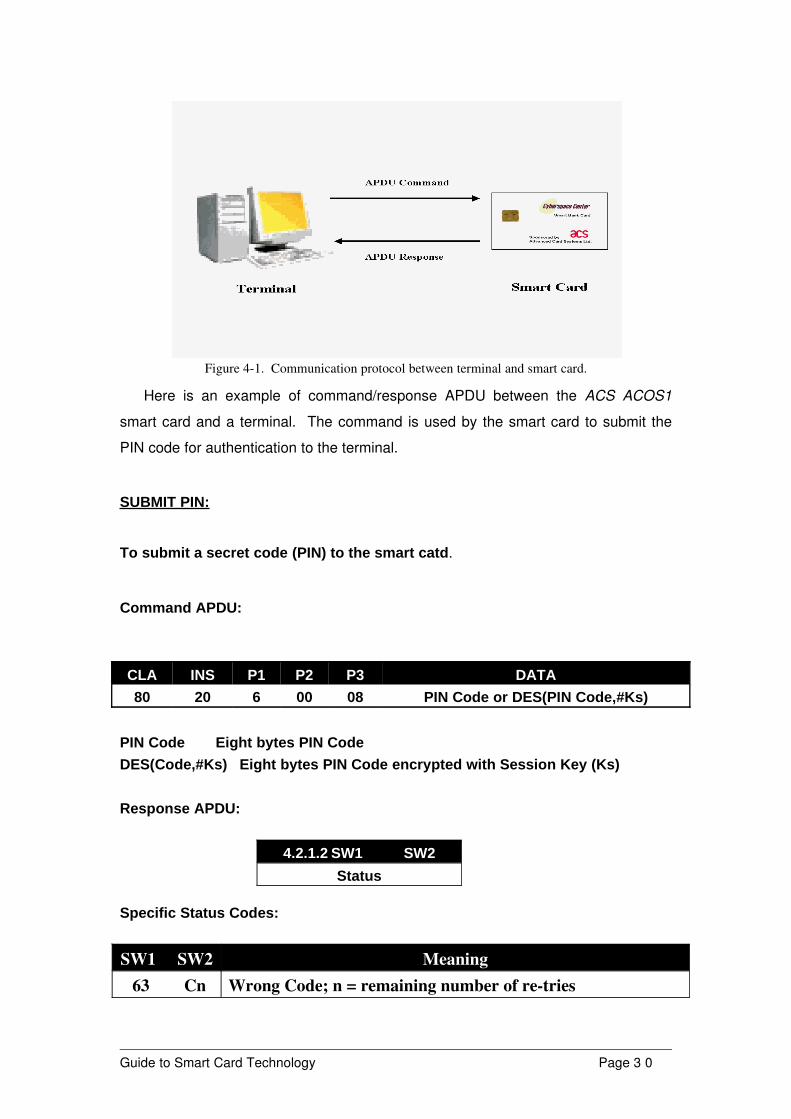

The communication between the terminal and smart card (as shown in figure 41) includes a command APDU which is sent by the terminal to the smart card and a response APDU by the smart card to the terminal based on the result of the command APDU. These exchanges are all encoded in transport protocol level TPDUs. A command/response exchange at the application protocol level APDU may require more than one TPDU exchange.

Guide to Smart Card Technology Page 2 9

Figure 41. Communication protocol between terminal and smart card.

Here is an example of command/response APDU between the ACS ACOS1 smart card and a terminal. The command is used by the smart card to submit the PIN code for authentication to the terminal.

SUBMIT PIN:

To submit a secret code (PIN) to the smart catd.

Command APDU:

CLA INS P1 P2 P3 DATA80 20 6 00 08 PIN Code or DES(PIN Code,#Ks)

PIN Code Eight bytes PIN CodeDES(Code,#Ks) Eight bytes PIN Code encrypted with Session Key (Ks)

Response APDU:

4.2.1.2 SW1 SW2Status

Specific Status Codes:

SW1 SW2 Meaning 63 Cn Wrong Code; n = remaining number of retries

Guide to Smart Card Technology Page 3 0

69 83 The specified Code is locked 69 85 Mutual Authentication not successfully completed prior to

the SUBMIT PIN CODE command

In the SUBMIT PIN procedure, the terminal can either submit the PIN code in plain text format (without encryption) or in DES encrypted format if the corresponding option bit DES in the Security Option Register is set.

4.3 Overview of File Systems The file system in the ISO78164 is one of the important components in the

smart card for data storage. The file system is a hierarchical file system like MSDOS:

• A file system has a root, which is called the master file (MF).• Directories which are called dedicated files are used to organize (DF).• Normal files are called elementary files (EF).

Files are referenced by a file identifier (FID) which is two bytes long. There are several kinds of elementary files:

• Transparent files, which are seen as a sequence of bytes.• Linear fixed files, which are seen as a sequence of fixedlength records.• Linear variable files, which are seen as a sequence of variablelength

records.• Cyclic files, which are seen as an endless sequence of fixedsize records.

In the ACS ACOS1 smart card, the files are defined and constructed in the personalization stage. The application program running on the terminal can then access the files using APDU commands if it is authenticated. Here is an example of SELECT FILE command which is used to select a data file for subsequent READ RECORD and WRITE RECORD commands.

SELECT FILE:

To select a data file for subsequent READ RECORD and WRITE RECORD commands.

Command APDU:

Guide to Smart Card Technology Page 3 1

CLA INS P1 P2 P3 DATA80 A4 00 00 02 File ID

File ID Two bytes file identifier

Response APDU:

4.3.1.1 SW1 SW2Status

Specific Status Codes:

SW1 SW2 Meaning 6A 82 File does not exist. 91 xx File selected.

xx is the number of the record in the User File Management File which contains the File Definition Block of the selected file.

4.4 Overview of Naming SchemeThe ISO 78165 standard defines a naming scheme for smart card applications. Each application is identified by an application identifier (AID). The AID is between 1 to 16 bytes long. The smart card provider needs to get a registered application provider identifier (RID) from ISO. The AID is constructed as shown below:

RID PIX

The first five bytes are the RID, and the last 11 bytes (PIX) can be freely assigned by the smart card provider.

4.5 Overview of the Security ArchitectureThere are two main security mechanisms provided for smart card applications:

access control and cryptography. For access control, the application or cardholder

Guide to Smart Card Technology Page 3 2

may need to submit a PIN (Personal Identification Number) before any APDU command. In the ACS ACOS1 smart card, the application also needs to submit the Issuer Code (IC) which is assigned by the smart card manufacturer in order to submit any APDU command. Furthermore, there is a set of Application Codes (AC) which can be set in order to enhance the access control in the file system. Each file is assigned a security attribute of Read and Write. Security Attributes define the security conditions that must be fulfilled to allow the respective operation. The communication channel between the smart card and terminal can be protected by cryptography like DES (symmetric algorithm) and RSA (publickey algorithm). Moreover, there may be other different specific security mechanisms provided by different smart card manufacturers. For example, the following security mechanisms are provided by the ACS ACOS1 smart card:

• DES and MAC calculation:DES refers to the DEA algorithm for data encryption and decryption. MAC refers to the algorithm for the generation of cryptographic checksum.

• Mutual Authentication and Session Key based on Random Numbers:Mutual Authentication is a process in which both the smart card and smart card reader verify each other’s validity. The Session Key is a result of the successful execution of the Mutual Authentication procedure. It is used for data encryption and decryption during a session. A session is defined as the time between the successful execution of a Mutual Authentication procedure and a reset of the card or the execution of another START SESSION command.

• Secret Codes:Secret Codes and the PIN code are used to selectively enable access to data stored in the card and to features and functions provided by the smart card.

• Secure Account Transaction Processing:Account Transaction Processing provides a mechanism for the secure and auditable manipulation of data in the Account Data Structure.

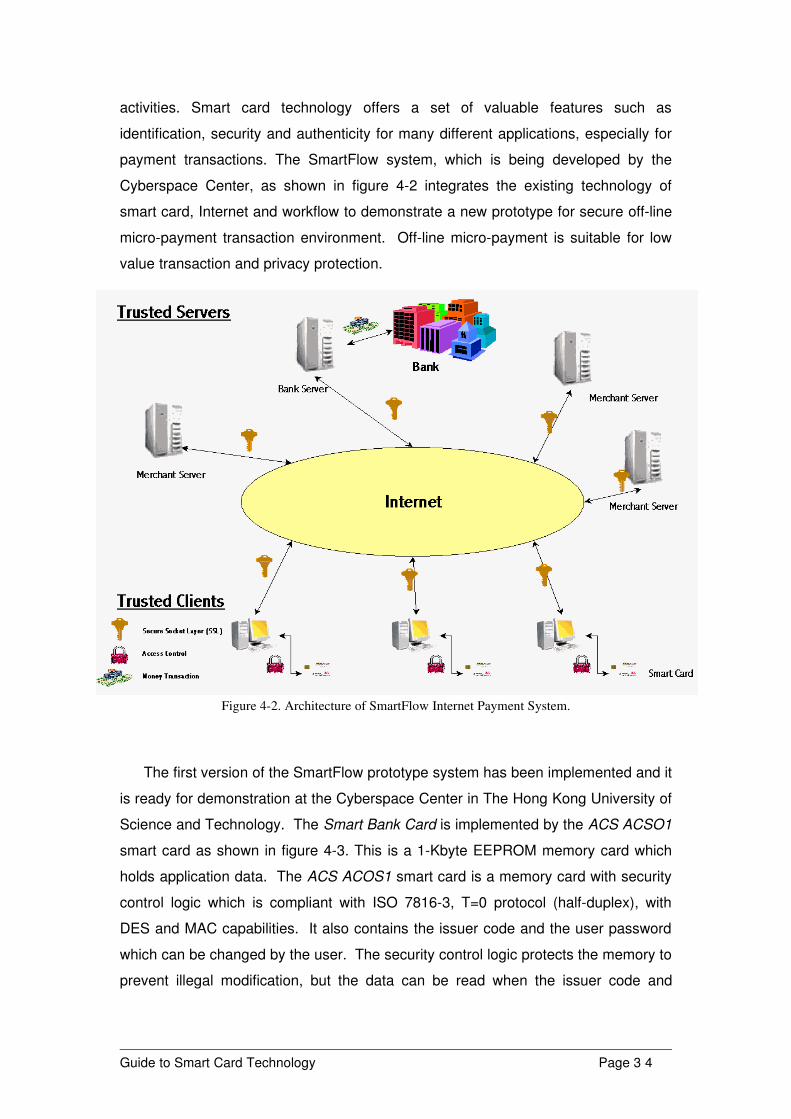

4.6 An Example of Smart Card Application : SmartFlow Internet Payment System

Electronic commerce on Internet is a popular research area, but the lack of secure payment transfer protocol is the main barrier to promote webbased business

Guide to Smart Card Technology Page 3 3

activities. Smart card technology offers a set of valuable features such as identification, security and authenticity for many different applications, especially for payment transactions. The SmartFlow system, which is being developed by the Cyberspace Center, as shown in figure 42 integrates the existing technology of smart card, Internet and workflow to demonstrate a new prototype for secure offline micropayment transaction environment. Offline micropayment is suitable for low value transaction and privacy protection.

Figure 42. Architecture of SmartFlow Internet Payment System.

The first version of the SmartFlow prototype system has been implemented and it is ready for demonstration at the Cyberspace Center in The Hong Kong University of Science and Technology. The Smart Bank Card is implemented by the ACS ACSO1 smart card as shown in figure 43. This is a 1Kbyte EEPROM memory card which holds application data. The ACS ACOS1 smart card is a memory card with security control logic which is compliant with ISO 78163, T=0 protocol (halfduplex), with DES and MAC capabilities. It also contains the issuer code and the user password which can be changed by the user. The security control logic protects the memory to prevent illegal modification, but the data can be read when the issuer code and

Guide to Smart Card Technology Page 3 4

password are correctly submitted. Also, different memory locations can be protected by different security controls.

Figure 43. ACS ACSO1 Smart Card in Cyberspace Center.

The system is developed on the Windows Platform using ActiveX which is written in Visual Basic to build the system logic and frontend. The backend is supported by the Windows NT Server and all the related data are stored and managed by the MS SQL Database Server. The system is supported by the Internet Information Server running on the Windows NT Server, and the communication channel is secured by Secure Socket Layer (SSL). We are using Internet Explorer 4.0 for the browser because the system is developed on Active X which is only supported by Internet Explorer as shown in figure 44.

Figure 44. SmartFlow Internet Payment System.

Guide to Smart Card Technology Page 3 5

For illustration, here is the source code of the Select_File function in the SmartFlow Internet Payment System. This function is used to select a file on the smart card. The APDU command of SELECT FILE was described earlier, the CLA is 80H, INS is A4H, P1 is 00H, P2 is 00H and P3 (Lc) is 02H because the file identifier is two bytes long and Le is 00 H which means to use the default value which is 256 bytes long. The API function APDUExchangeFull starts the communication session with the smart card and then the APDU command (SELECT FILE) is submitted to the smart card. The APDU response (SW1 and SW2) and Data (ResponseTempOut), if any, will be returned from the smart card to the application (terminal).

Public Const CONST_SELECT_FILE = "80A400000200"Dim TempCLA As StringDim TempINS As StringDim TempP1 As StringDim TempP2 As StringDim TempLc As StringDim TempLe As String

Public Sub Select_File( ResponseTempOut As String, FileIdentifier As String, SW1Out As String, SW2Out As String) Dim DummyDataOut As String

Guide to Smart Card Technology Page 3 6

TempCLA = LTrim(Mid(CONST_SELECT_FILE, 1, 2)) TempINS = LTrim(Mid(CONST_SELECT_FILE, 3, 2)) TempP1 = LTrim(Mid(CONST_SELECT_FILE, 5, 2)) TempP2 = LTrim(Mid(CONST_SELECT_FILE, 7, 2)) TempLc = LTrim(Mid(CONST_SELECT_FILE, 9, 2)) TempLe = LTrim(Mid(CONST_SELECT_FILE, 11, 2)) Call APDUExchangeFull(TempCLA, TempINS, TempP1, TempP2, TempLc, TempLe, SW1Out, SW2Out, FileIdentifier, ResponseTempOut, DummyDataOut)End Sub

Guide to Smart Card Technology Page 3 7

5.JAVA CARD PROGRAMMING

Java card programming brings a new era to smart card application development. The card supports a Java Virtual Machine (JVM). Java programs can be stored and executed on the card. Java card programming is based on Java Card 2.0 (the latest version is 2.0) specification (http://java.sun.com/products/javacard) which is maintained by Sun. Here are the main features of JVM on Java card:

• A restricted version of the Java Virtual Machine supports a subset of the Java language that can be used in Java Card applets.

• An API dedicated to smart card applet development based on the lowlevel ISO 7816 standards is available to support development of legacy applications.

• An abstract runtime environment is included which supports applet management functions like the applet selection mechanism. This environment is called the JCRE (Java card Runtime Environment).

Due to technical constraints on the card processor and since some features like multithreading is clearly not a necessity for Java card only a subset of the Java language is supported. There are also new classes (like javacard.framework.APDU) which are related to the ISO 7816 standards or to cryptography in the Java Card 2.0 specification. The implementation of a JVM is made up of a bytecode verifier, a class loader and a bytecode interpreter. The verifier is used to verify that a class file is a valid Java class file. The class loader is used to load classes into the system. The bytecode interpreter is used to actually execute the application.

A bytecode verifier is a complex and large piece of software which cannot fit onto a smart card. Therefore, the implementation of a JVM for a smart card is split into two parts as shown in figure 51:

• The Offcard part manages the verification of classes and ensures that all necessary classes are available.

Guide to Smart Card Technology Page 3 8

• The Oncard part is primarily responsible for executing the bytecode.

The JVM is a persistent machine, so that the state of programs and objects are preserved even when the card is powered off. The related data are stored in EEPROM. Another consequence of the JVM is that classes are only loaded and initialized once in the JVM, where they remain active until disposed of.

Figure 51. Architecture of Bytecode Verifier on Java Card.

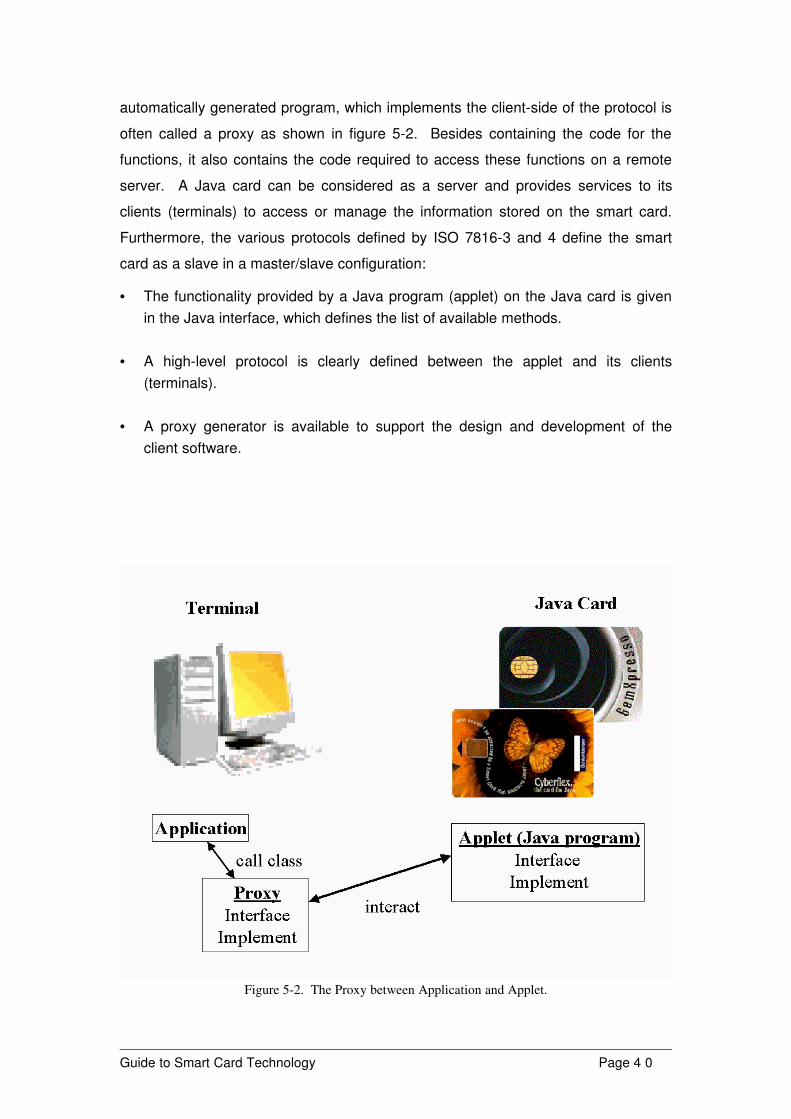

Beside the standard APDU command/response methodology, the other standard way to interact a program on the Java card is to use Remote Method Invocation (RMI). RMI, a distributed object technology, is an architecture that enforces the principle that a service provided on a server (Java card) must be described through an interface. The interface provides a list of methods publicly available for a given object. An interface like this is a kind of contract that binds a server to its clients (terminals). The server guarantees that it will respond to the methods defined in its interface. On the other hand, the protocol links the server to its clients. The protocol defines the way in which the server and clients communicate. Since the implementation of protocols is often quite complex, the implementation of these protocols is often automatically generated for a given object in JCRE. This

Guide to Smart Card Technology Page 3 9

automatically generated program, which implements the clientside of the protocol is often called a proxy as shown in figure 52. Besides containing the code for the functions, it also contains the code required to access these functions on a remote server. A Java card can be considered as a server and provides services to its clients (terminals) to access or manage the information stored on the smart card. Furthermore, the various protocols defined by ISO 78163 and 4 define the smart card as a slave in a master/slave configuration:

• The functionality provided by a Java program (applet) on the Java card is given in the Java interface, which defines the list of available methods.

• A highlevel protocol is clearly defined between the applet and its clients (terminals).

• A proxy generator is available to support the design and development of the client software.

Figure 52. The Proxy between Application and Applet.

Guide to Smart Card Technology Page 4 0

There are three main rules for controlling the security and visibility of applets in the Java Card:

• The visibility of a package is platformdependent.

• Within a visible package, only the public classes are visible from the outside.

• If an applet is able to get a reference to an object, then the applet is allowed to use the object.

Actually, these three rules are the same as the standard Java rules. Furthermore, most of the Java card manufacturers include an additional security feature – firewall – between applets. This feature is global to the card, and the purpose is to isolate every object in its own sandbox in order to reduce the risk of illegal access.

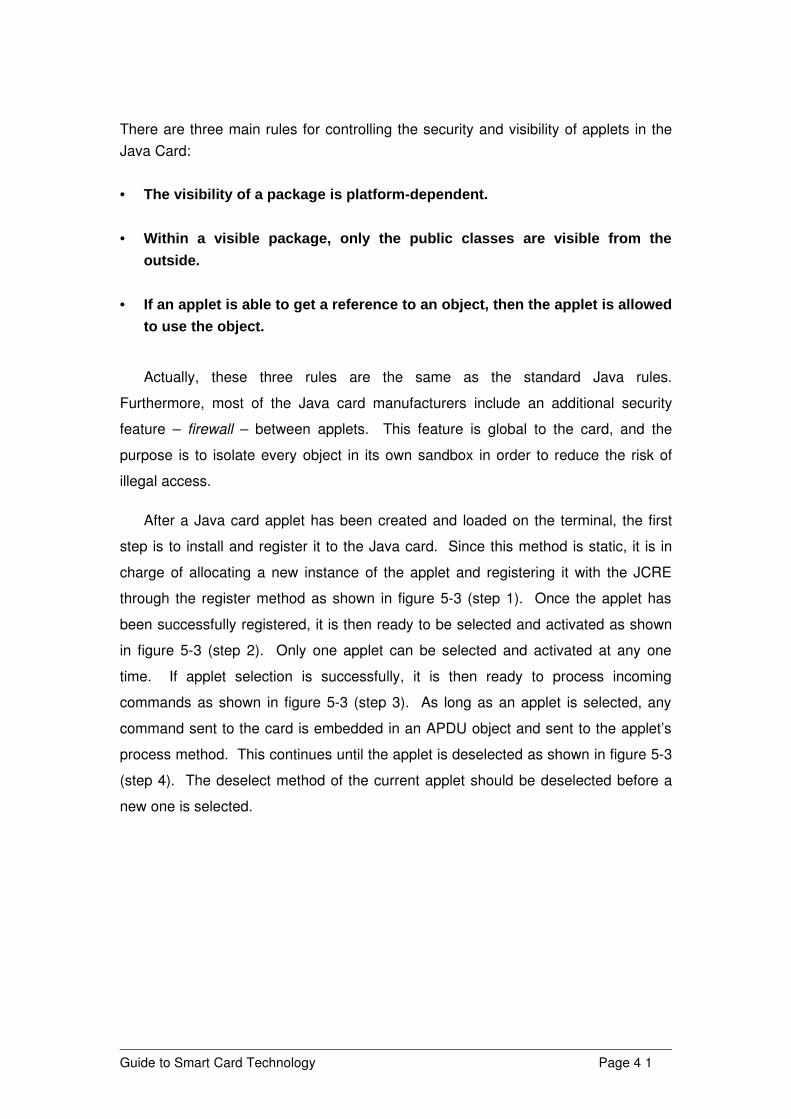

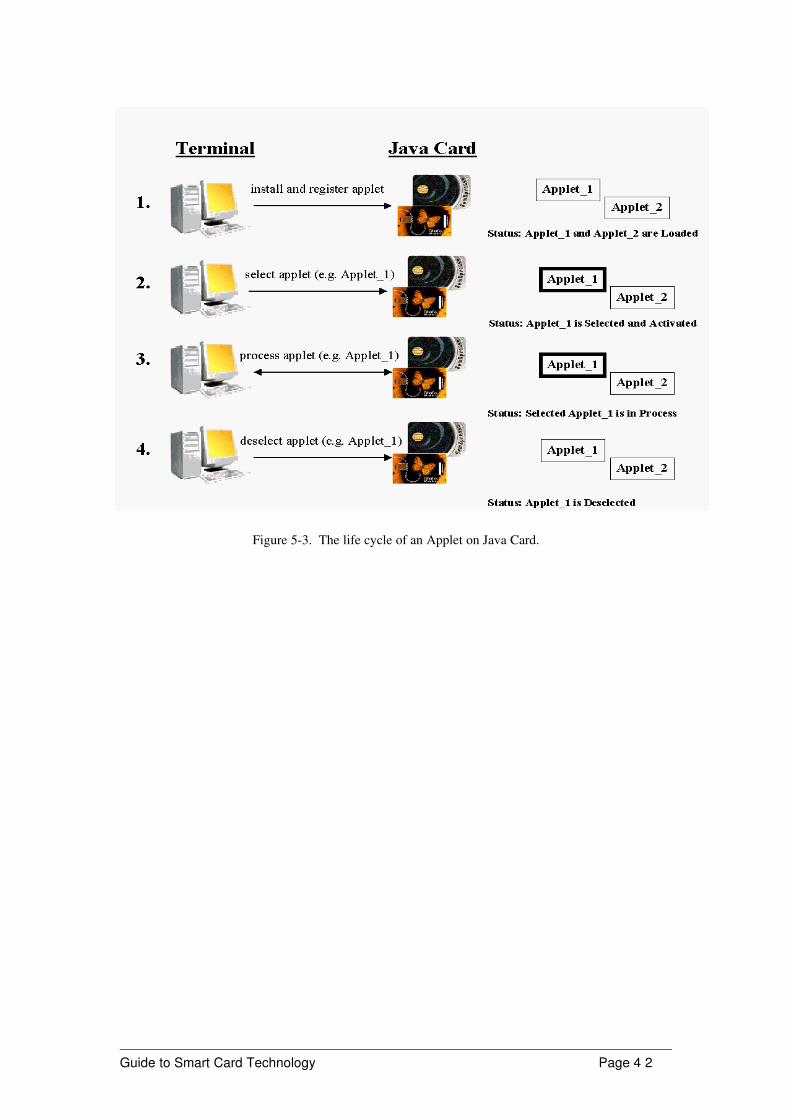

After a Java card applet has been created and loaded on the terminal, the first step is to install and register it to the Java card. Since this method is static, it is in charge of allocating a new instance of the applet and registering it with the JCRE through the register method as shown in figure 53 (step 1). Once the applet has been successfully registered, it is then ready to be selected and activated as shown in figure 53 (step 2). Only one applet can be selected and activated at any one time. If applet selection is successfully, it is then ready to process incoming commands as shown in figure 53 (step 3). As long as an applet is selected, any command sent to the card is embedded in an APDU object and sent to the applet’s process method. This continues until the applet is deselected as shown in figure 53 (step 4). The deselect method of the current applet should be deselected before a new one is selected.

Guide to Smart Card Technology Page 4 1

Figure 53. The life cycle of an Applet on Java Card.

Guide to Smart Card Technology Page 4 2

6.BUILDING YOUR OWN SMART CARD APPLICATION

In the previous chapter, we outlined the basic information for smart card programming. We shall now briefly describe the procedures for developing a smart card application.

Developing a smart card solution is similar to developing a distributed system. The following steps listed below can be used as the guidelines for building a smart card application:

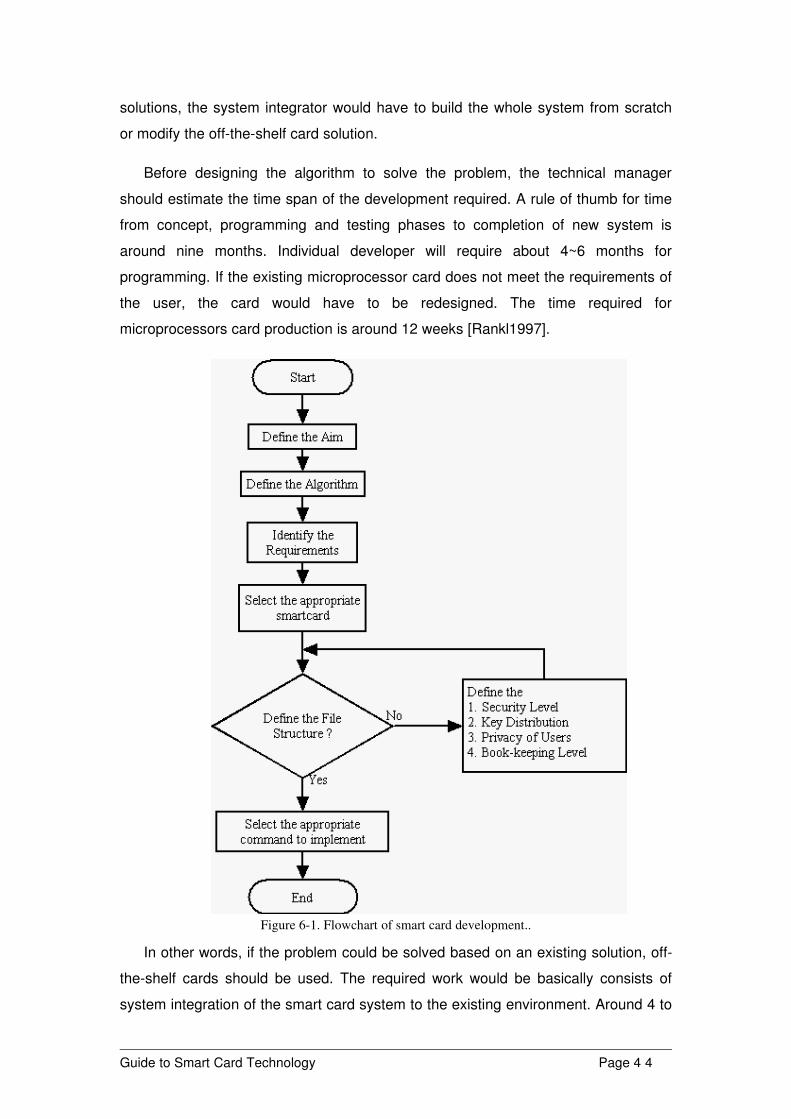

1. Determine the objective of the solution2. Define the appropriate algorithm3. Identify the requirements and select the appropriate smart card4. Specify the system security level, key distribution and key usage

algorithms5. Set the privacy and security levels of the users6. Set the security bookkeeping level7. Specify the directory and file structure of the smart card8. Select the application commands/instructions needed

In the following section, we shall describe each development step in detail. We hope that this information would be useful in helping the technical managers in developing smart card applications.

6.1 Plan the smart card solutionWhen designing a smart card solution, we have to understand the aim of this

solution first. Smart card as mentioned in the previous chapters is mainly used for identification, security, and electronic money related aspects.

If the solution is mainly based on standard existing smart card solutions (for instance door access control system, electronic purse, secure identification card and Digital Certificate card) an offtheshelf card could be chosen. However, if the problem has not been implemented before, or is different from the common

Guide to Smart Card Technology Page 4 3

solutions, the system integrator would have to build the whole system from scratch or modify the offtheshelf card solution.

Before designing the algorithm to solve the problem, the technical manager should estimate the time span of the development required. A rule of thumb for time from concept, programming and testing phases to completion of new system is around nine months. Individual developer will require about 4~6 months for programming. If the existing microprocessor card does not meet the requirements of the user, the card would have to be redesigned. The time required for microprocessors card production is around 12 weeks [Rankl1997].

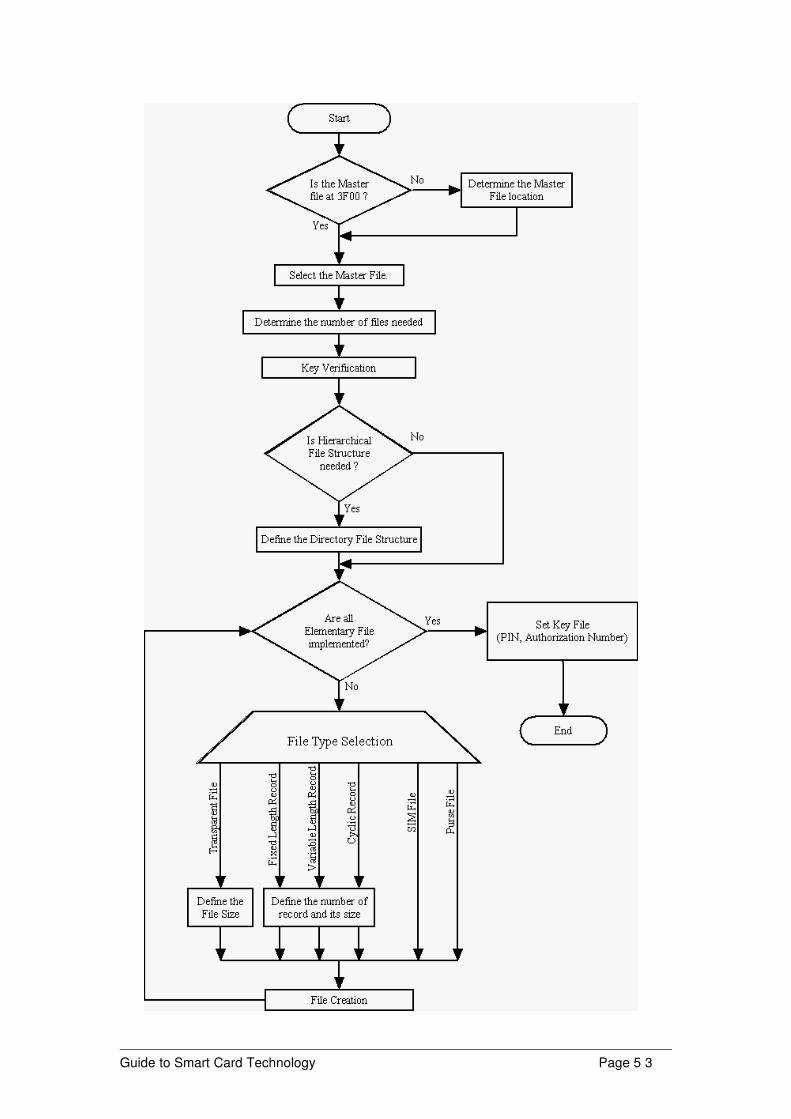

Figure 61. Flowchart of smart card development..

In other words, if the problem could be solved based on an existing solution, offtheshelf cards should be used. The required work would be basically consists of system integration of the smart card system to the existing environment. Around 4 to

Guide to Smart Card Technology Page 4 4

6 week’s time would be needed for this development. However, if no existing solution can meet the requirements of the user, development of the solution would have to start from the design of the chip card microprocessor. As a result, around 9 month’s time would be required.

The core part of the solution is to define the algorithm for the smart card solution. Developers need to choose an appropriate algorithm. They also have to understand the flow of the system and identify the appropriate role of the smart card.

In addition, developers have to understand the restriction of different smart cards. This information is used together with the requirements on the smart card for selecting the most appropriate card type. The first restriction of a smart card is the lifetime of the card.

The life expectancy of a smart card basically depends on the application of the card. For instance, GSM cards can stay in the phone permanently while identification cards and canteen cards would have to be renewed after 23 years [Rankl1997].

The number of insertion will also affect the life expectancy of the card. The goldplated contact could survive about 10,000,000 insertions. While the data storage (EEPROM) usually fails after 20,000 to 40,000 read/write cycles. A first sign of failing performance is when the first write attempt does not set the desired value in the EEPROM, or the written data no longer stay in memory after a few hours [Rankl1997].

Even though the smart card could hold the stored data securely, it should not be considered as a permanent safe for confidential data. EEPROM is based on electrical charges. Therefore due to current leakage, stored data could be lost. This effect is exacerbated by high temperatures. Normally the data content in a smart card is guaranteed for 10 years.

The second limitation is the memory space on the card. Because smart card is an embedded system, the memory size of the card could not be increased after the manufacturing stage. The current largest available memory space and the largest possible memory space in an 8bit CPU smart card are 32K bytes and 64K bytes respectively. However, development cost is affected by the cost of the card which is heavily dependent on the size of the memory. For example, changing from a 1Kbyte

Guide to Smart Card Technology Page 4 5

card to 8Kbyte card raises the production cost 4 times. Therefore a balance between costeffectiveness and card memorysize has to be struck.

6.2 Understand the need of smart cardAfter understanding the restrictions and limitations of smart cards, we would be

able to select the appropriate card for the problem according to the requirements. Though technical characteristics of smart card is hardwarespecific, most of the properties of smart card chips are identical. Therefore, design specifications can be the same.

Traditionally, there are two main criteria for selecting a smart card. These include the speed of instruction execution and the security level requirement of the system.

The speed of instruction execution depends on the processor chip and the speed of data transmission. The internal speed for executing instructions also affects the data transmission rate. The current clock rate of the CPU is in the range from 3.5MHz to 4.9MHz. The faster the internal instruction execution speed, the faster the data transmission rate. Although the maximum possible data transmission rate of contact smart card is 115200 bits per second (bps), the current normal transmission rate is 9600 bps [Guthery1998].

Other than the data transmission rate, the execution speed also depends on the Read/Write speed of the EEPROM and the card activation time. The Read/Write time of EEPROM is around 3.5ms while Ferro Electrical RAM (FERAM) is around 200ns [Klaus1998]. When the same type of nonvolatile memory is used, the time differences will be mainly on the card activation time. The execution time required in normal set of instructions is around 1 – 3 seconds, while the time required for card insertion and ejection is around 2 – 3 seconds. Therefore, for massive public transportation system, contactless card is preferred, because using contactless cards could reduce the total processing time by half compared with using contact cards. Generally speaking, different applications may require different execution speed.

Besides memory size and processing speed, security and addon features of the card are very important considerations. If the card is used as a personal security related card, special cryptographic engine may have to be added on the card. When financial processing is required, the card should have the electronic purse feature.

Guide to Smart Card Technology Page 4 6

6.3 Managing data storage on the cardHaving selected the smart card, developers have to design the data structures to